Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Plasma Lighting Market Report is Segmented by Component (Electrodeless Plasma Lamps, Electronic Power Supply/RF Driver, and More), Wattage (Less Than 700 W, 700 - 1000 W, and Above 1000 W), Application (Street and Roadway Lighting, Parking and Area Lighting, and More), Distribution Channel (Direct Sales, and Distributor and Systems Integrator), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

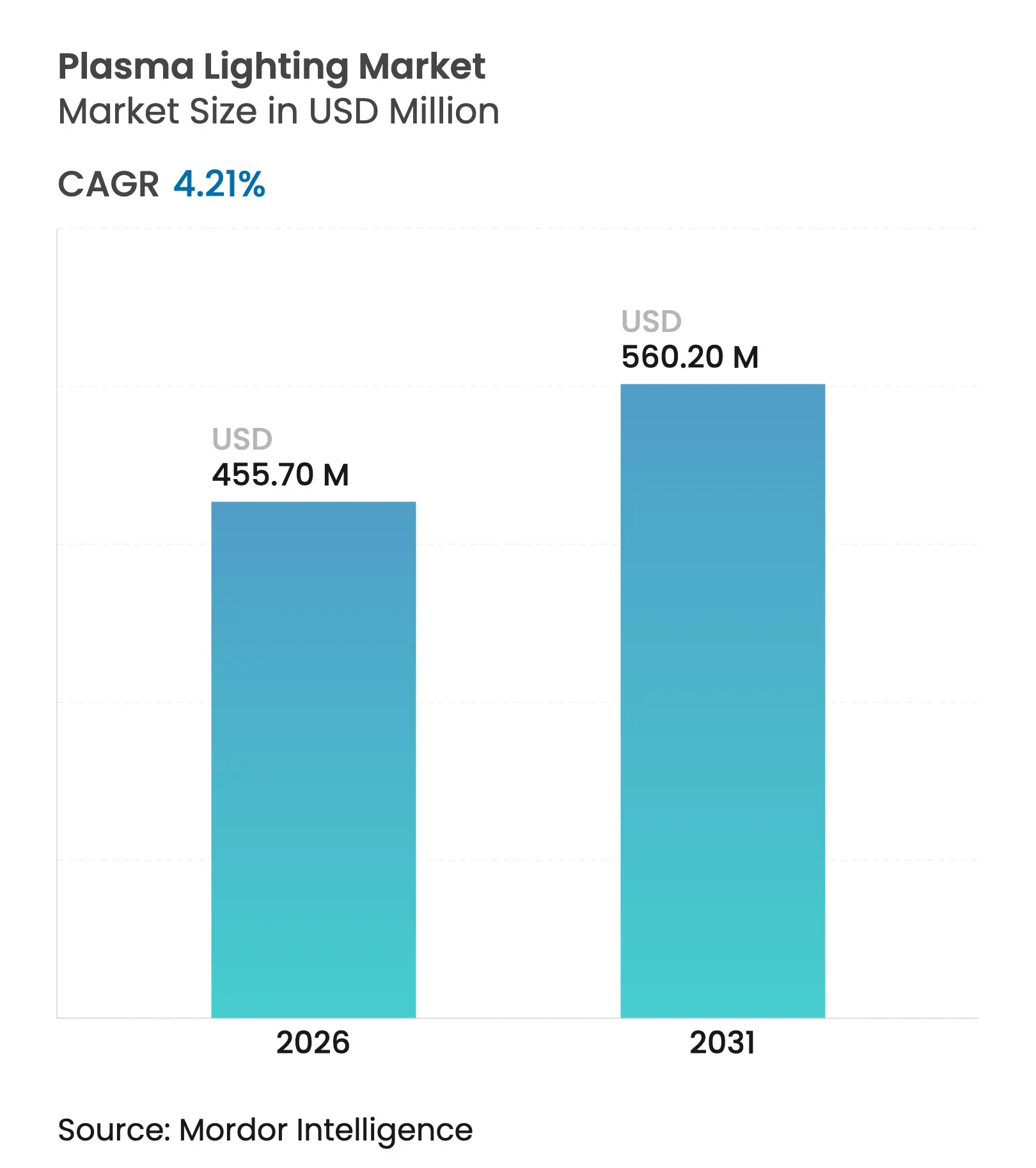

| Market Size (2026) | USD 455.7 Million |

| Market Size (2031) | USD 560.2 Million |

| Growth Rate (2026 - 2031) | 4.21 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

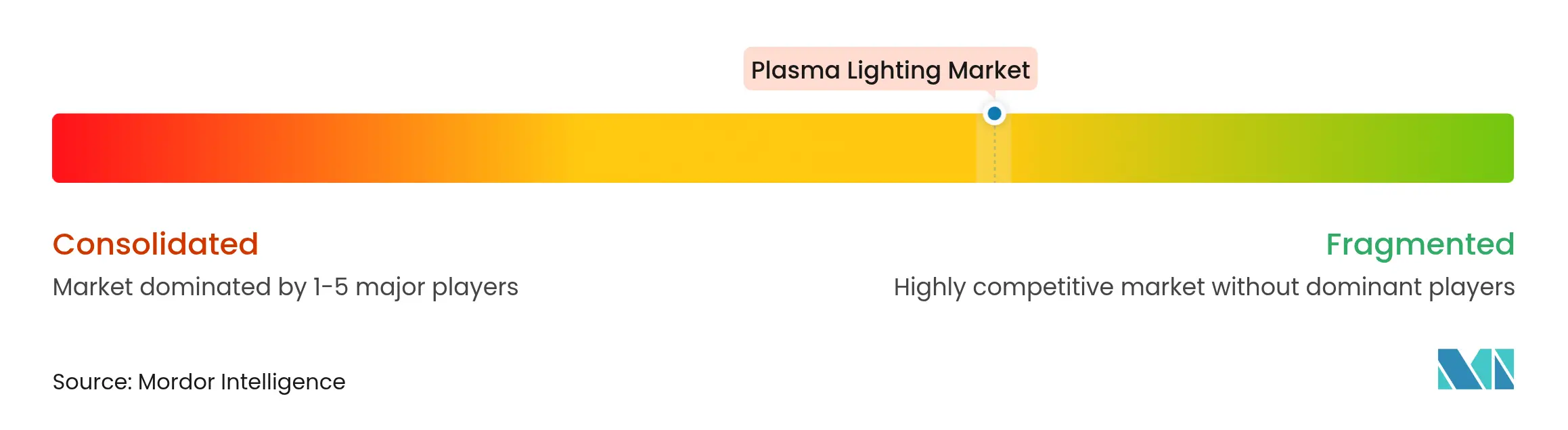

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Plasma lighting market size in 2026 is estimated at USD 455.7 million, growing from 2025 value of USD 437.3 million with 2031 projections showing USD 560.2 million, growing at 4.21% CAGR over 2026-2031. Growth rests on plasma’s ability to deliver very high luminous efficacy, flicker-free output, and ultra-high color rendering in niches where commodity LEDs still struggle, notably high-mast street lighting, indoor vertical farms, broadcast studios, and harsh marine sites. Regulatory pressure to replace mercury-based HID lamps is accelerating procurement in Europe and Gulf Cooperation Council states, while power-supply innovations are reducing system complexity and broadening appeal. Meanwhile, falling LED prices temper adoption in cost-sensitive applications, so vendors focus on value propositions built around lifetime, spectral uniformity, and reduced maintenance.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expanding adoption of plasma grow lights in vertical farms Expanding adoption of plasma grow lights in vertical farms | +0.8% | Asia-Pacific, spill-over to North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:Asia-Pacific, spill-over to North America | Impact Timeline:Medium term (2-4 years) |

Municipal retrofits of high-mast plasma street lighting Municipal retrofits of high-mast plasma street lighting | +0.6% | Europe, selective uptake in North America | Short term (≤ 2 years) | |||

Ultra-high CRI demand from film and broadcast studios Ultra-high CRI demand from film and broadcast studios | +0.4% | North America, expanding to Europe | Medium term (2-4 years) | |||

High-lumen underwater and marine fixtures High-lumen underwater and marine fixtures | +0.3% | Global, coastal concentrations | Long term (≥ 4 years) | |||

Smart stadium investment for flicker-free HDTV broadcast Smart stadium investment for flicker-free HDTV broadcast | +0.5% | Global, led by North America & Europe | Medium term (2-4 years) | |||

Mercury-free mandates in GCC countries Mercury-free mandates in GCC countries | +0.7% | Middle East, spill-over to Asia-Pacific | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Expanding adoption of plasma grow lights in high-value vertical farms across Asia

Commercial vertical-farm operators are selecting plasma systems for the broad, uniform spectrum needed to optimize photosynthesis in premium crops. Trials in Singapore and Japan document 40% energy savings versus legacy HID lamps while maintaining yield quality.[1]Luisa Lozano-Castellanos et al., “Technologies Applied to Artificial Lighting in Indoor Agriculture,” Sustainability, mdpi.com Accelerating urbanization and food-security initiatives push municipalities to subsidize controlled-environment agriculture, reinforcing demand for adaptive IoT-enabled plasma fixtures that vary spectral recipes by growth stage. As a result, the Plasma lighting market gains a differentiated foothold in horticulture despite higher initial purchase prices, and component suppliers ramp specialized reflectors to improve canopy penetration.

Municipal retrofits targeting high-mast plasma street lighting to cut maintenance cycles in Europe

European cities pursue lifetime cost savings by replacing high-mast HID arrays with 50,000-hour electrodeless plasma lamps connected to smart-city dashboards. The long re-lamp interval reduces crane truck deployments by as much as 60% and fits procurement frameworks emphasizing total cost of ownership. Successful retrofits in Spain, Germany, and Norway showcase instant-on capability required for adaptive dimming strategies tied to pedestrian density. These public-sector exemplars strengthen regional specifications that reference flicker-free plasma performance, lifting contract visibility for OEMs across the Plasma lighting market through 2027.

Demand for ultra-high CRI lighting for film and broadcast studios in North America

Content producers filming in 8K and high-frame-rate formats specify plasma luminaires that exceed 97 CRI while eliminating temporal flicker across any shutter angle. The ability to light large sets without the heat profile of tungsten fixtures reduces HVAC load and generator capacity, lowering shoot logistics costs. Rental houses highlight reduced consumable spend because electrode-less lamps hold output over thousands of hours, and studios cite fewer color correction steps in post-production. These performance gains keep the premium tier of the Plasma lighting market insulated from LED price erosion.

Growth of underwater and marine exploration platforms requiring high-lumen plasma fixtures

Ports, subsea research vessels, and offshore wind projects prefer sealed plasma luminaires that deliver high lumen density, neutral spectrum, and corrosion resistance. Demonstrations at Oakland and Newark ports cut lighting energy use by 65%, validating total project ROI even where fixture prices are double HID baselines.[2]Thomas Ward and Brad Lurie, “Light-Emitting Plasma Fixtures for Port Facilities,” American Society of Civil Engineers, ascelibrary.org Researchers also explore co-locating optical data links within the same housing, creating a combined illumination-and-communication module that promises new revenue pools for component makers. The persistent need for robust deep-water lighting sustains a niche yet profitable slice of the Plasma lighting market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid decline in high-power LED cost performance Rapid decline in high-power LED cost performance | -1.2% | Global, strongest in Asia-Pacific | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.2% | Geographic Relevance:Global, strongest in Asia-Pacific | Impact Timeline:Short term (≤ 2 years) |

Limited availability of qualified plasma lamp ballasts in emerging markets Limited availability of qualified plasma lamp ballasts in emerging markets | -0.4% | Africa, Latin America | Medium term (2-4 years) | |||

Thermal management challenges above 1 kW in compact fixtures Thermal management challenges above 1 kW in compact fixtures | -0.6% | Global industrial & commercial | Long term (≥ 4 years) | |||

Capital-intensive EU horticulture certification Capital-intensive EU horticulture certification | -0.3% | Europe, may spread to other regulated regions | Medium term (2-4 years | |||

| Source: Mordor Intelligence | ||||||

Rapid decline in high-power LED cost performance narrowing plasma’s value proposition

Between 2003 and 2024 high-output LED devices improved efficacy by 60% while per-lumen cost fell by 95.5%. These gains allow LED arrays to match plasma spectral quality in many tasks, eroding the traditional performance gap. Municipalities with budget ceilings often default to LEDs even where long-term plasma savings would be higher, pressuring vendors to justify lifetime advantages case by case. Consequently, the Plasma lighting market must focus on specialized formats-very wide beams, extreme CRI, or difficult environments-where LED commoditization offers limited differentiation.

Limited availability of qualified plasma lamp ballasts in emerging markets

RF drivers require advanced LDMOS transistors and precision impedance matching that only a handful of suppliers manufacture at scale.[3]S. Theeuwen, “RF-Driven Plasma Lighting,” Microwave Journal, microwavejournal.com Import dependence lengthens lead times and raises service risks, deterring buyers in Africa and parts of Latin America. The scarcity of local technicians fluent in high-frequency power electronics further limits adoption. To unlock these regions, manufacturers within the Plasma lighting industry are investing in modular driver designs with field-replaceable cartridges and offering remote diagnostics to shrink maintenance windows.

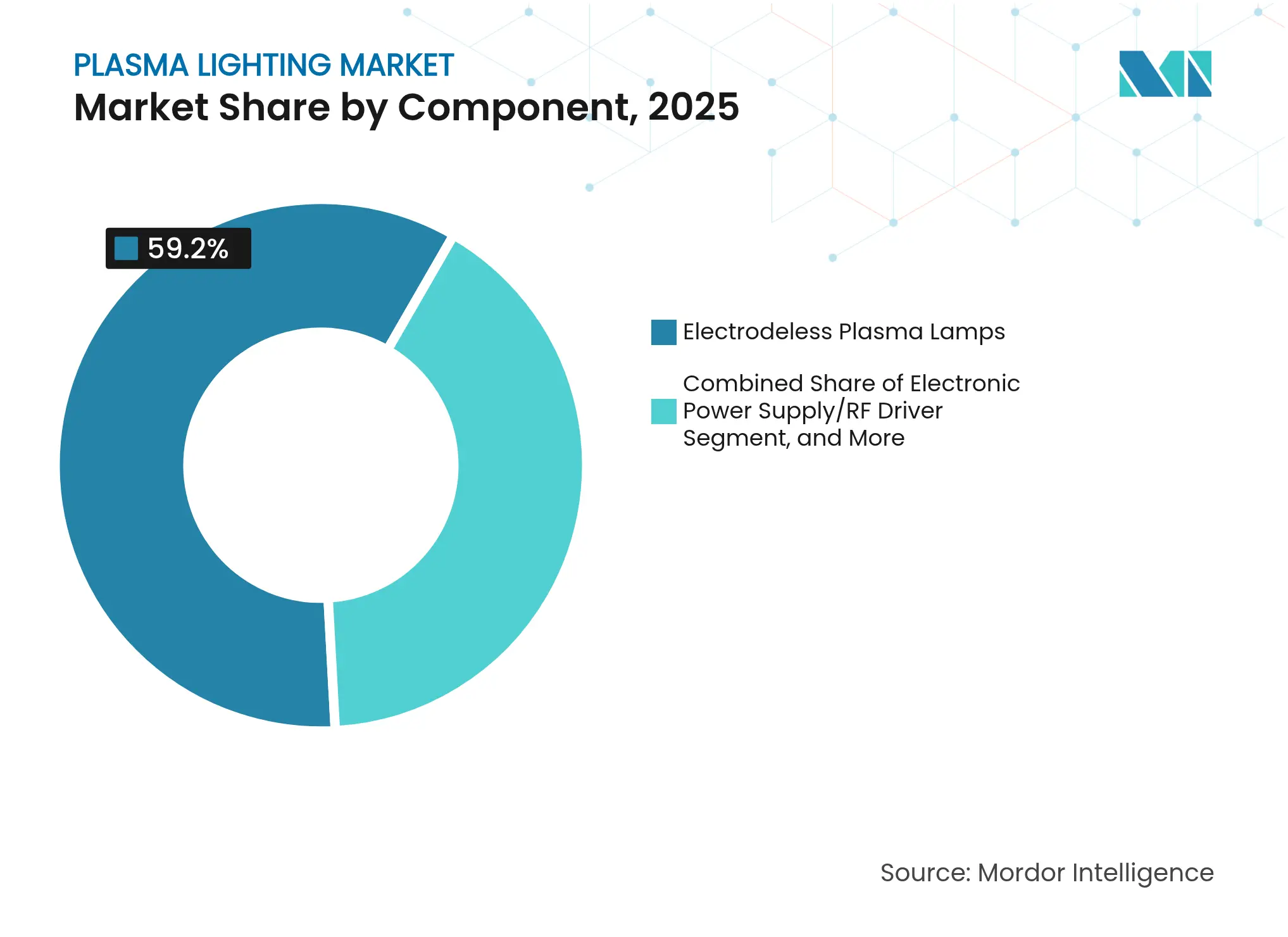

By Component: Electronic power supply drives innovation

The component mix generated USD value consistent with the overall Plasma lighting market size and is headed for reshaping as power electronics mature. Electrodeless lamps retained 59.20% revenue in 2025 thanks to their maintenance-free architecture, but RF driver revenue is projected to rise 6.99% annually to 2031 as silicon LDMOS advances lift conversion efficiency and ruggedness. New drivers also integrate digital telemetry, helping plant managers monitor lamp health and schedule replacements only when photometric output dips below set thresholds.

Reflectors now employ multi-facet aluminum optics that capture a greater share of plasma arc output, boosting fixture efficacy by almost 12%. Housing vendors add liquid micro-channels or vapor-chamber heat sinks to handle hotspot temperatures from larger drivers, while accessory makers release gateway modules that link plasma arrays into building-automation protocols. In aggregate these subsystem innovations underpin the Plasma lighting market’s ability to meet project specifications that formerly defaulted to HID or induction alternatives, cementing plasma’s premium status despite supply-chain complexity.

Note: Segment shares of all individual segments available upon report purchase

By Wattage: Thermal management shapes power distribution

Wattage distribution illustrates how thermodynamics defines addressable space for the Plasma lighting market. The 700-1000 W band kept 44.40% volume in 2025 by offering a sweet spot between luminous flux and manageable junction temperature. Application engineers regard this class as plug-compatible with legacy 1 kW metal-halide luminaires, easing retrofit decisions and supporting the Plasma lighting market share lead at this rating.

Below 700 W, shipments rise 4.73% per year as compact urban farms, architectural façades, and retail environments endorse slimmer fixtures. Vendors deploy graphite-enhanced heat spreaders, phase-change materials, and active airflow channels to scale output without exceeding 90 °C board temperature. Conversely, the ≥ 1 kW class stagnates until liquid cooling costs fall or adjacent LED arrays fail to supply needed punch. This segmentation points to incremental but realizable gains if driver miniaturization continues and building codes permit water-loop retrofits.

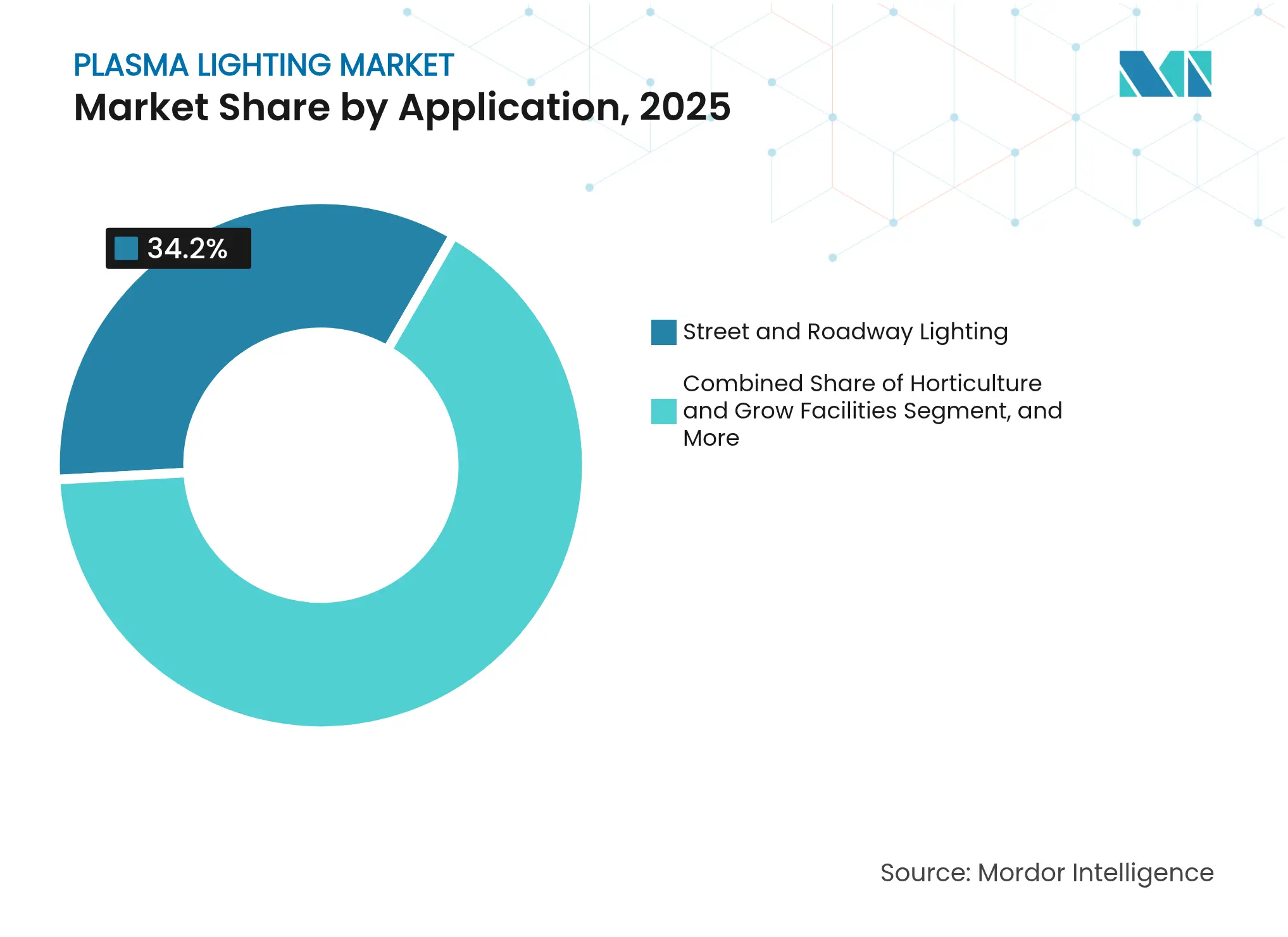

By Application: Horticulture leads growth transformation

Street and roadway schemes formed 34.20% of 2025 turnover as municipalities swapped aging HID poles for plasma units delivering uniform luminance over wide carriageways. Yet the horticulture segment expands 6.19% annually, giving vertical-farm installers confidence that the Plasma lighting market will keep pace with ambitious greenhouse construction. Because leafy greens and strawberries sell at higher margins when pigment consistency and shelf life improve, growers justify plasma as a revenue-protective tool.

Industrial and warehouse adopters value high-lumen density to reduce fixture count at tall mounting heights, while smart stadium operators appreciate the absence of flicker for 1,000 fps replays. Film studios account for a meaningful but specialized slice, leveraging 97 CRI and low infra-red output to minimize actor fatigue. Finally, marine engineers specify pressure-sealed housings that leverage plasma’s electrode-less chamber to extend service life where salt and vibration cripple other lamps.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Technical consultation drives direct sales

Direct sales secured 64.00% of the Plasma lighting market in 2025. OEM engineers partner with contractors early, modeling optical pathways and RF enclosure grounding to avoid electromagnetic interference with adjacent telecom gear. This high-touch model also supports life-cycle costing bids that demonstrate lower OPEX relative to LEDs in demanding locales.

A 5.22% CAGR for distributors and integrators signals progress toward catalog-grade products. Larger integrators bundle plasma floodlights with solar PV, motion sensors, and wireless mesh controls, offering turnkey packages to mid-tier municipalities. Training programs certify third-party technicians, which gradually lessens reliance on factory staff and should diversify the Plasma lighting industry’s revenue geography by the decade’s close.

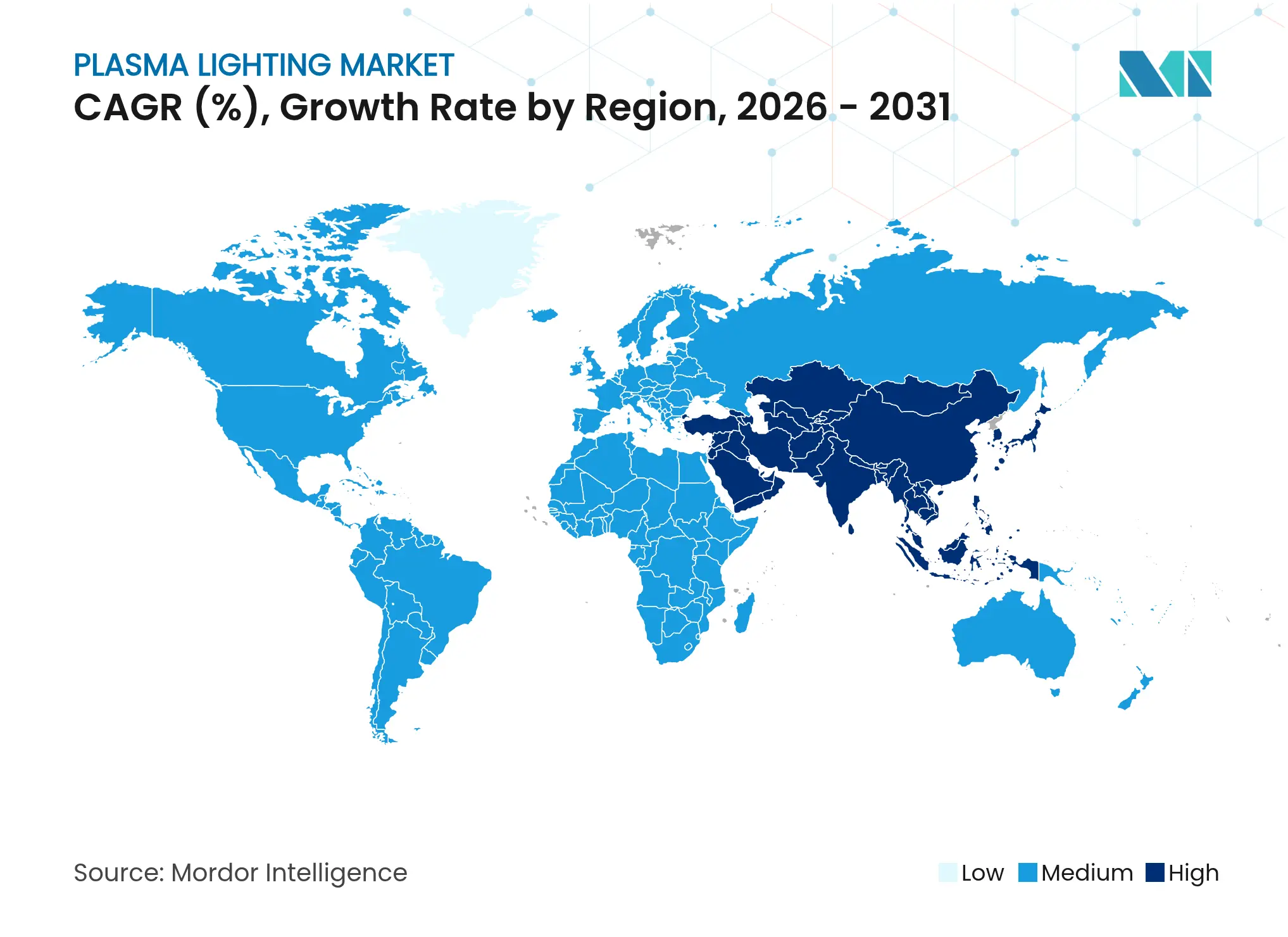

Europe, holding 29.40% of global sales in 2025, benefits from eco-design rules that remove mercury lamps from procurement lists. Coupled with aging high-mast poles that incur costly lane closures for maintenance, plasma’s 50,000-hour rating anchors vendor frameworks in Germany, Spain, and the Nordics. Regional smart-city programs feed data from luminaire sensors into traffic-management suites, enhancing safety and optimizing dimming schedules to cut emissions.

Asia-Pacific is forecast to expand at 5.61% CAGR as China’s tunnel upgrades, Japan’s resilient street-light pilots, and Singapore’s automated greenhouses create fertile ground for plasma solutions. Local RF-electronics clusters in Shenzhen and Osaka shorten lead times and allow iterative driver revisions tailored to indigenous grid conditions. Investors’ CNY 785 million commitment to LUSTER LightTech underscores confidence that domestic suppliers will capture a larger slice of the Plasma lighting market by mid-decade.

North America records moderate expansion anchored in ultra-high CRI requirements for Hollywood sound stages and the Gulf Coast’s offshore oil platforms. Professional sports arenas from Dallas to Toronto replaced metal-halide rigs with plasma to guarantee flicker-free HDTV broadcast rights, and operators report shorter reboot intervals after power faults. Regulatory regimes emphasize safety and photobiological compliance, favoring plasma’s negligible UV output in occupied spaces. Collectively, the three regions sustain the Plasma lighting market’s global relevance despite localized swings in commodity LED pricing.

Market Concentration

The Plasma lighting market is structurally fragmented, with numerous niche specialists rather than a single dominant brand. Entry barriers arise from proprietary driver designs, know-how in vacuum-arc chamber fabrication, and the ability to tune spectral output for vertical farming, marine, or broadcast needs. Top vendors focus on end-to-end solutions-combining lamps, RF drivers, optics, and control software-to lock in replacement-part revenue and defend margins against LED substitutes.

Strategically, suppliers pursue vertical integration. Driver makers collaborate with ceramic chamber producers to co-optimize impedance and heat extraction, yielding packages that pass military-grade shock tests sought by defense shipyards. Others partner with agritech firms to overlay sensor-driven dimming algorithms on plasma arrays, unique IP that shifts competition away from upfront lumens per watt and toward yield per kilowatt hour.

White-space opportunities include pairing plasma luminaires with underwater optical-communication modules, enabling tetherless data collection at offshore wind foundations. Academic consortia funded by the UK Atomic Energy Authority are also trialing plasma-resistant sensor housings for fusion reactors, potentially spawning adjacent demand for radiation-hardened lighting.[4]Heping Xie, “Direct Seawater Electrolysis Platform,” Nature Communications, nature.com In sum, differentiation through application expertise and accessory ecosystems helps players secure wallet share in a market where volumetric economies of scale remain elusive.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Light Emitting Plasma (LEP) is a high-intensity light source that shares the same benefits as LED, like longevity and reliability, but has a much greater lumen density (up to 200 times greater) and can distribute light evenly across wide areas such as ports, street lights etc. The full-colour spectrum of the plasma lights provides a greater than 2 times advantage over HPS in nighttime visibility.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.