High-Performance Liquid Chromatography (HPLC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

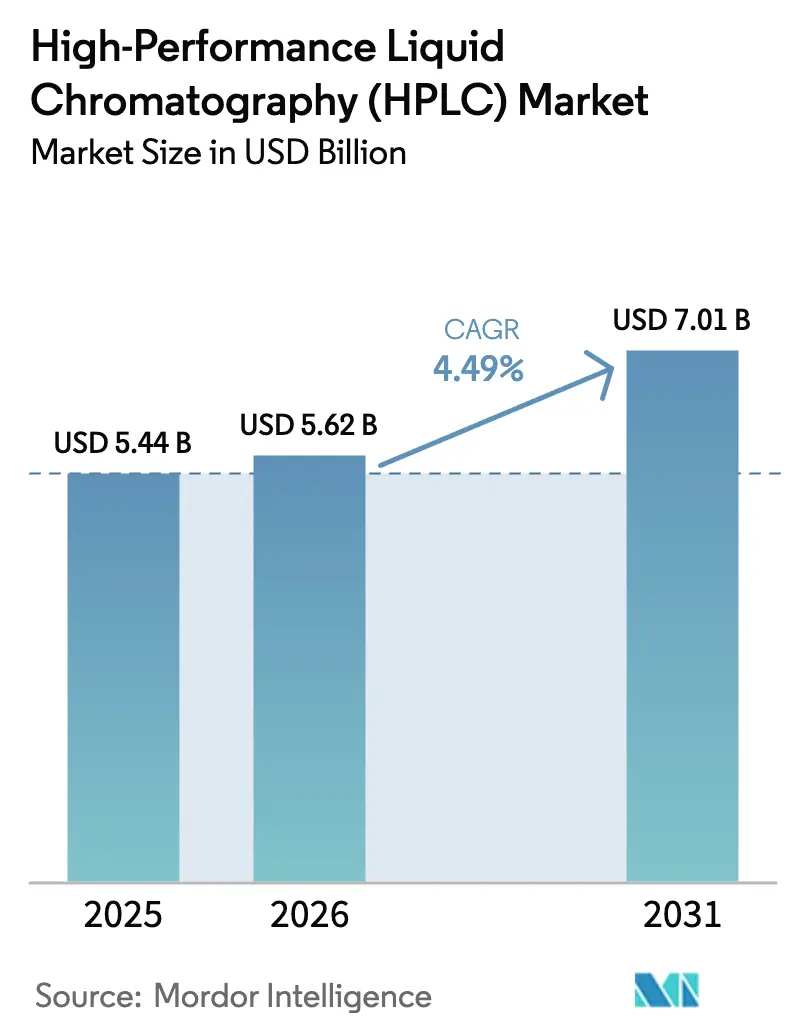

| Market Size (2026) | USD 5.62 Billion |

| Market Size (2031) | USD 7.01 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

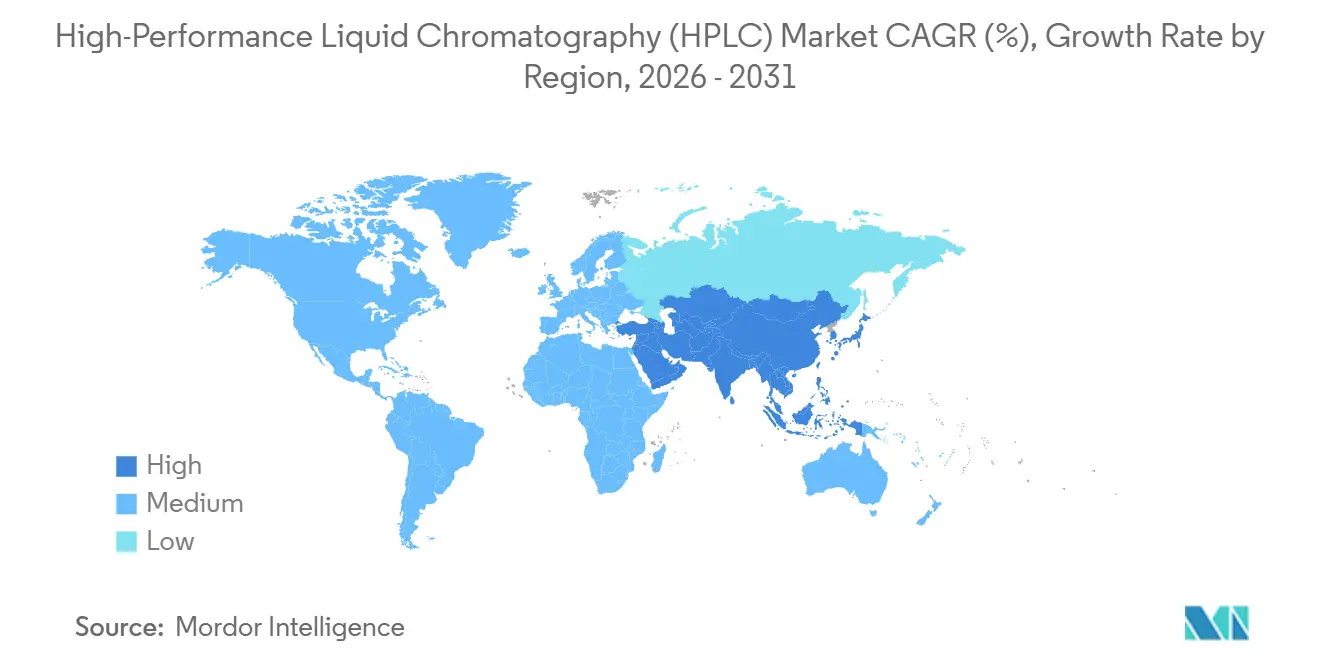

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-Performance Liquid Chromatography (HPLC) Market Analysis by Mordor Intelligence

The High-Performance Liquid Chromatography Market size is expected to grow from USD 5.44 billion in 2025 to USD 5.62 billion in 2026 and is forecast to reach USD 7.01 billion by 2031 at 4.49% CAGR over 2026-2031.

The steady course reflects durable instrument lifecycles that anchor recurring consumable sales, while periodic demand spikes originate from biopharmaceutical breakthroughs, stricter global quality-assurance mandates, and migration toward ultra-high-performance systems. Incumbent vendors are accelerating platform refreshes that bundle AI-enabled diagnostics and solvent-savings accessories to defend installed bases. Rising adoption in food safety labs, the pivot to antibody and gene-therapy pipelines, and Asia-Pacific’s regulatory harmonization with Western agencies together widen the addressable High-Performance Liquid Chromatography market opportunity. Competitive intensity remains moderate because razor-and-blade economics reward suppliers that can embed exclusive column chemistries into validated methods, yet white-space niches in microfluidic chips and predictive maintenance invite agile entrants.

Key Report Takeaways

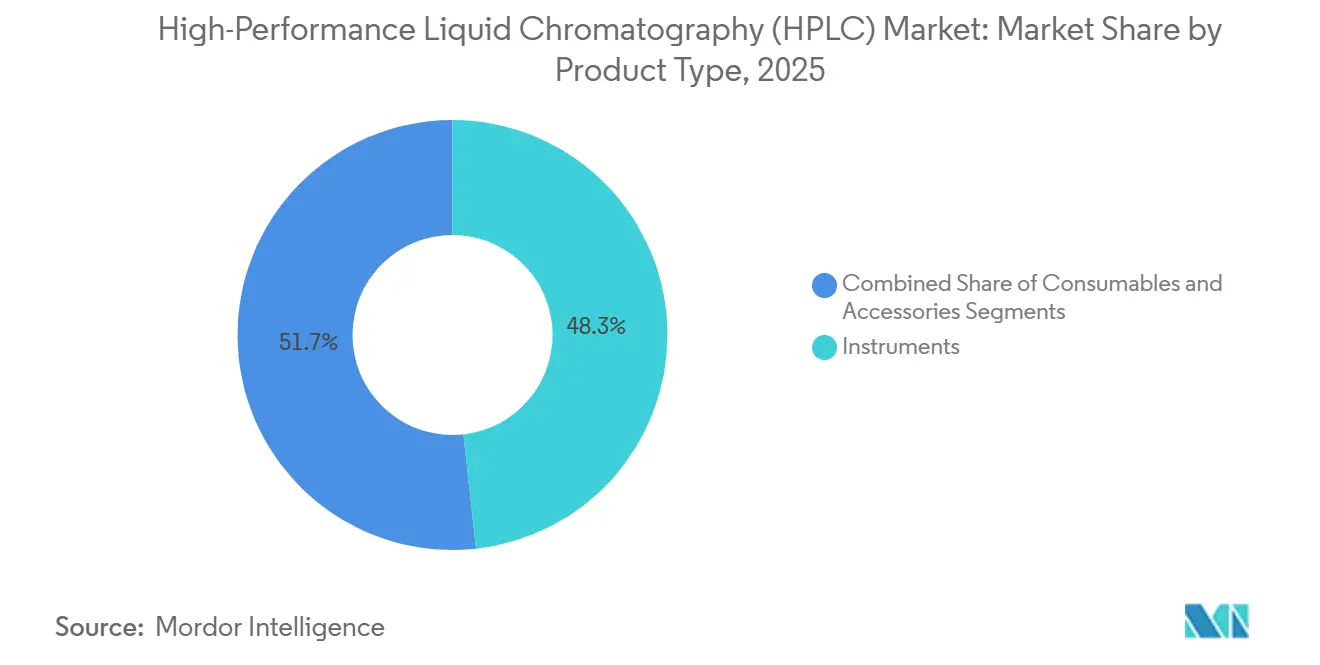

- By product type, instruments accounted for 48.25% of revenue share in 2025 while consumables are expanding at an 8.26% CAGR through 2031.

- By application, food and beverage testing is growing at 7.23% CAGR to 2031, whereas pharmaceutical and biotechnology research led with a 37.47% share in 2025.

- By separation mode, reverse-phase held 53.21% share in 2025, and affinity HPLC shows the fastest 8.66% CAGR to 2031.

- By detection method, UV/Vis dominated with 60.72% share in 2025, whereas mass-spectrometry detection is advancing at a 7.89% CAGR.

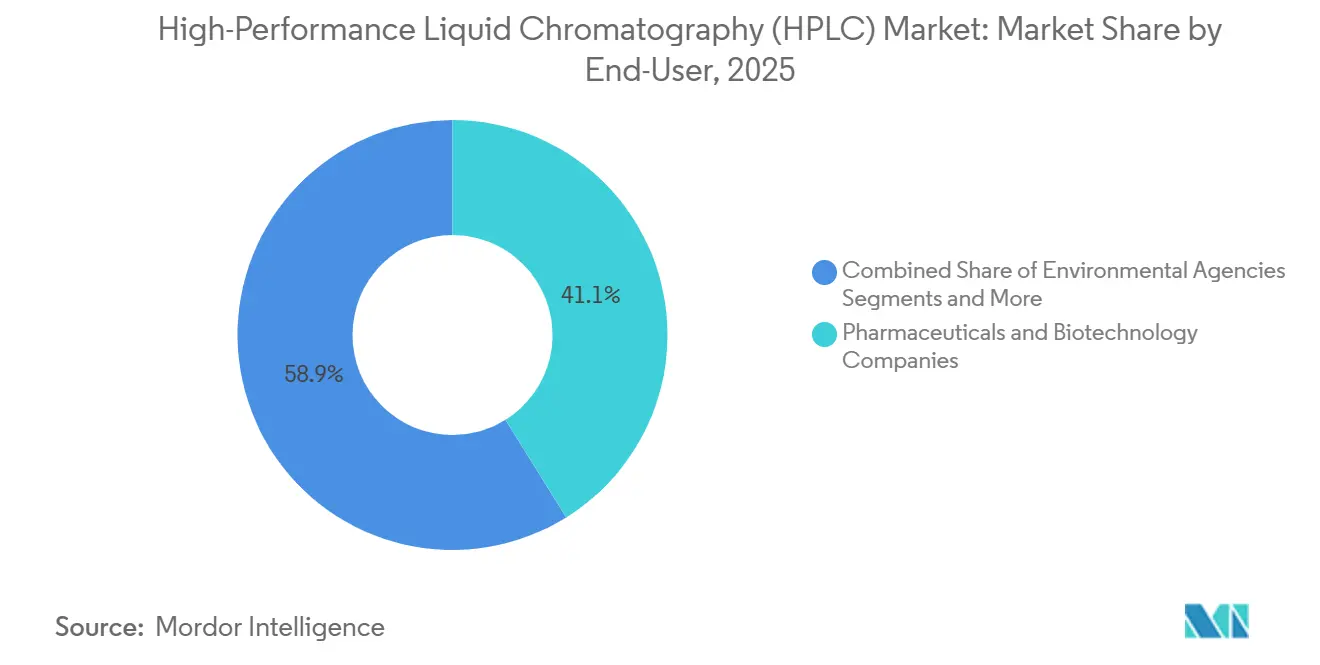

- By end-user, pharmaceutical and biotechnology companies captured 41.12% share in 2025, yet contract research organizations are pacing ahead at 6.34% CAGR.

- By geography, North America retained a 37.66% share in 2025, while Asia-Pacific is progressing at a 6.72% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High-Performance Liquid Chromatography (HPLC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for biopharmaceuticals & monoclonal antibodies | +1.2% | North America, Europe, China, India, South Korea | Long term (≥ 4 years) |

| Increasing adoption in food safety & environmental testing | +0.8% | China, India, European Union, North America | Medium term (2-4 years) |

| Growing prominence of UHPLC for high-throughput screening | +0.7% | United States, Germany, Japan | Short term (≤ 2 years) |

| Advances in microfluidic / chip-based HPLC platforms | +0.5% | United States, Germany, United Kingdom | Long term (≥ 4 years) |

| Integration of AI-driven predictive maintenance | +0.4% | United States, Canada, Western Europe | Medium term (2-4 years) |

| Stringent regulatory guidelines for pharma QA | +0.9% | Global, prominence in United States, Europe, China, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Biopharmaceuticals & Monoclonal Antibodies

Eighteen monoclonal antibodies won FDA approval in 2024, sustaining a pipeline that now depends on multi-column purification trains combining affinity, ion-exchange, and size-exclusion modes to assure 99% purity thresholds.[1]U.S. Food and Drug Administration Staff, “Novel Drug Approvals 2024,” U.S. Food and Drug Administration, fda.gov Contract manufacturers without in-house method-development talent are therefore acquiring complete HPLC workstations bundled with vendor service contracts covering validation and lifecycle support. Biosimilar producers in India and China face 18-month bioequivalence windows that reward validated UHPLC methods over legacy protocols, compressing buying cycles for high-throughput instruments. EMA’s 2025 revision of ICH Q6B now compels orthogonal glycosylation confirmation, driving demand for dual-detector configurations that pair UV with fluorescence or mass spectrometry. Cell- and gene-therapy vectors require quantification of residual plasmid DNA at parts-per-billion levels, catalyzing column innovation toward sub-2 µm particle beds that withstand 18,000 psi operating pressures. Collectively, these factors enlarge the High-Performance Liquid Chromatography market footprint in bioprocess analytics.

Increasing Adoption in Food Safety & Environmental Testing

The U.S. FDA’s final preventive-controls rule added mandatory mycotoxin screening for imported grains, triggering around 2,500 instrument placements across border laboratories in 2024.[2]U.S. Food and Drug Administration Staff, “FDA Updates Mycotoxins in Domestic and Imported Human Foods Compliance Program,” U.S. Food and Drug Administration, fda.gov China released 47 new food-safety standards in 2025, most citing HPLC as the reference technique for pesticides, thereby shifting provincial budgets toward columns and solvent packs rather than gas-chromatography alternatives.[3]Zhuohong Wang and Xiong Yuyang, “47 National Food Safety Standards Released,” Foreign Agricultural Service, fas.usda.gov The European Union incorporated HPLC-MS into its 2024 Drinking Water Directive update to monitor PFAS compounds that lack chromophores. Brazil now obliges aflatoxin verification in coffee exports using HPLC, illustrating how emerging economies retrofit facilities to meet EU thresholds, which in turn fertilizes regional demand in the High-Performance Liquid Chromatography market. Authenticity testing for olive oil and honey further expands column throughput by applying chromatographic fingerprints to verify geographic origin for premium labeling.

Growing Prominence of UHPLC for High-Throughput Screening

Operating beyond 15,000 psi, UHPLC shortened routine assays from 30 minutes to under 5 minutes, enabling pharmaceutical discovery groups to screen approximately 1.2 million compounds per year, according to a 2025 Journal of Medicinal Chemistry survey. Although a UHPLC system costs roughly USD 150,000 versus USD 50,000 for conventional units, heavy-use laboratories recover the premium within 18 months through instrument consolidation. Novel sub-2 µm polysaccharide-based chiral columns now resolve enantiomers inside 3 minutes, feeding CRO service models that bill per injection rather than per sample batch. Compact form factors under 0.5 m² and <500 W power consumption bring UHPLC capabilities to universities in Southeast Asia and Latin America where infrastructure limits once curbed adoption. Solvent usage remains a friction point; higher flow rates can double acetonitrile consumption, so vendors are integrating recycling loops and method-optimization software, strengthening consumables pull-through in the High-Performance Liquid Chromatography market.

Advances in Microfluidic / Chip-Based HPLC Platforms

Microfluidic chips no larger than a credit card now integrate injection valves, separation channels, and on-chip UV detection, achieving 90% correlation with benchtop systems in a 2024 Analytical Chemistry validation. Production costs have fallen near USD 50 per chip, yet fragile glass and a lack of connector standards curb commercialization outside research. Agilent’s 2025 patent on a polymer chip with built-in gradient mixing signals incumbent hedging, even as they prioritize consumable-rich conventional columns. Open-source academic consortia may accelerate commoditization if regulators accept chip workflows for method validation, a shift that could fragment the High-Performance Liquid Chromatography market. Integration with MS remains challenging because low-nanoliter flow rates depress ionization efficiency, confining chip platforms to analytes amenable to UV detection and delaying their use in proteomics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of instruments & maintenance | -0.6% | Emerging markets in Asia-Pacific, Middle East & Africa, South America | Short term (≤ 2 years) |

| Shortage of skilled chromatographers | -0.4% | Asia-Pacific, Middle East & Africa | Medium term (2-4 years) |

| Regulatory push toward greener analytical techniques | -0.3% | Europe, North America | Long term (≥ 4 years) |

| Competition from alternative separation technologies | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Instruments & Maintenance

Entry-level systems priced at USD 40,000 escalate to >USD 250,000 when mass-spectrometry compatibility and CFR Part 11 software are included, intimidating small labs in emerging economies. Annual service contracts add another 8–12% of purchase price, yet forgoing OEM maintenance often voids warranties and jeopardizes regulatory compliance. High-throughput sites may burn through 30 columns per year at USD 500–1,500 each, lifting total ownership above USD 500,000 across ten years, a barrier that stretches replacement cycles and dampens High-Performance Liquid Chromatography market growth. Lease-to-own models offer relief but impose interest costs near 8%, and clauses frequently restrict buyers to vendor consumables.

Shortage of Skilled Chromatographers

An American Chemical Society 2025 survey found 38% of labs struggle to hire HPLC-trained analysts, as university enrollment in analytical chemistry wanes. Training novices to manage gradient optimization, system-suitability metrics, and audit-trail software takes up to 18 months, delaying productivity gains. Modern instruments meld fluidics, electronics, and informatics, demanding hybrid skill sets scarce in Asia-Pacific production hubs. Vendor-run certification courses cover basic operation but seldom impart troubleshooting acumen, prolonging downtime when ghost peaks or retention drift occur. Dependence on expatriate specialists elevates costs for manufacturers in India and China, tightening High-Performance Liquid Chromatography market margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Outpace Instruments

Consumables are projected to grow at 8.26% through 2031, nearly twice the overall High-Performance Liquid Chromatography market. Column turnover every 200–500 injections, solvent consumption that averages 10–20 L of acetonitrile weekly, and proprietary buffer packs together reinforce a steady consumable pull. The instruments segment, which captured 48.25% in 2025, expands more slowly because robust UHPLC chassis remain serviceable for >10 years with regular maintenance.

Column innovations extend lifetime by up to 50%, yet higher UHPLC pressures hasten wear, ensuring recurring demand. Accessories—autosamplers, degassers, column ovens—add incremental upgrades as labs retrofit legacy systems for data-integrity compliance. Vendors leveraging razor-and-blade economics secure durable footholds in the High-Performance Liquid Chromatography market, especially when validated methods embed exclusive column chemistries.

By Application: Food Testing Gains Momentum

Food and beverage testing advances at 7.23% CAGR to 2031, driven by import regulations, contamination scandals, and authenticity verification. Pharmaceutical and biotechnology research still represents the single largest slice at 37.47% in 2025, but its share erodes as generic competition compresses R&D budgets and biologics rely on orthogonal analytics.

Clinical diagnostics grows slowly because point-of-care immunoassays replace many HPLC tests, relegating chromatography to specialist panels. Environmental monitoring remains stable, while forensic labs expand usage for seized-drug profiling and toxicology. Demand diversification cushions the High-Performance Liquid Chromatography market against cyclical swings in pharmaceutical capital expenditure.

By Separation Mode: Affinity HPLC Surges

Reverse-phase systems held 53.21% of 2025 revenue, fueled by small-molecule versatility, yet affinity HPLC exhibits the strongest 8.66% CAGR, mirroring monoclonal antibody growth. Ion-exchange and size-exclusion remain essential for charge-variant and aggregation analyses, though lengthy run times constrain throughput.

Affinity HPLC adoption accelerates in biosimilar manufacturing hubs across Asia, where multi-column setups purify concurrent antibody projects. Reverse-phase methods face sustainability scrutiny for acetonitrile consumption, encouraging greener buffer systems that could subtly tilt High-Performance Liquid Chromatography market preferences over the next decade.

By Detection Method: Mass Spectrometry Ascends

UV/Vis detectors dominated with 60.72% share in 2025 thanks to compendial references, yet mass-spectrometry detectors are climbing at 7.89% CAGR, propelled by falling triple-quadrupole prices and expanding metabolomics datasets. Fluorescence, refractive-index, and electrochemical detectors inhabit specialist niches but jointly account for a minority share.

High-resolution time-of-flight systems now support routine impurity profiling, eroding UV-only installations in drug-development labs. As capital costs drop below USD 200,000, LC-MS adoption rises among mid-tier CROs and academic cores, widening the addressable High-Performance Liquid Chromatography market.

By End-User: CROs Capture Share

Pharmaceutical and biotechnology companies retained 41.12% share in 2025, yet contract research organizations are pacing ahead at 6.34% CAGR, reflecting the sector’s shift to asset-light models. Academic institutes show minimal expansion due to grant cycles, while hospital labs migrate toward point-of-care devices, capping HPLC demand.

Environmental agencies maintain a steady replacement cadence governed by statutory monitoring, whereas food-processing firms bring testing in-house to safeguard supply chains. Outsourcing momentum ensures CRO laboratories remain a pivotal growth engine within the High-Performance Liquid Chromatography market.

Geography Analysis

North America commanded 37.66% of 2025 revenue courtesy of FDA-driven validation norms that stipulate triplicate HPLC runs for each batch release. An aging installed base—40% of systems exceed 10 years—creates a ripe replacement pool as vendors offer trade-in credits toward AI-enabled UHPLC platforms. Canada and Mexico contribute incremental growth, the latter benefitting from near-shoring that places analytical labs near manufacturing plants to shorten logistics.

Asia-Pacific advances at 6.72% CAGR through 2031 as China, India, and South Korea tighten GMP parity with Western agencies. China’s 2024 Drug Administration Law amendment forces chromatographic testing even for traditional medicines, while Indian generic producers invest in data-integrity upgrades to satisfy FDA observations. Southeast Asian exporters adopt HPLC to meet EU pesticide residue limits, diffusing demand across Thailand, Vietnam, and Indonesia and enlarging the regional High-Performance Liquid Chromatography market.

Europe exhibits steady uptake anchored by EMA and EFSA directives. Western European nations modernize fleets with solvent-savings accessories aligned to the EU Green Deal, and Southern Europe’s olive-oil and wine sectors deploy HPLC authenticity assays to secure denomination-of-origin labels. Eastern Europe attracts pharmaceutical investments seeking EU-based yet cost-effective production, channeling instrument placements into Poland and the Czech Republic. Middle East & Africa and South America maintain modest shares, yet public investment in food-safety and local drug manufacturing underpins incremental growth, with Brazil and GCC states leading regional adoption.

Competitive Landscape

The High-Performance Liquid Chromatography market demonstrates moderate concentration. These incumbents bind customers through multi-year service pacts that couple preventative maintenance with proprietary consumable supply, elevating switching barriers. Yet microfluidic chip start-ups and software-centric entrants challenge this hold by offering open architectures that welcome third-party columns and detectors.

Product differentiation now tilts toward informatics. Agilent’s AI-driven method-development assistant recommends gradients from molecular structure libraries, cutting development cycles. Waters’ cloud analytics platform aggregates chromatograms across facilities, employing multivariate models to flag subtle batch deviations in real time. These software pivots turn hardware into gateways for recurring subscription revenue, reframing competitive stakes inside the High-Performance Liquid Chromatography market.

Disruptors face regulatory inertia, as pharmaceutical firms favor platforms with documented precedent in FDA submissions. ISO 17025 accreditation further deters unproven hardware. Nonetheless, white-space remains in ruggedized, battery-powered instruments for on-site water assessment and point-of-care drug monitoring, where incumbents’ large-footprint systems struggle. Strategic partnerships, such as Shimadzu’s 2024 biopharma alliance and Waters’ cross-licensing of microfluidic patents, illustrate how leaders hedge against erosion while reinforcing installed ecosystems.

High-Performance Liquid Chromatography (HPLC) Industry Leaders

Waters Corporation

Agilent Technologies Inc.

Thermo Fisher Scientific Inc.

Shimadzu Corporation

Danaher Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Agilent launched Altura Ultra Inert HPLC columns optimized for peptide GLP-1 and oligonucleotide QC.

- September 2025: Infitek unveiled the HPLC-W3200, HPLC-W3400, and HPLC-6000 systems, spotlighting reliability improvements for global customers.

- April 2025: Waters expanded its Alliance iS Bio line with integrated photodiode array detection to streamline QC workflows.

- March 2025: Axcend introduced a palm-sized low-flow system with 40-vial autosampler, enabling real-time analysis at the sampling point.

- November 2024: The Berthiaume Institute for Precision Health and Waters Corporation delivered an HPLC training workshop that issued digital micro-credentials to participating graduate students.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the high-performance liquid chromatography (HPLC) market covers all new bench-top or floor-standing instruments, associated columns, solvents, and small accessories used to separate, identify, and quantify analytes as liquids are pushed through packed columns under high pressure. This study includes conventional, ultra-high-pressure, nano, and micro-chip formats that are factory built and sold for research, quality control, and diagnostic use across life science, chemical, food, environmental, and forensic laboratories worldwide.

Scope exclusion: disposable cartridge kits integrated in point-of-care analyzers and chromatography methods based on gas, thin-layer, or paper principles are out of scope.

Segmentation Overview

- By Product Type

- Instruments

- Consumables

- Accessories

- By Application

- Pharmaceutical & Biotechnology Research

- Clinical Diagnostics

- Food & Beverage Testing

- Environmental Analysis

- Forensic Science

- Other Industrial Applications

- By Separation Mode

- Reverse-Phase HPLC

- Ion-Exchange HPLC

- Size-Exclusion HPLC

- Affinity HPLC

- Hydrophobic-Interaction HPLC

- Other Modes

- By Detection Method

- UV/Vis Detectors

- Fluorescence Detectors

- Refractive-Index Detectors

- Mass-Spectrometry Detectors

- Electrochemical Detectors

- Others

- By End-User

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations

- Hospitals & Clinics

- Environmental Agencies

- Food & Beverage Companies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed laboratory managers, third-party service engineers, distributor heads, and regulatory consultants across North America, Europe, China, India, and Brazil. These conversations confirmed replacement cycles, consumable pull-through ratios, and regional ASP spreads, and then helped validate preliminary desk findings before final modeling.

Desk Research

We began with publicly available datasets such as US FDA 510(k) clearances, European Medicines Agency labeling dossiers, World Bank health-related R and D spending, OECD trade codes for HS 9018.90 instruments, and peer-reviewed articles indexed on PubMed, which together map installed base and application mix. Company 10-Ks, investor decks, and national procurement portals added pricing color, while D&B Hoovers and Questel supplied revenue splits and patent trends. Such sources underpin the historical demand curve. The examples listed illustrate our approach; many additional references were consulted for triangulation and clarification.

Market-Sizing & Forecasting

A top-down installed base reconstruction blending production registers, import-export flows, and average replacement intervals gave the initial 2025 demand pool, which we cross-checked with selective bottom-up roll-ups of supplier revenues and sampled ASP × volume estimates. Key variables in the model include laboratory installed base, mean five-year replacement cycle, pharma R and D outlay, number of clinical research trials, solvent consumption per run, and price premium shift from conventional to UHPLC. Multivariate regression, supplemented by an ARIMA trend overlay, projects each driver and yields the 2025-2030 value trajectory; expert feedback guides scenario weighting where historic volatility exists. Gaps appearing in bottom-up samples are prorated using regional penetration benchmarks drawn from primary interviews.

Data Validation & Update Cycle

Before sign-off, an analyst runs variance checks against external price and trade indicators, elevating outliers for review. Reports refresh every year, and we trigger interim updates when regulatory, macroeconomic, or technology events materially sway any core variable. A last-minute sense check is completed just before delivery so clients always receive the latest view.

Why Our High-Performance Liquid Chromatography Baseline Stands Up to Scrutiny

Published market values often disagree because firms pick different product baskets, service add-ons, and refresh intervals, and because currency conversions vary.

Key gap drivers are usually widened scopes that mix service contracts, refurbished units, or adjacent chromatography techniques, or alternatively optimistic uptake rates for emerging UHPLC systems that lack on-the-ground validation. Mordor keeps a tighter lens on new hardware plus immediate consumables, employs annual refreshes instead of multi-year static baselines, and converts revenues at average yearly exchange rates to dampen volatility.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.22 B (2025) | Mordor Intelligence | - |

| USD 5.25 B (2025) | Global Consultancy A | Includes refurbished systems and multi-year service bundles |

| USD 5.65 B (2025) | Industry Analytics B | Applies aggressive UHPLC penetration and lists solvent recycling equipment |

The comparison shows that once overlapping additions are stripped away, Mordor's disciplined scope, driver-verified assumptions, and annual update cadence deliver a balanced and repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the forecast value of the High-Performance Liquid Chromatography market in 2031?

The market is expected to reach USD 7.01 billion by 2031.

Which application area will grow the fastest through 2031?

Food and beverage testing is projected to expand at a 7.23% CAGR, the highest among all applications.

Why are consumables outperforming instruments?

Recurring column and solvent needs, combined with method-validation lock-in, drive consumables’ 8.26% CAGR versus slower instrument replacement cycles.

What region will contribute the most new revenue?

Asia-Pacific, with a 6.72% CAGR, will add the largest incremental revenue due to regulatory harmonization and manufacturing expansion.

Which detection method is gaining momentum over UV/Vis?

Mass-spectrometry detectors are rising at a 7.89% CAGR on the back of proteomics and metabolomics adoption.

Page last updated on: