Porcine Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

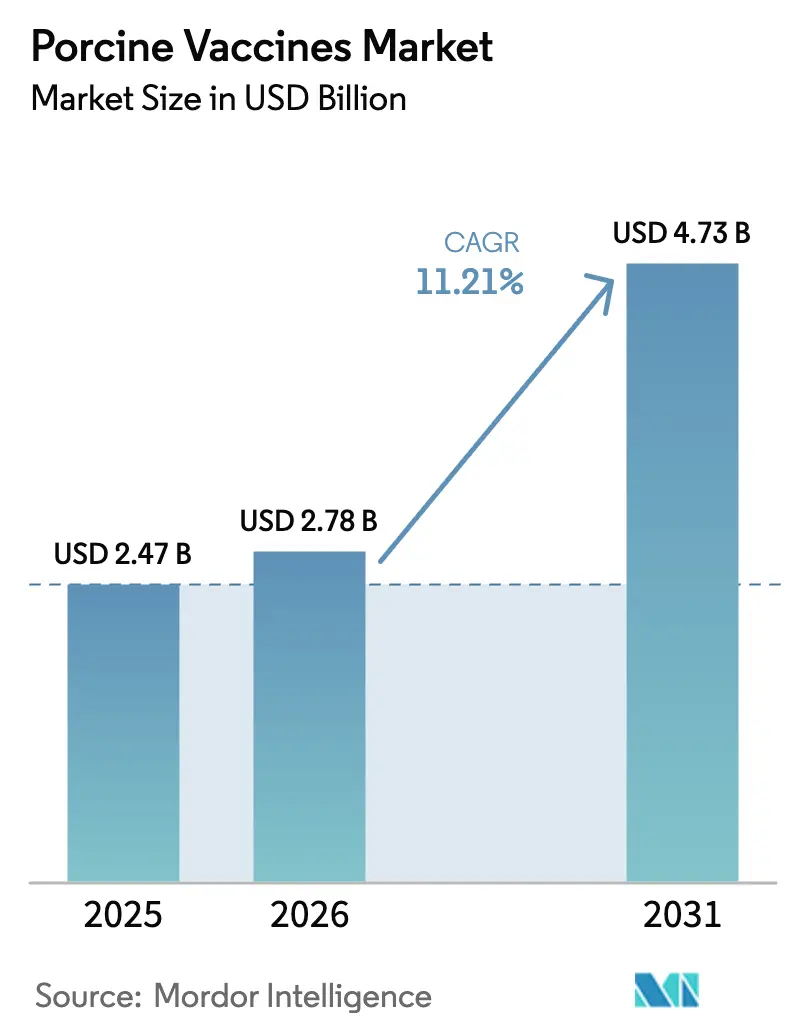

| Market Size (2026) | USD 2.78 Billion |

| Market Size (2031) | USD 4.73 Billion |

| Growth Rate (2026 - 2031) | 11.21% CAGR |

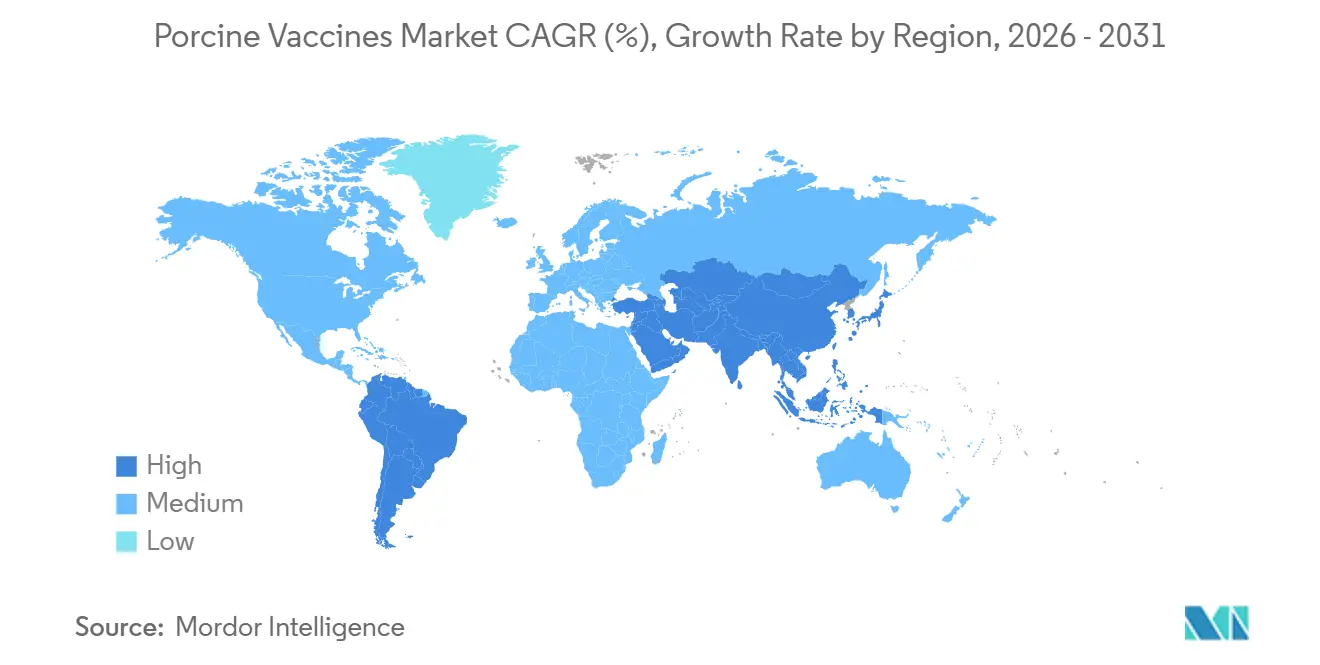

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

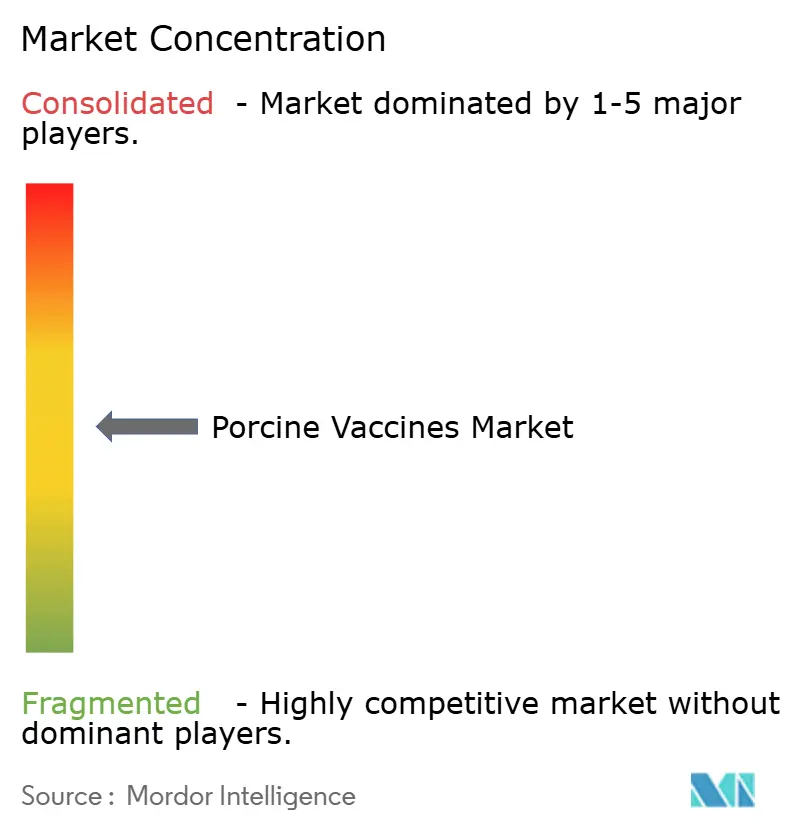

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Porcine Vaccines Market Analysis by Mordor Intelligence

The Porcine Vaccines Market size is projected to be USD 2.47 billion in 2025, USD 2.78 billion in 2026, and reach USD 4.73 billion by 2031, growing at a CAGR of 11.21% from 2026 to 2031.

Strong demand for pork protein in emerging economies, rising prevalence of African Swine Fever (ASF) and Porcine Reproductive and Respiratory Syndrome (PRRS), and the continued phase-out of prophylactic antibiotics in major producing nations are the core forces propelling the porcine vaccine market. Vertically integrated producers in North America protect export certification through comprehensive immunization, while Asian governments subsidize mass-vaccination programs that compress adoption cycles. Advances in thermostable formulations, needle-free devices, and AI-enabled surveillance platforms are lowering logistical barriers and improving return on investment for producers. At the same time, regulatory agencies in the United States and the European Union are streamlining line-extension pathways, accelerating time-to-market for combination products that address new serotypes with fewer injections. Intense price competition from Chinese manufacturers, however, is pressuring global margins and reshaping supply chains.

Key Report Takeaways

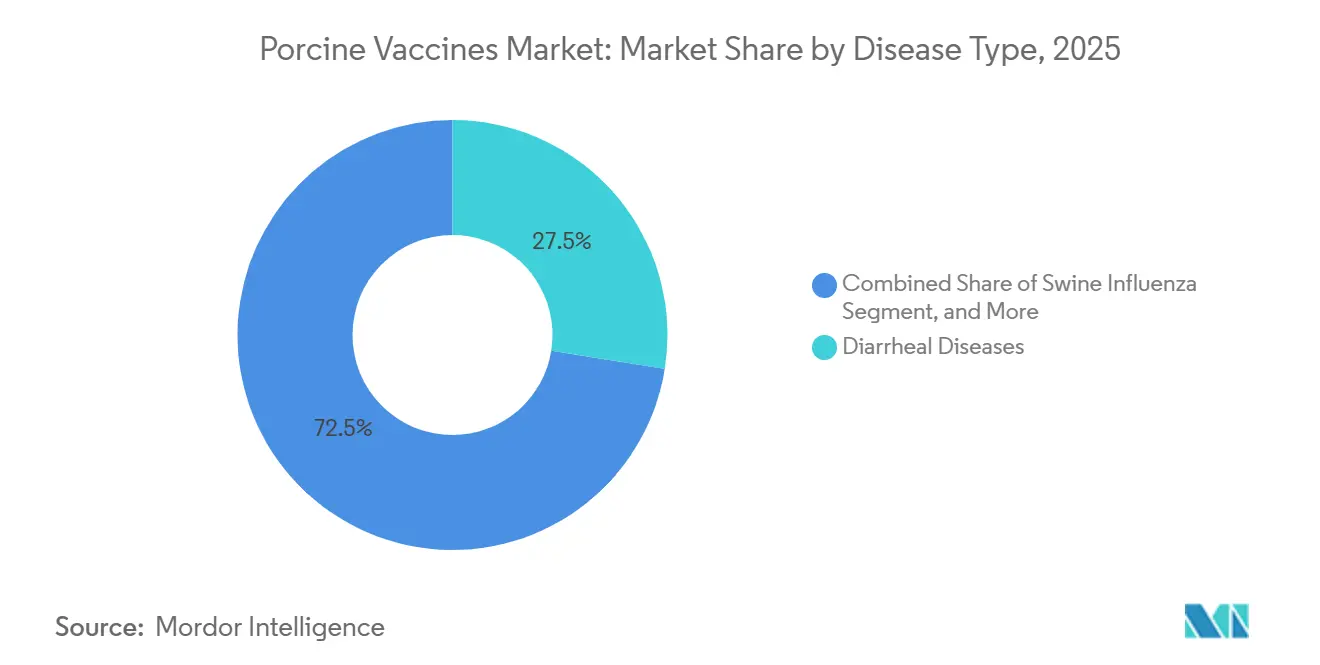

- By disease type, diarrheal vaccines led with 27.48% of 2025 porcine vaccine market share, while swine influenza products are expanding at a 12.76% CAGR through 2031.

- By technology platform, live-attenuated products commanded 35.62% of 2025 revenue, whereas recombinant-vector vaccines are advancing at a 14.73% CAGR.

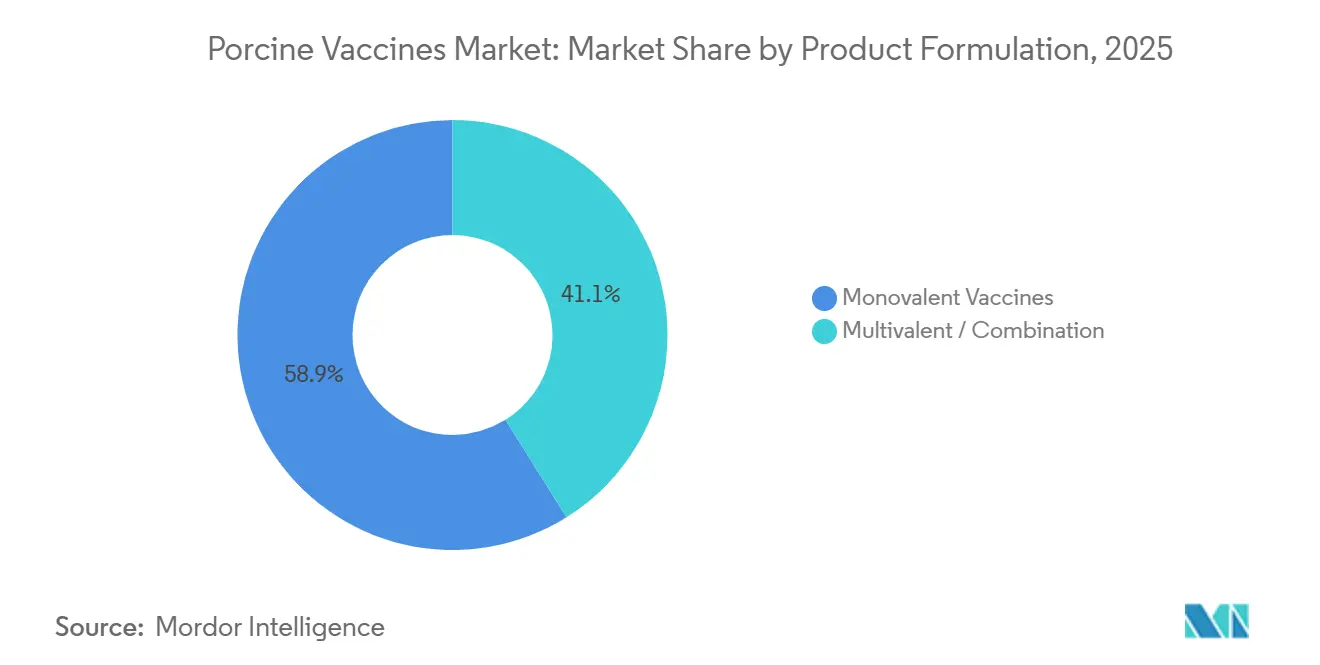

- By product formulation, monovalent doses captured 58.88% of 2025 sales; however, multivalent combinations are growing at a 12.08% CAGR.

- By administration route, intramuscular delivery held a 45.74% share in 2025, as oral and intranasal options accelerate at 15.31% CAGR.

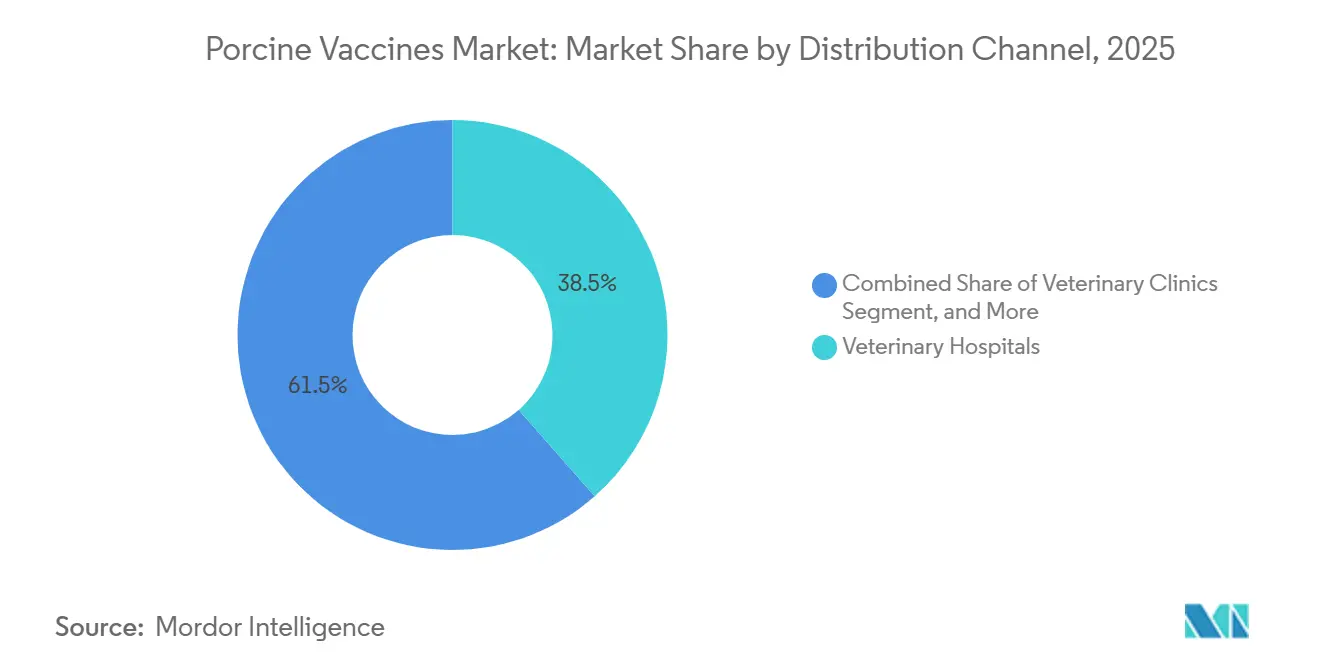

- By distribution channel, veterinary hospitals accounted for 38.46% of 2025 revenue, while veterinary clinics represented the fastest-growing channel, with a 13.25% CAGR.

- By geography, North America dominated with 38.35% of the 2025 revenue, while the Asia-Pacific region is the fastest-growing at a 14.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Porcine Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for pork protein in emerging economies | +1.8% | Asia-Pacific core, spillover to Middle East & Africa | Medium term (2-4 years) |

| Increasing prevalence of PRRS, PEDV & ASF | +2.5% | Global, with acute pressure in Asia-Pacific and Eastern Europe | Short term (≤ 2 years) |

| Government-backed mass-vaccination programs | +1.5% | China, Vietnam, Brazil, select EU member states | Medium term (2-4 years) |

| Shift to antibiotic-free pork production | +1.2% | North America & EU, early adoption in Australia | Long term (≥ 4 years) |

| Thermostable & needle-free delivery unlocking low-infrastructure markets | +0.9% | Sub-Saharan Africa, South Asia, rural Latin America | Long term (≥ 4 years) |

| AI-enabled disease-surveillance guiding targeted vaccination | +0.6% | North America, Western Europe, advanced Asia-Pacific operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Pork Protein in Emerging Economies

Rapid urbanization increased Southeast Asian per-capita pork consumption by 7% between 2024 and 2025, making vaccination a prerequisite for contract farming agreements with modern processors.[1]U.S. Department of Agriculture, “Livestock and Poultry Outlook,” USDA.gov China’s sow herd recovered to 43.9 million head by late 2025, and provincial regulations now require quarterly vaccination logs to be submitted before slaughterhouse entry. Middle-Eastern importers mandate proof of PRRS and influenza immunization on veterinary certificates, even in exporting nations with historically low coverage. Producers view a USD 2–3 per-head vaccine outlay as negligible compared to the financial shock of a 10% mortality event, especially where pork accounts for 40% of animal protein spending. Consequently, the porcine vaccine market is tracking closely with income growth in Vietnam, the Philippines, and southern China.

Increasing Prevalence of PRRS, PEDV & ASF

ASF detections in Philippine herds surged 34% in 2025, forcing culling radii to widen and catalyzing demand for experimental subunit candidates.[2]Philippine Bureau of Animal Industry, “ASF Update,” da.gov.ph PRRS still costs U.S. producers USD 664 million annually, and heterologous strains cut performance 5–8% even in vaccinated herds.[3]Food and Agriculture Organization, “Meat Market Review,” FAO.org PRRS recombinant variants emerging in central China erode existing vaccine protection, compelling manufacturers to replace seed strains and sustain demand for fast-pivot platforms. Europe’s winter 2024-2025 PEDV outbreaks demonstrated that waning disease pressure reduces compliance, creating pools of susceptible pigs that amplify the subsequent incursion. These evolutionary dynamics keep the porcine vaccine market on a perpetual R&D cycle, rewarding technologies that enable rapid antigen substitution.

Government-Backed Mass-Vaccination Programs

Vietnam earmarked VND 1.2 trillion (approximately USD 50 million) in 2025 to achieve 80% breeding-herd coverage by 2026. Brazil’s National Swine Health Program linked PRRS and influenza vaccination to federal credit access in 2025, driving uniform adoption across operations exceeding 500 head. Chinese provinces offering 50% co-payment for farms enrolled in digital-traceability schemes tie immunization directly to market access. Within the European Union, Category A/B status for PRRS and ASF empowers states to enforce vaccination in protection zones. These interventions underwrite demand, enabling suppliers to invest confidently in production capacity.

Shift to Antibiotic-Free Pork Production

FDA Guidance #263 ended the preventive use of medically necessary antimicrobials in 2024, making vaccines central to the herd health strategy. U.S. processors have mandated “No Antibiotics Ever” certification by 2027, accelerating the adoption of multivalent vaccines at Smithfield Foods. Retail premiums of 15–20% on antibiotic-free pork in Europe further incentivize upstream vaccination. Without vaccines, antibiotic-free finishing pigs suffer 3–5% higher mortality and an extra 7–10 days on feed, eroding margin. As more markets replicate these restrictions, the porcine vaccine market benefits from a policy-driven tailwind.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain logistics cost in developing regions | -0.9% | Sub-Saharan Africa, South Asia, rural Latin America | Short term (≤ 2 years) |

| Adverse reactions & vaccine failure with live-attenuated strains | -0.8% | Global, with heightened scrutiny in North America & EU | Medium term (2-4 years) |

| Vaccine-derived recombination eroding efficacy | -0.7% | Global, acute in Asia-Pacific and Eastern Europe dense production zones | Medium term (2-4 years) |

| Capital flight toward looming ASF subunit vaccines | -0.6% | Asia-Pacific core, spillover to Eastern Europe and select Latin American markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cold-Chain Logistics Cost in Developing Regions

Keeping vaccines at 2–8 °C adds USD 0.80–1.20 per dose where electricity exceeds USD 0.25/kWh and last-mile transport relies on motorcycles. Surveys in Nigeria, Tanzania, and Uganda revealed that 42% of deliveries exceeded temperature limits, reducing potency by up to 60% and eroding trust in vaccines. Solar refrigerators reduced spoilage in India’s Assam state from 28% to 9%, yet a unit cost of USD 1,500 is prohibitive without a subsidy. The result is cyclical under-vaccination, which perpetuates disease and dampens near-term growth in the porcine vaccine market.

Adverse Reactions & Vaccine Failure with Live-Attenuated Strains

Reversion-to-virulence episodes prompted updated isolation protocols in 2024. European pharmacovigilance logged 127 hypersensitivity cases during 2024-2025, forcing label changes and biosecurity upgrades. Live-attenuated failures, often linked to cold-chain lapses or maternal antibody interference, occur at a rate of 8–15% in commercial herds. These risks drive producers toward recombinant and subunit alternatives despite a 2–3 × price premium, nudging the porcine vaccine market toward higher-value but costlier platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Enteric Leaders, Respiratory Sprinters

Diarrheal formulations held a commanding 27.48% share in 2025, making them the single most significant slice of the porcine vaccine market revenue. Swine influenza lines, however, are advancing at a 12.76% CAGR as H1N1 and H3N2 variants circulate more aggressively in densely stocked barns. Influenza also poses a zoonotic spillover risk, underscoring the need for regulatory agencies to support the rapid development and update of vaccines. PRRS vaccines, long considered indispensable, face efficacy challenges as recombinant field strains evade existing immunogens, necessitating sustained research and development (R&D) investment. ASF remains a white-space opportunity; no globally commercialized dose exists outside of China and Vietnam, but subunit candidates in late-stage development could unlock substantial incremental demand for the porcine vaccine market once regulatory hurdles are cleared.

The performance of diarrheal products is influenced by acute mortality in farrowing units; mortality exceeding 40% in outbreaks justifies immediate allocation of an immunization budget. In contrast, respiratory vaccines appeal to integrators for improving feed efficiency and days-to-market. Both segments illustrate a bifurcation: enteric lines drive steady volume, while respiratory solutions contribute significantly to the growth of the porcine vaccine market.

By Technology Platform: Safety Shapes Adoption Curves

Live-attenuated formats still accounted for 35.62% of 2025 revenue due to their low cost and durable immunity, yet they shoulder pharmacovigilance burdens and potential reversion events. Recombinant-vector platforms are rising at 14.73% CAGR, benefiting from dual humoral-cellular responses and the absence of live-virus risk. Inactivated vaccines dominate where safety trumps potency, especially for swine influenza, though booster-dose labor can deter smaller producers. Subunit offerings, such as the latest PCV2d constructs, bypass cold-chain fragility, securing uptake in high-temperature regions. DNA and nanoparticle-adjuvanted prototypes in Phase III U.S. trials signal the next frontier, positioning the porcine vaccine market for even faster antigen-switch cycles as pathogen landscapes shift.

Economics influence platform choice: while recombinant doses cost 2–3 times more than MLV products, their predictable safety profile justifies the premium where export certification or consumer labeling is a consideration. Consequently, multinationals deploy tiered portfolios, pricing traditional formats aggressively to defend share while upselling novel vectors to customers with tighter biosecurity requirements.

By Product Formulation: Combining to Conserve Labor

Monovalent shots accounted for 58.88% of 2025 revenue because they let veterinarians tailor schedules herd-by-herd. Multivalent combinations, growing at a 12.08% annual rate, compress labor windows by bundling PRRS, PCV, and Mycoplasma antigens into a single visit. A 2,000-sow Iowa site reduced injection time by 35% after switching to a trivalent schedule, underscoring labor as a hidden cost driver. Regulatory agencies now permit line-extension dossiers that add new serotypes without repeating full efficacy trials, shortening approval timelines by 12–18 months. This policy shift removes a key barrier and should accelerate the uptake of multivalent vaccines, propelling the incremental growth of the porcine vaccine market for combination formats.

Still, antigen-interference remains a formulation challenge. Manufacturers deploy proprietary adjuvants and staggered-release technologies to maintain immune titers for each component. Success stories, such as Fostera Gold PCV MH, demonstrate that properly engineered blends can displace monovalent incumbents in under two commercial cycles.

By Administration Route: Toward Herd-Level Immunity

Intramuscular delivery retained 45.74% of 2025 usage because depot effects prolong antigen exposure. Yet, oral and intranasal modalities, which expand at a rate of 15.31% per year, unlock herd-level immunity where individual injections are uneconomic. Danish trials demonstrated that oral PRRS vaccination achieved 81% seroconversion at 70% lower labor costs, making the approach attractive for finishing barns. Needle-free intradermal systems reduce handling stress and decrease seroconversion time by 15–20%, indicating a route-driven efficacy advantage that can command pricing power. As these alternatives mature, the porcine vaccine market will diversify beyond traditional needles, especially in markets facing chronic labor shortages.

By Distribution Channel: Clinics Gain Ground

Veterinary hospitals accounted for 38.46% of 2025 revenue, primarily due to bulk purchasing by large integrators. Clinics, growing at a rate of 13.25% annually, fill gaps in decentralized regions where mobile veterinarians combine diagnostics and same-day dosing. A National Pork Board survey revealed that 34% of U.S. producers with fewer than 1,000 head now rely on mobile clinics, up from 22% in 2020. Digital commerce adds another twist: direct-to-farm platforms logged USD 47 million in 2025 swine-vaccine sales, shaving distribution margins and promoting price transparency. Channel fluidity ultimately supports broader market penetration of porcine vaccines by matching service models to farm scale.

Geography Analysis

North America contributed 38.35% of 2025 revenue, anchored by the United States’ 74 million-head inventory and export-oriented, vertically integrated systems. Canada’s shift toward antibiotic-free production aligns with U.S. processor mandates, pushing PRRS and PCV sales into double-digit growth during 2024-2025. Mexico’s 6% increase in pork output in 2025 reflects near-shored processing; however, vaccine penetration remains below 50% among smallholders due to credit constraints. The FDA's antimicrobial curbs, effective 2024, will convert vaccines into the default disease-prevention tool, while Zoetis’ USD 120 million investment in a Michigan biologics plant will expand regional capacity by 30% by 2027.

The Asia-Pacific region is projected to grow at a rate of 14.25% annually, driven by China’s post-ASF rebound and subsidies in Southeast Asia. Vietnam’s state funding aims for 80% breeding-herd coverage by 2026, while Japan and South Korea maintain near-universal vaccination but flat herd sizes. India’s pilot programs achieved 91% coverage in participating villages during 2025, hinting at latent potential if logistical hurdles are solved. Australia, disease-free but small in scale, provides a steady niche for erysipelas and leptospirosis doses. Sustained progress hinges on China avoiding major ASF relapses and governments continuing to treat vaccination as a strategic, partially subsidized input.

Europe maintains robust demand due to regulatory enforcement under the Animal Health Law, which classifies PRRS and ASF in the top two disease categories. Germany, Spain, and Denmark generate 58% of the regional pork supply and display near-total vaccine adoption, while Poland and Romania record high double-digit growth due to ongoing ASF incursions in wild boar populations. Spain’s integrated producers increased per-pig vaccine spending to EUR 3.50 in 2025, driven by animal welfare metrics demanded by retailers. The United Kingdom harmonizes with EU standards but seeks quicker pathways for novel platforms, attracting Ceva’s UK-specific Hyogen dossier in 2024. Eastern Europe’s consolidation phase favors multinationals offering technical support tailored to large-scale operations, reinforcing the moderate concentration of the porcine vaccine market.

Competitive Landscape

The top five suppliers held a significant share of the global revenue in 2025, reflecting a moderately concentrated porcine vaccine market. Zoetis, Boehringer Ingelheim, Merck Animal Health, Ceva Santé Animale, and Elanco maintain their leadership through the combination of products, proprietary adjuvants, and bundled digital services. Boehringer Ingelheim’s 2024 acquisition of a German viral-vector platform shaved 18 months off its recombinant PRRS timeline, signaling incumbents’ reliance on mergers and acquisitions (M&A) to offset internal research and development (R&D) bottlenecks. Patent grants for nanoparticle adjuvants increased by 34% between 2023 and 2025, indicating that next-generation immune modulation is an emerging competitive vector.

Chinese challengers Ringpu, Qilu, Winsun undercut multinationals by 30–40% with thermostable lyophilized doses, winning share in Southeast Asia and Africa. Elanco’s Healthy Outcomes suite combines vaccines with analytics and consulting, generating USD 210 million in 2025 swine revenue and demonstrating how service bundles can help defend premiums even amid price pressure. Regulatory tightening around live-attenuated pharmacovigilance makes recombinant and subunit pipelines strategic priorities; suppliers able to pivot quickly stand to capture incremental porcine vaccine market share once ASF or new PRRS variants demand updated antigens.

Smaller disruptors leverage agility in niche geographies. Indian Immunologicals uses ISO-certified facilities to supply Southeast Asia, while Virbac’s thermostable erysipelas launch targets smallholders lacking refrigeration in East Africa. The competitive field thus divides into premium technology-service ecosystems and cost-focused regional specialists, with neither side yet able to lock in universal dominance.

Porcine Vaccines Industry Leaders

Zoetis Inc.

Vetoquinol

HIPRA

Elanco Animal Health

Boehringer Ingelheim Animal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Boehringer Ingelheim introduced INGELVAC CIRCOFLEX AD, the first dual PCV2a/PCV2d single-dose vaccine, building on nearly two decades of CIRCOFLEX field success.

- September 2025: The Pirbright Institute demonstrated a needle-free solid-dose vaccine that protected pigs against PRRSV, marking a first for any livestock species.

- September 2025: HIPRA opened a EUR 65 million Girona facility for intradermal swine vaccines, reducing manufacturing cycles from 90 to 60 days.

Global Porcine Vaccines Market Report Scope

Porcine Vaccines are a clinical and administrative drug that ameliorates swine health by protecting them from various bacteria, viruses, and other pathogens. The market is segmented by Target Disease (Diarrhea, Swine Influenza, Arthritis, Bordetella Rhinitis, Porcine Reproductive and Respiratory Syndrome (PRRS), Porcine Circovirus Associated Disease (PCVAD), Other Target Diseases), Technology (Inactivated Vaccines, Live Attenuated Vaccines, Toxoid Vaccines, Recombinant Vaccines, Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.

| Porcine Reproductive & Respiratory Syndrome |

| Porcine Circovirus Associated Disease |

| Diarrheal Diseases |

| Swine Influenza |

| Classical & African Swine Fever |

| Other Diseases |

| Live-attenuated |

| Inactivated/Killed |

| Toxoid & Subunit |

| Recombinant Vector |

| Other Technology Platform |

| Monovalent Vaccines |

| Multivalent / Combination |

| Intramuscular |

| Intradermal |

| Oral & Intranasal Mucosal |

| Veterinary Hospitals |

| Veterinary Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | Porcine Reproductive & Respiratory Syndrome | |

| Porcine Circovirus Associated Disease | ||

| Diarrheal Diseases | ||

| Swine Influenza | ||

| Classical & African Swine Fever | ||

| Other Diseases | ||

| By Technology Platform | Live-attenuated | |

| Inactivated/Killed | ||

| Toxoid & Subunit | ||

| Recombinant Vector | ||

| Other Technology Platform | ||

| By Product Formulation | Monovalent Vaccines | |

| Multivalent / Combination | ||

| By Administration Route | Intramuscular | |

| Intradermal | ||

| Oral & Intranasal Mucosal | ||

| By Distribution Channel | Veterinary Hospitals | |

| Veterinary Clinics | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the porcine vaccine market by 2031?

The porcine vaccine market is expected to reach USD 4.73 billion by 2031.

Which region is forecast to grow the fastest through 2031?

Asia-Pacific is projected to expand at a 14.25% CAGR, the highest among all regions.

Which disease segment currently generates the most revenue?

Vaccines targeting diarrheal diseases hold the largest slice at 27.48% of 2025 revenue.

Why are multivalent vaccines gaining popularity?

Multivalent formulations cut labor time by bundling multiple antigens into a single injection while maintaining efficacy.

How is regulation influencing vaccine adoption in North America?

FDA Guidance #263 ended preventive antibiotic use in 2024, making vaccines the primary preventive tool for swine producers.

Page last updated on: