Resins In Paints And Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 40.76 Billion |

| Market Size (2031) | USD 51.65 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

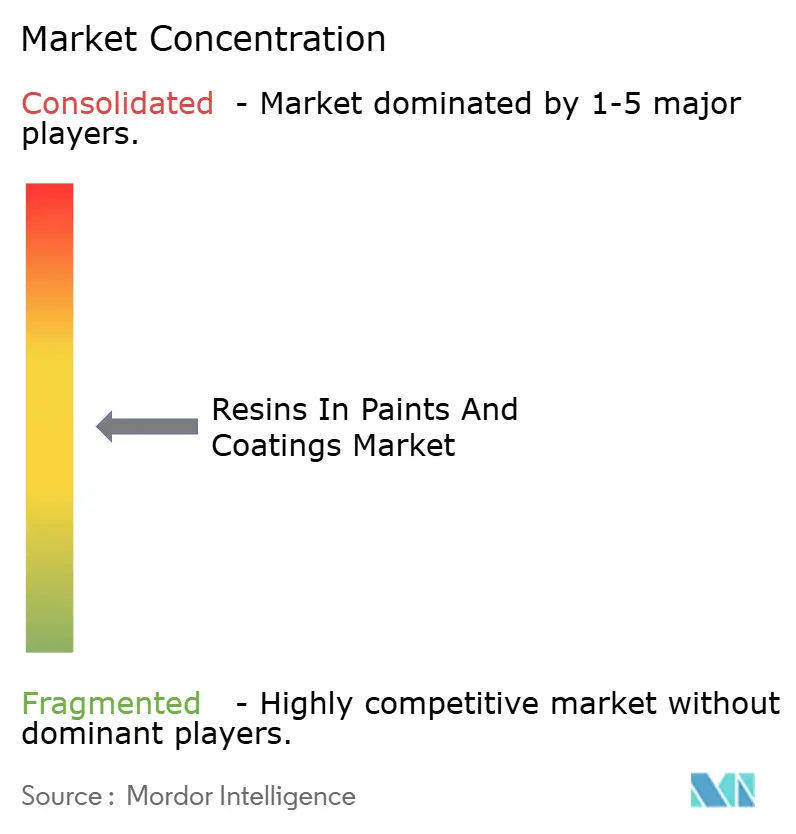

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Resins In Paints And Coatings Market Analysis by Mordor Intelligence

The Resins In Paints And Coatings Market size is expected to grow from USD 38.89 billion in 2025 to USD 40.76 billion in 2026 and is forecast to reach USD 51.65 billion by 2031 at 4.85% CAGR over 2026-2031. Demand pivots toward water-based acrylic and low-bake polyurethane chemistries as regulators tighten VOC ceilings across 40 national jurisdictions, while infrastructure programs in Asia-Pacific, the Middle-East, and North America channel stimulus dollars into corrosion-control and refurbishment coatings. Automotive OEM electrification reinforces the shift, because battery packs restrict oven temperatures and force clearcoat innovations that lower energy consumption and cycle times. Resin producers respond by scaling emulsion polymerization and bio-based epoxy capacity, although petrochemical feedstock volatility and the migration to powder-only finishing lines compress margins and challenge legacy alkyd assets. Patent activity around lignin-derived epoxies and cardanol-based polyols underscores a strategic realignment toward renewable feedstocks that satisfy emerging carbon-disclosure mandates.

Key Report Takeaways

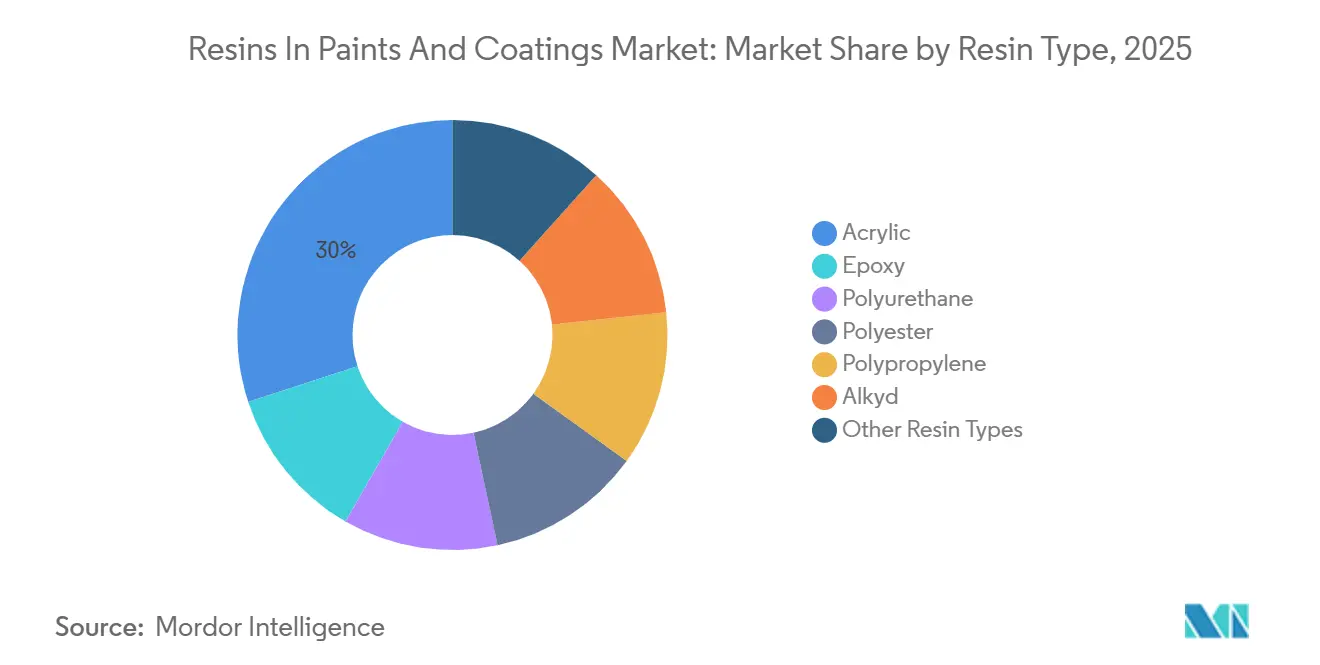

- By resin type, acrylic captured 30.05% of resins in paints and coatings market share in 2025, and this segment is forecast to post a 5.30% CAGR through 2031.

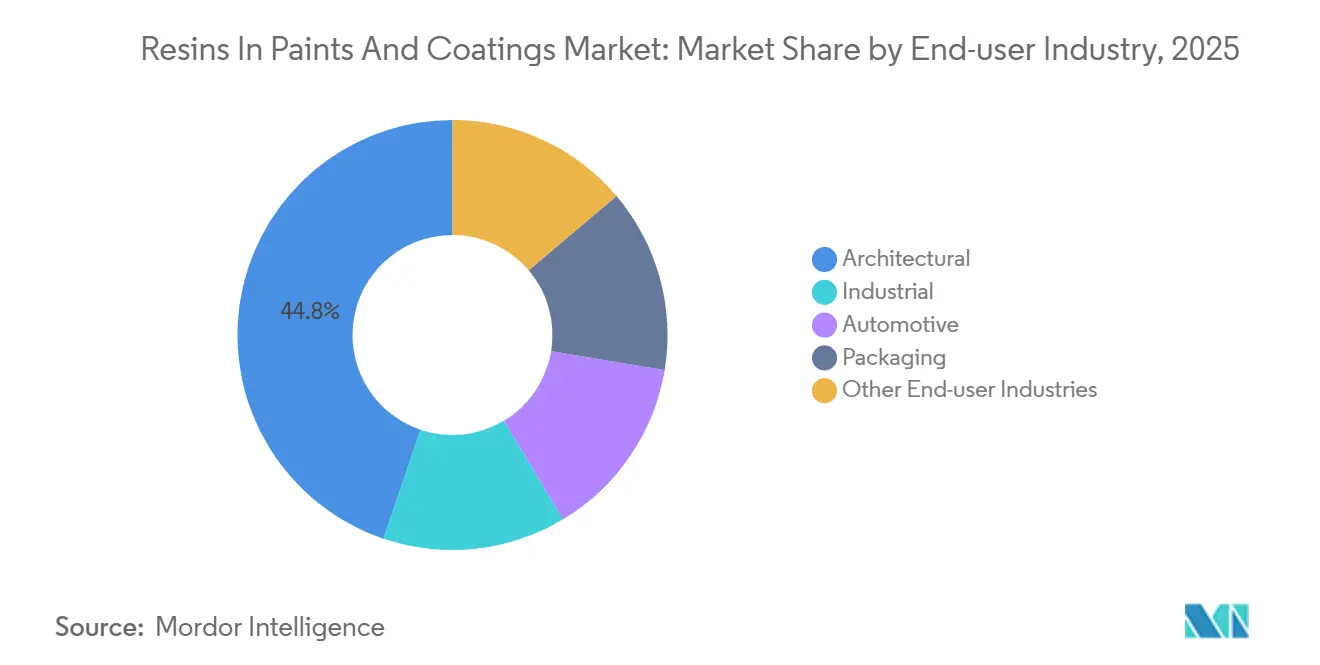

- By end-user industry, architectural accounted for 44.80% of the resins in paints and coatings market share in 2025 and is projected to expand at a 5.05% CAGR through 2031.

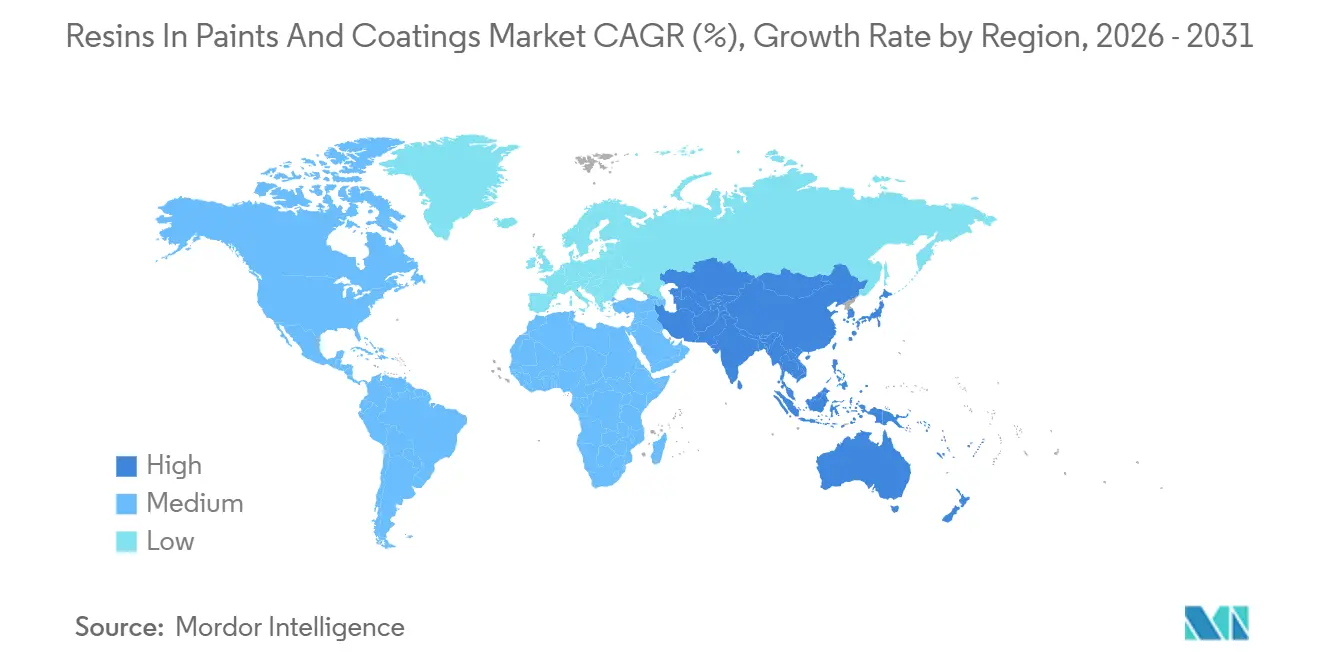

- By geography, the Asia-Pacific region captured 44.15% of the resins in paints and coatings market share in 2025 and is projected to expand at a 5.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Resins In Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction boom across Asia-Pacific | +1.2% | APAC core, spillover to Middle-East | Medium term (2-4 years) |

| Growing demand from automotive industry | +0.9% | Global, concentrated in East Asia and North America | Short term (≤ 2 years) |

| Refurbishment wave in Middle-East and Africa housing | +0.6% | Middle-East and Africa, secondary impact in South Asia | Medium term (2-4 years) |

| Growing demand for on-site 3D printing repair resins | +0.4% | North America and EU industrial clusters | Long term (≥ 4 years) |

| Increasing bio-based epoxy scale-up incentives | +0.7% | EU core, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Boom Across Asia-Pacific

Infrastructure programs in China, India, and ASEAN nations convert raw resin demand into multi-year contracts for waterborne acrylic and hybrid polyurethane systems. China’s 2025 mandate requiring low-VOC interior coatings in public buildings above 10,000 m² eliminated solvent-based alkyd primers from the commercial segment[1]Ministry of Housing and Urban-Rural Development, “Low-VOC Coating Directive,” mohurd.gov.cn . India’s plan to build 1,000 km of new metro track by 2027 specifies high-solids epoxy linings that resist monsoon moisture. Logistics-warehouse construction tied to e-commerce fulfillment in Vietnam and Indonesia embeds acrylic or methyl methacrylate polymers in polymer-concrete flooring, compressing cure times and downtime. Demand volatility remains high; a 10% dip in Chinese residential starts could strip roughly 150,000 t of annual acrylic volume, reinforcing the need for agile emulsion capacity.

Growing Demand from Automotive Industry

Battery-electric vehicle lines cap oven bake temperatures at 120 °C, replacing traditional 140-160 °C alkyd systems with 2-component polyurethane or acrylic-melamine clearcoats that rely on new catalyst packages. Hyundai’s USD 45 million e-coat upgrade in Ulsan finished in late 2025, adopting low-cure cathodic epoxies that perform at 110 °C. UV-curable acrylic resins increasingly coat plastic exterior parts, removing oven energy entirely. Dual-track demand forces suppliers to maintain alkyd assets for internal-combustion platforms while investing in acrylic and polyurethane emulsions for EVs, complicating capital allocation.

Refurbishment Wave in Middle-East and Africa Housing

Saudi Arabia’s Vision 2030 housing program earmarked SAR 12 billion (USD 3.2 billion) in 2025 for repainting projects that stipulate low-VOC acrylic emulsions. Dubai Municipality insists on chloride-resistant acrylic or silicone-modified resins for coastal zones. Egypt’s Cairo and Alexandria upgrades prioritize styrene-acrylic exterior masonry coatings. These projects demand rapid-drying, low-odor formulations packaged in smaller pails, spurring regional resin toll-blending. Temperature swings from 45 °C midday highs to 15 °C nights favor acrylic films with minimal stress cracking.

Growing Demand for On-Site 3D Printing Repair Resins

Portable 3D printers extrude UV-curable epoxies and acrylics that bond to pipelines and offshore structures in minutes, bypassing spray-application logistics. Dow’s 2025 patent (US 11,234,567) details a thixotropic epoxy enabling vertical surface printing. Offshore wind projects value these repairs because helicopter visits cost USD 10,000 each. While annual resin volume may remain below 5,000 t by 2031, the model signals a decentralized supply chain with on-demand resin synthesis. Certification hurdles by the American Petroleum Institute temper near-term uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock price volatility | -0.8% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Shift toward powder-only systems | -0.5% | North America and EU industrial segments | Medium term (2-4 years) |

| Free monomer exposure limits tightening | -0.6% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility

Benzene averaged USD 820 t⁻¹ in Q1 2025, spiked 25% after cracker outages, and fell back to USD 840 t⁻¹ by Q4, eroding margins for styrene-acrylic and unsaturated polyester producers. Propylene’s decoupling from crude oil following new PDH units adds forecasting uncertainty. Resin makers without naphtha hedges delay expansions when price-band risk exceeds 15%, tightening supply and amplifying cyclical swings. Bio-feedstocks provide partial insulation but remain volume-constrained.

Free Monomer Exposure Limits Tightening

The U.S. EPA’s proposed 50 ppm residual styrene cap for interior paints forces vacuum-steam stripping that adds USD 80-120 t⁻¹ to styrene-acrylic costs[2].U.S. Environmental Protection Agency, “Proposed Styrene Residual Limit,” epa.gov ECHA’s January 2026 restriction on methyl methacrylate below 100 ppm compels longer polymerization runs in EU acrylic plants. Small formulators unable to retrofit distillation equipment may exit architectural markets, shifting demand toward waterborne polyurethane dispersions that contain no vinyl monomer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Resins Capture Architectural and Automotive Share

Acrylic resins held 30.05% of resins in paints and coatings market share in 2025 and are projected to advance at a 5.30% CAGR through 2031, outperforming epoxy and polyurethane segments. Demand originates from interior wall paints that now dominate residential repaint cycles and from EV basecoats requiring low-bake performance. Epoxy maintains a premium niche in chemical-resistant marine applications, yet powder-coating substitution trims its liquid volume. Polyurethane bifurcates into 2-component systems for aerospace composites and single-component waterborne dispersions for cabinetry, preserving price premiums.

Polyester’s role in powder lines secures metal-finishing growth, while alkyd demand retrenches in high-VOC markets. Specialty silicone-modified acrylics and fluoropolymers command margins that attract R&D funding. Continuous emulsion polymerization coupled with machine-learning process control underscores why acrylic R&D filings at the 2025 European Coatings Show outnumbered rival chemistries four-to-one.

By End-user Industry: Architectural Lead, Industrial Segment Fragments

Architectural consumed 44.80% of resins in paints and coatings market share in 2025 and will grow at a 5.05% CAGR to 2031, anchored in Asia-Pacific housing and Middle-East refurbishment grants. Industrial fragment under bespoke substrate requirements, limiting plant utilization and inflating batch-changeover costs.

Automotive OEMs purchase high-value resins—polyurethane clearcoats and acrylic-melamine basecoats—with an average resin intensity 40% above other segments, yet global vehicle output plateau tempers volumetric growth. Packaging coatings rely on polypropylene-based or BPA-free epoxy alternatives to satisfy FDA and EU migration ceilings, providing a regulatory moat. Wood coatings and coil-coatings constitute a resilient sub-segment as renovation booms and appliance output rise, albeit at lower scale.

Geography Analysis

Asia-Pacific generated 44.15% of 2025 revenue and is projected to post the fastest 5.36% CAGR through 2031. China’s urban-migration target of 70% by 2030 sustains interior repaint cycles, while India’s highway and metro projects elevate epoxy and polyurethane demand for steel and concrete protection. Japanese and South Korean OEMs realign to EV coating requirements, sourcing low-bake resins that cut electricity use 20%. ASEAN’s electronics expansion necessitates durable coatings for device enclosures, drawing imports of acrylic and polyester intermediates. Currency swings and import reliance for benzene challenge profitability across the region.

North America is buoyed by the U.S. Infrastructure Investment and Jobs Act, which funds USD 110 billion of road and bridge work through 2026. Traffic-marking and bridge-deck overlays lean on fast-cure acrylic and epoxy chemistries. Canada tightens building codes to enforce low-VOC interiors, further shifting away from solvent alkyds. Mexican automotive clusters apply high-solids polyurethanes but trim paint usage per vehicle as manufacturers adopt thinner coat architectures.

Europe is shaped by renovation grants and stringent chemical policy. Germany’s EUR 5 billion retrofit fund in 2025 underwrote facade coatings with silicone-modified acrylics that limit algae growth. France and Italy stipulate renewable-content thresholds, accelerating lignin-based epoxy trials in public projects. The European Chemicals Agency’s 2027 microplastics ban will necessitate reformulation of certain acrylic copolymers, signaling capex needs. South America and Middle-East and Africa demand is also accelerating because Brazil, Saudi Arabia, and Egypt bankroll housing upgrades emphasizing durable, low-cost emulsions.

Competitive Landscape

The resins in paints and coatings market exhibits moderate concentration: BASF, Dow, Sherwin-Williams, Arkema, and Allnex jointly hold about 45% of global capacity, yet regional formulators in ASEAN and the Gulf retain local architectural share via agile color-matching and short lead times. BASF’s 2025 annual report cites a 12% sales increase in acrylic emulsions driven by Indian and Southeast Asian housing. Dow’s 47 active patents for low-temperature-cure polyurethane dispersions indicate strategic focus on EV lines.

Machine-learning optimization of emulsion polymerization, carbon-footprint disclosure, and supply-chain traceability differentiate multinationals, while smaller players compete by co-locating blending assets adjacent to paint plants. Specialty entrants exploit white spaces—bio-based hardeners, algae-derived acrylic monomers, on-site 3D-printing resins—leveraging public sustainability mandates. ISO 9001 remains baseline, but customers increasingly award contracts based on audited Scope 3 emissions, pressuring laggards.

Service bundling intensifies: suppliers offer formulation co-development, inventory management, and digital color libraries that reduce mismatch scrap by 30%. Powder-coating resin demand concentrates around BASF, Axalta, and AkzoNobel, shrinking liquidity for independent liquid-resin producers. Yet architectural volume encourages toll-blending partnerships in markets where import duties inflate landed costs.

Resins In Paints And Coatings Industry Leaders

Dow

Arkema

BASF

The Sherwin-Williams Company

Allnex GMBH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Westlake Epoxy and Brenntag announced the strategic expansion of their long-standing distribution partnership to include South and West India. Brenntag will distribute Westlake Epoxy's specialized product portfolio, which includes established brands such as EPON, EPIKOTE, EPIKURE, and EPI-REZ.

- July 2025: Chugoku Marine Paints, Ltd. and Mitsui Chemicals, Inc. launched CMP NOVA 2000 (Bio), a bio-based epoxy resin. It was selected for use on the ballast tanks of a liquefied ammonia tanker and utilized Mitsui Chemicals' bio-based epoxy resin to help reduce CO₂ emissions.

Global Resins In Paints And Coatings Market Report Scope

Resins serve as essential binders in paints and coatings, forming protective and adhesive films that hold pigments together while influencing durability, gloss, and chemical resistance. Major types include acrylics, known for weather resistance; epoxies, valued for corrosion protection; and alkyds, recognized for their gloss and durability. These resins are widely used in industrial, automotive, and architectural applications.

The resins in paints and coatings market is segmented by resin type, end-user industry, and geography. By resin type, the market is segmented into acrylic, epoxy, polyurethane, polyester, polypropylene, alkyd, and other resin types. By end-user industry, the market is segmented into architectural, industrial, automotive, packaging, and other end-user industries. The report also covers the market size and forecasts for resins in paints and coatings in 19 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Acrylic |

| Epoxy |

| Polyurethane |

| Polyester |

| Polypropylene |

| Alkyd |

| Other Resin Types |

| Architectural |

| Industrial |

| Automotive |

| Packaging |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Resin Type | Acrylic | |

| Epoxy | ||

| Polyurethane | ||

| Polyester | ||

| Polypropylene | ||

| Alkyd | ||

| Other Resin Types | ||

| By End-user Industry | Architectural | |

| Industrial | ||

| Automotive | ||

| Packaging | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the resins in paints and coatings market?

The resins in paints and coatings market size stands at USD 40.76 billion in 2026 and is forecast to reach USD 51.65 billion by 2031, expanding at a 4.85% CAGR from 2026.

What geographic region contributes most to future volume growth?

Asia-Pacific represents 44.15% of 2025 revenue and is set to deliver the fastest 5.36% CAGR through 2031, driven by urbanization, infrastructure programs, and EV production.

How are feedstock price swings impacting resin producers?

Benzene, propylene, and ethylene price volatility of 20-25% in 2025 compressed margins for non-integrated producers and delayed expansion plans, trimming near-term supply growth.

Which regulatory trend could force major reformulation in liquid coatings?

Tighter residual monomer caps—50 ppm styrene in the U.S. and 100 ppm methyl methacrylate in the EU—require costly stripping investments or shifts to alternative chemistries such as waterborne polyurethanes.

Page last updated on: