Saudi Arabia Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

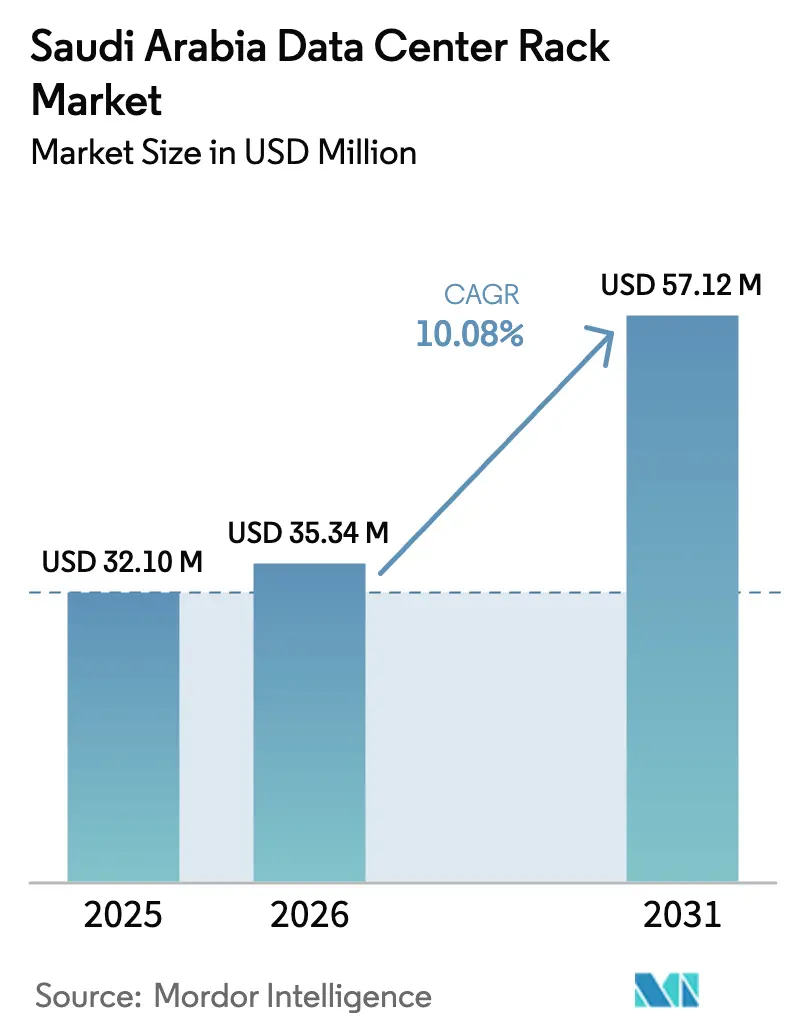

| Base Year Market Size (2025) | USD 32.1 Million |

| Market Size (2026) | USD 35.34 Million |

| Market Size (2031) | USD 57.12 Million |

| Growth Rate (2026 - 2031) | 10.08% CAGR |

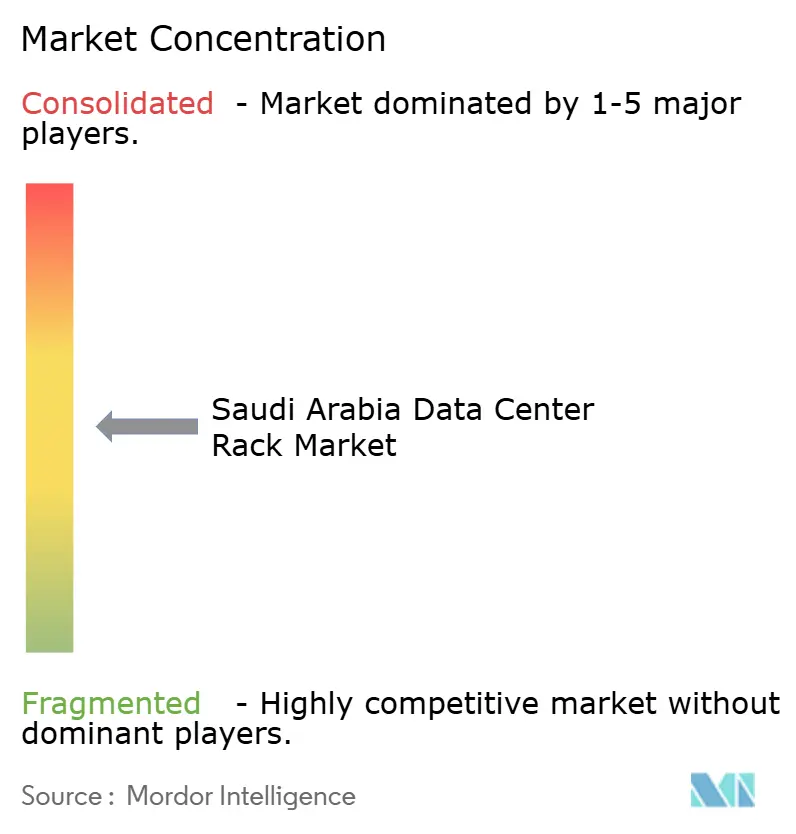

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Data Center Rack Market Analysis by Mordor Intelligence

The Saudi Arabia data center rack market size is expected to grow from USD 32.1 million in 2025 to USD 35.34 million in 2026 and is forecast to reach USD 57.12 million by 2031 at 10.08% CAGR over 2026-2031. Near-term momentum reflects a surge of hyperscale projects backed by Vision 2030, a USD 18 billion national data-center program, and aggressive 5G rollouts that push IT equipment closer to end users. Expanding cloud adoption by public agencies is accelerating demand for secure, high-load racks, while AI workloads are raising average rack power densities and driving liquid-cooling readiness. At the same time, operators seek lighter and corrosion-resistant materials to deal with coastal humidity and to simplify edge deployments in remote zones. Continuous localization of content, coupled with a widening skills base, reinforces the overall growth trajectory of the Saudi Arabia data center rack market.

Key Report Takeaways

- By rack size, full racks held 61.62% of the Saudi Arabia data center rack market share in 2025, while quarter racks are projected to grow at 14.03% CAGR to 2031.

- By rack height, 42U racks led with 51.90% revenue share in 2025; the 48U segment is expanding at 12.95% through 2031.

- By rack type, cabinet enclosures commanded 71.35% share of the Saudi Arabia data center rack market size in 2025; wall-mount racks post the fastest 14.62% CAGR to 2031.

- By data-center type, colocation sites held 55.78% of the Saudi Arabia data center rack market size in 2025, whereas hyperscalers record a 15.02% CAGR through 2031.

- By material, steel accounted for 71.22% of the Saudi Arabia data center rack market share in 2025, while aluminum solutions register an 11.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's data center rack market share coverage captures this comparative structure.

Saudi Arabia Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing penetration of FTTH and 5G backhaul | 3.5% | National, with concentration in Riyadh, Jeddah, and Dammam | Medium term (2-4 years) |

| Hyperscale DC build-outs by STC / AWS / Google | 2.7% | Major urban centers (Riyadh, Jeddah, Dammam) | Short term (≤ 2 years) |

| Vision 2030 digital-government push | 1.8% | National | Long term (≥ 4 years) |

| Colocation demand surge from OTT and BFSI (data-localization) | 1.3% | Riyadh and Jeddah | Medium term (2-4 years) |

| AI-dedicated GPU campuses needing high-density racks | 0.9% | Riyadh and NEOM | Medium term (2-4 years) |

| Solar + battery PPAs enabling low-OPEX remote DCs | 0.8% | Secondary cities and remote locations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing penetration of FTTH and 5G backhaul

Rapid fiber and 5G deployment has reached 77% of the population, forcing the creation of edge sites that place compute within one hop of mobile users.[1]U.S. Department of Commerce, “Saudi Arabia – Digital Economy,” trade.gov These micro-facilities need compact quarter and wall-mount racks that fit telecom closets and rooftop shelters. Operators now specify integrated battery backups and dust-proof door seals to cope with power fluctuations and desert particulates. Suppliers are therefore releasing shallow-depth enclosures with rear-cable swing frames and filtered side panels. Over the next three years, rack demand is projected to rise sharply in secondary towns where 5G small-cell clusters outnumber traditional central offices.

Hyperscale DC build-outs by STC, AWS, Google

Center3, Pure Data Centres, and DataVolt anchor more than 300 MW of new hyperscale capacity scheduled before 2027. Build contracts specify 48U racks supporting >3,000 lb static loads, hot-aisle containment, and liquid-cooling manifolds. Modular rail kits and tool-less airflow blanking panels shorten installation windows that hyperscalers cap at 14 weeks. Vendors answer with factory-integrated rack-and-power pods that ship fully wired. Standardization around identical footprints gives suppliers predictable volume, lowering per-unit cost and reinforcing the Saudi Arabia data center rack market.

Vision 2030 digital-government push

The Cloud-First Policy seeks 50% public-sector cloud adoption by 2025, doubling current consumption. [2]World Bank, “The Cloud Imperative: Strategy and Practices from the Kingdom of Saudi Arabia,” worldbank.org Ministries now demand biometric doors, tamper seals, and electromagnetic shielding on every rack. Central procurement guidelines require that new enclosures pass seismic and thermal-shock tests, raising the average bill of materials. Manufacturers have introduced government-grade lines with bonded-steel frames and audit-ready smart locks. Long-term demand looks resilient because refresh cycles align with multiyear e-services rollouts that underpin Vision 2030 milestones.

Colocation demand surge from OTT and BFSI

Data-localization rules obligate OTT video platforms and banks to host traffic within the Kingdom . Colocation operators reply with micro-segmented cages equipped with electronic rack locks, per-door sensors, and dual PDUs. AI-native tenants seek 30 kW cabinets featuring rear-door heat exchangers, incentivizing facility owners to upgrade entire rows. Rising tenancy levels improve utilization, allowing landlords to negotiate multi-year rack frame contracts that stabilize supply and reduce lead-time volatility.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CapEx and energy-intensive OPEX for Tier III/IV builds | -1.5% | National | Medium term (2-4 years) |

| Global supply-chain lead times for high-density racks | -1.2% | National, with greater impact in secondary cities | Short term (≤ 2 years) |

| Limited redundant grid capacity in key metros | -0.9% | Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Shortage of certified liquid-cooling integration talent | -0.7% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CapEx and energy-intensive OPEX for Tier III/IV builds

Data Centers Services Regulations introduced in 2024 elevate redundancy and testing thresholds, driving per-rack costs 30% above baseline. Cooling in peak summer conditions pushes PUE penalties that leave operators cautious on new halls. To soften the burden, facility designers adopt perforated doors delivering up to 70% open area and chimney-based containment that channels exhaust directly to ceiling plenums. Suppliers also promote in-row evaporative coolers that lower compressor runtime. Still, sticker shock postpones non-essential expansions and trims the CAGR contribution of smaller enterprises.

Global supply-chain lead times for high-density racks

Liquid-cooling-ready frames rely on valves, gaskets, and manifolds sourced from a narrow supplier base. Port congestion in Asia and extended factory backlogs stretch delivery to 18–22 weeks, slowing GPU cluster projects. Supermicro’s USD 20 billion partnership with DataVolt vividly illustrates demand that currently outpaces capacity.[3]Super Micro Computer Inc., “Supermicro Announces Strategic Partnership with DataVolt,” ir.supermicro.com Regional fabricators respond by tooling local plants for 48U skeletons and front-door heat exchangers, aiming to cut lead time by half. Some operators hedge risk through frame-agnostic layouts enabling phased integration of cooling skids once parts arrive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Quarter Racks Gain Momentum

Full racks dominate the Saudi Arabia data center rack market with 61.62% share in 2025. They remain the default choice for hyperscalers because standardized footprints simplify hot-aisle containment and bulk cabling. The segment benefits from AI clusters that regularly exceed 30 kW, levels that full-height frames handle without structural compromise. Demand also stems from colocation corridors in Riyadh, where common hall designs are pre-engineered around 600 mm x 1,200 mm footprints. Rollout of GPU cloud zones by STC continues to reinforce volume ordering of full racks, sustaining price competitiveness and high availability in distributor stock.

Quarter racks, however, exhibit the speediest rise at a 14.03% CAGR. Edge computing units in 5G base-station huts, shopping malls, and university campuses favor these compact enclosures. Micro data–center vendors package a pair of quarter racks with fire suppression and battery strings inside shipping-container shells, allowing turnkey deployment within six weeks. Logistics convenience—two technicians can hand-carry an empty quarter rack upstairs—further widens addressable markets. Converter kits that merge two quarter racks into a half rack add flexibility for capacity upgrades, enhancing life-cycle value and minimizing stranded capital.

By Rack Height: Vertical Optimization Drives Adoption

Traditional 42U frames hold 51.90% of revenue yet face share dilution as operators pursue denser floors. The 42U standard carries a reputation for easy reachability and abundant accessory options, a heritage that keeps it entrenched in colocation meet-me rooms and enterprise server halls. Techniques such as top-of-rack switching and side-cable troughs help maintain airflow clarity even at 15 kW. Meanwhile, server OEMs certify new AI chassis within 42U envelopes, ensuring backward compatibility.

The 48U cohort is projected to expand 12.95% through 2031, supported by hyperscalers that prioritize compute density over walk-in clearance. Taller cabinets often pair with motorized lifts to streamline maintenance. EAE Elektrik delivers KabinPLUS 48U frames rated at 1,500 kg, offering high static strength that accommodates eight-GPU blades per 1U slot. Operators that replace every sixth 42U row with 48U gain roughly 15% extra rack count without extending the white space envelope, an important advantage where land prices continue to climb around Riyadh Tech Valley.

By Rack Type: Wall-Mount Solutions Address Edge Requirements

Cabinet enclosures account for 71.35% of the Saudi Arabia data center rack market size. Their closed design supports ducted exhaust and front-door filtration, essential for minimizing particulate ingress in desert climates. Most models integrate side panels with quick-release locks, allowing rapid extraction for cable upgrades. Security features such as swing-handle keypads and centralized monitoring via Modbus complement compliance requirements under the Personal Data Protection Law.

Wall-mount racks grow quickest at 14.62% CAGR as rail-side deployments for 5G edge nodes multiply. Tripp Lite’s 12U hinged model illustrates this demand by offering 200-lb capacity and reversible doors in only 18 inches depth tripplite.eaton.com. Telecommunications operators value fold-out brackets that enable single-person maintenance on street-level cabinets. Hybrid “swing-mount” concepts further extend usability, letting customers deploy small UPS units behind access switches while preserving frontal airflow pathways.

By Data Center Type: Hyperscalers Drive Innovation

Colocation facilities held 55.78% share of the Saudi Arabia data center rack market size in 2025. They attract enterprises pursuing data-sovereignty compliance without heavy CapEx. These providers outfit cages with modular busbars that snap into rack roofs and support mixed power feeds, making them appealing to BFSI tenants with complex redundancy needs. Continuous power-density upgrades keep colocation halls competitive when courting AI research projects.

Hyperscale operators deliver the fastest 15.02% CAGR. DataVolt has signed multi-gigawatt PPA commitments to secure renewable electricity, enabling GPU campuses that each consume up to 120 MW. Within such facilities, every rack is ordered factory-fitted with front-to-back airflow baffles, dual busbars, and immersion-ready bays. Fixed-spec procurement unlocks manufacturing scale, compressing per-unit costs and elevating the Saudi Arabia data center rack market.

By Material: Aluminum Gains Traction in Specialized Applications

Steel frames remain entrenched at 71.22% market share because they carry heavy point loads economically. Vendors supply welded or bolted variants; both satisfy 3,000 lb static targets required for dense blade arrays. Yet weight constraints in rooftop micro-sites drive interest in aluminum frames that are 35% lighter yet still meet 1,100 lb benchmarks. Aluminum naturally resists saline corrosion, a benefit for Jeddah’s coastal data centers where sea air accelerates galvanic wear.

Composite and hybrid materials surface in special-purpose enclosures for EMI-sensitive workloads. Legrand’s latest lineup applies powder-coated steel uprights with die-cast aluminum doors to optimize stiffness and thermal exchange legrand.us. Engineers can attach copper mesh grounding straps directly onto internal aluminum members, ensuring a continuous earth path across mixed materials. Adoption remains niche but grows as military and aerospace tenants request high-shielding cabinets to house satellite-uplink control systems.

Geography Analysis

Riyadh commands the largest cluster of commercial and governmental data centers, with six active sites from five providers baxtel.com. Capital city facilities favor high-density racks engineered for AI inference nodes and rely on chilled-water rear-door heat exchangers to manage 40 kW loads. The Saudi Arabia data center rack market size in Riyadh is expected to nearly double by 2030 as DataVolt and Alfanar inject more than USD 1.4 billion into new halls.

Jeddah follows as the second-largest hub, benefitting from submarine-cable landings that attract international content platforms. Zoom’s freshly launched facility in the city underscores rising demand for corrosion-resistant aluminum cabinets that withstand humid coastal air. Operators here install desiccant dehumidifiers directly within row-level containment to keep internal RH below 50%. Dammam and the Eastern Province are emerging zones where oil-and-gas digital twins generate compute loads requiring ruggedized racks sealed against airborne hydrocarbons. Nokia and stc Group’s 1 Tbps optical link trial in the region paves the way for hybrid cloud analytics that demand low-latency edge sites. Further north, NEOM’s ZeroPoint DC pioneers renewable-powered infrastructure in a desert setting, relying on double-walled cabinets with reflective paint and roof solar shade to reduce inlet-air temperatures. Rack suppliers must therefore tailor corrosion protection, thermal coatings, and seismic anchoring based on each region’s micro-climate and regulatory stipulations.

Analysis of the data center rack market by Mordor Intelligence spans multiple other regional evaluations across Middle East, South America, and Europe, supported by country-level insights for Spain, Switzerland, Chile, Denmark, United Kingdom, and Sweden, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The Saudi Arabia data center rack market features a blend of international giants—Schneider Electric, Vertiv, Rittal—and agile regional specialists such as Norden Communication. Global brands supply pre-engineered SKUs validated under international standards, securing large block orders from hyperscalers who prefer multi-country harmonization. Local vendors use geographic proximity to offer swift onsite modification, a trait prized by edge-site owners that need custom wall-mount brackets within days.

Strategic alliances broaden solution scope. Schneider Electric pairs its Easy Rack line with chilled-water distribution panels from local HVAC partners to deliver turnkey rows for high-density AI labs. Norden Communication promotes dual-rack systems whose vertical cable troughs align with third-party busbar trunks, simplifying power reticulation across multitenant cages.

Technology differentiation deepens as racks become sensor platforms. Top vendors embed environmental probes, firmware-based access logs, and API hooks for predictive maintenance analytics. Combined with server telemetry, these racks let operators fine-tune airflow and adapt fan curves, yielding energy savings of 6–8% in test deployments. Competitive intensity is expected to rise once local fabrication capacity scales up, narrowing cost gaps between imported and domestic frames and increasing buyer leverage in large procurement cycles.

Saudi Arabia Data Center Rack Industry Leaders

Schneider Electric SE

Vertiv Group Corp.

Rittal GmbH and Co. KG

Dell Technologies Inc.

Eaton Corporation plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Super Micro Computer and DataVolt announced a USD 20 billion partnership to deploy ultra-dense GPU racks in green AI campuses

- May 2025: Humain partnered with Nvidia to build 500 MW AI data centers requiring 18,000 Grace Blackwell units, driving demand for high-density liquid-ready racks

- March 2025: Alfanar invested USD 1.4 billion to develop four data centers in Riyadh and Dammam, boosting regional rack orders

- February 2025: Cisco expanded Saudi operations, adding cloud infrastructure that increases demand for networking-optimized racks

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Saudi Arabia data center rack market as factory-built steel or aluminum frames (quarter, half, and full cabinets) installed in colocation, hyperscale, and enterprise white space to hold servers, storage, and networking gear under the EIA-310 standard. Integrated power strips are counted because they lift the average selling price.

Scope exclusion: outdoor telecom cabinets and petrochemical-grade enclosures are not considered.

Segmentation Overview

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Heights (?52U and Custom)

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with hyperscale project leads, colocation operations heads, rack distributors, and IT managers in Riyadh, Jeddah, and Dammam. Their guidance on density road maps, local-content premiums, and lead times sharpened every assumption.

Desk Research

We assembled the baseline using CST data-center license logs, Saudi Customs HS-847330 import files, General Authority for Statistics trade tables, ITU indicators, and Vision 2030 project trackers. Company 10-Ks, investor decks, and news archived on Dow Jones Factiva, plus vendor financials in D&B Hoovers, revealed shipment volumes and blended ASPs. These references are illustrative, and many additional open records informed our desk work.

Market-Sizing & Forecasting

We begin with a top-down capacity model: forecast IT load (MW) multiplied by racks per MW, adjusted for rising power density. Bottom-up checks that draw on distributor shipments and sampled ASP multiplied by volume roll-ups anchor totals. Multivariate regression then projects demand using five vital signals: hyperscale capex pipeline, utilized MW, median 42U cabinet ASP, local steel index, and average kW per rack. Linear interpolation fills minor data gaps before final triangulation.

Data Validation & Update Cycle

Outputs face variance scans against CST permits and customs totals, peer review, and sign-off. The model refreshes annually, with interim updates triggered by material policy or project news.

Why Mordor's Saudi Arabia Data Center Rack Baseline Commands Confidence

Published estimates diverge because scopes, refresh cadences, and density rules vary. Some sources drop liquid-cooling cabinets, others bundle PDUs, several still anchor to 2023, and a few scale global ratios without testing them against Vision 2030 contracts.

Our 2024 base year captures nine hyperscale builds and the latest import data, giving decision-makers a Saudi-specific view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 32.10 mn (2025) | Mordor Intelligence | |

| USD 33.08 mn (2024) | Regional Consultancy A | Catalog ASP basis and omission of edge micro-sites |

| USD 30.10 mn (2023) | Trade Journal B | Older base year and exclusion of GPU halls |

| USD 250.00 mn (2025) | Global Consultancy A | Bundles racks with PDUs and uses global spend share |

The comparison shows that Mordor's regularly updated model, grounded in license data, verified shipments, and operator interviews, delivers a balanced and transparent baseline executives can rely on.

Key Questions Answered in the Report

What is driving double-digit growth in the Saudi Arabia data center rack market?

Vision 2030 investments, hyperscale cloud build-outs, nationwide 5G coverage, and stringent data-localization laws collectively lift rack demand across hyperscale, colocation, and edge segments.

Which rack sizes are gaining popularity for edge deployments?

Quarter racks and wall-mount enclosures are preferred for edge sites because their compact footprint fits telecom closets and remote shelters while still supporting integrated power backup.

Why are aluminum racks becoming more common in Saudi data centers?

Aluminum frames weigh less, resist coastal corrosion, and dissipate heat effectively, attributes valued in humid coastal cities such as Jeddah and in rooftop edge locations.

How are hyperscalers influencing rack specifications?

Operators such as DataVolt and center3 standardize on 48U racks with >3,000 lb load capacity, liquid-cooling compatibility, and integrated cable ducts, pushing vendors to scale identical SKUs.

Page last updated on: