E-commerce ERP Integration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.21 Billion |

| Market Size (2031) | USD 21.31 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

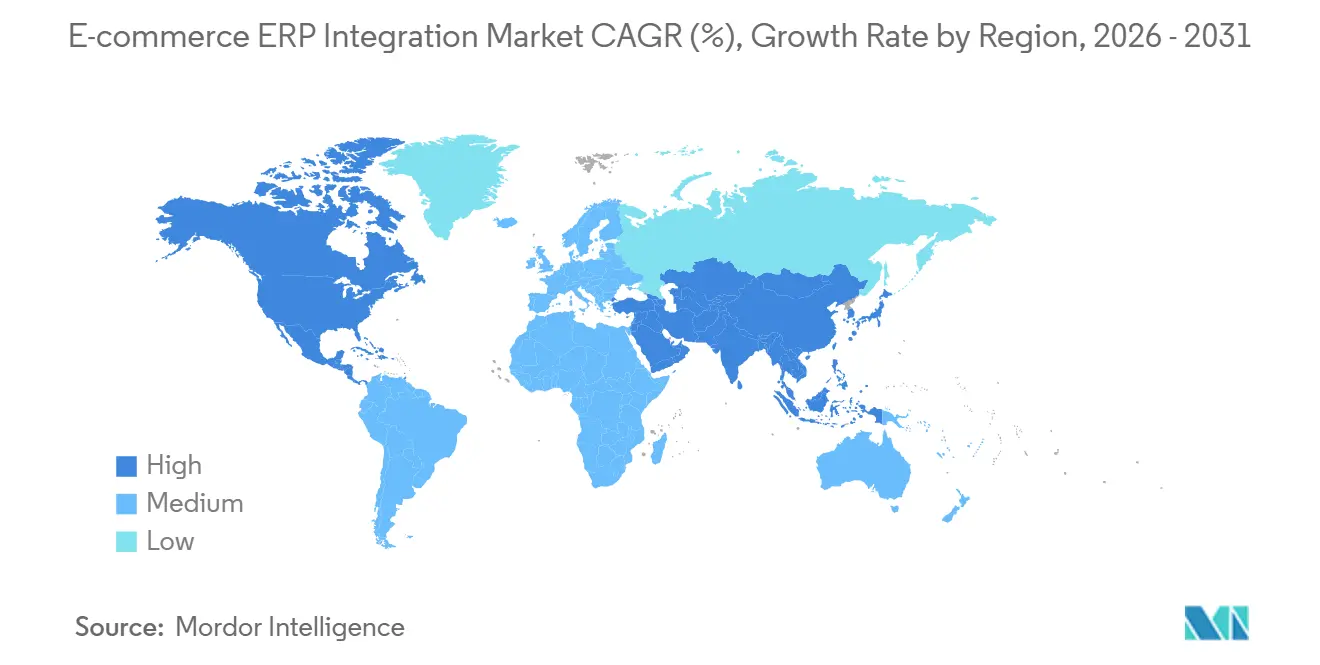

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

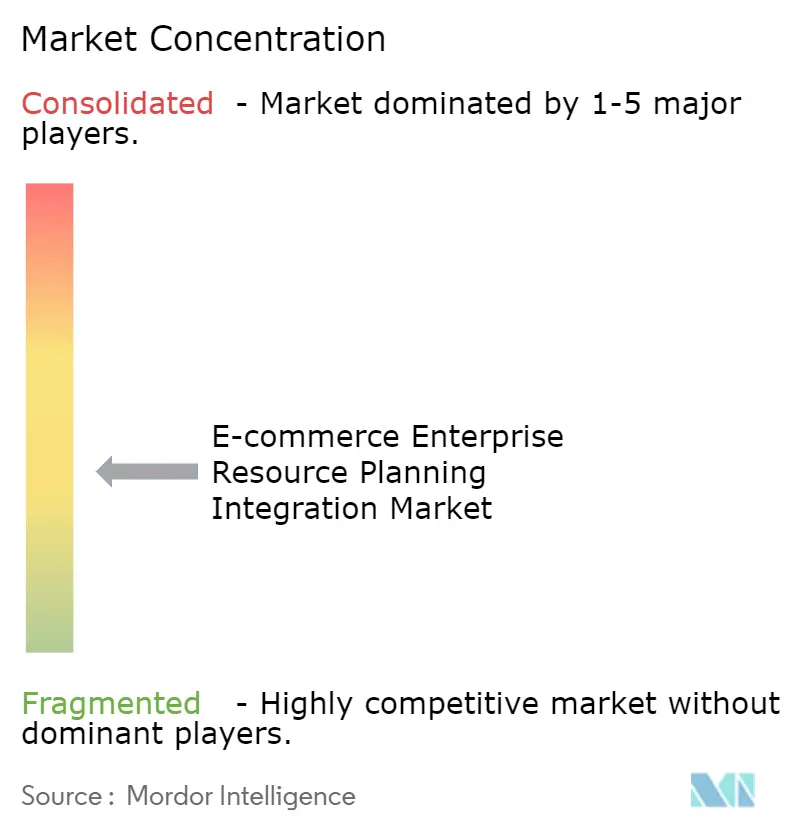

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-commerce ERP Integration Market Analysis by Mordor Intelligence

The E-commerce enterprise resource planning integration market size is projected to expand from USD 14.21 billion in 2025 and USD 15.21 billion in 2026 to USD 21.31 billion by 2031, registering a CAGR of 6.98% between 2026 and 2031. Rising omnichannel retail expectations, real-time tax-compliant invoicing, and the shift toward composable digital commerce are reshaping integration from a back-office IT task into a board-level priority. Mandatory e-invoicing rules across the European Union and India, the rapid spread of headless commerce storefronts, and mounting service-level penalties on global marketplaces are driving retailers to seek low-latency middleware capable of orchestrating thousands of API calls per second. Cloud deployments dominate as subscription economics align integration spending with transaction peaks, while low-code iPaaS tools democratize connectivity for resource-constrained teams. Competitive intensity stems from vendors that bundle integration with ERP suites and from specialists that differentiate through pre-built connectors for niche applications.

Key Report Takeaways

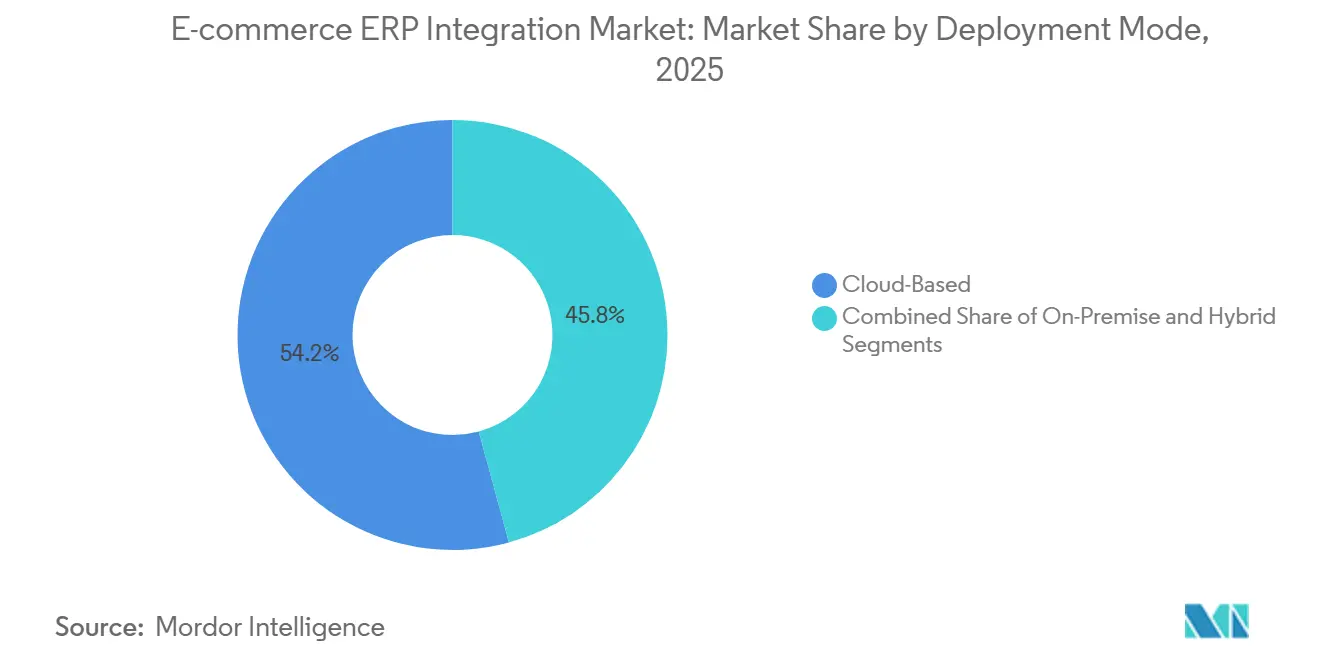

- By deployment mode, cloud-based solutions captured 54.23% of the market share in 2025, whereas hybrid architectures are forecast to grow at a 7.58% CAGR through 2031.

- By organization size, small and medium enterprises accounted for 62.14% of the E-commerce enterprise resource planning integration market in 2025, while both SMEs and large enterprises are expected to grow at a 7.38% CAGR through 2031.

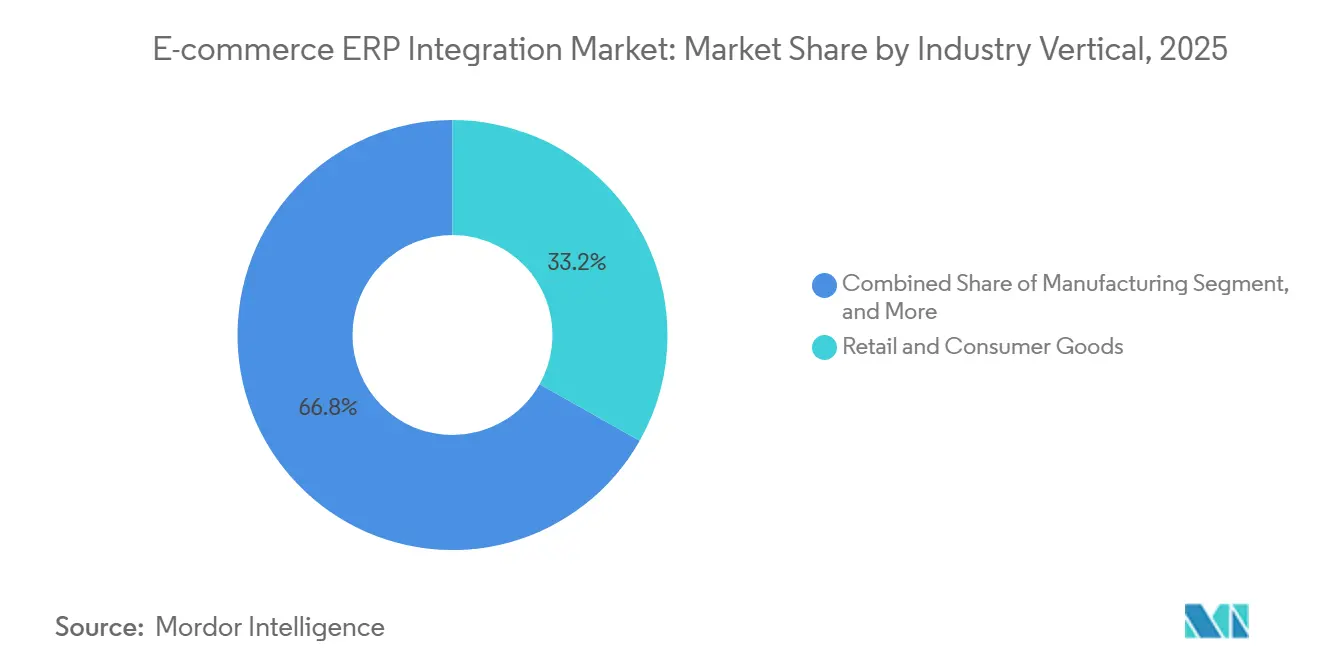

- By industry vertical, retail and consumer goods led with 33.18% revenue share in 2025; healthcare is poised to expand at a 7.98% CAGR during the forecast period.

- By integration approach, API integration retained 46.49% of the 2025 revenue base, while iPaaS is the fastest-growing approach, with a 7.78% CAGR to 2031 in the e-commerce ERP integration market.

- Asia-Pacific accounted for 29.37% of global revenue in 2025, while Africa is the fastest-growing region, with a 7.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global E-commerce ERP Integration Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Headless Commerce Architectures | +1.4% | North America and Europe, early APAC cities | Medium term (2-4 years) |

| Rising Adoption of SaaS-Based ERP Suites Among Mid-Market Retailers | +1.3% | Global, strongest in North America and Western Europe | Short term (≤ 2 years) |

| Mandatory E-Invoicing and Taxation Compliance Integrations | +1.2% | Europe, India, Brazil, spillover to Middle East and Africa | Short term (≤ 2 years) |

| Growth of Omnichannel Retail Requiring Unified Inventory Visibility | +1.1% | Global, high intensity in North America, Europe, APAC | Medium term (2-4 years) |

| Surge in Marketplace Sellers Integrating ERP to Meet SLA Penalties | +0.9% | Core APAC with expansion to South America and Africa | Short term (≤ 2 years) |

| Low-Code iPaaS Platforms Lowering Integration Complexity and Cost | +0.8% | Global, fastest in mid-market segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Headless Commerce Architectures

Headless commerce decouples the storefront from back-end logic, allowing brands to deploy multiple touchpoints, such as web, voice, and IoT interfaces, simultaneously. This architecture significantly increases the number of API endpoints, requiring middleware to handle three to five times as many calls per transaction as traditional monolithic platforms. Retailers adopting headless frameworks often prefer Integration Platform as a Service (iPaaS) solutions that include certified connectors for platforms such as Shopify Plus, BigCommerce, and others. The increased volume of API calls introduces data-consistency challenges, particularly when discrepancies arise in cart contents or delivery estimates across different channels. To address these issues, integration vendors are incorporating real-time monitoring capabilities and adopting outcome-based pricing models that align with transaction throughput, ensuring seamless operations and improved reliability for retailers.

Rising Adoption of SaaS-Based ERP Suites Among Mid-Market Retailers

Mid-market merchants are increasingly transitioning from outdated on-premise Enterprise Resource Planning (ERP) systems to modern cloud-based suites such as SAP S/4HANA Cloud, Oracle NetSuite, and Microsoft Dynamics 365. These cloud solutions offer native commerce connectors that significantly reduce project timelines by enabling retailers to synchronize orders across various web stores and marketplaces in a matter of weeks rather than months. By shifting infrastructure costs to vendors, these solutions also help businesses optimize their operational expenses. Additionally, continuous updates provided by these platforms ensure that connector compatibility is maintained over time. However, the multi-tenant nature of cloud deployments introduces data residency and compliance challenges, particularly for businesses operating in regions with stringent data protection regulations. This has led to a growing demand for region-specific deployment options that address these compliance concerns while maintaining the efficiency and scalability of cloud-based ERP systems.

Mandatory E-Invoicing and Taxation Compliance Integrations

Real-time electronic invoicing has become mandatory across several jurisdictions, requiring ERP systems to interface directly with national clearance platforms before transactions can be finalized. For instance, the European Union’s ViDA initiative aims to standardize, and authorities approved a mandate that will gradually roll out until 2028.[1]European Commission, “Data Protection in the EU,” ec.europa.eu This directive stipulates that all cross-border B2B transactions must pass through a centralized e-invoicing hub and streamline VAT reporting across member states, while India’s expanded Goods and Services Tax Network enforces compliance through electronic invoice validation. Retailers operating in these regions must integrate multi-jurisdictional tax logic into their order-to-cash workflows to ensure compliance. Failure to do so can result in invoice rejections, penalties, and even marketplace listing suspensions. This regulatory environment has elevated integration from a mere operational necessity to a critical compliance requirement, compelling businesses to prioritize robust, adaptable ERP solutions.

Growth of Omnichannel Retail Requiring Unified Inventory Visibility

Buy online, pick up in store, ship from store, and same-day delivery models rely heavily on maintaining a single, accurate source of inventory truth. To achieve this, integration platforms play a critical role by aggregating data from various systems, including warehouse management systems, point-of-sale (POS) systems, and e-commerce platforms. These platforms ensure that inventory changes are propagated within seconds, preventing overselling or stock discrepancies. As a result, event-driven architectures are increasingly replacing traditional nightly batch jobs, offering real-time updates and improved operational efficiency. Additionally, vendors are now enhancing their offerings by pairing connectivity solutions with advanced data-quality tools. These tools help reconcile product catalogs, pricing hierarchies, and other critical data across multiple channels, ensuring consistency and accuracy in omnichannel retail operations.

Restraint Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy On-Premise ERP Customizations Hindering Standardized Connectors | -1.1% | Global, with highest impact in North America and Europe where legacy systems are entrenched | Long term (≥ 4 years) |

| Data Security and Compliance Concerns Around Cross-Border Flows | -0.9% | Europe, China, Russia, with emerging restrictions in Africa and Middle East | Medium term (2-4 years) |

| High TCO for Complex Multi-Site Rollouts in Emerging Markets | -0.7% | Africa, South America, Southeast Asia, with infrastructure constraints amplifying costs | Long term (≥ 4 years) |

| Shortage of Skilled Integration Architects and Middleware Developers | -0.6% | Global, with acute shortages in APAC and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy On-Premise ERP Customizations Hindering Standardized Connectors

Years of bespoke code in on-premise ERP landscapes create brittle and highly customized data models that off-the-shelf connectors cannot easily accommodate. Retailers often face significant challenges and incur substantial consulting fees to map these custom fields, workflows, and processes to normalized schemas required for modern systems. This complexity frequently delays cloud migration projects by an estimated 6 to 12 months, as businesses work to ensure compatibility and minimize disruptions. The difficulty is further compounded when multiple ERP instances are deployed across different regions, requiring integration platforms to maintain and manage parallel connectors for what ideally should function as a unified system. These challenges highlight the critical need for robust planning and execution strategies to streamline the migration process and ensure operational continuity.

Data Security and Compliance Concerns Around Cross-Border Flows

Regulations like GDPR and China’s Personal Information Protection Law restrict where and how customer information may travel. Even seemingly benign metadata can be deemed personal data, forcing retailers to implement field-level encryption, tokenization, and geo-fenced routing within integration workflows. Hybrid topologies that keep identifiers in-country while sending transactional data to cloud hubs add latency and complexity, particularly for mid-market firms with limited infrastructure budgets. The WTO and OECD emphasize the need for harmonized data transfer frameworks to reduce frictions. However, progress remains slow as geopolitical tensions drive divergence instead of convergence.[2]WTO and OECD, “Handbook on Measuring Digital Trade,” wto.orgRetailers operating across multiple markets are adopting data residency-aware integration platforms to dynamically route data based on customer location. Yet, these capabilities are still emerging and are priced at a premium, limiting adoption to large enterprises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Amid Hybrid Resurgence

Cloud-based solutions accounted for 54.23% of 2025 revenue as retailers gravitated toward elastic scaling during holiday peaks and avoided hardware refresh cycles. The hybrid approach is forecast to rise at a 7.58% CAGR, balancing on-premise control for sensitive finance modules with cloud speed for customer-facing commerce services. The E-commerce enterprise resource planning integration market size for hybrid deployments is projected to widen as edge runtimes in stores support local order processing and later synchronize with central ERPs, mitigating connectivity outages. Second-generation hybrid platforms route data dynamically based on real-time latency and compliance thresholds, integrating edge devices, private clouds, and public SaaS endpoints in a single policy domain.

Organizations still running fully on-premises middleware cite data sovereignty rules and long depreciation cycles for existing servers. Yet, rising maintenance costs and limited talent pools accelerate the pivot toward managed services. Vendors now bundle continuous security updates, micro-segmented network controls, and AI-driven anomaly detection to ease the transition. These value-adds, combined with subscription pricing, make cloud and hybrid offerings increasingly attractive, especially for merchants operating across multiple tax regimes and payment ecosystems.

By Organization Size: SME Momentum Reshapes Vendor Strategies

SMEs accounted for 62.14% of 2025 revenue, underscoring how low-code iPaaS subscriptions starting at USD 300 per month unlock enterprise-grade capabilities for smaller budgets. Template libraries compress deployment to as little as 6 weeks, enabling rapid pivots to new sales channels and fulfillment partners. Larger retailers, while fewer in number, drive high-value custom projects that fuse omnichannel orchestration with proprietary pricing algorithms. Both cohorts, however, pursue a bimodal strategy: pre-built connectors for commodity processes and bespoke coding for differentiating workflows.

The vendor landscape mirrors this dichotomy. Pure-play iPaaS firms add enterprise governance modules, role-based access, versioned API gateways, and SOC 2 attestations to penetrate the upper tier, while traditional middleware suites introduce drag-and-drop designers to defend mid-market share. These converging roadmaps reduce technology gaps, making pricing, support, and vertical expertise the main buying criteria. Consequently, the market continues to broaden its appeal across company sizes without sacrificing depth for complex rollouts.

By Industry Vertical: Healthcare Acceleration Signals Broader Digitization

Retail and consumer goods retained a 33.18% share in 2025 as fashion, grocery, and electronics brands embed real-time ERP synchronization into baseline commerce operations. Healthcare, however, is the fastest-growing vertical at a 7.98% CAGR. Providers integrate e-commerce storefronts for medical devices and telehealth with legacy billing systems that require HIPAA-compliant audit trails, driving demand for specialized connectors. The E-commerce enterprise resource planning integration market share in healthcare is expected to grow as prescription fulfillment workflows converge with patient record systems, enabling seamless insurance verification and regulatory reporting.

Manufacturers and logistics companies deploy integration platforms to support build-to-order models and dynamic shipping orchestration. Financial services, education, and hospitality adopt ERP integrations for subscription billing, online enrollment, and property management. This cross-industry convergence pushes vendors to supply horizontal capabilities such as usage-based billing engines and customer data platforms configurable for multiple domains, nudging the market toward modular, metadata-driven architectures rather than siloed vertical stacks.

By Integration Approach: iPaaS Gains Ground on API Incumbents

Direct API integration accounted for 46.49% of 2025 revenue, favored for latency-sensitive inventory adjustments that must post within seconds. Yet maintaining dozens of individual endpoints scales poorly; enterprises now average 47 active integrations, spotlighting orchestration complexity. iPaaS, therefore, grows at a 7.78% CAGR, offering centralized monitoring, transformation, and event triggers critical to composable commerce. The E-commerce enterprise resource planning integration market size for iPaaS solutions is forecast to outpace traditional middleware as AI-assisted mapping and automated error resolution lower the total cost of ownership.

Legacy ESB patterns endure in firms with established service-oriented architectures, particularly where message governance remains paramount. Custom coding persists for unique value-add processes such as proprietary discount engines or warehouse robotics. Nonetheless, vendors increasingly expose SDKs. For instance, in 2025, SAP highlighted that its Integration Suite enables customers to start with standard templates and customize them as needed, all within the platform.[3]SAP, “SAP Integration Suite,” sap.com This is made possible through both pre-built connectors and custom adapters developed using SAP's SDK, so bespoke adapters extend rather than replace platform components, ensuring that even edge-case logic benefits from shared security, logging, and scaling layers.

Geography Analysis

Asia-Pacific accounted for 29.37% of global revenue in 2025, driven by digital-first consumers in China, India, and Southeast Asia who expect uninterrupted commerce across super-apps, chat, and social video. Local payment rails like India’s Unified Payments Interface process billions of monthly transactions, requiring ERP connectors that reconcile micro-payments in near real time. Africa, expanding its market, relies on mobile money systems such as M-Pesa, prompting vendors to build adapters for USSD-based confirmations and offline synchronization when cellular coverage lapses.

North America and Europe generate the largest absolute spend. Retailers are moving beyond order synchronization to advanced use cases such as real-time carbon footprint tracking and AI-driven delivery routing. The European Union’s phased ViDA mandate accelerates investment in tax-compliant invoice data bridges, while U.S. merchants integrate state-level sales tax engines alongside Buy Now Pay Later services. Middle Eastern economies, especially Saudi Arabia and the United Arab Emirates, channel public funds into omnichannel infrastructure, demanding connectors that blend local gateways with global logistics APIs.

Geography-specific data privacy laws fragment architecture choices. . The EU-US Data Privacy Framework, enacted in 2023, legitimizes transatlantic data transfers. However, ongoing legal challenges cast doubt on its longevity. As a precaution, retailers are crafting hybrid architectures, ready to shift to on-premise processing should the framework face invalidation.[4] European Commission, “EU-US Data Transfers,” ec.europa.eu China’s localization rules compel in-country ERP hosting, Europe enforces rigorous consent tracking under GDPR, and Russia mandates domestic data storage. Integration platforms answer with location-aware routing that respects residency without compromising performance. Emerging markets also push for offline-first runtimes capable of queuing transactions at the edge, an area where only a few vendors currently excel, signaling untapped growth opportunities.

Competitive Landscape

The E-commerce ERP integration market is moderately fragmented: the top ten vendors accounted for about 45% of 2025 revenue, while numerous niche specialists address regional and vertical gaps. ERP incumbents such as SAP, Oracle, and Microsoft bundle integration suites into broader cloud subscriptions, leveraging existing relationships. Pure-play iPaaS providers, Celigo, Boomi, and MuleSoft, compete on out-of-the-box connectors, low-code design, and consumption-based pricing that resonates with SMEs. Emerging challengers introduce AI-generated data mapping, incident prediction, and auto-documentation to reduce reliance on scarce integration architects.

White-space remains in vertical-specific compliance, notably healthcare, where HL7 FHIR and HIPAA dictate stringent workflows. Vendors with certified healthcare pipelines command premium pricing. Geographical expansion in Africa and parts of Southeast Asia also presents upside, contingent on runtimes that support offline use and mobile money. Security certifications such as ISO 27001 and SOC 2 have become procurement prerequisites, rendering them table stakes rather than differentiators.

Strategic moves underline market dynamism. Microsoft extended Azure Integration Services with connectors for emerging social commerce channels in February 2026. SAP teamed with Alibaba Cloud in January 2026 to launch localized adapters for Tmall and Taobao that honor Chinese data-residency laws. Oracle’s November 2025 acquisition of a healthcare interoperability specialist added HIPAA-ready pipelines, while Workato, Boomi, IBM, and Celigo each invested in template libraries, AI tooling, or partner ecosystems to compress time-to-value and broaden reach.

E-commerce ERP Integration Industry Leaders

Celigo, Inc.

MuleSoft, Inc.

Workato, Inc.

SAP SE

Boomi, LP.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Microsoft expanded Azure Integration Services with Shopify Markets Pro and TikTok Shop connectors.

- January 2026: SAP partnered with Alibaba Cloud to deliver localized integration services for Chinese retailers.

- November 2025: Oracle acquired a middleware firm specializing in healthcare interoperability.

- October 2025: Workato launched an out-of-the-box retail integration solution with AI-powered data mapping.

- September 2025: Boomi invested USD 50 million in co-developing vertical connectors with independent software vendors.

Global E-commerce ERP Integration Market Report Scope

The market refers to the market for solutions that enable seamless integration between enterprise resource planning (ERP) systems and e-commerce platforms. These integrations streamline operations, including inventory management, order processing, customer data synchronization, and financial reporting, enhancing efficiency and accuracy across business processes.

The E-commerce Enterprise Resource Planning Integration Market Report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Retail and Consumer Goods, Manufacturing, Healthcare, Logistics and Transportation, and Other Industry Verticals), Integration Approach (API Integration, Middleware / ESB, Custom / Bespoke Integration, and Integration Platform as a Service), and Geography (North America, South America, Europe, Asia Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Retail and Consumer Goods |

| Manufacturing |

| Healthcare |

| Logisitcs and Transportation |

| Other Industry Verticals |

| API Integration |

| Middleware / ESB |

| Custom / Bespoke Integration |

| Integration Platform as a Service (iPaaS) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Industry Vertical | Retail and Consumer Goods | ||

| Manufacturing | |||

| Healthcare | |||

| Logisitcs and Transportation | |||

| Other Industry Verticals | |||

| By Integration Approach | API Integration | ||

| Middleware / ESB | |||

| Custom / Bespoke Integration | |||

| Integration Platform as a Service (iPaaS) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the E-commerce enterprise resource planning integration market be by 2031?

It is projected to reach USD 21.31 billion by 2031 at a 6.98% CAGR over 2026-2031.

Which deployment model is growing fastest in E-commerce enterprise resource planning integration?

Hybrid deployments are forecast to grow at a 7.58% CAGR as firms balance cloud agility with on-premise control.

Why is healthcare adoption accelerating?

Healthcare shows a 7.98% CAGR because providers must link e-commerce portals with legacy billing and comply with HIPAA audit requirements.

What challenges arise from legacy enterprise resource planning customizations?

Extensive custom code hinders use of standard connectors, inflates consulting costs, and can delay cloud migrations by up to a year.

How do data-localization laws influence integration strategy?

Regulations in the EU, China, and Russia compel geo-fenced data routing, often leading retailers to adopt hybrid or in-country deployments.

Which regions present the highest growth opportunities?

Africa and Southeast Asia, driven by mobile-first commerce and the need for offline-capable, low-code integration tools.

Page last updated on: