Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

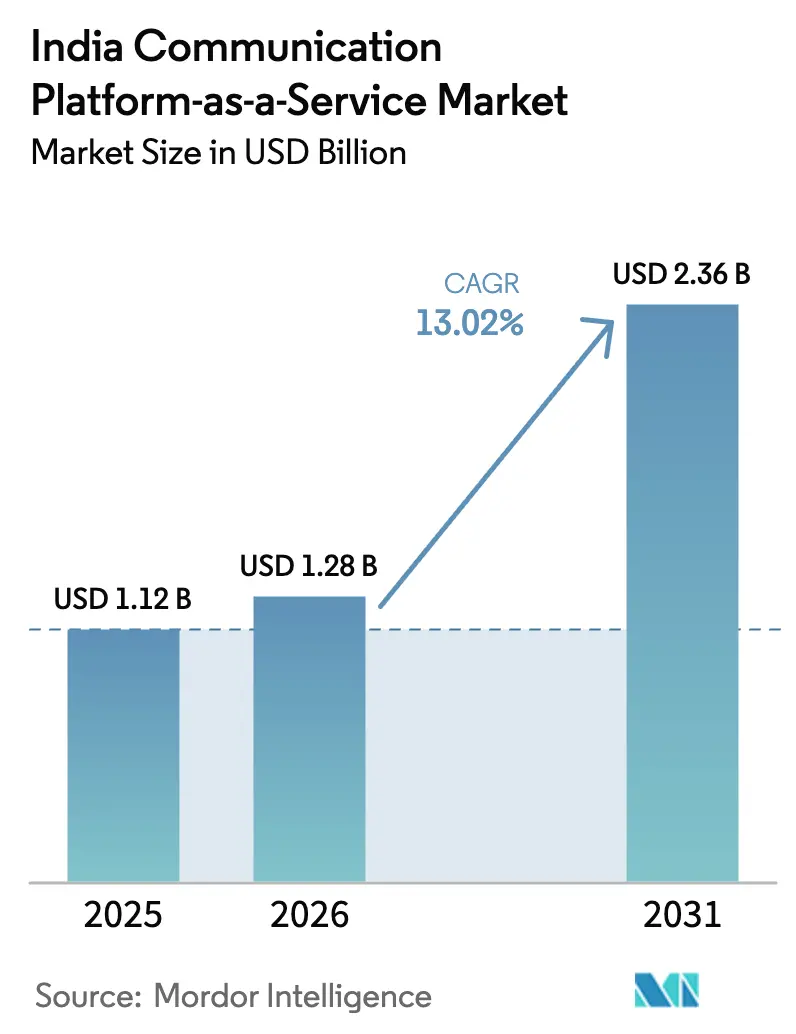

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 13.02% CAGR |

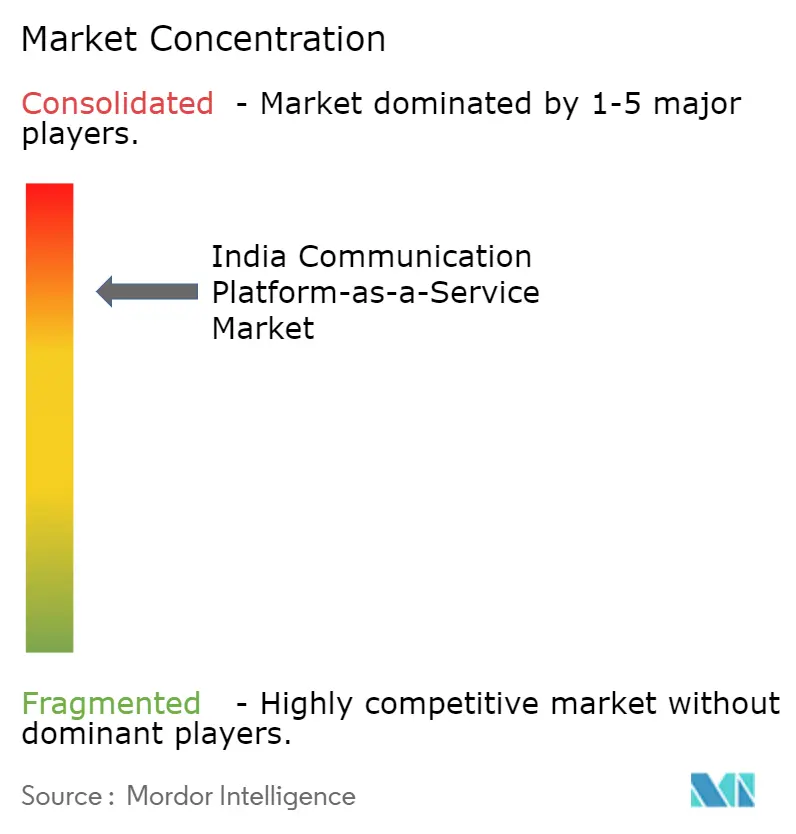

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Communication Platform-as-a-Service Market Analysis by Mordor Intelligence

The India communication platform-as-a-service market size is projected to expand from USD 1.12 billion in 2025 and USD 1.28 billion in 2026 to USD 2.36 billion by 2031, registering a CAGR of 13.02% between 2026 to 2031. Demand is accelerating as enterprises migrate from capital-intensive private-branch-exchange hardware to cloud APIs that charge only for actual use, shorten deployment cycles, and simplify omnichannel customer engagement. Large enterprises still dominate spending, but small and medium enterprises are scaling quickly because low-code tools now let non-developers embed messaging, voice, or video in existing apps within days instead of months. Industry consolidation among domestic providers, telco-led platforms, and global vendors keeps pricing competitive while pushing all players to deepen compliance features aligned with the Digital Personal Data Protection Act 2023. Hybrid-cloud preferences are rising, and 5G network API exposure is opening new programmable-communication use cases, both of which reinforce steady double-digit growth for the India communication platform-as-a-service market.

Key Report Takeaways

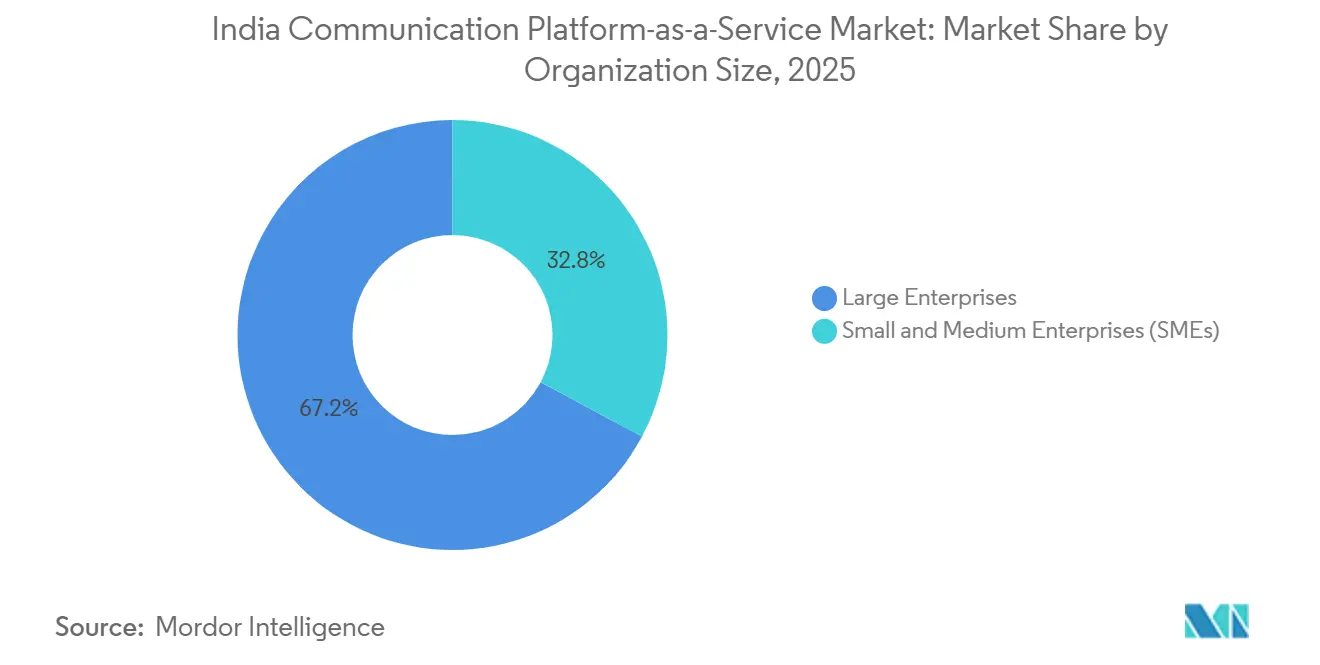

- By organization size, large enterprises held 67.18% of the India communication platform-as-a-service market share in 2025, while small and medium enterprises are advancing at a 13.63% CAGR to 2031.

- By end-user industry, banking, financial services and insurance commanded 28.59% revenue share in 2025, whereas logistics and transportation is projected to expand at a 14.12% CAGR through 2031.

- By communication channel, WhatsApp Business generated 40.26% of 2025 revenue, yet Rich Communication Services Business Messaging is forecast to grow at a 15.24% CAGR to 2031.

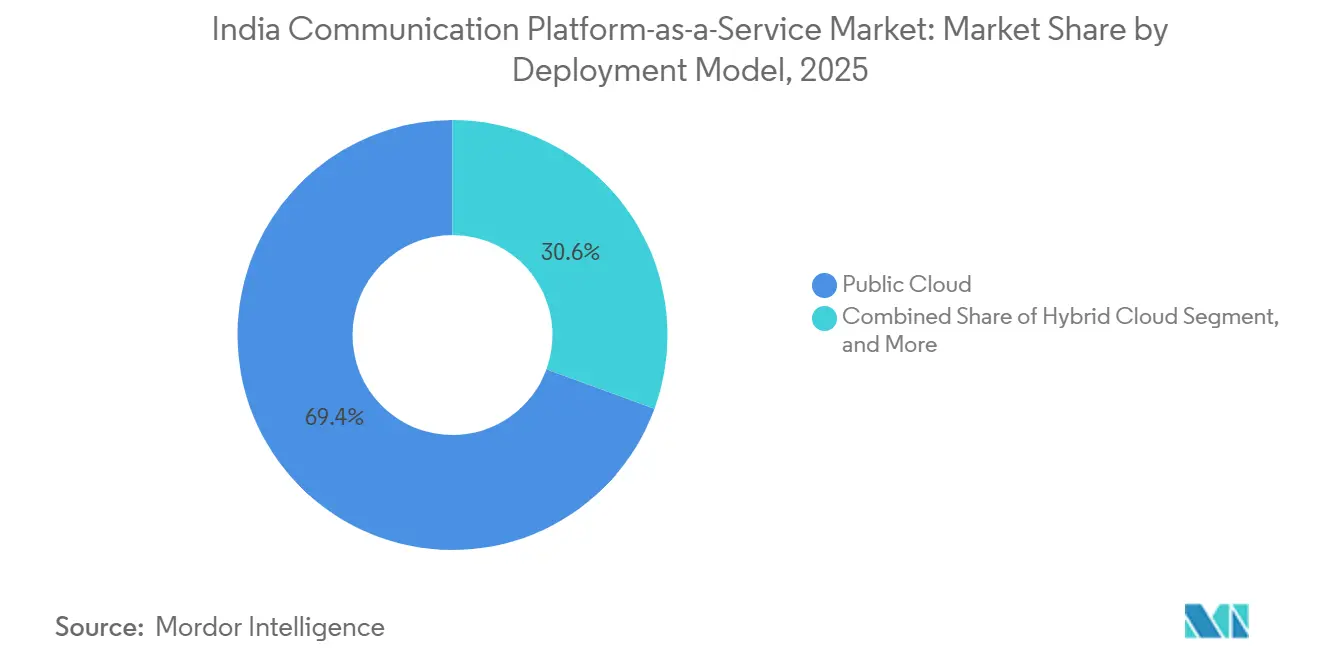

- By deployment model, public cloud represented 69.43% of 2025 implementations and hybrid cloud is on track for a 16.01% CAGR over 2026-2031.

- By CPaaS function, messaging APIs held 41.26% of revenue in 2025, while omnichannel orchestration APIs are poised for a 14.07% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Communication Platform-as-a-Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Pay-Per-Use Models to Minimize Capital Outlays | +2.8% | Global, early gains in Mumbai, Bangalore, Delhi NCR tech hubs | Medium term (2-4 years) |

| Exponential Surge in Omnichannel Engagement Adoption | +3.1% | BFSI and retail clusters across North, West and South India | Short term (≤ 2 years) |

| Low-Code and API-Led Enterprise Digital Transformation | +2.4% | National, strongest uptake in tier-1 cities | Medium term (2-4 years) |

| RBI Real-Time-Payments Push Boosting Mission-Critical Messaging APIs | +2.2% | National, led by BFSI and fintech | Short term (≤ 2 years) |

| Emergence of Sovereign-Cloud Offerings Enabling Compliant CPaaS Uptake | +1.6% | National, driven by DPDP Act and DoT rules | Long term (≥ 4 years) |

| 5G Network-API Exposure Creating New Programmable-Communication Use Cases | +0.9% | Urban centers with Jio, Airtel, Vi 5G | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Pay-Per-Use Models To Minimize Capital Outlays

Indian companies are replacing fixed PBX investments with usage-based CPaaS contracts that convert capital expense into predictable operating outflows, a shift that resonates strongly with budget-constrained small and medium enterprises. The model enables instant capacity scaling during festival-season ecommerce peaks or fraud-alert surges without over-provisioning infrastructure. Domestic leaders are reinforcing this theme through acquisitions that pool carrier connections and lower unit costs, further improving margins.[1]Tanla Platforms Limited, “Tanla acquires ValueFirst India from Twilio“, "Update on Strategic Acquisitions,” tanla.com Pay-per-use economics also facilitate cross-border expansion because vendors can light up new regions via cloud points of presence instead of building data centers. As compliance mandates grow stricter, enterprises favor providers that pair elastic pricing with audit trails, encryption, and role-based controls.

Exponential Surge in Omnichannel Engagement Adoption

Approximately eighty percent of brands used WhatsApp Business APIs in 2025 alongside SMS fallback, confirming that single-channel outreach leaves customers unreachable when they switch devices or apps. Orchestration APIs now automate dynamic routing, sending an SMS for guaranteed delivery, then elevating to RCS carousels or live WhatsApp chat if the user engages.[2]Karix Mobile Private Limited, “Results that speak for themselves,” karix.com This approach cut communication spend by up to 20% and boosted click-through six-fold in documented pilots. Vendors are embedding these flows directly into marketing suites such as Adobe Journey Optimizer and Oracle Responsys to remove integration friction. Resulting data unification lets companies measure end-to-end journey performance and optimize channel mix in real time.

Low-Code and API-Led Enterprise Digital Transformation

Drag-and-drop journey builders and pre-configured connectors to Salesforce, Shopify, and SAP let non-technical staff deploy new engagement flows in weeks. Conversational-AI toolkits such as Surbo now process more than 100 million messages monthly, highlighting convergence between bot frameworks and CPaaS messaging rails Low-code flexibility is particularly valuable for retail and ecommerce brands that iterate campaigns quickly around flash sales. API-first design also guards against vendor lock-in because enterprises can swap providers by switching endpoints rather than rewriting entire stacks. Modular suites like Infobip CPaaS X and Twixor white-label offerings show how the ecosystem is standardizing around composable building blocks.[3]Juniper Research, “Global Conversational AI Market 2025-2029: Infobip profile,” juniperresearch.com

RBI Real-Time-Payments Push Boosting Mission-Critical Messaging APIs

Unified Payments Interface processed more than 131 billion transactions in fiscal 2024-2025, triggering huge volumes of one-time passwords, transaction alerts, and fraud notifications that require near-instant delivery. Banks now demand 99.99% uptime, dual-carrier routing, and real-time dashboards highlighting latency outliers. Karix’s AI-powered Wisely ATP blocked over 6 million phishing attacks for leading lenders, underscoring the security stakes. With 80% of India’s monthly SMS classified as utility traffic, CPaaS has evolved from promotional marketing to essential financial infrastructure.[4]Twixor, “India's Leading Telecom Aggregator Enhances Engagement with White-Labelled CPaaS,” twixor.ai Generative-AI assistants layered on top of these secure channels are already improving conversion rates and net promoter scores for early adopters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implementation Complexity Across Heterogeneous Legacy Stacks | -1.4% | National, acute in large BFSI enterprises | Medium term (2-4 years) |

| Security and Data-Privacy Concerns Amid Rising Cyber-Attacks | -1.1% | National, higher scrutiny in BFSI, healthcare, government | Short term (≤ 2 years) |

| Volatile Telco A2P-SMS Wholesale Pricing Squeezing Margins | -0.8% | National, affects all aggregators | Short term (≤ 2 years) |

| Fragmented State-Level Telecom Rules Raising Compliance Cost | -0.6% | National, varying by state | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Implementation Complexity Across Heterogeneous Legacy Stacks

Mainframe cores and proprietary middleware inside large banks force CPaaS integrations to traverse custom gateways, extending project timelines and inflating professional service costs. Audit requirements demand end-to-end traceability, so vendors must supply pre-built connectors for systems such as Oracle Financials and Temenos. Tanla’s retention of ValueFirst leadership, each with more than a decade of domain expertise, reflects how human capital is as important as technology in navigating legacy environments. Enterprises are also pushing for open standards that ease vendor switching, increasing pressure on proprietary protocols. Without simplified adapters and robust middleware, modernization initiatives risk stalling halfway.

Security and Data-Privacy Concerns Amid Rising Cyber-Attacks

India logged 1.4 million cyber incidents in 2024, including breaches that exposed tens of millions of records, elevating encryption and intrusion detection from check-box items to core buying criteria.[5]CERT-In, “Monthly Phishing and Malware Reports,” cert-in.org.in The DPDP Act enforces explicit consent and 72-hour breach notification, prompting many providers to deploy sovereign-cloud zones inside the country. Airtel’s network-level AI stopped 48.3 billion spam calls in its first year, showing that abuse threats span voice and messaging channels.[6]Developing Telecoms, “Airtel working with Google to launch RCS,” developingtelecoms.com Infobip’s Signals module now detects grey-route SMS and pumping fraud, while Karix’s TruBloq blockchain adds tamper-evident logs for regulators. Sim-binding rules effective February 2025 add another compliance layer, forcing vendors to verify device continuity for WhatsApp and RCS sessions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs Accelerate Low-Code API Adoption

Small and medium enterprises are growing faster than the overall India communication platform-as-a-service market, expanding at a 13.63% CAGR through 2031, while large enterprises retained 67.18% of 2025 spending. The India communication platform-as-a-service market size for SMEs is benefiting from pay-per-use pricing that removes capital hurdles and from low-code interfaces bundled by telcos and cloud vendors. Tanla’s ValueFirst purchase unlocked mid-market accounts that were previously outside its direct reach. E-commerce sellers in tier-2 cities now launch WhatsApp notifications within minutes through plug-ins on Shopify or WooCommerce, signaling that self-service onboarding is decisive. Larger firms continue to account for the bulk of traffic because they send billions of OTPs and alerts each month, yet they increasingly mirror SME agility by adopting modular orchestration layers.

Second-order effects include elevated security baselines for all vendors, since even the smallest customers now request ISO 27001 or SOC 2 evidence amid tighter data-privacy rules. The India communication platform-as-a-service market share of large enterprises may edge down as SMEs expand, but absolute enterprise spend will keep rising thanks to regulatory messaging volumes in banking and insurance. Telco-backed CPaaS suites such as Airtel IQ complement this trend by bundling data connectivity and local-language support, further lowering barriers in regional markets. Venture funding into conversational-AI firms like Gupshup and Exotel indicates confidence that SME demand still has headroom.

By End-User Industry: Logistics Disrupts BFSI Dominance

Banking, financial services and insurance delivered 28.59% of 2025 revenue, a figure powered by regulatory mandates around real-time payments. Yet logistics and transportation is the fastest mover, expected to grow 14.12% annually to 2031 as delivery firms deploy status updates and rerouting prompts that cut failed drops by up to 20%. The India communication platform-as-a-service market size attached to logistics is therefore rising faster than for any other vertical. Retailers that outsource fulfilment also lean on these APIs to push proactive pickup or delay notices, proving that the channel shift is not limited to couriers.

Healthcare, government services, and education add incremental growth but remain smaller bases today. Logistics’ expansion could gradually erode BFSI’s India communication platform-as-a-service market share, especially if regulatory OTP rules ease and banks experiment with free WhatsApp utility messages. For vendors, diversification into high-velocity logistics traffic hedges against pricing pressure in financial messaging and illustrates how programmable communications is permeating every step of physical supply chains.

By Communication Channel: RCS Challenges WhatsApp’s Lead

WhatsApp Business captured 40.26% of 2025 revenue, yet Rich Communication Services is set for the fastest compound growth at 15.24% through 2031 as telcos reclaim messaging revenues via 70-30 or 80-20 splits with Google. Enterprises favor RCS because it combines rich cards, verified sender IDs, and operator-level control, elements that satisfy auditors more readily than over-the-top platforms. The India communication platform-as-a-service market size tied to SMS remains large because regulatory OTP requirements persist, but price cuts by WhatsApp in 2024 and 2025 have redirected some utility traffic toward its free tiers.

Voice and video APIs serve customer support, telemedicine, and education, yet their spend is modest compared with messaging. Omnichannel orchestration layers blur channel distinctions by selecting the optimal route on each interaction, a trend that further consolidates traffic under vendors that can provision SMS, WhatsApp, RCS, voice, email, and push through a single contract. Upcoming SIM-binding rules introduce uncertainty for RCS classification and could reshape wholesale pricing structures.

By Deployment Model: Hybrid Cloud Gains Ground

Public cloud delivered 69.43% of deployments in 2025 because of speed and elastic scale, yet hybrid architectures are forecast to climb 16.01% per year as data-localization clauses from the DPDP Act push sensitive workloads on-premise. The India communication platform-as-a-service market share for hybrid cloud will therefore expand as banks keep customer records inside gated data centers while consuming outbound messaging through cloud endpoints. DoT draft rules published in 2025 are likely to formalize these preferences and could require local traffic termination, favoring providers with in-country points of presence.

On-premise instances persist inside defense and highly regulated agencies that ban external connectivity, although their proportion of the India communication platform-as-a-service market size will keep shrinking. Vendors must maintain feature parity across delivery modes so clients can move workloads without retraining staff or rewriting code. Partnerships such as Nokia’s with Bharti Airtel to expose 5G network APIs illustrate new hybrid possibilities where telco edge nodes process latency-sensitive calls while public clouds handle analytics.

By CPaaS Function: Orchestration APIs Outpace Stand-Alone Messaging

Messaging APIs controlled 41.26% of 2025 spend, but orchestration suites that unify channel selection are projected to grow 14.07% annually to 2031 as enterprises seek holistic journey design. Inserting India communication platform-as-a-service market size context at the point of campaign design helps marketers choose the cheapest path per outcome. Documented savings of 20% and click-through lifts of six-fold on travel campaigns show why firms now budget for orchestration licenses rather than only per-message fees.

Voice remains vital for two-factor authentication and IVRs, yet AI chatbots are automating many calls, pausing expansion in pure voice minutes. Verification APIs for SIM-swap checks and device scoring are climbing in relevance as cybercrime rises, locking them into bundled plans. Eventually, feature boundaries may dissolve entirely, and competition will shift to interface simplicity, analytics depth, and compliance coverage instead of any single API advantage.

Geography Analysis

South India led adoption in 2025 thanks to Bangalore and Hyderabad technology clusters that gravitate toward API-first communication stacks. Concentrated global capability centers and venture-backed startups trial new channels early, reinforcing a virtuous talent and tooling cycle. Karix and ValueFirst both operate sizeable engineering hubs in Bangalore, underlining the region’s strategic weight.

West India, anchored by Mumbai and Pune, commands heavy traffic from banking, financial services and insurance headquarters that must meet strict regulator timelines for transaction alerts. The India communication platform-as-a-service market share attributed to West India therefore remains high despite slower startup density. North India, including Delhi NCR, benefits from central-government e-governance programs that send billions of public-service notifications, such as the CoWIN vaccine campaigns, confirming its importance for volume-driven providers.

East and North-East India and Central India contribute smaller absolute revenue but deliver faster percentage growth as CPaaS bundles reach tier-2 cities in local languages. Telco-backed suites give ubiquitous network reach, while pure-play vendors cultivate channel partners for regional penetration. Emerging multilingual natural-language processing support across Hindi, Tamil, Bengali, and Marathi lowers cost of customer engagement outside metro areas.

Competitive Landscape

Tanla Platforms consolidated roughly 35% of overall traffic and 45% of SMS after buying ValueFirst for INR 346 crore (USD 42 million), placing it at the apex of the India communication platform-as-a-service market. Karix, already inside Tanla’s fold since 2019, controls about 45% of national long-distance messaging and serves nine of the top ten banks. Route Mobile, Gupshup, Exotel, and Netcore Cloud make up the next tier, competing on channel breadth, local support, and price.

Telcos have entered forcefully: Airtel IQ bundles connectivity with messaging, while Vodafone Idea’s RCS monetization plan seeks to claw back OTT erosion. Global vendors Twilio, Infobip, and Sinch embed APIs inside marketing suites and public clouds to secure multinational accounts, an approach that sidesteps some localization challenges but demands in-country data centers to win regulated clients.

Mergers will likely continue because scale drives lower termination costs, stronger carrier ties, and faster compliance updates. Nokia’s API collaboration with Airtel signals infrastructure providers want a share of high-margin developer services. Startups focused on conversational AI could become attractive targets as customer-service automation merges with CPaaS backbones, mirroring Tanla’s earlier move for ValueFirst.

India Communication Platform-as-a-Service Industry Leaders

-

Twilio Inc.

-

Tanla Platforms Limited

-

Route Mobile Limited

-

Gupshup Technology India Private Limited

-

Infobip Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Bharti Airtel partnered with Google to roll out Rich Communication Services messaging to Indian enterprises under an 80-20 revenue-share model.

- December 2025: Nokia and Bharti Airtel announced joint exposure of 5G network APIs covering network slicing, device-location, and SIM-swap detection.

- April 2025: WhatsApp confirmed it will make utility messages free worldwide, following earlier removal of customer-service fees in Nov 2024.

India Communication Platform-as-a-Service Market Report Scope

A cloud-based communication platform-as-a-service (CPaaS) allows the addition of real-time communication channels, like audio, video, chat apps, and messaging applications, to one's current applications or business solutions. The Indian ecosystem of the CPaaS space is covered in the report, and active stakeholders were discussed throughout the period under consideration.

The India Communication Platform-as-a-Service Market Report is Segmented by Organization Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (IT and Telecom, BFSI, Retail and E-Commerce, Healthcare, Government and Public Sector, Logistics and Transportation, and Other End-User Industries), Communication Channel (SMS, Voice, WhatsApp Business, RCS Business Messaging, Video API, Email, Push Notifications), Deployment Model (Public Cloud, Hybrid Cloud, On-Premise), CPaaS Function (Messaging API, Voice API, Video API, Verification and Security API, Omnichannel Orchestration API), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Organization Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By End-User Industry

| IT and Telecom |

| Banking, Financial Services, and Insurance (BFSI) |

| Retail and E-Commerce |

| Healthcare |

| Government and Public Sector |

| Logistics and Transportation |

| Other End-User Industries |

By Communication Channel

| SMS |

| Voice |

| WhatsApp Business |

| RCS Business Messaging |

| Video API |

| Push Notifications |

By Deployment Model

| Public Cloud |

| Hybrid Cloud |

| On-Premise |

By CPaaS Function

| Messaging API |

| Voice API |

| Video API |

| Verification and Security API |

| Omnichannel Orchestration API |

| By Organization Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Industry | IT and Telecom |

| Banking, Financial Services, and Insurance (BFSI) | |

| Retail and E-Commerce | |

| Healthcare | |

| Government and Public Sector | |

| Logistics and Transportation | |

| Other End-User Industries | |

| By Communication Channel | SMS |

| Voice | |

| WhatsApp Business | |

| RCS Business Messaging | |

| Video API | |

| Push Notifications | |

| By Deployment Model | Public Cloud |

| Hybrid Cloud | |

| On-Premise | |

| By CPaaS Function | Messaging API |

| Voice API | |

| Video API | |

| Verification and Security API | |

| Omnichannel Orchestration API |

Key Questions Answered in the Report

What is the projected size of the India CPaaS space by 2031?

It is forecast to reach USD 2.36 billion by 2031, expanding at a 13.02% CAGR from 2026 to 2031.

Which organization-size segment is expanding the fastest?

Small and medium enterprises are advancing at a 13.63% CAGR through 2031, outpacing large-enterprise growth.

Which end-user group is expected to record the highest growth?

Logistics and transportation is projected to post a 14.12% CAGR as real-time tracking and delivery alerts gain priority.

How quickly will hybrid cloud deployments grow?

Hybrid implementations are on track for a 16.01% CAGR between 2026 and 2031 as firms balance scalability with data-residency mandates.

Which communication channel is poised for the fastest uptake?

Rich Communication Services Business Messaging is forecast to increase at a 15.24% CAGR, challenging WhatsApp's current lead.

What share do messaging APIs currently hold?

Messaging APIs generated 41.26% of 2025 revenue, but orchestration suites are rising faster as firms unify channel management.

Page last updated on: