Saudi Arabia Data Center Storage Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

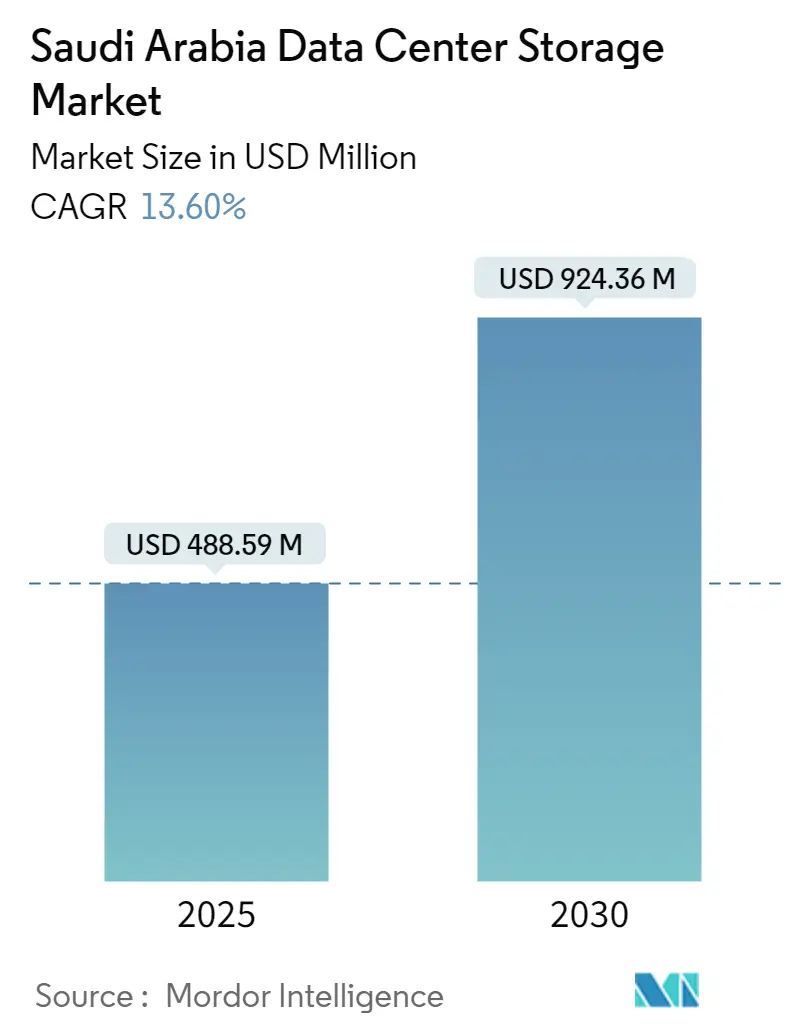

| Market Size (2025) | USD 488.59 Million |

| Market Size (2030) | USD 924.36 Million |

| Growth Rate (2025 - 2030) | 13.60% CAGR |

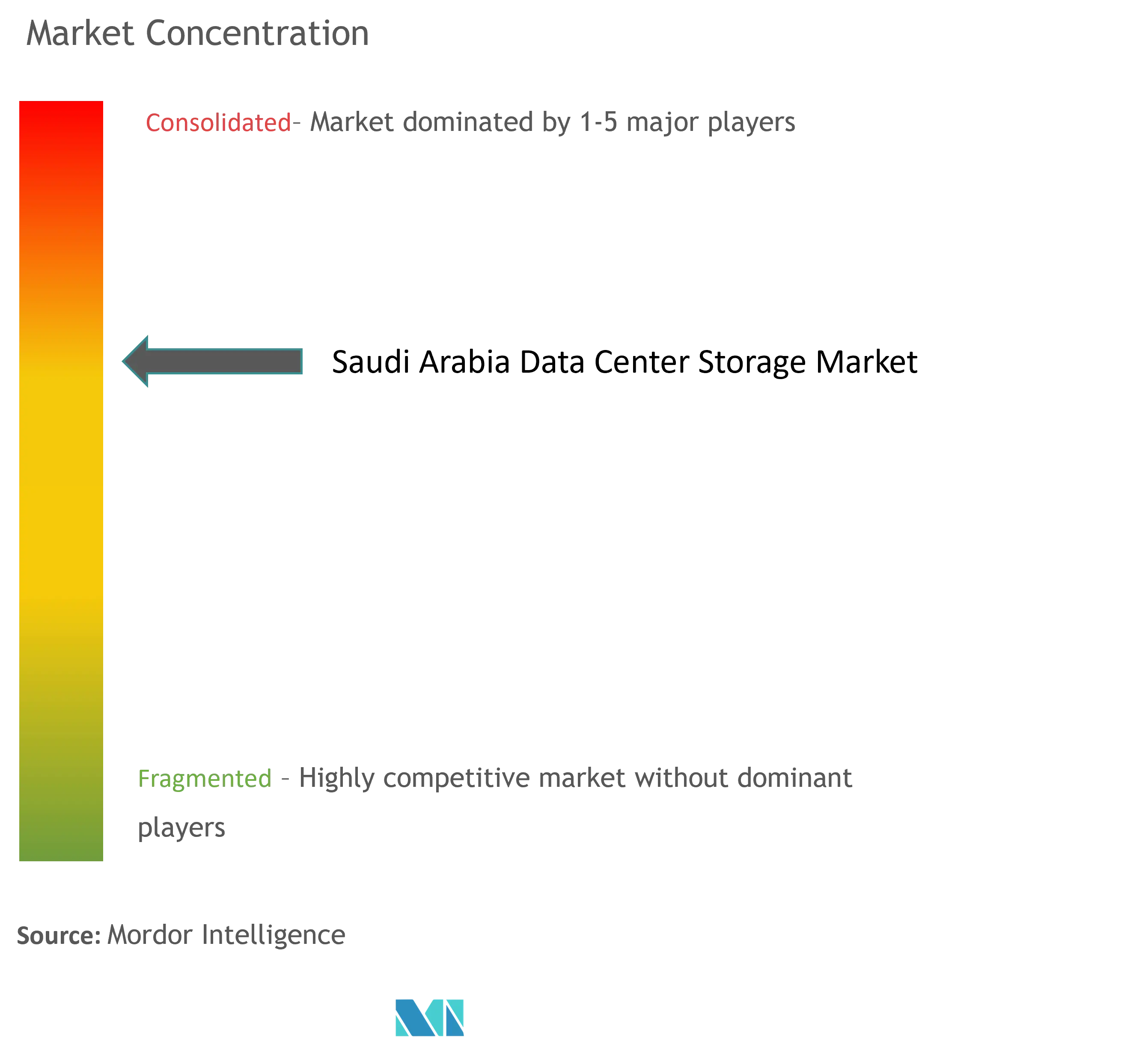

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Data Center Storage Market Analysis by Mordor Intelligence

The Saudi Arabia data center storage market size is expected to be valued at USD 488.59 million in 2025 and is forecast to climb to USD 924.36 million by 2030, yielding a 13.6% CAGR. Rising public-sector cloud mandates, rapid enterprise workload migration, and sizable hyperscale capital expenditure keep investment momentum strong, positioning the Kingdom as the Middle East’s preferred digital infrastructure hub. Government incentives have narrowed power costs, enabling operators to deploy high-density storage while meeting sustainability targets. Steady demand from IT, telecom, and BFSI workloads fuels upgrades to flash arrays and NVMe fabrics, while new AI clusters heighten the need for sub-millisecond latency. Competitive intensity remains moderate; international vendors bring deep portfolios and R&D heft, yet regional suppliers win deals through localized compliance support. Despite legacy integration hurdles and flash capex barriers, renewable energy contracts, SDAIA encryption rules, and NEOM’s data-centric design open material growth lanes across the Saudi Arabia data center storage market.

Key Report Takeaways

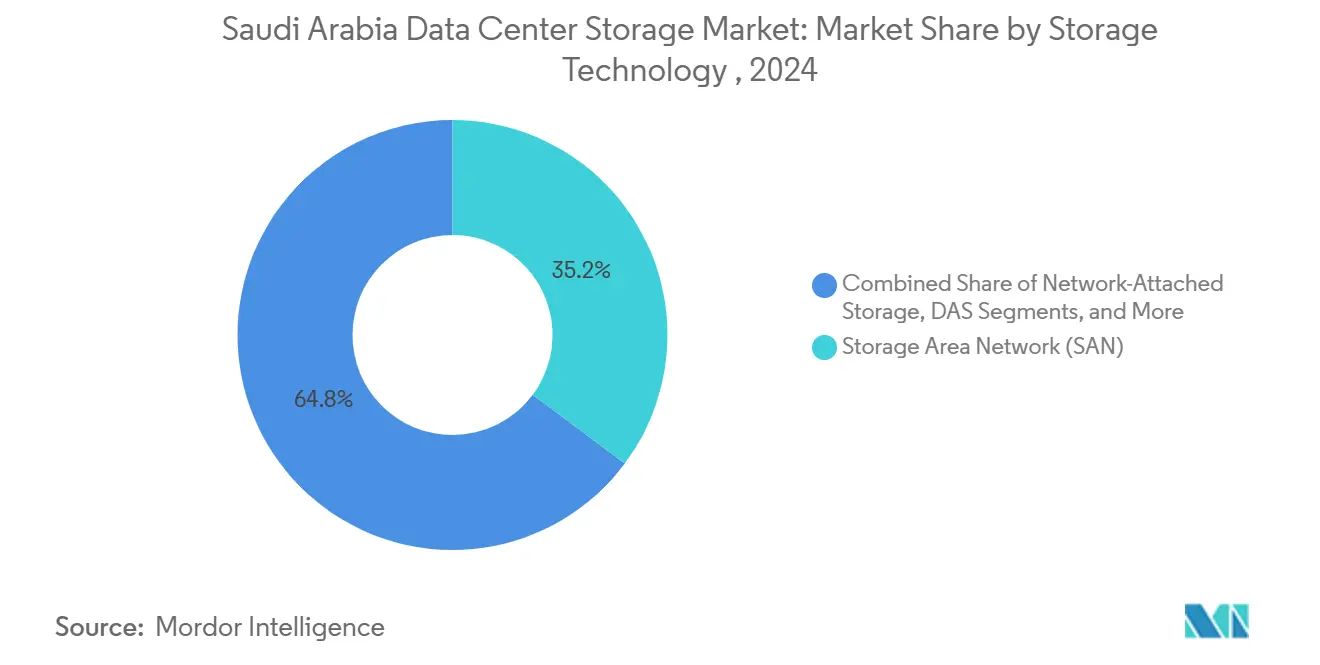

- By storage technology, SAN led with 35.2% revenue share in 2024; NAS is expanding at a 14.2% CAGR through 2030.

- By storage type, HDD arrays held 43.2% of the Saudi Arabia data center storage market size in 2024, while all-flash arrays are set to grow at 14.5% CAGR to 2030.

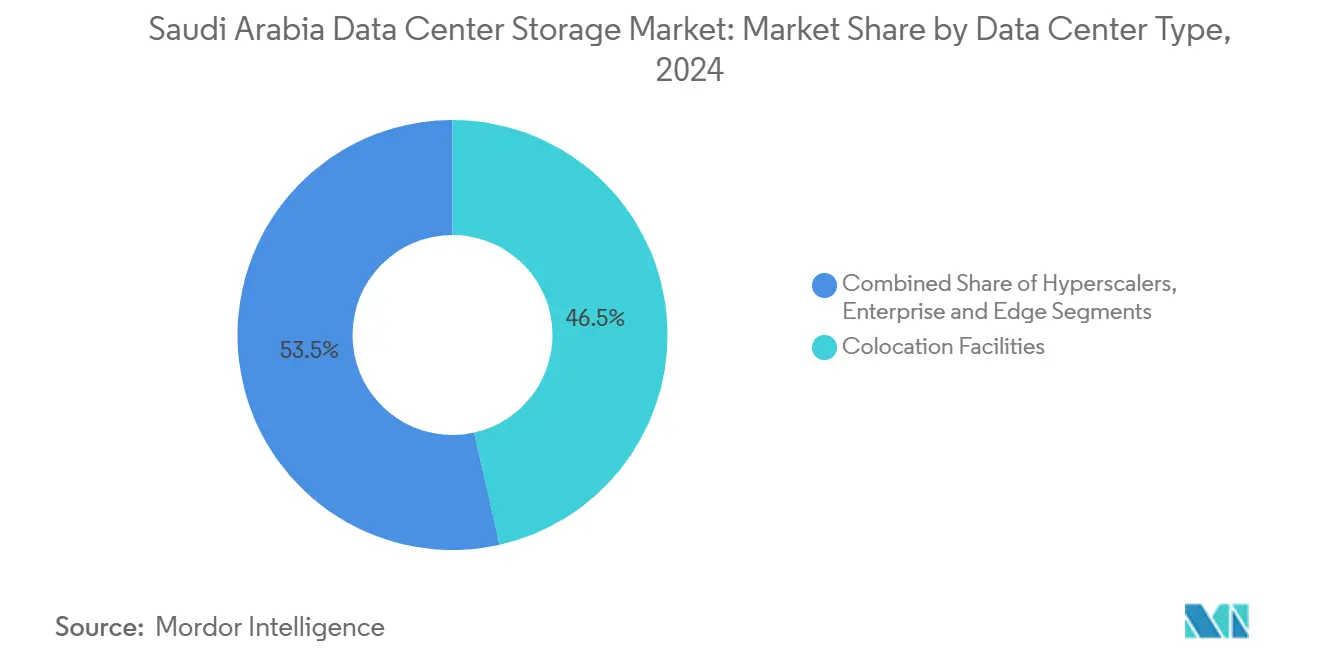

- By data-center type, colocation captured 46.5% of Saudi Arabia data center storage market share in 2024; hyperscalers show the fastest trajectory at 15.1% CAGR.

- By end user, IT & telecom accounted for 21.3% share in 2024; BFSI is forecast to advance at 15.9% CAGR.

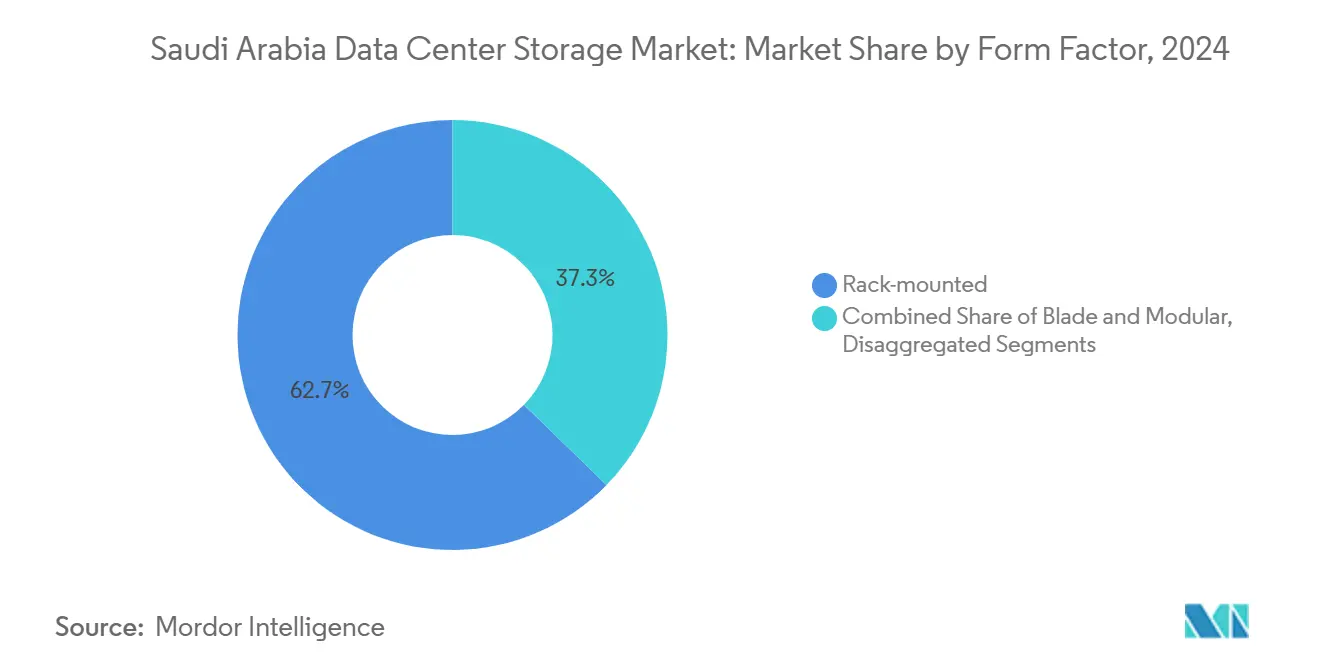

- By form factor, rack-mounted systems commanded 62.7% share in 2024; disaggregated architectures post a 14.2% CAGR.

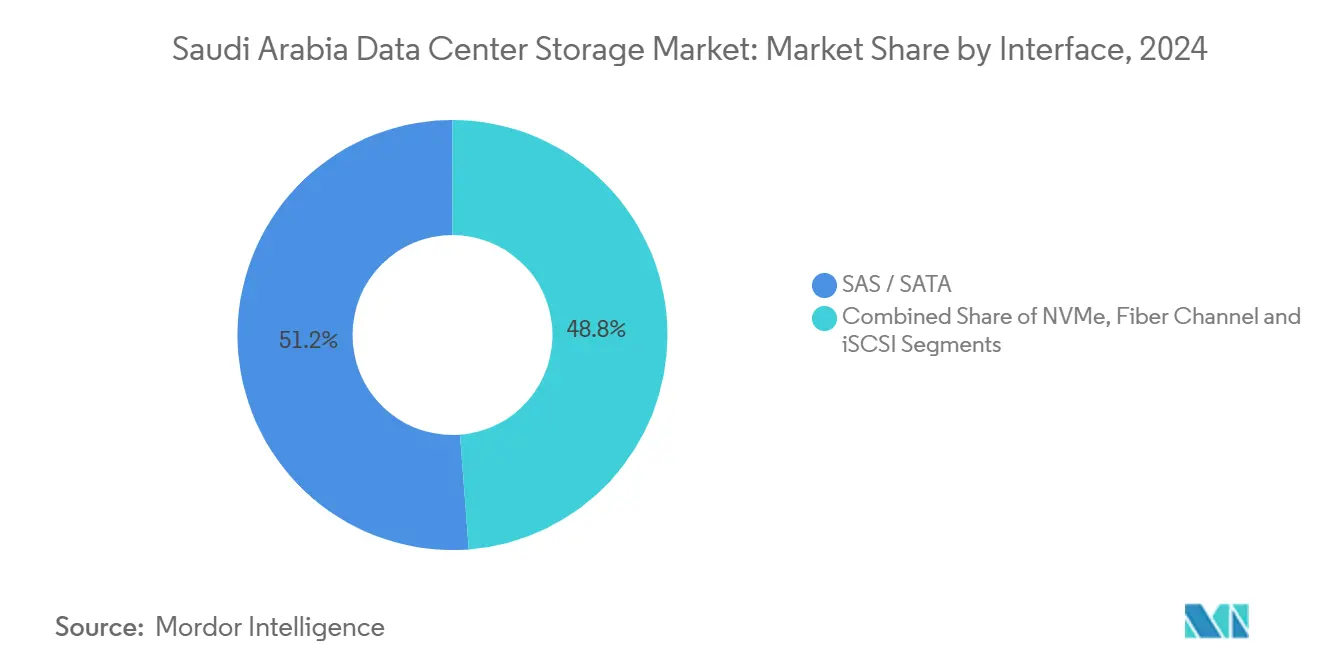

- By interface, SAS/SATA retained 51.2% share in 2024; NVMe solutions accelerate at 15.7% CAGR.

Saudi Arabia Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 cloud-first mandate and hyperscale capex | +3.2% | National, concentrated in Riyadh, Jeddah, NEOM | Medium term (2-4 years) |

| Surge in hybrid and all-flash array adoption | + 2.8% | National, with early adoption in financial districts | Short term (≤ 2 years) |

| Expansion of colocation hubs (Riyadh, Jeddah, NEOM) | + 2.1% | Regional, focused on major urban centers | Long term (≥ 4 years) |

| Abundant low-cost renewable PPAs enabling high-density storage | +1.9% | National, with concentration in solar-rich regions | Medium term (2-4 years) |

| SDAIA data-classification policy boosting on-prem encryption demand | +1.7% | National, government and regulated sectors | Short term (≤ 2 years) |

| AI/ML GPU clusters requiring ultrafast NVMe architectures | +1.5% | National, concentrated in research and tech hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Cloud-First Mandate and Hyperscale Capex

Mandatory migration timelines have driven ministries and state-owned enterprises to shift core workloads into cloud environments by 2025. The policy acts as a demand catalyst for hybrid architectures because many agencies must retain sensitive datasets on-premise while tapping elastic cloud compute for peak loads. Global hyperscalers are therefore fast-tracking regional zones and edge caches, channeling multibillion-dollar construction budgets into Riyadh and NEOM. Their arrival forces local service providers to modernize storage tiers, boosting purchases of scale-out SANs and NVMe arrays that can balance performance, encryption, and sovereign data residency rules.[1]Vision 2030 Secretariat, “Cloud First Policy Framework,” vision2030.gov.sa

Surge in Hybrid and All-Flash Array Adoption

Enterprise architects increasingly pair flash tiers with cost-optimized capacity drives to align performance to workload criticality. In financial trading desks, sub-millisecond responsiveness eliminates slippage risk, pushing banks toward 100% flash for core order-matching engines. Meanwhile, archival and compliance datasets remain on slower media. This tiering discipline reduces overall rack space, power draw, and cooling overhead, offsetting higher USD/GB purchase prices. Vendors reinforce the trend by bundling inline compression and deduplication licenses, which further shrink raw capacity requirements and sweeten return-on-investment projections.

SDAIA Data-Classification Policy Boosting On-Prem Encryption Demand

National guidelines compel public and critical-infrastructure entities to store Confidential and Restricted tiers within sovereign borders and apply AES-256 at rest. Compliance gaps now spark fast-tracked refresh cycles favoring arrays with built-in hardware encryption and government-validated key managers. Vendors offering tamper-proof audit trails and role-based access controls secure early wins, especially when they can demonstrate FIPS 140-3 certifications that align with cyber-resilience directives.[2]Saudi Data & AI Authority, “National Data Classification Guidelines,” sdaia.gov.sa

AI/ML GPU Clusters Requiring Ultrafast NVMe Architectures

As local universities and fintech labs deploy petascale GPU farms, legacy SAS/SATA backplanes throttle tensor-flow pipelines. NVMe-over-Fabrics boosts queue depth and slashes latency to microsecond levels, ensuring expensive GPUs sustain >90% utilization. Enterprises funding AI pilots discover that storage under-provisioning negates algorithmic gains, prompting accelerated investment in PCIe Gen5 flash modules and cache-heavy controllers Saudi Arabia's USD 100 billion AI initiative, Project Transcendence, positions the Kingdom among the top 15 AI countries by 2030, creating structural demand for storage systems optimized for machine learning workloads. [3]CIO, “Saudi Arabia launches US100 Billion AI initiative to lead in global tech,” cio.com

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy system compatibility and migration risk | -1.8% | National, concentrated in established enterprises | Medium term (2-4 years) |

| High capex of flash/NVMe over fibre infrastructures | -1.5% | National, affecting SME adoption rates | Short term (≤ 2 years) |

| Water-scarcity cooling limits on megawatt-class facilities | -1.2% | Regional, affecting desert locations | Long term (≥ 4 years) |

| Shortage of local storage-architecture talent | -0.9% | National, concentrated in technical centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy System Compatibility and Migration Risk

Fibre Channel fabrics entrenched in banks and utilities cannot natively interface with NVMe transports, compelling multiyear phased migrations. Data custodians fear extended downtime or integrity loss, prolonging pilot cycles and dampening procurement budgets. Vendors counter with gateway bridges and nondisruptive copy tools. Yet CIOs still earmark conservative schedules, which drags on refresh velocity and tempers otherwise vibrant demand across the broader Saudi Arabia data center storage market.multi-year

High Capex of Flash/NVMe-over-Fibre Infrastructures

All-flash builds carry list prices several times higher than disk-centric equivalents. SMEs reliant on cash flows struggle to clear board-level investment hurdles, even when long-term opex savings are calculated favorably. Leasing schemes, pay-per-use metering, and managed-service bundles are gaining traction, though adoption lag persists. Consequently, the bulk of SME workloads continue to sit on mid-range hybrid arrays until economic inflection points justify full NVMe conversion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN Dominance Faces NAS Disruption

SAN solutions collected 35.2% of the Saudi Arabia data center storage market share in 2024, underscoring entrenched demand for block-level, high-availability clusters. Within finance and telecom, synchronous replication and multi-pathing bolster uptime commitments, so CIOs prioritize fabric-level resilience. However, file-based workloads—video archives, DevOps repositories, container registries—expand quickly and propel NAS shipments at a 14.2% CAGR. Vendors now deliver unified controllers that expose both block and file protocols, blurring once-rigid product segments.

Software-defined offerings compound change by abstracting physical media and pooling capacity across heterogeneous nodes. Admin teams thus orchestrate dynamic service-level policies without touching cabling diagrams. As container adoption spreads, stateless microservices ask for lightweight persistent volumes, a niche where NAS excels. Global interconnection providers roll out edge appliances that cache hot file objects close to users, driving incremental gains for NAS license revenue inside the Saudi Arabia data center storage market.

By Storage Type: Flash Arrays Challenge HDD Incumbency

HDD arrays retained 43.2% share of Saudi Arabia data center storage market size in 2024 because capacity-centric backups and video workloads remain price sensitive. Yet all-flash systems will post 14.5% CAGR, converting disk estates as bit-cost gaps narrow. Performance uplift proves compelling: consistent sub-1 ms latency doubles virtual-machine density per host and slashes query runtimes on analytic clusters. Dual-port NVMe drives also cut failure domains versus legacy SATA sleds, enhancing SLA postures.

Hybrid arrays persist as stepping-stones. They combine small flash caches with dense disk shelves to balance cost and responsiveness until CFOs approve full flash. Meanwhile, quad-level cell NAND and controller-side compression drive cost curves toward parity. When 16 TB flash modules mature, rack consolidation savings plus lower power overhead tip TCO decisively, accelerating displacement of rotational media across the wider Saudi Arabia data center storage market.

By Data Center Type: Colocation Leads Hyperscaler Pursuit

Colocation providers absorbed 46.5% workload share in 2024, catering to enterprises seeking carrier neutrality and sovereign hosting. Floor-space take-up rose markedly in Riyadh’s financial district as banks exited ageing server rooms. Hyperscalers trail but clock the fastest 15.1% CAGR because cloud giants add local availability zones that guarantee <20 ms user latency. Tenants weigh lift-and-shift versus cloud-native rewrites, often ending with hybrid topologies straddling both models.

Edge mini-hubs also proliferate along content-delivery routes to cut buffering. Renewable-ready rooftops in NEOM host micro-data centers running lithium-ion UPS stacks, freeing adjacent racks for storage gear. The resulting spatial fluidity underpins a multi-tier topology where cold storage resides centrally, active datasets sit in colocation halls, and metadata hops into hyperscale object stores. Such hierarchies fuel incremental spending across the Saudi Arabia data center storage market.

By End User: Telecom Leadership Yields to BFSI Growth

IT and telecom operators commanded 21.3% share in 2024 thanks to subscriber data lakes, video streaming caches, and 5G core network repositories. Their early adoption of NVMe caches to accelerate packet routing kept them storage technology front-runners. Yet BFSI workloads crescendo faster at 15.9% CAGR. Open-banking APIs and real-time settlement protocols spur low-latency tier-one storage demands. Encryption at rest is mandatory, which pushes banks toward arrays with native secure key modules.

Media studios and OTT platforms widen object-store footprints for 8K mastering and regional distribution. Healthcare cloud picture-archiving systems double image retention widths for AI diagnosis. Each vertical diversifies I/O patterns, obliging solution vendors to tailor controllers, cache algorithms, and placement policies. Such sector-specific nuance expands addressable revenue pools throughout the Saudi Arabia data center storage market.

By Form Factor: Rack-Mount Stability Meets Composable Innovation

Standard rack-mount chassis held 62.7% share in 2024. Integrated cable management, broad spare-parts ecosystems, and predictable airflow keep them the default choice. Conversely, disaggregated-composable frames rise at 14.2% CAGR. They sever the historic one-server-per-drive bond, enabling pooled NVMe shelves to be mapped to compute nodes on demand. Enterprises stretch capex value by reallocating idle resources overnight to high-priority workloads.

Blade enclosures remain common in branch-office contexts that prioritize space efficiency. Modular converged stacks bundle compute, storage, and networking under a single SKU, easing lifecycle support for lean IT teams. Yet as AI training spikes memory and I/O demands, composable gear that scales each resource independently gains momentum, reinforcing upgrade waves inside the Saudi Arabia data center storage market.

By Interface: SAS/SATA Incumbency Faces NVMe Acceleration

SAS/SATA commanded 51.2% interface share in 2024 owing to vast installed estates and cost-friendly drive options. Firmware maturity and hot-swap convenience safeguard mission-critical uptime. Nevertheless, NVMe will outpace all rivals with 15.7% CAGR. Parallel queue de-serialization slashes latency from double-digit milliseconds to microseconds, indispensable for AI inferencing and high-frequency trading. NVMe-over-TCP also negates pricey Fibre Channel licenses, easing adoption in mid-market segments.

Fibre Channel retains favor where deterministic 16/32 Gb bandwidth and lossless transport trump cost. iSCSI remains the budget SAN toolkit for development labs. Over the forecast horizon, controller cards offering tri-mode flexibility let admins stage gradual NVMe introductions without forklift upgrades, smoothing adoption for cautious operators in the larger Saudi Arabia data center storage market.

Geography Analysis

Riyadh anchors the bulk of enterprise storage demand, driven by public-sector digitization mandates and a densely clustered financial ecosystem. Local colocation campuses interlink with metro fiber rings, yielding resilient dual-site architectures for ministries and banks. Data-sovereignty clauses necessitate primary and disaster-recovery instances inside national borders, effectively doubling addressable capacity. Jeddah’s coastal carrier hotels facilitate subsea cable landing stations that route traffic into Africa and Europe, motivating content distributors to deploy cache nodes that trim transit latency by 40% for westbound streams.

Further north, NEOM’s smart-city blueprint offers greenfield parcels pre-zoned for data center clusters. Operators leverage contiguous solar acreage and chilled-water loop easements to achieve power usage effectiveness below 1.2. Such operational headroom invites exabyte-scale storage farms, particularly for AI training corpora that can exceed 1 PB per model iteration. Eastern industrial corridors, rich in oil-and-gas telemetry, spawn edge micro-sites that capture refinery sensor data for near-real-time analytics

Competitive Landscape

Global heavyweights such as Dell Technologies, Hewlett Packard Enterprise, NetApp, IBM, and Pure Storage dominate top-tier enterprise tenders, leveraging IP rich in compression, replication, and AI-powered analytics. Their Saudi channel partners bundle migration services and compliance audits that de-risk upgrades for regulated clients. Regional challengers exploit proximity advantages, customizing Arabic language interfaces and local support SLAs. White-box ODMs, meanwhile, win price-sensitive hyperscale and edge bids with commodity NVMe sleds orchestrated by open-source software-defined stacks.

Product roadmaps coalesce around NVMe-over-Fabrics, quad-level cell NAND endurance boosts, and zero-trust security baselines. Vendors increasingly preload ransomware detection engines that inspect file entropy for early breach signals. Strategic alliances proliferate: flash makers pair with GPU card vendors to assemble reference architectures for AI workloads; telecom incumbents co-build edge nodes with storage suppliers to monetize 5G data surges. M&A also intensifies: platform vendors acquire observability startups to deliver single-pane-of-glass insights across compute, storage, and network resources.

Saudi Arabia Data Center Storage Industry Leaders

Dell Technologies Inc.

Hewlett Packard Enterprise

Hewlett Packard Enterprise

NetApp Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Equinix completed the acquisition of three data centers in the Philippines for USD 180 million, broadening its Asia-Pacific reach.

- March 2025: A Manassas data center site changed hands for USD 190 million, underscoring robust investor appetite for digital-infrastructure real estate.

- February 2025: Hyperscale cloud providers disclosed plans to spend USD 215 billion on data centers in 2025, with Amazon contributing over USD 75 billion.

- January 2025: Leading technology firms launched the USD 500 billion Stargate AI program to fund global AI data centers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Saudi Arabia data center storage market as revenue from new, factory-integrated storage subsystems (DAS, SAN, NAS, object, and tape) deployed inside colocation, hyperscale, enterprise, and edge facilities that host workloads within the Kingdom. According to Mordor Intelligence, values are expressed in constant 2024 US dollars.

Scope Exclusions: Backup software licenses, battery-based energy storage, and consumer device drives are not included.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Primary Research

We spoke with storage architects at Riyadh hyperscalers, procurement heads at three colocation operators, and distributor executives serving BFSI and telecom clients. Interviews validated import price bands, confirmed average gigabyte-per-kilowatt ratios, and highlighted purchase intentions for all-flash arrays through 2027.

Desk Research

We gathered baseline signals from CITC traffic bulletins, GASTAT fixed-asset tables, and ZATCA import records listing HS-code 8471 storage hardware, then cross-referenced these with SDAIA policy papers and SNIA surveys that map all-flash and NVMe uptake. Trade press releases and operator sustainability reports helped capture rack density, power-usage effectiveness, and campus commissioning schedules.

Our team also tapped D&B Hoovers for vendor financials and Dow Jones Factiva for contract tracking that revealed multiyear hyperscaler deals. These sources illustrate the breadth of material reviewed, and many additional references supported data checks and narrative clarity.

Market-Sizing & Forecasting

We open with a top-down reconstruction that converts installed IT load and floor space into petabyte demand pools using observed storage-to-compute ratios, then test the totals against sample ASP × volume roll-ups from supplier channel partners. Key variables include Vision 2030 cloud-migration targets, rack power envelopes, flash array share, and announced hyperscale capital-expenditure pipelines. A multivariate regression, supported by expert consensus, projects demand to 2030, while bottom-up checks adjust for currency shifts and mega-campus phases.

Data Validation & Update Cycle

Analysts run anomaly and variance checks against customs imports and vendor disclosures. If discrepancies exceed three percent, they re-contact sources before sign-off. We refresh every twelve months, with interim updates for major policy or project events, so clients receive the latest view.

Why Mordor's Saudi Arabia Data Center Storage Baseline Commands Reliability

Published values differ because studies apply varied asset boundaries, convert currencies at different dates, and update on unequal schedules.

Key gap drivers include other studies' reliance on Middle East averages, omission of edge and composable architectures, and exclusion of hyperscaler spending, each of which narrows totals or duplicates counts that distort the baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 488.6 Mn (2025) | Mordor Intelligence | |

| USD 430.1 Mn (2025) | Global Consultancy A | MEA averaging, hyperscaler spend omitted |

| USD 430.0 Mn (2024) | Industry Journal B | Enterprise-only scope, static FX base |

Overall, we've shown that Mordor's disciplined scope selection, variable tracking, and annual refresh deliver a transparent, reproducible baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the current size of the Saudi Arabia data center storage market?

The market stands at USD 488.59 million in 2025 and is forecast to reach USD 924.36 million by 2030.

Which storage technology leads in market share?

Storage Area Networks (SAN) hold the largest share at 35.2% in 2024, although Network Attached Storage (NAS) is growing faster

Why are all-flash arrays gaining momentum?

They deliver sub-millisecond latency, lower power usage, and higher virtual-machine density, factors that outweigh their higher purchase price over time.

How do SDAIA regulations impact storage strategy?

The data-classification policy requires on-premise, encrypted storage for sensitive data, spurring demand for arrays with built-in security.

Page last updated on: