Robotic Vision Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.56 Billion |

| Market Size (2031) | USD 5.56 Billion |

| Growth Rate (2026 - 2031) | 9.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

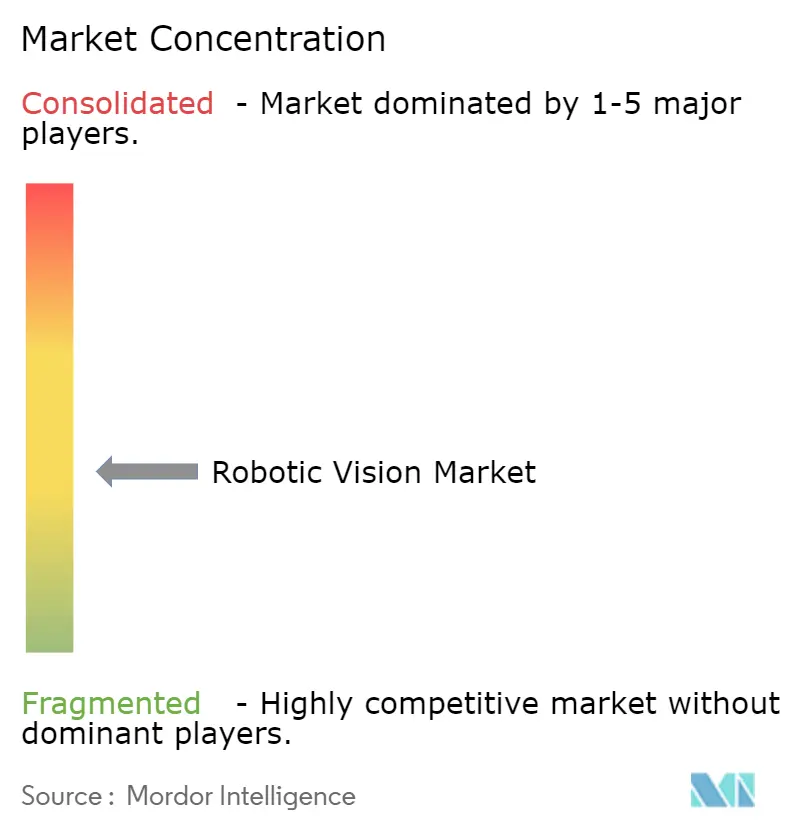

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Vision Market Analysis by Mordor Intelligence

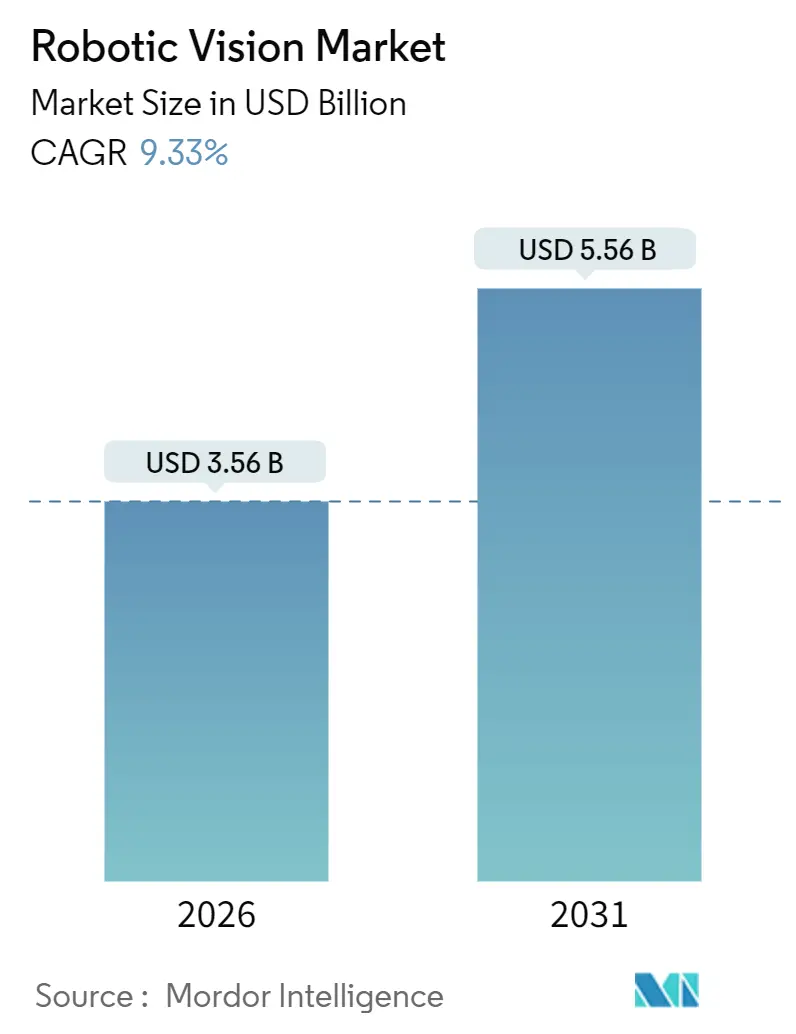

The global robotic vision market size reached USD 3.56 billion in 2026 and is forecast to climb to USD 5.56 billion by 2031, advancing at a 9.33% CAGR. Heightened demand for adaptive, zero-defect manufacturing is steering investment from legacy 2D inspection toward AI-enabled 3D vision that handles complex geometries and non-rigid parts. Regional data-sovereignty laws in the European Union and China have accelerated the shift to on-device inference, trimming cycle latency below 10 milliseconds and enabling real-time bin-picking and defect classification. Collaborative-robot adoption in Southeast Asia, Eastern Europe, and Mexico is rising faster than traditional industrial-robot rollouts as governments subsidize automation to counter labor shortages. Vision-as-a-service subscriptions are lowering capital barriers for small and medium manufacturers, while edge-AI chips from Qualcomm, Intel, and NVIDIA boost throughput without costly cloud infrastructure.

Key Report Takeaways

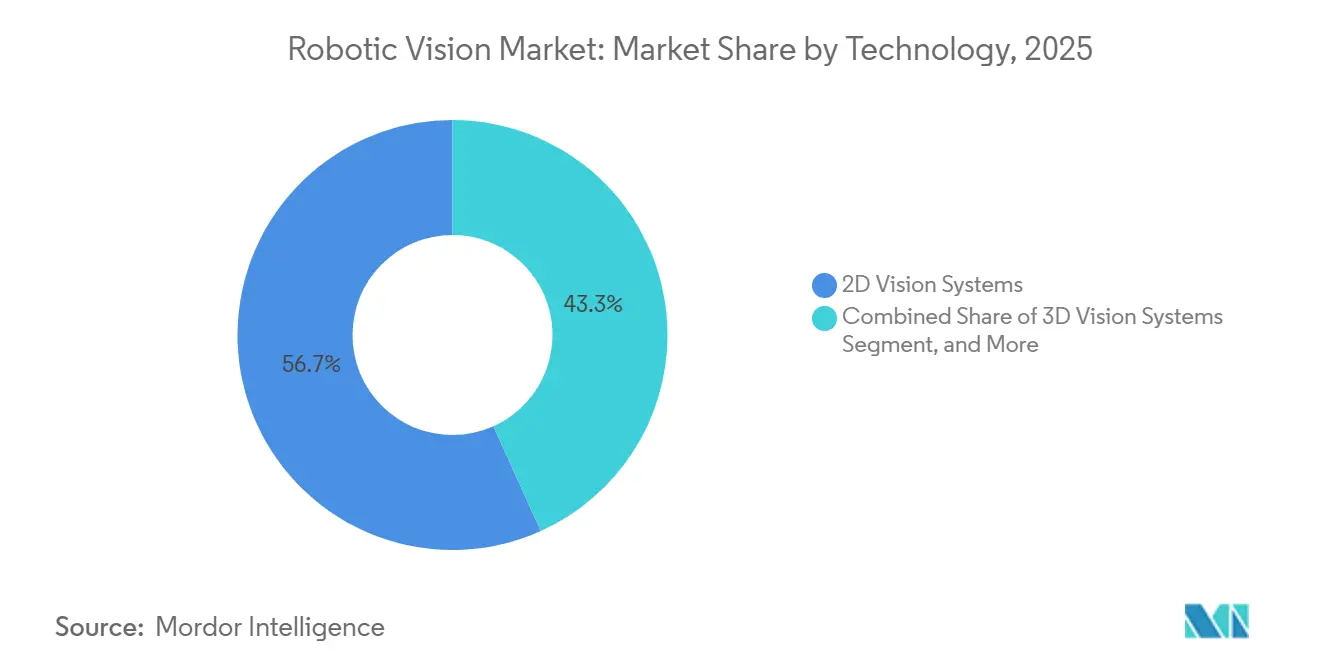

- By technology, 2D vision systems led the robotic vision market with 56.73% market share in 2025; 3D vision systems are projected to grow at a 10.32% CAGR through 2031.

- By component, hardware accounted for 66.89% of revenue in 2025, while software is expected to expand at a 9.92% CAGR to 2031.

- By robot type, industrial robots captured 49.73% share of the robotic vision market size in 2025; collaborative robots are forecast to post a 10.41% CAGR through 2031.

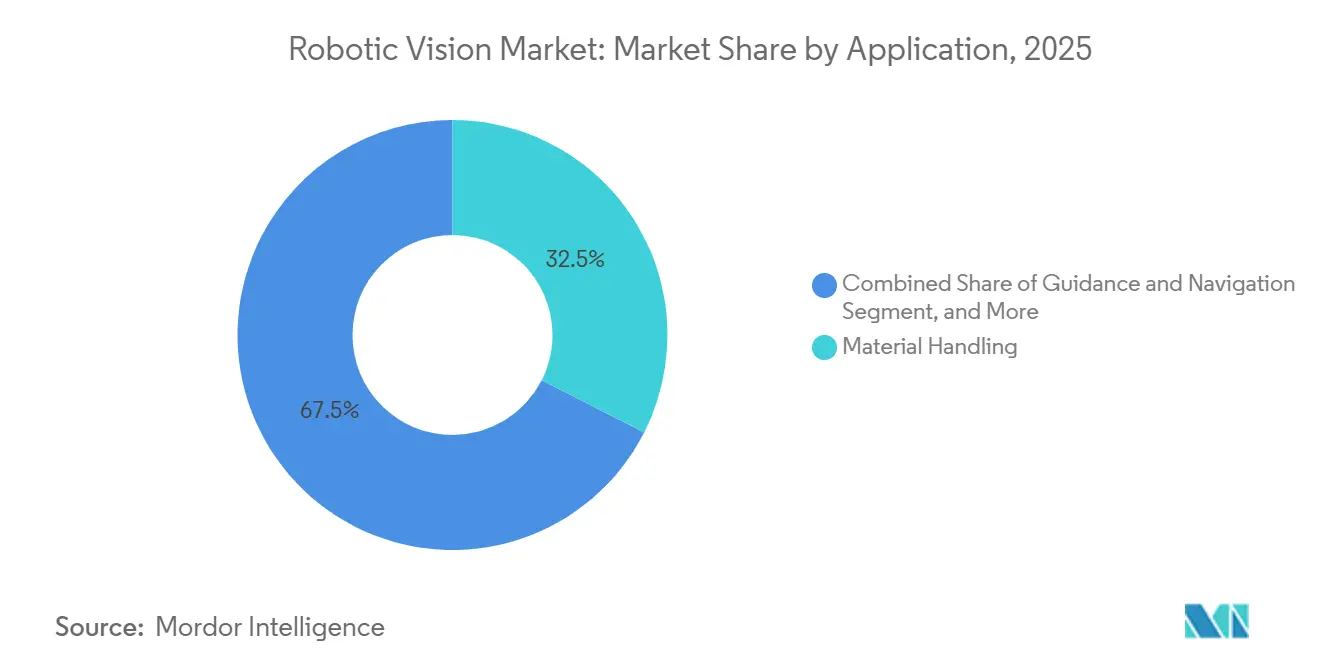

- By application, material handling held 32.49% of the robotic vision market in 2025, and guidance and navigation is advancing at an 11.21% CAGR through 2031.

- By end-user, automotive retained 35.83% revenue share in 2025, whereas logistics and warehousing are poised for an 11.16% CAGR through 2031.

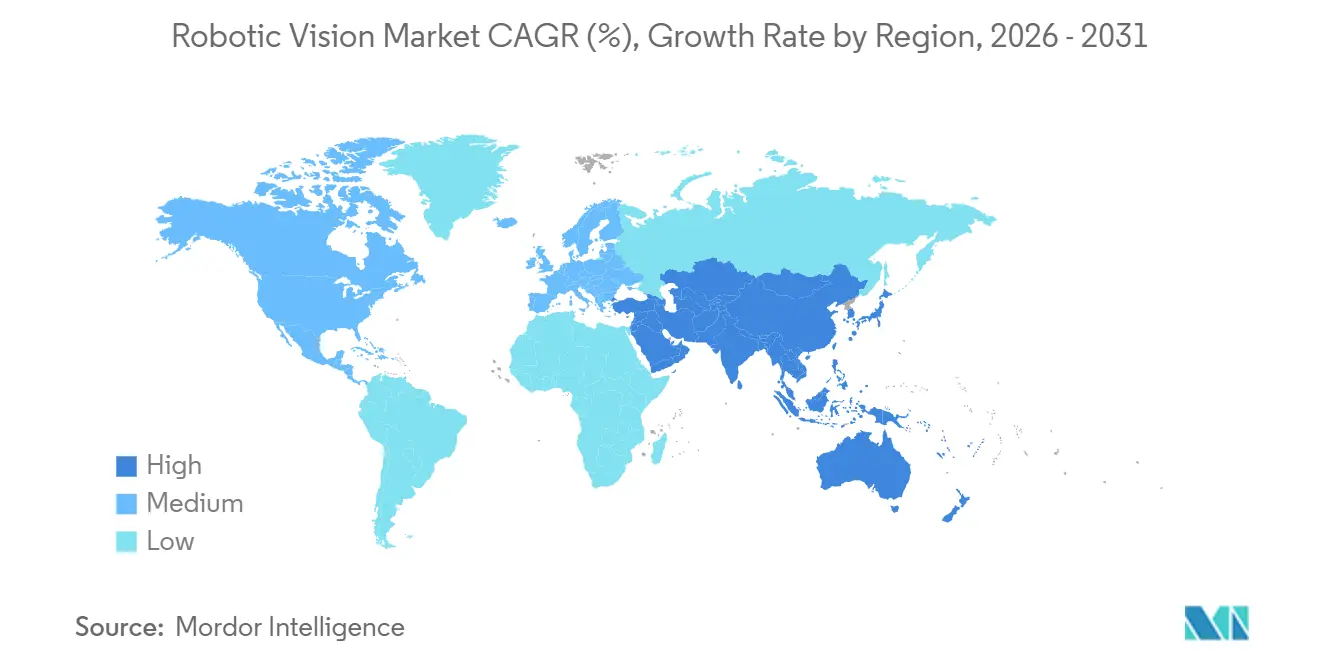

- By geography, Asia-Pacific dominated with a 47.91% share in 2025 and is expected to progress at a 10.37% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Robotic Vision Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating adoption of AI-embedded 3D vision for complex assembly | +2.1% | Germany, Japan, South Korea, United States | Medium term (2-4 years) |

| Government incentives for automation amid labor shortages | +1.8% | China, Japan, South Korea, Germany, Poland, United States, Mexico | Short term (≤ 2 years) |

| Rapid scale-up of vision-enabled cobots in Tier-2 hubs | +1.6% | Vietnam, Thailand, Czech Republic, Romania, Mexico | Medium term (2-4 years) |

| Edge-AI chips slashing latency below 10 ms | +1.9% | Taiwan, South Korea, Germany, United States, China | Short term (≤ 2 years) |

| Post-2025 ESG mandates pushing zero-defect manufacturing | +1.2% | Europe, North America, Japan, South Korea | Long term (≥ 4 years) |

| Vision-as-a-service subscription models lowering upfront costs | +0.7% | North America, Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating adoption of AI-embedded 3D vision for complex assembly

AI-embedded 3D Vision lets robots interpret depth, pose, and surface texture in real time, enabling adaptive placement of battery cells, circuit boards, and molded plastics. Automotive plants in Germany and the United States cut battery-module scrap rates by up to 50% after switching from fixed jigs to 3D vision-guided placement.[1]ABB Robotics, “Prismatic-Cell Assembly Case Study,” abb.com Electronics makers in China and South Korea improved solder-joint detection on curved substrates, overcoming 2D cameras. Commodity edge processors such as Intel Movidius and Qualcomm RB5 now execute neural inference at under 5 watts, eliminating heat constraints inside lightweight cobots. As component prices fall, 3D systems that once cost 2 to 3 times more than 2D alternatives now carry only a 50% premium, speeding replacement cycles. The advance aligns with zero-defect mandates that tie supplier bonuses to ppm defect targets.

Government incentives for automation amid labor shortages

Advanced economies face shrinking labor pools as participation rates remain below pre-pandemic levels. The United Kingdom awarded GBP 250 million (USD 312 million) in grants to factories integrating vision-equipped cobots, thereby trimming payback periods to under 2 years.[2]UK Government, “Smart Machines Strategy,” gov.uk Japan’s tax credit covering 30% of vision-system outlays favored food-processing and drug-manufacturing SMEs. Germany co-funded EUR 500 million (USD 565 million) in vision deployments for Mittelstand firms, prioritizing projects that replace repetitive manual tasks. These programs accelerate project approvals, incentivize transparent AI algorithms, and channel subsidies to vendors offering explainable vision models.

Rapid scale-up of vision-enabled cobots in Tier-2 hubs

Investors diversifying supply chains toward Vietnam, Thailand, and Mexico demand flexible automation that absorbs frequent product changes. Southeast Asia industrial and service robot deployments are also accelerating across automotive, electronics, warehousing, and healthcare environments as manufacturers address labor shortages and scale flexible automation strategies. Universal Robots shipped vision-ready cobots in 60% of its Southeast Asian orders in 2025, up from 35% in 2023. 3D bin-picking deployments across 200 Eastern European suppliers eliminated costly fixtures, saving USD 50,000-100,000 per line. Mexico’s cross-border assembly flow leveraged cobot vision to verify part orientation at each handoff, cutting rework shipments by roughly 25%. These savings resonate with contract manufacturers awarded shorter but more frequent production runs, underpinning sustained demand.

Edge-AI chips slashing latency below 10 ms

Processors such as NVIDIA Jetson Thor provide 2,000 TOPS at 20 watts, shrinking inference latency to single-digit milliseconds.[3]NVIDIA, “Jetson Thor Platform Brief,” nvidia.com Semiconductor fabs in Taiwan rely on sub-10 millisecond control loops to prevent wafer-edge chipping during high-speed transfers. Food processors use multicamera fusion on Qualcomm QCS8550 to flag contaminants and temperature anomalies in a single pass, halving false-reject rates. By moving compute to the camera or robot arm, plants avoid IT-infrastructure overhauls and comply with data-sovereignty statutes that bar cloud uploads. Low-latency control also unlocks vision-guided precision welding and adhesive-dispensing tasks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High integration costs with legacy brown-field production lines | -1.4% | United States, Canada, Germany, France | Short term (≤ 2 years) |

| Shortage of vision-system integration talent | -0.9% | Southeast Asia, Latin America, Eastern Europe | Medium term (2-4 years) |

| Fragmented sensor and software standards hindering interoperability | -0.8% | Global multivendor factories | Long term (≥ 4 years) |

| Rising cybersecurity compliance costs for vision-rich factories | -0.6% | Europe, North America, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High integration costs with legacy brown-field production lines

Plants built before 2010 seldom feature network bandwidth, power routing, or physical layouts suitable for camera clusters and edge servers. A 2025 survey showed that 65% of North American automotive suppliers face vision integration costs above USD 500,000 per line, with electrical and safety upgrades accounting for nearly half. European factories often run legacy PLCs that lack the headroom to ingest high-resolution image streams, forcing parallel control architectures that inflate budgets. Custom brackets for cameras and lighting add weeks to commissioning, while tight margins push many suppliers to defer projects until full line replacements.

Shortage of vision-system integration talent

Robotic vision deployment needs blended expertise in optics, AI, and industrial networking, a skill mix scarce outside Germany, Japan, or U.S. tech hubs. The World Economic Forum lists machine-vision engineering among the top-10 global skill gaps, with demand outstripping supply three-to-one in Southeast Asia and Latin America. Vendor-led training spans up to a year, delaying rollout schedules. Remote commissioning, common for plants in Vietnam or Mexico, prolongs projects by roughly one-third and elevates error rates. University curricula in emerging regions rarely cover 3D Vision, perpetuating the talent bottleneck.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: 3D Vision Closes the Gap on Established 2D Platforms

2D systems accounted for 56.73% of the robotic vision market share in 2025, supported by low camera costs and mature barcode and presence-detection software. The surge of electric-vehicle battery and semiconductor inspection is lifting 3D depth sensing, which is set to grow at a 10.32% CAGR through 2031. Automotive lines merging CAD-driven inspections with point-cloud comparison raised defect-detection rates to 99.9%. Time-of-flight sensor pricing fell sharply after 2024, bringing the total cost of 3D cells to just 1.5 times that of a 2D alternative. Multispectral and infrared options are gaining traction in pharma and food safety, where they detect contaminants invisible to RGB. Hybrid architectures that record high-resolution 2D images while streaming 3D point clouds now handle pick, inspect, and place in a single scan, cutting cycle time by 20%.

The diffusion of AI-powered analytics further narrows the performance gap. Systems overlaying neural networks on traditional filters learn new defect classes without manual reprogramming, minimizing downtime. Logistics providers integrate 3D Vision into autonomous mobile robots to automatically measure pallet dimensions and detect overhang, slashing loading errors by 60%. As the price premium narrows and AI toolchains simplify, 3D Vision will penetrate mid-tier factories across China, India, and Eastern Europe, locking in a durable growth runway for the robotic vision market.

By Component: Software and Services Erode Hardware Dominance

Hardware generated 66.89% of 2025 revenue, anchored by cameras, optics, and processors. Area-scan sensors dominate 2D, while structured-light and time-of-flight devices power 3D bin-picking. Edge modules such as NVIDIA Jetson carry 20-25% of hardware spend. Yet software is on track for a 9.92% CAGR to 2031 as vision-as-a-service bundles subscription licenses, synthetic-data model training, and remote calibration. Vendors like Cognex converted perpetual licenses to annual plans, slashing entry cost by 60% and guaranteeing continuous updates. Middleware that abstracts hardware idiosyncrasies lets integrators swap sensors without rewriting code, easing vendor lock-in pain.

Services trail closely, covering system design, operator training, and AI model maintenance. As small factories lack resident data scientists, fully managed packages are gaining market share, particularly in North America, where labor rates justify outsourcing. Over the forecast window, software and services combined are set to capture incremental points of market share in the robotic vision market each year, signaling a strategic pivot from hardware margins to recurring revenue.

By Robot Type: Cobots Accelerate as Safety-Rated Vision Matures

Industrial robots retained 49.73% of 2025 revenue, thriving in high-speed welding, painting, and palletizing. Collaborative robots, aided by depth cameras and force sensors, will log a 10.41% CAGR through 2031. ISO 15066 safety envelopes rely on Vision to modulate speed on human approach, enabling barrier-free operation that saves floor space. Electronics assemblers report 70–80% faster SKU changeovers after migrating from six-axis industrial arms to vision-guided cobots. Mobile robots, propelled by ceiling-mounted lidar and 3D cameras, are surging in warehouses that drop magnetic-tape guidance to gain route flexibility.

Humanoid projects in automotive R&D labs are testing vision-driven dexterity for wire-harness insertion, hinting at long-term opportunities. Aerial drones with optic flow and depth-sensing capabilities conduct inventory counts in mezzanines unreachable by ground robots, a niche expanding as fulfillment centers scale. This diversification underpins robust unit growth for vision modules across the full robot spectrum, preserving momentum for the robotic vision market.

By Application: Guidance and Navigation Lead the Growth Arc

Material handling accounted for 32.49% of 2025 revenue, as 2D cameras located parts for high-speed pick-and-place. Guidance and navigation will outpace all other uses at an 11.21% CAGR, driven by autonomous mobile robots that build maps on the fly using stereo vision. Inspection remains core, with deep-learning segmentation used to flag micro-scratches on reflective metal housings at 1,000 parts per minute. Assembly tasks now exploit eye-in-hand cameras to manage tolerance stacks without fixtures, reducing tooling costs by double-digit percentages.

Welding lines overlay seam-tracking vision to correct torch trajectory in real time, while paint booths measure wet-film thickness to avoid runs. Emerging adaptive tasks, such as flexible-cable routing and soft-material manipulation, depend on AI vision to estimate deformation, opening new addressable fields. The iterative spread of intelligent guidance cements vision’s role as the nervous system of next-generation automation, underpinning sustained expansion of the robotic vision market.

By End-User Industry: Logistics and Warehousing Steal the Spotlight

Automotive remained the largest spender at 35.83% in 2025, leveraging 3D Vision for battery-module assembly and final paint inspection. Logistics and warehousing riding e-commerce parcel volumes will chart an 11.16% CAGR to 2031. Fulfillment centers deploy goods-to-person robots with vision-guided navigation, trimming pick times and boosting throughput. Semiconductor fabs sustain premium demand for sub-micron wafer handling, while food and beverage processors rely on multispectral cameras to flag foreign objects and verify fill levels.

Pharma lines enforce 100% vial inspection, employing AI-vision to spot cracks and sell-by misprints. Aerospace suppliers deploy robot vision in composite lay-up and turbine-blade metrology, tolerating higher spends for mission-critical accuracy. Agriculture gains traction as fruit-picking robots discern ripeness via color and texture. Across sectors, zero-defect imperatives and labor gaps converge to keep the robotic vision market expanding deep into mid-decade.

Geography Analysis

Asia-Pacific retained 47.91% of 2025 revenue and is on course for a 10.37% CAGR to 2031, buoyed by China’s Made in China 2025 targets and South Korea’s semiconductor capital outlays. Japan’s aging workforce pushes cobot adoption in food and pharma factories, while India’s USD 2 billion incentive steers electronics makers toward vision-driven automation. Australia’s mining firms deploy vision-guided autonomous trucks and drills, cutting operator exposure to hazards.

North America trails but benefits from the Inflation Reduction Act tax credits that fund vision-enabled battery plants. U.S. logistics hubs in Kentucky and Texas are retrofitting distribution centers with camera-equipped AMRs to handle holiday peak orders. Canada’s aerospace corridor in Quebec invests in 3D Vision for composite inspection, aiming to achieve defect rates below 0.05 ppm.

Europe faces brownfield integration hurdles yet remains pivotal. Germany’s automotive Tier-1s spent EUR 1.5 billion (USD 1.7 billion) on battery inspection lines across 2024-2025. The United Kingdom offsets post-Brexit labor shortages with lights-out vision-guided machining in aerospace and pharma. Central European nations such as Poland and the Czech Republic lure near-shoring contracts by bundling automation rebates with low energy tariffs.

Middle East and Africa, Latin America, and smaller regions grow from modest bases. Mexico’s USD 20 billion near-shoring windfall channeled funds to vision-ready wiring harness plants. Brazil’s ag-equipment makers integrate Vision into autonomous harvesters, slashing operator costs nearly in half. Saudi Arabia’s Vision 2030 earmarks USD 500 million for food and petrochemical automation, with Vision a prerequisite for subsidy approval. South Africa trials vision-guided ore sorters that uplift grade while curbing safety incidents.

Competitive Landscape

The top five vendors, Cognex, Keyence, SICK, Basler, and Teledyne DALSA, commanded roughly 40-45% of 2025 revenue, yielding a moderately concentrated field. These incumbents leverage installed bases, global distribution, and multi-year service contracts to protect share. Cognex’s 2025 purchase of a European AI startup signals an arms race to own proprietary algorithms that differentiate beyond sensor pixels. Keyence opened a USD 200 million vision-sensor plant in Vietnam to reduce lead times to 2 weeks for Southeast Asian customers.

Semiconductor giants and cobot builders are vertically integrating Vision to capture system margins. NVIDIA tunes Jetson SoCs for turnkey perception stacks, while ABB bundles wrist cameras with collaborative arms. Open-source frameworks such as ROS and OpenCV lower entry barriers, enabling integrators to assemble bespoke solutions from commodity parts and undercut turnkey systems by up to 40%.

Patent filings in 3D sensing and edge inference surged 60% between 2023 and 2025, reflecting a contest for intellectual property moats. White-space lies in healthcare robotics, agricultural automation, and infrastructure inspection, domains where incumbent industrial-automation vendors lack domain depth. Vendors that offer end-to-end platforms addressing sensor, software, and cybersecurity compliance stand to widen their moat as factories seek single-throat accountability.

Robotic Vision Industry Leaders

Keyence Corporation

FANUC Corporation

ABB Ltd.

Omron Corporation

Qualcomm Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Omron Corporation received ISO 13849 certification for its FH-SMD vision system, allowing barrier-free collaborative deployments.

- October 2025: ABB Robotics partnered with NVIDIA to embed Jetson Thor edge-AI in its next cobots, promising sub-10 millisecond perception.

- September 2025: Cognex launched its In-Sight 3D-L4000 system combining laser profiling with AI defect classification at 99.5% detection accuracy.

- August 2025: Basler released the ace 2 Pro camera line with on-board AI preprocessing that trims latency by up to 40%.

Global Robotic Vision Market Report Scope

The Robotic Vision Market Report is Segmented by Technology (2D Vision Systems, 3D Vision Systems, AI-Powered Vision, Multispectral/Infrared Vision, Hybrid Vision Architectures), Component (Hardware, Software, Services), Robot Type (Industrial Robots, Collaborative Robots (Cobots), Mobile Robots (AMR/AGV), Humanoid Robots, Aerial Drones), Application (Material Handling, Assembly and Disassembly, Inspection and Quality Assurance, Guidance and Navigation, Packaging and Palletizing, Pick and Place, Welding and Soldering, Surface Finishing and Painting, Adaptive Tasks and Emerging Use Cases), End-User Industry (Automotive, Electronics and Semiconductor, Food and Beverage, Pharmaceutical and Healthcare, Aerospace and Defense, Logistics and Warehousing, E-commerce and Retail, Agriculture, Energy and Utilities), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| 2D Vision Systems |

| 3D Vision Systems |

| AI-Powered Vision |

| Multispectral / Infrared Vision |

| Hybrid Vision Architectures |

| Hardware | Cameras |

| Sensors | |

| Processors and Edge Modules | |

| Optics and Lighting | |

| Communication Modules | |

| Software | Image-Processing Algorithms |

| AI/ML Models | |

| Vision Middleware | |

| Calibration and Simulation Tools | |

| Services | Integration and Engineering |

| Training and Support | |

| Maintenance and Upgrades | |

| Vision-as-a-Service |

| Industrial Robots |

| Collaborative Robots (Cobots) |

| Mobile Robots (AMR/AGV) |

| Humanoid Robots |

| Aerial Drones |

| Material Handling |

| Assembly and Disassembly |

| Inspection and Quality Assurance |

| Guidance and Navigation |

| Packaging and Palletizing |

| Pick and Place |

| Welding and Soldering |

| Surface Finishing and Painting |

| Adaptive Tasks and Emerging Use Cases |

| Automotive |

| Electronics and Semiconductor |

| Food and Beverage |

| Pharmaceutical and Healthcare |

| Aerospace and Defense |

| Logistics and Warehousing |

| E-commerce and Retail |

| Agriculture |

| Energy and Utilities |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology | 2D Vision Systems | ||

| 3D Vision Systems | |||

| AI-Powered Vision | |||

| Multispectral / Infrared Vision | |||

| Hybrid Vision Architectures | |||

| By Component | Hardware | Cameras | |

| Sensors | |||

| Processors and Edge Modules | |||

| Optics and Lighting | |||

| Communication Modules | |||

| Software | Image-Processing Algorithms | ||

| AI/ML Models | |||

| Vision Middleware | |||

| Calibration and Simulation Tools | |||

| Services | Integration and Engineering | ||

| Training and Support | |||

| Maintenance and Upgrades | |||

| Vision-as-a-Service | |||

| By Robot Type | Industrial Robots | ||

| Collaborative Robots (Cobots) | |||

| Mobile Robots (AMR/AGV) | |||

| Humanoid Robots | |||

| Aerial Drones | |||

| By Application | Material Handling | ||

| Assembly and Disassembly | |||

| Inspection and Quality Assurance | |||

| Guidance and Navigation | |||

| Packaging and Palletizing | |||

| Pick and Place | |||

| Welding and Soldering | |||

| Surface Finishing and Painting | |||

| Adaptive Tasks and Emerging Use Cases | |||

| By End-User Industry | Automotive | ||

| Electronics and Semiconductor | |||

| Food and Beverage | |||

| Pharmaceutical and Healthcare | |||

| Aerospace and Defense | |||

| Logistics and Warehousing | |||

| E-commerce and Retail | |||

| Agriculture | |||

| Energy and Utilities | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large will the robotic vision market be by 2031?

The robotic vision market size is projected to reach USD 5.56 billion by 2031, growing at a 9.33% CAGR from 2026.

Which segment is expanding fastest within robotic vision applications?

Guidance and navigation, driven by autonomous mobile robots, is advancing at an 11.21% CAGR through 2031.

Why are collaborative robots gaining share?

Vision-guided safety features let cobots work next to people without fences, enabling faster changeovers and driving a 10.41% CAGR to 2031.

Which region leads adoption of robotic vision?

Asia-Pacific held 47.91% of 2025 revenue and is forecast to grow at a 10.37% CAGR, underpinned by China’s and South Korea’s electronics and battery investments.

What is the main barrier to wider robotic vision deployment?

High integration costs in legacy brown-field factories, often exceeding USD 500,000 per line, remain the most significant barrier.

How are vendors countering capital-cost concerns?

Vision-as-a-service subscription models lower upfront spend by up to 60%, bundling software, updates, and remote support into a predictable annual fee.

Page last updated on: