Canada Food Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

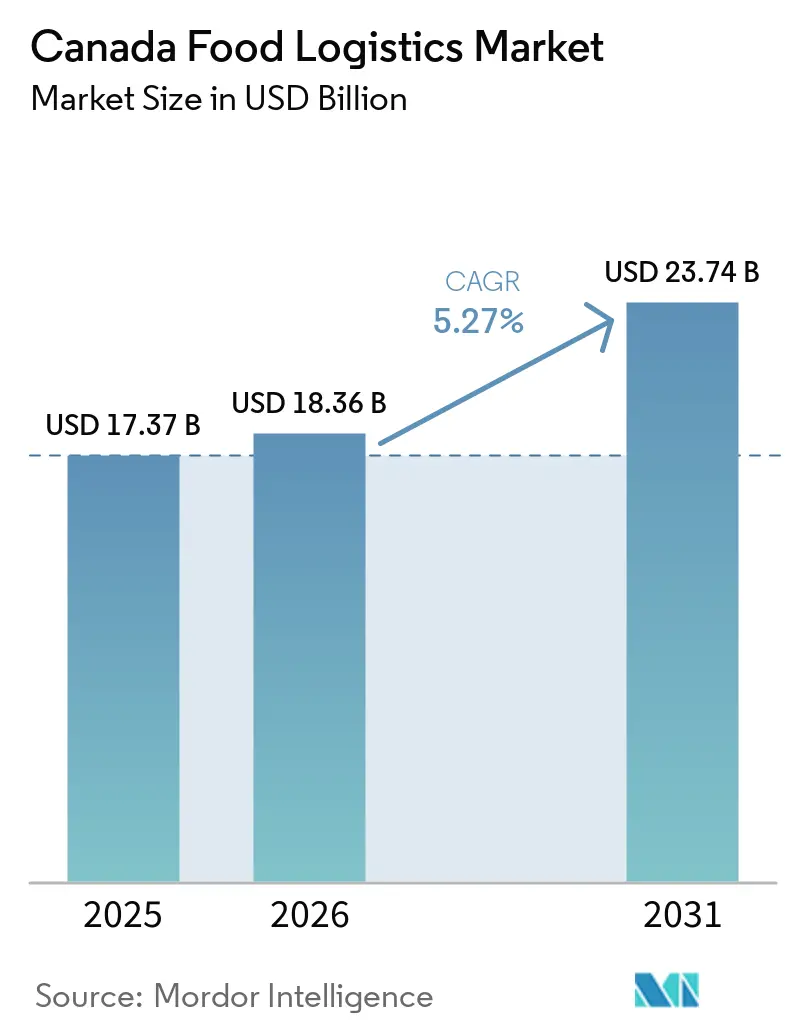

| Base Year Market Size (2025) | USD 17.37 Billion |

| Market Size (2026) | USD 18.36 Billion |

| Market Size (2031) | USD 23.74 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

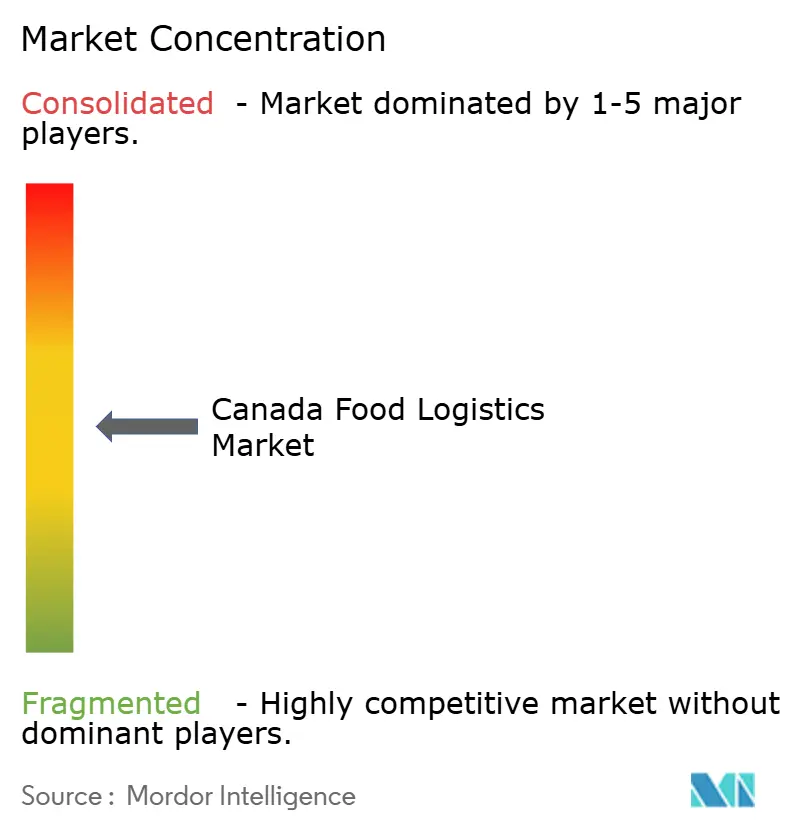

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Food Logistics Market Analysis by Mordor Intelligence

The Canada food logistics market size is projected to be USD 17.37 billion in 2025, USD 18.36 billion in 2026, and reach USD 23.74 billion by 2031, growing at a CAGR of 5.27% from 2026 to 2031.

A measured growth trajectory conceals rapid structural change as plant-based protein adoption, hydrogen-powered reefer fleets, and Indigenous food-security corridors reconfigure distribution networks across a nation where 90% of citizens live within 160 km of the United States border. Capital from the National Trade Corridors Fund is accelerating intermodal node construction, while AI-enabled customs clearance shortens port inspection times to under 90 minutes, improving cargo integrity and asset turns. Demand for differentiated handling, blast-chilling, humidity-controlled packaging, and SKU-level traceability continues to shift value from basic transport toward technology-rich services. At the same time, chronic diesel taxation volatility, technician shortages, and cyber-risk premiums compress margins and spur consolidation across the Canada food logistics market.

Key Report Takeaways

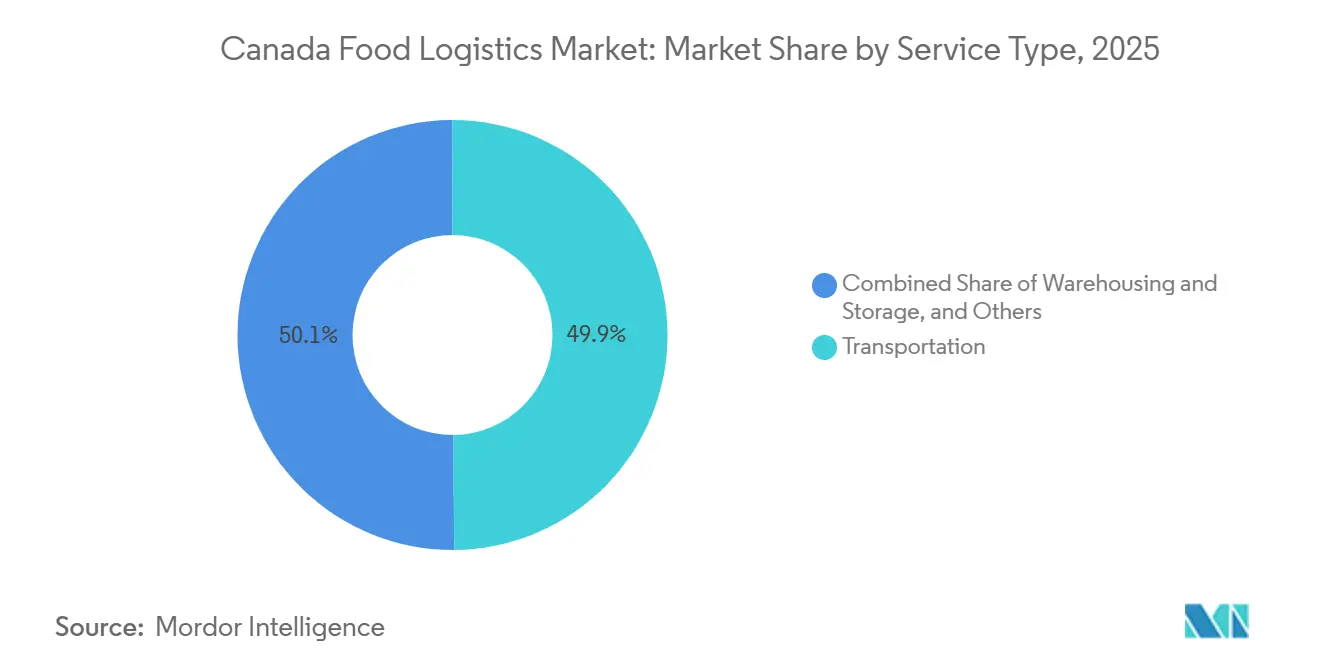

- By service, transportation led with 49.87% of the Canada food logistics market share in 2025, value-added services are forecast to expand at a 7.84% CAGR, the fastest among service categories, through 2031.

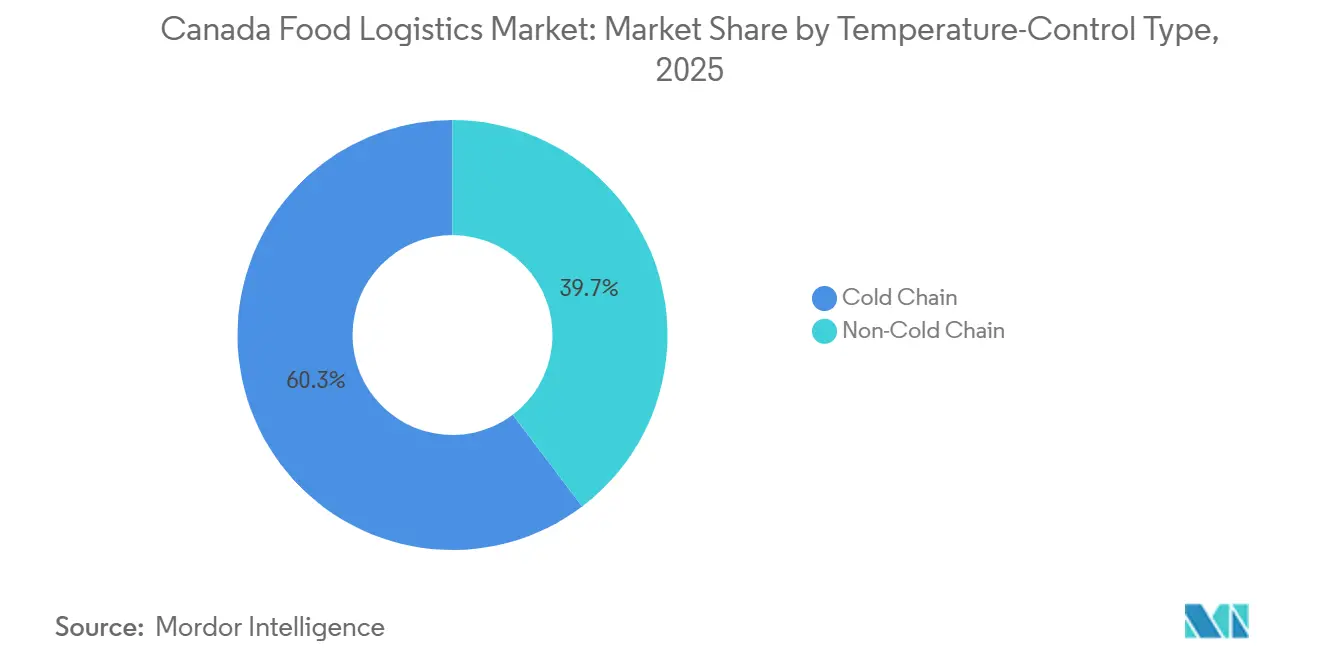

- By temperature-control type, cold chain operations commanded 60.31% of the Canada food logistics market size in 2025, and are projected to advance at a 6.70% CAGR to 2031, outpacing chilled and ambient segments.

- By end-product, meat, seafood, and poultry logistics held 26.42% of the Canada food logistics market size in 2025, while pet food distribution posts the strongest 8.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Food Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging consumer shift toward plant-based & fresh-produce SKUs requiring stricter humidity-controlled logistics | +1.1% | National, concentrated in urban centers and BC Lower Mainland | Medium term (2-4 years) |

| Federal Trade Corridors Fund capital grants are accelerating cold-storage and intermodal node build-outs | +0.9% | National, priority corridors: Vancouver-Calgary, Montreal-Toronto, Halifax gateway | Long term (≥ 4 years) |

| Cross-border e-commerce exports of Canadian specialty foods are boosting small-lot, temperature-controlled freight | +0.7% | Border regions, Ontario-Quebec corridor, BC coastal zones | Medium term (2-4 years) |

| Roll-out of hydrogen fuel-cell–powered refrigerated trailers, lowering long-haul emissions and OPEX | +0.6% | Prairie provinces, Ontario-Quebec corridor | Long term (≥ 4 years) |

| Indigenous-community food-security programs catalyzing new northern cold-chain corridors | +0.4% | Northern territories, remote First Nations communities | Long term (≥ 4 years) |

| AI-based import-inspection scheduling at ports is cutting clearance times for perishables | +0.5% | Major ports: Vancouver, Montreal, Halifax | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Consumer Shift Toward Plant-Based & Fresh-Produce SKUs Requiring Stricter Humidity-Controlled Logistics

Plant-based protein sales climbed 37% between 2020 and 2024, reaching CAD 1.2 billion (USD 867 million) and intensifying demand for cold-chain assets that maintain 85-95% relative humidity alongside precise temperatures. Fresh produce such as leafy greens and berries dehydrates quickly under standard reefers, encouraging carriers to adopt modified-atmosphere packaging and ethylene-scrubbing systems. British Columbia’s Lower Mainland, which produces 60% of Canada’s greenhouse vegetables, now requires farm-to-DC hand-offs in as little as four hours to protect shelf life. Carbon-aware shoppers scrutinize food miles, prompting operators to highlight route-optimization and renewable-energy footprints. Because plant-based items lack preservatives, ISO 22000 compliance is essential to prevent quality loss during even brief thermal excursions[1]Agriculture and Agri-Food Canada, “Statistical Overview of the Canadian Horticulture Sector 2023,” agriculture.canada.ca.

Federal Trade Corridors Fund Capital Grants Accelerating Cold-Storage and Intermodal Node Build-Outs

The National Trade Corridors Fund has allocated CAD 4.6 billion (USD 3.3 billion) through 2028, with 18% earmarked for cold-chain projects such as automated reefer plug-ins and temperature-controlled warehousing. Vancouver’s terminal expansion adds 150,000 ft², of cold storage supporting 1,200 concurrent connections, while Montreal’s Contrecoeur port integrates tri-modal refrigerated capacity to streamline Asia-bound exports. Inland ports in Winnipeg and Saskatoon capture prairie agrifood volumes by pairing pre-cooling infrastructure with bonded rail service. Each federal dollar crowds in CAD 3.20 (USD 2.31 billion) of private capital, underscoring investor confidence in the long-run demand for the Canada food logistics market. Long-lead projects scheduled beyond 2028 ensure sustained capacity infusion well past the current forecast window.

Cross-Border E-Commerce Exports of Canadian Specialty Foods Boosting Small-Lot, Temperature-Controlled Freight

Specialty food e-commerce exports advanced 23% year-over-year in 2024 to reach CAD 2.8 billion (USD 2.02 billion), dominated by maple products, wild Pacific salmon, and organic pulses. Online orders average 5-50 kg, unsuitable for conventional LTL, and thus require temperature-controlled parcel services and customs-bonded micro-fulfillment centers on the United States border. AI-enabled pre-clearance lowered spoilage-related rejections below 2%, enhancing service reliability. Providers are therefore engineering cross-dock hubs in Surrey, Niagara Falls, and Lacolle to guarantee next-day delivery into United States metro areas. The higher average selling price of artisanal SKUs also raises liability, pressing 3PLs to invest in real-time condition monitoring as part of their Canada food logistics market offering[2]Statistics Canada, “Canadian International Merchandise Trade,” 150.statcan.gc.ca.

Roll-Out of Hydrogen Fuel-Cell–Powered Refrigerated Trailers Lowering Long-Haul Emissions and OPEX

Pilot fleets show 40% lower total cost of ownership versus diesel when carbon pricing is included, positioning hydrogen as a viable zero-emission alternative on long-haul prairie corridors. Alberta’s blue-hydrogen capacity supports refueling between Calgary and Vancouver, while noise reduction of 65 dB unlocks overnight urban deliveries. The technology’s vibration-free operation is prized for temperature-sensitive biologics, allowing logistics firms to charge 15-20% service premiums. However, with only 12 heavy-duty hydrogen stations nationwide, infrastructure remains the gating factor. Ongoing federal subsidies of CAD 680 million (USD 491 million) for new stations signal policy alignment with decarbonization goals that benefit the Canada food logistics market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile diesel taxation surcharges are inflating long-haul reefer operating costs | -0.7% | National, particularly Prairie provinces and Ontario | Short term (≤ 2 years) |

| The national shortage of certified industrial-refrigeration technicians is delaying facility commissioning | -0.6% | Alberta, Saskatchewan, Manitoba, rural Ontario | Medium term (2-4 years) |

| Escalating cyber-insurance premiums after cold-chain ransomware attacks are raising overheads | -0.4% | National, concentrated in major logistics hubs | Short term (≤ 2 years) |

| Seasonal ice-road melt disrupting northern last-mile refrigerated deliveries | -0.3% | Nunavut, Northwest Territories, northern Manitoba | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Diesel Taxation Surcharges Inflating Long-Haul Reefer Operating Costs

Fuel surcharges strain shipper relationships and erode fixed-rate contracts, prompting modal shifts toward rail on select corridors. Smaller fleets without hedging tools exit the Canada food logistics market or merge with larger carriers that can absorb volatility. In the near term, taxation uncertainty remains the single biggest cost-side variable for road-based cold chain operators[3]Natural Resources Canada, “Fuel Prices in Canada,” nrcan.gc.ca.

National Shortage of Certified Industrial-Refrigeration Technicians Delaying Facility Commissioning

Vacancy rates exceed 22% in Alberta and Saskatchewan, extending time-to-fill beyond 180 days and pushing wage offers 30% above national averages. Commissioning new ammonia or CO₂ cascade systems now adds four-to-six-month delays, slowing capacity additions even as demand rises. Aging workforce demographics suggest 38% attrition by 2031 without a material uptick in apprenticeships. Developers, therefore concentrate projects in regions with better talent pipelines, influencing geographic deployment of the Canada food logistics market. Regulatory mandates for certified technicians under TSSA rules compound the urgency, since non-compliance risks costly shutdowns[4]Statistics Canada, “Job Vacancies, Payroll Employees,” 150.statcan.gc.ca.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services: Specialized Handling Commands Premium Growth

Transportation captured 49.87% of the Canada food logistics market share in 2025, anchored by road haulage that connects production regions to urban demand centers. Yet value-added services, blast-chilling, humidity-controlled packaging, and SKU-level traceability are growing at 7.84% CAGR, reflecting shipper demand for differentiated quality assurance. Warehousing investment is shifting toward automation; AI-guided put-away and robotic picking raise accuracy to 99.8% while slicing labor hours by 35%. Intermodal rail gains on high-volume corridors as CN and CP inject CAD 1.8 billion (USD 1.3 billion) into refrigerated container fleets. Air freight remains indispensable for premium seafood and berries bound for overseas markets, commanding double-digit margins inside the Canada food logistics market.

The service mix is evolving toward end-to-end solutions that embed transport, storage, and compliance reporting under single-provider SLAs. Blast-chilling protects plant-based proteins from textural degradation, justifying premiums of 40-60% over standard storage. Modified-atmosphere ‘smart’ packaging cuts produce waste by 20% while delivering verifiable ESG gains. Blockchain-linked IoT sensors meet Safe Food for Canadians Regulations, making digital traceability table stakes for large RFPs. Such complexity raises capex thresholds and favors incumbents with multi-modal footprints and robust IT stacks across the Canada food logistics market.

By Temperature-Control Type: Cold Chain Dominance Persists

Cold chain operations held 60.31% of the Canada food logistics market size in 2025, and are expanding at a CAGR of 6.70% through 2031. Chilled storage at 2–8 °C underpins dairy, fresh meat, and ready-to-eat salads, now layering humidity control to retain produce crispness. Ambient climate control at 15–25 °C protects confectionery and shelf-stable beverages from temperature swings that drive bloom or flavor loss. Non-cold chain services maintain relevance for dry staples but face shrinking share as consumer baskets tilt toward perishables.

Capex intensity diverges sharply: automated cold facilities cost CAD 800-1,200 (USD 578-867) per ft2 versus CAD 200-350 (USD 145–254) for ambient, creating clear financial barriers. Energy forms 40% of cold-storage opex, spurring adoption of rooftop solar and waste-heat recapture. Ammonia systems lead among large warehouses for efficiency, though they require scarce technician expertise, reinforcing earlier labor constraints. Sustainability audits now accompany RFQs, pushing operators to disclose carbon intensity per pallet and renewable-energy mix, trends that will define competitive advantage in the Canada food logistics market.

By End-Product Category: Pet Food Disrupts Traditional Hierarchies

Meat, seafood, and poultry retained 26.42% share in 2025 on the strength of Canada’s beef and pork export complexes. Yet premium pet food is the breakout, growing at 8.13% CAGR thanks to fresh-frozen formats that require -18 °C integrity and pharmaceutical-grade traceability. Dairy and frozen desserts benefit from continued indulgence spending, while plant-based dairy alternatives nibble double-digit share within the category. Produce logistics remains volatile, tethered to seasonality and high import dependence 80% of fresh vegetables consumed domestically traverse at least one United States border crossing.

Pet ownership now spans 58% of households, with an annual spend of CAD 1,847 (USD 1,334) per family, validating capital allocation toward pet-food-ready freezer tunnels and HACCP protocols. Fresh-frozen meal kits demand validated cold chains akin to vaccine distribution, raising service expectations across other categories. Meanwhile, horticulture shippers push for humidity-optimized packaging to extend shelf life on berries and leafy greens, adding new revenue layers. Category diversification thus multiplies specialized service niches inside the Canada food logistics market.

Geography Analysis

Federal corridors funding shapes regional build-outs. The Vancouver Calgary artery expands rail-truck intermodal yards, reinforcing Vancouver’s 2.4 million TEU refrigerated throughput and anchoring Asia-Canada protein flows. Ontario’s Golden Horseshoe houses 40% of national cold storage and grants same-day access to United States Northeast metros, while Quebec’s low-cost hydroelectricity slices energy bills 30–40%, supporting mega-warehouses outside Montreal. Prairie inland ports in Winnipeg and Saskatoon aggregate grain and pulse exports, deploying pre-cooling to lift container fill factors and reduce spoilage.

Atlantic Canada, led by Halifax, leverages an ice-free port that shortens the transit to Europe by two days during winter when the Great Lakes locks close. Hydrogen corridor pilots now extend eastward, bolstering green-fuel uptake on the Montreal-Halifax lane. Conversely, northern territories remain challenged; reliance on ice roads for up to 85% of annual food volume renders supply chains fragile as melt seasons shrink. Indigenous-led cold-hub initiatives partly mitigate risk but still leave costly air freight as the only year-round option, constraining equitable market access within the Canada food logistics market.

Population density skews infrastructure; 90% of Canadians live within 160 km of the United States border, yet national networks must still span 9.98 million sq km. AI-enabled inspection at Vancouver, Montreal, and Halifax freed up berth capacity equivalent to 120,000 additional reefer plugs by cutting dwell times 75%, a capacity gain not yet matched by smaller ports. Regional disparities in technician availability, electricity cost, and tax policy further influence where new cold-chain assets materialize, reinforcing the hub-and-spoke geography of the Canada food logistics market.

Competitive Landscape

The top 10 providers hold a collective 45% share, pointing to moderate fragmentation. Leaders differentiate via IoT sensor grids that cut spoilage 20% and blockchain-verified chain-of-custody reports that satisfy stringent retailer audits. Early adopters of hydrogen reefers lock in multiyear freight contracts with ESG-focused shippers, creating first-mover moats. M&A momentum accelerates as small fleets unable to fund cyber defenses or technician premiums look for exit options, consolidating capacity within the Canada food logistics market.

Technology is the decisive battleground. Warehouse management systems integrated with predictive maintenance algorithms push uptime over 99.5%. Route-optimization AI reduces empty miles by 12%, offsetting fuel tax surcharges. Safe Food for Canadians Regulations elevate baseline compliance costs, favoring large incumbents who amortize investments across national footprints. Niche disruptors penetrate by focusing on micro-fulfillment for e-commerce perishables and drone-assisted northern last-mile, but must scale quickly to remain viable.

Pricing discipline remains elusive amid volatile diesel costs and rising insurance premiums, yet customers increasingly select providers on total supply-chain cost rather than rate cards alone. Sustainability auditing, real-time visibility, and incident-response readiness have become weighted scoring criteria in RFPs. Consequently, operational excellence and digital capability now outweigh raw fleet size in determining long-term winners within the Canada food logistics market.

Canada Food Logistics Industry Leaders

Lineage Logistics Holdings

Congebec Logistics

Conestoga Cold Storage

Versacold Logistics

Americold Realty Trust

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lineage Logistics committed CAD 220 million (USD 159 million) to a 600,000 ft² automated Calgary cold store featuring hydrogen fuel-cell backup and AI inventory control, targeting plant-based protein clients.

- November 2025: Lineage Logistics launched a USD 806 million private placement to support capacity expansion and working capital as it continues growth across the United States and international cold chain network.

- August 2025: Americold Realty Trust opened a new 335,000 ft2 import export cold storage hub in Kansas City, Missouri, in partnership with Canadian Pacific Kansas City, supporting the Mexico Midwest Express (MMX) rail service for refrigerated freight across North America and creating nearly 190 new jobs.

- July 2025: Congebec Logistics invested CAD 85 million (USD 61.4 million) in solar-powered refrigeration across Quebec, trimming grid draw 45%.

Canada Food Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Water | |

| Air | |

| Warehousing and Storage | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) |

| Cold Chain | Ambient (15-25 °C) |

| Chilled (2-8 °C) | |

| Frozen (Less than 0 °C) | |

| Non Cold Chain |

| Meat, Seafood, and Poultry |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) |

| Horticulture (Fresh Fruits and Vegetables) |

| Processed Food Products |

| Pet Food |

| Others (Spreads, Seasoning, dressing, Specialty and Functional Foods, etc.) |

| By Services | Transportation | Road |

| Rail | ||

| Sea and Inland Water | ||

| Air | ||

| Warehousing and Storage | ||

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) | ||

| By Temperature-Control Type | Cold Chain | Ambient (15-25 °C) |

| Chilled (2-8 °C) | ||

| Frozen (Less than 0 °C) | ||

| Non Cold Chain | ||

| By End-Product Category | Meat, Seafood, and Poultry | |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) | ||

| Horticulture (Fresh Fruits and Vegetables) | ||

| Processed Food Products | ||

| Pet Food | ||

| Others (Spreads, Seasoning, dressing, Specialty and Functional Foods, etc.) | ||

Key Questions Answered in the Report

How large will the Canada food logistics market be by 2031?

It is projected to reach USD 23.74 billion by 2031, expanding at a 5.27% CAGR from 2026.

Which service is growing fastest?

Value-added services such as blast-chilling and traceability are forecast to grow at 7.84% CAGR through 2031.

What fuels hydrogen reefer adoption in Canada?

A 40% lower total cost of ownership versus diesel under carbon pricing and federal subsidies drives uptake on long-haul routes.

Why is pet food logistics a hot segment?

Fresh-frozen pet diets need -18 °C distribution and are advancing at an 8.13% CAGR, the fastest among end-product categories

Why is pet food logistics growing quickly?

Premiumization and 11.3% e-commerce penetration push pet food logistics at a 9.1% CAGR.

How does AI improve port clearance times?

Predictive scheduling has reduced perishable inspection from six hours to under 90 minutes at major Canadian ports.

Page last updated on: