Paper Coating Material Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.4 Billion |

| Growth Rate (2026 - 2031) | 2.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

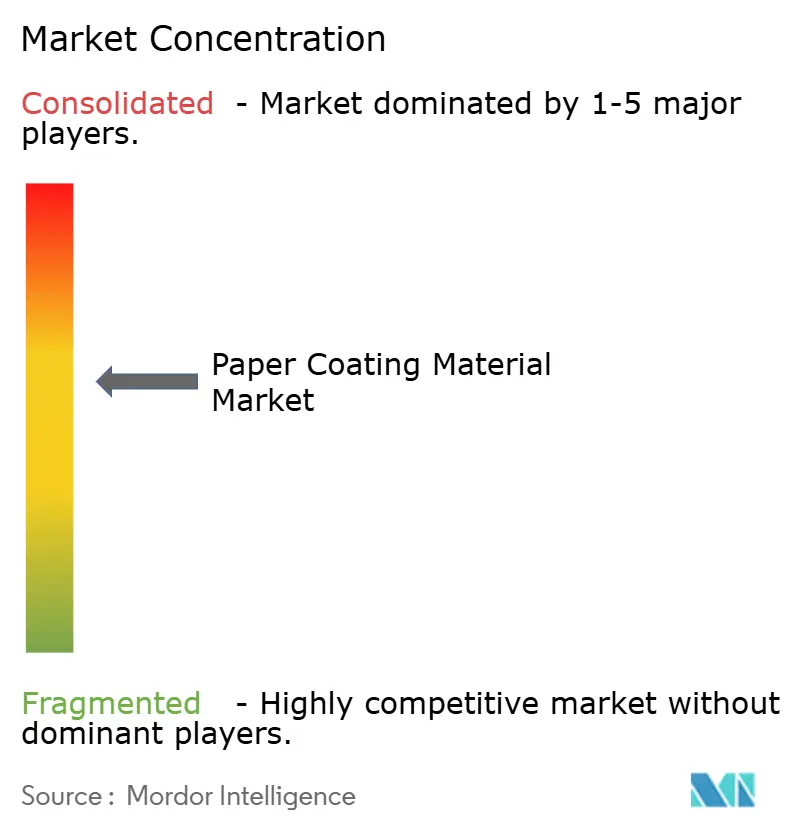

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper Coating Material Market Analysis by Mordor Intelligence

The Paper Coating Material market size is expected to grow from USD 1.23 billion in 2025 to USD 1.26 billion in 2026 and is forecast to reach USD 1.4 billion by 2031 at 2.18% CAGR over 2026-2031. Rising substitution of single-use plastics, rapid e-commerce growth, and sustained investment in barrier-coating capacity collectively anchor the medium-term outlook for the paper coating materials market, even as digital media pressures legacy print volumes. Calcium carbonate’s 42.37% 2024 share secures cost advantages and optical performance that check higher-priced polymer rivals, while polymer coatings post a faster 3.24% CAGR through 2030 on the back of food-grade barrier requirements. Regionally, the Asia-Pacific commands 47.36% of global demand, thanks to China’s 7.2% expansion in coated-paper production in 2024 and India’s packaging boom, which creates economies of scale for raw material suppliers. Ongoing volatility in kaolin, pulp, and latex-binder prices remains the leading cost headwind, yet regulatory tailwinds tied to plastic bans and recycling mandates sustain investment in next-generation sustainable formulations.

Key Report Takeaways

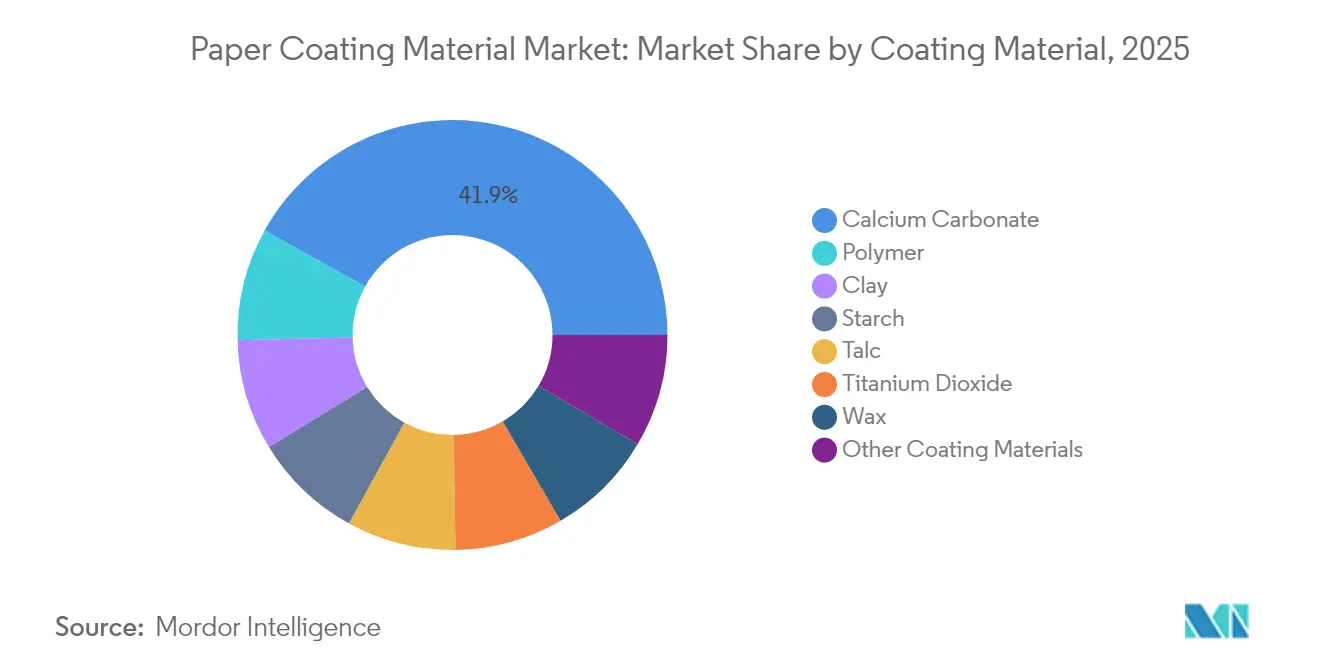

- By coating material, calcium carbonate led with a 41.92% share of the paper coating materials market in 2025, while polymer coatings are projected to expand at a 3.07% CAGR through 2031.

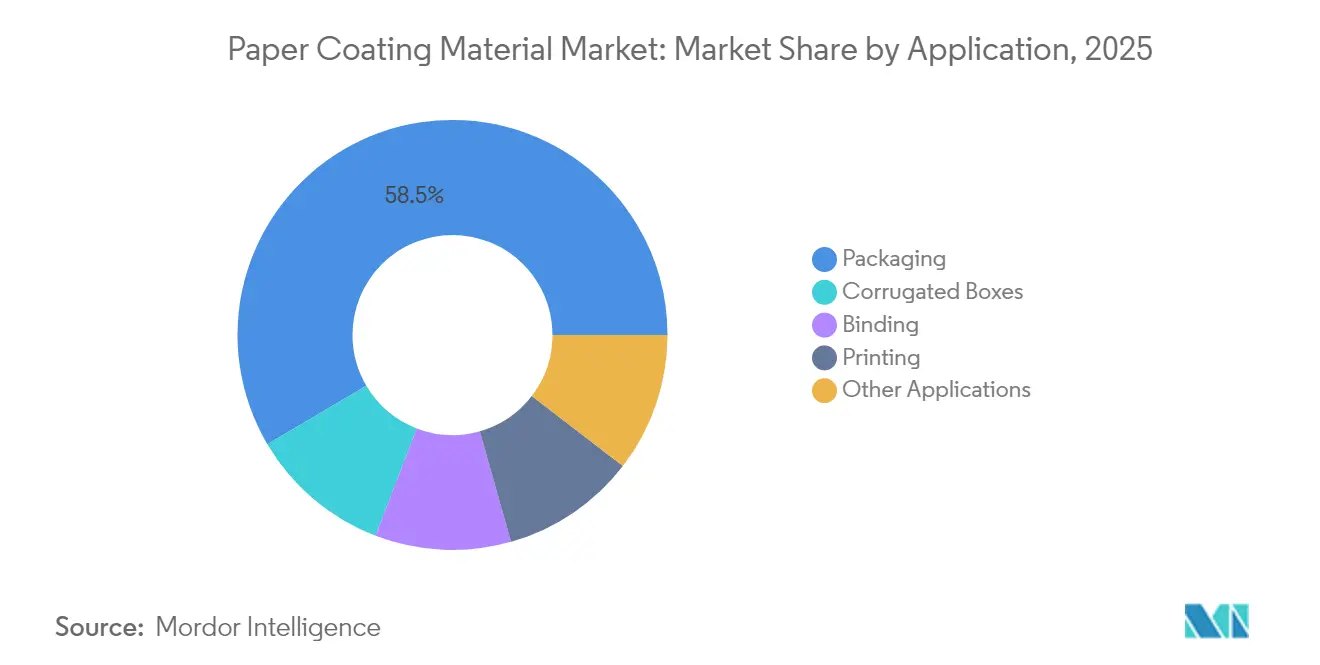

- By application, packaging captured 52.96% of the paper coating materials market size in 2025, and corrugated boxes are forecast to post a 2.97% CAGR between 2026 and 2031.

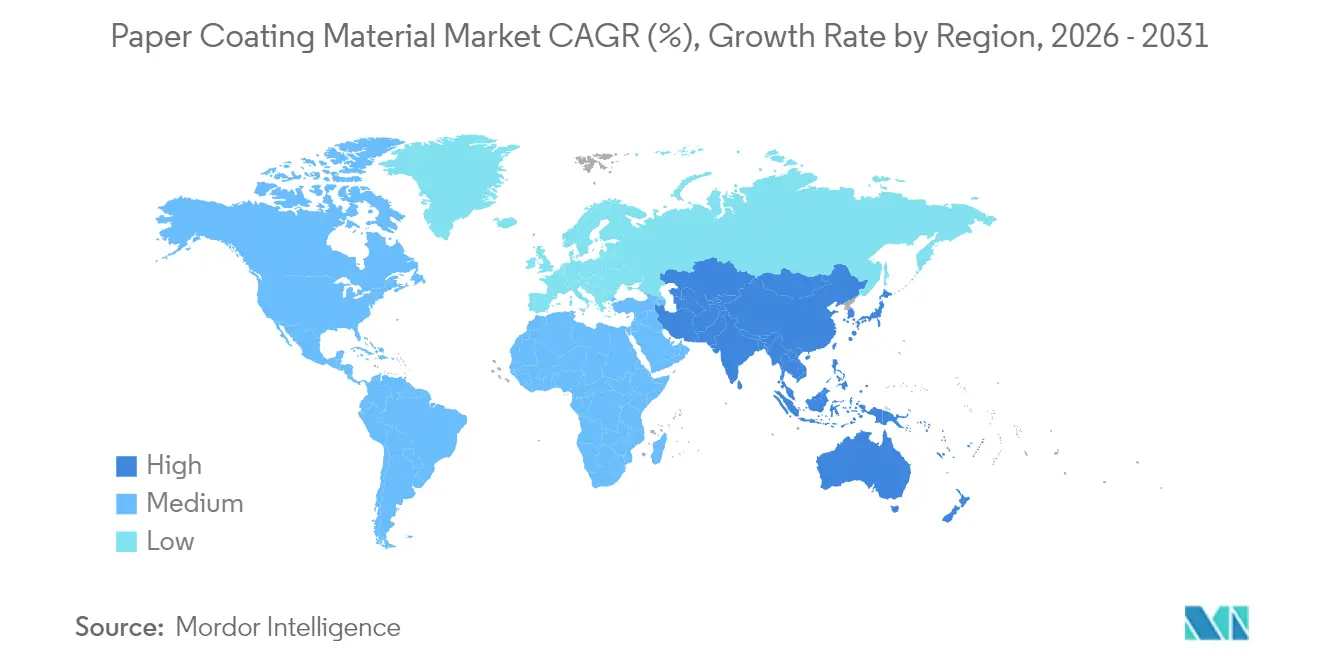

- By geography, the Asia-Pacific region held 46.88% of total demand in 2025; it is expected to advance at a 3.39% CAGR to 2031, the fastest growth rate worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paper Coating Material Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from printing and packaging industry | +0.8% | Global, with APAC leading growth | Medium term (2-4 years) |

| Regulatory bans on single-use plastics boosting paper substitution | +0.6% | EU & North America core, expanding to APAC | Long term (≥ 4 years) |

| E-commerce-led surge in corrugated and flexible paper packaging | +0.7% | Global, concentrated in urban markets | Short term (≤ 2 years) |

| Cost-effective optical performance of calcium-carbonate-rich coatings | +0.4% | Global manufacturing hubs | Medium term (2-4 years) |

| Mill-scale barrier-coating lines coming online post-2025 | +0.5% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand From Printing and Packaging Industry

Brand owners pivot toward sustainable packaging as governments restrict single-use plastics, lifting overall demand for paper substrates coated to provide barrier, printability, and aesthetic attributes[1]European Commission, “Packaging and Packaging Waste Revision,” ec.europa.eu. E-commerce volumes climbed 12.3% in 2024, driving unprecedented corrugated-box throughput and elevating coating consumption per thousand boxes shipped. Premium luxury packaging uses multilayer coatings that deliver high-gloss finishes, supporting margin expansion even as mass-print volumes taper. Supply-chain stakeholders increasingly co-develop specialized chemistries that enable paper to replace film in frozen-food and ready-meal packaging. This demand profile maintains high mill utilization despite structural declines in print volumes.

Regulatory Bans on Single-Use Plastics Boosting Paper Substitution

The European Union’s 65% recycling mandate for packaging by 2025 accelerates migration toward coated paper solutions that meet food-contact and recyclability benchmarks. PFAS phase-outs in North America and Europe eliminate fluorinated options, creating space for calcium-carbonate- and polymer-based alternatives that comply with stringent migration limits. Standards such as EN 13432 and ISO 12625 encourage suppliers to engineer biodegradable coatings. Extended producer responsibility laws pressure brands to adopt packaging that avoids landfill fees, placing coated paper formats at the center of design decisions. Regulatory alignment across regions shortens commercialization cycles for globally uniform coating grades.

E-Commerce-Led Surge in Corrugated and Flexible Paper Packaging

Online retail requires sturdy yet lightweight shipping media, reinforcing demand for moisture-resistant coatings that protect goods through dense distribution networks[2]Corrugated Packaging Alliance, “2024 Market Analysis,” corrugated.org. Corrugated boxes are projected to post a 3.10% CAGR through 2030 as omnichannel fulfillment expands to include groceries and pharmaceuticals. Flexible paper wraps are gaining traction in food delivery, relying on starch-polymer blends to block grease and prevent leakage. Coating suppliers capture value with high-runability grades that reduce basis weight without sacrificing compression strength. Retailers monetize branded unboxing experiences, pushing printers to specify high-opacity, high-gloss coatings that elevate graphic quality.

Cost-Effective Optical Performance of Calcium-Carbonate-Rich Coatings

Ground and precipitated calcium carbonate maintains optical brightness and opacity at a fraction of the cost of titanium dioxide, supporting its wide adoption in high-volume packaging. Advanced surface-modification processes tailor particle morphology for low-viscosity slurries, thereby improving coat weight uniformity. Abundant mineral reserves and mature logistics networks maintain predictable pricing amid petrochemical volatility. Hybrid CaCO₃-polymer formulations extend barrier functionality into grease-resistant snack wraps and chilled-food liners. As mills integrate on-site PCC capacity, coating suppliers strengthen long-term volume tie-ups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital media cannibalising print volumes | -0.5% | Global, most severe in developed markets | Long term (≥ 4 years) |

| Volatile prices of pulp, minerals and latex binders | -0.3% | Global supply chains | Short term (≤ 2 years) |

| Rising compliance costs for VOC and wastewater emissions | -0.2% | EU & North America primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Media Cannibalising Print Volumes

Traditional print applications are facing a structural decline as digital media consumption patterns shift permanently toward electronic formats, reducing demand for coated printing papers. Commercial printing volumes declined 4.2% annually since 2020, with newspaper and magazine segments experiencing the steepest contractions. Book printing maintains relative stability, but the digital transformation of educational publishing reduces demand for textbook coating in developed markets. The transition creates overcapacity in print-grade coating production, which pressures margins and forces suppliers to pivot toward packaging applications. Legacy coating formulations optimized for print applications often require reformulation to meet packaging performance requirements, resulting in transition costs and technical challenges.

Volatile Prices of Pulp, Minerals and Latex Binders

Raw material price instability disrupts coating supplier profitability and customer contract negotiations, with kaolin prices increasing 10% in 2024 following supply chain disruptions. Pulp price volatility affects paper mill economics and coating application rates, creating demand uncertainty that complicates capacity planning decisions. Latex binder costs fluctuate with petrochemical feedstock prices, impacting polymer coating segment margins and competitive positioning versus mineral-based alternatives. Supply chain concentration in key mineral deposits creates geographic risk, particularly for specialty coating grades requiring specific particle size distributions. Currency fluctuations exacerbate the volatility of raw material costs for global coating suppliers with multi-regional operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Material: Calcium Carbonate Dominance Faces Polymer Innovation

Calcium carbonate held 41.92% of the paper coating materials market share in 2025, translating into the single largest contributor to the total paper coating materials market size that year. Polymer coatings, however, exhibit the fastest growth at a 3.07% CAGR because food packaging requires moisture and grease barriers that minerals alone cannot provide.

Starch-based chemistries win brand favor in compostable snack packs, merging renewability with competitive economics. Talc and titanium dioxide serve niche roles in terms of brightness or smoothness, yet their higher cost limits their penetration to premium grades. Wax formulations remain a staple for controlling moisture in produce and frozen foods, although their share is shrinking as bio-based polymers mature. Suppliers are increasingly promoting hybrid mineral-polymer systems that combine the scattering efficiency of CaCO₃ with polymeric sealing to balance performance and price.

By Application: Packaging Supremacy Drives Market Evolution

Packaging applications accounted for 52.96% of overall demand in 2025, making them the largest slice of the paper coating materials market. Corrugated boxes headline with a 2.97% CAGR to 2031 as omni-channel retail scales, whereas flexible wraps capture emerging share as quick-service food shifts toward fiber formats.

Printing and writing grades decline in tandem with digital substitution, although pockets such as art books, photo albums, and security printing sustain limited but stable demand for coated paper. Bindery and specialty labels benefit from brand security features, leveraging micro-embossing coatings to thwart counterfeits. As consumer goods shift to minimal-plastics pledges, packaging-grade coatings diversify into water-based dispersion barriers and bio-waxes, enlarging the portfolio addressable to high-margin segments.

Geography Analysis

The Asia-Pacific region represented 46.88% of global consumption in 2025 and is projected to advance at a 3.39% CAGR, underscoring its central role in shaping the future scale and mix of paper coating materials market demand. China’s 7.2% production increase, combined with India’s surging packaged-goods output, sustains incremental tonnage. Cost-competitive labor, dense raw-material networks, and government-supported infrastructure foster a self-reinforcing manufacturing hub that anchors regional supply chains.

North America sustains a sizable but mature demand where innovation carries more weight than sheer volume. Food-grade dispersion barriers compliant with FDA migration rules command premium pricing, and mills increasingly retrofit curtain coaters to deliver on-trend recyclable cupstock. Europe’s policy alignment with circular-economy goals moves buyers toward biodegradable coatings, and the 65% recycling target by 2025 accelerates qualification cycles for new chemistries.

South America and the Middle East & Africa evolve from nascent baselines, but urbanization and retail expansion raise per-capita packaging use. Brazil’s return to GDP growth revives corrugated shipments, while Saudi Arabia’s Vision 2030 localization incentives attract coating-line investments from multinational paper producers. Supply-chain risk, currency volatility, and political uncertainty temper pace, yet first-mover suppliers secure footholds through joint ventures and in-country technical-service centers.

Regulatory Landscape

Regulatory pressure on paper coating materials is closely tied to packaging circularity targets and chemicals management, with the tightest expectations concentrated in Europe and North America. In the European Union, REACH obligations and the European Commission's Chemicals Strategy for Sustainability under the European Green Deal are pushing coating formulations toward safer chemistries, with heightened attention on substances used in consumer-facing and food-related applications. On the packaging side, the EU policy direction toward higher recycling performance, including the 65% packaging recycling target referenced for 2025 in the report context, supports demand for repulpable, PFAS-free barrier approaches that can work within fiber-based recycling systems.

In the United States, food-related coated papers fall under the food-contact framework. Paper and paperboard components for dry foods are addressed under 21 CFR 176.180 and related FDA food-contact substance pathways, which increases the need for migration and safety documentation for binders, dispersions, and functional additives. It also raises compliance costs for suppliers selling packaging-grade coatings into North America. Across both regions, tighter production-site expectations for VOC and wastewater performance influence technology choices, including water-based dispersions and optimized mineral slurries, and affect qualification timelines with mills and converters.

Value Chain Analysis

The paper coating materials value chain starts with upstream feedstocks and mineral inputs, then moves into formulation and application at paper and packaging mills before reaching converters and brand owners. Core ingredients include GCC/PCC calcium carbonate, kaolin and talc, titanium dioxide for premium optical performance, starch and waxes, and polymer binders such as styrene-acrylic and vinyl acetate-based latexes, along with functional additives that support printability and barrier performance. Coating suppliers compound these inputs into slurries or dispersions and typically provide technical service for runnability and end-use compliance, particularly for food-contact and repulpability needs.

Cost and availability risks are concentrated in petrochemical-linked monomers and specialty binder supply, along with logistics constraints for certain emulsions. The evidence pack highlights Celanese pricing actions on vinyl acetate monomer and related acetyl-chain products in June 2026, showing how upstream binder economics can flow through to coating formulators and, ultimately, to coated paper pricing and qualification decisions at mills. Downstream, the shift toward dispersion barrier coatings and in-line application increases collaboration between chemical suppliers and equipment and printing ecosystems. At the same time, vertical integration initiatives at mills and specialized coating lines shorten lead times and help stabilize supply for packaging customers.

Competitive Landscape

The Paper Coating Material market is moderately concentrated. Market leaders leverage integrated production and R&D to differentiate themselves on the basis of barrier performance and sustainability credentials. BASF’s 2024 divestment of non-core coating assets refocuses capital on high-barrier bio-dispersion lines that cater to premium packaging. Dow opened its USD 15 million BLUEWAVE platform in France during 2025 to quicken the rollout of dispersion technologies for recyclability-ready cups and wraps. Strategic collaborations are growing as mills install in-line barrier coaters; paper and chemical partners co-engineer grades to meet shelf-life and printability targets, while shortening the time-to-market. Intellectual property portfolios centered on PFAS-free dispersion and enzymatic cross-linkers are emerging as new competitive moats. Despite moderate consolidation, regional players continue to retain niches through agile services and tailored formulations for local substrates.

Paper Coating Material Industry Leaders

BASF

Dow

Imerys

Omya International AG

APP Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Barrier coatings for fiber-based food and beverage packaging remain a key whitespace, because performance requirements for oil, grease, moisture, and oxygen resistance have often been addressed using plastic laminations or fluorinated chemistries. In 2026, commercialization signals and partnerships support active market activity: Stahl introduced its Repura barrier-coatings portfolio for paper-based packaging (May 2026), Michelman introduced Nuvita Life 4002 and 4605 bio-based, plastic-free coatings for fiber-based retail food packaging (April 2026), and UPM Specialty Materials with Felix Schoeller introduced customizable fiber-based barrier technology for flexible food packaging formats such as snacks and chocolate bars (April 2026). These steps support opportunities for coating suppliers that can deliver tunable barrier levels while maintaining compatibility with fiber recycling.

Scale-up and localization investments also point to near-term opportunities, particularly in Europe, where circular-economy policy is driving packaging redesign. Elopak announced an investment in a new coating line at its Terneuzen facility to laminate cartonboard for Pure-Pak packaging (February 2026), indicating continued capex around advanced coating and converting capacity for paper-based alternatives. In parallel, applied research progress is broadening the formulation toolbox. The University of Oulu reported semi-pilot production of a water-based, bio-based coating derived from suberin extracted from birch bark (June 2026), which reinforces the development pipeline for bio-based, waterborne barriers designed to reduce reliance on petrochemical binders and align with brand-owner requirements for microplastic-free solutions.

Recent Industry Developments

- May 2026: BASF and UPM Specialty Materials announced a collaboration that combines UPM barrier papers with BASF Joncryl HPB high-performance barrier resins for fiber-based, recyclable packaging. The pairing links a specialty paper substrate portfolio with barrier resin chemistry to accelerate qualification of recyclable paper packaging structures where moisture and grease resistance are critical.

- September 2025: HEIDELBERG and Solenis introduced an inline process for applying barrier coatings to flexible paper packaging using the Boardmaster flexographic web printing system. Inline application connects coating chemistry with converting hardware, helping brand owners and converters reduce process steps and broaden barrier-coated paper adoption at industrial speeds.

- March 2024: BASF completed the divestment of selected non-core coating-related assets as part of its portfolio actions, sharpening focus on higher-value, sustainability-linked coating technologies. The move concentrated R&D and capital allocation toward barrier and dispersion innovations used in packaging-grade paper and paperboard applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers materials used to coat paper or paperboard surfaces to improve printability, smoothness, gloss, opacity, and basic barrier performance, and it is sized in value terms at the material level sold into paper coating uses.

Scope exclusions: It excludes finished coated paper and paperboard products, along with coating equipment, application services, and off-paper uses of the same minerals or polymers.

Segmentation Overview

- By Coating Material

- Clay

- Calcium Carbonate

- Starch

- Talc

- Titanium Dioxide

- Wax

- Polymer

- Other Coating Materials

- By Application

- Packaging

- Binding

- Printing

- Corrugated Boxes

- Other Applications

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Turkey

- Russia

- NORDICS Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- Qatar

- South Africa

- United Arab Emirates

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the industry chain, build a realistic demand pool for coated paper grades, and set guardrails for volumes and pricing. We referenced public sources such as the USGS mineral summaries, FAO forestry and paper indicators, UN Comtrade trade statistics, and EPA and EU policy releases that affect packaging substitution and coated paper demand, and then we cross-checked directionally with academic and technical journals on paper coatings.

To convert these signals into usable model inputs, we also reviewed company annual reports, investor presentations, and association publications for capacity additions, mill operating rates, and comments on binder and pigment availability. Where needed, paid subscriptions for company financials and patent databases were used to verify product focus and technology shifts, and an import export shipment-level database was used selectively to sanity-check traded flows of key coating inputs. The sources mentioned above are illustrative and not exhaustive, and additional public and paid references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating how coating material demand tracks coated paper production and mix, and on stress-testing average pricing and formulation shifts across grades. We spoke with a mix of coating material suppliers, paper mills, distributors, and downstream converters across APAC, EMEA, and the Americas, and then we rechecked any large variances through follow-up discussions so assumptions did not drift.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 50% |

| Mid tier: 48% | Functional/Unit leaders: 35% | EMEA: 31% |

| Smaller Players: 21% | Managers: 52% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where coated paper and paperboard output and trade patterns are reconstructed by region, and then coating add-on rates are applied to estimate the addressable coating-material consumption. Because coating recipes are not identical across grades, the model uses a practical set of inputs such as coated paper production by grade family, typical coating coat weight ranges, pigment to binder ratios, and the split between mineral pigments and polymer or wax coatings in packaging-oriented applications.

The resulting volumes are converted into value using regional price bands for major materials (for example calcium carbonate, kaolin clay, starch, latex binders, and titanium dioxide), which are adjusted for currency timing and mix changes. We then corroborate the totals with selective bottom-up approximations, such as supplier revenue exposure checks, sampled price per ton times implied tons, and channel feedback on spot versus contract pricing, which helps close gaps where public statistics are thin. For forecasting, scenario analysis is used around coated packaging growth, print demand softness, and substitution trends, and assumptions are aligned to what interviewees expect for capacity utilization and formulation changes over the next few years.

Data Validation & Update Cycle

Validation is done in layers so the final numbers do not rely on a single data stream. We compare calculated demand against independent signals such as coated paper trade balances, mineral supply availability, and announced paper machine or coating line changes, and then any sharp jumps are reworked until the drivers are clearly explained. A second analyst review is completed before sign-off, and re-contact is triggered when the model conflicts with field feedback or when new capacity or policy shifts appear.

The report is refreshed annually, and we also do interim checks when material events occur that can move pricing or volumes. Before delivery, a final update pass is completed so the output reflects the latest public releases and the most recent primary validations.

Mordor Intelligence's Paper Coating Material Market Size Compared Against Other Published Estimates

Published market sizes for paper coating materials can look far apart even when the topic sounds similar, and this usually happens due to scope definitions, the way volume is converted to value, and how fast assumptions are refreshed. Differences in whether coatings are treated as raw inputs versus finished coated paper products also create big swings in the total.

Finished coated paper and paperboard sales are kept outside Mordor Intelligence's scope, which reduces double counting when other estimates appear to mix material inputs with the value of coated end products. The spread also comes from how pricing is modeled, where some sources use broad chemical price inflation or a single global average, while this study uses region-specific price bands and checks them with supplier and mill feedback. Currency conversion timing and base-year selection matter as well, especially when titanium dioxide or latex binder prices move quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.23 B (2025) | |

| Industry Research Publisher A | USD 2.32 B (2025) | Often uses a broader definition that can include a wider specialty-chemical basket (pigments, binders, additives) across paper and paperboard uses, which can expand value capture beyond coating-material demand tied to coated-grade output. |

| Global Research Publisher B | USD 6.13 B (2025) | May treat the market closer to a total paper coatings and chemicals spend view, where upstream material value can be combined with wider application coverage and higher assumed average prices, which lifts totals versus material-only sizing anchored to coated production and coat-weight logic. |

Across the three figures, the main drivers are definition breadth and the price and mix assumptions used to translate tons into dollars. When the scope is kept at coating materials sold into paper coating uses, and the inputs are tied back to coated production, coat weight, and regional pricing checks, the estimate becomes easier to replicate and explain to decision-makers.

Key Questions Answered in the Report

What CAGR does the paper coating materials market expect between 2026 and 2031?

The market is projected to expand at 2.18% annually, moving from USD 1.26 billion in 2026 to USD 1.4 billion by 2031.

Which coating material holds the largest share today?

Calcium carbonate dominates at 41.92% of 2025 demand because it balances cost and optical performance.

Why is Asia-Pacific the top regional consumer?

China’s 7.2% production rise and India’s packaging surge give Asia-Pacific 46.88% share and the highest 3.39% growth rate.

What is driving faster growth for polymer coatings?

Polymer chemistries provide grease and moisture barriers essential for food packaging, yielding a 3.07% CAGR through 2031.

How do plastic-ban regulations influence demand?

EU and North American recycling mandates steer converters toward coated paper that meets barrier and compostability targets.

Page last updated on: