Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Industrial Integrated Circuits Market is Segmented by IC Type (Analog, Logic, Memory, and Micro), Function (Power-Management, Signal-Processing, Sensor-Interface, and More), Technology Node (≥45 Nm, 22-32 Nm, 14-16 Nm, and ≤10 Nm), End-Use Industry (Factory Automation, Process Automation, Energy and Power Infrastructure, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

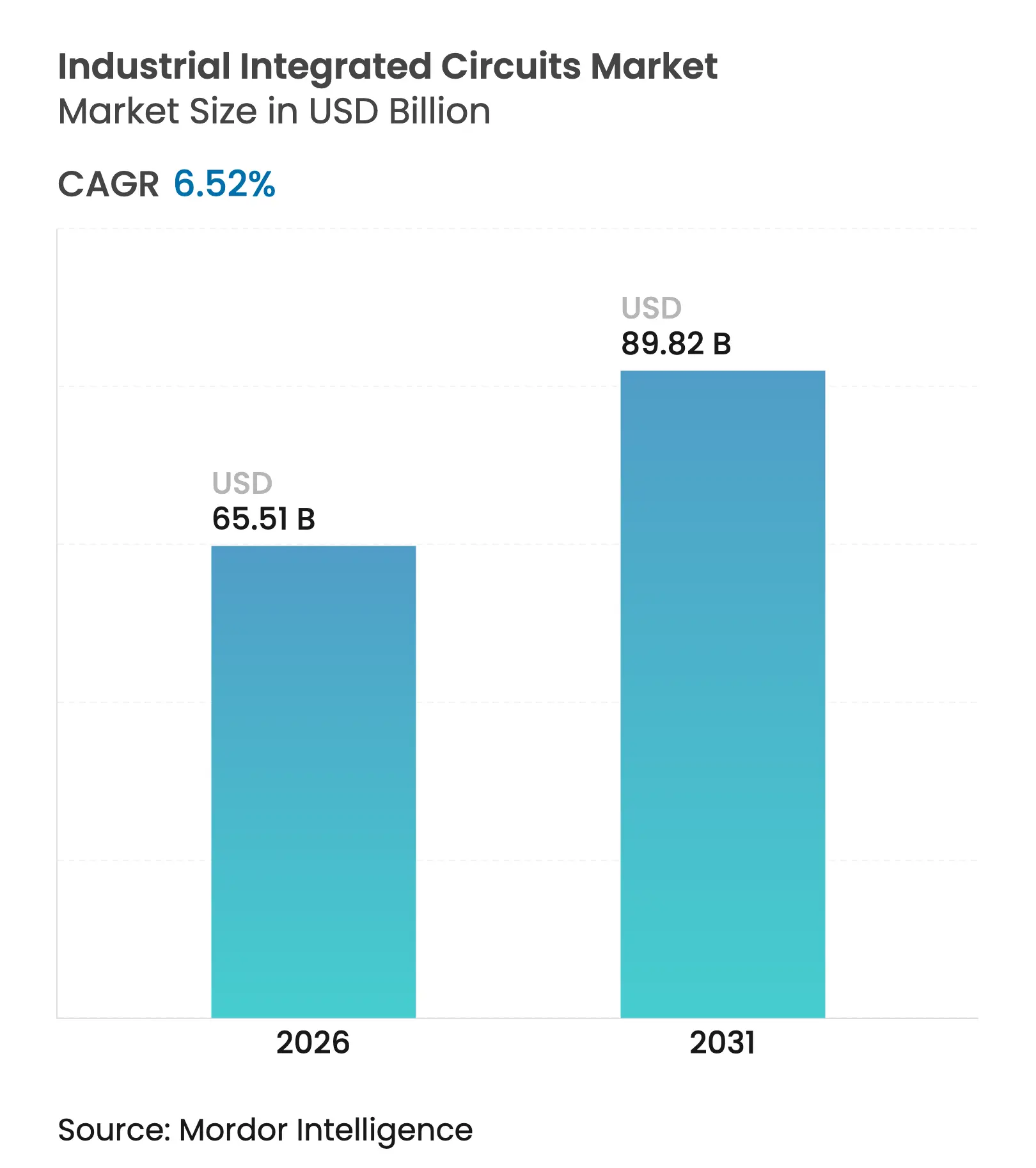

| Market Size (2026) | USD 65.51 Billion |

| Market Size (2031) | USD 89.82 Billion |

| Growth Rate (2026 - 2031) | 6.52 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The industrial integrated circuits market size was valued at USD 61.50 billion in 2025 and estimated to grow from USD 65.51 billion in 2026 to reach USD 89.82 billion by 2031, at a CAGR of 6.52% during the forecast period (2026-2031). Growth momentum stemmed from sustained digitization of factories, expanding semiconductor content per machine, and policy-led reshoring that strengthened domestic chip capacity in key regions. Wide-bandgap power devices, sensor-rich automation platforms, and edge AI microcontrollers lifted average bill-of-materials values across motion control, robotics, and process instrumentation. Government programs such as the USD 52.7 billion CHIPS and Science Act and the EUR 43 billion (USD 50.62 billion) EU Chips Act redirected capital toward local fabrication, favoring suppliers able to co-design silicon and software for safety-critical environments.[1]U.S. Department of Commerce, “Commerce Department Outlines Vision for Success of CHIPS for America Program,” commerce.gov Meanwhile, export controls accelerated supply-chain bifurcation, prompting industrial OEMs to dual-source legacy nodes to hedge against geopolitical risk.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Proliferation of Industry-4.0 Smart Factories Requiring

High-Reliability ASICs in Europe

Proliferation of Industry-4.0 Smart Factories Requiring

High-Reliability ASICs in Europe

| +1.2% | Europe, with spillover to North America | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Europe, with spillover to North America

|

Impact Timeline

:

Medium term (2-4 years)

|

Rapid Electrification of Heavy Industrial Equipment

Driving Demand for High-Voltage Power-Management ICs in North America

Rapid Electrification of Heavy Industrial Equipment

Driving Demand for High-Voltage Power-Management ICs in North America

| +1.5% | North America, expanding to the Global | Short term (≤ 2 years) | |||

Expansion of 5G-Enabled Industrial IoT Networks

Accelerating Adoption of Ultra-Low-Latency Logic ICs in East Asia

Expansion of 5G-Enabled Industrial IoT Networks

Accelerating Adoption of Ultra-Low-Latency Logic ICs in East Asia

| +1.8% | East Asia core, spillover to APAC | Medium term (2-4 years) | |||

Government Incentives for Semiconductor Localization

Boosting Industrial IC Capacity Additions

Government Incentives for Semiconductor Localization

Boosting Industrial IC Capacity Additions

| +1.1% | Global, concentrated in the US, EU, Japan | Long term (≥ 4 years) | |||

Growing Integration of Edge-AI in Machine-Vision and

Predictive-Maintenance Systems

Growing Integration of Edge-AI in Machine-Vision and

Predictive-Maintenance Systems

| +0.9% | Global, led by developed markets | Medium term (2-4 years) | |||

Rising Safety and Functional-Integrity Standards Creating

Demand for Fail-Safe Redundant IC Architectures

Rising Safety and Functional-Integrity Standards Creating

Demand for Fail-Safe Redundant IC Architectures

| +0.6% | Global, stricter in Europe and North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Proliferation of Industry-4.0 Smart Factories Requiring High-Reliability ASICs in Europe

European manufacturers increased deployment of distributed automation that mandates ASICs qualified to IEC 61508 functional-safety levels. German and Scandinavian plants integrated custom silicon for deterministic motor-control loops, often packaged in hermetic enclosures to survive aggressive wash-down environments. Qualification cycles commonly spanned 18-24 months, limiting new-entrant penetration yet deepening account stickiness for established suppliers. Capital support from the EU Chips Act broadened local design capacity, reinforcing the industrial integrated circuits market in the region.

Rapid Electrification of Heavy Industrial Equipment Driving Demand for High-Voltage Power-Management ICs in North America

Mining, construction, and material-handling OEMs shifted from hydraulic actuation to electric drives, raising voltage ceilings above 1,000 V. Silicon-carbide FETs and gate drivers supplied by onsemi, Infineon, and Microchip captured design wins in excavators and haul trucks that reduced lifetime operating costs by up to 30%. Regulatory emissions targets created time-critical replacement cycles, propelling the industrial integrated circuits market toward high-reliability power stages compliant with UL 1741 and IEC 61800-5-1 standards.

Expansion of 5G-Enabled Industrial IoT Networks Accelerating Adoption of Ultra-Low-Latency Logic ICs in East Asia

Private 5G deployments in South Korea and Japan supported robotic pick-and-place systems requiring sub-1 ms end-to-end latency. Foundries delivered logic ICs integrating RF transceivers, deterministic Ethernet, and hardware root-of-trust blocks on a single die. Samsung’s foundry nodes below 5 nm addressed thermal budgets inside compact teach pendants, enabling vision algorithms that previously relied on centralized PCs. Heterogeneous SiP packaging from JCET sped up the commercialization of integrated 5G RF power amplifiers.

Government Incentives for Semiconductor Localization Boosting Industrial IC Capacity Additions

The CHIPS and Science Act awarded up to USD 1.6 billion to Texas Instruments to expand 300 mm analog fabs, ensuring a domestic supply of low-power data-converters and MCU wafers. SkyWater’s purchase of Infineon’s Austin facility unlocked 65 nm production lines dedicated to industrial and aerospace-grade devices. Similar grant schemes in Japan and Germany incentivized legacy-node expansions, stabilizing the industrial integrated circuits market against future allocation shocks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Acute Shortages of 8-Inch Foundry Capacity Restricting

Supply of Legacy Analog and Mixed-Signal Nodes

Acute Shortages of 8-Inch Foundry Capacity Restricting

Supply of Legacy Analog and Mixed-Signal Nodes

| -1.4% | Global, most severe in Asia-Pacific | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-1.4%

|

Geographic Relevance

:

Global, most severe in Asia-Pacific

|

Impact Timeline

:

Short term (≤ 2 years)

|

Escalating Clean-Room and EUV Tool Costs Elevating Entry

Barriers for New Industrial IC Vendors

Escalating Clean-Room and EUV Tool Costs Elevating Entry

Barriers for New Industrial IC Vendors

| -0.8% | Global, concentrated in advanced node facilities | Long term (≥ 4 years) | |||

Extended Qualification Cycles in Industrial OEMs Slowing

Uptake of Latest Process Nodes

Extended Qualification Cycles in Industrial OEMs Slowing

Uptake of Latest Process Nodes

| -0.7% | Global, most pronounced in automotive and aerospace | Medium term (2-4 years) | |||

Geopolitical Export Controls on Advanced Semiconductor

Equipment Disrupting Cross-Regional Supply Chains

Geopolitical Export Controls on Advanced Semiconductor

Equipment Disrupting Cross-Regional Supply Chains

| -0.9% | Global, concentrated in the US-China trade corridors | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Acute Shortages of 8-Inch Foundry Capacity Restricting Supply of Legacy Analog and Mixed-Signal Nodes

Demand for mature-node analog and power devices outpaced incremental capacity, stretching lead times for power-management ICs to as long as 40 weeks in 2025. Foundries prioritized more lucrative 300 mm ramps, leaving industrial customers exposed to allocation shortfalls. ABB and Siemens reported delayed variable-speed-drive shipments, prompting redesigns around multi-source footprints and multi-year supply agreements that locked in higher unit prices. STMicroelectronics responded by announcing 200 mm silicon-carbide wafer lines coming online in late 2025 to alleviate pinch points.

Escalating Clean-Room and EUV Tool Costs Elevating Entry Barriers for New Industrial IC Vendors

A single High-NA EUV scanner exceeded USD 380 million, shifting capital budgets toward incumbents and lengthening payback periods beyond 10 years. Even though industrial integrated circuits rarely demand EUV lithography, the scarcity of conventional steppers and inflation in clean-room construction raised wafer-cost floors across all nodes. Emerging fabless firms developing low-volume ASICs struggled to secure slotting, funneling design activity toward multi-project wafers and licensed core platforms. The resulting consolidation tempered the entry of niche suppliers and overall competitiveness.

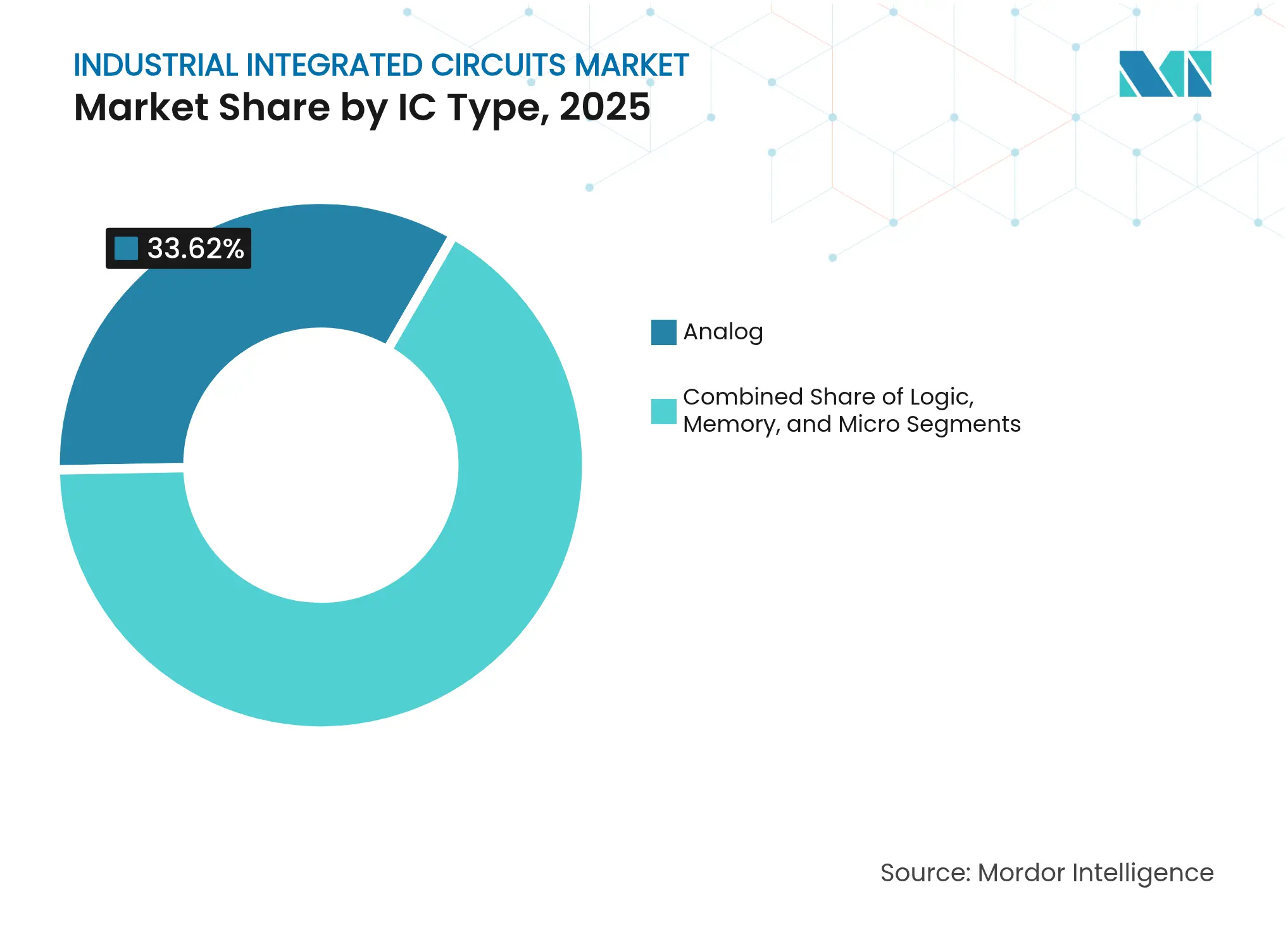

By IC Type: Analog Dominance Faces Microcontroller Disruption

Analog devices secured 33.62% of 2025 revenue, underpinning power regulation, sensor conditioning, and isolation circuits at the heart of factory and process automation. The industrial integrated circuits market benefited from rising sensor counts per asset, thereby expanding demand for precision op-amps, ADCs, and gate drivers. Tier-one vendors lengthened longevity commitments to 15 years, addressing OEM concerns over field-service continuity.

Microcontrollers are projected to post an 8.12% CAGR, the highest among micro-class devices, as edge AI inference migrates onto local cores with integrated DSP blocks. The industrial integrated circuits market size for microcontrollers is forecast to reach USD 20.62 billion by 2031, representing 22.95% of the total value. Hybrid MCU-plus-FPGA architectures emerged in robotics and inspection cameras, balancing deterministic control with machine-vision acceleration. Memory elements, although smallest in value, gained visibility through embedded MRAM that shortens write cycles and eliminates external EEPROM, enhancing functional-safety diagnostics.

Note: Segment shares of all individual segments available upon report purchase

By Function: Power-Management Leadership Challenged by Sensor-Interface Growth

Power-management ICs held a 34.55% share in 2025 on the back of electrification in motion control, traction inverters, and battery management systems. Wide-bandgap GaN stages delivered >98% efficiency in data-center rectifiers introduced by Texas Instruments in March 2025. Energy storage integrators favored multichip modules combining FET drivers, current sensing, and protection logic, lowering PCB count by 25%.

Sensor-interface ICs are on track for a 8.98% CAGR, outpacing all other functional groups. Predictive-maintenance programs in rotating equipment consume high-gain analog front-ends able to digitize low-level vibration signatures at 24-bit resolution. The industrial integrated circuits market share of sensor-interface chips is expected to climb to 19.05% by 2031, driven by built-in AI accelerators that compress edge analytics workloads.

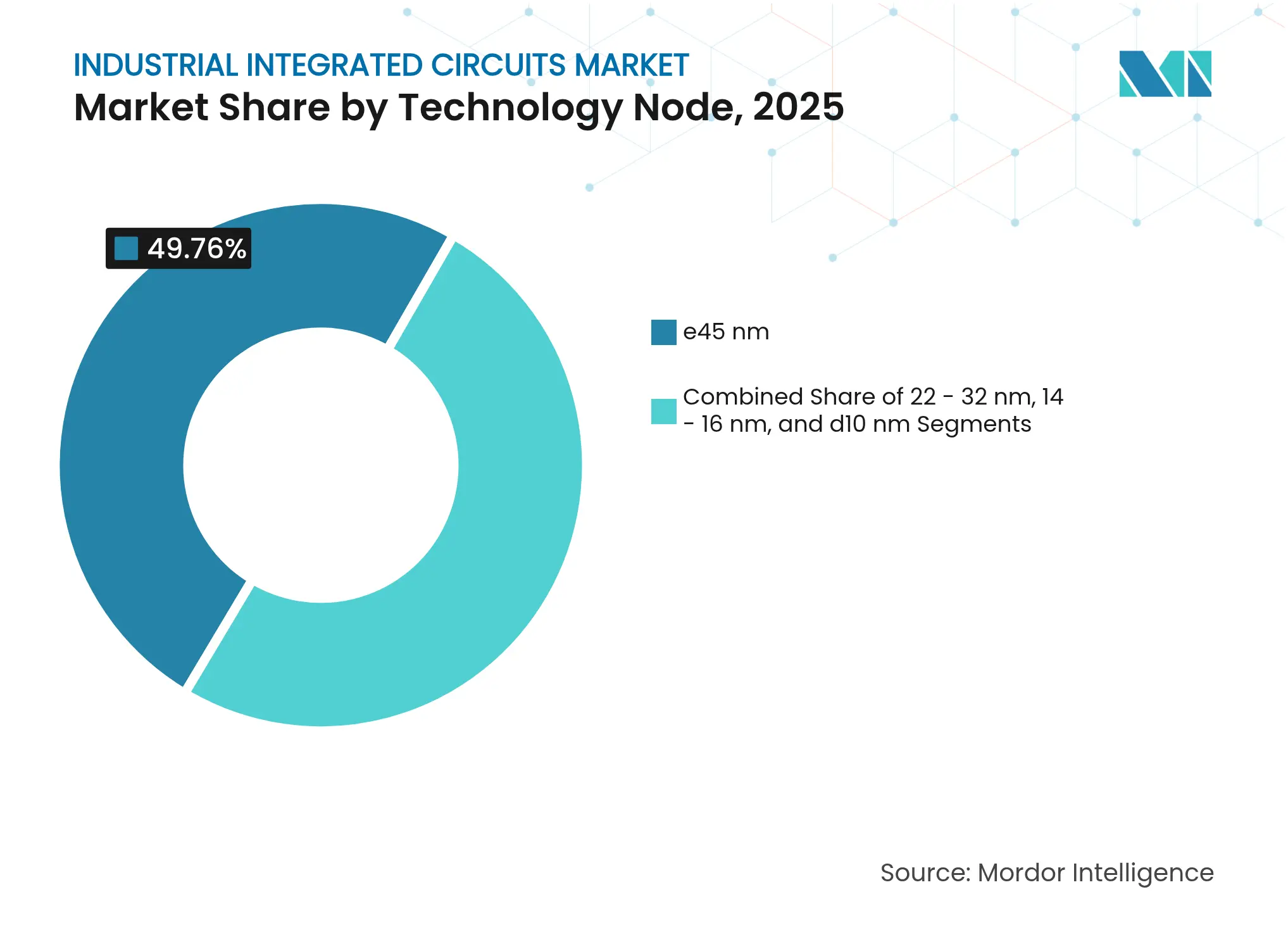

By Technology Node: Legacy Nodes Persist Despite Advanced Process Adoption

Devices manufactured on ≥45 nm geometries represented 49.76% of 2025 shipments, reflecting OEM preference for stable processes with extensive qualification records. Qualification roadmaps in defense and aerospace still mandate up to 20-year availability, reinforcing mature node demand.

Advanced processes ≤10 nm are forecast to expand at a 9.72% CAGR as machine-vision systems require high-TOPS neural engines. The industrial integrated circuits market size for ≤10 nm devices is projected to capture USD 10.42 billion by 2031. STMicroelectronics’ selection of 18 nm FD-SOI for mixed-signal MCUs illustrates selective migration where power efficiency outweighs die cost. Intermediate 22-32 nm nodes serve real-time Ethernet switches and motor-control DSPs that balance cost and frequency.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: Factory Automation Leads While IoT Segments Accelerate

Factory automation retained a 27.94% share in 2025 as PLCs, servo drives, and HMI panels incorporated more silicon per unit to support real-time analytics and cybersecurity. Automotive assembly lines adopted vision-guided robots requiring specialized 60 GHz radar sensors released by Texas Instruments in January 2025.

Industrial IoT devices and gateways deliver the highest 10.94% CAGR, aided by Ethernet-APL and 5G campus networks. The industrial integrated circuits market size attributed to gateways is forecast to hit USD 12.08 billion by 2031. Energy infrastructure applications gained traction through SiC-based HVDC converters, while industrial transportation embraced on-board chargers integrating AC/DC and DC/DC stages within compact traction inverters.

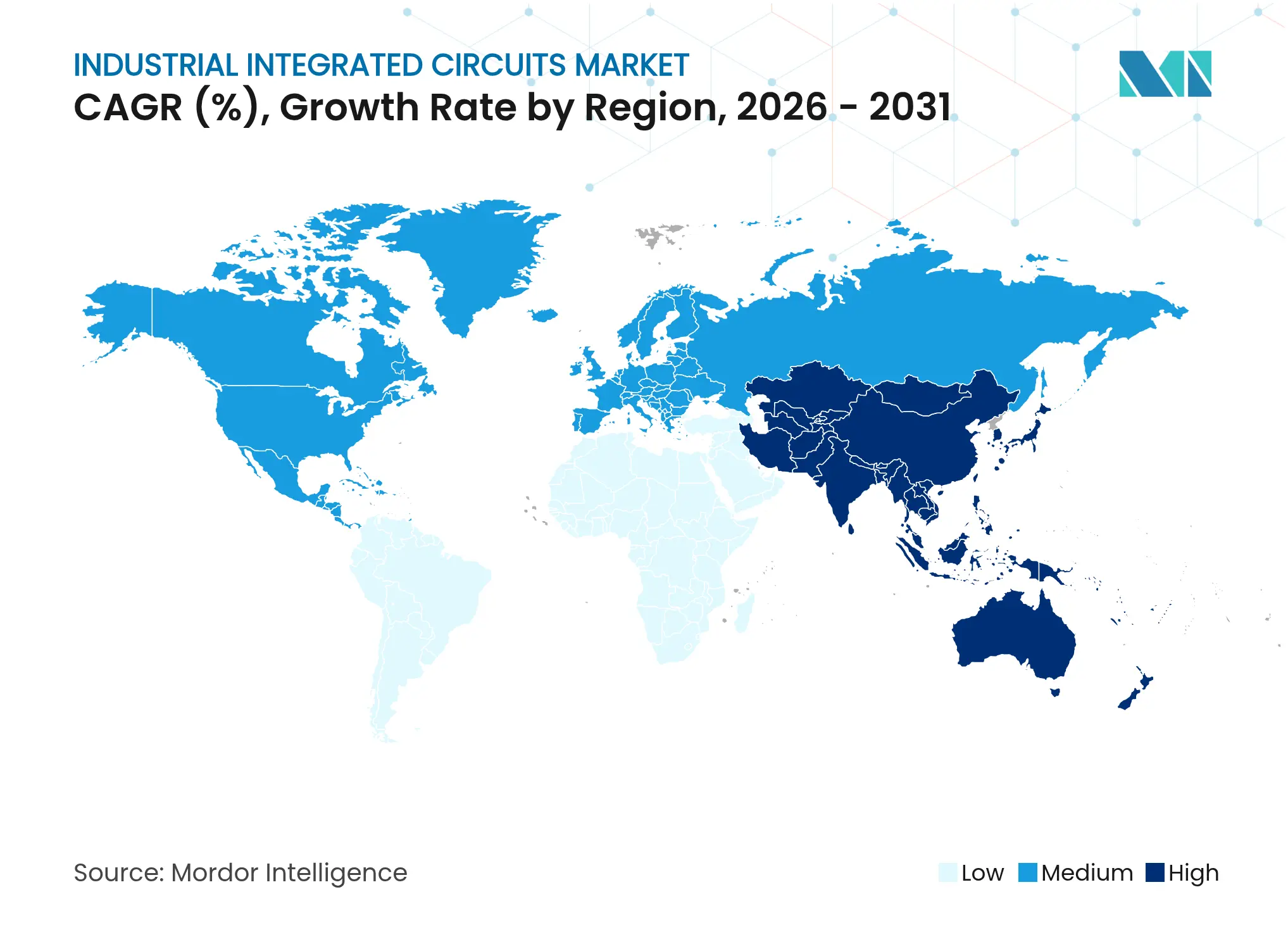

Asia-Pacific carried 64.02% revenue share in 2025, underpinned by China’s localization agenda and Taiwan’s foundry dominance. Local subsidies financed 28 new fabs breaking ground between 2024-2025, expanding front-end capacity across 65 nm to 14 nm tiers. Japanese consortia channelled capital into power-device fabs tailored for renewable-energy inverters, while South Korean IDMs leveraged existing DRAM lines to fabricate industrial sensor hubs. Edge-AI camera modules built in Shenzhen adopted heterogeneous SiP packaging to compress thermal footprints.

North America ranked second by value and benefited from an unprecedented wave of reshoring. Texas Instruments’ USD 30 billion Sherman campus is committed to four 300 mm lines focused on analog and embedded products, with first silicon expected in 2026. SkyWater’s expansion at the former Infineon Austin site added trusted-foundry capacity for aerospace ASICs. Mexico emerged as a near-shoring hub for electronics system integrators, stimulating local demand for rugged sensor-interface ICs in medical device assembly.

Europe posted steady growth, anchored by Germany’s automotive electrification needs and France’s avionics programs. The EUR 43 billion (USD 50.62 billion) Chips Act earmarked incentives for analog mixed-signal fabs, seeking to mitigate supply risks exposed during 2021-2022 shortages. Nordic infrastructure-grid upgrades accelerated the procurement of HVDC control silicon. Eastern European EMS providers ramped up board-level assembly for PLCs, relying on long-life-cycle components procured through allocation contracts to soften lingering 8-inch scarcity.

Market Concentration

Competitive intensity remained consolidated but rising as catalog analog specialists contended with system-on-chip integrators and ASIC design houses. Texas Instruments, Analog Devices, Infineon, onsemi, and Microchip dominated power and signal-chain revenues through in-house wafer capacity and broad field-application engineering networks. Infineon’s USD 830 million GaN Systems acquisition plugged a technology gap in low-voltage converters serving data-center power shelves.

Vertically integrated strategies gained ground. onsemi committed USD 2 billion to a Czech SiC facility, while Microchip slated USD 880 million for Colorado Springs to de-risk raw wafer supply. Design-service firms offered turnkey ASICs that bundle firmware and safety certifications, targeting robotics and process-safety niches. Patent filings for industrial semiconductor IP expanded 23% year-on-year after 2024, with concentration in redundant fail-safe topologies and low-latency AI co-processors.[4]IEEE, “Heterogeneous Integration Roadmap 2021,” ieee.org

Emerging challengers exploited advanced packaging to bypass wafer-fab entry barriers. Heterogeneous SiP modules combined RF, logic, and power dies, shortening time-to-market for 5G sensors without full node migration. OEMs placed growing emphasis on software ecosystems and cybersecurity certification, elevating suppliers that deliver secure bootloaders and over-the-air patch frameworks alongside silicon. Export-control regimes split the market into parallel technology stacks, compelling global vendors to maintain duplicate bill-of-materials for Western and Chinese customer bases.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Integrated circuits (ICs) serve as the essential building blocks of electronic devices, consisting of a network of interconnected transistors, resistors, and capacitors. These elements are meticulously constructed on a thin layer of semiconductor material, usually silicon, resulting in a compact chip or wafer.

The study tracks the revenue accrued through the sale of industrial ICs by various players in the global market. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The industrial integrated circuits market is segmented by type (analog IC, logic IC, memory, and micro (microprocessors, microcontrollers, and digital signal processors) and by geography (United States, Europe, Japan, China, Korea, Taiwan, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for the abovementioned segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.