Arbitrary Waveform Generator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

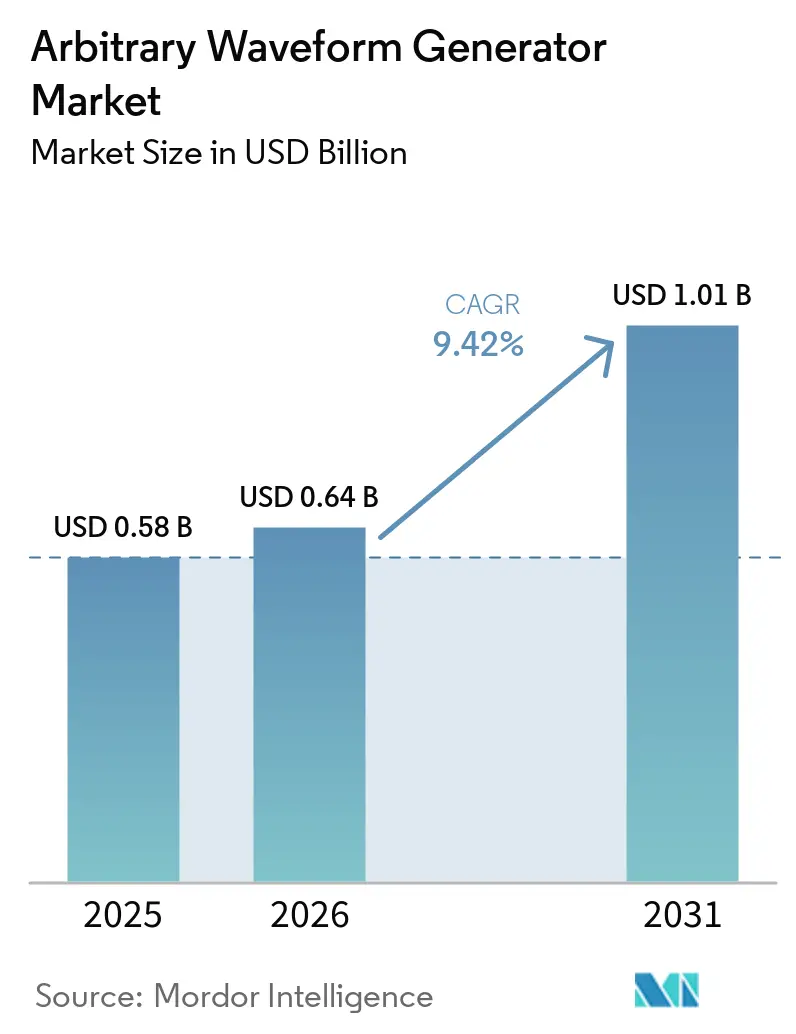

| Market Size (2026) | USD 0.64 Billion |

| Market Size (2031) | USD 1.01 Billion |

| Growth Rate (2026 - 2031) | 9.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Arbitrary Waveform Generator Market Analysis by Mordor Intelligence

The arbitrary waveform generator market size is expected to grow from USD 0.58 billion in 2025 to USD 0.64 billion in 2026 and is forecast to reach USD 1.01 billion by 2031 at a 9.42% CAGR over 2026-2031. Heightened demand from 6G trials, quantum-computing control systems, and imaging automotive radar is pushing waveform generators beyond conventional frequency and jitter limits. Semiconductor automated-test budgets expanded sharply in 2025, converting these instruments into bottlenecks for millimeter-wave validation and multi-channel qubit manipulation. Leading vendors are embedding real-time digital signal-processing engines so users can inject impairments on the fly instead of reloading multi-gigabyte files, which reduced setup cycles on advanced-packaging test floors. Meanwhile, pricing pressure at mid-tier original-equipment manufacturers is accelerating the shift toward cloud-hosted and subscription models that lower capital outlay yet preserve access to cutting-edge hardware.

Key Report Takeaways

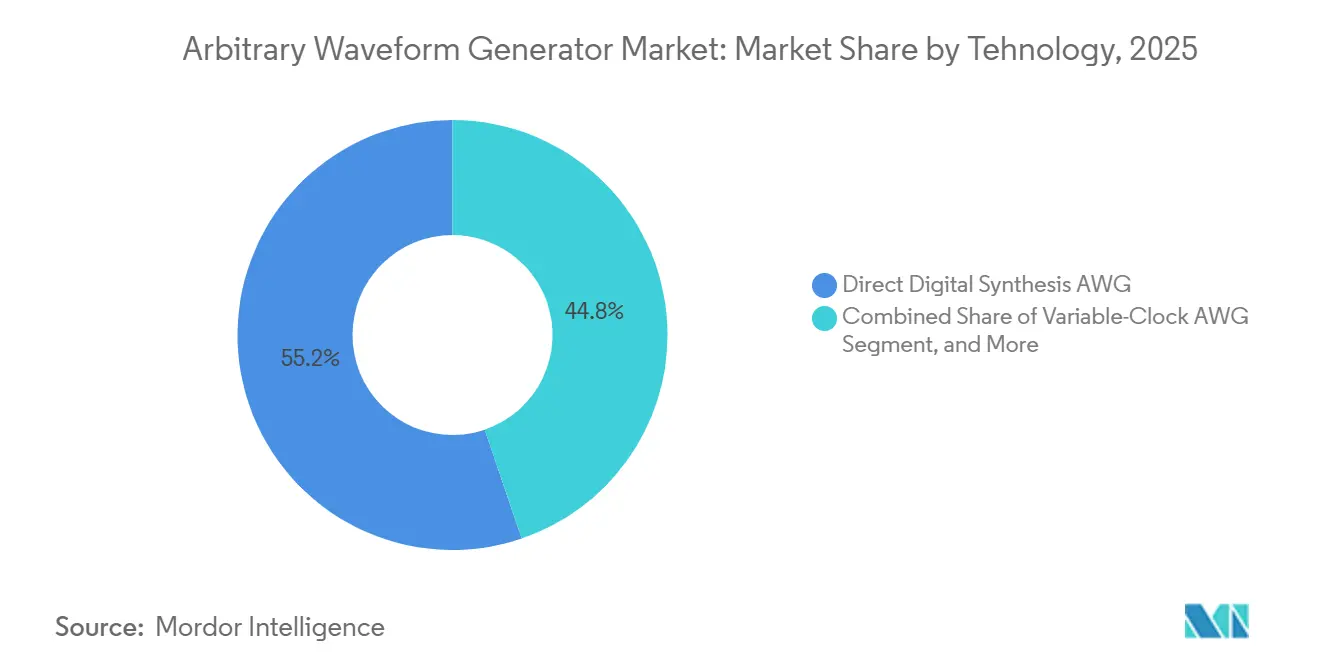

- By technology, direct digital synthesis led with 55.22% of the arbitrary waveform generator market share in 2025, while combined architectures are projected to expand at a 9.10% CAGR through 2031.

- By product, dual-channel configurations captured 60.22% revenue share in 2025 and are expected to grow at a 10.20% CAGR as I-Q modulation and dual-polarization coherent-optical links proliferate.

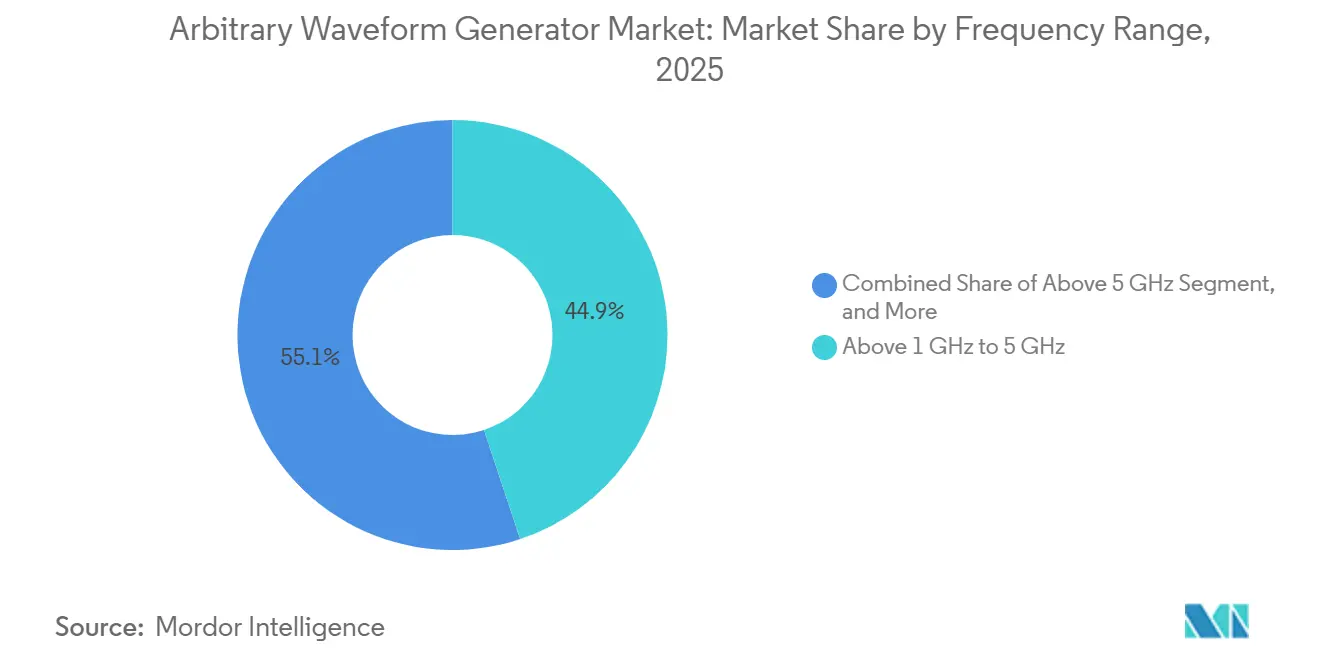

- By frequency range, units above 5 GHz are forecast to rise at a 9.27% CAGR, outpacing the 1 GHz-to-5 GHz segment that dominated with 44.90% revenue share in 2025.

- By end-user industry, electronics and semiconductor accounted for 29.10% demand in 2025, whereas quantum-computing laboratories represent the fastest-growing niche at a 10.45% CAGR through 2031.

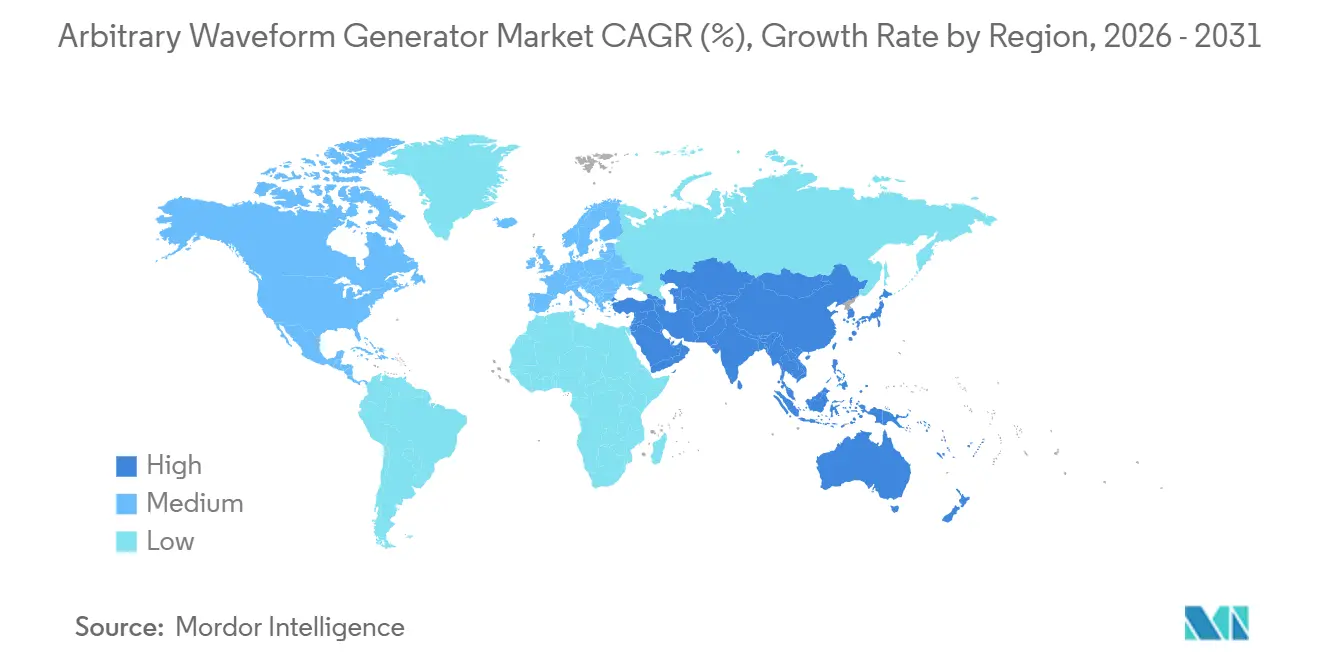

- By geography, North America retained 36.82% share in 2025, yet Asia-Pacific is advancing at a 10.67% CAGR on the back of domestic fab expansion and national 6G consortia.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Arbitrary Waveform Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Complexity of 5G and 6G RF Signal Testing | +2.8% | Global, strongest in North America, Europe, Asia‑Pacific | Medium term (2–4 years) |

| Semiconductor Rapid Prototyping and Automated Test‑Equipment Growth | +2.3% | Asia‑Pacific core, with spillover to North America and Europe | Short term (≤ 2 years) |

| Quantum‑Computing Demand for Ultra‑Channel Pulse Control | +1.9% | United States, Netherlands, Germany, United Kingdom | Long term (≥ 4 years) |

| Automotive Radar Systems Migrating Beyond 77 GHz | +1.2% | Europe, Japan, South Korea, with global rollout | Medium term (2–4 years) |

| High‑Resolution DACs Becoming Industry Standard | +0.8% | Global | Short term (≤ 2 years) |

| Adoption of Photonic‑Integrated AWGs for Optical I/O | +0.5% | North America, Europe, Japan, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Complexity of 5G and 6G RF Signal Testing

6G research prototypes reach carriers near 300 GHz and integrate sensing with communications, forcing test labs to generate terahertz-scale waveforms with sub-picosecond timing accuracy.[1]Nature Reviews Electrical Engineering, “6G Wireless Communications: Vision and Potential Techniques,” nature.com Field trials in South Korea and Japan confirmed that beam-steering errors under 0.5 degrees at 100 GHz halve link range, so engineers now replicate multipath fading, antenna-array defects, and Doppler shifts inside the arbitrary waveform generator itself rather than external software. The IEEE 802.11be Wi-Fi 7 amendment, ratified in 2024, likewise added 320 MHz channels and 4096-QAM, demanding 80 dB spurious-free dynamic range to avoid masking adjacent-channel leakage. Vendors responded by embedding field-programmable-gate-array impairment engines that let users adjust phase noise or I-Q imbalance on the fly, cutting reload times from minutes to seconds. Activity is concentrated in regions leading 6G spectrum allocation, yet the resulting specification uplift is permeating every major wireless laboratory.

Semiconductor Rapid Prototyping and Automated Test-Equipment Growth

Automated-test spending surged as foundries raced to qualify 3 nm and 2 nm nodes, requiring waveform generators that emulate PCIe 6.0 and USB4 Version 2.0 lanes at 64 GT-s and 80 Gb-s. Taiwan- and South Korea-based fabs installed multi-channel platforms supporting femtosecond-level coherence across 8 or 16 outputs to validate die-to-die chiplet links. Because any delay in delivery stalls billion-dollar product launches, lead times for high-end units stretched beyond six months. North American and European design houses also need short-lived prototypes before committing to tape-out, so demand concentrates in the 0-to-2-year window, underpinning the short-term growth outlook.

Quantum-Computing Demand for Ultra-Channel Pulse Control

Superconducting processors scaling toward 1,000 qubits must issue nanosecond-scale microwave pulses on hundreds of synchronized channels while maintaining 0.1% amplitude stability. IBM, Google, and European consortia published roadmaps linking logical-qubit milestones directly to control-electronics performance, propelling vendors to rack-mount 100-channel systems that calibrate skew in femtoseconds and update pulse envelopes within 100 ns feedback cycles. Cryogenic digital-to-analog converters remain experimental, so room-temperature instruments must drive signals through long coaxial runs, multiplying the need for precise pre-distortion. As public and private investment topped USD 10 billion in 2025, quantum laboratories now anchor the long-term demand curve.

Automotive Radar Systems Migrating Beyond 77 GHz

Regulators in Europe will mandate imaging-radar capabilities on all new vehicles by 2028, motivating suppliers such as Bosch and Continental to validate 4 D perception sensors that operate above 79 GHz. Arbitrary waveform generators must synthesize 4 GHz-wide chirp sequences with on-off ratios above 60 dB to mimic clutter from guardrails, tunnels, and adverse weather. ISO 26262 updates require hardware-in-the-loop coverage of corner cases, so production lines are adding gigasample-memory instruments capable of cycling through hundreds of synthetic targets per module. Because automotive design cycles span three to five years, procurement in 2026 underwrites modules entering mass production between 2029 and 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital Spending Freezes at Mid‑Tier Device OEMs | −1.5% | North America and Europe most affected | Short term (≤ 2 years) |

| Lack of Skilled Operators for Ultra‑Fast Gear | −1.1% | Asia‑Pacific and North America | Medium term (2–4 years) |

| Rising Competition from Vector Signal Generators | −0.7% | Global | Short term (≤ 2 years) |

| Uncertainty Around Cryogenic IC Development | −0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital Spending Freezes at Mid-Tier Device OEMs

Component inflation and soft consumer demand narrowed margins at many mid-tier manufacturers, prompting 38% of surveyed firms to postpone waveform-generator upgrades planned for 2026. These customers extended legacy-instrument life through firmware patches and third-party calibration, depressing mid-range unit shipments even as high-end backlogs swelled. Vendors now offer leasing and pay-per-use lab access, but data-sovereignty and latency concerns confine uptake to non-critical tasks. The impact should ease within two years once macro visibility improves.

Lack of Skilled Operators for Ultra-Fast Gear

Operating instruments above 10 GS-s demands mastery of Nyquist-zone mapping, pre-distortion, and S-parameter de-embedding, skills seldom taught outside specialized graduate programs. Liquid Instruments reports that many customers book extended commissioning for its 5 GS-s platform because in-house engineers cannot configure multi-instrument pipelines. Workforce gaps are most severe in rapidly expanding Asian fabs and among retiring North American specialists. Vendors are integrating AI-driven setup wizards, yet widespread proficiency will take three to five years of coordinated education and certification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Direct Digital Synthesis Dominates, Combined Architectures Gain Traction

Direct digital synthesis held 55.22% revenue share in 2025, benefiting from deterministic phase control and spurious-free dynamic range beyond 80 dBc, attributes vital for coherent-optical modulation and qubit manipulation. This dominance reinforced the arbitrary waveform generator market size leadership of the segment, yet combined architectures are projected to expand at a 9.10% CAGR because they merge variable-clock agility with RF precision in a single chassis.

Variable-clock models remain relevant where sample-rate flexibility outweighs phase coherence, for example when mimicking irregular sensor outputs or generating pulse-width-modulation signals for power electronics. IEEE 1658 revisions favor direct digital synthesis on dynamic-linearity metrics, but Zurich Instruments’ hybrid platform illustrates how vendors can bridge use cases without forcing labs to purchase multiple boxes, protecting adoption across mixed-signal environments.[2]IEEE, “IEEE 1658 Standard for ADC and DAC Testing (2024 Revision),” ieee.org

By Product: Dual-Channel Configurations Lead on I-Q and Coherent-Optical Demand

Dual-channel units captured 60.22% share in 2025 and are forecast to grow at a 10.20% CAGR. Their ability to drive I-Q modulators or dual-polarization photonics transceivers cements their lead, and falling cost premiums encourage even cost-sensitive labs to adopt two outputs. Keysight’s flagship 65 GS-s model became the benchmark reference for coherent-optical research, illustrating how a single module can generate four baseband channels for 400 Gb-s links, thereby raising the arbitrary waveform generator market share concentration within high-performance tiers.

Single-channel instruments still serve applications such as clock-jitter injection or university teaching labs, but their relevance erodes as integrated platforms like Liquid Instruments’ 4-output device enter the sub-USD 20,000 price band. This democratization broadens adoption yet simultaneously cements dual-channel as the de facto baseline for mainstream RF and photonics validation.

By Frequency Range: Above 5 GHz Segment Accelerates on Millimeter-Wave and Imaging Radar

Units covering 1 GHz-to-5 GHz generated 44.90% revenue in 2025, anchored by sub-6 GHz 5G nodes and 77 GHz radar modules that rely on baseband generation followed by up-conversion. However, the above-5 GHz tier is advancing at a 9.27% CAGR as 6G trials and 100 GHz imaging radar require direct RF synthesis up to 20 GHz or more, inflating the arbitrary waveform generator market size for this premium category.

Tektronix’s 50 GS-s platform typifies the high-end: it delivers 10 GHz instantaneous bandwidth and -80 dBc spurious-free dynamic range for electronic-warfare and coherent-optical testing. At the opposite end, Active Technologies’ deep-memory devices satisfy automotive and industrial engineers who prioritize 512 M-point pattern depth over headline sample rate, demonstrating that memory-rich mid-bandwidth units can still carve profitable niches.

By End-User Industry: Electronics and Semiconductor Lead, Quantum Computing Labs Surge

Electronics and semiconductor companies commanded 29.10% demand in 2025 by outfitting automated-test handlers with multi-channel waveform generators to exercise PCIe 6.0, USB4 V 2.0, and chiplet links. The arbitrary waveform generator market size tied to this segment should remain stable through enormous fab expansions in Asia-Pacific, yet the 10.45% CAGR growth crown shifts to quantum-computing laboratories as qubit counts climb.

Telecom OEMs rely on up to 256-antenna massive-MIMO trials, pushing some labs toward eight or more synchronized channels, while aerospace and defense users continue to procure wideband gear for electronic-warfare scenarios. Automotive customers are beginning to place waveform generators on production lines so every radar module sees 100% functional test, a change that favors lower-cost, batch-optimized units. Education, healthcare, and other verticals collectively form a steady but smaller revenue stream, often adopting software-defined platforms where firmware swaps extend instrument life.

Geography Analysis

In 2025, North America accounted for 36.82% of the revenue, driven by its well-established quantum-computing hubs, robust aerospace procurement activities, and the presence of leading semiconductor design houses. These factors collectively reinforce the region's dominant position in the arbitrary waveform generator market, ensuring its continued leadership. The region's advanced technological infrastructure and strong R&D capabilities further contribute to its market strength.

Meanwhile, the Asia-Pacific region is projected to grow at a notable 10.67% CAGR, fueled by significant investments from countries such as China, South Korea, and Japan. These nations are focusing on developing domestic semiconductor fabrication facilities (fabs) and establishing 6G research clusters, which are expected to drive substantial growth in the region. This strategic focus on innovation and infrastructure development is gradually shifting the center of volume growth toward the east.

Europe maintains a solid foundation in the market, supported by Germany's expertise in automotive radar technologies and the European Union's funding for photonics projects. These initiatives underscore the region's commitment to technological advancement and its ability to sustain a competitive edge. On the other hand, South America and the Middle East, while still in the early stages of market development, are emerging as strategically important regions. They are poised to play a critical role in future applications such as smart-city projects and satellite backhaul systems, which are expected to gain traction in the coming years.

Competitive Landscape

The market is moderately concentrated: Keysight Technologies, Tektronix, and Rohde and Schwarz together held roughly 55%-60% share in 2025. These incumbents compete by pushing sample-rate ceilings past 65 GS-s, embedding field-programmable-gate-array engines for real-time impairment insertion, and locking users into proprietary software suites. Challenger brands such as Liquid Instruments and Zurich Instruments exploit reconfigurable architectures that fold oscilloscope, spectrum, and waveform functions onto a single chip, enabling smaller labs to conserve rack space and synchronize instruments with sub-picosecond skew.

Strategic moves illustrate divergent roadmaps. Keysight refreshed its 65 GS-s generator with femtosecond inter-channel calibration and runtime digital-signal-processing tweaks that shorten coherent-optical test cycles. Zurich Instruments debuted a 100-channel quantum-control rack in March 2026, leveraging Rohde and Schwarz’s RF heritage after their earlier acquisition to address scalability bottlenecks in error-corrected qubit arrays.[3]Zurich Instruments, “Arbitrary Waveform Generators,” zhinst.com Liquid Instruments introduced agentic AI configuration in June 2025, letting operators describe waveforms in plain English, which could mitigate the global skills shortage.

White-space entrants focus on subscription access or application-specific plug-ins: spectrum analyzer, radar target simulator, or photonics impairment generator modules install via firmware keys, allowing labs to unlock features only when required. Consolidation is probable as vendors decide whether to invest in 100 GS-s silicon or cede high-end territory to neighbors, while niche providers may survive by targeting automotive radar production test or mid-bandwidth industrial automation with memory-rich value models.

Arbitrary Waveform Generator Industry Leaders

Keysight Technologies

TEKTRONIX, INC.

Rohde & Schwarz

SIGLENT TECHNOLOGIES

Anritsu

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The National Institute of Standards and Technology (NIST) has released a combined synopsis/solicitation for the procurement of an arbitrary waveform generator. The required specifications include a new unit with a minimum sampling rate of 6 GSa/s, 4 Gpts of waveform memory, two analog channels, and calibration traceable to SI units. This equipment will support applications in absolute magnetometer research and semiconductor supply chain metrology.

- March 2026: Zurich Instruments released its Quantum Computing Control System integrating up to 100 synchronized arbitrary-waveform channels in one rack.

- February 2026: Montana State University issued a brand-specific IFB for a Keysight M8196A 92 GSa/s arbitrary waveform generator, with bids due on February 13, 2026.

- September 2025: GW Instek introduced the GPP-1000 series power supplies featuring built-in arbitrary waveform generation for sub-USD 5,000 test benches.

Global Arbitrary Waveform Generator Market Report Scope

The Arbitrary Waveform Generator Market comprises entities that design and supply advanced electronic instruments capable of generating user-defined electrical waveforms with high precision. These devices are extensively utilized in research and development, telecommunications, aerospace, defense, medical equipment testing, and semiconductor manufacturing, where the simulation and validation of complex signals are essential.

The Arbitrary Waveform Generator Market Report is Segmented by Technology (Direct Digital Synthesis AWG, Variable-Clock AWG, Combined AWG), Product (Single-Channel, Dual-Channel), Frequency Range (Up to 1 GHz, Above 1 GHz to 5 GHz, Above 5 GHz), End-User Industry (IT and Telecommunications, Aerospace and Defense, Electronics and Semiconductor, Automotive, Healthcare, Education and Other End-User Industries), and Geography (North America, Europe, South America, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Direct Digital Synthesis AWG |

| Variable-Clock AWG |

| Combined AWG |

| Single-Channel |

| Dual-Channel |

| Up to 1 GHz |

| Above 1 GHz to 5 GHz |

| Above 5 GHz |

| IT and Telecommunications |

| Aerospace and Defense |

| Electronics and Semiconductor |

| Automotive |

| Healthcare |

| Education and Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Bahrain | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Technology | Direct Digital Synthesis AWG | |

| Variable-Clock AWG | ||

| Combined AWG | ||

| By Product | Single-Channel | |

| Dual-Channel | ||

| By Frequency Range | Up to 1 GHz | |

| Above 1 GHz to 5 GHz | ||

| Above 5 GHz | ||

| By End-User Industry | IT and Telecommunications | |

| Aerospace and Defense | ||

| Electronics and Semiconductor | ||

| Automotive | ||

| Healthcare | ||

| Education and Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Kuwait | ||

| Bahrain | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the arbitrary waveform generator market?

The arbitrary waveform generator market was valued at USD 0.64 billion in 2026, according to Mordor Intelligence.

How fast will the market grow over the next five years?

Between 2026 and 2031, the market is projected to register a 9.42% CAGR, driven by 6G trials, quantum-computing scale-ups, and millimeter-wave radar adoption.

Which technology segment holds the largest revenue share?

Direct digital synthesis platforms led with 55.22% revenue share in 2025 thanks to deterministic phase control and high spurious-free dynamic range.

Which region generates the highest demand for arbitrary waveform generators?

North America retained the lead with 36.82% revenue share in 2025, propelled by aerospace-defense procurement and quantum-computing test beds.

What end-user industry is expanding the fastest?

Quantum-computing laboratories are forecast to post a 10.45% CAGR through 2031 as qubit counts and channel requirements grow rapidly.

Who are the top three market players?

Keysight Technologies, Tektronix, and Rohde and Schwarz collectively controlled close to 60% of revenue in 2025.

Page last updated on: