Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 145.29 Billion |

| Market Size (2031) | USD 197.28 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Textile Market Analysis by Mordor Intelligence

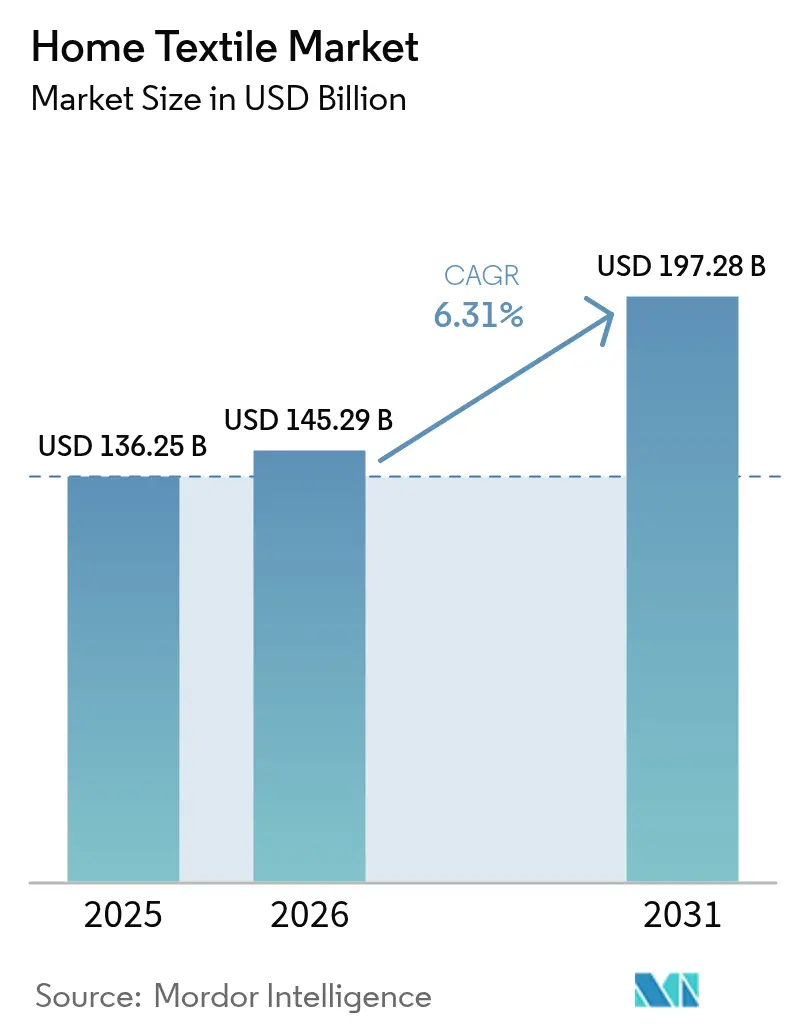

The global home textile market size stood at USD 145.29 billion in 2026, up from USD 136.25 billion in 2025, and is projected to reach USD 197.28 billion by 2031 at a 6.31% CAGR. Growth is supported by the steady shift to performance bedding that manages moisture, temperature, and allergens, as well as by rising consumer interest in natural and specialty fibers that carry credible sustainability credentials. Direct-to-consumer brands continue to redesign traditional supply chains through vertical integration, nearshoring, and selective retail presence to improve speed and control of merchandising. Asia-Pacific dominated in 2025 and leads regional expansion, helped by middle-class growth, investment in large-scale textile parks, and expanding omnichannel retail networks that improve accessibility in Tier 2 and Tier 3 cities. Regulatory signals in the European Union around extended producer responsibility and digital product passports are driving earlier adoption of traceability software and eco-design, prompting manufacturers to balance compliance with premium product positioning.

Key Report Takeaways

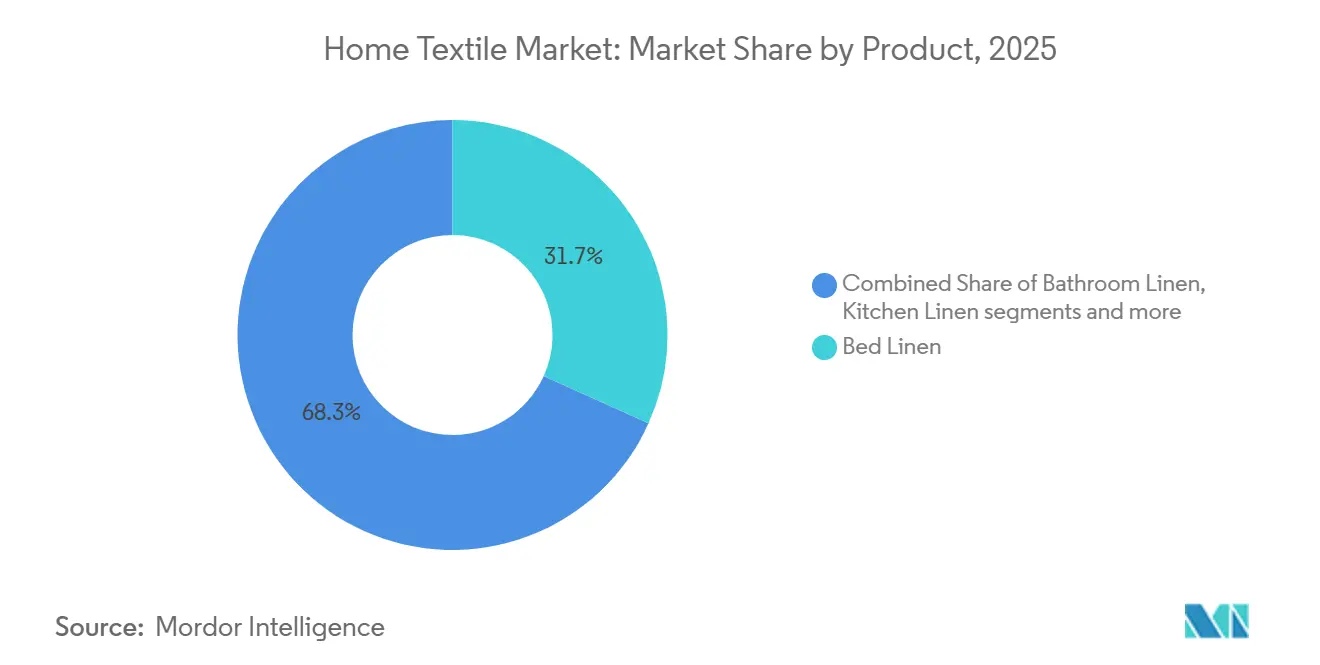

- By product, bed linen led with 31.74% revenue share in 2025, and bathroom linen is forecast to expand at a 7.92% CAGR to 2031.

- By material, cotton held a 57.12% share in 2025, while linen is projected to grow at a 7.42% CAGR through 2031.

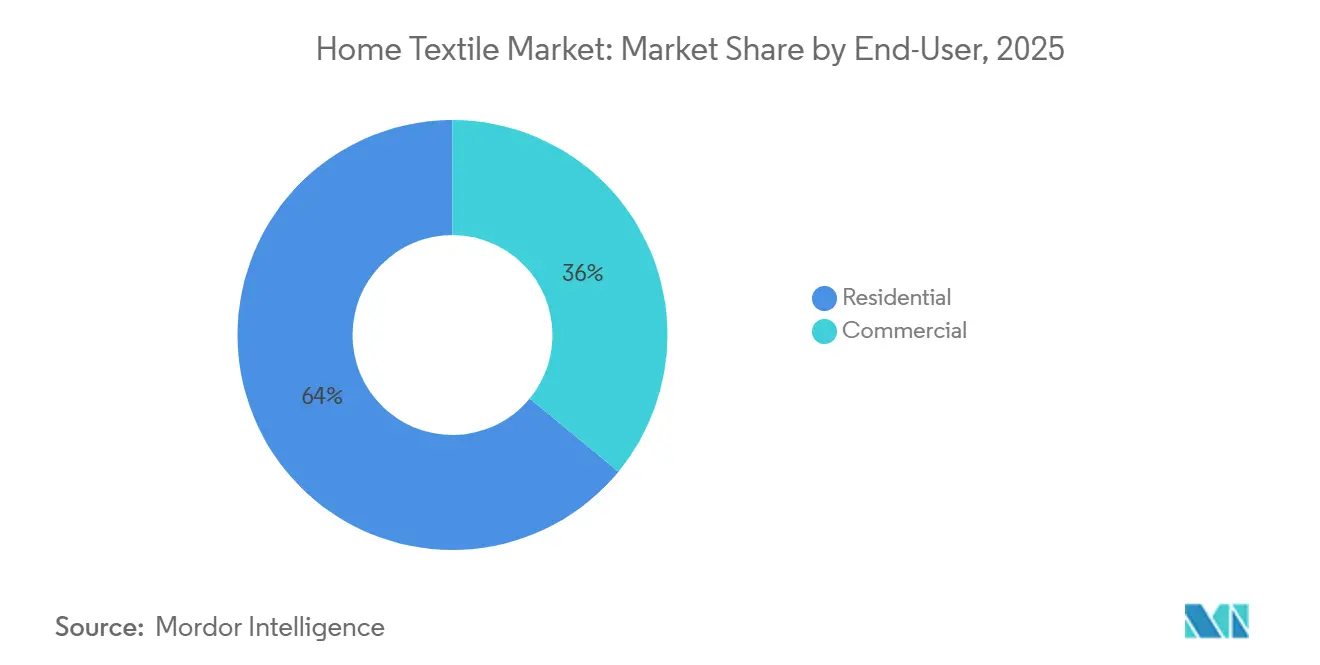

- By end-user, residential accounted for 64.03% of the volume in 2025 and is forecast to grow at a 6.12% CAGR through 2031.

- By distribution channel, specialty stores held a 43.88% share in 2025, and online channels are projected to grow at an 8.45% CAGR through 2031.

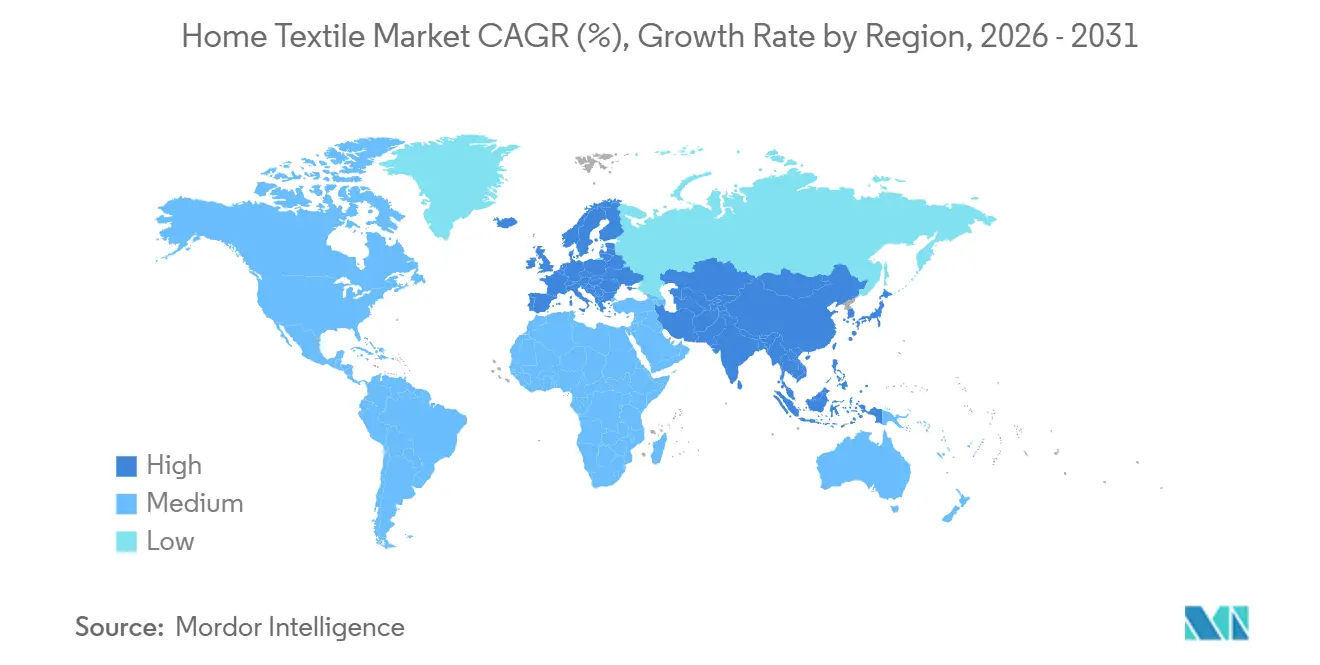

- By geography, Asia-Pacific commanded a 45.08% share in 2025 and is expected to expand at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sleep-wellness and performance bedding adoption (cooling, hypoallergenic, antimicrobial) | +0.8% | Global, concentrated in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Premiumization via natural fibers and specialty blends (linen, bamboo, lyocell) | +0.9% | Global, Europe for linen, North America, and Asia-Pacific for lyocell and bamboo | Medium term (2-4 years) |

| Expansion of organized retail and specialty chains in emerging markets | +0.7% | Asia-Pacific core with spill-over to the Middle East and Africa | Medium term (2-4 years) |

| Asia-Pacific middle-class expansion lifting per-capita spend on home textiles | +1.2% | Asia-Pacific markets, including India and China | Long term (≥ 4 years) |

| Bio-based and man-made cellulosic fibers scaling in home textiles | +0.6% | Global, with capacity growth in China, India, and Vietnam | Long term (≥ 4 years) |

| Textile circularity policies (EPR/DPP) steering product design and traceability | +0.5% | Europe first, then gradual global diffusion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sleep-Wellness and Performance Bedding Adoption (Cooling, Hypoallergenic, Antimicrobial)

Consumer demand for cooling, antimicrobial, and hypoallergenic bedding continues to rise as buyers connect sleep quality with health and daily performance. Brands have embedded phase-change and moisture-wicking technologies into sheets and protectors to reduce thermal discomfort during sleep, which supports premium price points in performance lines[1]National Sleep Foundation, “Bedding and Sleep Quality Evidence,” Sleep Foundation, sleepfoundation.org. Product roadmaps are expanding through partnerships and technology transfers from sports performance and health monitoring to home textiles, and teams are testing thermal modulation solutions in high-performance environments. Antimicrobial finishing based on silver-ion chemistries continues to address sensitivity and hygiene concerns in multi-occupancy or pet-friendly households, which improves adoption in North America and urban Asia-Pacific. Companies are pairing material innovation with channel expansion through direct websites and owned stores, which shortens feedback loops for product iteration and replenishment. The net effect is a steady shift toward performance bedding in the home textile market across the mid-price and premium tiers, improving category resilience across economic cycles.

Premiumization Via Natural Fibers and Specialty Blends (Linen, Bamboo, Lyocell)

Linen, lyocell, and bamboo-based lyocell are gaining traction due to tactility, breathability, and credible sustainability narratives that resonate with European and North American consumers. Branded fiber programs such as TENCEL help translate closed-loop solvent recovery and lower resource use into recognizable product claims for bedding and filled goods. Specialty blends are expanding use cases into cooling and moisture management, which supports a premium tier across sheeting and duvet inserts within the home textile market. Early adopters of traceable bamboo lyocell demonstrate strong repeat-purchase intent and a willingness to pay for verified environmental benefits, which supports brand-led pricing strategies. Capacity plans from leading cellulosic suppliers through 2025 are aligning with rising demand from bedding brands for fiber-differentiated products that offer comfort and sustainability. The result is a gradual, sustained premiumization trend that lifts average selling prices in the home textile market, where traceability and third-party certifications are visible at the point of sale.

Bio-Based and Man-Made Cellulosic Fibers Scaling in Home Textiles

Global output of regenerated cellulosics increased in 2024 as bedding and upholstery brands sought renewable feedstocks with lower environmental footprints, supported by large suppliers’ investments in efficient, closed-loop systems that recover solvents and reduce emissions[2]Lenzing AG, “TENCEL Technology and 2024 Sustainability Update,” Lenzing, lenzing.com. Product extensions into fill and upholstery applications broadened material choice across comforters, pillows, and furniture textiles, which helps diversify the home textile market’s reliance on cotton and generic polyesters. Supplier expansion programs targeted capacity growth by mid-decade, aligning with downstream adoption of natural-origin fibers in North America and Europe. Policy programs in India and trade frameworks in Vietnam are shaping new capacity decisions in bamboo-based value chains, adding geographic resilience to cellulosic sourcing strategies across Asia-Pacific. Downstream brands are experimenting with recycled inputs in mattress and top-of-bed fabrics to address waste-reduction goals, adding a sustainability dimension to product design in the home textile market. These developments, together, support a long-term shift in the material mix toward cellulosics and recycled inputs, providing product differentiation along performance and environmental metrics.

Textile Circularity Policies (EPR/DPP) Steering Product Design and Traceability

The European Union’s amended Waste Framework Directive entered into force in October 2025 and requires member states to implement extended producer responsibility schemes for textiles by April 2028, which is accelerating planning for eco-design and take-back across brands that sell in the region[3]European Commission, “Digital Product Passport and EPR Guidance,” European Commission, europa.eu. The European Commission’s digital product passport initiative is expected to publish delegated acts in 2027, with phased rollouts starting mid-2028, requiring item-level data on fiber content, origin, and end-of-life options that consumers and recyclers can access. Early movers are aligning supply chain systems and product labeling to prepare for DPP and EPR, embedding traceability into design and packaging, and integrating water and energy stewardship into operations. Manufacturers are investing in renewable power and circular production technologies to reduce operational emissions and align with large buyers’ procurement criteria, which creates a performance and compliance moat in the home textile market. Compliance preparation is shifting cost structures and timelines for smaller brands, prompting them to partner with solution providers to manage data capture and reporting across multi-brand portfolios. Over the long term, transparency and circularity are expected to be embedded across assortments in Europe first and then spread to other regions through retailer policies and trade agreements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trade barriers and tariff volatility on textile imports | -0.9% | Global, with acute exposure in United States corridors | Short term (≤ 2 years) |

| Substitution by hard-surface flooring reduces the demand for rugs and carpets demand | -0.4% | North America and Europe | Long term (≥ 4 years) |

| Recyclability and fiber-blend complexity are raising redesign and compliance burden | -0.3% | Europe first, then broader markets | Long term (≥ 4 years) |

| Digital Product Passport and due diligence compliance costs for SMEs | -0.2% | Europe first with potential expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Trade Barriers and Tariff Volatility on Textile Imports

Cost inflation from tariff changes has pressured margins for export-oriented suppliers selling into the United States, prompting several producers to pass on incremental costs to customers or adjust assortments to lower average selling prices in the short term. Companies are diversifying production footprints and revenue exposure, aiming to reduce over-reliance on a single market while expanding into Europe, the Middle East, and India to offset volatility. Multi-country manufacturing networks provide flexibility to route orders and navigate changing duty regimes, helping stabilize delivery timelines and service levels in the home textile market. Suppliers are also building North American manufacturing capacity to support utility bedding and related categories, which improves speed to shelf for replenishment programs. Trade agreements under negotiation or recently concluded are expected to support long-horizon export strategies from India to key partners in Europe and the United Kingdom, improving the regional mix for leading suppliers. These moves, taken together, mitigate near-term volatility from tariffs and improve strategic flexibility for companies serving both branded and private-label channels.

Digital Product Passport and Due-Diligence Compliance Costs for SMEs

Digital product passport requirements, starting in Europe, will add data-collection and labeling steps for each product, increasing complexity for companies with broad SKU ranges and multi-brand portfolios. Small and medium-sized enterprises face a higher relative administrative load from EPR and DPP compliance, which can strain cash flows and require upgrades to information systems and supplier onboarding workflows. Exporters that sell into Europe are incorporating traceability and zero-liquid-discharge projects into their capital plans to align with incoming regulations and customer expectations for sustainability. Multi-brand portfolios require brand-specific implementations and data governance, which increases software costs and vendor management overhead relative to single-brand peers. In the near term, compliance programs are expected to phase in by product category and geography, which gives brands time to test and refine digital labeling and reporting solutions. Over the long term, compliance will be a baseline capability in the home textile market, and companies that practice early adoption will be positioned to capture retailer preference and consumer trust.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bath Linen Surges on Hospitality Refurbishments

Bed linen accounted for 31.74% of 2025 revenue, while bathroom linen is forecast to be the fastest-growing application at a 7.92% CAGR to 2031, reflecting sustained replacement cycles and hospitality-led upgrades to antimicrobial terry. Within the home textile market, bath towel and bathrobe programs benefit from product differentiation in quick-dry performance and hygiene features, which support premium assortments in hotel and wellness channels. Manufacturers are aligning capacity and automation to serve institutional buyers with consistent quality and reliable lead times, which helps capture contract wins and repeat orders. A new towel manufacturing facility with robotics and AI-enabled quality control is being leveraged to support expansion into Asia-Pacific, Africa, Australia, and the Middle East, indicating sustained demand for hospitality-focused bath programs. Product portfolios are increasingly organized around wellness and sustainability themes, which align with hotel procurement criteria and specialty retail positioning.

Carpet and area rug demand remains structurally sensitive to shifts in flooring preferences in mature markets, which encourages category leaders to emphasize outdoor, machine-washable, and commercial hospitality ranges that carry faster replacement cycles within the home textile market. Investments in energy and process efficiency are contributing to operating resilience, while collections and formats that meet maintenance and durability expectations are gaining share in commercial spaces. The bath linen uptrend is further reinforced by crossovers from spa and wellness settings to residential bathrooms, where antimicrobial and quick-dry features support a value proposition beyond softness alone. As hospitality refurbishment cycles continue in the Middle East and parts of Asia-Pacific, suppliers with ESG-aligned operations and premium terry innovations are well positioned to capture growth. Together, these application shifts favor bath and utility collections with performance finishes and clear sustainability credentials that align with buyer specifications across regions.

By Material: Linen Premiums Outpace Cotton Volume

Cotton accounted for 57.12% of 2025 revenue, underscoring its scale and familiarity, while linen is projected to grow at a 7.42% CAGR as design- and certification-led differentiation helps it capture premium share in the home textile market. Branded cellulosic fibers are expanding into fill and upholstery applications, offering performance and sustainability attributes that help brands broaden their material mix beyond conventional cotton and synthetics. The product relaunch, which emphasizes European flax credentials and artisanal finishing, continues to gain traction with premium consumers in North America and Europe. Traceable bamboo lyocell programs are securing strong repeat purchase rates where sustainability and comfort claims are validated and communicated effectively. Patent-backed yarn and finish innovations are helping bath textiles deliver higher absorption and faster drying, which further strengthens brand narratives in premium segments.

Cotton sourcing strategies are adjusting to cost differentials and tariff exposure, which is leading some integrated players to balance United States and Indian cotton inputs while preparing for expansion into adjacent product verticals. Investments in recycled content for mattress and top-of-bed fabrics continue as brands pursue waste-diversion targets and communicate cooling performance through recognizable recycled fiber brands in the home textile market. Linen and lyocell capacity expansions by leading suppliers are aligning with the rising demand for breathable, durable, and verified sustainable products in bedding and upholstery. Packaging and process changes, including alternative fiber-based materials and greater automation, further reduce waste and shorten lead times, thereby improving cost-to-serve and product consistency[4]Trident Limited, “Integrated Annual Report 2024-25,” Trident Limited, tridentindia.com. These material shifts underpin premiumization while maintaining an accessible base in cotton-led assortments that meet value and durability expectations.

By End-User: Residential Dominates, Commercial Accelerates

Residential end-users held 64.03% of the 2025 volume and are forecast at a 6.12% CAGR through 2031, supported by home renovation cycles in North America and rising discretionary spending in Asia-Pacific’s urban centers within the home textile market. Domestic expansion strategies in India are adding retail counters to premium chains for branded bed and bath collections, which raises visibility among higher-income households. Specialty retail is adding curated experiences, personalized consultation, and brand storytelling to reinforce product attributes and sustain higher average transaction values. Digitally native brands are complementing online storefronts with owned retail that highlights tactile qualities and helps consumers make confident material choices. This mix of digital and store-based presence improves assortment control and replenishment cadence across peak demand periods in the home textile market.

Commercial end-users are accelerating, led by hospitality and healthcare projects that prioritize antimicrobial, quick-dry, and fluid-barrier features in bath and bedding textiles. Companies with upholstery and bath capacity are reporting higher momentum in contract channels than in tariff-impacted United States retail bedding, signaling favorable demand in projects and property refresh cycles. ESG alignment through high water recycling and renewable energy use is strengthening supplier positioning with global hospitality groups that impose sustainability criteria on procurement. Institutional healthcare demand for antimicrobial and performance fabrics is growing in the Asia-Pacific region, which supports higher-margin programs across clinics and specialty care facilities. Over the next several years, residential volumes are expected to remain the anchor while commercial programs deliver mix uplift through performance-driven specifications within the home textile market.

By Distribution Channel: Online Disrupts Specialty Stronghold

Specialty stores accounted for 43.88% of 2025 sales, backed by experiential merchandising and advisory services, while online channels are set to grow at 8.45% CAGR to 2031 as consumers prioritize convenience, price transparency, and direct brand relationships in the home textile market. Brands are leaning into licensed and owned labels across e-commerce to diversify revenue and target value-added segments, which expands reach beyond traditional wholesale programs. Digitally native models have built scale by focusing on a small number of hero products, transparent pricing, and responsive product refresh cycles that reflect real-time feedback. Select brands are adding physical stores to improve tactile evaluation and build local communities through events and design partnerships that reinforce quality and sustainability claims. Product expansion and capacity investments by North American manufacturers of pillows and protectors provide supply-side support for private-label and brand programs across retail partners.

E-commerce capabilities are now core to replenishment bedding and utility categories, where fast fulfillment and easy returns support repeat purchases in the home textile market. Digital channels also improve assortment testing and micro-segmentation, allowing brands to tailor colorways, materials, and bundles to regional preferences without heavy in-store inventory commitments. Specialty stores continue to drive premium conversion in linen and lyocell through tactile trials and consultation, while digital marketplaces support entry-level price points and promotions for cotton-led assortments. European expansion strategies by leading manufacturers are adding senior commercial leadership and trade show presence to grow specialty-store partnerships. As omnichannel models mature, share is likely to continue shifting online while physical locations support higher engagement and premium positioning within the home textile market.

Geography Analysis

Asia-Pacific is the current demand and production anchor, accounting for 45.08% of the global base in 2025 and on track for an 8.12% CAGR through 2031 in the home textile market. Demand is supported by rising urban incomes, maturing retail formats, and government-backed park infrastructure that aggregates spinning, weaving, processing, and logistics on single campuses. India is deepening its positioning through seven PM-MITRA parks and an increased textiles budget, both of which support end-to-end investment and job creation linked to export growth. The export outlook is also tied to progress on EU and UK trade arrangements that reduce tariff disadvantages for categories such as bed linen, bath linen, drapery, and upholstery. Regional e-commerce expansion and broader specialty retail coverage continue to expand access in Tier 2 and Tier 3 cities, raising category penetration for bed and bath programs in the home textile market.

Europe’s trajectory is anchored in premiumization and regulatory readiness, with a 5.80% CAGR outlook that reflects consumer demand for European flax, organic cotton, and verifiable supply chains. The EU Waste Framework Directive, which entered into force in October 2025, sets a clear timeline for extended producer responsibility by April 2028, prompting brands and suppliers to invest in design-for-circularity and collection systems. Digital product passports are expected to phase in from mid-2028, following delegated acts in 2027 that will prioritize data governance, item-level labels, and cross-border interoperability for the home textile market. Major suppliers are moving early through sustainability-themed collections, enhanced European leadership, and participation in leading trade events to expand specialty-store partnerships. These moves support price realization and long-term buyer preference in Europe’s premium channels.

North America’s 4.70% growth profile reflects tariff-related volatility, retailer inventory caution, and category-level shifts favoring utility bedding and performance bath programs in the home textile market. To mitigate import exposure and serve replenishment-heavy ranges, suppliers are commissioning United States facilities for pillows, protectors, and related SKUs that require fast cycle times. This coexists with continued investment in automation and digital operations by long-standing manufacturers that serve both private-label and brand portfolios. The Middle East and South America maintain steady momentum driven by hospitality and urbanization, while Africa and Oceania advance more slowly due to infrastructure constraints. Across regions, compliance, traceability, and premium materials continue to define competitive differentiation in the home textile market.

Competitive Landscape

Competitive Landscape

The home textile market is fragmented, enabling specialized brands and manufacturers to grow by focusing on performance differentiation, premium materials, and traceability that strengthen category positioning. Direct-to-consumer players have scaled on the back of focused hero product strategies, transparent pricing, and online-first launches that later extend to owned retail for tactile experiences. Specialty brands that expanded store counts in 2025 saw strong retail performance, supported by curated assortments and high-touch service that reinforce quality claims. On the manufacturing side, vertical integration, automation, and reduced lead times are clear priorities among leaders seeking to protect margins and improve service levels. European expansion with dedicated leadership and trade show showcases is part of a broader strategy to capture specialty retail demand in premium markets.

Export-exposed suppliers are rebalancing geographic mix and product focus to mitigate tariff risks while building resilience within the home textile market. Strategic acquisitions and brand licensing in the United States have expanded the portfolio into utility bedding and enhanced distribution, supported by the commissioning of domestic facilities in multiple states. Operating model transformations that consolidate divisions and streamline facilities are driving multi-million-dollar savings to improve competitiveness and service. Investments by North American bedding manufacturers in robotics and AI-enabled systems in 2024 and 2025 are enhancing efficiency and quality while also adding capacity to meet higher demand from retailer partners. Sustainability commitments, including high water recycling and renewable energy adoption, are emerging as competitive moats in procurement-driven categories.

The competitive playbook centers on three reinforcing themes. First, product differentiation through performance technologies, breathable premium fibers, and credible eco-labels strengthens brand trust and price realization in the home textile market. Second, supply chain control through vertical integration, nearshoring, and automation reduces lead times and serves replenishment needs for utility categories. Third, compliance readiness for EU EPR and DPP creates barriers to entry and rewards early adopters who can demonstrate traceability at scale. Companies that execute across these fronts are positioned to gain share without relying on heavy discounting, supported by omnichannel strategies that balance online efficiency with store-based engagement.

Home Textile Industry Leaders

Welspun Living Ltd.

Mohawk Industries, Inc. (Rugs & Textiles)

Springs Global S.A.

Trident Group

Luolai Lifestyle Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Trident Limited accelerated European home textiles expansion with strategic investments and showcased its "TG collection" at Heimtextil 2026 in Frankfurt, focusing on contemporary design, sustainability, and innovation for European markets. The company appointed dedicated Directors for Germany and France to enhance customer engagement as proposed India-United Kingdom and India-EU Free Trade Agreements improve trade prospects.

- November 2025: Boll & Branch expanded its retail footprint to 15 stores nationwide with new openings in Charlotte, North Carolina, and Bethesda, Maryland, nearly doubling its retail portfolio within one year. Retail stores posted strong performance, with revenue up nearly 60% year over year, and plans for continued expansion in 2026.

- July 2025: Indo Count Industries launched the legacy United States brand "Wamsutta" direct-to-consumer, following acquisition in FY 2024-25, and flagged a USD 100 million revenue potential over three years through owned and licensed brands.

- April 2025: Ralph Lauren presented its Home Collection and debuted the Fall 2025 Canyon Road Collection at Milan Design Week, featuring natural materials and a collaboration with Diné textile artists Naiomi and Tyler Glasses.

Global Home Textile Market Report Scope

Home textiles refer to fabrics and garments specifically intended for enhancing the décor of a residential environment. The report provides a comprehensive analysis of the home textile market, encompassing an evaluation of economic factors and sectoral contributions, an overview of the market landscape, an estimation of market size for critical segments, an identification of emerging trends within market segments, an exploration of market dynamics, and examination of logistics expenditures by end-user industries.

The market is segmented by product, by distribution channel, and by geography. The market is further segmented by product into bed linen and bedspread, bathroom linen, kitchen linen, upholstery, curtains, and floor coverings. The market is further segmented by distribution channel into supermarkets/hypermarkets, specialty stores, online, and other distribution channels. And by geography, North America, Latin America, Europe, Asia-Pacific, and Middle East & Africa. The report offers market sizing and forecasts for home textiles in value (USD) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Others (Carpets & Area Rugs) |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Other Offline Channels | |

| Online |

By Region

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Others (Carpets & Area Rugs) | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Other Offline Channels | ||

| Online | ||

| By Region | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the home textile market?

The home textile market size was USD 136.25 billion in 2025 and is projected to reach USD 197.28 billion by 2031 at a 6.31% CAGR over 2026 to 2031.

Which region leads to demand in the home textile market, and how fast is it growing?

Asia-Pacific held 45.08% of 2025 revenue and is forecast to expand at an 8.12% CAGR through 2031, outpacing all other regions.

Which applications are driving incremental growth in the home textile market?

Bed linen led revenue in 2025, while bathroom linen is the fastest-growing application, with a 7.92% CAGR, driven by hospitality refurbishments and antimicrobial innovation.

How are regulations in Europe affecting the home textile market?

The EU’s Waste Framework Directive requires EPR by April 2028, and digital product passports are expected to phase in from mid-2028, accelerating investment in traceability and eco-design.

What strategies are suppliers using to navigate tariff volatility?

Companies are adding United States capacity for utility bedding, diversifying footprints across regions, and rebalancing revenue exposure to reduce single-market risk.

Which materials are gaining traction in premium segments?

Linen and artificial cellulosic fibers, such as TENCEL-based lyocell, are advancing in performance and sustainability, supporting premium positioning.

Page last updated on: