Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.07 Billion |

| Market Size (2026) | USD 14.6 Billion |

| Market Size (2031) | USD 17.58 Billion |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Telecom MNO Market Analysis by Mordor Intelligence

The Singapore Telecom MNO Market size is expected to grow from USD 14.07 billion in 2025 to USD 14.6 billion in 2026 and is forecast to reach USD 17.58 billion by 2031 at 3.78% CAGR over 2026-2031. In terms of subscriber volume, the market is expected to grow from 10.09 million units in 2025 to 11.69 million units by 2030, at a CAGR of less than 2.98% during the forecast period (2025-2030). This steady trajectory reflects resilient infrastructure investment, nationwide 5G standalone coverage, and aggressive cloud-first public initiatives that jointly lift enterprise demand while sustaining premium consumer upgrades. Household fiber penetration sits at 100%, enabling operators to bundle gigabit-class broadband with 5G mobile tiers, which in turn supports average monthly mobile data consumption above 50 GB. Intensifying digitalization across government and industry pushes demand for secure, high-capacity connectivity, and operators are responding with network-slicing products for mission-critical workloads and AI-enabled cybersecurity bundles. Competitive tension, sparked by the entry of Simba and more than ten MVNOs, has driven data prices to the lowest level in Southeast Asia, yet prudent capex cycles and new enterprise revenue streams help sustain margins. Maritime and port private-network pilots, plus aggressively funded cloud-edge rollouts, position the Singapore MNO telecom market as a regional showcase for industrial 5G use cases.

Key Report Takeaways

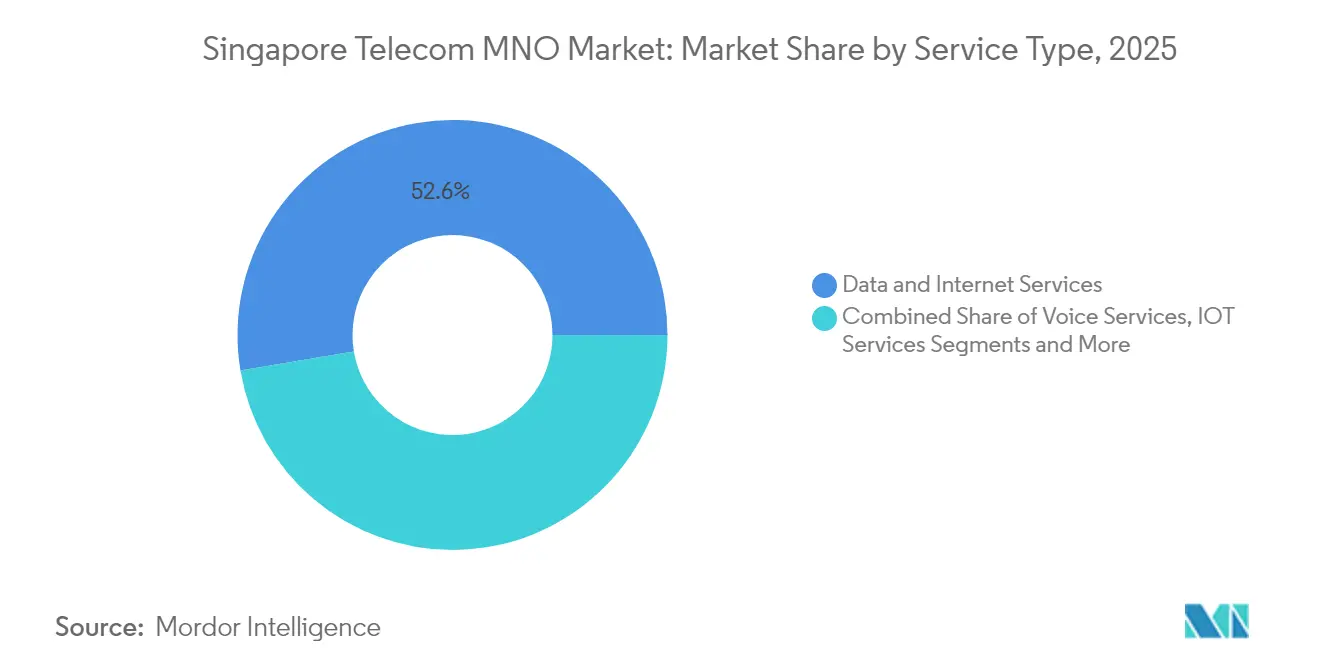

- By service type, data services led with 52.64% of Singapore MNO telecom market share in 2025; IoT services are forecast to expand at a 3.94% CAGR through 2031.

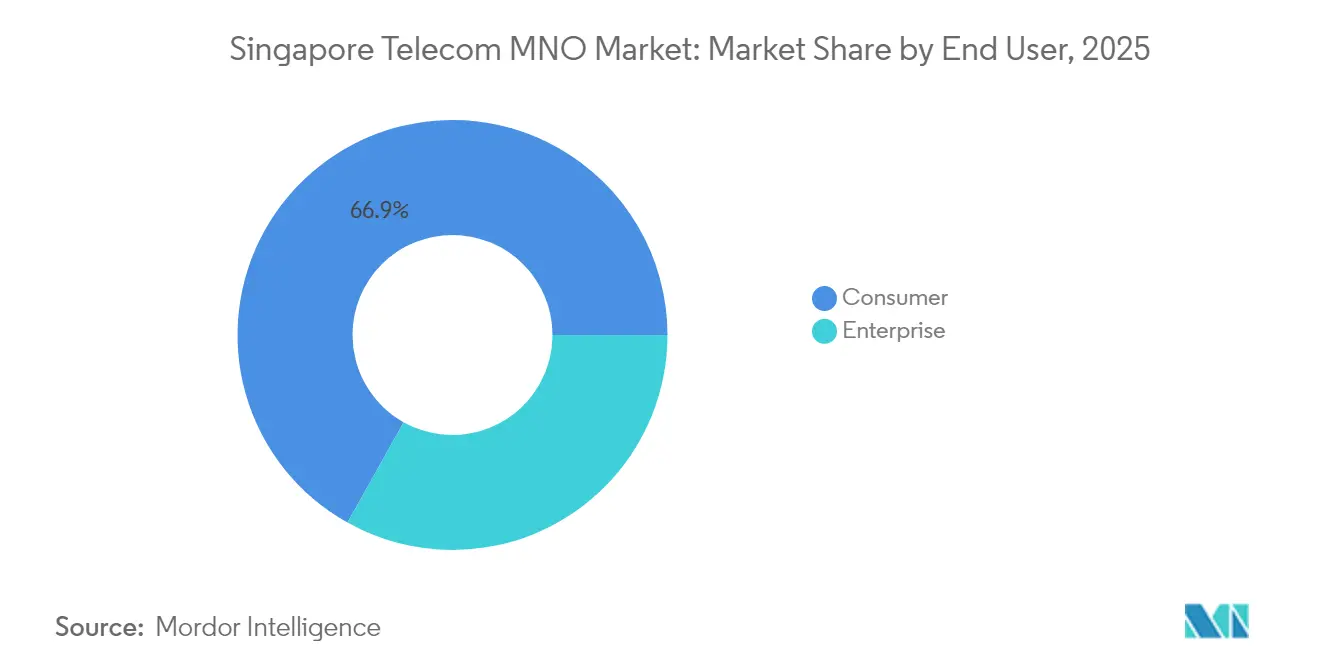

- By end user, the consumer segment captured a 66.88% share of the Singapore MNO telecom market size in 2025, whereas enterprise users are expected to advance at a 4.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide 5G standalone roll-out with network slicing | +1.2% | National | Medium term (2-4 years) |

| Digital-first public-sector initiatives and cloud migration | +0.8% | National | Short term (≤ 2 years) |

| Full fiber-to-the-home saturation enabling 10 Gbps upgrades | +0.6% | National | Short term (≤ 2 years) |

| Surging per-capita mobile data use (>50 GB monthly) | +0.7% | National | Medium term (2-4 years) |

| Maritime and port private-network pilots for industrial 5G | +0.3% | Tuas, Changi | Long term (≥ 4 years) |

| 5G network-slicing “priority lanes” for gaming and fintech users | +0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nationwide 5G standalone roll-out with network slicing

Singapore became the first country to blanket all populated areas with 5G standalone in 2025, giving operators the architectural freedom to allocate dedicated slices for latency-sensitive traffic. Singtel’s 700 MHz layer lifted indoor coverage by 40% while permitting ultra-low-bandwidth IoT slices that cost only a fraction of regular mobile plans, expanding addressable enterprise use cases. Network slicing also underpins premium consumer “5G +” bundles that guarantee bandwidth during peak hours, generating a 23% ARPU uplift among early adopters in 2025

Digital-first public-sector initiatives and cloud migration

More than 80% of eligible government systems ran on the commercial cloud by late-2024, a milestone that immediately multiplied secure connectivity demand from agencies and their vendors. The Shared Responsibility Framework launched in December 2024 further compels financial institutions to co-innovate with telecom operators on anti-phishing defenses, spawning new compliance-driven messaging and API-security revenues.

Full fiber-to-the-home saturation enabling 10 Gbps upgrades

Nationwide FTTH coverage allows rapid monetization of speed upgrades. The regulator earmarked SGD 100 million to push 10 Gbps residential service to 500,000 homes by 2028, letting operators craft symmetric upstream tiers coveted by content creators and cloud gamers. Bundled convergence packages now attach cybersecurity suites and unlimited mobile allowances, trimming churn by 18% year over year for leading ISPs in 2025

Surging per-capita mobile data use (>50 GB monthly)

Singaporeans spend 6 hours 33 minutes online daily and open Telegram 237 times per month, statistics that strain radio networks yet validate unlimited-data monetization strategies. Between 2017 and 2025, the effective price per GB collapsed from SGD 4 to below SGD 0.10, but larger data bundles and premium 5G tiers now offset headline ARPU erosion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-competition from MVNOs and Simba | -0.9% | National | Short term (≤ 2 years) |

| OTT substitution of voice/SMS and Pay-TV | -0.6% | National | Medium term (2-4 years) |

| High spectrum-renewal and energy costs | -0.4% | National | Medium term (2-4 years) |

| Limited domestic scale for capex-heavy 5G investments | -0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyper-competition from MVNOs and Simba

Simba’s SGD 10-for-50 GB plan re-anchored consumer price expectations and helped the fourth operator exceed 10% subscriber share by 2024. With more than ten MVNOs targeting micro-segments, churn has risen above 1.7% monthly, curbing the ability of any provider to push list prices upward despite rising radio-access energy costs.

OTT substitution of voice/SMS and Pay-TV

Voice revenue shrank 80% and SMS revenue 94% globally over the past decade as WhatsApp, Telegram, and streaming platforms displaced legacy services. In Singapore, pay-TV bases fell 40% at StarHub and 10% at Singtel between 2015 and 2024, making content partnerships and broadband bundling the only viable retention tools for legacy video.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data services dominate while IoT accelerates

Data products commanded 52.64% of Singapore telecom MNO market share in 2025, reflecting ubiquitous mobile broadband adoption and 100% household fiber access. IoT and M2M posted the highest 3.94% CAGR, fueled by smart-factory pilots and city-wide sensor grids that demand ultrareliable low-latency connectivity. Voice held 19.74% yet lagged in growth as OTT erosion persisted. OTT and PayTV represented 10.08%, bolstered modestly by streaming bundles. Other value-added services including managed security and GPU-as-a-Service grew at 3.88% as operators diversified revenue. This breadth underscores how the Singapore MNO telecom market size increasingly tracks enterprise digital-transformation budgets rather than legacy consumer voice trends.

The competitive configuration encourages convergence. Operators package unlimited-data SIM-only plans with 2 Gbps home broadband and cloud storage at price points equal to 2019 single surfaces, driving multi-product take-rates above 65%. Industrial 5G use cases from automated guided vehicles at Tuas Port to AR-guided aircraft checks at Changi are projected to inject USD 340 million incremental service revenue by 2031, reinforcing the structural pivot toward high-margin platform services.

By End User: Enterprise momentum overtakes consumer saturation

Enterprise clients produced 33.12% of 2025 value yet carry the fastest 4.12% CAGR through 2031. Government mandates for zero-trust architectures and sectoral digital roadmaps spur uptake of managed SD-WAN, SASE, and edge-compute nodes, providing sticky contract revenue with three-year renewals. M1’s enterprise segment expanded 50% YoY in 2024 on the back of maritime private networks and cloud contact-center solutions.

Conversely, consumer revenue growth slows to 3.58% as SIM-only price wars cannibalize traditional bundles. Still, the consumer base maintains a 66.88% share of the Singapore MNO telecom market size, thanks to record handset refresh cycles and rapid 5G adoption exceeding 75% of total subscriptions by mid-2025. Incremental growth derives from gaming-optimized data lanes and family cyber-wellness add-ons, signaling a shift from pure bandwidth sales to curated digital-lifestyle subscriptions.

Geography Analysis

Singapore’s compact 728 km² territory allows end-to-end fiber reach and city-wide 5G at population-density economics unreachable in larger markets. Central business and high-rise residential districts host premium 10 Gbps fiber rollouts and 5G mmWave nodes that cater to content creators and fintech traders requiring symmetric gigabit speeds. Western industrial corridors in Jurong and Tuas house the nation’s manufacturing and maritime clusters; here, private-network deployments deliver deterministic latency for autonomous cranes and digital twin simulations at Tuas Port, the world’s first fully automated mega-port. Eastern precincts around Changi Airport apply 5G network slicing to real-time aviation logistics, enhancing on-time performance while cutting turnaround times. Island-wide, over 30 submarine cables terminate in Singapore, elevating the city-state to a regional traffic hub and diversifying operator wholesale revenues.

Although total addressable population is only 5.9 million, the city’s role as a digital gateway to Southeast Asia supports disproportionate international bandwidth demand, translating into robust backhaul and data-center leasing for incumbent carriers. However, limited domestic scale also compels disciplined capex and co-build models; Singtel and StarHub now share 3,000 5G sites, trimming duplication and advancing sustainability targets by lowering energy draw per gigabyte.

Competitive Landscape

Four facilities-based operators—Singtel, StarHub, M1, and Simba—compete head-to-head, while a growing roster of MVNOs exploits digital-only brands to slice micro-segments at minimal opex. Singtel holds roughly 44% of mobile subscriptions, leveraging regional content partnerships and early 5G leadership to defend premium ARPU. StarHub focuses on enterprise managed services, achieving 24.8% growth in regional ICT revenue in 2024 by bundling SASE and edge computing. M1 redeployed capital toward IoT and marine private networks after delisting, bagging three national awards for enterprise innovation. Simba, originally an ISP, surged past 10% market share by 2024 with aggressive pricing and no-frills digital care.

Strategic alliances define upcoming playbooks: Singtel joined SKT, Deutsche Telekom, e&, and SoftBank to co-create an AI-native telco edge-cloud platform, pooling R&D while accelerating multinational customer acquisition. StarHub inked a low-code partnership with OutSystems to slash time-to-market for industry apps, while all operators align on Open RAN trials to curb vendor lock-in. Disruptive threats loom from satellite newcomers pitching direct-to-device broadband and from hyperscale cloud providers courting the same enterprise spend. Against this backdrop, operators double down on cybersecurity, IoT orchestration, and GPU-as-a-Service to defend relevance beyond bit-pipe economics.

Singapore Telecom MNO Industry Leaders

Singapore Telecommunications Limited

SIMBA Telecom Pte Ltd

M1 Ltd

MyRepublic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Singtel, in collaboration with Enterprise Singapore (EnterpriseSG), unveiled SPEED, a pioneering training initiative tailored for local small and medium-sized enterprises (SMEs) in Singapore. This comprehensive program aims to equip SMEs with the essential tools and capabilities to further their sustainability objectives. The acronym SPEED encapsulates its core focus: Smart technologies, Purpose-driven innovations, Enhanced capabilities, and Effective Digital transformation. Notably, this marks the inaugural sustainability initiative of its kind launched by a telecommunications company in Singapore.

- February 2025: Singtel deployed 700 MHz 5G spectrum, boosting indoor reach by 40%

- March 2025: StarHub partnered with OutSystems to accelerate AI-assisted low-code app delivery

- July 2024: The Singaporean government introduced a unified SMS identifier, "gov. sg," for all its SMS communications. This move replaces the previous practice where each agency had its distinct sender ID, such as LTA, IRAS, CPF, HDB, and ICA.

Singapore Telecom MNO Market Report Scope

Telecommunications, or telecom, refers to transmitting information over long distances using electromagnetic signals. The study on the Singapore MNO telecom market includes an in-depth trend analysis based on connectivity like fixed networks, mobile networks, and telecom towers. The Singapore MNO telecom market is segmented by services (Voice services, data and messaging, value added services(vas), IoT services, and Other Services) and by end user (enterprises B2B and retail customers (B2C). The impact of macroeconomic trends on the market is also covered under the scope of the study. Furthermore, the disturbance of the factors affecting the market's evolution in the near future, such as drivers and constraints, has been covered in the study. The market sizes and predictions are provided in terms of value (USD) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming & International Services, Enterprise And Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming & International Services, Enterprise And Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Singapore MNO telecom market?

It was valued at USD 14.6 billion in 2026 and is forecast to reach USD 17.58 billion by 2031.

How fast is the sector growing through 2031?

The market is projected to grow at a 3.78% CAGR during 2026-2031.

Which service category holds the largest share?

Data services accounted for 52.64% of 2025 revenue.

Which end-user group is expanding the quickest?

Enterprise customers are set to grow at a 4.12% CAGR, outpacing consumer growth.

How will 5G network slicing influence revenue?

Network slicing enables tiered premium services for industry and gaming, adding a projected 1.2 percentage-points to overall CAGR.

Page last updated on: