Veterinary Vaccine Adjuvants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

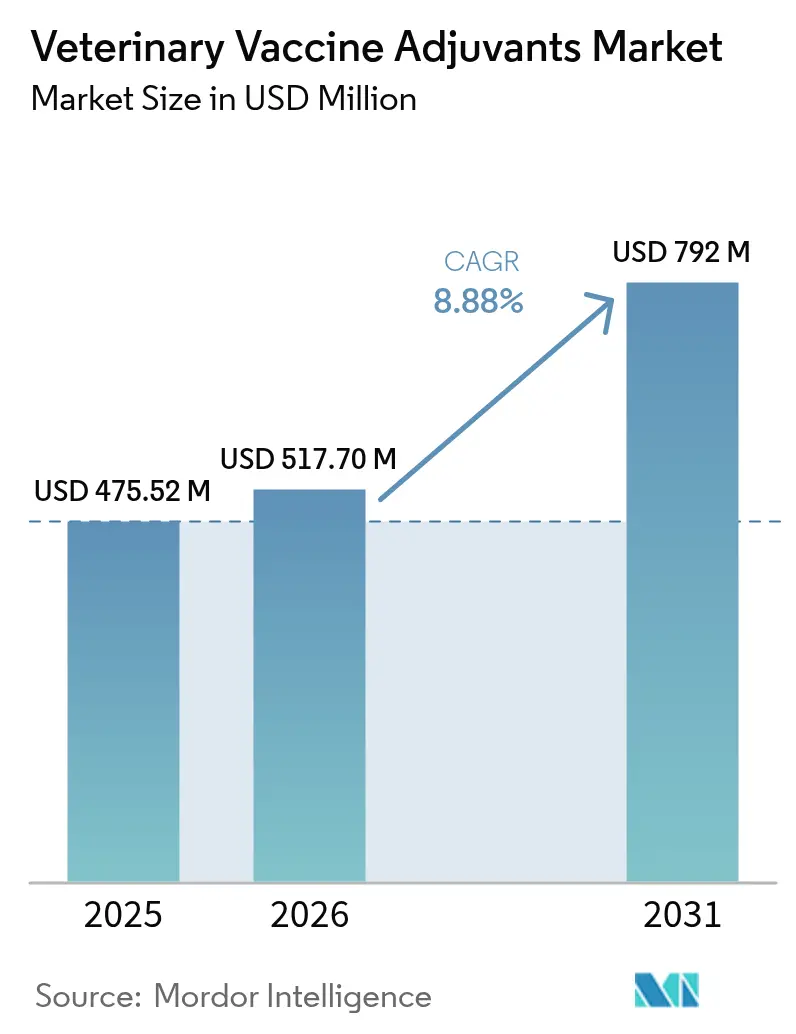

| Market Size (2026) | USD 517.70 Million |

| Market Size (2031) | USD 792 Million |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

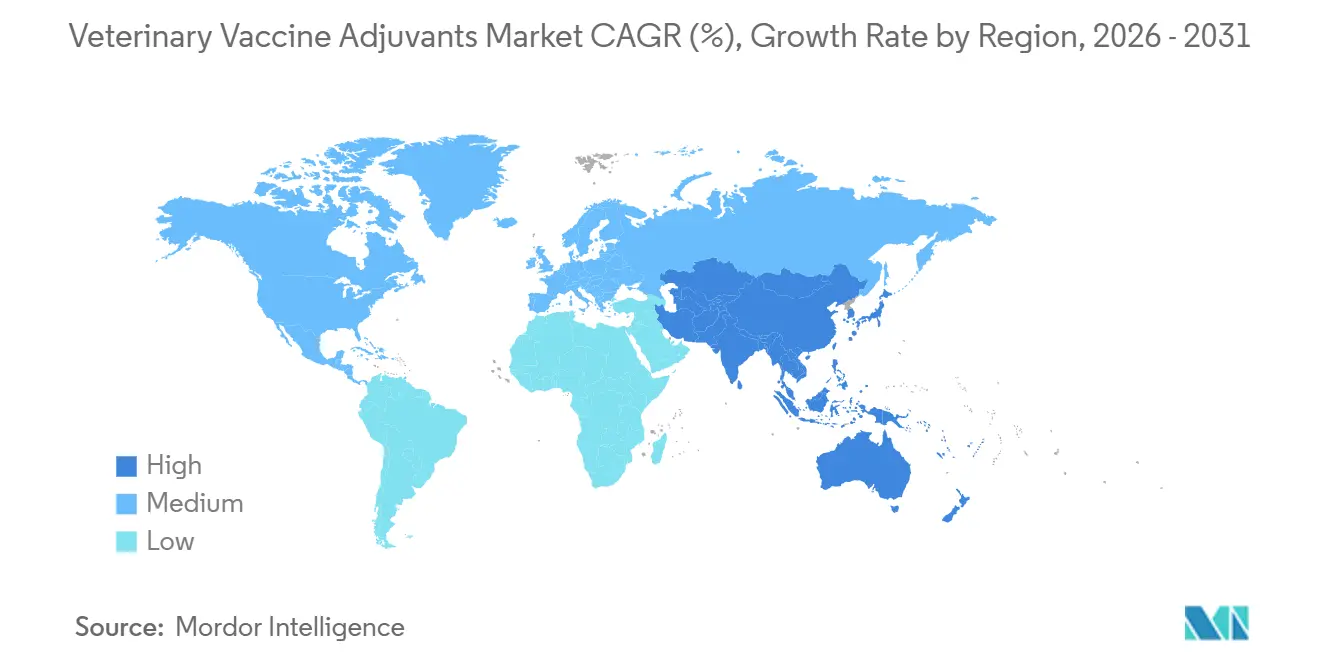

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Vaccine Adjuvants Market Analysis by Mordor Intelligence

The veterinary vaccine adjuvants market size was valued at USD 475.52 million in 2025 and estimated to grow from USD 517.73 million in 2026 to reach USD 792.08 million by 2031, at a CAGR of 8.88% during the forecast period (2026-2031). Demand accelerates as emerging livestock diseases expose the limits of alum-only formulations, governments intensify One-Health surveillance, and Asia-Pacific subsidies favor oil-emulsion technologies. Simultaneously, the veterinary vaccine adjuvants market faces a 24- to 36-month regulatory lag between pre-clinical proof and commercial launch, compressing innovation cycles while demand rises. Market leaders allocate record capital to emulsion capacity, yet squalene supply shocks, safety scrutiny, and temperature-stable needs shape investment toward nanoparticle and polymer systems. The convergence of these forces positions the veterinary vaccine adjuvants market for sustained, innovation-led expansion, particularly in companion-animal and aquaculture niches.

Key Report Takeaways

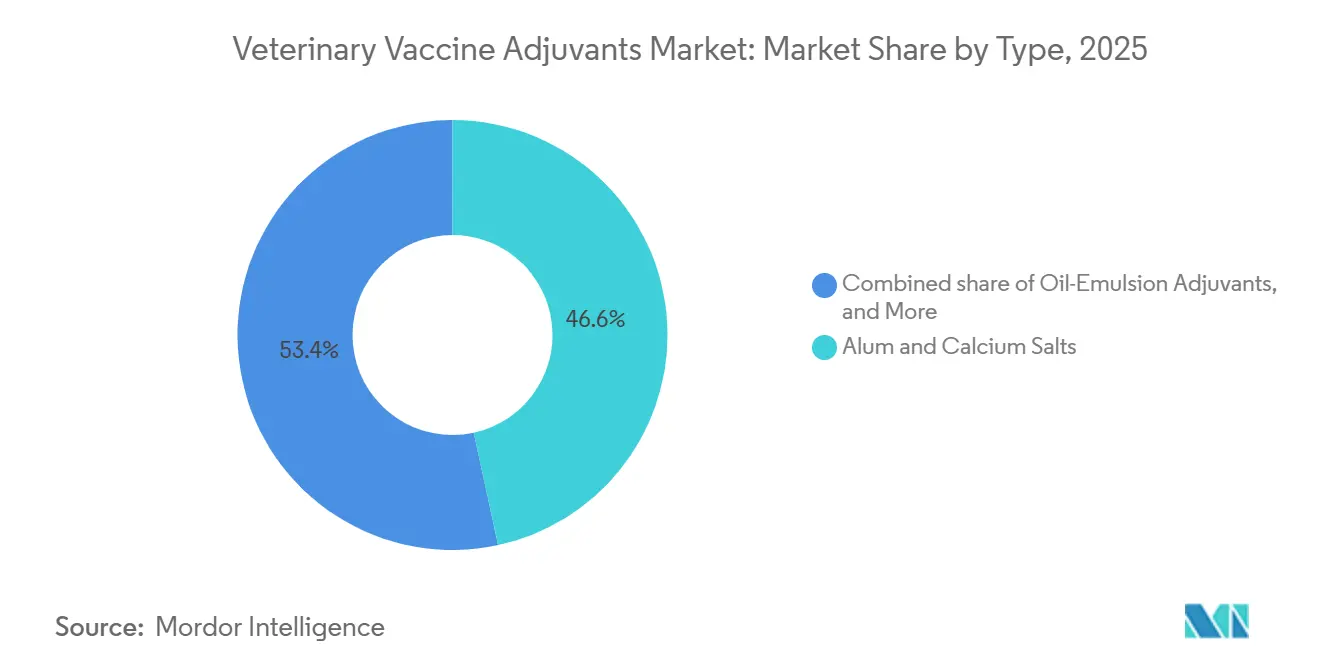

- By type, alum and calcium salts commanded 46.55% of the veterinary vaccine adjuvants market share in 2025, while particulate and nanoparticle systems are projected to expand at a 10.85% CAGR through 2031.

- By route, oral delivery accounted for 49.53% of 2025 revenue, but intranasal platforms are forecast to grow at a 9.75% CAGR through 2031.

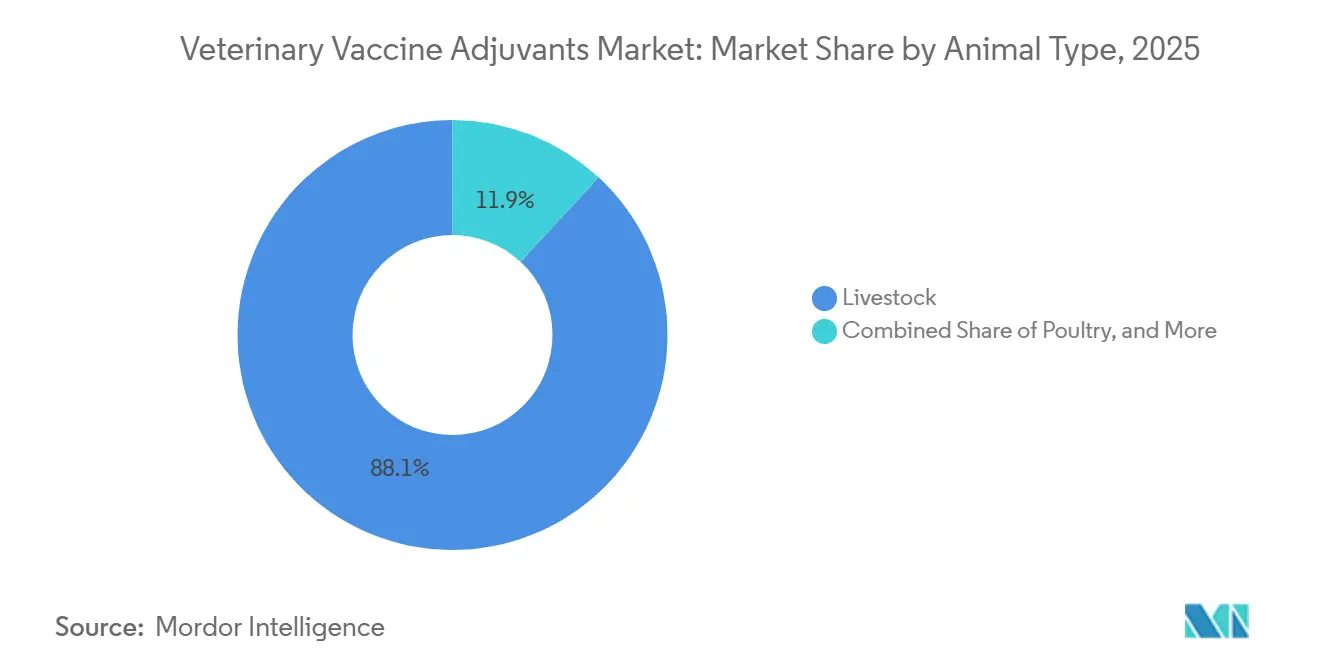

- By animal type, livestock dominated with an 88.15% share in 2025, whereas companion animals are advancing at a 9.82% CAGR to 2031.

- Geographically, North America led with 37.21% of 2025 revenue, yet Asia-Pacific is expected to expand at 9.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Vaccine Adjuvants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Global Animal Protein Consumption | +1.8% | Global, with strongest growth in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Rising Incidence of Emerging & Re-Emerging Livestock Diseases | +2.1% | Global, concentrated in North America (H5N1), Europe (FMD), Asia (ASF) | Short term (≤ 2 years) |

| Strengthening Government Immunization Mandates & Subsidies | +1.5% | North America, Europe, India | Medium term (2-4 years) |

| Growing Focus on One-Health & Zoonosis Prevention | +1.2% | Global, led by North America and Europe regulatory frameworks | Medium term (2-4 years) |

| Shift Toward High-Value Subunit & mRNA Veterinary Vaccines | +1.4% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| ESG-Driven Transition to Plant-Derived Squalene & Sustainable Emulsifiers | +0.9% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Global Animal Protein Consumption

Global meat output is projected to climb by 12% between 2024 and 2034, boosting stocking densities and reliance on vaccines. India’s 5.2 billion-bird poultry flock now adheres to mandatory Newcastle disease immunization, and Montanide ISA 71 VG cut mortality by 18 percentage points versus alum in large broiler houses[1]Organisation for Economic Co-operation and Development, “OECD-FAO Agricultural Outlook 2025-2034,” OECD.ORG. Southeast Asian aquaculture producers adopt chitosan-adjuvanted immersion vaccines, raising efficacy to 70% from 45%, underscoring the adjuvant's value despite regulatory fragmentation.

Rising Incidence of Emerging and Re-Emerging Livestock Diseases

The 2024 H5N1 incursion into 129 U.S. dairy herds triggered USD 98 million in emergency vaccine procurement after alum-based shots failed to curb shedding. Oil-emulsion plus TLR7/8 agonist combinations lowered nasal viral titers by 2.3 log10 in experimental cattle, while Europe’s 2025 foot-and-mouth flare-up compelled purchase of 4.5 million oil-adjuvanted doses. Persistent African swine fever outbreaks are accelerating the development of saponin-adjuvanted subunit vaccines now in Phase II trials.

Strengthening Government Immunization Mandates and Subsidies

USDA’s modernized surveillance network requires adjuvants that meet VICH stability criteria, disqualifying non-adjuvanted biologics from federal tenders. India subsidizes 75% of vaccine costs for smallholders if formulations deliver immunity beyond six months, favoring oil-emulsion and polymer systems. The EU Animal Health Law obliges member states to hold strategic reserves, harmonizes adjuvant dossiers, and shortens time-to-market.

Growing Focus on One-Health & Zoonosis Prevention

The U.S. National One Health Framework mandates human-safety assessment for food-animal adjuvants, elevating interest in biodegradable PLGA nanoparticles and plant-derived saponins. Japan now requires disclosure of adjuvant composition to monitor allergen exposure in farm workers, while the WHO calls for adjuvanted veterinary vaccines to curb zoonotic spillover.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse Reactions & Safety Concerns with Oil-Based Adjuvants | -1.1% | Europe, North America | Short term (≤ 2 years) |

| Complex & Fragmented Regulatory Approval Pathways | -0.8% | Asia-Pacific, Latin America | Medium term (2-4 years) |

| Volatile Pharmaceutical-Grade Squalene Supply | -0.7% | Europe, North America | Short term (≤ 2 years) |

| GMP Scale-Up Bottlenecks for Nanoparticle & Polymer Adjuvants | -0.6% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse Reactions and Safety Concerns with Oil-Based Adjuvants

EMA surveillance recorded 127 granuloma cases in cattle vaccinated with Montanide ISA 206 during 2024, slicing carcass value by EUR 45-60 per head and driving producers toward alum despite shorter protection[2]European Medicines Agency, “Post-Market Surveillance Guidance 2025,” EMA.EUROPA.EU. Companion-animal veterinarians cite a 14% sterile abscess rate in dogs receiving oil-adjuvanted leptospirosis vaccines, versus 2% with alum-adjuvanted vaccines, reshaping purchasing decisions.

Complex and Fragmented Regulatory Approval Pathways

FDA-CVM can green-light conditional licenses within 12 months, whereas China demands 36-month field trials, forcing multinationals to maintain region-specific adjuvant variants and inflating costs by up to 22%[3]U.S. Food and Drug Administration Center for Veterinary Medicine, “Warning Letter on Carbomer Quality,” FDA.GOV . Brazil’s requirement for local-breed toxicity testing delayed an oil-adjuvanted FMD vaccine by 14 months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Alum Anchors Volume, Nanoparticles Capture Premium Tiers

Alum and calcium salts held 46.55% of 2025 revenue, supported by USD 0.08-0.12 per-dose costs and a robust safety record. Particulate and nanoparticle systems are forecast to advance at a 10.85% CAGR, supported by companion-animal demand for formulations with minimal injection-site reactions. Oil-emulsion products such as Montanide and Emulsigen remain essential for inactivated viral vaccines that require strong cell-mediated immunity. Saponin platforms like Quil-A and the emerging Matrix-M add premium options, while pathogen-derived CpG and MPLA adjuvants remain niche due to manufacturing cost. Combination approaches—alum plus TLR agonists are emerging fastest, propelled by Ingelvac CircoFLEX’s double-digit growth. Polymer systems, however, must overcome endotoxin contamination incidents that led to FDA warnings in 2024. Venture-backed startups are funneling capital into thermostable virus-like particles, hinting at future cost parity with alum if scale hurdles are overcome.

By Route of Administration: Oral Dominance Masks Intranasal Disruption

Oral delivery commanded 49.53% share in 2025, led by wildlife rabies baits and drinking-water poultry vaccines that often dispense with conventional adjuvants. Yet chitosan micro-particles improved Newcastle disease seroconversion to 68% from 52%, illustrating incremental value. Intramuscular and subcutaneous routes remain preferred for precise dosing, but intranasal platforms are sprinting at a 9.75% CAGR as producers pursue needle-free labor savings. Bovilis Intranasal RSP Live secured 12% of the EUR 85 million European calf-vaccine market within 18 months, validating mucosal immunity economics. Intradermal jet injectors in aquaculture are scaling throughput tenfold, while dual-route formulations under development could let producers toggle between oral and intranasal pathways, shaving 3-5 percentage points from oral share by 2031.

By Animal Type: Livestock Lock-In Versus Companion-Animal Premiumization

Livestock absorbed 88.15% of demand in 2025, reflecting global herd scale and cost pressure that lock in alum and basic emulsions. Cattle programs fighting FMD and brucellosis drive volume, whereas swine vaccines pivot to combination adjuvants that cut handling time. Poultry segments increasingly adopt oil emulsions for breeder flocks requiring extended immunity. The veterinary vaccine adjuvants market for companion animals is smaller but expanding at a 9.82% CAGR, with canine vaccines adopting premium polymers that reduce pain at USD 25-45 per dose. Feline formulations shift toward recombinant antigens amid sarcoma concerns, while equine owners pay top dollar, USD 38 per shot, for carbomer-enhanced West Nile protection. Aquaculture, though the smallest, is set for acceleration as oil-emulsion immersion vaccines trim white-spot mortality by 62% in Pacific white shrimp, strengthening the segment’s contribution to the veterinary vaccine adjuvants industry.

Geography Analysis

North America led with 37.21% of 2025 revenue, underpinned by USDA’s rapid-response procurement and FDA-CVM’s conditional-license pathway that cleared 14 novel adjuvants during 2024-2025. The H5N1 emergency validated domestic manufacturing: Zoetis and Elanco expanded plants with in-house emulsion suites, insulating the supply chain. Canada’s research universities punch above their weight in nanoparticle science, while Mexico’s privatizing vaccine market offers a USD 55 million window for thermostable adjuvants suited to warm regions.

Asia-Pacific, forecast to grow at 9.89% CAGR, is on track to surpass North America by 2029. China’s aquaculture subsidy reimburses 60% of oil-emulsion vaccines, adding 22 million doses in its first year. India’s National Livestock Mission funds adjuvant procurement and cold-chain upgrades, thereby expanding the veterinary vaccine adjuvant market at the state level. Japan and South Korea approve liposome-adjuvanted canine vaccines, signaling premiumization, while Australia’s A$350 million Zoetis plant expansion cements regional export capacity.

Europe maintains a significant share but faces higher compliance costs after EMA’s 2025 surveillance rule for oil-emulsions. Emergency FMD outbreaks in Bulgaria and Romania sparked a rapid draw-down of 4.5 million oil-adjuvanted doses, spotlighting cold-chain gaps in Eastern states. Ceva’s new French plant, ISO-14001 certified, anchors the continent’s shift toward plant-derived squalene. South America streamlines dossiers Brazil cut approval time to 18 months for adjuvants vetted in the U.S. or EU potentially lifting imports by USD 20 million by 2027. The Middle East and Africa show the greatest unmet need; thermostable carbomer vaccines stored at 25 °C posted 74% efficacy in Kenyan trials, 22 percentage points above alum, hinting at latent demand once affordability improves.

Competitive Landscape

The veterinary vaccine adjuvants market remains moderately fragmented. The five integrated leaders, Zoetis, Boehringer Ingelheim, Elanco, Merck Animal Health, and Ceva, control the bulk of revenue, leveraging vertical plants that blend proprietary emulsions and nanoparticles. Zoetis’s USD 590 million Georgia build-out includes squalene purification that shields margins from supply shocks. Boehringer Ingelheim’s 2023 aquaculture portfolio buy unlocked cross-species deployment of carbomer technology. Mid-tier specialists such as SEPPIC, Croda, and Phibro capture margin in custom formulations but face feedstock volatility and stricter quality audits.

Disruptors focus on thermostable and needle-free solutions. VaxLiant raised USD 28 million in 2025 to commercialize a virus-like particle adjuvant stable at 37 °C for 1 year, potentially unlocking the 18-country African market. Phibro screened 1,200 saponin derivatives, producing three leads now in pre-clinical swine trials. Patent filings for TLR agonists hit 47 during 2024-2025, yet costs above USD 2 per dose constrain livestock uptake. Regulatory agility becomes decisive: Merck secured a May 2025 conditional license for a nanoparticle-adjuvanted bovine respiratory vaccine, seizing an 8-10% share of the USD 180 million U.S. calf segment before rivals could file.

Consolidation pressures will intensify as integrated firms acquire adjuvant innovators to secure inputs and compress time-to-market. The 2024 Zoetis purchase of Jurox’s adjuvant platform foreshadows this trajectory, while sustainable squalene sourcing emerges as a differentiator in tenders and ESG scorecards.

Veterinary Vaccine Adjuvants Industry Leaders

Merck Animal Health

Boehringer Ingelheim Vetmedica

Ceva Santé Animale

Elanco Animal Health

Zoetis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Merck Animal Health committed USD 895 million to expand its De Soto, Kansas, site with three fill-finish lines and a plant-based squalene suite, aiming for a 2027 start-up

- November 2024: Ceva opened a 7,000 m² French vaccine facility featuring ISO 14001-certified adjuvant blending and sourcing 100% plant-derived squalene by 2027.

Global Veterinary Vaccine Adjuvants Market Report Scope

As per the report's scope, vaccine adjuvants are substances added to vaccines to enhance the body’s immune response to an antigen. They work by stimulating the immune system, prolonging antigen exposure, or directing the type of immune response. Common adjuvants include aluminum salts, emulsions, and newer molecules designed to improve vaccine efficacy, reduce antigen dose, and provide longer‑lasting protection.

The veterinary vaccine adjuvants market segmentation includes type, route of administration, animal type, and geography. By type, the market is segmented into alum and calcium salts, oil emulsion adjuvants, liposomes and archaeosomes, nanoparticles and microparticles, and other types. By route of administration, the market is segmented into oral, subcutaneous, intramuscular, and other routes. By animal type, the market is segmented into livestock, Poultry, companion animals, and aquaculture. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Alum & Calcium Salts |

| Oil-Emulsion Adjuvants (W/O, O/W, W/O/W) |

| Saponin-based (Quil A, QS-21, flavonoid) |

| Pathogen-derived (MPLA, CpG, TLR agonists) |

| Particulate / Nanoparticle (liposomes, Nano-11, VLPs) |

| Polymer & Carbomer Systems |

| Combination / Next-Gen Emulsions |

| Other Types |

| Intramuscular |

| Subcutaneous |

| Intradermal |

| Intranasal / Mucosal |

| Oral |

| Livestock | Cattle & Buffalo |

| Sheep & Goat | |

| Swine | |

| Poultry | |

| Companion Animals | Canine |

| Feline | |

| Equine | |

| Aquaculture |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Alum & Calcium Salts | |

| Oil-Emulsion Adjuvants (W/O, O/W, W/O/W) | ||

| Saponin-based (Quil A, QS-21, flavonoid) | ||

| Pathogen-derived (MPLA, CpG, TLR agonists) | ||

| Particulate / Nanoparticle (liposomes, Nano-11, VLPs) | ||

| Polymer & Carbomer Systems | ||

| Combination / Next-Gen Emulsions | ||

| Other Types | ||

| By Route of Administration | Intramuscular | |

| Subcutaneous | ||

| Intradermal | ||

| Intranasal / Mucosal | ||

| Oral | ||

| By Animal Type | Livestock | Cattle & Buffalo |

| Sheep & Goat | ||

| Swine | ||

| Poultry | ||

| Companion Animals | Canine | |

| Feline | ||

| Equine | ||

| Aquaculture | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the veterinary vaccine adjuvants market expected to grow between 2026 and 2031?

It is projected to expand at an 8.88% CAGR, moving from USD 517.73 million in 2026 to USD 792.08 million by 2031.

Which adjuvant type currently holds the largest share?

Alum and calcium salts led with 46.55% of 2025 revenue because of low cost and a long safety record.

Which route of administration is growing the quickest?

Intranasal platforms are forecast to rise at a 9.75% CAGR as producers seek needle-free, labor-saving options.

How are sustainability trends affecting oil-emulsion adjuvants?

EU and California bans on shark-derived squalene have pushed suppliers toward plant-based alternatives, raising costs until production scales.

Which companies dominate the competitive landscape?

Zoetis, Boehringer Ingelheim, Elanco, Merck Animal Health, and Ceva collectively command about two-thirds of global revenue.

Page last updated on: