Rotogravure Printing Inks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

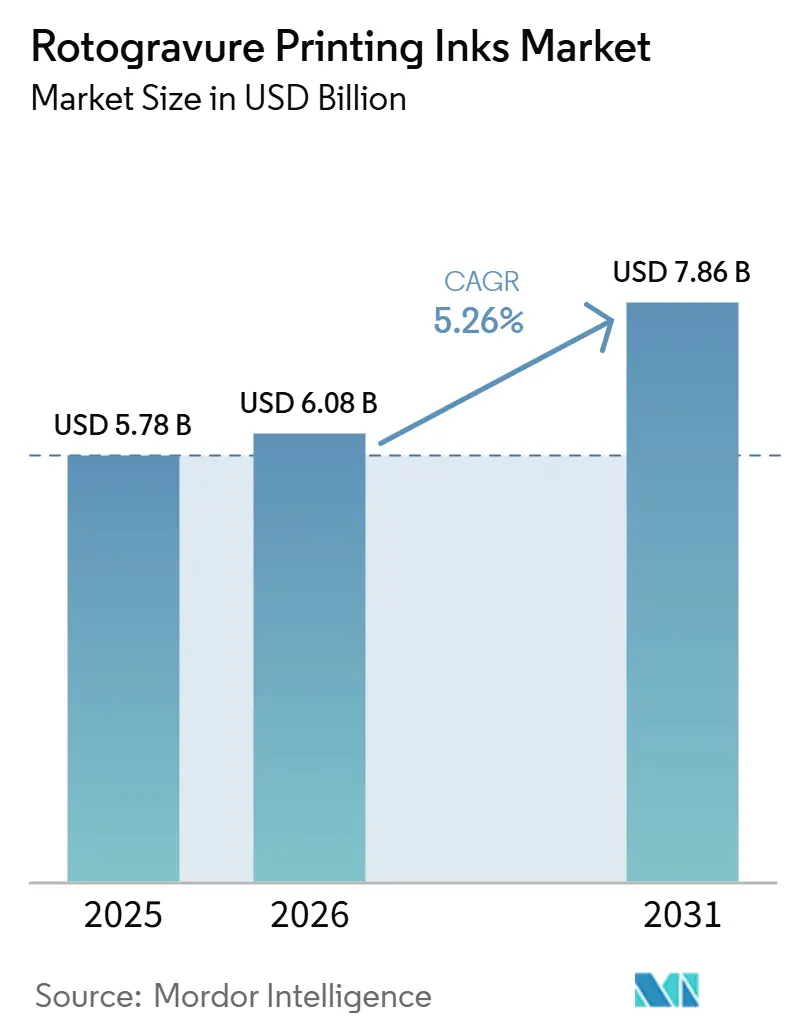

| Market Size (2026) | USD 6.08 Billion |

| Market Size (2031) | USD 7.86 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rotogravure Printing Inks Market Analysis by Mordor Intelligence

The Rotogravure Printing Inks Market size was valued at USD 5.78 billion in 2025 and is estimated to grow from USD 6.08 billion in 2026 to reach USD 7.86 billion by 2031, at a CAGR of 5.26% during the forecast period (2026-2031). Brand owners continue to value the process for its unmatched press speeds, capability to deliver eight-to-ten color fidelity on flexible packaging, and proven compatibility with emerging mono-material film structures. Nitrocellulose-based formulations represented 36.13% of global resin demand in 2025, even as Europe enforces stricter VOC thresholds, while solvent-based chemistries dominated the technology mix at 68.92% in 2025. Electron-beam and LED-UV systems are growing at a 6.04% CAGR through 2031, driven by pharmaceutical serialization requirements in the United States and European Union, which favor zero-migration curing. Asia-Pacific remains the primary growth driver, supported by Siegwerk’s March 2026 acquisition of Hi-Tech Inks India, which leads to a regional share of 46.83% in 2025 and highlights growing consolidation around low-migration, de-inkable portfolios. The rise of e-commerce adds urgency, as corrugate-heavy distribution chains now involve seven to ten hand-offs, emphasizing the need for abrasion-resistant prints that gravure achieves at 400 m/min line speeds.

Key Report Takeaways

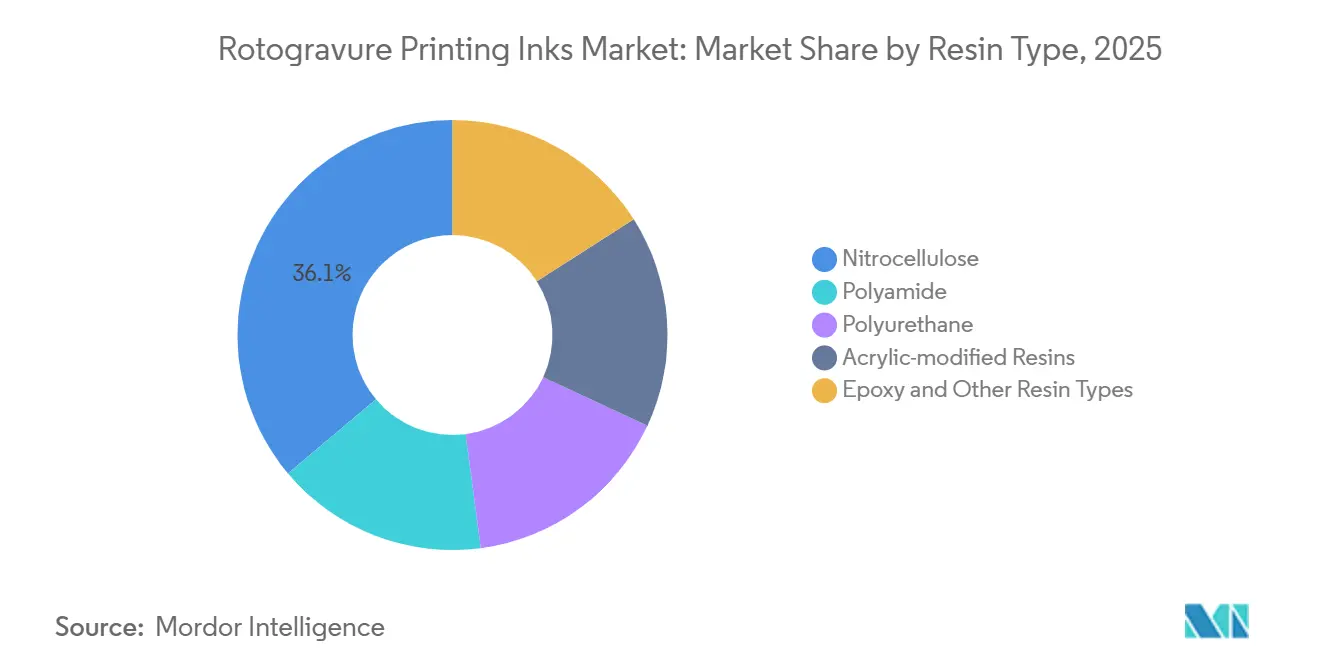

- By resin type, nitrocellulose commanded 36.13% of the rotogravure printing inks market share in 2025, while polyurethane is projected to advance at a 5.89% CAGR through 2031.

- By technology, solvent-based gravure inks commanded 68.92% of the rotogravure printing inks market share in 2025, while EB/UV-curable gravure inks are projected to advance at a 6.04% CAGR through 2031.

- By application, flexible packaging commanded 62.44% of the rotogravure printing inks market share in 2025, while gift wrap and decorative films are projected to advance at a 5.67% CAGR through 2031.

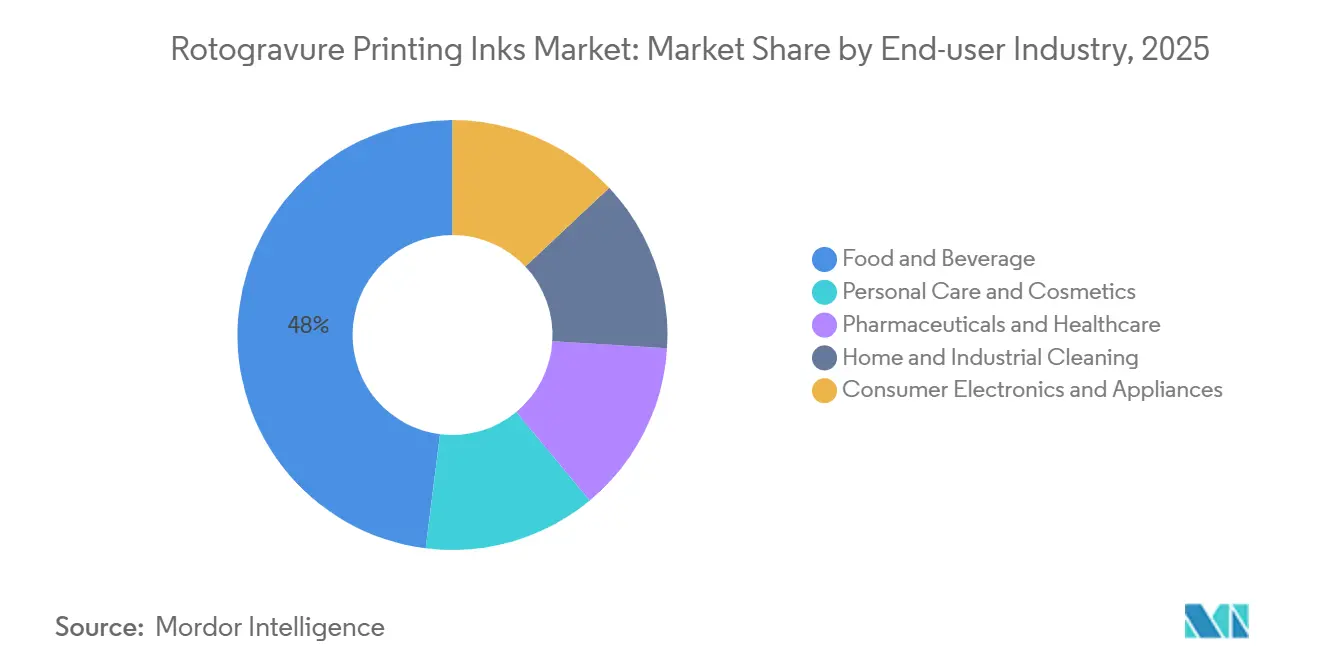

- By end-user industry, food and beverage commanded 48.02% of the rotogravure printing inks market share in 2025, while pharmaceuticals and healthcare is projected to advance at a 6.18% CAGR through 2031.

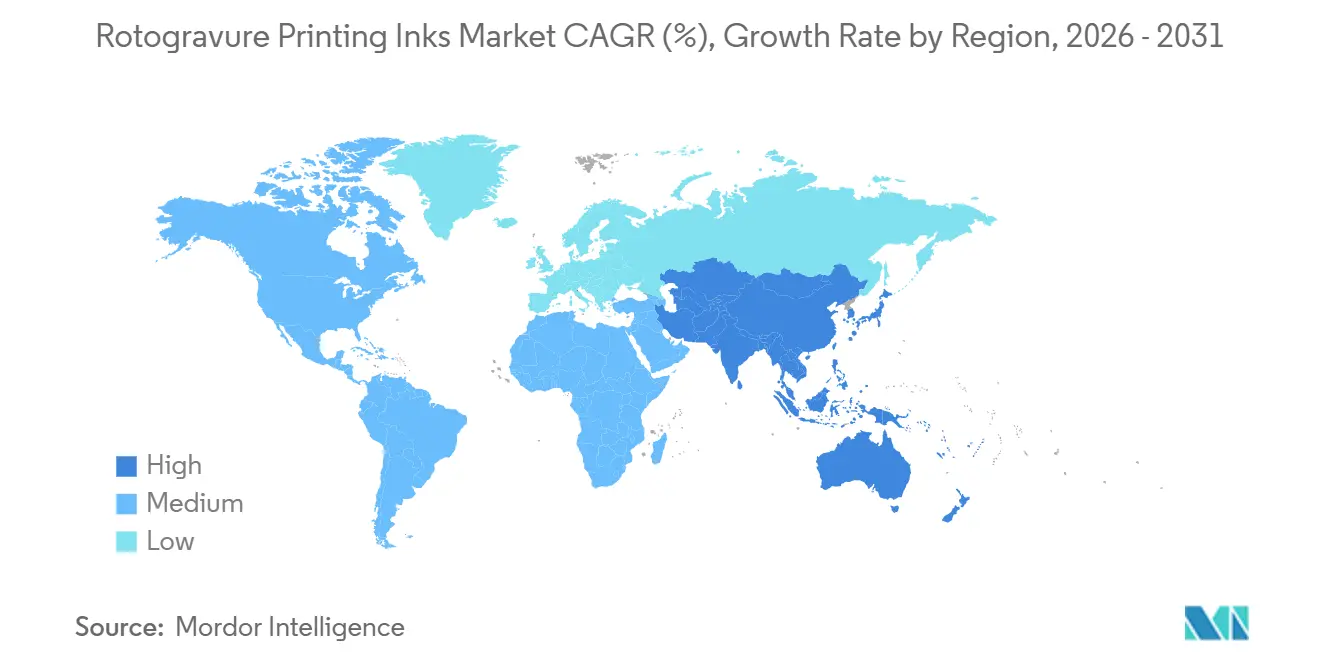

- By geography, Asia-Pacific commanded 46.83% of the rotogravure printing inks market share in 2025 and is projected to advance at a 6.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rotogravure Printing Inks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-speed printing in flexible packaging | +1.2% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| FMCG and food-beverage packaging growth in emerging markets | +1.4% | APAC core (India, China, ASEAN), spill-over to Latin America and Middle-East | Long term (≥ 4 years) |

| Brand-owner push for premium graphics on recyclable mono-material films | +0.9% | Europe and North America, early adoption in APAC urban centers | Medium term (2-4 years) |

| Expansion of e-commerce requiring long-run durable prints | +0.8% | Global, led by North America and APAC e-commerce hubs | Short term (≤ 2 years) |

| Bio-based polyurethane dispersions enabling less than 5% VOC gravure inks | +0.6% | Europe (REACH compliance), North America (EPA), spreading to APAC | Long term (≥ 4 years) |

| Embedded RFID/printed-electronics gravure inks for supply-chain traceability | +0.4% | North America and Europe pharmaceutical/retail, pilot projects in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Speed Printing in Flexible Packaging

Flexible packaging converters now operate central-impression gravure presses at sustained speeds of 400 m/min, a 25% increase compared to 2020, reducing lead times from two weeks to seventy-two hours in fast-moving consumer goods segments. The viscosity stability required for such speeds has shifted preferences toward polyurethane and acrylic-modified binders that resist solvent loss during printing. Asia-Pacific's flexible packaging expenditure reached USD 90.12 billion in 2026 and is projected to grow to USD 124.77 billion by 2035, driven by urbanizing populations in India, Indonesia, and Vietnam[1]Government of India, “Retail Growth Statistics 2025,” india.gov.in. Toyo Ink’s November 2025 plan to expand its Gujarat liquid-ink plant by 1.5 times reflects supplier confidence in the continued importance of high-throughput gravure printing in the region.

FMCG and Food–Beverage Packaging Growth in Emerging Markets

Food and beverage applications accounted for 48.02% of global ink volume in 2025 and are expected to maintain a similar share as per-capita packaged food consumption increases in India and Southeast Asia. In India alone, supermarket chains added 12,000 outlets in 2025, each requiring tamper-evident, high-definition graphics. Gravure printing offers cost advantages over flexography for production runs exceeding 100,000 impressions. Siegwerk’s INR 350 crore investment in September 2025 focuses on metallic-effect varnishes, which command a 15–20% price premium in the premium confectionery segment.

Brand-Owner Push for Premium Graphics on Recyclable Mono-Material Films

Mono-material polyethylene (PE) and polypropylene (PP) laminates accounted for 18% of flexible packaging substrates in 2025, driven by extended producer responsibility (EPR) fees on multilayer films in France and Germany. Gravure inks are now required to achieve at least 85% de-inkability in alkaline wash tests while maintaining eight-color fidelity. Sun Chemical’s nitrocellulose-free ink line, which meets these standards, received CEFLEX endorsement six months after its launch. Higher-cost polyurethane and acrylic resins are replacing nitrocellulose, enabling suppliers to meet procurement requirements from companies like Unilever and Nestlé, which mandate RecyClass certification.

Expansion of E-Commerce Requiring Long-Run Durable Prints

Packages pass through seven to ten mechanical touchpoints in online distribution, driving the adoption of solvent-based gravure systems with high cross-link density to resist scuffing on high-speed sorters processing up to 50,000 parcels per hour. Sun Chemical’s April 2025 launch of the SunPak PowerPace platform allows converters to overlay QR codes via inkjet on a gravure base without surface-energy conflicts, enabling mass customization while maintaining throughput efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening VOC and hazardous-solvent regulations | -0.7% | Europe (REACH, IED), North America (EPA NESHAP), spreading to APAC | Medium term (2-4 years) |

| Feedstock-price volatility (resins, pigments, solvents) | -0.5% | Global, acute in regions dependent on imported MEK/MIBK | Short term (≤ 2 years) |

| Rapid migration to digital inkjet for short runs | -0.4% | North America and Europe label segments, limited APAC impact | Medium term (2-4 years) |

| Photoinitiator toxicology scrutiny in UV/EB systems | -0.3% | Europe (EFSA migration limits), North America (FDA), early signals in Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening VOC and Hazardous-Solvent Regulations

The EU Industrial Emissions Directive has set a 50 mg/m3 ceiling for new gravure lines, while REACH Annex XVII restricts benzophenone levels to below 0.6 mg/kg in finished articles. Similar regulations in the United States under EPA guidelines are pushing converters toward water-based or electron-beam (EB) curable chemistries unless they invest USD 0.5–2 million in oxidizers. Flint Group’s EcoVadis Gold-certified nitrocellulose-free product suite entered 2025 tenders with RecyClass pre-clearance, enabling the company to respond to brand-owner requests for proposals (RFPs) in four weeks, compared to twelve weeks for regional competitors.

Photoinitiator Toxicology Scrutiny in UV/EB Systems

In 2024, the FDA flagged 106 photoinitiators, including 36 high-priority substances, while the European Food Safety Authority (EFSA) set a tolerable daily intake (TDI) of 0.03 mg/kg for benzophenone. Migration studies in cereal packaging have shown levels exceeding these limits[2]Food and Drug Administration, “Photoinitiator Hazard Identification Report 2024,” fda.gov. Although electron-beam curing eliminates the need for photoinitiators, the technology costs USD 300,000–800,000 per unit and reduces throughput by 10–15%. As a result, adoption remains concentrated in pharmaceutical blister packaging, where zero-migration curing meets stringent regulatory requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Nitrocellulose Dominance Erodes Under Recyclability Pressure

Nitrocellulose retained 36.13% of 2025 revenue. Polyurethane, supported by bio-based grades, is projected to grow at a CAGR of 5.89% through 2031. Polyamide continues to be preferred for high-speed publication printing, although growth in this application remains slow. Acrylic-modified systems maintain niche demand in decorative laminates due to their UV resistance, while epoxy binders are critical for antimicrobial functional layers.

Carbon pricing exceeding EUR 80 per ton is expected to eliminate the cost difference between castor-oil polyols and petrochemical alternatives by 2029. Toyo Ink’s toluene-free Neemrana plant highlights supplier efforts to reduce solvent exposure while ensuring adhesion on corona-treated films.

By Technology: Solvent-Based Systems Yield Ground to EB/UV Platforms

Solvent-based gravure inks accounted for 68.92% of demand in 2025, driven by their compatibility with 400 m/min press speeds on PE and PP substrates. Water-based inks are gaining traction, supported by DIC’s RePOS de-inkable line, which passed RecyClass wash tests at 60°C. EB/UV-curable gravure inks are anticipated to grow at a CAGR of 6.04% through 2031, driven by drug serialization requirements.

Hybrid workflows are becoming more common, with converters using high-solids solvent inks for opaque whites and overlaying CMYK with LED-UV inks, such as SunCure Advance ECO, which reduces photoinitiator mass by 40%. However, high capital costs remain a barrier to broader adoption of EB technology, limiting its use to high-margin applications like blister packs and cosmetics.

By Application: Flexible Packaging Anchors Revenue; Gift Wrap Leads Growth

Flexible packaging contributed 62.44% of tonnage in 2025, supported by demand for stand-up pouches and flow wraps requiring ten-color graphics. Labels and wrappers hold a mid-teens market share but face competition from digital printing for SKUs under 10,000 meters. Publication printing remains significant in Asia but is stagnant elsewhere. Gift wrap and decorative films are expected to grow at a CAGR of 5.67% through 2031, driven by luxury brands adopting holographic and tactile effects.

Sustainability regulations require inks on mono-material films to achieve at least 85% alkaline wash de-linkability, a standard met by Sun Chemical’s nitrocellulose-free system, which has received CEFLEX approval. Decorative laminates benefit from the outdoor durability of acrylic-modified resins, maintaining operating margins of 15-20%.

By End-user Industry: Pharmaceuticals and Healthcare Outpace Food and Beverage

The food and beverage industry held a 48.02% market share in 2025 and is expected to remain stable as packaged food consumption rises in developing markets. Pharmaceuticals and healthcare are projected to grow at the fastest CAGR of 6.18% through 2031, driven by EU FMD and U.S. DSCSA regulations requiring machine-readable codes on individual units. The personal care and cosmetics segment maintains a mid-teens share, with demand for metallic and pearlescent inks that command 20-30% price premiums.

Counterfeit drugs, estimated by WHO to represent a USD 432 billion global issue, are driving demand for gravure-printed RFID antennas for unit-level tracking. Toyo Ink’s aTIC-India center, launched in February 2026, underscores the focus on low-migration formulations for pharmaceutical applications.

Geography Analysis

Asia-Pacific absorbed 46.83% of 2025 demand and is projected to grow at a CAGR of 6.37% through 2031. Siegwerk’s acquisition of Hi-Tech Inks in March 2026 increased its market share in India to over 20%, combining expertise in low-migration technology with local solvent production. While China’s growth moderates, it is shifting toward premium packaging for chocolate, coffee, and cosmetics using DIC’s RePOS inks. Japan and South Korea show slow growth but continue adopting EB technology for blister packs. ASEAN nations are expected to add 18,000 supermarkets in 2025, driving demand for sachets and pouches.

In North America, U.S. converters face rising MEK prices due to tariff reforms, but e-commerce abrasion requirements sustain demand for solvent-based gravure inks. Canada and Mexico benefit from near-shoring trends, with cross-border just-in-time supply chains supporting automotive harness production.

In Europe, stringent IED regulations are accelerating the adoption of water-based and EB technologies. In Germany, France, and the United Kingdom, primarily in pharmaceutical blister packs and premium food wraps requires RecyClass certification. Russia’s market is contracting due to supply constraints, while Poland and the Czech Republic are emerging as secondary hubs for publication printing.

South America’s demand is driven by Brazilian coffee, confectionery, and personal care packaging. The Middle-East and Africa remain nascent markets, but WHO-backed serialization pilots for antimalarials are creating demand for RFID-enabled gravure sleeves produced by INVENTRA.

Competitive Landscape

The top five suppliers, including Siegwerk, Flint Group, Sun Chemical, Hubergroup, and SAKATA INX, controlled majority of the rotogravure printing inks market in 2025, competing on low-migration intellectual property, cylinder-engraving integration, and global shade consistency. DIC’s packaging segment grew 5.1% year-over-year to ¥569.8 billion (USD 3.8 billion) in FY 2024, with operating income increasing by 52.8% following RePOS RecyClass and CEFLEX certifications.

Siegwerk’s acquisition of Hi-Tech Inks has positioned it as India’s largest gravure ink supplier, combining metallic-effect technology with cost-effective solvent products. Sun Chemical leads in photoinitiator reduction through its SunCure Advance ECO line, while Flint Group leverages its EcoVadis Gold status to secure premium food packaging contracts. Toyo Ink’s Neemrana plant demonstrates large-scale solvent elimination, providing a competitive advantage under upcoming Indian VOC regulations.

Innovation is focused on functional inks with embedded oxygen barriers or antimicrobial properties, reducing lamination costs by USD 0.02–0.04 per square meter. BASF and Humanchem supply bio-based polyurethane dispersions, enabling converters to produce in-house and challenging traditional ink formulators. Technical services, such as GPI Gravure’s laser engraving and APC’s reduced cylinder lead times, differentiate upstream partners supporting hybrid gravure-digital workflows.

Rotogravure Printing Inks Industry Leaders

Flint Group

Sakata INX Corporation

Siegwerk Druckfarben AG & Co. KGaA

Sun Chemical

hubergroup Deutschland GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Siegwerk Druckfarben AG & Co. KGaA signed a definitive agreement to acquire Hi-Tech Inks, a leading Indian manufacturer of flexographic and gravure printing inks. The acquisition strengthened Siegwerk’s position in the rapidly expanding Indian flexible packaging market.

- July 2025: The Chemours Company introduced a new specialty low-abrasion grade of Ti-Pure titanium dioxide pigment, specifically developed to enhance the formulation and performance of printing inks. This new grade of Ti-Pure pigment (TS-4657) was chloride-processed and designed for use in water- and solvent-based inks for flexographic, digital, and gravure printing applications in labels and packaging.

Global Rotogravure Printing Inks Market Report Scope

Rotogravure printing ink is a specialized, low-viscosity liquid ink designed for high-speed printing applications. It provides fast drying times and strong adhesion to substrates such as flexible packaging films (BOPP, PET), paper, and foil. These inks are primarily solvent-based for industrial use but are also available in water-based or UV-curable formulations. They are often developed to deliver high color strength, vibrancy, and heat resistance.

The Rotogravure Printing Inks Market is segmented into resin type, technology, application, end-user industry, and geography. By resin type, the market is segmented into nitrocellulose, polyamide, polyurethane, acrylic-modified resins, epoxy, and other resin types. By technology, the market is segmented into solvent-based gravure inks, water-based gravure inks, and EB/UV-curable gravure inks. By application, the market is segmented into flexible packaging, labels and wrappers, publication printing, gift wrap and decorative films, and decorative laminates and wallpapers. By end-user industry, the market is segmented into food and beverage, personal care and cosmetics, pharmaceuticals and healthcare, home and industrial cleaning, and consumer electronics and appliances. The report also covers the market size and forecasts for rotogravure printing inks in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Nitrocellulose |

| Polyamide |

| Polyurethane |

| Acrylic-modified Resins |

| Epoxy and Other Resin Types |

| Solvent-based Gravure Inks |

| Water-based Gravure Inks |

| EB/UV-curable Gravure Inks |

| Flexible Packaging |

| Labels and Wrappers |

| Publication Printing |

| Gift Wrap and Decorative Films |

| Decorative Laminates and Wallpapers |

| Food and Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals and Healthcare |

| Home and Industrial Cleaning |

| Consumer Electronics and Appliances |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Nitrocellulose | |

| Polyamide | ||

| Polyurethane | ||

| Acrylic-modified Resins | ||

| Epoxy and Other Resin Types | ||

| By Technology | Solvent-based Gravure Inks | |

| Water-based Gravure Inks | ||

| EB/UV-curable Gravure Inks | ||

| By Application | Flexible Packaging | |

| Labels and Wrappers | ||

| Publication Printing | ||

| Gift Wrap and Decorative Films | ||

| Decorative Laminates and Wallpapers | ||

| By End-user Industry | Food and Beverage | |

| Personal Care and Cosmetics | ||

| Pharmaceuticals and Healthcare | ||

| Home and Industrial Cleaning | ||

| Consumer Electronics and Appliances | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the rotogravure printing inks market?

The rotogravure printing inks market stands at USD 6.08 billion in 2026 and is forecast to reach USD 7.86 billion by 2031 on a 5.26% CAGR trajectory.

Which application drives the highest revenue in 2025?

Flexible packaging accounts for 62.44% of 2025 usage, benefiting from 400 m min-1 press speeds and e-commerce durability requirements.

Which technology is growing fastest through 2031?

EB/UV-curable gravure inks are expanding at 6.04% CAGR through 2031 because they eliminate photo initiators and meet zero-migration mandates.

Why is Asia-Pacific so important to gravure suppliers?

Asia-Pacific holds 46.83% of demand in 2025 and is rising at a 6.37% CAGR through 2031 as India, Indonesia, and Vietnam adopt sachet and pouch formats in modern retail.

Page last updated on: