Telecom Billing Revenue Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

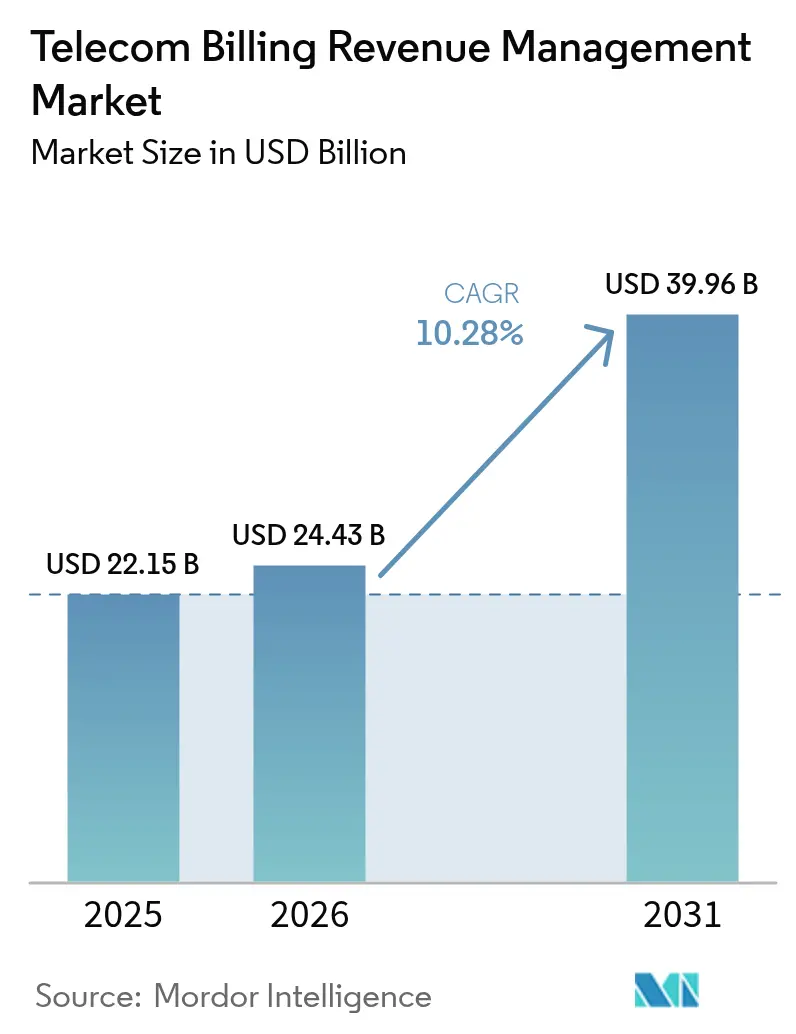

| Market Size (2026) | USD 24.43 Billion |

| Market Size (2031) | USD 39.96 Billion |

| Growth Rate (2026 - 2031) | 10.28% CAGR |

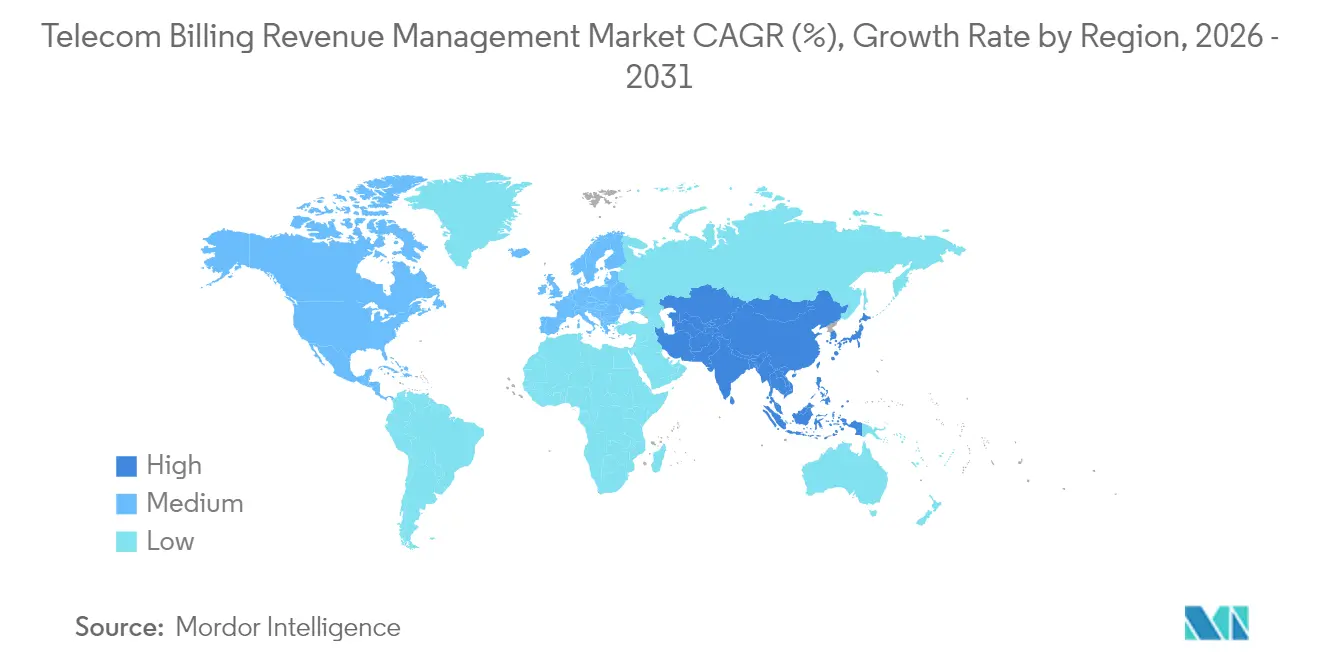

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telecom Billing Revenue Management Market Analysis by Mordor Intelligence

Telecom Billing Revenue Management market size in 2026 is estimated at USD 24.43 billion, growing from 2025 value of USD 22.15 billion with 2031 projections showing USD 39.96 billion, growing at 10.28% CAGR over 2026-2031.

This growth trajectory reflects the sector's response to mounting complexity in 5G monetization, where traditional billing architectures struggle to accommodate dynamic network slicing and edge computing services. The market's expansion is fundamentally driven by the convergence of cloud-native billing platforms with artificial intelligence capabilities, enabling real-time revenue optimization that legacy systems cannot match.

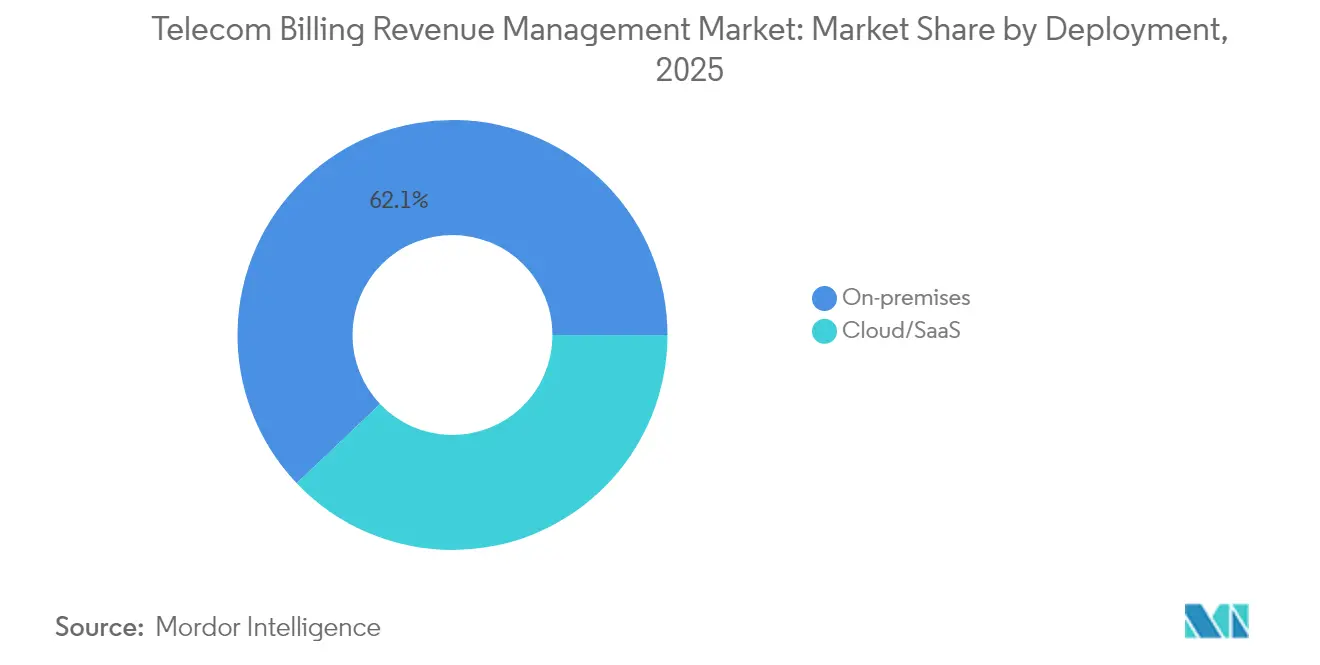

Geographic dynamics reveal North America commanding 35.24% market share in 2024, while Asia Pacific emerges as the fastest-growing region with 12.88% CAGR through 2030. This regional divergence stems from North America's mature infrastructure investments versus Asia Pacific's aggressive digital transformation initiatives, particularly in India and China, where regulatory frameworks are accelerating billing system modernization. The deployment segmentation shows on-premises solutions maintaining 62.85% market dominance, yet cloud deployments are experiencing 13.64% growth as operators prioritize scalability over control.

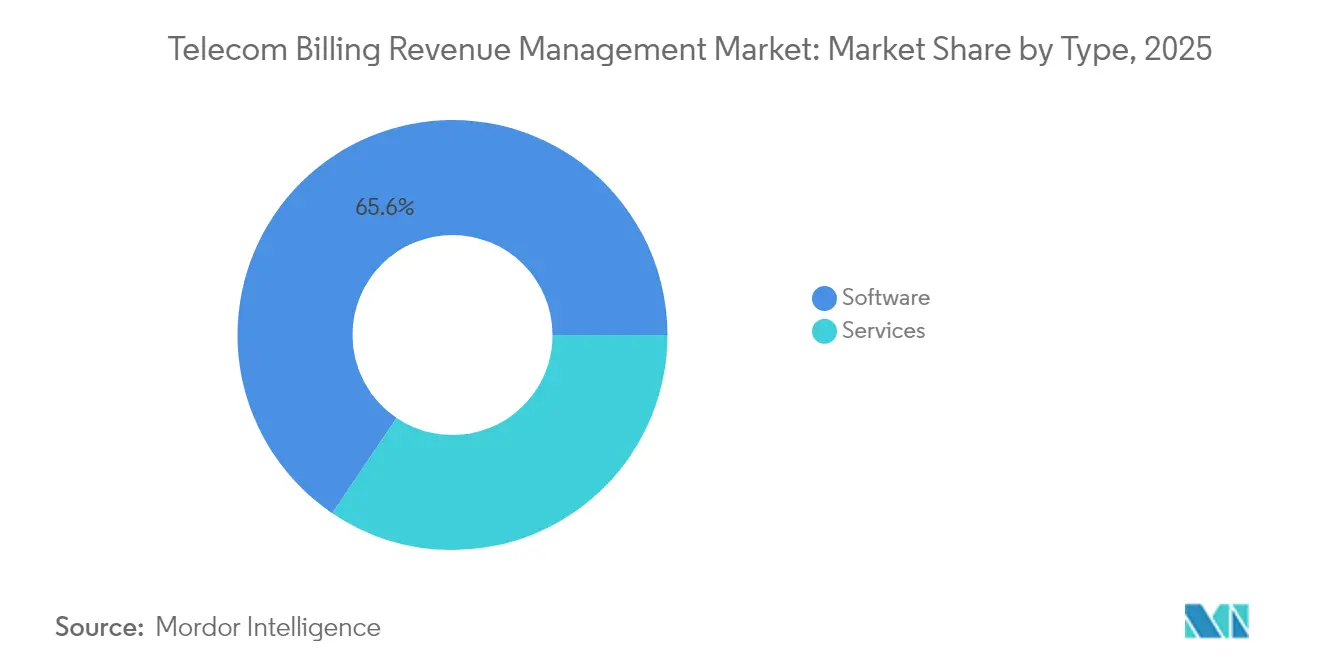

Competitive intensity has intensified as traditional BSS/OSS vendors face disruption from cloud-native specialists and AI-powered analytics platforms. The software segment's 66.24% market share contrasts sharply with services growing at 14.32% CAGR, indicating a shift toward managed billing solutions as operators seek to reduce operational complexity. Mobile operators retain 63.42% market control, though Internet Service Providers are expanding at 13.21% CAGR as fiber deployments create new revenue management requirements.

The market faces dual pressures from regulatory compliance costs and technological obsolescence risks. European operators confront EUR 2.5 billion in additional compliance expenses under the EU AI Act, while legacy billing systems increasingly constrain 5G service innovation[1]TM Forum, “EU AI Act Implications for Telcos,” TM Forum, May 1, 2025, tmforum.org. Simultaneously, the emergence of network API monetization through initiatives like Aduna represents a USD 10-30 billion revenue opportunity that demands fundamentally different billing architectures.

Key Report Takeaways

- By deployment type, on-premises solutions held 62.10% of 2025 revenue, while cloud deployments are projected to post the fastest 13.12% CAGR to 2031.

- By type, software commanded 65.55% of the 2025 segment, and services are set to grow fastest at 13.88% CAGR through 2031.

- By operator category, mobile operators contributed 62.85% of 2025 revenue, whereas Internet Service Providers are forecast to expand at 12.96% CAGR to 2031.

- By geography, North America captured 34.95% of 2025 revenue; the Asia Pacific segment is projected to grow at the fastest 12.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Telecom Billing Revenue Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Number of Cellular or Mobile Subscribers | +3.20% | Global, with strongest impact in Asia Pacific and Africa | Medium term (2-4 years) |

| Growing Complexities in Revenue Sharing Across the Telecom Ecosystem | +2.80% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Cloud-native BSS transformations by Tier-1 CSPs | +2.50% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expansion of private 5G and campus networks | +1.80% | North America, Europe, Asia Pacific enterprise markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Number of Cellular or Mobile Subscribers

The exponential growth in mobile subscribers, particularly in emerging markets, is fundamentally reshaping billing system requirements beyond traditional voice and SMS models. Asia Pacific's mobile subscriber base reached 1.8 billion in 2024, with 5G connections projected to grow significantly by 2030, creating unprecedented billing complexity for operators managing hybrid 2G-5G customer portfolios. This subscriber surge drives demand for real-time charging systems capable of processing millions of micro-transactions per second, particularly as operators launch IoT services requiring granular usage-based billing. For instance, India's implementation of anti-fraud measures that reduced spoofed calls by 90% demonstrates how subscriber growth necessitates sophisticated revenue assurance capabilities. The challenge extends beyond volume to service diversity, where a single subscriber might simultaneously consume mobile broadband, edge computing, and network API services, each requiring distinct billing logic. The billing infrastructure investment required to support this growth represents a fundamental shift from periodic batch processing to continuous real-time revenue management.

Growing Complexities in Revenue Sharing Across the Telecom Ecosystem

Revenue sharing complexity has evolved from simple interconnect agreements to intricate multi-party ecosystems involving cloud providers, content partners, and API developers. The emergence of network API monetization through platforms like Aduna, where AT&T, T-Mobile, and Verizon collaborate to standardize 5G capabilities, creates new revenue-sharing models that traditional billing systems cannot accommodate. These partnerships require real-time revenue allocation across multiple stakeholders, with settlement periods measured in minutes rather than months. The complexity deepens with 5G network slicing, where enterprise customers purchase dedicated network resources that must be billed based on performance guarantees and usage patterns across multiple network domains. For example, Ericsson's collaboration with major operators to create a global network API platform highlights how revenue sharing now extends beyond traditional telecom boundaries into software-as-a-service models[2]Capacity Media, “Operators Unite on Global API Marketplace,” Capacity Media, August 7, 2025, capacitymedia.com. The billing systems must now support dynamic revenue allocation algorithms that adjust in real-time based on service performance, usage patterns, and contractual terms across multiple parties.

Cloud-native BSS transformations by Tier-1 CSPs

Tier-1 Communication Service Providers are accelerating cloud-native BSS transformations to achieve operational agility and cost efficiency that legacy systems cannot deliver. These transformations enable operators to launch new services in weeks rather than months, while reducing total cost of ownership by 30-40% through automated scaling and reduced infrastructure overhead. For instance, TIM Brasil's selection of Ericsson's cloud billing solution exemplifies this transition, enabling the operator to modernize its revenue management capabilities while reducing infrastructure complexity. The cloud-native approach facilitates microservices architectures that allow operators to update individual billing components without system-wide disruptions, critical for maintaining service continuity during rapid product launches. Material cost pressures in data center hardware have accelerated these migrations, as cloud-native platforms eliminate the need for expensive on-premises infrastructure refresh cycles. The transformation extends beyond cost savings to enable real-time analytics and AI-powered revenue optimization that legacy systems cannot support. However, the migration complexity requires specialized expertise and careful orchestration to avoid revenue disruption during transition periods.

Expansion of private 5G and campus networks

Private 5G and campus network deployments are creating entirely new billing paradigms that challenge traditional connectivity-based revenue models. Enterprise customers increasingly demand performance-guaranteed network slices with usage-based billing tied to specific application requirements rather than simple bandwidth consumption. For example, Verizon's launch of 5G Standalone network slicing for public safety demonstrates how operators are developing specialized billing models for dedicated network resources. These deployments require billing systems capable of measuring and charging for network performance metrics, including latency, reliability, and security levels, rather than traditional volume-based metrics. The complexity increases with multi-tenant campus networks where multiple enterprises share infrastructure while requiring isolated billing and service-level agreements. Material cost inflation in 5G equipment has driven operators to implement more sophisticated billing models that capture the full value of private network investments. The billing challenge extends to edge computing services co-located with private networks, where operators must charge for compute resources, storage, and data processing in addition to connectivity services.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of Stringent Telecom Regulations | -1.80% | Global, with the highest impact in Europe and North America | Short term (≤ 2 years) |

| Legacy OSS/BSS integration complexity | -1.50% | Global, particularly established operators in mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Presence of Stringent Telecom Regulations

Regulatory compliance costs are creating significant headwinds for billing system investments, particularly as operators navigate conflicting requirements across multiple jurisdictions. The EU AI Act's implementation through 2027 imposes substantial compliance burdens on telecom operators deploying AI-powered billing systems, with penalties reaching 4% of global annual revenue for non-compliance. European operators face additional complexity from the Electronic Communications Code's harmonized termination rates, requiring billing system modifications to accommodate EUR 0.2 per minute mobile call rates by 2024. For instance, India's Personal Data Law creates compliance costs that directly impact billing system architecture and data processing capabilities, forcing operators to implement additional security layers and audit trails. These regulations often conflict with operational efficiency goals, forcing operators to choose between compliance and innovation. The cumulative effect constrains billing system modernization budgets as operators allocate resources to regulatory compliance rather than revenue-generating capabilities.

Legacy OSS/BSS integration complexity

Legacy OSS/BSS integration complexity represents a fundamental barrier to billing system modernization, as operators struggle to maintain service continuity while upgrading decades-old infrastructure. The challenge stems from proprietary interfaces and custom integrations that create technical debt exceeding USD 100 million for major operators attempting comprehensive system replacements. For example, the complexity of integrating new cloud-native billing platforms with existing customer databases, network management systems, and regulatory reporting tools often doubles implementation timelines and costs. Material cost pressures have intensified this challenge, as operators cannot afford parallel system operations during extended migration periods. The integration complexity is compounded by data migration requirements, where operators must transfer millions of customer records and billing histories without revenue disruption. Legacy systems often lack APIs necessary for real-time integration with modern billing platforms, requiring expensive middleware solutions or custom development. The technical debt accumulated over decades of incremental upgrades creates interdependencies that make system replacement a high-risk proposition for operators dependent on continuous revenue flow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Migration Accelerates Despite Security Concerns

On-premises deployments maintained 62.10% market share in 2025, reflecting operators' continued preference for direct control over mission-critical billing infrastructure. However, cloud deployments are experiencing 13.12% CAGR through 2031, driven by operators seeking to reduce capital expenditure and accelerate time-to-market for new services. The deployment divide reflects fundamental differences in operator priorities, where established carriers prioritize security and regulatory compliance while emerging operators focus on operational agility and cost efficiency. For instance, M1 Singapore's implementation of Amdocs' cloud-native charging platform demonstrates how operators can achieve both scalability and security through carefully architected cloud solutions.

The cloud migration trend is accelerating as vendors introduce hybrid deployment models that address security concerns while delivering cloud benefits. Material cost inflation in data center equipment has made cloud deployments increasingly attractive, as operators can avoid capital expenditure cycles while accessing the latest-generation infrastructure. The deployment choice increasingly depends on regulatory requirements, with European operators favoring on-premises solutions due to data sovereignty concerns, while Asian operators embrace cloud deployments for rapid market expansion. This segmentation will likely converge toward hybrid models as cloud security capabilities mature and regulatory frameworks adapt to cloud-native architectures.

By Type: Services Growth Outpaces Software as Complexity Increases

Software solutions command 65.55% market share in 2025, yet services are growing at 13.88% CAGR, indicating operators' increasing reliance on managed billing solutions to navigate technological complexity. This growth differential reflects the market's evolution from product-centric to outcome-based business models, where operators prioritize billing system performance over ownership. The services growth is particularly pronounced in emerging markets, where operators lack the technical expertise to manage complex billing transformations independently. For instance, Telecom Namibia's partnership with SATEC for its ISBP 2027 digital transformation illustrates how operators are outsourcing billing system management to focus on core business activities.

The services segment's expansion is driven by the complexity of integrating AI and machine learning capabilities into billing systems. Optiva's introduction of generative AI-enabled BSS platforms demonstrates how vendors are packaging advanced capabilities as managed services rather than standalone software products. Software vendors are increasingly adopting software-as-a-service models to capture recurring revenue while reducing customer implementation risks. This shift suggests the traditional software licensing model will give way to outcome-based pricing, where vendors share revenue risk with operators in exchange for performance guarantees.

By Operator: ISPs Challenge Mobile Operator Dominance

Mobile operators retain 62.85% market share in 2025, leveraging their subscriber scale and billing infrastructure investments to maintain market leadership. However, Internet Service Providers are expanding at 12.96% CAGR, driven by fiber deployment acceleration and the emergence of fixed wireless access services that blur traditional service boundaries. The ISP growth reflects fundamental changes in connectivity consumption patterns, where consumers increasingly prioritize broadband speed over mobility, creating new billing requirements for usage-based and performance-guaranteed services. For instance, Verizon's addition of 408,000 broadband subscribers in Q4 2024 demonstrates how traditional mobile operators are expanding into ISP territories.

MVNO/MVNE operators represent an emerging segment driving billing innovation through specialized service models and agile business approaches. These operators often pioneer new billing technologies due to their flexibility and lack of legacy infrastructure constraints. The operator segmentation is converging as 5G technology enables mobile operators to offer fixed wireless access while ISPs deploy mobile backhaul services. This convergence creates billing complexity as operators must manage hybrid service portfolios that span traditional boundaries. The competitive dynamics are shifting toward platform-based business models, where operators monetize network capabilities through API access rather than traditional connectivity services.

Geography Analysis

North America maintained 34.95% market share in 2025, driven by mature infrastructure investments and regulatory stability that encourage billing system modernization. The region's market leadership reflects operators' willingness to invest in advanced billing capabilities, with Verizon's USD 20 billion acquisition of Frontier Communications demonstrating the scale of infrastructure consolidation driving billing system requirements. For instance, AT&T has implemented comprehensive digital transformations, with Oracle Cloud ERP and EPM deployments enabling more sophisticated revenue management capabilities. The United States dominates regional growth through 5G network API initiatives and private network deployments, while Canada and Mexico contribute through fiber infrastructure expansion and regulatory modernization efforts. However, growth is moderating as market saturation limits subscriber expansion and operators focus on optimizing existing infrastructure rather than expanding capacity.

Asia Pacific emerges as the fastest-growing region with 12.51% CAGR through 2031, fueled by aggressive digitalization initiatives and regulatory reforms that accelerate billing system modernization. China's three major operators, China Mobile, China Unicom, and China Telecom, collectively generated over CNY 1.6 trillion (USD 240 billion) in revenue during 2024, with significant investments in cloud-native billing platforms and AI-powered revenue optimization Sohu. For instance, China Mobile's intelligent operations management system demonstrates the region's leadership in AI-driven billing optimization. India's telecom sector demonstrates the region's transformation potential, with operators implementing tariff increases to fund 5G infrastructure while deploying advanced fraud prevention systems. Japan contributes through enterprise 5G deployments and network slicing innovations that require sophisticated billing capabilities.

South America presents emerging opportunities driven by fiber infrastructure expansion and regulatory modernization, with Brazil leading regional growth through operator consolidation and technology upgrades. For example, Millicom's 2024 revenue reached USD 5.80 billion, with strong growth in postpaid subscribers driving billing system requirements across multiple Latin American markets. Europe faces mixed growth prospects due to regulatory compliance costs under the EU AI Act and Electronic Communications Code, constraining billing system investment budgets. However, the region benefits from advanced 5G deployments and network API initiatives that create new revenue opportunities. The Middle East and Africa present emerging opportunities, with operators like Omantel completing comprehensive digital transformations that modernize billing infrastructure.

Regulatory Landscape

Tariff regulation, regulatory accounting, and reporting regimes shape telecom billing and revenue management across jurisdictions. In India, the Telecommunication Tariff (Seventy Second Amendment) Order, 2026, issued March 2026, updates regulatory reporting and accounting separation provisions, pushing operators to harden billing controls, reconciliation, and documentation workflows.

In the United States, the FCC advanced intercarrier compensation reforms via a 2026 NPRM that moves remaining charges toward a bill-and-keep framework and proposes removing ex ante tariffing for certain access charges. International and regional anchors include ITU-T Recommendation D.265 (April 2025) with data service tariff regulation principles, and BEREC Regulatory Accounting in Practice 2025 (December 2025) reinforcing converging costing and accounting approaches, which raises the need for regulator-ready outputs.

Value Chain Analysis

The value chain spans standards and frameworks that define charging and billing interfaces, CSPs that own customer relationships and service catalogs, BSS software vendors delivering convergent charging, billing, product catalog, and revenue assurance capabilities, and system integrators and cloud providers enabling scalable deployments and analytics. On the standards layer, 3GPP TS 32.240 (charging architecture) and TS 32.291 (service-based interfaces) influence real-time charging for 5G and converged services, while TM Forum APIs and bill calculation specifications shape interoperability and integration patterns.

Implementation bottlenecks and partner ecosystems show up in B2B2X settlement and revenue-sharing workflows, where billing is tied to partner management, fraud and anomaly detection, and customer experience tooling. TIM Brasil worked with Ericsson to consolidate cloud billing on Oracle Cloud Infrastructure, and Circles signed a strategic collaboration with Huawei to combine network and cloud capabilities with a digital BSS SaaS platform, highlighting how cloud infrastructure, vendor software, and integration expertise are packaged together to accelerate modernization.

Competitive Landscape

The telecom billing revenue management market exhibits moderate consolidation with intensifying competition between traditional BSS/OSS vendors and cloud-native specialists. Established players like Amdocs, Oracle, and Ericsson maintain market leadership through comprehensive platform offerings, yet face disruption from agile competitors leveraging AI and cloud-native architectures. For instance, Amdocs' research revealing that 90% of service providers consider generative AI critical for business goals, while only 22% have implemented it, highlights the innovation gap that creates opportunities for specialized vendors. The competitive dynamics are shifting toward platform-based business models, where vendors compete on ecosystem breadth rather than individual product capabilities. Strategic partnerships are becoming essential, as demonstrated by Optiva's collaboration with GDi to deliver integrated BSS and OSS solutions[4]OSS News Review, “Optiva and GDi Partner for Integrated BSS/OSS,” OSS News Review, April 4, 2024, ossnewsreview.com.

Technology differentiation increasingly centers on AI capabilities and cloud-native architectures that enable real-time revenue optimization. Vendors are investing heavily in generative AI platforms that can analyze customer behavior patterns and automatically generate pricing strategies, creating significant competitive advantages for early adopters. The market structure favors vendors that can deliver end-to-end solutions spanning billing, charging, and revenue assurance, as operators seek to reduce integration complexity. White-space opportunities exist in specialized areas like network API monetization and 5G network slicing billing, where traditional vendors lack domain expertise. Emerging disruptors are targeting these niches with purpose-built solutions that challenge incumbents' comprehensive platform strategies.

Telecom Billing Revenue Management Industry Leaders

Oracle Corporation

Nokia

Ericsson

SAP

Huawei Technologies

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Two opportunity areas are shaping market activity. First, legacy replacement programs and cloud-scale modernization: KDDI selected Oracle Cloud Scale Charging and Billing in February 2026 to replace legacy charging and rating and support a large catalog of use cases, while Vi expanded use of cloud-native Ericsson Charging in March 2026 alongside AI applications for anomaly detection and order fallout prediction. These programs raise demand for migration services, data conversion, catalog rationalization, and real-time mediation alongside core charging and billing software.

A second opportunity area sits at the intersection of national digital agendas, techco repositioning, and enterprise services monetization. Omantel partnered with Cerillion in April 2026 for a BSS/OSS transformation on Cerillion Cloud aligned to Oman Vision 2040, and Zain KSA (Yaqoot) partnered with Huawei in April 2026 to upgrade BSS to accelerate digital product development and automation. As private networks, network slicing, and B2B offerings expand, operators and wholesale providers pull billing closer to service fulfillment and operations. In May 2026, Ishan Technologies selected Oracle Cloud Scale Monetization and Oracle Unified Operations to link charging and billing with service fulfillment, pointing to demand for end-to-end, API-driven monetization stacks rather than standalone billing upgrades.

Recent Industry Developments

- June 2026: Lightpath implemented Oracle Cloud Scale Billing to modernize its billing operations and support digital services monetization across enterprise offerings. The update strengthens cloud-scale billing adoption for fiber-centric providers and aligns billing with faster product configuration and service changes in B2B portfolios.

- May 2026: Ishan Technologies selected Oracle Communications to implement Oracle Cloud Scale Monetization and Oracle Unified Operations as part of an end-to-end charging and billing transformation. The program ties monetization more tightly to service fulfillment and operations, reinforcing demand for integrated, cloud-native revenue stacks over isolated billing replacements.

- October 2024: Omantel and Optiva completed a comprehensive digital transformation project to enhance telecom billing and revenue management capabilities as part of broader operational modernization. The completion shows continued operator investment in modern billing foundations that can support new digital products and reduce friction from legacy processes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the telecom billing revenue management market covers software and services used by telecom operators to rate usage, produce bills, collect payments, and reduce revenue leakage across prepaid and postpaid customers, with delivery available through on-premise deployments and cloud setups.

Scope exclusions: We exclude general IT outsourcing and non-telecom enterprise billing tools that are not sold for telecom operator billing and revenue assurance needs.

Segmentation Overview

- By Deployment

- On-premise

- Cloud/SaaS

- By Type

- Software

- Services

- By Operator

- Mobile Operator

- Internet Service Provider

- MVNO/MVNE

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- Turkey

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research built the first structure of the model by mapping what operators must run to monetize services, and how these needs shift with newer plans (bundles, data-heavy offers, and digital channels). We reviewed public references such as ITU indicators, GSMA publications, FCC releases, OECD telecom statistics, and World Bank data to anchor subscriber trends, traffic growth, and regional market maturity.

We then cross-checked the supply side using sources like annual reports, investor presentations, press releases, and relevant standards documentation. This helped us understand product boundaries between billing, charging, mediation, and revenue assurance. In addition, paid subscriptions for company financials and intelligence, along with patent databases and a news and financials feed, supported faster validation of vendor exposure and product direction. The desk sources listed here are illustrative only, and many other public references were also used to collect, verify, and clarify data points.

Primary Interviews and Surveys

Primary work focused on validating what is actually purchased, how deals are structured (software versus services), and how cloud adoption changes spend timing. We spoke with a mix of telecom operator stakeholders and solution-side experts across major regions, so assumption gaps from desk research could be closed. Key inputs such as adoption pace, pricing direction, and refresh cycles were also confirmed through these discussions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 48% |

| Mid tier: 52% | Functional/Unit leaders: 33% | EMEA: 31% |

| Smaller Players: 15% | Managers: 55% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool, where operator counts, subscriber base direction, and service mix are used to reconstruct likely spend on billing and revenue management capabilities by region. The model is then corroborated with selective bottom-up checks, such as sampled deal values from public disclosures, vendor revenue exposure signals, and channel feedback on implementation and managed services shares, and the totals are adjusted when gaps show up.

A few inputs mattered most were the pace of cloud migration for BSS, the prepaid versus postpaid mix and how it changes charging requirements, new digital product launches that increase catalog complexity, and the intensity of revenue leakage and fraud controls that drives revenue assurance upgrades. We also tracked operator modernization cycles and the typical split between software license or subscription and associated services (implementation, integration, and support), because these choices change annual spend patterns.

Forecasts were built using scenario analysis, where adoption curves for cloud BRM, 5G monetization readiness, and operator capex-to-opex shifts are stress-tested, and then aligned to what interviewees describe as realistic budget windows. When bottom-up visibility is incomplete in smaller regions, we apply conservative penetration and spend-per-operator assumptions, then re-check them with primary feedback before finalizing the series.

Data Validation & Update Cycle

To validate results, we compare outputs against independent signals like subscriber additions, telecom service revenue direction, and publicly discussed BSS transformation activity, then investigate outliers at the region and component level. If a variance is driven by one assumption, we rework that input and, when needed, re-contact experts so the change is justified and documented.

Before sign-off, the model goes through multiple analyst review steps, including sanity checks on pricing progression, services mix, and year-to-year continuity. Reports are refreshed annually, with interim updates triggered by material events such as large operator modernization waves, policy shifts impacting telecom billing, or clear changes in cloud adoption. Right before delivery, a fresh review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Telecom Billing Revenue Management Market Size Measured Against Other Published Estimates

Published market sizes for telecom billing revenue management often differ because the scope lines are drawn differently, and because some studies lean more on vendor-side headlines than on operator-side demand checks. We treated the market as the combined spend on billing and revenue management software plus related services, and we kept the time series consistent so year-over-year movement stays explainable.

Operator transformation programs, cloud BSS migration signals, and the observed split between software and implementation services are the evidence checks that keep Mordor Intelligence's estimate tied to what telecom operators actually budget and deploy. Differences usually come from whether adjacent areas like broader BSS, CRM, or general managed IT are included, from how prepaid charging modules are counted, and from whether currency timing and inflation assumptions are refreshed to the same base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 24.43 B (2026) | |

| Industry Newswire A | USD 18.00 B (2024) | Uses an earlier base year cycle and a shorter horizon, and the scope description is broader at the module level, which can shift boundaries between billing, charging, and adjacent BSS functions. |

| Market Bulletin B | USD 6.99 B (2027) | Reports market growth over a period (incremental value) instead of a single-year market size, which makes the figure not directly comparable to an annual USD market value. |

The spread in the table is mainly explained by definition choices and reporting formats, not by a single universal number being right for every use case. By keeping the spend boundary focused on telecom operator billing and revenue management, and by validating key variables with real adoption and budgeting signals, the final market value stays traceable to clear steps that can be repeated during updates.

Key Questions Answered in the Report

What is the current size of the telecom billing revenue management market?

The market is valued at USD 24.43 billion in 2026 and is projected to climb to USD 39.96 billion by 2031.

Which region is growing fastest?

Asia Pacific is forecast to post a 12.51% CAGR through 2031, outpacing all other regions.

Why are cloud deployments accelerating?

Operators migrate to cloud-native billing to shorten feature launch cycles and avoid large capital outlays, driving a 13.12% CAGR in cloud revenue.

How are regulations affecting billing investments?

The EU AI Act, India’s PDPA, and similar rules raise compliance spending, temporarily diverting budgets from modernization projects.

What role does AI play in billing transformation?

Generative AI automates product design, price optimization, and anomaly detection, enabling real-time revenue assurance and faster monetization of new services.

Who are the leading vendors in this market?

Amdocs, Oracle, and Ericsson dominate large-scale projects, although cloud-native entrants such as Optiva are gaining share with AI-driven platforms.

Page last updated on: