Revenue Assurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.25 Billion |

| Market Size (2031) | USD 3.48 Billion |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Revenue Assurance Market Analysis by Mordor Intelligence

The revenue assurance market size in 2026 is estimated at USD 2.25 billion, growing from 2025 value of USD 2.06 billion with 2031 projections showing USD 3.48 billion, growing at 9.18% CAGR over 2026-2031. Rising data volumes from 5G network slicing, usage-based software subscriptions, and smart meter rollouts are exposing gaps in legacy billing engines, prompting operators and enterprises to deploy AI-driven analytics that reconcile transactions in real-time. Adoption is moving beyond telecom into utilities, BFSI, healthcare, and government as stakeholders recognize that revenue, cost, and margin leakages all erode profitability if left unchecked. Cloud-native delivery is accelerating adoption by reducing capital expenditure requirements, while managed services alleviate the shortage of data engineers who understand both billing protocols and machine learning pipelines. At the same time, privacy regulations that limit cross-border call-detail-record transfers are prompting regionally distributed deployments that favor vendors with flexible data-residency controls.[1]U.S. Government Accountability Office, “Tax Gap: IRS Needs Specific Goals and Strategies for Improving Compliance,” gao.gov

Key Report Takeaways

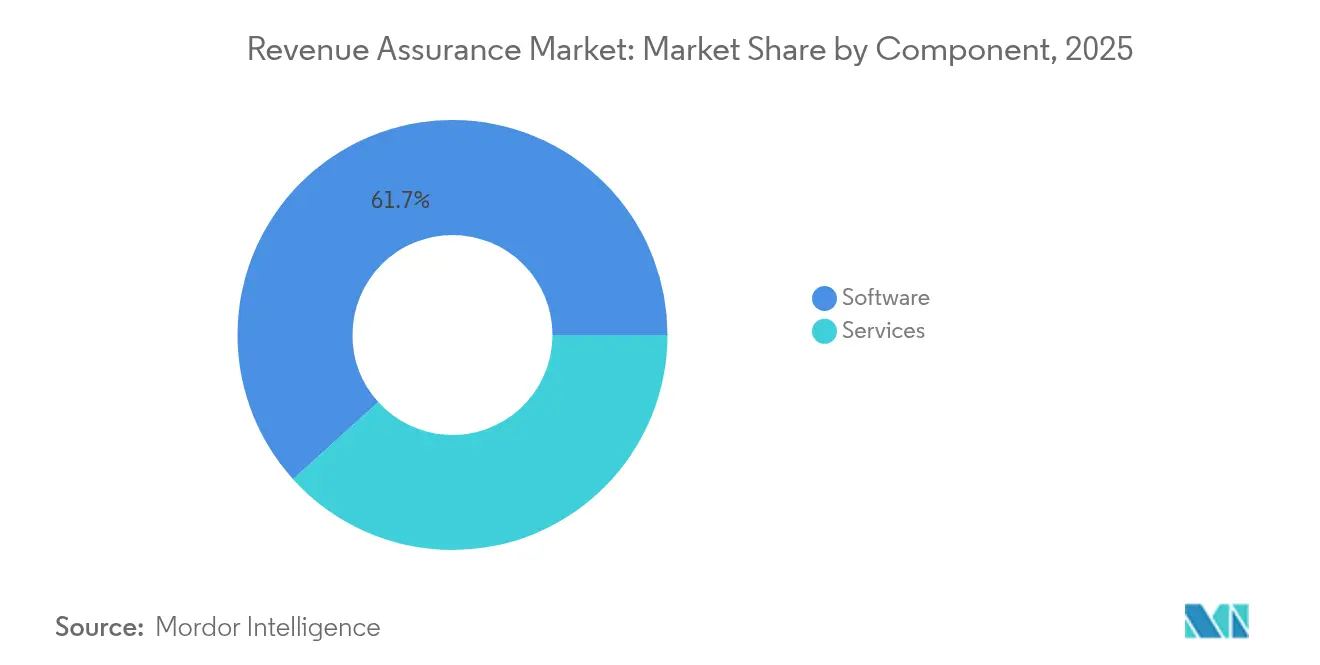

- By component, software captured 61.70% of the revenue assurance market share in 2025, while the services segment is expected to expand at a 10.62% CAGR through 2031.

- By deployment mode, cloud deployment accounted for 56.30% of the revenue assurance market size in 2025 and is forecast to grow at an 10.88% CAGR to 2031.

- By end-use industry, telecom held 48.20% of revenue of the revenue assurance market share in 2025; utilities are the fastest-growing end-use vertical, advancing at a 12.96% CAGR through 2031.

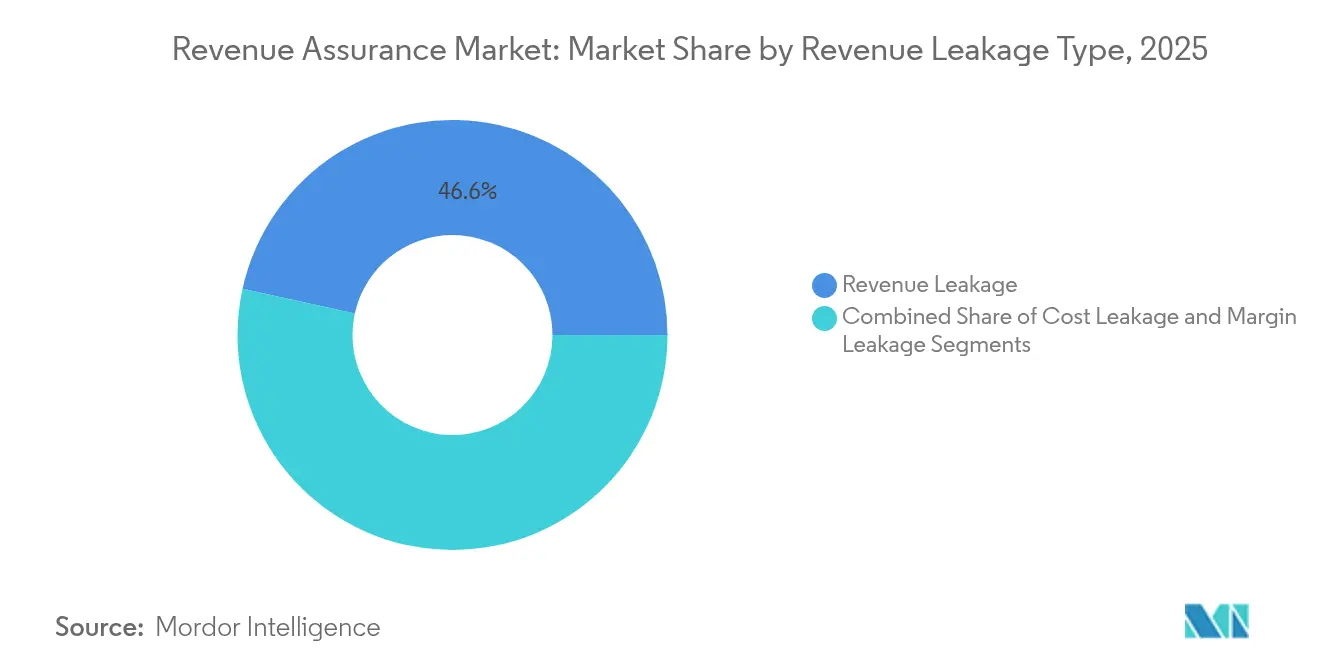

- By revenue leakage type, revenue leakage represented 46.55% of the 2025 base of the revenue assurance market share; however, margin leakage is the fastest-growing leakage category, with a 11.74% CAGR forecast.

- By organization size, large enterprises commanded 64.40% of the 2025 spending of the revenue assurance market share; small and medium-sized enterprises are expected to adopt cloud modules at a 10.63% CAGR through 2031.

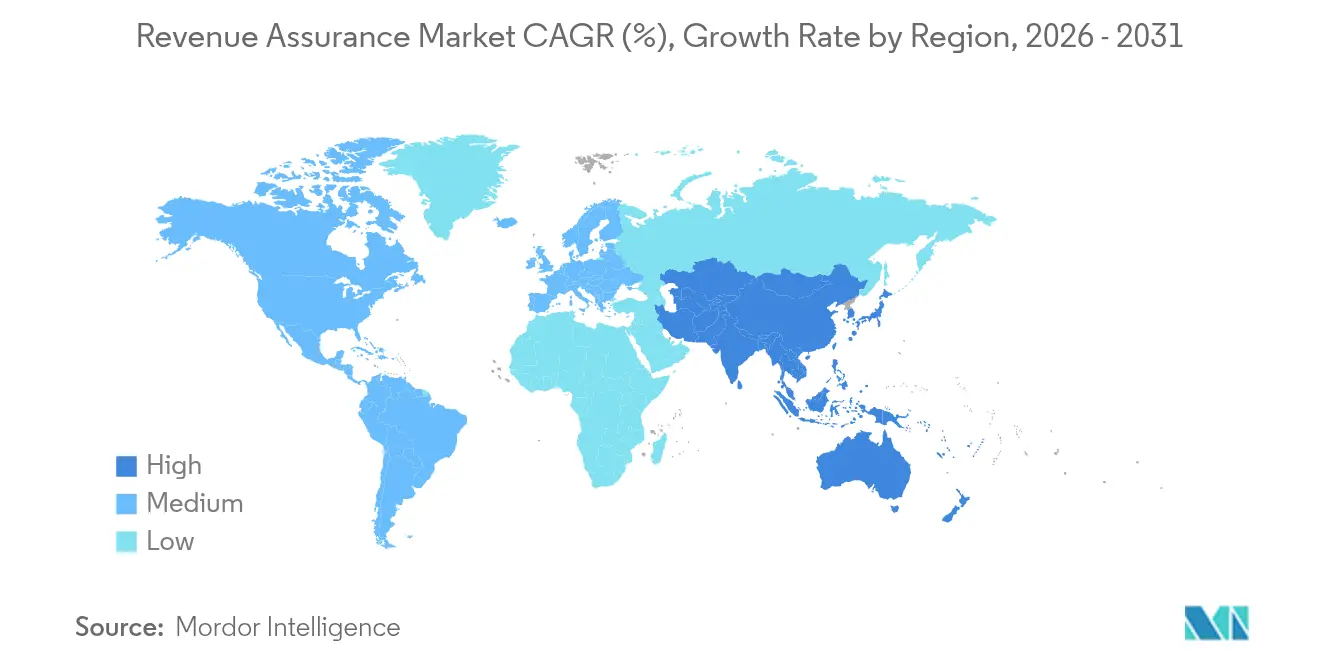

- By geography, North America led with a 35.95% share of the global revenue assurance market in 2025, while the Asia-Pacific is projected to record the highest regional CAGR of 11.98% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Revenue Assurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising complex business environment and practices | +1.8% | Global, pronounced in North America and Europe | Medium term (2-4 years) |

| Rising need to adhere to numerous revenue streams | +1.6% | Global, especially Asia-Pacific and North America | Short term (≤2 years) |

| Proliferation of subscription-based business models | +1.9% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Real-time AI-driven anomaly detection adoption | +2.1% | Global, led by North America and Asia-Pacific | Short term (≤2 years) |

| Emergence of blockchain-based smart contracts | +1.3% | Europe, Middle East, select Asia-Pacific markets | Long term (≥4 years) |

| 5G network slicing monetization complexity | +1.5% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Complex Business Environment And Practices

Digitally enabled supply chains now encompass direct sales, e-commerce, channel partners, and API ecosystems, generating heterogeneous transaction files that exceed the reconciliation capabilities of legacy billing engines. Siemens documented manual interventions in project-based revenue recognition when contract amendments spanned fiscal periods, reinforcing the need for automated allocation logic.[2]Siemens AG, “Annual Report 2024,” siemens.com The TM Forum’s Open Digital Architecture, adopted by more than 800 service providers in 2024, harmonizes API contracts while still leaving gaps when third-party applications inject pricing overrides. SAP’s convergent invoicing release consolidates subscription charges, usage fees, and one-time items onto a single invoice, thereby reducing reconciliation cycles that historically masked leakage. Softcat disclosed that principal-versus-agent classification missteps materially skewed margins, demonstrating how nuanced accounting logic drives demand for analytics that parse contract clauses at scale. As enterprises normalize multi-channel commerce, CFOs increasingly view revenue assurance as essential infrastructure rather than optional insurance.

Rising Need To Adhere To Numerous Revenue Streams

Organizations selling bundled hardware, software, and services face highly granular revenue-recognition calendars that shift with every contract modification. Industrial firms juggling milestone-based projects and product-as-a-service contracts must synchronize progress percentages, time-based subscriptions, and usage triggers in a single ledger. The result is a proliferation of sub-ledgers, each vulnerable to timing mismatches that leak invoiceable events. Utilities replacing flat-rate tariffs with real-time, time-of-use pricing encounter similar challenges as millions of 15-minute smart-meter reads multiply transaction counts. Government agencies digitizing tax collection mirror the dynamic, multiple filing channels feed a central treasury, and mismatched identifiers cause leakage when returns cannot be matched to payments. Enterprises, therefore, deploy analytics engines that ingest heterogeneous feeds, standardize identifiers, and surface missing or duplicated events before they hit the general ledger.

Proliferation Of Subscription-Based Business Models

Recurring-revenue models magnify even small rating errors because a mispriced unit propagates across every renewal cycle. Adecco demonstrated that compressing days-sales-outstanding by four days unlocked USD 120 million in working capital, proof that billing precision influences cash velocity.[3]Adecco Group, “Investor Presentation Q3 2024,” adeccogroup.com Zuora’s Subscription Economy Index revealed that involuntary churn from failed payments accounted for up to 40% of total churn among small SaaS vendors, a risk that revenue assurance platforms mitigate through automated dunning and payment method refreshing. Netflix and Spotify pioneered retry logic, but many mid-market firms lack engineering bandwidth, creating demand for SaaS-based assurance modules. Usage-based pricing deepens complexity because consumption meters may under-report due to throttling or misconfigured APIs, eroding revenue even when invoices technically reconcile with logs. Automated validation against entitlement rules, therefore, becomes central to recurring models.

Real-Time AI-Driven Anomaly Detection Adoption

Batch reconciliation exposes discrepancies only after the financial close, leaving operators to chase errors that are weeks old. Neural Technologies’ 2024 deployment with a Middle Eastern carrier reduced detection latency from 72 hours to under five seconds, exemplifying the value of streaming analytics. Tecton’s feature platform automates feature engineering, enabling data science teams to deploy anomaly detection models in hours instead of weeks. PwC found that the share of telecom executives using AI for fraud management grew from 38% in 2023 to 51% in 2024. StarTree’s real-time database, built on Apache Pinot, delivers sub-second scans over billions of billing events, allowing operators to flag unauthorized promotional discounts before month-end. As models mature, enterprises are feeding margin, cost, and revenue attributes into unified pipelines, expanding detection beyond fraud to profitability leakage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic slowdown and currency fluctuations | –1.2% | Global, acute in Europe and emerging markets | Short term (≤2 years) |

| High implementation and integration costs for SMEs | –1.4% | Global, pronounced in South America and Africa | Medium term (2-4 years) |

| Shortage of skilled revenue-assurance data engineers | –0.9% | Global, severe in Asia-Pacific and Middle East | Long term (≥4 years) |

| Privacy regulations limiting cross-border CDR data transfer | –0.7% | Europe, North America, emerging Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Slowdown And Currency Fluctuations

Macroeconomic headwinds tighten IT budgets and lengthen procurement cycles, delaying projects even when margin erosion occurs. Flexera’s 2025 survey reported that firms waste 27% of cloud spending, yet 84% actively manage costs, signaling finance leaders’ willingness to cut discretionary initiatives before core optimizations. Currency volatility inflates imported software costs for operators in South America and Africa, depressing ROI calculations. Public-sector austerity further postpones modernization; the U.K. Treasury’s 2024 audit cited a GBP 21.9 billion overspend, forcing agencies to prioritize frontline services over system upgrades. In this atmosphere, vendors emphasize modular SaaS pricing and outcome-based contracts to preserve pipeline momentum.

High Implementation And Integration Costs For SMEs

Legacy billing platforms from the early 2000s often lack documented APIs, requiring bespoke connectors that add USD 50,000–USD 200,000 to deployment budgets. Oracle’s NetSuite SuiteBilling, priced at USD 999 per month, reduces licensing expenses but still relies on professional services engagements that can double the total cost of ownership. Many SME telecom operators in Latin America and Africa operate on thin EBITDA margins, which forces them to adhere to strict payback thresholds. Although managed services shift spending from capex to opex, stakeholders remain cautious until reference cases prove hard savings within 12 months. Vendors are responding with pre-configured templates and success-based pricing, yet cost remains the leading adoption hurdle below the enterprise tier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain As Integration Complexity Rises

Services are expanding at an 10.62% CAGR through 2031, reflecting enterprise demand for integration, data engineering, and model tuning expertise that complements packaged applications. Although software retained 61.70% of the 2025 value, cloud migrations and 5G monetization have made bespoke configuration unavoidable. Oracle’s purchase of Cerner’s revenue-cycle team included 1,200 consultants specializing in convergent billing, underscoring the strategic pivot toward bundled implementation support. The rise of managed services further blurs traditional lines, as providers remotely operate assurance stacks on behalf of clients seeking managed detection and response for billing events.

Professional services remain the largest sub-segment, but managed services are gaining ground as SMEs adopt outcome-based contracts. eClerx reported double-digit growth in outsourced assurance for hospitality and retail clients, industries that view billing accuracy as non-core. This momentum suggests the revenue assurance market will see services outpace license growth through 2031, particularly where AI models must be trained on client-specific leakage patterns.

By Deployment Mode: Cloud Dominance Driven By SaaS Economics

Cloud deployment captured 56.30% of 2025 spending and is forecast to grow at an 10.88% CAGR, enabled by elastic compute and subscription pricing that lower barriers for proof-of-concept pilots. Amdocs’ CES on Azure lets telecom operators scale resources during rating peaks without permanently over-provisioning on-premises hardware. CSG’s cloud-only Ascendon reduces implementation timelines from 18 months to under 16 weeks, accelerating time to revenue when launching new 5G tariffs.

On-premises deployment remains necessary in jurisdictions with strict data-sovereignty mandates. The European Union’s GDPR prohibits exporting call-detail records outside the EEA, forcing regional nodes despite the cost-benefit of public clouds. Hybrid architectures are therefore proliferating: Netcracker’s 2024 Middle East rollout kept subscriber identifiers on private servers while streaming anonymized metrics to cloud AI engines. The revenue assurance market size for hybrid environments is projected to outgrow pure on-premises installations as compliance and cost optimization strategies converge.

By End-Use Industry: Utilities Surge On Smart-Meter Data Volumes

Telecom generated 48.20% of total revenue in 2025, but utilities are advancing at a 12.96% CAGR amid nationwide smart-meter rollouts that multiply billing events ninety-six fold. Itron’s deployment of 2.5 million meters across Europe introduced 15-minute interval reads, which overwhelmed manual reconciliation and cemented the case for automated analytics. Landis+Gyr’s Gridstream identified negative consumption spikes that previously went undetected, resulting in a 22% reduction in truck rolls in North America.

Healthcare, BFSI, and government are next-wave adopters. The U.S. GAO’s documentation of a USD 606 billion annual tax gap prompted public agencies to import telecom-style assurance into indirect tax collection. Oracle’s integration of Cerner assets aligns healthcare billing with insurance reimbursement, mirroring the convergence of telecom services. This industry diversification supports resiliency, insulating the revenue assurance market from telecom-specific capex cycles.

By Revenue Leakage Type: Margin Leakage Gains Focus As Profitability Pressures Mount

Revenue leakage accounted for a 46.55% share in 2025, as unbilled usage and rating errors directly impacted top-line results. However, margin leakage’s 11.74% CAGR suggests that CFOs are now prioritizing profitability. Siemens reported that project overruns required manual margin reviews, a vulnerability now mitigated by dashboards that compare actual versus budget data in real-time. Softcat showed margin swings of 30 percentage points depending on principal-agent judgments, highlighting that correct invoices can still mask earnings erosion.

Platforms increasingly integrate cost feeds and pricing rules, enabling finance teams to trace leakages across revenue, cost, and margin dimensions. Oracle’s Fusion ERP links revenue recognition to project costing, surfacing budget deviations before quarter close. As macro conditions tighten, enterprises view margin assurance not as a luxury add-on but as the next evolution of billing accuracy.

By Organization Size: SMEs Adopt Cloud Modules As Vendors Unbundle Capabilities

Large enterprises controlled 64.40% of 2025 outlays, reflecting transaction volumes that demand customized solutions. Tier-1 carriers deploying Amdocs’ CES routinely process billions of call records monthly, projects with professional services tags exceeding USD 10 million.

Conversely, SMEs are forecast to post an 10.63% CAGR as vendors unbundle monolithic suites into modular SaaS offerings. NetSuite SuiteBilling’s flat monthly fee and Subex’s ROC Fraud Management-as-a-Service, priced at USD 5,000 per month, democratize access to core functionality while masking infrastructure complexity behind managed services. Zuora found that SME SaaS vendors suffer involuntary churn rates up to 40%, making even small leakage fixes high-ROI. The pattern underscores how the revenue assurance market can drive volume growth by targeting underserved mid-market users.

Geography Analysis

North America generated 35.95% of 2025 revenue as telecom, financial, and utility incumbents embedded assurance workflows over the last decade. AT&T and Verizon reduced SIM-swap fraud detection times to seconds by utilizing real-time AI, and government agencies drew lessons from a USD 606 billion tax gap report to digitize audit trails. Privacy mandates, such as the California Consumer Privacy Act, force operators to keep CDR data in-region, complicating vendor consolidation but driving demand for flexible, multi-cloud architectures. Despite market maturity, the region remains an incubator for AI and blockchain pilots that later scale globally.

The Asia-Pacific is the fastest-growing territory, with a 11.98% CAGR, thanks to 5G standalone deployments by China Mobile, Bharti Airtel, Reliance Jio, KDDI, and SoftBank. China Mobile’s industrial IoT slicing imposes dynamic pricing tied to latency, a billing challenge addressed by real-time assurance engines. Regional talent shortages are prompting operators to turn to managed services provided by Tata Consultancy Services and Tech Mahindra. By the early 2030s, rapid subscriber and data-usage growth is expected to make the Asia-Pacific the largest regional contributor to the revenue assurance market size.

Europe, the Middle East, and Africa together present a mixed picture. GDPR’s strict data-residency rules create headwinds for centralized cloud deployment, yet operators like Vodafone and Orange achieved 15%–20% leakage reductions after rolling out AI fraud platforms. Middle Eastern carriers, such as Etisalat, leverage sovereign-wealth funding to modernize quickly, deploying convergent charging that aligns 5G and fixed services in a single ledger. Sub-Saharan Africa’s mobile-money surge introduces payment-processing risks that legacy voice-centric billing never managed. Currency volatility and economic cycles restrain near-term spending, but regulatory pressure for consumer protection sustains baseline demand.

Competitive Landscape

The market tilts toward moderate fragmentation. Incumbent BSS suppliers Amdocs, Oracle, Ericsson, Nokia, and CSG, bundle revenue assurance into broader charging and policy suites. Amdocs embedded real-time anomaly detection in its CES platform, reducing fraud latency from 72 hours to five seconds for a Gulf operator. Meanwhile, Oracle unified charging, revenue management, and payments on a single cloud stack, thereby slashing integration overhead for mid-tier carriers.[4]Amdocs Ltd., “CES Platform Machine Learning Integration,” amdocs.com

Specialists such as Subex, Mobileum, TEOCO, and Araxxe focus on fraud analytics and reconciliation, often winning deals where buyers value best-of-breed tools over stack consolidation. Mobileum accelerated its roadmap by acquiring a fraud analytics startup in January 2024, adding 35 data scientists who enhanced latency-sensitive account takeover prevention.

System integrators, including Tata Consultancy Services, Tech Mahindra, and eClerx, capitalize on the skills gap by offering managed services that operate clients’ platforms. The TM Forum’s Open Digital Architecture weakens historical lock-ins, allowing challengers to interoperate through standardized APIs and creating whitespace opportunities in government tax collection and utility smart metering. Vendors with embedded GDPR compliance and data-sovereignty controls possess an edge in Europe and similarly regulated markets.

Revenue Assurance Industry Leaders

Amdocs Limited

Hewlett Packard Enterprise Development LP

Araxxe SAS

Cartesian Limited

Adapt IT Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Oracle allocated USD 150 million to scale its cloud revenue assurance platform in the Asia-Pacific, funding new data center capacity in Singapore, Mumbai, and Tokyo to meet data residency rules while supporting real-time fraud detection and convergent 5G slice charging.

- November 2025: Cerillion introduced Billing Platform 12.0, which added usage-based pricing features for SaaS and cloud infrastructure. Early adopters shortened their billing cycles by 35% in the first quarter after deployment.

- October 2024: Ericsson has released Charging System 24.1, which includes policy controls that adjust 5G slice pricing in real-time according to congestion and quality targets. Initial rollouts are already handling more than 10 billion monthly transactions.

- September 2024: Oracle completed the integration of Cerner’s revenue-cycle assets, adding 1,200 professional-services specialists to help healthcare providers unify patient billing and insurance claims, with a goal of USD 2 billion in healthcare bookings by 2026.

Global Revenue Assurance Market Report Scope

The Revenue Assurance Market Report is Segmented by Component (Software and Services), Deployment Mode (Cloud and On-Premises), End-Use Industry (Telecom, Utilities, BFSI, Hospitality, Government, Healthcare, Retail, and Other End-Users), Revenue Leakage Type (Revenue Leakage, Cost Leakage, and Margin Leakage), Organization Size (Large Enterprises and Small and Medium-Sized Enterprises), and Geography (North America [United States, Canada, Mexico], South America [Brazil, Argentina, Rest of South America], Europe [Germany, United Kingdom, France, Italy, Spain, Russia, Rest of Europe], Asia-Pacific [China, Japan, India, South Korea, Australia, Rest of Asia-Pacific], and Middle East and Africa [Middle East – Saudi Arabia, United Arab Emirates, Turkey, Rest of Middle East; Africa – South Africa, Nigeria, Egypt, Rest of Africa]). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-premises |

| Telecom |

| Utilities |

| BFSI |

| Hospitality |

| Government |

| Healthcare |

| Retail |

| Other End-Users |

| Revenue Leakage |

| Cost Leakage |

| Margin Leakage |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-premises | |||

| By End-Use Industry | Telecom | ||

| Utilities | |||

| BFSI | |||

| Hospitality | |||

| Government | |||

| Healthcare | |||

| Retail | |||

| Other End-Users | |||

| By Revenue Leakage Type | Revenue Leakage | ||

| Cost Leakage | |||

| Margin Leakage | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-sized Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the revenue assurance market in 2026?

The revenue assurance market size is USD 2.25 billion in 2026 and is forecast to reach USD 3.48 billion by 2031.

Which segment grows fastest within revenue assurance solutions?

Services expand the quickest, advancing at an 10.62% CAGR as firms outsource integration and analytics workloads.

Why are utilities adopting revenue assurance tools?

Smart-meter rollouts generate high-frequency readings that overwhelm manual billing checks, driving utilities to automate reconciliation.

What role does AI play in modern assurance deployments?

AI models detect anomalies in real time, lowering fraud detection latency from days to seconds and reducing leakage mid-transaction.

Which region offers the highest growth opportunity?

Asia Pacific leads with a 11.98% CAGR, fueled by 5G standalone rollouts and complex network-slice billing requirements.

Page last updated on: