RF Front End Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

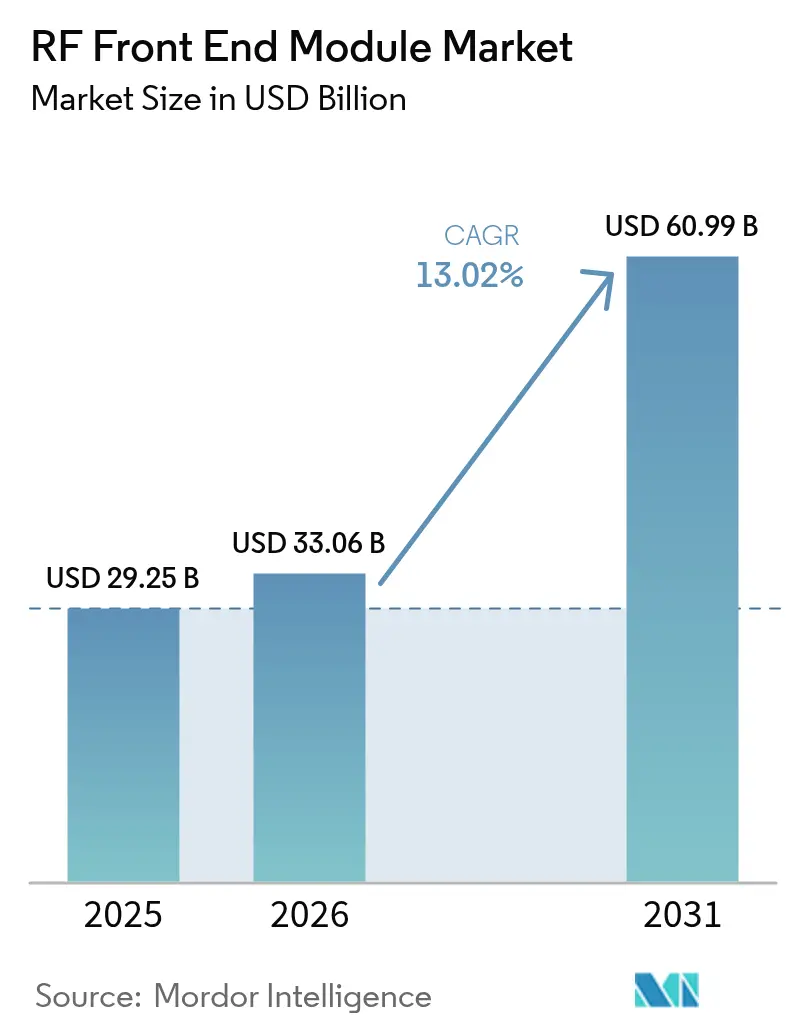

| Market Size (2026) | USD 33.06 Billion |

| Market Size (2031) | USD 60.99 Billion |

| Growth Rate (2026 - 2031) | 13.02% CAGR |

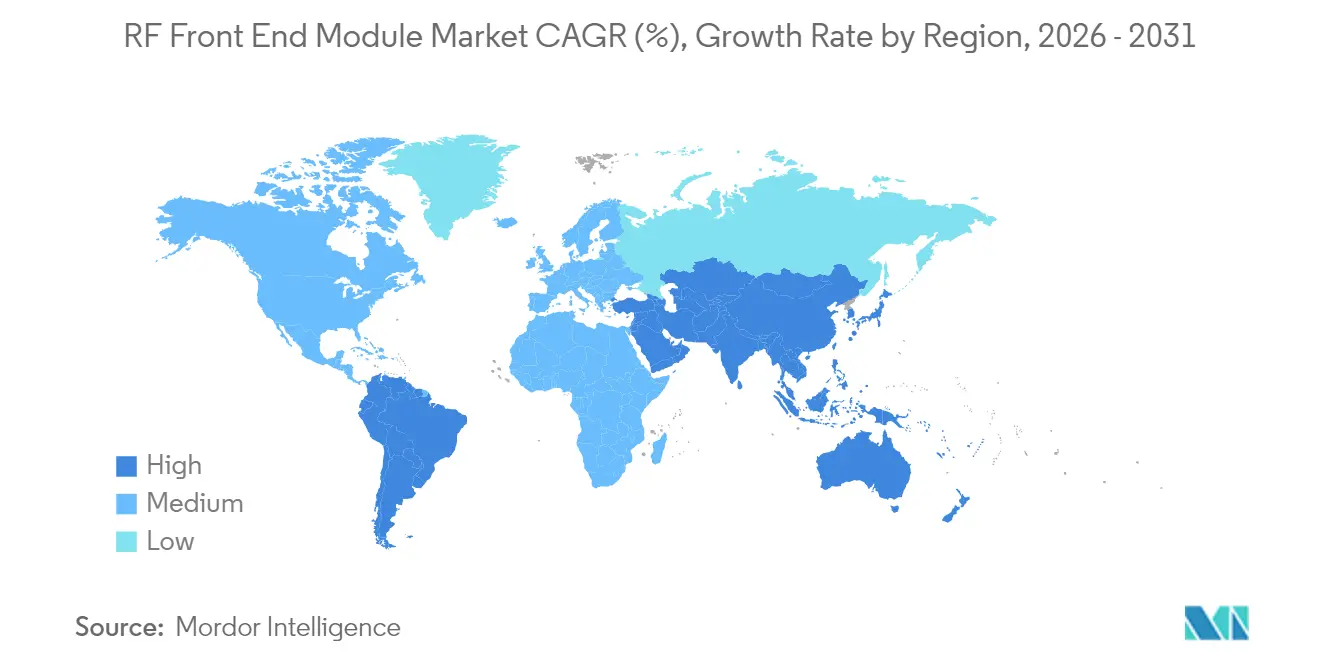

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

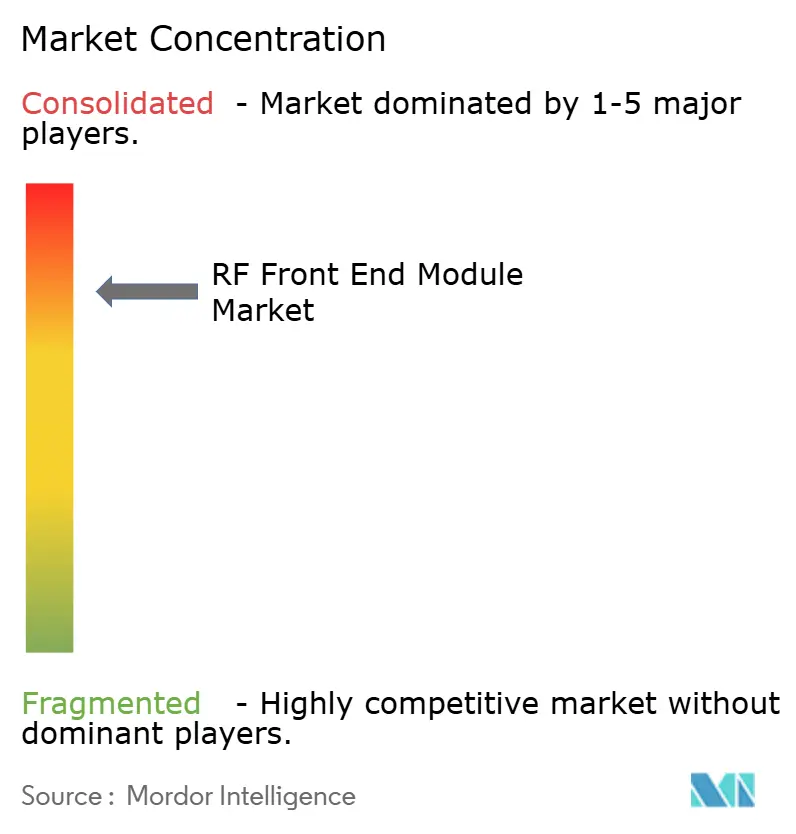

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RF Front End Module Market Analysis by Mordor Intelligence

The RF front-end module market size is expected to grow from USD 29.25 billion in 2025 to USD 33.06 billion in 2026 and is forecast to reach USD 60.99 billion by 2031 at 13.02% CAGR over 2026-2031. Demand acceleration stems from smartphone makers insisting on single-package RF solutions that free board space, while network operators push for higher performance density. The convergence of mass-scale 5G sub-6 GHz coverage and the first commercial mmWave fixed-wireless access rollouts adds momentum. Integrated designs also mitigate thermal stress and shorten design cycles, giving suppliers who master system co-optimization a clear edge. Meanwhile, gallium and wafer capacity constraints encourage long-term supply partnerships and drive regional investments in compound-semiconductor fabs.[1]Source: WIN Semiconductors, “2024 Capacity Expansion Announcement,” winsemi.com

Key Report Takeaways

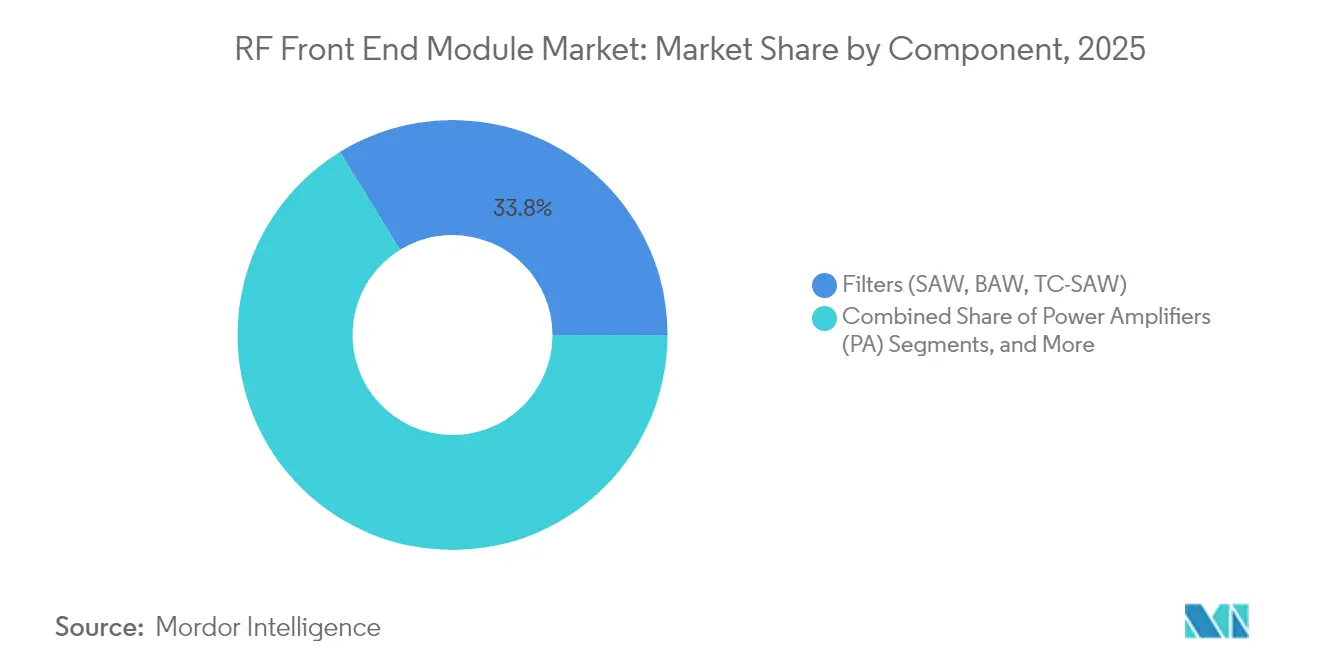

- By component, filters held 33.78% of the RF front end module market share in 2025; antenna tuners are projected to expand at a 13.98% CAGR through 2031.

- By application, consumer electronics led with 67.35% revenue share in 2025; automotive is forecast to advance at a 14.21% CAGR to 2031.

- By frequency range, sub-6 GHz accounted for 73.45% share of the RF front end module market size in 2025; mmWave (24–47 GHz, FR2) is forecast to advance at a 13.72% CAGR to 2031.

- By geography, Asia-Pacific commanded 56.88% share in 2025; Middle East and Africa is positioned to post the fastest 13.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global RF Front End Module Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive 5G design-wins in sub-6 GHz smartphones | +3.2% | Global, led by APAC and North America | Short term (≤ 2 years) |

| Rapid mmWave adoption in fixed wireless access (FWA) CPE | +2.8% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| OEM push for integrated modem-to-antenna platforms | +2.1% | Global, concentrated in premium segments | Medium term (2-4 years) |

| GaAs wafer capacity expansion in Taiwan and China | +1.9% | APAC core, supply benefits global | Long term (≥ 4 years) |

| Defense demand for GaN-based AESA radar modules | +1.7% | North America, EU, select APAC markets | Long term (≥ 4 years) |

| "Right-to-Repair" laws extending handset lifecycles | +0.8% | EU and select US states, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive 5G Design-Wins in Sub-6 GHz Smartphones

Carrier rollouts prioritize blanket coverage, making sub-6 GHz the volume engine for the RF front end module market. Samsung’s adoption of the SKY5 platform trimmed board area by 30% while boosting battery endurance.[2]Source: Skyworks Solutions, “Skyworks Announces Collaboration with Samsung,” skyworksinc.com Device makers now rate RF performance alongside camera quality when defining premium tiers. Tight footprints, multi-band carrier aggregation, and stricter SAR limits favor consolidated FEMs over discrete chains. Suppliers with algorithm-assisted envelope tracking add power efficiency, a point that resonates with sustainability targets. The result is a virtuous cycle in which every design win feeds production scale that, in turn, lowers per-unit cost.

Rapid mmWave Adoption in Fixed-Wireless Access (FWA) CPE

Verizon’s service footprint grew to 40 million homes in 2024, confirming the economic logic of mmWave FWA.[3]Source: Verizon, “Verizon 5G Home Internet Expansion 2024,” verizon.com CPE devices accept bigger antennas, so each install embeds four to eight mmWave RF chains-up to 4× the smartphone content. Higher bill-of-materials value per node lifts the RF front end module market even with moderate unit volumes. Policy makers allocate spectrum preferentially to fixed services, reducing interference risk and facilitating beam-steering antennas that remain stationary. Suppliers that master thermal dissipation in outdoor units secure sizable margins, because mmWave PAs still command premium ASPs.

OEM Push for Integrated Modem-to-Antenna Platforms

Qualcomm and TDK formed RF360 with a USD 3 billion valuation, linking baseband IP and discrete RF skills into turnkey stacks.[4]Source: Qualcomm, “Qualcomm-TDK RF360 Holdings Joint Venture,” qualcomm.com Mid-tier handset brands lacking custom RF expertise gravitate toward such platforms, thus concentrating demand on vendors that offer silicon-to-antenna coverage. Platform control shifts bargaining power away from discrete specialists, pressuring them to buy or license missing elements. Integration also trims software validation cycles, a value proposition when launch windows shrink. The RF front end module market therefore tilts toward vendors able to synchronize firmware, filters, PAs, and tuners in one reference design.

GaAs Wafer Capacity Expansion in Taiwan and China

WIN Semiconductors and mainland peers are adding 40% wafer output to ease bottlenecks. Expanded fabs lower per-wafer costs, stabilizing gross margins despite falling ASPs in power amplifiers. The geographic spread mitigates single-region risk exposed during recent lockdowns. Long-term supply contracts now include audit clauses for ESG practices, ensuring continuity for defense and telecom customers. For the RF front end module industry, capacity visibility de-risks project timelines, letting OEMs plan multiyear platforms with confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Looming IP shortages for BAW filter patents | -1.8% | Global, most acute in Asia-Pacific | Medium term (2-4 years) |

| Talent gap in mmWave packaging engineers | -1.2% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Tight gallium supply chain amid export restrictions | -2.3% | Global, most severe for GaN applications | Short term (≤ 2 years) |

| On-device AI reducing RF Tx duty-cycle | -0.9% | Premium smartphone segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Looming IP Shortages for BAW Filter Patents

Foundational BAW patents near expiry, yet follow-on innovations have plateaued. Few suppliers hold the residual know-how for GHz-range Q-factor leadership, so licensing fees climb. OEMs trying to add new bands must either pay premiums or switch to TC-SAW, which can underperform in high-temperature use. Patent cliffs motivate defensive litigation that diverts R&D funds. Smaller entrants face high barriers, concentrating bargaining power with incumbents and slowing price erosion in the filter slice of the RF front end module market.

Tight Gallium Supply Chain Amid Export Restrictions

China’s curbs on gallium export tighten feedstock for GaN wafers, vital to high-power PAs. Spot prices surged in 2024, prompting OEMs to dual-source or pre-buy inventory. Defense and satellite contracts, which cannot down-bin performance, absorb higher costs, but price-sensitive infrastructure projects consider silicon LDMOS substitutes. Western governments weigh strategic stockpiles, yet ramp-up timelines for alternative refining exceed two years. Such volatility injects risk premia into long-term supply agreements, mildly tempering the RF front-end module market CAGR despite ongoing volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Integration Consolidates Value Pools

Filters controlled a 33.78% share of the RF front-end module market in 2025 and remain indispensable for band proliferation. Antenna tuners, however, post a category-leading 13.98% CAGR as impedance-matching across a fragmented spectrum turns into a design must-have. The RF front-end module market size for hybrid FEMs is projected to climb steadily because integrating switches, LNAs, and duplexers lowers insertion loss and simplifies thermal layout. Power amplifiers face ASP compression as OEMs bundle them with controllers, though GaN processes preserve margin in high-power niches. Switches enjoy steady pull from carrier aggregation, especially as 3-CC downlink becomes mainstream in mid-band devices.

Low-noise amplifiers ride coverage-extension campaigns in rural zones, where receiver sensitivity outweighs peak data rate. Discrete duplexers stay relevant for legacy LTE bands, but next-gen time-division duplex lowers their attach rate in select 5G frequencies. Qorvo’s 2024 FEM line shaved 40% PCB footprint versus prior discrete builds, highlighting how form-factor wins can substitute for raw component performance. As a result, component vendors recalibrate roadmaps to favor highly integrated SIPs, aligning with OEM procurement strategies that reward module-level cost per function.

By Application: Automotive Upsets Consumption Hierarchy

Consumer electronics retained a 67.35% share in 2025, underscoring smartphones’ centrality to the RF front-end module market. Yet automotive applications clock a 14.21% CAGR as regulators mandate V2X capability and infotainment screens adopt Wi-Fi 7. Vehicle form-factors enable thicker boards and active-cooling PAs, widening the performance envelope. Industrial private-5G rollouts foster bespoke RF architectures tuned to factory-floor constraints, diverting some demand from broad-market chipsets. Aerospace and defense preserve premium ASPs through GaN-based AESA modules, a small-volume but margin-rich pocket.

Wireless infrastructure modules scale with mid-band macro base-station deployments, though commoditization persists as OEMs standardize RF lineups across regions. Automotive’s temperature and reliability mandates raise qualification costs but also lock in multiyear supply, stabilizing revenue. Suppliers adept at AEC-Q100 and ISO 26262 certification extract a higher share of the RF front-end module market size allocated to vehicles. Smartphone volatility, conversely, forces inventory agility, making platform reuse across price tiers a competitive requirement.

By Frequency Range: Sub-6 GHz Retains Mass, mmWave Captures Value

Sub-6 GHz held 73.45% of the RF front-end module market share in 2025, reflecting coverage-driven 5G priorities. Its unit dominance will persist, but mmWave segments expand at a 13.72% CAGR through 2031 on the back of urban densification and FWA. Suppliers bifurcate product lines: cost-optimized silicon for mid-band phones versus premium GaAs or SiGe for mmWave CPE and hotspots. Beamforming ASIC maturity lowers antenna-array bill-of-materials, trimming the adoption cost barrier for mmWave nodes. Research above 47 GHz remains exploratory, yet early 6G trials secure pipeline visibility for next-decade revenue.

The RF front-end module market size tied to mid-band frequencies benefits from high-yield processes and cheaper substrates. In contrast, mmWave modules command 2×-3× ASPs thanks to advanced packaging and phased-array complexity. Vendors capable of cross-frequency portfolios insulate themselves against cycles in any single band, while pure-play mmWave entrants bet on CAGR acceleration as spectrum demand grows.

Geography Analysis

Asia-Pacific maintained 56.88% share of the RF front end module market in 2025, powered by China’s handset output and South Korea’s dense 5G builds. Integrated supply chains encompass raw gallium refining, wafer fabrication, and module assembly, yielding cost and cycle-time advantages few regions can match. Japan’s USD 10 trillion semiconductor program strengthens local ecosystem resilience and funds compound semiconductor pilot lines.

North America leverages defense budgets and early 5G adoption to sustain high-performance design leadership. MACOM’s USD 345 million GaN expansion joins multiple advanced-packaging initiatives aimed at closing the manufacturing gap with Asia. However, component imports still dominate the volume of consumer devices, exposing OEMs to cross-border logistics risk.

Middle East and Africa posts a 13.95% CAGR as operators bypass 4G and leapfrog to standalone 5G. Government digital-economy strategies fund towers and spectrum, but device affordability dictates a sub-6 GHz focus. Europe enjoys demand from the automotive and Industry 4.0, where GDPR and supply-chain sovereignty push brands to source locally. South America and emerging ASEAN markets absorb technology transfer as suppliers chase untapped subscriber growth.

Competitive Landscape

Three dynamics now frame competition. First, systems integration overtakes discrete component specmanship. Skyworks partnered with Samsung to embed transceiver-to-antenna chains that save 30% board space, a response to OEM calls for turnkey stacks. Second, customer concentration cuts both ways: Apple’s decision to trim Skyworks orders by up to 25% revealed revenue fragility when top clients pivot sourcing. Third, patent depth in BAW filters and GaN epitaxy sustains defensive moats that slow commoditization.

The top five firms, Broadcom, Skyworks, Qorvo, Qualcomm-TDK RF360, and Murata, controlled about 60% of the RF front end module market share in 2024. Yet mid-tier challengers gain ground in automotive and industrial niches where incumbents remain phone-centric. M&A reshapes capability maps: Qorvo bought Anokiwave for beamforming ASICs, Guerrilla RF picked up a GaN PA portfolio, and pSemi introduced AI-tuned antenna modules. Price wars intensify for sub-6 GHz sockets, but mmWave and defense platforms defend margins through technology differentiation.

Intellectual-property leverage determines royalty flows, especially in filters. Vendors with aging portfolios accelerate next-gen TC-SAW or XBAR R&D to sustain licensing revenues. Contract manufacturing partnerships, particularly in Taiwan, help pure-play design houses scale output without capex overload. Sustainability metrics enter RF module RFQs, rewarding factories that document energy use and recyclable packaging.

RF Front End Module Industry Leaders

Qualcomm Technologies, Inc.

Skyworks Solutions, Inc.

Murata Manufacturing Co., Ltd.

Qorvo, Inc.

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Samsung Electronics and Skyworks Solutions disclosed a strategic partnership that integrates SKY5 platforms in Galaxy smartphones, shrinking RF board area by 30%.

- October 2024: Guerrilla RF acquired a specialized GaN PA portfolio for USD 85 million to accelerate defense and aerospace growth.

- March 2024: Qualcomm and TDK created RF360 Holdings with a USD 3 billion valuation to deliver combined modem and RF platforms for 5G and beyond.

- February 2024: MACOM announced a USD 345 million Massachusetts facility expansion to enlarge GaN RF capacity, with completion set for 2026.

Global RF Front End Module Market Report Scope

The RF front-end module incorporates all the circuitry between the antenna and at least one mixing stage of a receiver and possibly the transmitter's power amplifier.

The RF front-end module market is segmented by component (RF filters, RF switches, RF power amplifiers, and other components), application (consumer electronics, automotive, military, wireless communication, and other applications), and geography (North America (United States, Canada), Europe (Germany, United Kingdom, France, and the rest of Europe), Asia-Pacific (India, China, Japan, and the rest of Asia-Pacifc), and rest of the World (Latin America, Middle East and Africa)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments. Further, the report covers the major vendors in the market and their investments. The report also presents a comprehensive study of the geographical segmentation of the market and the impact of COVID-19 on the market.

| Power Amplifiers (PA) |

| Duplexers and Diplexers |

| Filters (SAW, BAW, TC-SAW) |

| Switches |

| Low-Noise Amplifiers (LNA) |

| Antenna Tuners |

| Integrated/Hybrid FEMs |

| Consumer Electronics (Smartphones, Wearables) |

| Automotive (ADAS, V2X Communication) |

| Wireless Communication (5G, Wi-Fi 6/6E) |

| Industrial |

| Aerospace and Defense |

| Others Applications |

| Sub-6 GHz (FR1) |

| mmWave (24-47 GHz, FR2) |

| More than 47 GHz (6G R&D bands) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Power Amplifiers (PA) | ||

| Duplexers and Diplexers | |||

| Filters (SAW, BAW, TC-SAW) | |||

| Switches | |||

| Low-Noise Amplifiers (LNA) | |||

| Antenna Tuners | |||

| Integrated/Hybrid FEMs | |||

| By Application | Consumer Electronics (Smartphones, Wearables) | ||

| Automotive (ADAS, V2X Communication) | |||

| Wireless Communication (5G, Wi-Fi 6/6E) | |||

| Industrial | |||

| Aerospace and Defense | |||

| Others Applications | |||

| By Frequency Range | Sub-6 GHz (FR1) | ||

| mmWave (24-47 GHz, FR2) | |||

| More than 47 GHz (6G R&D bands) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the RF front end module market in 2026?

The RF front end module market size is USD 33.06 billion in 2026.

What is the forecast CAGR for RF front-end modules through 2031?

The market is projected to grow at a 13.02% CAGR from 2026 to 2031.

Which region leads demand for RF front-end modules?

Asia-Pacific commands 56.88% share owing to its combined manufacturing base and 5G deployment scale.

Which segment is the fastest-growing application?

Automotive applications expand at a 14.21% CAGR as V2X and infotainment connectivity become standard.

Why are antenna tuners growing faster than other components?

Adaptive impedance matching across fragmented 5G bands lifts antenna tuner demand, driving a 13.98% CAGR.

What is driving mmWave module adoption?

Fixed-wireless access deployments allow larger CPE units that incorporate multiple mmWave RF chains, boosting module value per install.

Page last updated on: