Retail Enterprise Resource Planning (ERP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

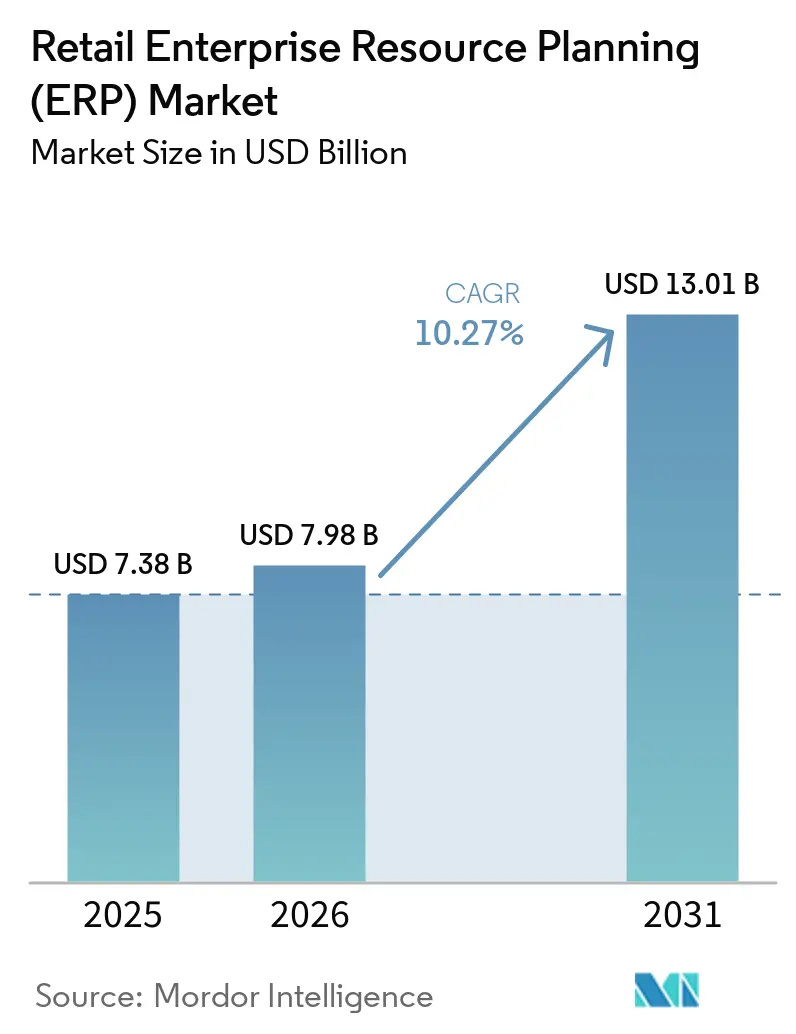

| Market Size (2026) | USD 7.98 Billion |

| Market Size (2031) | USD 13.01 Billion |

| Growth Rate (2026 - 2031) | 10.27% CAGR |

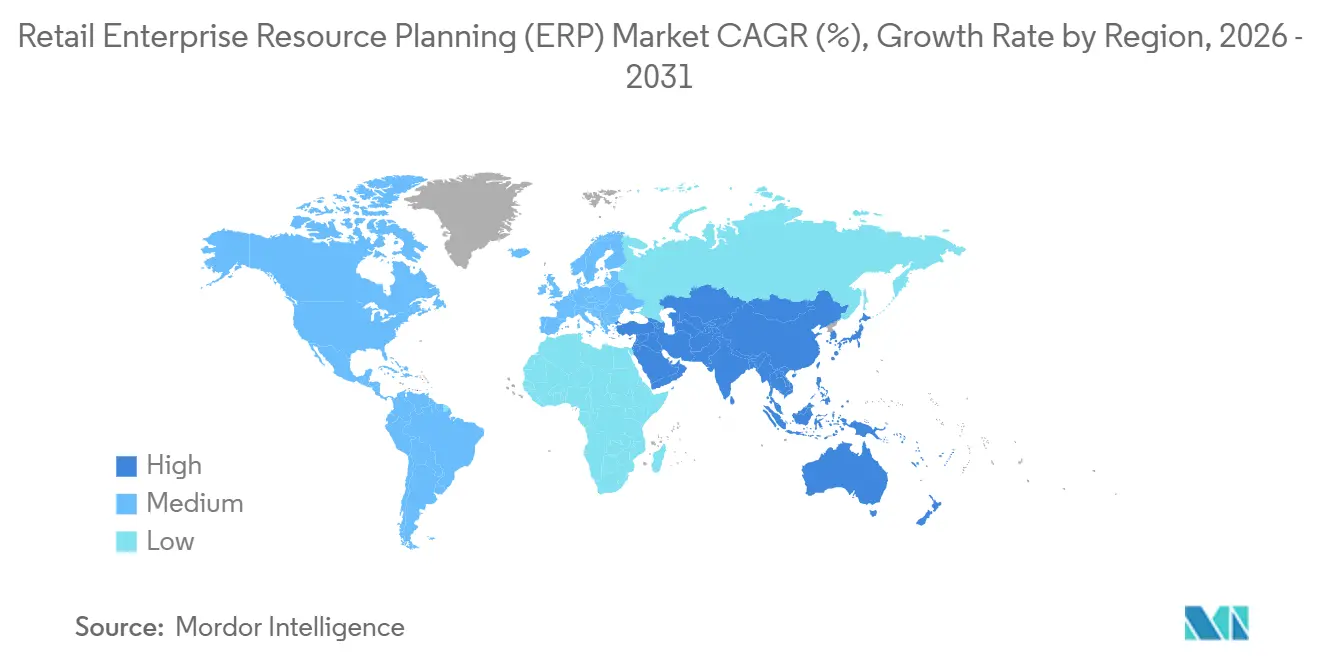

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

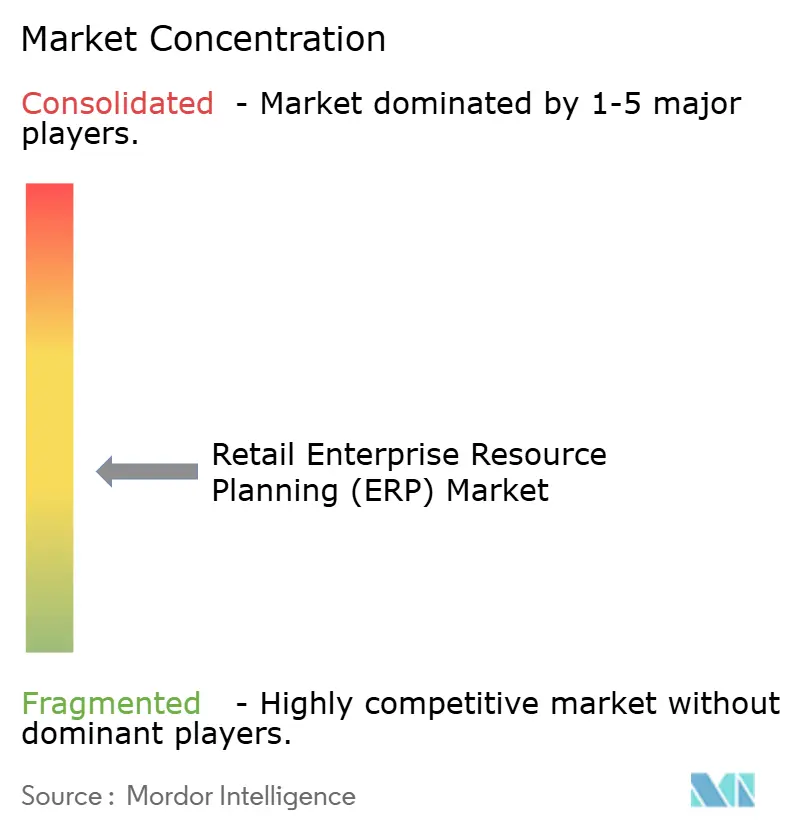

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retail Enterprise Resource Planning (ERP) Market Analysis by Mordor Intelligence

The retail enterprise resource planning market size is projected to expand from USD 7.38 billion in 2025 and USD 7.98 billion in 2026 to USD 13.01 billion by 2031, registering a CAGR of 10.27% between 2026 to 2031. Unifying store, e-commerce, and social-commerce operations into one data model anchors this growth, while cloud subscriptions lower entry barriers for mid-tier chains. Composable microservices let retailers swap modules without vendor lock-in, which is attracting specialty formats that need rapid innovation. Asia-Pacific keeps outpacing all other regions as mandatory e-invoicing drives platform upgrades, and embedded artificial intelligence baked into SaaS releases pushes real-time decision-making into every store aisle.

Key Report Takeaways

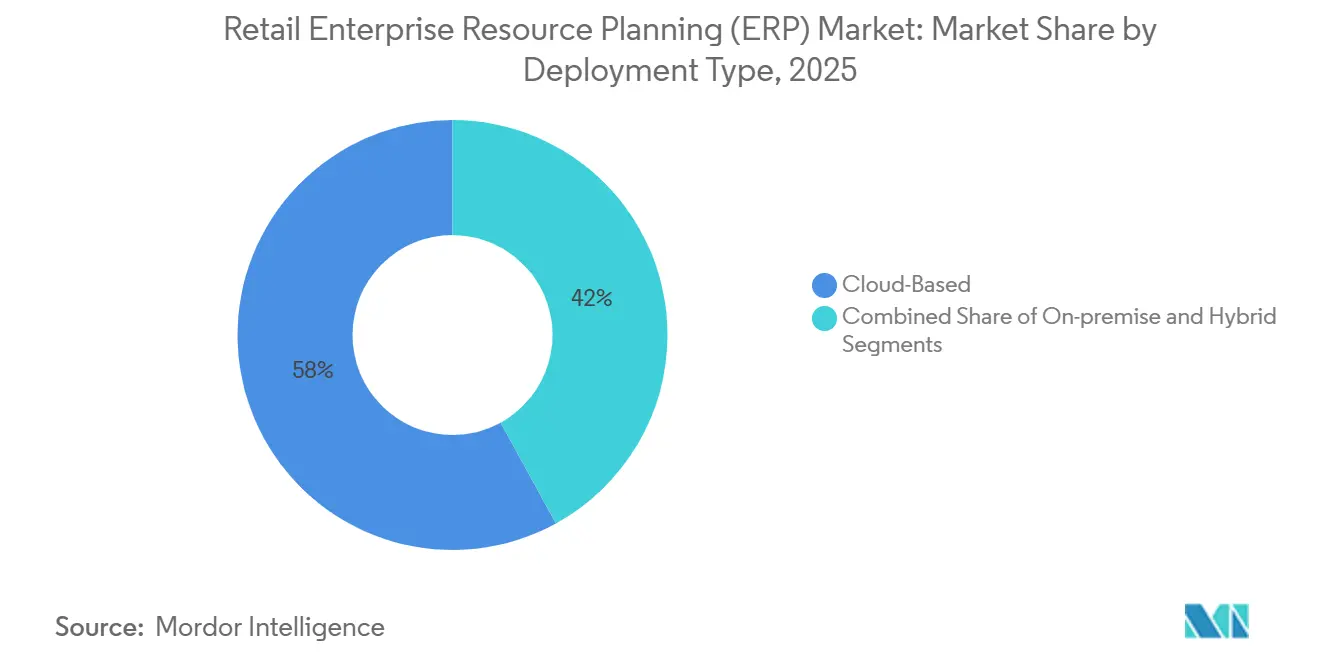

- Cloud deployments led with 58% retail enterprise resource planning market share in 2025, while the hybrid model is advancing at a 9.4% CAGR through 2031.

- Small and medium-sized enterprises commanded 62.4% of installations in 2025 and are growing at a 10.1% CAGR through 2031.

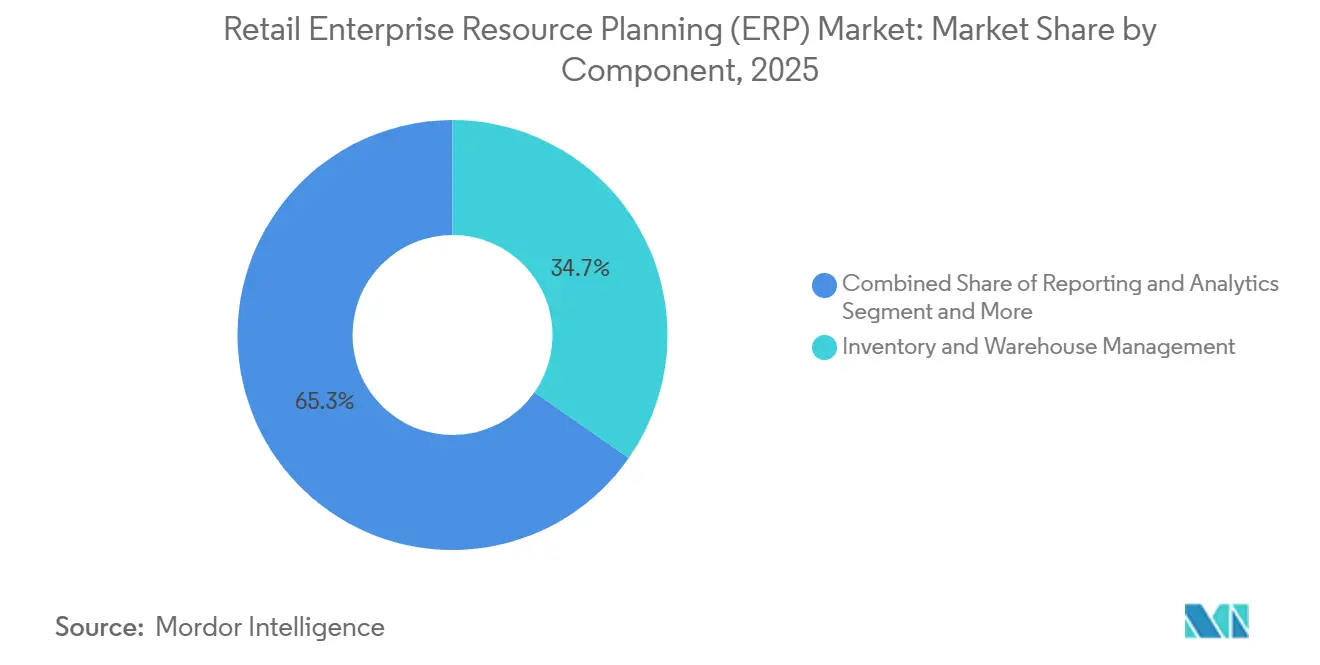

- Inventory and warehouse management accounted for 34.7% of component revenue in 2025; reporting and analytics modules are growing fastest at a 11.5% CAGR through 2031.

- Supermarkets and hypermarkets accounted for 29.5% of format revenue in 2025, yet e-commerce and omnichannel retailers are expanding at a 12.6% CAGR during the forecast period.

- Asia-Pacific accounted for 37.9% of global revenue in 2025 and is set to grow at a 12.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Retail Enterprise Resource Planning (ERP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Shift to Cloud-Based ERP in Retail | +2.8% | Global, highest penetration in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing Omnichannel Retail Complexity | +2.3% | Global, especially North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Rising Demand for Real-Time Inventory Visibility | +1.9% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Government Mandates for E-Invoicing and Digital Tax Compliance | +1.6% | Asia-Pacific, Middle East, South America | Short term (≤ 2 years) |

| AI-Driven Demand Forecasting Reduces Stockouts and Markdowns | +1.2% | Global, led by large enterprises in North America and Europe | Long term (≥ 4 years) |

| Integration of Embedded Payments within ERP Ecosystems | +0.8% | Asia-Pacific and Europe, emerging in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift to Cloud-Based ERP In Retail

Cloud subscriptions represented most new installs in 2025 because retailers want automatic upgrades, elastic compute, and lower infrastructure costs. Hybrid strategies are catching on as chains keep sensitive customer data on local servers to meet data-residency laws, while stream analytics workloads run in public clouds for scale. Mid-sized specialty retailers gain the most because per-store pricing now replaces six-figure perpetual licenses, slashing up-front costs and shrinking implementation windows to under 18 months. The transition also unlocks embedded AI features, such as dynamic pricing, that depend on scalable compute unavailable in legacy data centers.

Growing Omnichannel Retail Complexity

Click-and-collect, ship-from-store, and endless aisle services drive demand for real-time order-management engines. Split-shipment costs drop and fulfillment decisions are optimized when inventory, pricing, and loyalty data live in a single ledger that spans stores, websites, and social-commerce feeds. Modern ERP suites eliminate overnight batch transfers, so a markdown decision propagates in minutes across all locations where the product appears. Social-commerce integrations raise the bar further, compelling retailers to surface products, process payments, and resolve service tickets on external platforms that their legacy systems never contemplated.

Rising Demand for Real-Time Inventory Visibility

Item-level radio-frequency identification tagging lifted tracking accuracy above 98% in apparel and footwear, and retailers that moved early cut stockouts and unlocked same-store sales gains.[1]RAIN RFID Alliance, “RFID Statistics,” rainrfid.org IoT sensors on shelves, freezers, and conveyors now stream status data straight into the ERP core, creating digital twins that flag spoilage risks or replenish gaps before customers notice. Large chains report double-digit reductions in excess stock and billions freed in working capital once real-time data replaces overnight cycle counts.

Government Mandates for E-Invoicing and Digital Tax Compliance

Brazil, Saudi Arabia, and India now require invoices to be cryptographically signed and sent to government servers within seconds, pressuring even the smallest retailers to modernize. Vendors with pre-built connectors to national tax portals gain an advantage, while smaller software houses scramble to code updates for each jurisdiction. Europe is set to expand the net with continuous transaction reporting across all member states by 2028, pushing multinationals toward single ERP instances capable of handling divergent formats and rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation Costs and Budget Overruns | -1.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Data Security and Privacy Concerns | -1.1% | Global, especially Europe and selected U.S. states | Medium term (2-4 years) |

| Shortage of Retail-Specific ERP Talent | -0.6% | Global, most severe in Asia-Pacific and Africa | Long term (≥ 4 years) |

| Disruption Risk from Composable Architectures | -0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs and Budget Overruns

Nearly three-quarters of recent projects ran over budget, with overruns due to scope creep, messy data migrations, and underestimated change management inflate service hours. Mid-market retailers feel the crunch most because they lack deep IT benches and discover too late that canned templates still need customization. Hidden costs such as third-party integration licenses, dual-running old and new systems, and per-user SaaS fees that spike during peak seasons can drive total ownership above a decade of perpetual-license spend.

Data Security and Privacy Concerns

Retail breaches exposed over a billion customer records in 2024, reminding chains that centralized ERP databases attract cybercriminals.[2]Identity Theft Resource Center, “Data Breach Report 2024,” idtheftcenter.org GDPR fines reached multibillion-dollar levels, and retailers remain on the hook even when the breach stems from a cloud vendor misconfiguration. The explosion of application-programming-interface connections multiplies potential vulnerabilities, while data-localization rules in China and cross-border data transfers in Europe complicate architectural decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Models Bridge Compliance and Agility

Hybrid deployments are gaining ground in the retail enterprise resource planning market as chains mix on-premises data stores with cloud analytics to comply with local regulations while still tapping elastic compute. The retail enterprise resource planning market size for hybrid solutions is advancing alongside edge servers that keep point-of-sale running during network outages, then synchronize later for central reporting. Multinationals operating in China or the European Union prefer this setup because customer data never leaves national borders, while aggregate insights roll into a global dashboard. Edge modules running on compact servers extend uptime in rural stores where broadband is shaky, ensuring every sale posts even during outages.

Hybrid adoption also supports phased migration paths. Retailers move finance and HR to SaaS first, test integrations, then tackle inventory and order workflows once data cleanliness improves. Azure Stack and similar platforms provide a unified management plane, so IT teams can monitor on-premises and cloud workloads from a single console, reducing admin effort. While on-premise still survives in high-control environments such as luxury or pharmacy, the operational burden of patches and hardware refresh cycles continues to erode its share.

By Organization Size: SMEs Drive Volume Through Subscription Economics

SMEs accounted for 62.4% of deployments in 2025 and will continue to expand faster than their larger peers because per-resource pricing eliminates six-figure entry fees. Subscription bundles that include infrastructure, support, and future upgrades compress implementation to fewer than 90 days, allowing small chains to focus on merchandising rather than server upkeep. Vendors now ship pre-configured chart-of-accounts and promotional engines that drop into a new tenant without coding, shaving consultant hours, and accelerating value capture. The retail enterprise resource planning industry nevertheless faces a skills gap, as SMEs rarely employ full-time ERP administrators and must rely on vendor-managed services for troubleshooting.

Large enterprises buy deeper functionality such as multi-entity consolidations, global tax engines, and advanced supply-chain planning, which boosts average deal size. Yet complexity stretches deployments well beyond a year and inflates customization budgets, especially where franchise or joint-venture accounting demands unique data models. As a result, total enterprise license revenue outweighs sheer SME volume, and system integrators still build sizable practices around big-chain projects.

By Component: Analytics Modules Outpace Core Financials

Inventory and warehouse management accounted for the largest share at 34.7% in 2025, as right-sizing stock remains mission-critical. Reporting and analytics, however, top the growth chart, with a 11.5% CAGR as merchants embed machine learning to set dynamic prices and preempt markdowns. The retail enterprise resource planning market size for analytics components is expected to eclipse finance modules near the forecast horizon, as predictive dashboards sit directly within the transactional system, avoiding data hops into standalone BI stacks.

Finance keeps steady but commoditized, while supply-chain modules gain momentum among grocers and apparel sellers that juggle volatile demand and short shelf lives. CRM and marketing tools converge within ERP suites to build a single customer view that fuels loyalty campaigns and personalized promotions. HR remains niche because retailers prefer specialist workforce-management applications for shift planning and labor law compliance.

By Retail Format: E-Commerce Velocity Reshapes System Requirements

Supermarkets and hypermarkets generated the highest revenue in 2025, reflecting large SKU counts and perishable goods that demand robust integration between point-of-sale and back-office replenishment systems. At the same time, e-commerce and omnichannel operators are the fastest-growing cohort, with a 12.6% CAGR. They prioritize unified order management and real-time stock checks that legacy systems cannot match, driving migration to modular cloud suites.

Specialty stores ranging from cosmetics to sporting goods adopt ERP systems to compete with category killers, often starting with core inventory and loyalty modules before layering on complex supply-chain planning. Department stores face the steepest path due to vendor-managed inventory and consignment models that complicate data models, while convenience stores gravitate toward lightweight SaaS that runs on mobile devices and syncs offline sales once connectivity returns.

Geography Analysis

Asia-Pacific anchors the retail enterprise resource planning market, driven by stringent e-invoicing laws and exploding mobile commerce volume. Government portals in India processed billions of invoices in fiscal 2025, making automated tax reconciliation a must-have rather than a future wish. In China, over two-thirds of sizable retail chains already run cloud ERP, integrating local payment gateways directly into back-office ledgers to accelerate cash settlement.[3]Cyberspace Administration of China, “Cybersecurity Law,” cac.gov.cn Southeast Asian sellers on regional marketplaces must meet 24-hour fulfillment promises, which requires ERP-driven inventory accuracy at the seller level rather than the warehouse level.

North America is a mature yet innovative landscape, shifting its focus from migration to optimization. Retailers fine-tune buy-online-pick-up-in-store workflows, trim split-shipment costs, and pilot AI recommendations inside store apps. Stringent state privacy laws drive granular role-based access controls and tokenization of customer identifiers inside ERP databases. Canada shows parallel trends, though bilingual requirements add another layer of design complexity.

Europe balances modernization with compliance. GDPR audits add months to cloud-vendor selection, but the upcoming VAT-in-the-Digital-Age program is already prompting chains to centralize onto platforms that can deliver continuous transaction reporting across 27 jurisdictions.[4]European Commission, “VAT in the Digital Age,” ec.europa.eu Nordic retailers push early into composable microservices, swapping modules without full re-platforming, while Southern European chains focus on cost control through SaaS subscriptions that replace aging on-premise systems.

Competitive Landscape

The market is moderately fragmented, with the top five vendors controlling a significant share in 2025, leaving room for vertical and regional challengers. SAP dominates large multinational deployments thanks to deep franchise accounting and multi-country consolidation, yet price pressure mounts from cloud-native players selling module-level subscriptions at a fraction of legacy fees. Microsoft wins over mid-market chains by bundling point-of-sale, e-commerce, and ERP into a single platform, eliminating middleware and simplifying support contracts.

Oracle covers both ends of the spectrum, positioning Fusion Cloud for global retailers and NetSuite for single-country brands, though internal channel conflicts require careful account planning to avoid overlap. White-space opportunities abound in niche formats such as pharmacies and automotive parts, where compliance needs differ sharply from those in mass fashion.

Vendors in the MACH Alliance advocate microservice architectures that let retailers swap underperforming modules without forklift upgrades, a model that appeals to digital-native brands that iterate quickly. Regional suppliers in India and Latin America undercut global names on price and localization, offering vernacular interfaces and tax-ready templates out of the box. Supply-chain specialists such as Blue Yonder now package ERP, warehouse, and transportation modules into unified suites, signaling convergence that blurs historical product boundaries.

Retail Enterprise Resource Planning (ERP) Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor, Inc.

Epicor Software Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Oracle launched Retail AI Foundation within Fusion Cloud ERP, with pilot users reporting 23% less excess stock and 15% gross-margin gains.

- February 2026: SAP and Google Cloud expanded collaboration to run S/4HANA Retail on Google Cloud Platform, bundling BigQuery for instant analytics.

- January 2026: Microsoft added Copilot conversational features to Dynamics 365 Commerce, supporting 12 languages for inventory checks and returns.

- December 2025: Infor acquired Aptos, merging the customer bases of more than 12,000 retail chains under CloudSuite Retail.

Global Retail Enterprise Resource Planning (ERP) Market Report Scope

The Retail ERP market refers to the ecosystem of specialized enterprise software solutions and associated services designed to manage, integrate, and optimize core business processes across retail organizations, including in-store, online, and omnichannel operations.

The Retail ERP Market Report is Segmented by Deployment Type (Cloud-Based, On-Premise, and Hybrid), Organization Size (SMEs and Large Enterprises), Component (Finance and Accounting, Inventory and Warehouse Management, and Other Components), Retail Format (Supermarkets and Hypermarkets, Specialty Stores, and Other Retail Formats), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premise |

| Hybrid |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| Finance and Accounting |

| Inventory and Warehouse Management |

| Sales and Customer Relationship Management |

| Human Resource Management |

| Supply Chain Management |

| Reporting and Analytics |

| Other Components |

| Supermarkets and Hypermarkets |

| Specialty Stores |

| Department Stores |

| Convenience Stores |

| E-Commerce and Omnichannel Retailers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Type | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Small and Medium-Sized Enterprises | |

| Large Enterprises | ||

| By Component | Finance and Accounting | |

| Inventory and Warehouse Management | ||

| Sales and Customer Relationship Management | ||

| Human Resource Management | ||

| Supply Chain Management | ||

| Reporting and Analytics | ||

| Other Components | ||

| By Retail Format | Supermarkets and Hypermarkets | |

| Specialty Stores | ||

| Department Stores | ||

| Convenience Stores | ||

| E-Commerce and Omnichannel Retailers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the retail enterprise resource planning market in 2026?

The sector stands at USD 7.98 billion in 2026 and is on track to reach USD 13.01 billion by 2031.

Which deployment model is gaining share the fastest?

Hybrid architectures are growing at a 9.4% CAGR because they balance data-residency compliance with cloud scalability.

Why are SMEs adopting ERP platforms more rapidly than large chains?

Subscription pricing removes six-figure license fees and pre-configured workflows cut project timelines to under 90 days, making ERP attainable for smaller retailers.

Which component category shows the highest growth over the forecast?

Reporting and analytics modules rise at an 11.5% CAGR as merchants embed machine learning to fine-tune demand forecasts and pricing.

What geographic region leads future growth?

Asia-Pacific leads with a 12.0% CAGR due to mandatory e-invoicing and rapid mobile-commerce expansion.

What is the main barrier to ERP adoption mentioned by retailers?

High implementation costs and frequent budget overruns remain the top hurdle, with 72% of projects exceeding initial estimates.

Page last updated on: