Small Unmanned Aerial Systems (sUAS) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

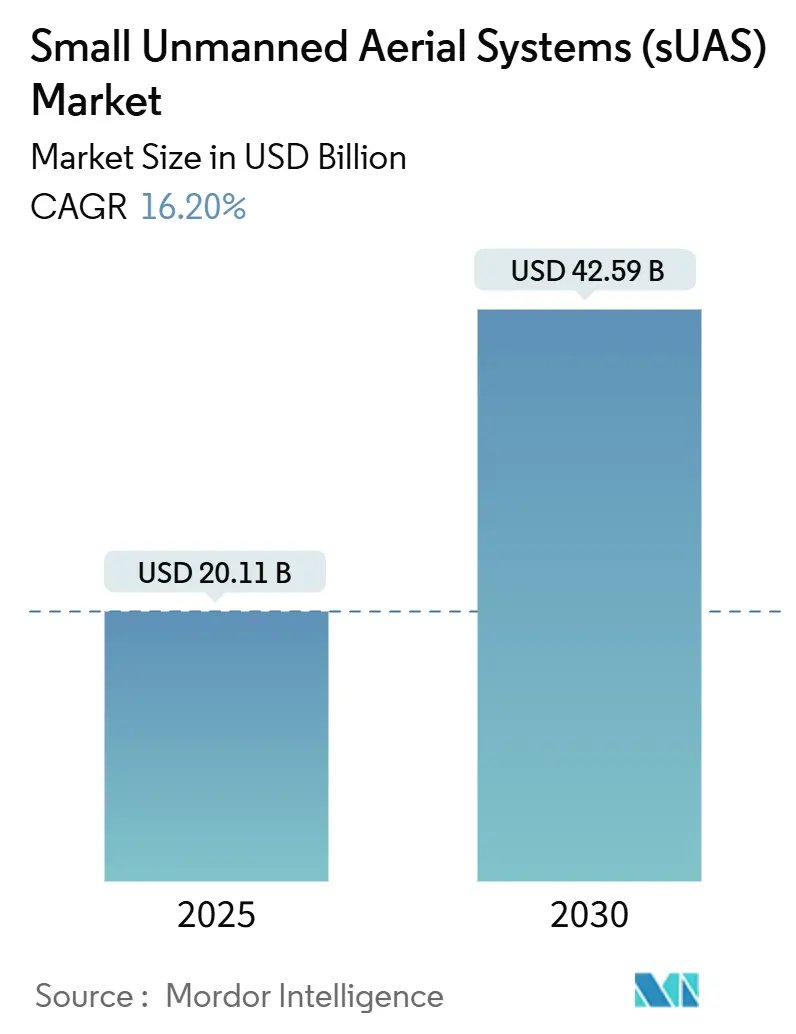

| Market Size (2025) | USD 20.11 Billion |

| Market Size (2030) | USD 42.59 Billion |

| Growth Rate (2025 - 2030) | 16.20% CAGR |

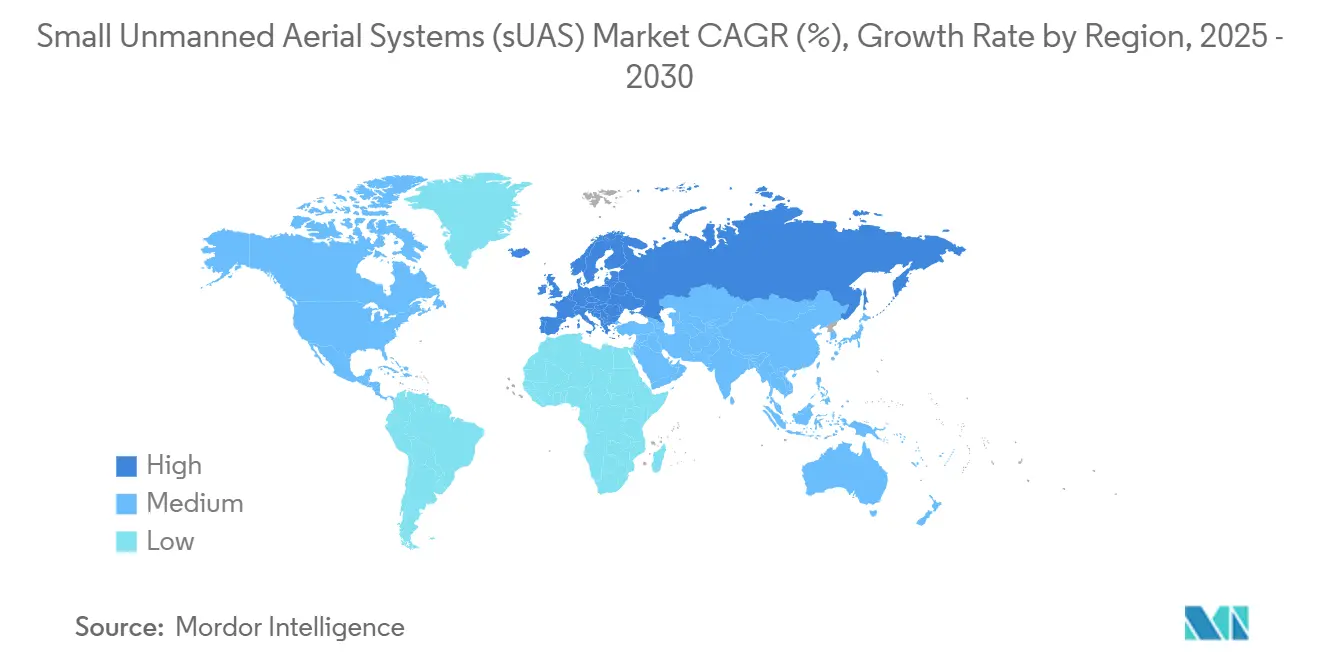

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Unmanned Aerial Systems (sUAS) Market Analysis by Mordor Intelligence

The small unmanned aerial systems (sUAS) market size stands at USD 20.11 billion in 2025 and is projected to reach USD 42.59 billion by 2030, advancing at a 16.2% CAGR. This surge reflects the technology’s steady migration from experimental use cases into indispensable infrastructure for defense, public safety, agriculture, and logistics. Regulatory liberalization of beyond-visual-line-of-sight (BVLOS) operations, rapid sensor miniaturization, and rising demand for low-cost aerial data collection collectively underpin the upward trajectory of the sUAS market. China’s September 2024 export controls on high-performance components triggered an urgent pivot toward domestic sourcing within Western supply chains, accelerating investment in US and European manufacturing hubs. Simultaneously, tariffs that inflate battery and motor costs by 15-20% have spurred exploration of hydrogen fuel cells and hybrid powertrains, further broadening the addressable opportunity for the sUAS market.

Key Report Takeaways

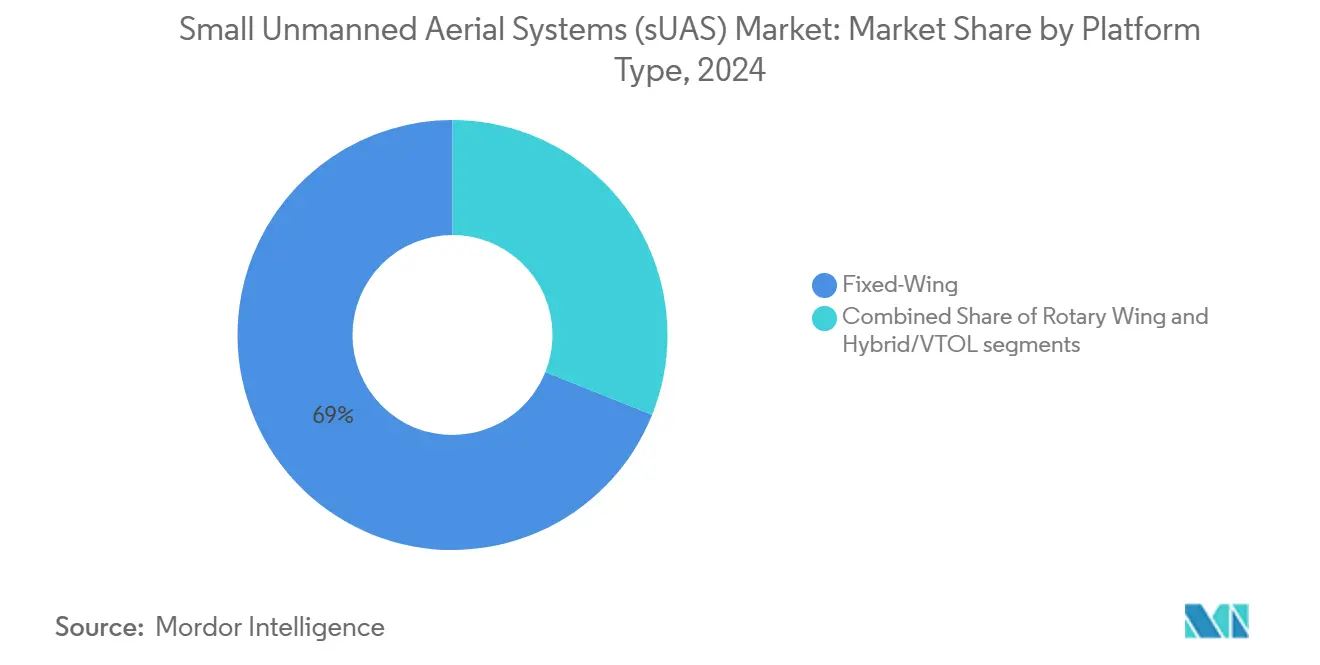

- By platform type, fixed-wing aircraft held 68.95% of the sUAS market share in 2024, while hybrid/VTOL platforms are set to expand at a 19.42% CAGR through 2030.

- By size, the micro class (250g to 2 kg) accounted for 43.58% of the sUAS market size in 2024; nano-drones under 250 g are forecasted to grow 16.3% annually to 2030.

- By application, defense and security led with 36.43% revenue share in 2024, whereas logistics and delivery showed the strongest outlook at 17.83% CAGR.

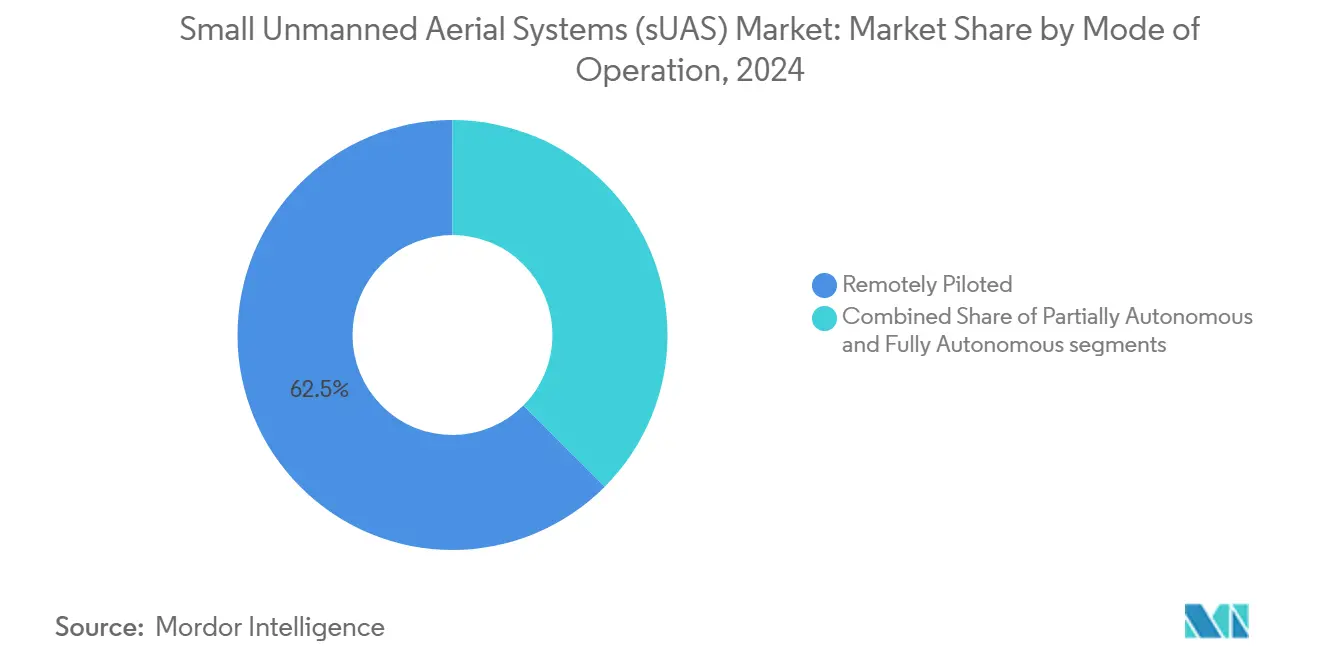

- By mode of operation, remotely piloted systems captured a 62.53% share in 2024; fully autonomous craft will post an 18.91% CAGR across the forecast window.

- By propulsion, electric-battery models represented a 39.41% share in 2024, yet hydrogen fuel cells will advance 18.35% annually to 2030.

- By geography, North America dominated with a 38.38% share in 2024, but Europe is on track for the fastest regional pace at 15.36% CAGR.

Global Small Unmanned Aerial Systems (sUAS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth in drone-as-a-service (DaaS) subscriptions | +2.10% | North America, Europe | Medium term (2-4 years) |

| Rapid miniaturization of high-performance sensors and onboard AI | +1.80% | Global tech hubs | Short term (≤ 2 years) |

| National BVLOS corridors unlocking long-range missions | +1.20% | North America, Europe, Australia | Medium term (2-4 years) |

| Agro-chemistry bans accelerating shift to drone crop-spraying | +0.80% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Edge-compute chips enabling autonomous swarming operations | +0.60% | Developed defense markets | Long term (≥ 4 years) |

| Defense procurement of loitering munitions and tactical sUAS | +0.40% | NATO and allies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth in Drone-as-a-Service Subscriptions

Subscription-based aerial data collection has transformed the small sUAS market by converting costly capital purchases into manageable operating fees. Service providers bundle aircraft, software, pilot training, and regulatory compliance into monthly contracts that appeal to agriculture co-operatives, utilities, and municipal agencies. Predictable recurring revenue allows vendors to fund ongoing R&D, accelerating feature rollouts and shortening replacement cycles. The model’s scalability further lowers entry barriers for small businesses lacking funds for high-end payloads. Mature communications infrastructure in North America and Europe positions these regions to capture an outsized share of early adoption.

Rapid Miniaturization of High-Performance Sensors and Onboard AI

Component engineers now produce sub-50 g thermal, LiDAR, and multispectral modules that deliver enterprise-grade imagery on recreational-weight airframes. Parallel progress in edge AI chips enables real-time object detection, navigation, and data compression onboard craft weighing less than 250 g. This convergence blurs the line between hobbyist and professional equipment, expanding the sUAS market into inspection niches previously reserved for larger vehicles. Lower mass also reduces energy demand, indirectly extending endurance or enabling smaller battery packs that free payload capacity for additional sensors.

National BVLOS Corridors Unlocking Long-Range Missions

The US Federal Aviation Administration has issued over 230 BVLOS exemptions, and the United Kingdom targets routine BVLOS operations by 2027.[1]Federal Aviation Administration, “BVLOS Waiver Grant List,” faa.gov Dedicated corridors trim insurance premiums and regulatory paperwork, letting operators scale linear-infrastructure surveys and suburban parcel delivery. Harmonized European regulations under EASA enhance fleet utilization for multinational operators, giving the sUAS market a clear runway for cross-border services. As national authorities publish performance-based standards, hardware makers can design to a consistent specification instead of bespoke waiver criteria.

Agro-Chemistry Bans Accelerating Shift to Drone Crop-Spraying

Tighter pesticide guidelines in the European Union and select Asia-Pacific countries have made precision application mandatory for many large farms. Small multirotors fitted with variable-rate nozzles deliver herbicides only where optical sensors confirm weed presence, reducing chemical use by up to 30% while limiting operator exposure. Demonstrated success in large-scale Chinese rice fields shows the scalability of unmanned spraying fleets. Therefore, policy pressure toward sustainable agriculture translates into inelastic demand that shields the sUAS market from macroeconomic cycles.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightened export controls on Chinese-made flight controllers | −1.5% | North America, Europe | Short term (≤ 2 years) |

| Component tariffs inflating battery and motor costs | −0.9% | Import-dependent markets | Medium term (2-4 years) |

| Air-traffic management (UTM) integration delays | −0.7% | Global dense-airspace regions | Medium term (2-4 years) |

| Operator-skills shortage in emerging economies | −0.5% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Air-Traffic Management (UTM) Integration Delays

Unmanned traffic management roll-outs lag behind original timetables, curbing commercial drone activity in controlled airspace. Real-time conflict-resolution between crewed and uncrewed flights remains technically complex, and current prototypes struggle to scale beyond small pilot zones. The FAA forecasts full operational capability after 2027, two years later than its target. Europe’s SESAR program faces similar headwinds, as national systems must interoperate across 27 member states, lengthening certification cycles.[2]SESAR Joint Undertaking, “European U-space Blueprint,” sesarju.eu For operators eyeing urban delivery or infrastructure inspection along busy corridors, prolonged approval timelines raise costs and dent return-on-investment models. The resulting uncertainty restrains uptake in metropolitan regions that would otherwise generate high-volume demand.

Operator-Skills Shortage in Emerging Economies

Expanding fleets in Asia-Pacific, Africa, and Latin America encounter a scarcity of certified pilots and maintenance technicians. Specialized missions such as crop spraying, linear-asset surveying, and public-safety response require advanced credentials rarely offered by local training centers. Limited aviation education infrastructure slows the pipeline for new personnel, compelling firms to import talent or restrict operations. High travel and salary premiums inflate project budgets, discouraging small and mid-sized enterprises from adopting drone solutions. Without accelerated investment in standardized curricula and certification bodies, these skills gaps will continue to cap market penetration in regions with otherwise strong demand potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Fixed-Wing Dominance Faces Hybrid Challenge

Fixed-wing craft generated the most significant revenue slice, accounting for 68.95% of 2024 demand. The aerodynamic efficiency supports six-hour patrols and 100 km mapping sorties that rotary designs cannot economically match. Nevertheless, hybrid/VTOL designs show a forecast of 19.42% CAGR through 2030, which positions them as the most disruptive force inside the sUAS market. Urban planners value vertical takeoff for rooftop launch pads, and humanitarian groups rely on tail-sitter hybrids that land on confined clearings. Edge AI autopilots now switch seamlessly between hover and forward flight, narrowing the technical gap once protected by fixed-wing incumbents.

Endurance gains from lighter composites and high-energy-density batteries let new VTOL models cross the 60-minute barrier while carrying multispectral cameras. Regulatory agencies consider these hybrids quieter than helicopters, aiding acceptance in densely populated corridors. Defense planners also prize their ability to launch from makeshift clearings yet still loiter at altitude for hours. The cumulation of these operational advantages indicates that hybrid airframes will chip away at fixed-wing share even as overall sUAS market demand expands.

By Size: Micro Segment Leadership Under Nano Pressure

Micro drones between 250 g and 2 kg retained 43.58% of revenue in 2024. Their payload allowance supports dual-sensor gimbals, lidar, or small cargo bays while qualifying for simplified licensing in many jurisdictions. However, the nano class below 250 g is slated to grow 16.3% annually. Regulatory freedom explains part of the surge: pilots face fewer administrative steps, and insurance premiums remain low. Onboard tech improvements compound that advantage. Miniaturized image sensors capture 48-MP stills, and foldable antenna arrays now stream 4K video with sub-200-ms latency.

Municipal agencies testing shielded operations waivers highlight how nano platforms reduce collision risk in urban settings. Their compact form also fits indoor inspection tasks such as boiler rooms or warehouse racks. As more industries calibrate missions to the capabilities of these featherweight craft, nano volume growth could dilute micro segment share, though the latter will continue to command higher unit prices. Together, both tiers secure a resilient base for the sUAS market.

By Application: Defense Leadership Challenged by Logistics Growth

Defense and security maintained the top share at 36.43% in 2024, led by ISR, target acquisition, and loitering munition programs across NATO states. Still, logistics and delivery will clock a brisk 17.83% CAGR thanks to regulatory green lights for routine BVLOS routes. The first Part 107 drone-for-hire waiver granted to a US police department broadened the legal precedent for commercial deliveries, aerial first-aid, and spare-parts resupply missions. Ambient social acceptance increases as communities witness faster emergency responses and lower traffic congestion.

E-commerce giants, meanwhile, invest in micro-fulfillment centers tailored to 5-kg payload multicopters, shrinking last-mile costs. Agricultural demand persists as farms deploy fleets for crop-health mapping and variable-rate spraying, although growth is steadier. Entertainment and media segments gain incremental revenue from 8K live broadcasts, but their relative weight within the sUAS market remains smaller. Dynamic shifts suggest a diversified customer mix that lowers exposure to any vertical.

By Mode of Operation: Autonomous Systems Gaining Ground

Remotely piloted systems still held 62.53% of 2024 deployments. Operator trust, legal liability standards, and insurance underwriting favor a human-on-the-loop. Nonetheless, the fully autonomous category is predicted to post an 18.91% CAGR. Edge computing boards execute collision avoidance and object tracking locally, enabling sparse connectivity missions such as offshore wind-farm surveys. Regulators now view autonomy as a safety enhancement rather than a hazard, mainly when platforms operate inside shielded or predefined corridors.

Hybrid control architectures emerge whereby takeoff and landing remain piloted, while cruise segments run autonomously. This compromise expedites certification while familiarizing end-users with autonomy benefits. As datasets validate superior safety performance, remotely piloted share will erode, positioning autonomy as the default configuration for next-generation fleets. That transition further expands the sUAS market by easing training bottlenecks and widening the available labor pool.

By Propulsion Type: Electric Dominance Faces Alternative Energy Challenge

Electric battery powertrains represented 39.41% of 2024 revenue, supported by falling lithium-ion prices and proven reliability. Hydrogen fuel cells, however, are poised for an 18.35% CAGR, making them the most exciting propulsion innovation inside the sUAS market. Test flights in early 2025 demonstrated three-hour endurance for 45-kg-payload multicopters, surpassing battery benchmarks without the noise and emissions of gasoline engines.

Tariff-driven battery cost inflation magnifies the appeal of hydrogen. Operators conducting long-range pipeline or coastline inspections see a lower total cost of ownership despite a higher upfront acquisition cost. Hybrid battery-fuel cells serve niche theaters where silent operation and rapid power bursts are critical. Solar-augmented wings power persistent stratospheric platforms but remain a specialized slice. Environmental legislation that penalizes carbon emissions will likely hasten hydrogen adoption, particularly in Europe and Japan.

Geography Analysis

North America commanded 38.38% of global revenue in 2024 due to sizeable defense contracts, robust venture financing, and a clear FAA waiver pathway. As civilian BVLOS operations mature, the sUAS market size for North America is projected to reach USD 18.3 billion by 2030. Canada’s streamlined micro-drone rules and growing need for Arctic infrastructure inspections supplement US demand. Mexico is emerging as a precision-agriculture hotspot, leveraging government incentives for modern farming.

Europe will register the fastest pace at 15.36% CAGR through 2030, propelled by harmonized EASA regulations and aggressive sustainability mandates. Germany’s multiyear procurement of loitering munitions and France’s investment in medical drone corridors illustrate diversified traction.[3]European Union Aviation Safety Agency, “Drone Regulation Roadmap,” easa.europa.eu The region’s drone surveying market is forecast to double as governments digitize construction oversight and renewable-energy asset monitoring. The sUAS market benefits from EU recovery funds channelled toward green and digital projects.

Asia-Pacific ranks as the second-largest region and boasts heterogeneous growth drivers. China’s giant agricultural fleet validates scalability, yet export controls encourage self-reliance among competitors such as South Korea and India. Japan pioneers thermal-imaging payloads for disaster-response missions, and Australia’s vast mining concessions demand autonomous long-range platforms. Elsewhere, the Middle East and Africa show nascent uptake centered on pipeline security and humanitarian aid drops. Targeted public-private partnerships could accelerate adoption as regulations evolve.

Competitive Landscape

Market concentration remains moderate, with DJI retaining roughly 70% of the global share. That dominance introduces supply-chain risk for Western customers wary of equipment sourced from China. The September 2024 export controls heightened urgency for local alternatives, boosting sales pipelines at US and European firms specializing in secure flight-control software. Investment patterns reveal vertical integration strategies. Camera makers acquire AI analytics startups, and airframe vendors purchase power-system specialists to insulate themselves from upstream shocks.

Strategic moves since late 2024 underscore differentiation around autonomy and mission-specific payloads. Skydio secured USD 170 million in Series E funding to scale defense-grade autonomous craft. Teledyne FLIR landed a USD 15 million contract with German forces for Black Hornet 4 nano-systems, spotlighting demand for ISR micro-platforms.[4]Teledyne FLIR, “FLIR Wins German Defense Contract for Black Hornet 4,” flir.com Firestorm Labs’ USD 100 million additive-manufacturing contract signals defense appetite for agile production. These deals reconfigure value pools inside the sUAS market toward software and specialized services rather than commoditized airframes.

White-space opportunities abound in hydrogen propulsion, underground-mine surveying, and maritime launch swarms. Startups leveraging proprietary power systems or AI-based fleet orchestration can carve profitable niches even while overall competition intensifies. Over time, the top five vendors are expected to hold close to 55% combined revenue, allowing smaller specialists to thrive through application focus and regional compliance expertise.

Small Unmanned Aerial Systems (sUAS) Industry Leaders

SZ DJI Technology Co., Ltd.

Skydio, Inc.

Autel Robotics Co., Ltd.

AeroVironment, Inc.

Elbit Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The NATO Support and Procurement Agency (NSPA) selected Skydio and its European partner COBBS BELUX BV to supply small ISR drones to NATO member nations through the UAS Support Partnership.

- February 2025: Teledyne FLIR secured USD 15 million from Germany for Black Hornet 4 nano-drones to enhance urban reconnaissance.

- January 2025: The US Air Force awarded Firestorm Labs a USD 100-million contract for its sUAS.

- December 2024: Performance Drone Works (PDW) secured contracts worth USD 15.3 million to supply its C100 sUAS to the US Army.

Global Small Unmanned Aerial Systems (sUAS) Market Report Scope

| Fixed-Wing |

| Rotary-Wing |

| Hybrid/VTOL |

| Nano (Less than 250 g) |

| Micro (250 g to 2 kg) |

| Mini (2 kg to 25 kg) |

| Defense and Security |

| Agriculture and Environment |

| Infrastructure Inspection and Monitoring |

| Mapping and Surveying |

| Media and Entertainment |

| Logistics and Delivery |

| Public Safety and Emergency Response |

| Other Commercial Applications |

| Remotely Piloted |

| Partially Autonomous |

| Fully Autonomous |

| Electric Battery |

| Hybrid (Fuel + Battery) |

| Solar-Powered |

| Hydrogen Fuel Cell |

| Gasoline/ICE |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Platform Type | Fixed-Wing | ||

| Rotary-Wing | |||

| Hybrid/VTOL | |||

| By Size | Nano (Less than 250 g) | ||

| Micro (250 g to 2 kg) | |||

| Mini (2 kg to 25 kg) | |||

| By Application | Defense and Security | ||

| Agriculture and Environment | |||

| Infrastructure Inspection and Monitoring | |||

| Mapping and Surveying | |||

| Media and Entertainment | |||

| Logistics and Delivery | |||

| Public Safety and Emergency Response | |||

| Other Commercial Applications | |||

| By Mode of Operation | Remotely Piloted | ||

| Partially Autonomous | |||

| Fully Autonomous | |||

| By Propulsion Type | Electric Battery | ||

| Hybrid (Fuel + Battery) | |||

| Solar-Powered | |||

| Hydrogen Fuel Cell | |||

| Gasoline/ICE | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 market value for small unmanned aerial systems (sUAS) and the expected CAGR through 2030?

The sector stands at USD 20.106 billion in 2025 and is projected to grow at a 16.20% CAGR through 2030.

Which platform type holds the largest revenue share today?

Fixed-wing aircraft commanded 68.95% of 2024 global revenue.

Which end-use application is projected to expand the fastest by 2030?

Logistics and delivery is on track for a 17.83% CAGR, the highest among all applications.

What propulsion technology is seeing the strongest growth momentum?

Hydrogen fuel-cell systems are forecasted to advance at an 18.35% CAGR through 2030.

Which geography is anticipated to record the quickest expansion over the forecast window?

Europe is expected to post the fastest regional growth at a 15.36% CAGR.

How are autonomous drones reshaping deployment trends?

Fully autonomous systems are set to grow at an 18.91% CAGR, steadily eroding the dominance of remotely piloted models.

Page last updated on: