Swine Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

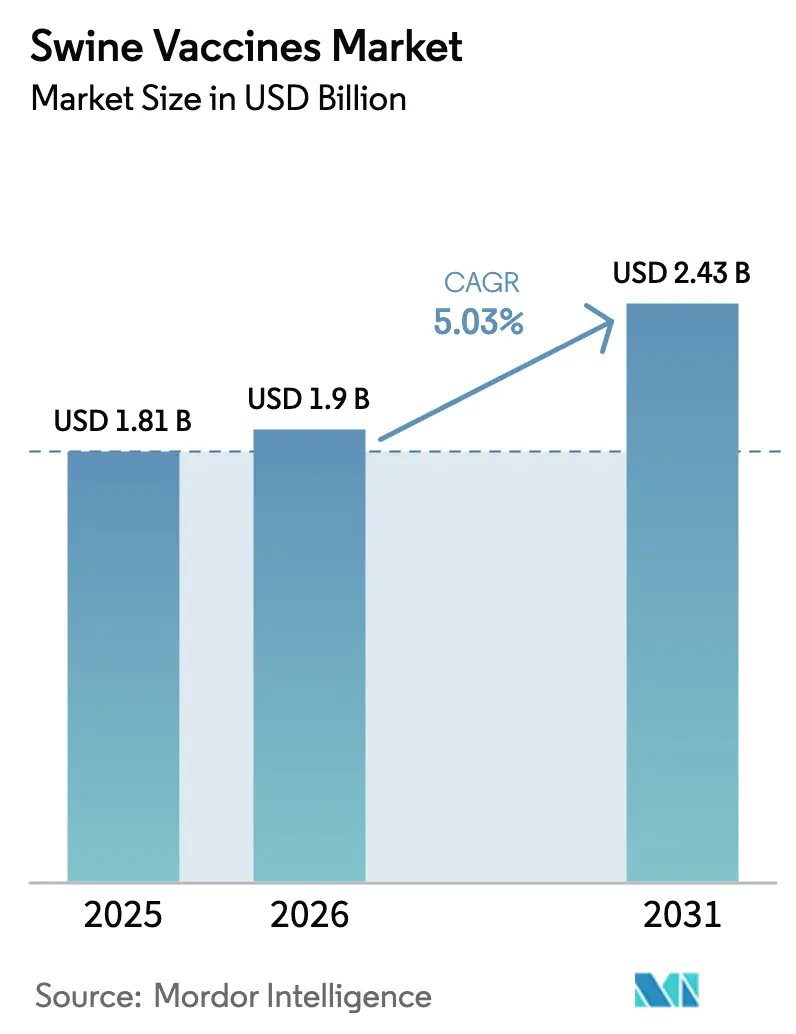

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.43 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Swine Vaccines Market Analysis by Mordor Intelligence

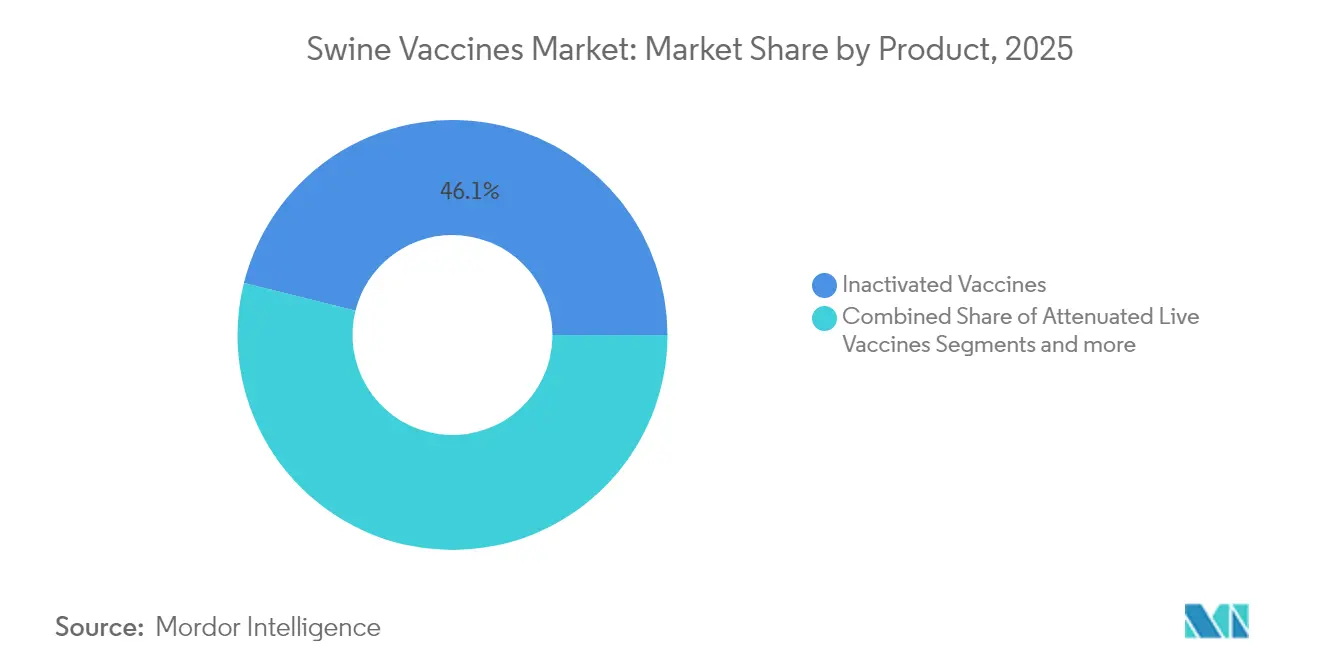

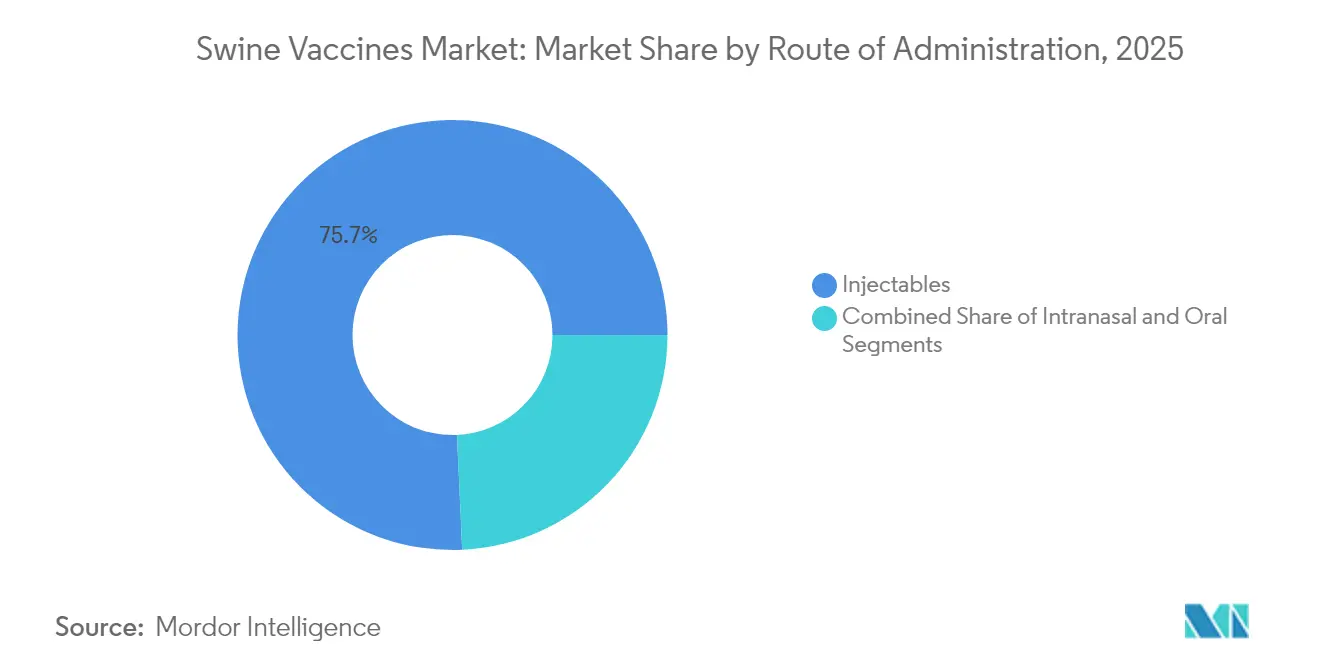

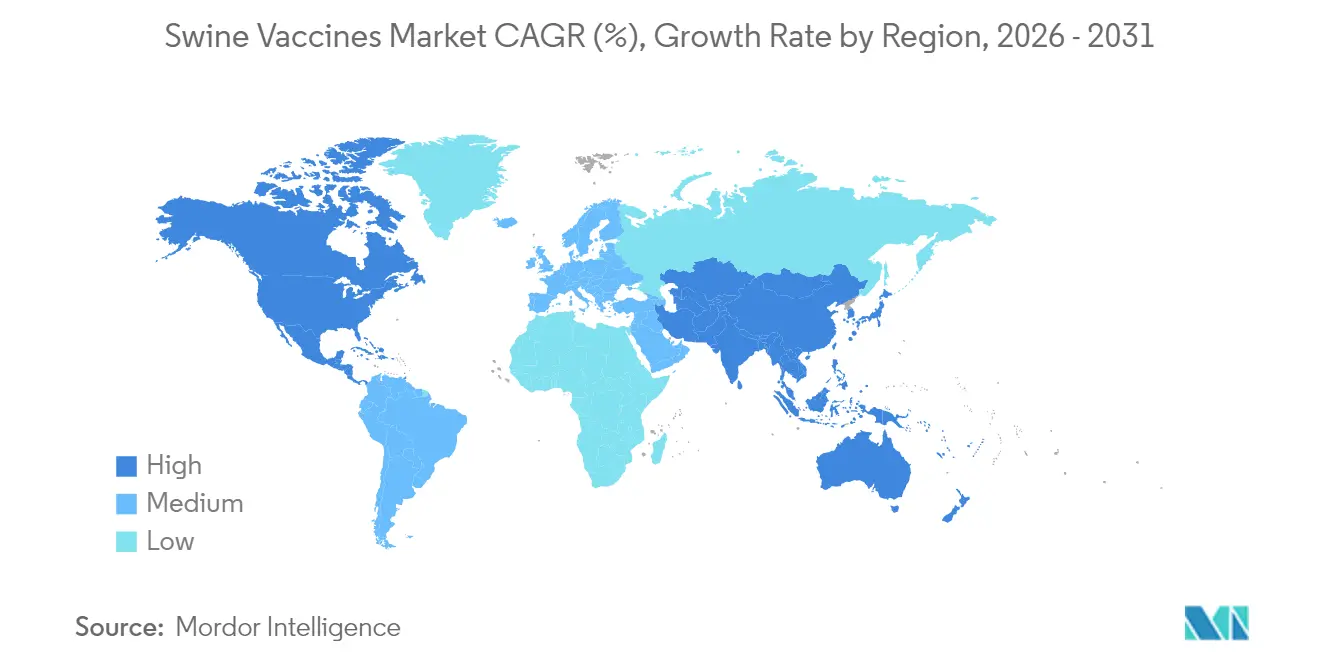

The swine vaccines market size was valued at USD 1.81 billion in 2025 and estimated to grow from USD 1.9 billion in 2026 to reach USD 2.43 billion by 2031, at a CAGR of 5.03% during the forecast period (2026-2031). Strong growth reflects a permanent shift from treating outbreaks to preventing them, as biosecurity rules tighten and producers protect herds that are more valuable than ever. Vaccination already offsets the USD 1.2 billion lost each year to porcine reproductive and respiratory syndrome, turning immunization from an optional cost into standard risk control. Technology disruption reinforces expansion: RNA particle platforms cut custom vaccine lead times to 12–16 weeks, while gene-edited pigs resistant to PRRS broaden the toolbox beyond traditional antigens. Regionally, North America holds 38.45% 2024 revenue on the back of advanced veterinary infrastructure, whereas Asia-Pacific posts the fastest CAGR at 6.23% as producers rebuild after African swine fever. Inactivated products stay ahead with 46.77% share, but recombinant lines grow at 6.02% as buyers favor safer DIVA-compliant options.

Key Report Takeaways

- By product type, inactivated formulations led with 46.12% of the swine vaccines market share in 2025; recombinant platforms are set to expand at a 5.88% CAGR through 2031.

- By disease type, classical swine fever accounted for 39.60% of the swine vaccines market size in 2025, while swine influenza is projected to climb at a 5.84% CAGR to 2031.

- By route of administration, injectable vaccines held 75.72% of 2025 revenue; intranasal delivery is forecast to grow at a 5.95% CAGR over 2026–2031.

- By geography, North America captured 38.02% revenue in 2025; Asia-Pacific is the fastest-growing region at 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Swine Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Initiatives Toward Swine-Flu Management & Higher Public Awareness | +0.8% | Global, with strongest impact in Asia-Pacific and Europe | Medium term (2-4 years) |

| Growth In R&D Outlays for Novel Vaccine Platforms | +1.2% | North America & EU leading, spill-over to APAC | Long term (≥ 4 years) |

| Escalating Global Pork Consumption & Intensifying Bio-Security Mandates | +1.0% | Global, particularly emerging markets | Medium term (2-4 years) |

| Rapid-Response Autogenous/RNA Platforms Shorten Time-To-Immunity | +0.9% | North America & EU core markets | Short term (≤ 2 years) |

| AI-Driven Herd Analytics Enable Precision Vaccination & Lower TCO | +0.7% | North America, early adoption in EU and Asia-Pacific | Long term (≥ 4 years) |

| Trade-Oriented Shift Toward DIVA-Compliant Vaccines | +0.6% | Global, with emphasis on export-oriented regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Initiatives Toward Swine-Flu Management & Higher Public Awareness

Mandatory health programs convert voluntary actions into structured prevention plans. The proposed U.S. Swine Health Improvement Plan creates national rules for tracking African swine fever and classical swine fever, rewarding farms that vaccinate [1]Animal and Plant Health Inspection Service, "APHIS Announces Proposed Rule to Establish U.S. Swine Health Improvement Plan as a Federal Regulatory Program," aphis.usda.gov. The Philippines issued 10,000 ASF doses under state supervision to test efficacy and build public trust. Taiwan achieved disease-free status for three major swine infections after years of coordinated campaigns, proving that clear government-industry alignment can lower routine vaccination needs. These successes reinforce positive feedback loops: as outbreaks fall, producers keep investing in vaccines to protect market access. In parallel, the incentive to comply grows because vaccinated herds earn smoother domestic movement and export clearance.

Growth in R&D Outlays for Novel Vaccine Platforms

Investment is shifting toward platforms that close gaps in speed and strain coverage. Merck earmarked USD 895 million for Kansas facilities that underpin its RNA particle line, Sequivity. The University of Pittsburgh’s trans-amplifying mRNA work shows similar immunity with far less active ingredient, lowering cost per dose. USDA grants fund self-amplifying mRNA projects against ASF and classical swine fever, signaling official support for next-gen approaches. Start-ups push the frontier too; Aptamer Group licensed nanobody adjuvants to boost swine responses. Collectively, rising R&D spend accelerates roll-out of vaccines that are easier to tailor and more economical to scale.

Escalating Global Pork Consumption & Intensifying Biosecurity Mandates

Higher protein demand collides with stronger safety rules, keeping the swine vaccines market on a persistent growth path. U.S. output is set to rise 1.7% in 2025 even as PRRS continues to drain USD 1.2 billion each year, affirming vaccination as insurance against lost revenue. Thailand’s pork consumption is climbing 3.91% annually, driving feed giants such as Cargill to boost capacity and prompting producers to vaccinate aggressively. European foot-and-mouth disease flare-ups forced immediate trade restrictions, highlighting how disease events turn preventive immunization into a compliance requirement. China’s post-ASF herd rebuild further underlines the link between vaccination and stable supply [2]United States Department of Agriculture, "Livestock and Products Annual," apps.fas.usda.gov. As markets liberalize, exporters rely on DIVA-compliant products that keep borders open, reinforcing demand.

Rapid-Response Autogenous/RNA Platforms Shorten Time-To-Immunity

New platforms tackle the core problem of viral evolution outpacing conventional development. Merck’s Sequivity delivers farm-specific vaccines in 12–16 weeks by using RNA particles matched to local pathogen sequences. USDA cleared the platform to pair with Microsol Diluvac Forte, extending protection length without adding months of lead time. Canada’s rules for autogenous biologics let veterinarians order custom batches for urgent threats. Self-amplifying mRNA models need less material yet trigger strong immunity, lowering production cost in emergency campaigns. Producers gain the agility to vaccinate sooner and more precisely, limiting losses during the critical early weeks of an outbreak.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cold-Chain Costs & Risk of Adverse Reactions | -0.9% | Global, particularly challenging in developing regions | Medium term (2-4 years) |

| Lengthy, Stringent Regulatory Approval Cycles | -0.7% | Global, with varying intensity by region | Long term (≥ 4 years) |

| Viral Genotype Drift Outpacing Vaccine Strain Updates | -0.8% | Global, with highest impact in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Budget Diversion To Antibiotic-Free Certification Programs | -0.5% | North America & EU primarily, expanding to export-oriented farms globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cold-Chain Costs & Risk of Adverse Reactions

Temperature-controlled logistics add sizeable expenses, particularly where power grids are unreliable. Freeze-drying research on African swine fever vaccine kept potency for 1 year at 4 °C, but adoption is pending broader field proof [3]Nallely Espinoza, "Lyophilization of ASFV vaccine candidate ASFV-G-ΔI177L offers long term stability," Scientific Reports, nature.com. Freeze-preventive cold boxes evaluated in Nepal solved freezing but became heavier and harder to transport over rough terrain. Vietnam’s smart-pig trials found vaccination bills between USD 4.7 and 9 per pig, with chilling and handling making up a major share. FAO manuals emphasize that broken cold chains undermine efficacy, leading to revaccination costs and liability concerns. These factors slow uptake among smallholders who operate on thin margins despite clear disease-control benefits.

Lengthy, Stringent Regulatory Approval Cycles

Comprehensive safety dossiers protect animal health but stretch timelines and costs. FDA biologics data from 2024 show multi-year paths from investigational studies to licensure, a hurdle that favors incumbents with deep regulatory teams. Merck’s PORCILIS PCV M Hyo ID cleared the European Medicines Agency only after an extended review covering multiple member states. The Philippines’ ASF pilot required government-run phases before wider use, delaying commercial roll-out even though initial results were positive. For exporters, USDA certification must also match rules in each importing country, adding another layer. Protracted approvals limit the agility needed to counter fast-moving viral threats and raise the capital bar for start-ups targeting the swine vaccines market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Recombinant Platforms Drive Innovation

In 2025, inactivated vaccines claimed 46.12% of the swine vaccines market share thanks to decades of field success and straightforward production. Recombinant lines post the fastest 5.88% CAGR to 2031 as buyers prize DIVA features that keep trade channels open. Attenuated live options remain in use for robust cellular immunity, though safety rules curtail volumes in high-density farms. Recombinant tools also ease updates when viral genotypes drift beyond current strain panels. The swine vaccines market size for recombinant products is positioned to accelerate as regulators gain experience with platform approvals.

The mRNA wave underscores this tilt toward precision. Sequivity’s RNA particles, ready in 12–16 weeks, contrast sharply with classical antigen culture timelines. PEDV spike-mRNA prototypes already trigger stronger responses than inactivated benchmarks. Meanwhile, oral and nanobody-based ideas broaden the “Others” bucket by tackling ease-of-use and stronger mucosal immunity. Together these shifts indicate that future sales will track how quickly each supplier can update antigens while keeping pricing inside producer budgets.

By Disease Type: Classical Swine Fever Dominance Faces Influenza Challenge

Classical swine fever vaccines contributed 39.60% of 2025 revenue as the disease carries heavy trade and mortality penalties. Live-attenuated FlagT4G shows how efficacy can coexist with DIVA tags, supporting eradication drives and verification testing. Swine influenza formulations grow at 5.84% CAGR because zoonotic risks and rapid viral drift push regular updates. Studies in China link vaccination pressure to faster H1N1 evolution, proving that constant surveillance and reformulation are essential.

Porcine parvovirus products deliver steady returns by safeguarding litter sizes, while circovirus vaccines shift to bivalent blends covering PCV2 and PCV3 variants. Research groups fast-track ASF candidates now that farm trials can replicate natural infection. The swine vaccines industry expects more disease-specific platforms that tailor immunity without compromising diagnostics.

By Route of Administration: Injectable Dominance Meets Intranasal Innovation

Injectable delivery accounted for 75.72% of 2025 sales, reflecting veterinarian familiarity and precise dosing. Intradermal products such as PORCILIS PCV M Hyo ID reduce needle volume and stress but keep the core injection model. The swine vaccines market size for intranasal routes is rising on a 5.95% trajectory as producers seek lower labor and stronger mucosal defense. Influenza-vectored intranasal trials show protection at the pathogen’s entry point.

Oral sprays and feed-based carriers serve niche mass-piglet programs, yet stability challenges limit their spread. Needle-free jet devices trim injury risk and enhance throughput. As AI monitoring becomes common, farms can match precise respiratory scores with intranasal boosters, raising the likelihood that alternative routes will chip away at injectable dominance.

Geography Analysis

North America generated 38.02% of 2025 revenue, supported by strict biosecurity and well-funded producers willing to pay for autogenous and RNA solutions. Federal plans such as the Swine Health Improvement Plan formalize traceability and vaccination compliance. Canada’s USD 57.5 million vaccine bank for foot-and-mouth disease signals public investment in rapid response. The swine vaccines market size in North America is also buoyed by a deep cold-chain and dense veterinary service network that ensures uptake.

Asia-Pacific registers the fastest 6.12% CAGR as the region rebuilds inventories after ASF. China’s restocking proves that coordinated vaccination, enhanced genetics, and modern barns stabilize supply. The Philippines runs supervised ASF vaccination using a Vietnamese-developed candidate, testing efficacy under field stress. Vietnam’s smart-farming push prices vaccination between USD 4.7 and 9 per pig and demonstrates willingness to pay when productivity gains are clear. Thailand’s rising pork appetite compounds momentum.

Europe, the Middle East and Africa, and South America offer varied prospects. Europe’s FMD cases in 2024 forced emergency vaccine orders that protected export licenses. The bloc’s rigorous approval process slows new entrants yet builds end-user confidence, supporting steady demand for premium recombinant products. Middle East and African markets struggle with cold-chain gaps, inviting thermostable formulations. South America’s export players adopt DIVA vaccines to secure market access, expanding volume while raising bar for compliance among domestic peers.

Regulatory Landscape

Regulation of swine vaccines continues to tighten around harmonized quality, safety, and traceability requirements, with global standards increasingly shaping national authorization and trade rules. In May 2025, the World Organisation for Animal Health (WOAH) adopted its first international standards for African swine fever (ASF) vaccines (Terrestrial Manual Chapter 3.9.1). This is now an anchor for how countries evaluate products that affect cross-border movement of pigs and pork under SPS frameworks.

In Europe, the EMA remains a key gatekeeper for veterinary biologicals under the EU veterinary medicines framework. In 2025, the agency highlighted a record level of activity, including 30 veterinary medicines recommended for marketing authorisation, among them 16 vaccines. The European Commission also updated disease-control-related use rules through Commission Delegated Regulation (EU) 2026/1073, while WOAH expanded ASF vaccine governance in May 2026 with guidance for field evaluation and post-vaccination monitoring. This shifts compliance from dossier-only reviews toward demonstrable real-world performance and surveillance readiness.

Competitive Landscape

The swine vaccines market shows moderate concentration. Zoetis, Merck Animal Health, and Boehringer Ingelheim anchor the top tier with broad portfolios and global distribution. Zoetis markets more than 300 animal-health products and maintains deep technical support, which shields share even as niche rivals appear. Merck leverages Sequivity to target precision needs and is scaling output through a USD 895 million Kansas build-out. Boehringer’s Dynamic Pig Health program integrates ten FLEX vaccines with gut-health brands to cover respiratory and enteric threats in one protocol.

Mid-tier firms broaden capabilities through acquisitions. Phibro spent USD 350 million on Zoetis’ medicated feed additive assets, pairing nutrition and vaccine lines to create bundled health solutions. Technology specialists focus on narrow breakthroughs: mRNA start-ups iterate immunogens in weeks, adjuvant innovators supply nanobody boosters, and software firms turn sensor data into vaccination-timing alerts. Larger incumbents respond by forming research pacts or buying these niche skills outright.

Competition now hinges on five levers: platform speed, strain-update agility, cold-chain simplicity, combined respiratory-enteric coverage, and digital integration. Firms that align all five command pricing power, while laggards face commoditization in basic inactivated products. The swine vaccines market continues to reward scale economies along with differentiated science.

Swine Vaccines Industry Leaders

-

Merck & Co., Inc.

-

Elanco

-

Boehringer Ingelheim International GmbH

-

Zoetis Inc.

-

Ceva Sante Animale

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

ASF-specific and trade-sensitive prevention needs are creating whitespace for vaccines that combine field-usable monitoring with internationally recognized standards. WOAH's 2025 ASF vaccine standards and its May 2026 guidance on field evaluation and post-vaccination monitoring help countries structure national programs, and they give suppliers a clearer basis to plan products and data packages that support movement controls and export continuity. That framework supports demand for DIVA-aligned and surveillance-friendly solutions.

In 2026, commercial actions show portfolio building around differentiated swine indications and cross-border supply. In June 2026, Ceva Animal Health acquired Aquilón CyL S.L., adding control of Europes only commercial swine dysentery vaccine (Brachyspira hyodysenteriae) and reinforcing the strategic value of narrow, high-impact bacterial indications alongside viral portfolios. In South Korea, APQA export item approvals and subsequent export permission for ASF vaccines, including Suishot ASF-X and PROVAC ASF, offer a concrete route for manufacturers to serve ASF-affected destinations such as Vietnam and the Philippines. EU regulatory maintenance actions also continue, including the April 2026 marketing authorisation amendment for Zoetis Suvaxyn PRRS MLV, which reflects ongoing lifecycle management for core respiratory and reproductive vaccines. Technology opportunity remains tied to faster strain updates and operational simplicity, alongside continued industry focus on platform approaches (RNA/DNA and LNP delivery in published 2026 pig studies) and ready-to-use combination products that reduce on-farm handling steps.

Recent Industry Developments

- June 2026: Ceva Animal Health acquired Spanish biotechnology firm Aquilón CyL S.L., adding control of Europes only commercial swine dysentery vaccine targeting Brachyspira hyodysenteriae. The acquisition expands Cevas swine portfolio into a high-consequence enteric bacterial indication and strengthens its positioning in Europe, where differentiated products can support protocol placement.

- December 2025: Merck Animal Health announced commercial availability of CIRCUMVENT CL, a ready-to-use vaccine for pigs three weeks and older against Porcine Circovirus types 2a and 2d and Lawsonia intracellularis. The RTU format reduces mixing steps on farm, supporting faster and more standardized vaccination workflows in large production systems.

- March 2024: Merck Animal Health received USDA licensure for SEQUIVITY with Microsol Diluvac Forte adjuvant as a prescription vaccine for use in gilts and sows. The approval reinforced the regulatory footing of RNA particle technology in swine, supporting customized vaccine approaches designed around herd-specific sequences and program needs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from vaccines used to prevent and control infectious diseases in pigs, counted at the point of sale into veterinary channels and farm users across major swine producing regions.

Scope exclusions: We exclude swine therapeutics (antibiotics and antiparasitics), diagnostics, feed additives, and vaccination services that are billed separately from vaccine product sales.

Segmentation Overview

-

By Product

- Inactivated Vaccines

- Attenuated Live Vaccines

- Recombinant Vaccines

- Others

-

By Disease Type

- Classical Swine Fever (CSF)

- Porcine Parvovirus

- Swine Influenza

- Porcine Circovirus (PCV)

- Others

-

By Route of Administration

- Injectables

- Intranasal

- Oral

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping swine populations and production economics to understand where vaccine demand can realistically sit. We reviewed public datasets such as FAOSTAT, WOAH animal health updates, USDA livestock and veterinary services publications, and Eurostat agriculture statistics, along with open scientific literature on swine disease epidemiology and vaccination programs.

To connect those demand signals to revenue, we relied on accessible sources like national animal health authority guidance, vaccine label and regulatory information, and import or export trade codes where they are used for veterinary biologicals. We also referenced company filings and investor presentations to sanity check exposure to the swine portfolio, and a paid subscription focused on company financials and news helped track launches, recalls, and production changes. These desk sources are illustrative only, and we used many other public and paid references to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work focused on validating how farms and veterinarians choose vaccines based on disease risk, pig age group, and delivery route, and then how pricing changes by region and product format. We interviewed a mix of vaccine manufacturers, distributors, large integrated producers, swine veterinarians, and academic or lab experts across APAC, EMEA, and the Americas to close gaps left by published data and to test our key assumptions before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 47% |

| Mid tier: 52% | Functional/Unit leaders: 39% | EMEA: 31% |

| Smaller Players: 15% | Managers: 49% | Americas: 22% |

Market-Sizing & Forecasting

Sizing used a top-down and bottom-up approach, where swine inventory and production by region are converted into an addressable vaccination pool using disease incidence, program intensity, and coverage rates, which are then translated into value using typical dosing schedules and average selling prices by vaccine type and route. The totals were checked with selective bottom-up approximations, such as rolling up sampled supplier revenues where disclosed, distributor channel checks, and volume times ASP builds for a few high-use disease areas, and then adjusted when the two views did not align.

Key model inputs included country and regional swine population, share of commercial versus backyard production, prevalence and outbreak cadence for common swine diseases, dosing frequency by production stage, route of administration mix (injectable versus oral or intranasal), and price progression by vaccine platform (inactivated, live attenuated, and recombinant). When local data was thin, gaps were handled by applying proxy uptake rates from comparable swine producing countries and then validating those proxies with interview feedback.

For the forecast, scenario analysis was used so the outlook can reflect shifts in herd rebuilding after disease events, changes in biosecurity and vaccination compliance, and regulatory or supply disruptions. Variables were projected using recent historical patterns and expert expectations, and then the scenarios were reconciled back to a single base case for the final series.

Data Validation & Update Cycle

Outputs were validated through multiple checks, including comparing implied spend per head against independent production indicators and reviewing whether regional splits match known swine output concentration. Outliers, sudden step-changes, and price or volume jumps were investigated, and follow-up conversations were triggered when a key assumption could not be defended with at least two supporting signals.

Before sign-off, the model and write-up pass through multi-step analyst review so the logic, units, and currency treatment stay consistent from country level builds to global totals. Reports are refreshed annually, and interim updates are made when material events occur such as major outbreaks, new approvals, or manufacturing constraints. Right before delivery, we run a final refresh pass to reflect the latest public releases and confirmed expert inputs.

Mordor Intelligence's Swine Vaccines Market Size Measured Against Other Published Estimates

Published market values for swine vaccines often do not match because the counted scope and the way volumes are translated into revenue can differ, even when the same disease areas are discussed. We also see gaps due to base year choice, currency timing, and whether the estimate is built from animal population signals or from a narrower set of reported sales.

The main gap comes from whether the estimate includes only preventive vaccine product revenues used in pigs, or whether adjacent animal health items are blended in to make the total look larger, and then how disease-driven demand swings are handled year to year. Some sources assume steady, uniform vaccine uptake and a simple price curve, while Mordor Intelligence ties dosing intensity and ASPs to route of administration, vaccine platform mix, and post-outbreak herd rebuilding patterns that were validated through primary discussions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.90 B (2026) | |

| Trade Publisher A | USD 1.53 B (2024) | Uses an earlier base year and a manufacturer-consumption framing, and it does not clearly show how dosing schedules and route mix are converted into value across regions. |

| Industry Media B | USD 1.60 B (2022) | Applies a longer-range projection with broad assumptions on adoption and pricing, and the scope description is high level, which makes it harder to separate vaccine-only revenue from nearby animal health items. |

Taken together, the spread mainly reflects differences in what is counted as swine vaccine revenue, plus how uptake and pricing are updated when disease pressure and herd size change. By keeping the model anchored to measurable herd and disease indicators, and then cross-checking with channel feedback, our estimate stays traceable to clear inputs that can be revisited as market conditions move.

Key Questions Answered in the Report

What is the current size of the swine vaccines market?

The market stands at USD 1.9 billion in 2026 and is projected to grow steadily to USD 2.43 billion by 2031.

Which region leads swine vaccine revenue today?

North America holds 38.02% of global revenue owing to advanced veterinary infrastructure and strict biosecurity rules.

Which product segment is growing the fastest?

Recombinant vaccines record the highest 5.88% CAGR through 2031 as producers adopt safer, DIVA-ready platforms.

Why are intranasal vaccines gaining attention?

They stimulate local respiratory immunity, cut labor time, and are forecast to expand at 5.95% CAGR over 2026–2031.

What are the main restraints affecting market growth?

High cold-chain costs in developing regions and lengthy regulatory approvals together shave roughly 1.6 percentage points off potential CAGR.

How are rapid-response RNA platforms changing the landscape?

Technologies such as Sequivity cut vaccine customization cycles to 12–16 weeks, enabling quicker containment of new viral strains.

Page last updated on: