Geomarketing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

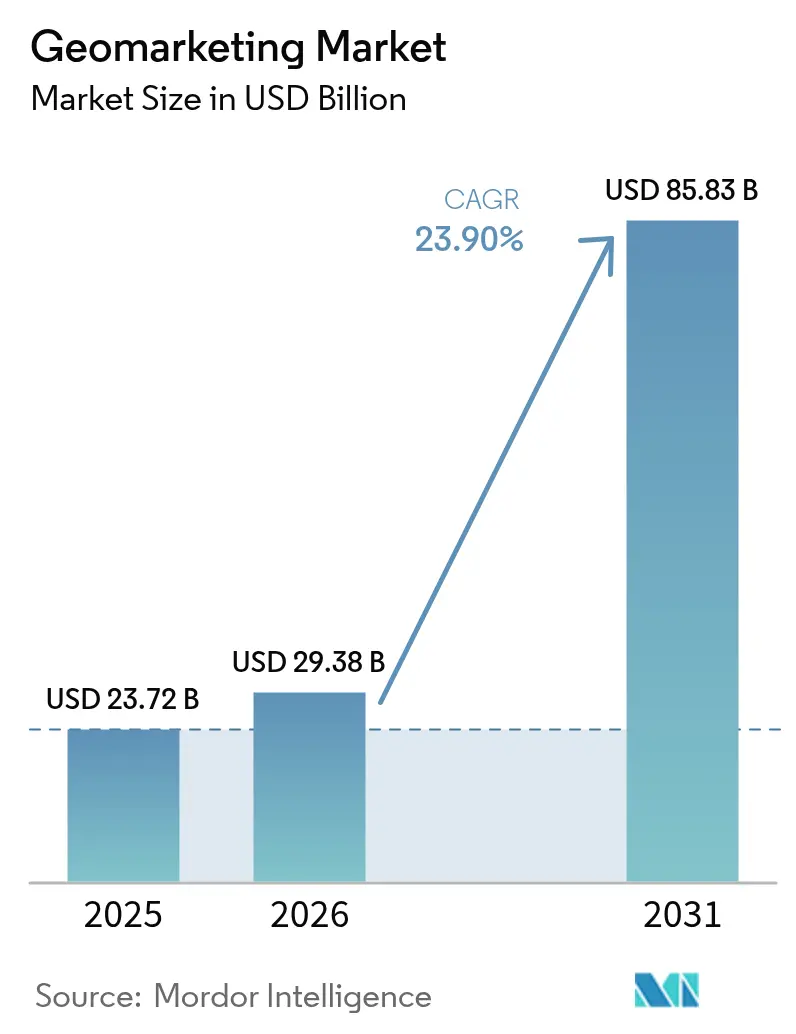

| Market Size (2026) | USD 29.38 Billion |

| Market Size (2031) | USD 85.83 Billion |

| Growth Rate (2026 - 2031) | 23.90% CAGR |

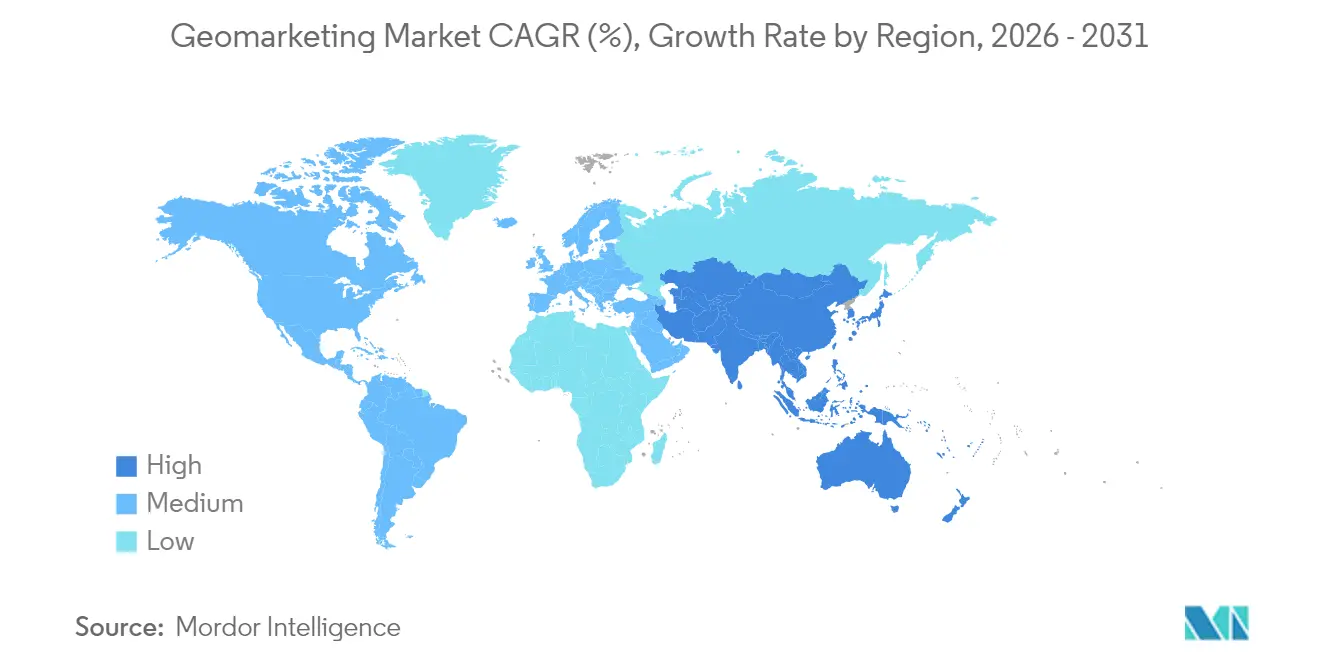

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Geomarketing Market Analysis by Mordor Intelligence

Geomarketing market size in 2026 is estimated at USD 29.38 billion, growing from 2025 value of USD 23.72 billion with 2031 projections showing USD 85.83 billion, growing at 23.9% CAGR over 2026-2031. Software-defined platforms and cloud deployments enable rapid feature releases and elastic scaling, while indoor positioning breakthroughs unlock new venue-level use cases. Regulatory pressure around data consent and the technical impact of mobile identifier deprecation temper growth yet also spur innovation in privacy-preserving analytics. Competitive intensity is rising as hyperscale cloud providers, telcos, and specialist vendors compete on data accuracy, real-time insights, and verticalized solutions, making strategic partnerships and cross-stack integration central to differentiation.

Key Report Takeaways

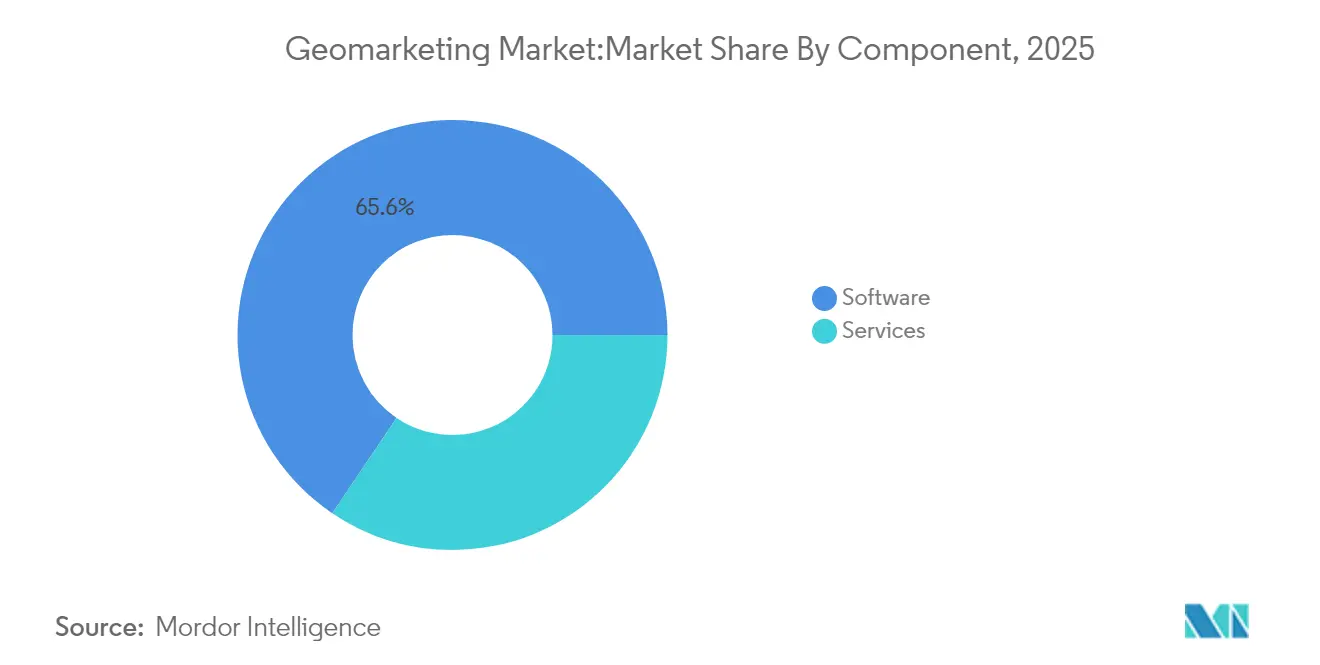

- By component, software held 65.55% of the geomarketing market share in 2025; services post the fastest CAGR at 26.69% through 2031.

- By deployment, cloud platforms captured 70.42% of the geomarketing market in 2025, expanding at 25.46% CAGR to 2031.

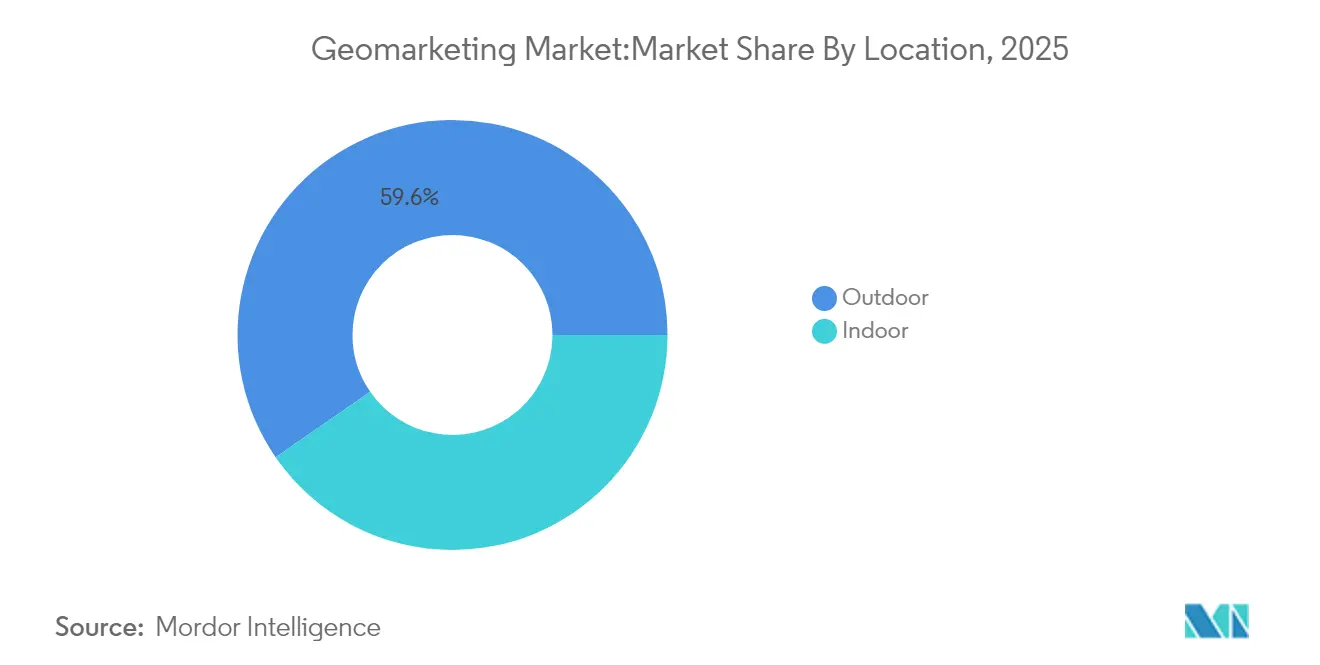

- By location, outdoor services led with a 59.62% share of the geomarketing market size in 2025, while indoor positioning is set to grow at a 26.74% CAGR.

- By end-user industry, retail and e-commerce commanded 27.12% share of the geomarketing market in 2025; travel and hospitality accelerates at 25.88% CAGR.

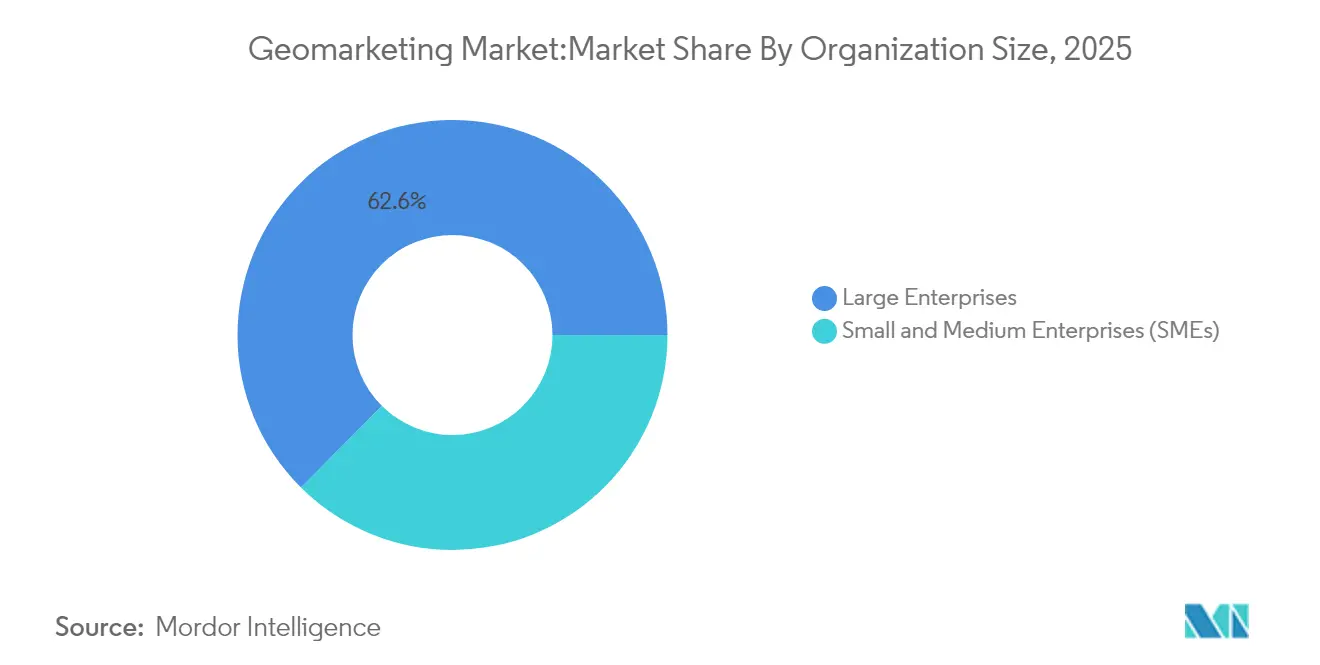

- By organization size, large enterprises contributed 62.55% revenue in 2025; SMEs record the highest 27.01% CAGR.

- By technology, GPS/cellular retained 42.78% share, whereas BLE beacons advance at 26.05% CAGR.

- By solution type, geo-fencing and proximity marketing led with 33.12% in 2025; real-time tracking scales at 26.25% CAGR.

- By geography, North America controlled 37.25% revenue in 2025, while Asia-Pacific exhibits the quickest 26.31% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Geomarketing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven hyper-personalization of location ads | +4.2% | Global, led by North America and APAC | Medium term (2-4 years) |

| Growing 5G roll-outs expand indoor accuracy | +3.8% | APAC core, spill-over to North America and EU | Long term (≥ 4 years) |

| Retail digital twins link foot-traffic and spend | +2.9% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Mainstream adoption of beacons in quick-service restaurants | +2.1% | Global, led by North America | Short term (≤ 2 years) |

| Rideshare and micromobility data monetization | +1.7% | Urban centers globally | Medium term (2-4 years) |

| MarTech stacks embedding real-time geofencing | +1.5% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Driven Hyper-Personalization of Location Ads

Real-time machine-learning models now adapt creatives to an individual’s movement patterns, dwell time, and venue preferences, enabling retailers to improve ad-spend efficiency by up to 40% compared with traditional geo-targeting methods. [1]Flybuy, “Five Guys + Flybuy: Success, Innovations, and What's Next,” flybuy.com Arrival-time predictions shrink fulfillment gaps, while computer vision links foot traffic to demographic insights, as seen when Aura Vision boosted conversion at Flannels and returned a 4.5 X ROI. These capabilities elevate personalized engagement from optional to indispensable and keep the geomarketing market on an aggressive growth trajectory.

Growing 5G Roll-Outs Expand Indoor Accuracy

Carrier-phase measurements introduced in 3GPP Release 18 deliver sub-meter precision, allowing geomarketing in airports, malls, and factories where GPS once failed. [2]Ericsson, “5G Advanced positioning in 3GPP Release 18,” ericsson.com Enterprises have documented 15-20% productivity gains via automated asset tracking, though mmWave infrastructure requires dense cells and capital investment. Hybrid stacks blending 5G with BLE and Wi-Fi are emerging as a pragmatic route to comprehensive coverage, reinforcing near-term demand for indoor location solutions.

Retail Digital Twins Link Foot-Traffic and Spend

Virtual store replicas correlate movement data with sales to guide merchandise placement, layout changes, and staffing. GUESS reported a 200% merchandising productivity jump using Matterport’s platform. Mall operator Vicinity Centres processed feeds from over 300 dashboards to slash debt by 36% and optimize energy use. Digital twins sharpen return-on-space metrics, keeping retailers invested in advanced location analytics.

Mainstream Adoption of Beacons in Quick-Service Restaurants

Low-cost BLE beacons (< USD 50 each) create location triggers that cut wait times and boost basket sizes. McDonald’s drove an 8% sales lift for select menu items within four weeks of rollout. Sonny’s BBQ then trimmed average pickup times to 2 minutes 30 seconds across 90+ restaurants. Proven ROI and contactless service demand position beacons as a staple across high-volume dining chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent opt-in consent under GDPR/CCPA | -3.1% | EU and California, expanding to other US states | Long term (≥ 4 years) |

| Depreciation of mobile ad-IDs lowers match rates | -2.7% | Global, highest impact in North America | Medium term (2-4 years) |

| Indoor triangulation accuracy gaps in large venues | -1.9% | Global | Medium term (2-4 years) |

| High TCO for multi-source data normalization | -1.4% | Global, concentrated in enterprise segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Opt-In Consent Under GDPR/CCPA

Regulators now require explicit, affirmative location-data consent, raising compliance costs that range from USD 500,000 to USD 2 million for enterprise platforms. With 21 US states enacting similar laws, fines can touch USD 10,000 per incident. Geo-contextual consent banners aid regional compliance but add operational overhead, keeping privacy at the center of vendor roadmaps.

Depreciation of Mobile Ad-IDs Lowers Match Rates

Opt-in rates for Apple IDFA now sit below 25%, slashing deterministic audience links and trimming attribution accuracy by up to 40%. Probabilistic modeling, first-party data, and differential privacy emerge as alternatives yet carry added technical complexity and may never fully restore granularity, compelling geomarketing platforms to revise performance benchmarks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Innovation

Software platforms accounted for 65.55% revenue in 2025, underscoring the geomarketing market preference for cloud-native, feature-rich stacks that can ingest varied data sources and comply with changing privacy rules. Continuous updates funnel AI segmentation, compliance dashboards, and API connectors into user hands without on-premise friction. Services, led by integration and managed analytics, accelerate at 26.69% CAGR as enterprises seek guidance on stitching geomarketing insights into sprawling MarTech architectures.The geomarketing market size tied to services climbs quickly because tailored onboarding, custom algorithm design, and regulatory audits remain outside most in-house skill sets. Oracle’s 2025 cloud revenue growth to USD 11.7 billion illustrates how bundled software-plus-services agreements satisfy enterprise appetite for turnkey location intelligence.

By Deployment: Cloud Adoption Accelerates

Cloud held 70.42% share of the geomarketing market in 2025 and posts the highest 25.46% CAGR as brands favor elastic compute and rapid scaling for high-volume campaigns. Microsoft Azure’s 31% revenue jump reflects surging demand for GPU-accelerated analytics and serverless geospatial pipelines.On-premise persists in sectors with strict data sovereignty, yet faces cost headwinds; enterprises cutting hardware and maintenance achieve 40-60% savings in total cost of ownership. Network egress fees and latency constraints keep certain low-latency applications hybrid, but incremental cloud security advances continue drawing workloads into multitenant environments, expanding the geomarketing market footprint.

By Location: Indoor Positioning Gains Momentum

Outdoor services preserved 59.62% revenue in 2025 thanks to ubiquitous GPS, while indoor positioning’s 26.74% CAGR showcases demand for asset tracking and immersive retail. China Mobile’s 5G system reached 3-5 meter accuracy across 90% of covered space, setting functional benchmarks for venues worldwide.As enterprises embed hybrid BLE–Wi-Fi–5G arrays, the geomarketing market size for indoor services swells, enabling queue management, real-time navigation, and proximity offers. Deployment complexity and cost remain hurdles, but declining beacon prices and managed-service bundles reduce entry barriers for mid-tier retailers and hospitals.

By End-user Industry: Retail Leadership with Hospitality Surge

Retail and e-commerce continued to dominate with 27.12% of the geomarketing market in 2025, exploiting site selection analytics and omnichannel foot-traffic attribution to sharpen margin management. Telstra achieved 95% accuracy in foot-traffic analysis for store planners, exemplifying mature use cases.Travel and hospitality emerges as the fastest-rising adopter as hotels and airlines deploy dynamic pricing and on-premise mobile concierge services. The geomarketing market share captured by hospitality is forecast to expand swiftly, mirroring pandemic recovery and heightened guest-experience expectations. Financial services, media, and healthcare follow with fraud detection, event marketing, and asset monitoring cases that extend addressable revenue.

By Organization Size: Enterprise Dominance with SME Acceleration

Large enterprises retained 62.55% revenue in 2025, leveraging large datasets and multi-site operations to drive holistic customer journey analytics. Cross-stack integrations with CRM, CDP, and BI platforms create 360-degree views, reinforcing lock-in with leading cloud providers.SMEs, historically constrained by budget and expertise, now gain access to SaaS bundles with per-seat pricing, powering the geomarketing market’s democratization. Vendors embed guided workflows and AI-based optimization to mask complexity and accelerate ROI, pushing SME CAGR to 27.01% even as data hygiene and IT resource gaps persist.

By Technology: GPS Stability with BLE Innovation

GPS/cellular retained 42.78% revenue in 2025, offering reliable outdoor positioning for navigation, ride-hailing, and last-mile delivery. BLE beacons however post a 26.05% CAGR, propelled by indoor proximity marketing and order-ahead logistics. Beacon hardware under USD 50 and low power demands reduce rollout friction for franchises and shopping centers.Wi-Fi and NFC serve niche cases, but hybrid technology stacks rise as the geomarketing market chases meter-level accuracy. Patent filings on carrier-phase ranging and ML-enhanced localization show a pipeline of innovations aimed at tighter error bounds and energy efficiency.

By Solution Type: Geofencing Leadership with Real-Time Growth

Geo-fencing and proximity campaigns delivered 33.12% revenue in 2025, valued for clear attribution links between footfall and spend. Retailers and QSR chains rely on polygon-based triggers and competitor “geo-conquesting” to win incremental visits.Real-time tracking’s 26.25% CAGR highlights surging need for logistics orchestration, cold-chain compliance, and customer ETA transparency. 5G latency improvements and edge compute accelerate sub-second updates, expanding the geomarketing market size tied to operational visibility solutions across transport, healthcare, and manufacturing.

Geography Analysis

North America maintained 37.25% of global revenue in 2025, underpinned by mature ad-tech ecosystems, broad 5G penetration, and balanced privacy statutes. Google Cloud logged 30% revenue growth as enterprises layered spatial intelligence on existing data lakes. Federal and state data-privacy frameworks mandate explicit consent yet still permit innovation, ensuring continued investment in precision targeting and omni-channel attribution.Asia-Pacific posts the sharpest 26.31% CAGR, fuelled by population-scale mobile adoption, government 5G incentives, and a mobile-first retail ethos. The GSMA estimates mobile contributed USD 880 billion to regional GDP in 2023, while policies in China, Japan, and Malaysia finance AI and indoor-location pilots. Dual-network 5G frameworks and satellite backhaul projects promise to extend high-accuracy coverage into rural areas, widening the geomarketing market opportunity.Europe advances steadily despite GDPR compliance costs. Enterprises adopt edge processing, federated learning, and differential privacy to reconcile localization with regulatory stringency. Middle East and Africa and Latin America remain emergent yet promising: smart-city investments in the Gulf and rising smartphone penetration in Brazil and Mexico catalyze pilot deployments. Infrastructure gaps and legal uncertainty temper immediate scale, but urbanization and digital payments create fertile ground for localized growth in the next planning cycle.

Regulatory Landscape

The regulatory backdrop for geomarketing is tightening around precise geolocation as a sensitive data class, with stronger requirements for consent, deletion, and restrictions on use. In California, updated CCPA regulations and the California Delete Act took effect on January 1, 2026. The framework establishes the Delete Request and Opt-out Platform (DROP) for data brokers, with registered brokers required to begin honoring deletion requests through DROP by August 1, 2026 (with a 45-day processing window). At the federal level, the US Senate introduced S. 4211, the Consumer Data Privacy and Security Act of 2026, on March 25, 2026, explicitly defining precise geolocation as sensitive personal data, reinforcing conservative handling expectations even amid ongoing legislative flux.

Across jurisdictions, enforcement and statutory constraints increasingly target sensitive-location use cases, affecting how platforms configure geofencing and proximity marketing for healthcare and other protected venues. State-level restrictions, including rules tied to Oregon HB 2008 and California AB 45, prohibit geofencing around sensitive facilities, so platforms need to document exclusions and implement controls beyond default vendor settings. In the EU, Regulation (EU) 2024/1689 (the AI Act) becomes fully applicable on August 2, 2026, adding requirements for data governance and representativeness for high-risk AI systems, which intersects with location-based modeling and segmentation workflows used in geomarketing.

Value Chain Analysis

The geomarketing value chain starts with location-signal generation and collection (mobile OS and app ecosystems, telecom networks, and in-venue sensors such as BLE beacons and Wi-Fi). It then passes through data suppliers and aggregators that normalize signals with POIs and demographic or behavioral attributes. Location intelligence and mapping specialists, including HERE Technologies partners and mobility data providers, package these inputs into curated datasets and APIs, which geomarketing software and cloud platforms operationalize through campaign tools, analytics dashboards, and integration connectors into CRM/CDP/BI stacks.

Implementation partners and managed-service providers sit downstream, handling identity resolution alternatives, consent orchestration, data normalization, and ongoing model tuning for enterprise deployments. Cloud-based SaaS and API delivery dominate distribution, which speeds up feature rollouts and simplifies multiregion deployments, but it also increases reliance on compliant data sourcing and governance. Partnerships increasingly function as a value-chain shortcut to expand coverage and reduce integration friction, illustrated by Mapidea joining the NielsenIQ Partner Network in June 2025 to integrate NielsenIQ datasets into its geospatial intelligence SaaS, and by CARTO partnering with Marker in July 2026 to extend its Agentic GIS reach across Argentina, Chile, Uruguay, and Paraguay. Persistent bottlenecks remain in harmonizing multi-source location inputs and meeting privacy-first requirements (GDPR/CCPA and emerging state rules), which pushes vendors to treat consent management, auditability, and data quality tooling as core product layers rather than add-ons.

Competitive Landscape

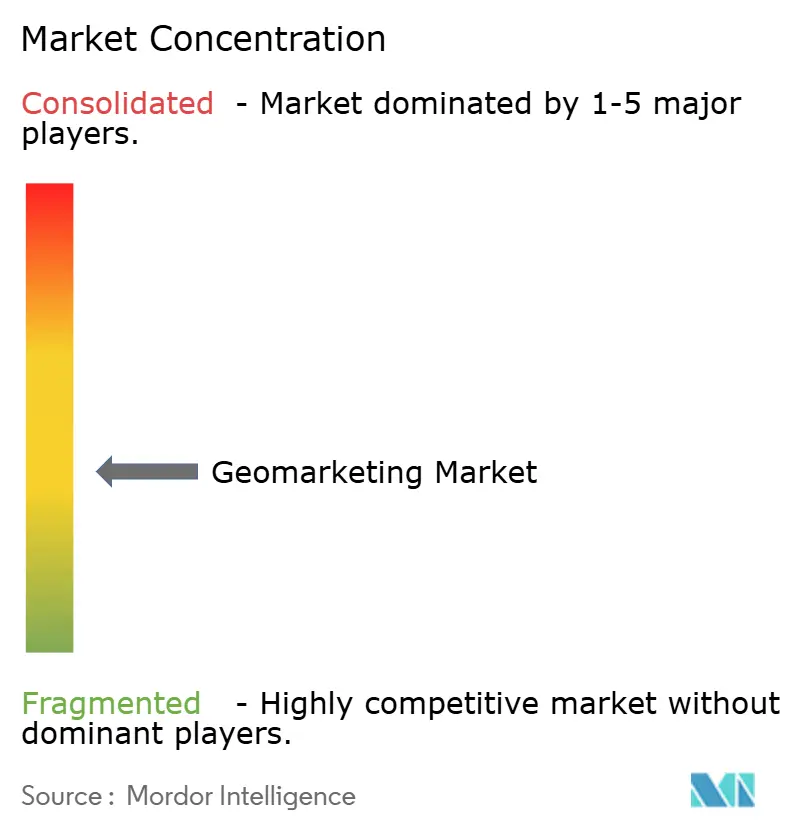

The geomarketing market is moderately fragmented: no vendor controls outsized revenue, creating room for both hyperscalers and focused specialists. Google, Microsoft, and Oracle bundle location APIs, AI services, and analytics dashboards into their clouds, leveraging scale advantages and enterprise contracts. Foursquare, HERE Technologies, and Mapbox focus on data enrichment, SDK flexibility, and white-label mapping to win developer mindshare.

Strategic positioning revolves around data depth, latency, and privacy. Vendors invest in real-time ingestion engines, AI‐driven segmentation, and consent orchestration to withstand identifier loss and regulatory overhead. Verizon’s 2025 acquisition of Senion adds sub-meter indoor wayfinding to its 5G edge footprint, illustrating telco convergence into analytics. Cisco channels USD 600 million in AI edge orders to embed geospatial triggers in network fabric, highlighting infrastructure players’ offensive.

Patent velocity underscores continuous R&D in multi-sensor fusion and privacy preservation; Qualcomm’s filings on 5G-assisted extended-reality positioning mark the next frontier. [4]Google Patents, “Method and/or system for positioning of a mobile device,” patents.google.com White-space opportunities persist in healthcare, government, and manufacturing verticals where domain compliance and deterministic accuracy outstrip generalist roadmaps, allowing niche vendors to gain footholds even as consolidation looms.

Geomarketing Industry Leaders

Adobe Inc.

Airship Group Inc.

Bluedot Industries Pty Ltd.

CartoDB Inc.

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Privacy and identifier constraints are opening whitespace for privacy-preserving geomarketing architectures that still support measurement and activation, including consent orchestration, deletion workflows for broker-sourced data, and greater use of first-party and contextual signals. The California DROP implementation, effective January 1, 2026, with broker compliance milestones starting August 1, 2026, raises the operational bar for location-data handling and increases demand for platform features that can operationalize deletion and opt-out requests across data pipelines. Separately, the EU AI Act becoming fully applicable on August 2, 2026, elevates requirements around data governance and dataset representativeness for high-risk AI systems, supporting investment in provenance tracking, audit logs, and bias checks for geography-linked modeling.

On the demand side, opportunities are shifting beyond classic geofencing into hyper-local catchment modeling, indoor positioning, and omnichannel planning tied to measurable outcomes. Channel 4 partnering with CACI in June 2026 to launch a Geo Mapping tool for streaming campaigns is a concrete example, moving from regional zones to postcode-sector targeting using Acorn data and isochrone modeling. This signals broader use of finer-grain spatial segmentation in media buying. Telecom and ISP workflows also continue to absorb geomarketing-adjacent capabilities, with operators using geospatial platforms for network planning, tower placement optimization, and data monetization. ISPs are also adopting address-level visualization to distinguish service-eligible and ineligible homes, which expands the buyer set beyond retail-led marketing teams into network, operations, and monetization groups.

Recent Industry Developments

- June 2026: Adobe announced Adobe Brand Visibility within Adobe CX Enterprise, introducing Generative Engine Optimization (GEO) insights and agentic AI recommendations across platforms such as ChatGPT, Google AI, and Microsoft Copilot. The release extends geomarketing-style optimization from physical location context to discoverability within AI-driven search and assistant interfaces, tightening the link between experience orchestration and measurable visibility signals.

- February 2025: Rezolve AI Limited completed its acquisition of Bluedot Industries for approximately AUD 3.9 million (share-based consideration). The deal consolidated an established proximity and location-engagement player into a broader AI commerce platform, reshaping go-to-market options for location-triggered engagement and payments-adjacent use cases.

- October 2024: Adobe announced general availability of GenStudio for Performance Marketing, including integrations with Google Campaign Manager 360, Meta, and TikTok. This expanded cross-channel creative production and activation pathways that many geomarketing programs rely on for rapid localized campaign iteration and performance feedback loops.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the geomarketing market is the revenue earned from software and related services that use location signals to plan, run, and measure marketing actions across digital and physical channels.

Scope exclusions: We exclude stand-alone geospatial analytics that are used only for surveying or asset tracking, and hardware sensors that do not have a clear marketing activation layer.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment

- Cloud

- On-Premise

- By Location

- Indoor

- Outdoor

- By End-User Industry

- BFSI

- IT and Telecommunications

- Retail and E-commerce

- Media and Entertainment

- Travel and Hospitality

- Other End-user Industries

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Technology

- GPS/Cellular

- BLE Beacons

- Wi-Fi/WLAN

- NFC/RFID

- By Solution Type

- Mapping and Geocoding

- Location Analytics and Visualization

- Geo-Fencing and Proximity Marketing

- Real-Time Tracking

- Campaign Planning and Management

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the core demand and supply view, and to set practical boundaries for what should be counted as geomarketing revenue. We relied on public signals that describe adoption and usage, such as smartphone penetration and mobile internet usage published by the ITU, along with privacy and consent rules, including guidance published by the FTC and the European Commission.

We also reviewed location and mapping standards and technical references from the OGC, and market-enablement indicators like digital advertising spend and channel trends from IAB and OECD datasets. These were cross-checked with company filings, earnings call notes, investor decks, and product documentation to understand typical pricing motions and packaging. We used paid subscriptions for company financials and intelligence, news and financials, and patent databases to support revenue splits and to track product change events. The desk sources mentioned here are illustrative only, and many other public and paid references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually billed as geomarketing in customer deployments, and what is handled as adjacent location analytics or general data tools. We spoke with solution owners, marketing operations leaders, and channel partners across major regions, then used those inputs to confirm typical contract structures, usage-based pricing triggers, and how service revenues are recognized in delivery projects.

These conversations were also used to sanity-check adoption drivers like geofencing usage, store network expansion, privacy-safe targeting shifts, and the practical split between platform subscription and implementation support.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 47% |

| Mid tier: 45% | Functional/Unit leaders: 30% | EMEA: 32% |

| Smaller Players: 18% | Managers: 56% | Americas: 21% |

Market-Sizing & Forecasting

The market model starts from a top-down demand reconstruction, where digital advertising activity, location-enabled mobile usage, and enterprise adoption of location-based campaign tools are converted into an addressable spend pool. That pool is then filtered through what is typically purchased as geomarketing software and services, before being allocated across regions based on enterprise IT spend patterns and marketing digitization levels.

To keep totals realistic, we corroborated the output with selective bottom-up checks, such as sampled vendor revenue disclosures, channel feedback on average contract values, and a volume-by-ASP build for common packages (for example, platform subscriptions plus implementation and managed services). When vendor reporting was bundled, gaps were handled using proxy splits informed by product mix, pricing pages, and interview-based attach rates.

For forecasting, scenario analysis was used and then anchored using variable outlooks discussed with experts. Key inputs included smartphone-based location signal availability, privacy and consent enforcement intensity, cloud migration pace for marketing stacks, growth in footfall analytics use, and the shift toward first-party data activation that changes how targeting is executed and priced.

Data Validation & Update Cycle

Model outputs were checked against independent signals like digital ad spend direction, enterprise marketing software budgets, and observable changes in privacy restrictions that can affect measurable demand. Large variances triggered a second pass on assumptions, and the team re-contacted select experts when pricing logic or adoption curves appeared out of line for a region or end market.

Before sign-off, the numbers go through multi-step analyst reviews, including currency conversion checks and year alignment checks so like-for-like comparisons are maintained. Reports are refreshed annually, and interim updates are made when there are material events such as major policy changes, product shifts that affect pricing, or meaningful changes in customer buying behavior. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Geomarketing Market Sizing Compared With Other Published Estimates

Published geomarketing market values often differ because the boundaries are not set the same way, and because price and currency assumptions are not updated at the same time. In fast-growing software markets, even a small change in what is counted as subscription revenue versus services can move the total by billions.

The biggest gap drivers usually come from scope and refresh choices, such as whether adjacent location intelligence tools are included, whether purely non-marketing geospatial analytics is counted, and whether the year's average exchange rates or a point-in-time rate is used. More variance can also appear when ASP changes are projected as a flat uplift, instead of being tied to packaging shifts like usage-based pricing, add-on modules, and managed service attach. These checks are handled on an annual refresh cycle with currency timing and pricing logic re-validated, a process followed by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 29.38 B (2026) | |

| Trade Publication A | USD 21.34 B (2024) | Uses an earlier base year with a shorter look-ahead, and the scope wording suggests broader marketing activity without clearly removing non-geomarketing location analytics and bundled data tooling, which can shift what gets counted. |

| Industry Research Firm B | USD 22.81 B (2025) | Uses a different base-year and segmentation lens, and does not make currency timing and pricing progression steps transparent, so ASP-driven expansion and service attach can be treated inconsistently across regions. |

The table shows that timing and boundary choices explain most of the spread, not a single demand assumption. When pricing steps, exchange-rate timing, and clear inclusions are kept consistent year to year, the estimate becomes easier to trace back to real buying and repeatable inputs.

Key Questions Answered in the Report

What is the current value of the geomarketing market?

The geomarketing market is valued at USD 29.38 billion in 2026 and is projected to reach USD 85.83 billion by 2031.

Which component segment leads the geomarketing market?

Software solutions lead with 65.55% revenue in 2025, driven by cloud-native platforms that integrate diverse data sources.

Why is indoor positioning growing faster than outdoor services?

Sub-meter accuracy enabled by 5G, BLE, and Wi-Fi fusion opens asset tracking and in-store engagement opportunities, driving a 26.74% CAGR for indoor positioning.

How are privacy regulations affecting geomarketing?

GDPR and CCPA require explicit consent, increasing compliance costs and reducing addressable audiences, which lowers forecast CAGR by an estimated 3.1%.

Which region is expanding the fastest?

Asia-Pacific shows the highest growth at 26.31% CAGR through 2031, supported by large mobile populations and aggressive 5G rollout programs.

What technologies will shape geomarketing over the next five years?

Continued 5G deployment, AI-powered personalization, BLE beacons, and privacy-preserving analytics are expected to dominate investment priorities across industries.

Page last updated on: