Blockchain Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.30 Billion |

| Market Size (2031) | USD 6.96 Billion |

| Growth Rate (2026 - 2031) | 39.85% CAGR |

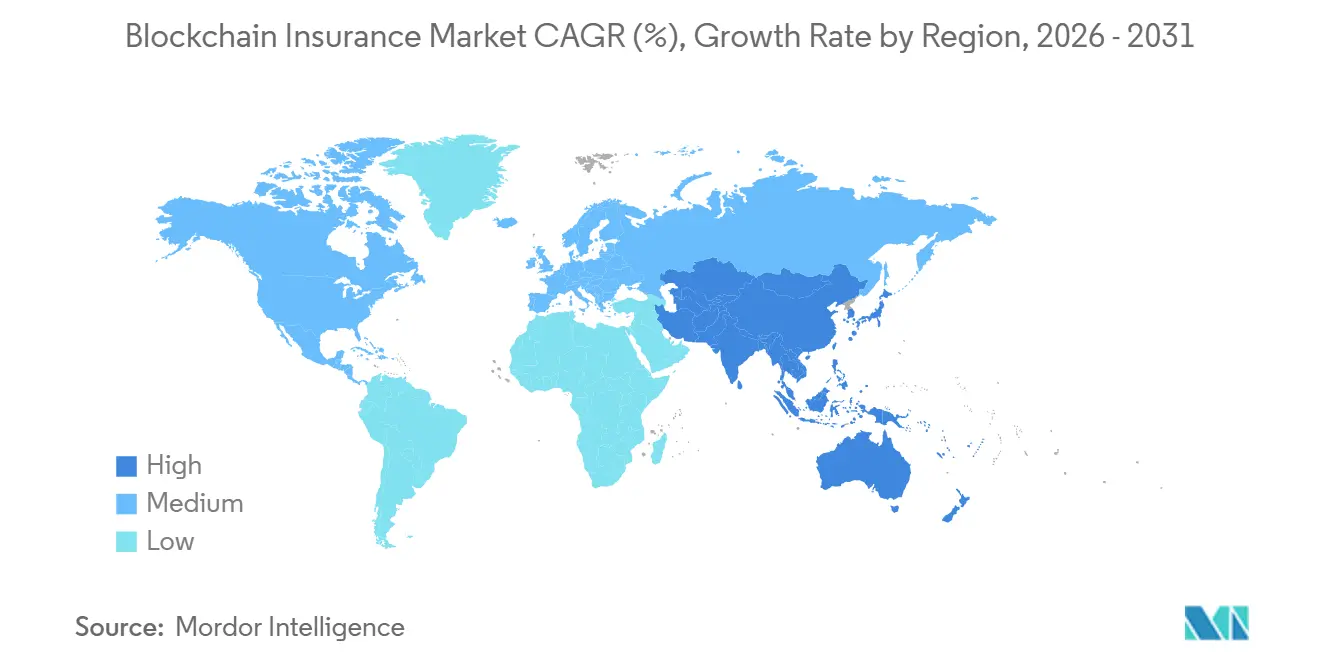

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

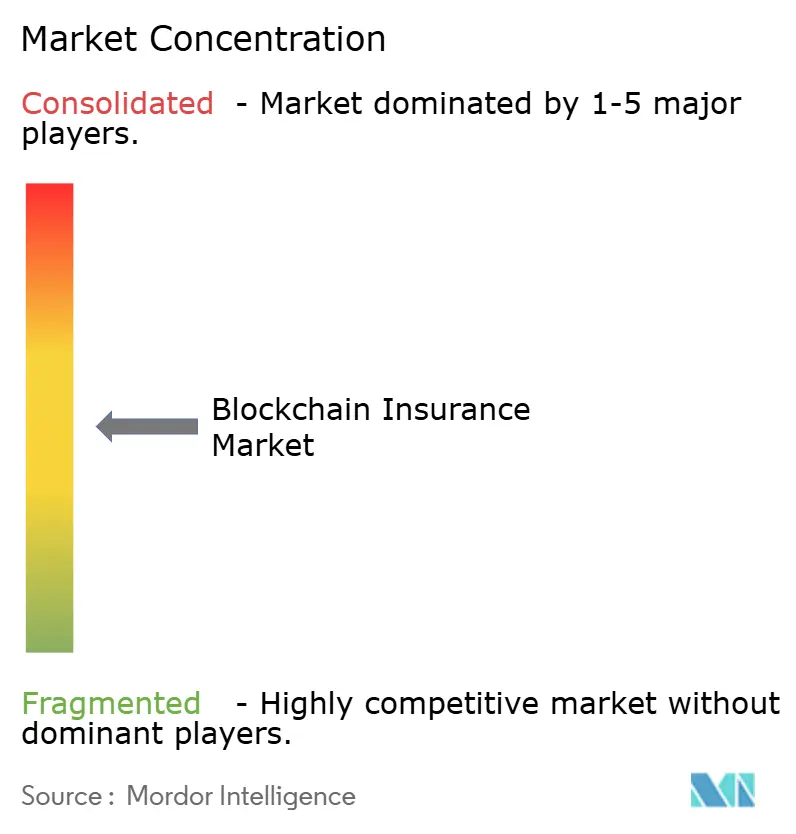

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blockchain Insurance Market Analysis by Mordor Intelligence

The Blockchain Insurance Market size is projected to expand from USD 0.93 billion in 2025 and USD 1.30 billion in 2026 to USD 6.96 billion by 2031, registering a CAGR of 39.85% between 2026 to 2031.

Expanding regulatory pressure for real-time reporting, rising fraud losses that top USD 40 billion each year, and the maturation of smart-contract toolkits are combining to accelerate adoption across underwriting, claims, and reinsurance workflows. Cloud platforms now give insurers on-demand ledger infrastructure, while private networks safeguard customer data, resolving a long-standing tension between openness and confidentiality. Rapid growth in parametric insurance, tokenized ILS trading, and ESG-linked audit trails shows how blockchain stretches beyond basic record keeping into entirely new revenue streams. Together, these forces create an environment where first movers can compress operating costs, capture new customers, and satisfy supervisors in one coordinated upgrade to their core systems.

Key Report Takeaways

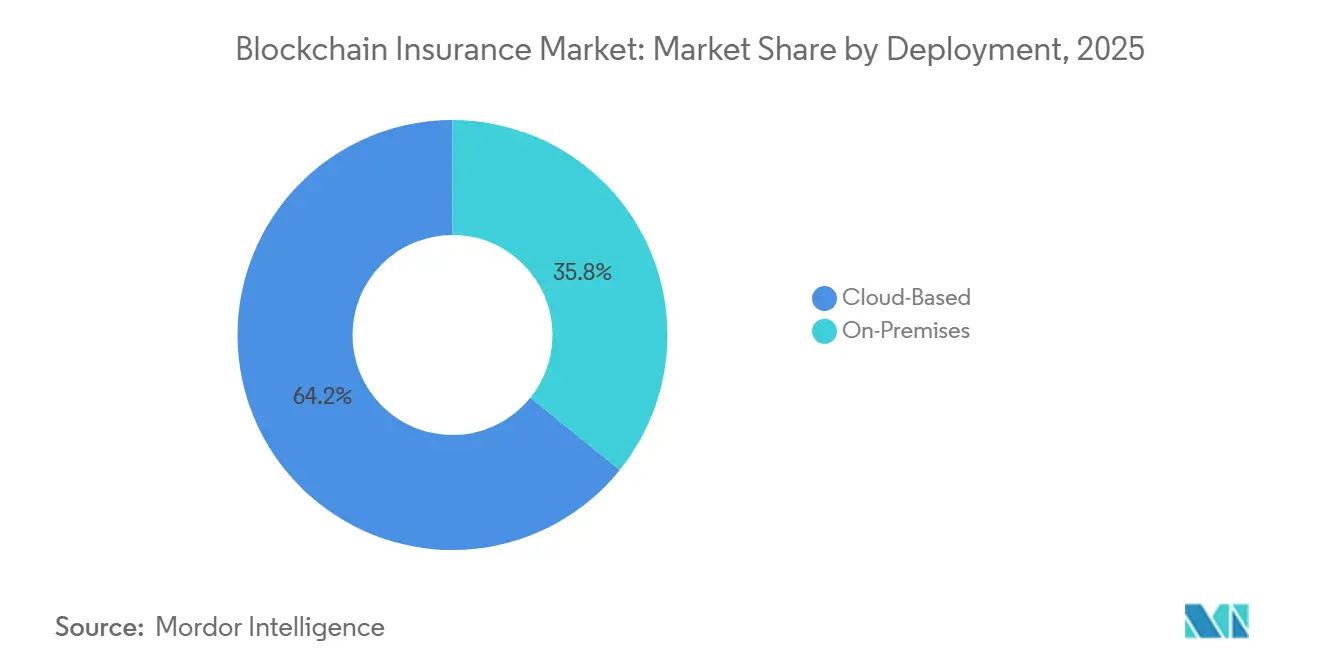

- By deployment, cloud solutions led with 64.20% revenue share of the blockchain insurance market size in 2025, whereas on-premises implementations are projected to grow at a 41.35% CAGR through 2031.

- By blockchain type, private networks held 61.10% of the blockchain in insurance market share in 2025, while consortium chains recorded the fastest expansion at 41.20% CAGR to 2031.

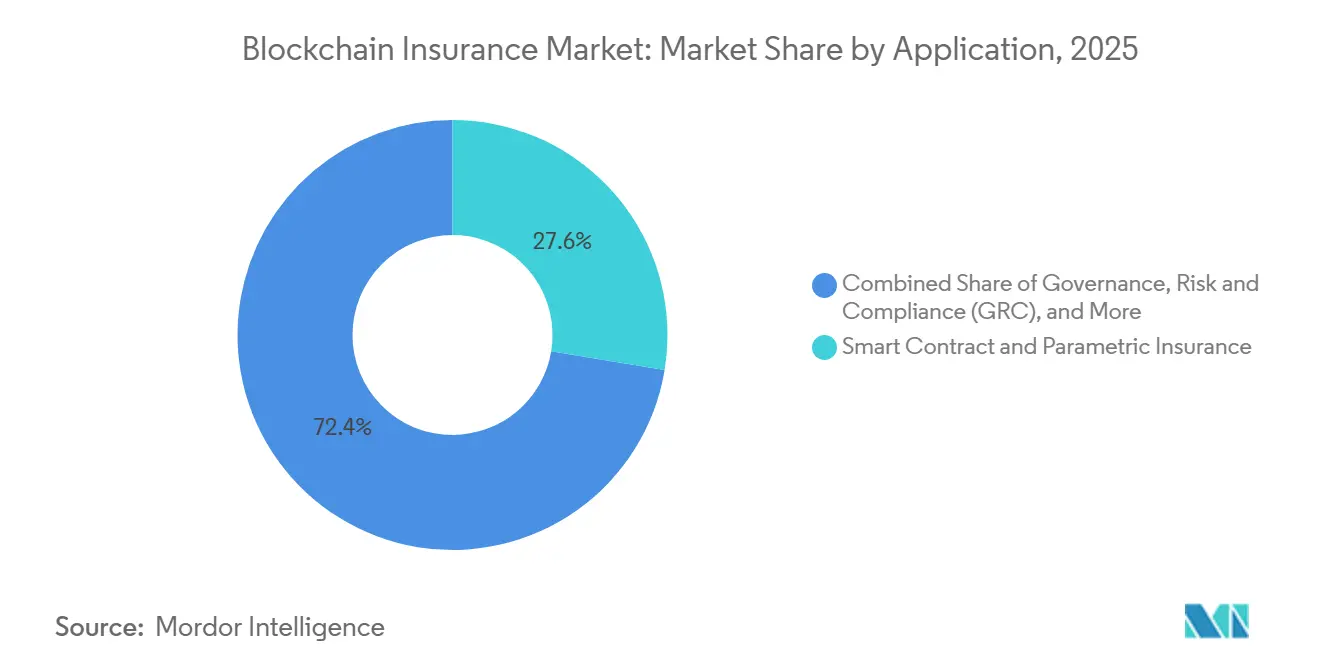

- By application, smart-contract and parametric offerings captured a 27.60% share of the blockchain nsurance market size in 2025 and are advancing at a 41.05% CAGR through 2031.

- By enterprise size, large carriers controlled a 67.10% share in 2025, yet SMEs are on track for a 40.95% CAGR amid rising blockchain-as-a-service options.

- By geography, North America commanded a 44.30% share of the blockchain insurance market size in 2025, whereas Asia Pacific is set to post the highest CAGR at 41.35% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blockchain Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising fraud-related losses demand tamper-proof claims data | +8.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Smart-contract automation lowers administrative costs | +7.8% | Global, led by developed markets with regulatory clarity | Short term (≤2 years) |

| Regulatory mandates for real-time reporting and transparency | +6.5% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Parametric micro-insurance for climate and crop risks in emerging markets | +5.9% | APAC, Africa, Latin America | Long term (≥4 years) |

| On-chain tokenization of risk portfolios and ILS trading | +4.7% | North America and Europe (institutional markets) | Long term (≥4 years) |

| ESG audit trails driving verifiable carbon offset underwriting | +3.8% | Global, with early adoption in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising fraud-related losses are demanding tamper-proof claims data

Insurance fraud inflates global claims outlays by more than USD 40 billion each year, and 5–10% of all submissions contain a fraudulent element. Blockchain records lock each event into a shared, append-only ledger, enabling carriers, reinsurers, and TPAs to cross-check entries and reject duplicates in seconds. Allianz validated the approach by rolling out a multi-country blockchain claims hub that cut investigation cycle times by 35%. Predictive models now mine the immutable store to uncover suspicious patterns within hours, pivoting anti-fraud tactics from retroactive policing to proactive interdiction. For multicarrier ecosystems, a single source of truth also removes the need for reconciliations, further curbing loss-adjustment expenses.

Smart-contract automation lowers administrative costs

Back-office functions consume up to 40% of an insurer’s expense base, yet smart contracts can settle routine claims in minutes rather than weeks. Sompo Japan’s train-delay micro-policy pushes payouts instantly once the rail operator’s API confirms a service disruption.[1]Finextra, “Sompo Japan Automates Train Delay Payouts,” finextra.com Across pilots, implementation budgets range from USD 50,000 to USD 2 million, with average payback within 18 months thanks to labor savings. Rigorous code audits are essential because decentralized hacks siphoned USD 2.2 billion from DeFi protocols in 2024. Standardized security frameworks and regulator-approved templates are emerging to balance speed with consumer protection.

Regulatory mandates for real-time reporting and transparency

Solvency II updates, Japan’s economic value-based solvency tests, and IFRS 17 disclosures all push firms to deliver granular, near-instant risk data. A distributed ledger can feed supervisors with tamper-proof positions, cutting the reconciliation burden that traditional quarterly filings impose. The EU’s Markets in Crypto-Assets rulebook likewise rewards blockchain-native insurance products that embed compliance logic directly into contract code. In China, regulators permit permissioned ledgers so long as nodes stay within sovereign cloud centres, blending innovation with policy control. Carriers able to prove real-time solvency earn lower capital add-ons, turning compliance investment into a capital-efficiency play.

Parametric micro-insurance for climate and crop risks in emerging markets

The global climate protection gap eclipses USD 1.8 trillion, yet parametric covers can disburse funds within 72 hours of a trigger without loss adjustors.[2]Generali Group, “Parametric Insurance and Climate Resilience,” generali.com India uses satellite rainfall data on a blockchain oracle to send automatic payouts to smallholder farmers the moment thresholds are breached. The parametric sector was valued at USD 14.8 billion in 2024 and is growing 11.5% annually through 2032. Transparent code-based triggers foster trust, raising take-up where legacy products failed. For carriers, automated settlement slashes overhead, creating viable margins in markets once deemed too costly to serve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Blockchain scalability and interoperability limitations | -6.8% | Global, particularly affecting enterprise implementations | Short term (≤2 years) |

| Data-privacy regulations are complicating immutable ledgers | -5.2% | Europe and North America (GDPR markets) | Medium term (2-4 years) |

| Scarcity of actuarial talent with Web3 skillsets | -4.1% | Global, concentrated in developed markets | Long term (≥4 years) |

| Growing cyberattacks on smart-contract codebases | -3.9% | Global, affecting all blockchain implementations | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Blockchain scalability and interoperability limitations

Mainnet Ethereum processes 15 TPS while major card networks handle thousands, forcing insurers to wrestle with throughput ceilings. Layer-2 channels and sharding raise capacity yet add architectural complexity that boosts audit costs. In 2024, the Ethereum Enterprise Alliance published cross-chain specs, though adoption is still uneven. Vendors try to ease lock-in by offering API bridges, but few mission-critical insurance deployments trust immature cross-chain routing today. Until shared standards gain traction, large programmes opt for closed, high-performance ledgers, limiting ecosystem knits and slowing network effects.

Data-privacy regulations are complicating immutable ledgers

GDPR’s right-to-erasure clashes with the permanence of on-chain entries. Many European insurers resort to hybrid models that hash personal data on-chain while storing raw files off-chain, diluting blockchain’s single-source purity. Zero-knowledge proofs promise compliance without disclosure, but energy costs and integration hurdles inhibit high-volume use. With 75% of the world under modern privacy laws by 2024, multinationals juggle divergent rules that erode scale benefits. Harmonised supervisory guidance would accelerate rollouts, yet near-term projects must navigate a complex regulatory maze.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Infrastructure Accelerates Enterprise Adoption

Cloud-hosted ledgers controlled 64.20% of the blockchain in the insurance market in 2025 and are projected to log a 40.80% CAGR through 2031, a pace that underscores carriers’ preference for outsourcing node maintenance and uptime assurance. In monetary terms, the cloud slice of the blockchain in the insurance market size is expected to climb from USD 0.60 billion in 2025 to more than USD 4.4 billion by the end of the decade, reflecting rapid scale gains without large capital outlays. Subscription models allow firms to align costs with transaction volumes, while pre-configured governance modules shorten build cycles from months to weeks.

On-premise deployments keep a foothold among reinsurers that juggle cross-border treaty data under local-host strictures. Implementation budgets here can top USD 2 million, but the trade-off buys total hardware control and tailored security postures that some risk committees demand. Hybrid blueprints now splice on-prem custody of sensitive claims images with cloud analytics for fraud scoring, blending compliance assurance with elastic compute. This architectural flexibility ensures the blockchain in the insurance market can serve both multinational groups navigating patchwork rules and smaller carriers aiming for quick wins.

By Blockchain Type: Private Networks Balance Security with Innovation

Private ledgers held 61.10% of the blockchain in the insurance market in 2025 as C-suites prioritised permissioned access that meets prudential audit norms. That dominance translates into USD 0.57 billion of the blockchain in insurance market size in 2025, and growth continues at 34.60% annually as insurers wrap existing policy systems with private APIs rather than expose data to public miners. Consortium frameworks grow faster still, expanding 41.20% a year as carriers co-fund shared utilities like policy verification hubs.

RiskStream Collaborative exemplifies the model, letting members cut development spend by 40% while retaining product differentiation. Public chains remain niche because supervisors worry about data jurisdiction and throughput, yet zero-knowledge rollups hint at future convergence by permitting private computation on shared settlement layers. Over the forecast horizon, hybrid constructs that record proofs to a public chain while storing sensitive fields in an enclave may capture outsized interest, giving carriers a “best of both worlds” path to openness and control.

By Application: Smart Contracts Drive Parametric Insurance Innovation

Smart-contract and parametric modules already claim 27.60% of total revenue and will accelerate at 41.05% CAGR, fuelled by instant settlement temptations for catastrophe, travel, and crop covers. In value terms, this cohort adds nearly USD 1.7 billion to the blockchain in insurance market size between 2026 and 2031 as carriers package weather, seismic, or IoT telemetry into low-touch triggers. Governance, risk, and compliance suites follow closely, especially among global groups responding to Solvency II and IFRS 17 data calls.

Identity management tools supporting KYC and claims fraud screening round out the demand stack, leveraging distributed identifiers to let underwriters pull verified profiles in seconds. Reinsurance placements also inch forward, with tokenised layers attracting capital market investors who appreciate transparent exposure maps. Each use case reinforces the narrative that blockchain in the insurance market momentum now stems from operational payoffs and new-product revenue rather than tech novelty.

By Enterprise Size: SMEs Accelerate Adoption Through Platform Solutions

Large carriers still dominate expenditure, accounting for 67.10% of blockchain in insurance market share in 2025, but SMEs clock the swiftest trajectory at 40.95% CAGR. Pay-per-use models trimmed entry costs below USD 50,000, letting regional MGAs pilot fraud-detection ledgers without commandeering the IT roadmap. Research indicates that SMEs integrating blockchain gain faster credit access as lenders trust immutable cash-flow auditable records.

For scale incumbents, multi-year transformation budgets unlock deeper integrations across underwriting, claims, and actuarial reserving. Vendor ecosystems tailor industry micro-services quotation, policy issuance, and claims FNOL so midsize firms can launch a minimum viable ledger in under 120 days. As adoption widens, network effects emerge, making it easier for small brokers to query coverage status from primary blocks, completing an inclusion loop that further expands overall demand.

Geography Analysis

North America captured 44.30% of global revenue in 2025, equal to nearly USD 0.41 billion of the blockchain in insurance market size, underpinned by clear supervisory sandboxes and plentiful venture capital. The National Association of Insurance Commissioners actively studies distributed ledgers, giving carriers confidence to scale proofs into live production. Canada’s principles-based crypto rules complement the United States' initiatives, while Mexico’s cross-border trade agreements incentivise regional policy verification platforms. Mature personal-lines books offer test beds where carriers like Nationwide trial real-time proof-of-insurance certificates.

Asia Pacific is the growth pacesetter at 41.35% CAGR and could exceed North American spending by 2030. China’s National Financial Regulatory Administration endorses permissioned chains anchored in sovereign cloud clusters, and scores of mainland insurers are piloting blockchain claims orchestration. Japan’s Financial Services Agency plans economic value-based solvency metrics for 2026 that favour real-time ledger feeds, amplifying incentives for domestic carriers. India spearheads parametric flood and crop pilots using weather-oracle smart contracts that slash rural payout times from weeks to days.

Europe weighs privacy risks against transparency value. Only 15% of undertakings reported active blockchain use to EIOPA in 2024, yet firms experiment with zero-knowledge proof overlay networks to satisfy GDPR while keeping audit trails visible. The region’s climate agenda sparks the development of on-chain ESG assurance products, positioning European vendors to export compliance-by-design blueprints to other jurisdictions. Once supervisory guidance harmonises, analysts see a step-change in EU volumes that will expand the blockchain in the insurance market well beyond today’s cautious proofs.

Competitive Landscape

Industry structure remains moderately fragmented as incumbent insurers weigh buy-versus-build choices. Most choose to co-develop through consortia such as RiskStream, where 30+ carriers pool resources for mortality, proof-of-insurance, and subrogation modules. Technology majors IBM, Microsoft, and Amazon Web Services monetise platform and SI capabilities, capturing spend from carriers that prefer managed nodes over self-hosted stacks. Specialist houses like ConsenSys, R3, and Etherisc focus solely on policy, claims, or parametric contract tooling.

Tokenisation of insurance assets forms a new competitive arena. Infineo issued USD 100 million in tokenised life policies on Provenance Blockchain, giving investors tradable exposure to an illiquid class.[3]Provenance Blockchain, “Tokenised Life Policies Launch,” provenance.io Schroders Capital ran a pilot for tokenised ILS notes that promises to compress settlement from weeks to days. Start-ups such as Lemonade blend blockchain, AI, and behavioural incentives to return unused premiums to policyholders’ chosen charities, creating brand differentiation on transparency.

Security service vendors rise in tandem because USD 2.2 billion vanished from DeFi exploits in 2024 alone. Certified code-audit providers and cyber-insurance wrappers now accompany almost every production launch. As the blockchain in the insurance market matures, players that marry rigorous security with regulatory fluency and measurable cost take-outs will consolidate share, although near-term diversity of experiments keeps rivalry vibrant.

Blockchain Insurance Industry Leaders

Microsoft Corporation

IBM Corporation

Amazon Web Services, Inc.

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Blockchain Deposit Insurance Corp. formed a global crypto-asset insurance unit in Bermuda, focusing on digital-wallet coverage.

- January 2025: Qantev partnered with InsureMO to fuse AI analytics with blockchain plumbing, enhancing multi-line claims straight-through processing.

- January 2025: Nayms structured a tokenised reinsurance facility on Base layer-2 Ethereum to cover Florida wind losses.

- October 2024: Generali and UNDP released a joint paper on parametric micro-covers to bridge the USD 1.8 trillion protection gap, spotlighting blockchain triggers.

Global Blockchain Insurance Market Report Scope

Blockchain technology is a robust database mechanism that enables the transparent sharing of information within a corporate network. We can build an unalterable database for monitoring payments, orders, accounts, and other transactions using blockchain technology. The system includes mechanisms for preventing unauthorized transaction entry and ensuring consistency in the shared view of these transactions.

Within insurance, the claims and finance functions are high-value areas where blockchain could be beneficial, especially when you look at processes that need ongoing reconciliation with external parties. Insurers and customers waste a lot of time verifying their documents and identities. This can be reduced with a blockchain platform that can talk to other blockchain platforms to verify the identity of the user. The market includes various standalone services in the insurance sector, such as smart contracts, identity management, and fraud detection, death and claims management, and governance, risk, and compliance management.

The blockchain market in the insurance industry is segmented by deployment (on-premise, cloud-based), type (public, private), application (GRC management, smart contracts, financial management, identity management & fraud detection, death and claims management, and other applications), geography (North America (United States, Canada), Europe (United Kingdom, Germany, France, and Rest of Europe), Asia Pacific (China, Japan, Singapore, Australia, and Rest of Asia Pacific), and rest of the world.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| On-Premise |

| Cloud-Based |

| Public |

| Private |

| Consortium/Hybrid |

| Governance, Risk and Compliance (GRC) |

| Smart Contract and Parametric Insurance |

| Payments and Financial Management |

| Identity Management and Fraud Detection |

| Claims and Death Management |

| Reinsurance and P2P Insurance |

| Customer On-Boarding and KYC |

| Other Applications |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Turkey |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Deployment | On-Premise | ||

| Cloud-Based | |||

| By Blockchain Type | Public | ||

| Private | |||

| Consortium/Hybrid | |||

| By Application | Governance, Risk and Compliance (GRC) | ||

| Smart Contract and Parametric Insurance | |||

| Payments and Financial Management | |||

| Identity Management and Fraud Detection | |||

| Claims and Death Management | |||

| Reinsurance and P2P Insurance | |||

| Customer On-Boarding and KYC | |||

| Other Applications | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Singapore | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Turkey | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected size of the blockchain in the insurance market by 2031?

The blockchain in the insurance market size is forecast to reach USD 6.96 billion by 2031, growing at a 39.85% CAGR.

Which deployment model currently leads the market?

Cloud-based deployments dominated with a 64.20% share in 2025, reflecting carriers’ preference for rapid, capital-light rollouts.

Why are smart contracts important for insurers?

Smart contracts cut manual processing costs and can settle parametric claims in minutes, with pilots showing payback periods inside 18 months.

Which region is expected to grow fastest?

Asia Pacific is projected to expand at a 41.35% CAGR through 2031 as regulators and governments sponsor blockchain pilots in crop, health, and catastrophe insurance.

What are the main barriers to wider adoption?

Key restraints include network scalability limits, cross-chain interoperability gaps, and the tension between immutable ledgers and data-privacy laws such as GDPR.

How are insurers addressing blockchain security risks?

Companies increasingly mandate third-party code audits and cyber-insurance add-ons after DeFi exploits caused USD 2.2 billion in losses during 2024.

Page last updated on: