Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 100.28 Billion |

| Market Size (2031) | USD 123.96 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Architectural Coatings Market Analysis by Mordor Intelligence

The architectural Coatings Market size is projected to be USD 96.12 billion in 2025, USD 100.28 billion in 2026, and reach USD 123.96 billion by 2031, growing at a CAGR of 4.33% from 2026 to 2031. The measured headline growth hides an accelerated shift toward low-VOC, water-borne systems that is compressing the economic life of legacy solvent-borne assets, raising capital-intensity for smaller producers that cannot fund rapid retooling. Water-borne coatings already hold just over half of global volume, yet infrastructure gaps in parts of South and Southeast Asia delay full adoption by 3-5 years, especially where tinting equipment and controlled distribution remain under-developed. Acrylic resins dominate formulation choices because they align with tightening emission rules and perform well in humid climates, while alkyd demand continues to erode as solvent limits tighten. Regionally, Asia-Pacific underpins demand expansion through rapid urbanization, whereas North America and Europe depend on renovation cycles in housing built after 1970 in an era of high borrowing costs.

Key Report Takeaways

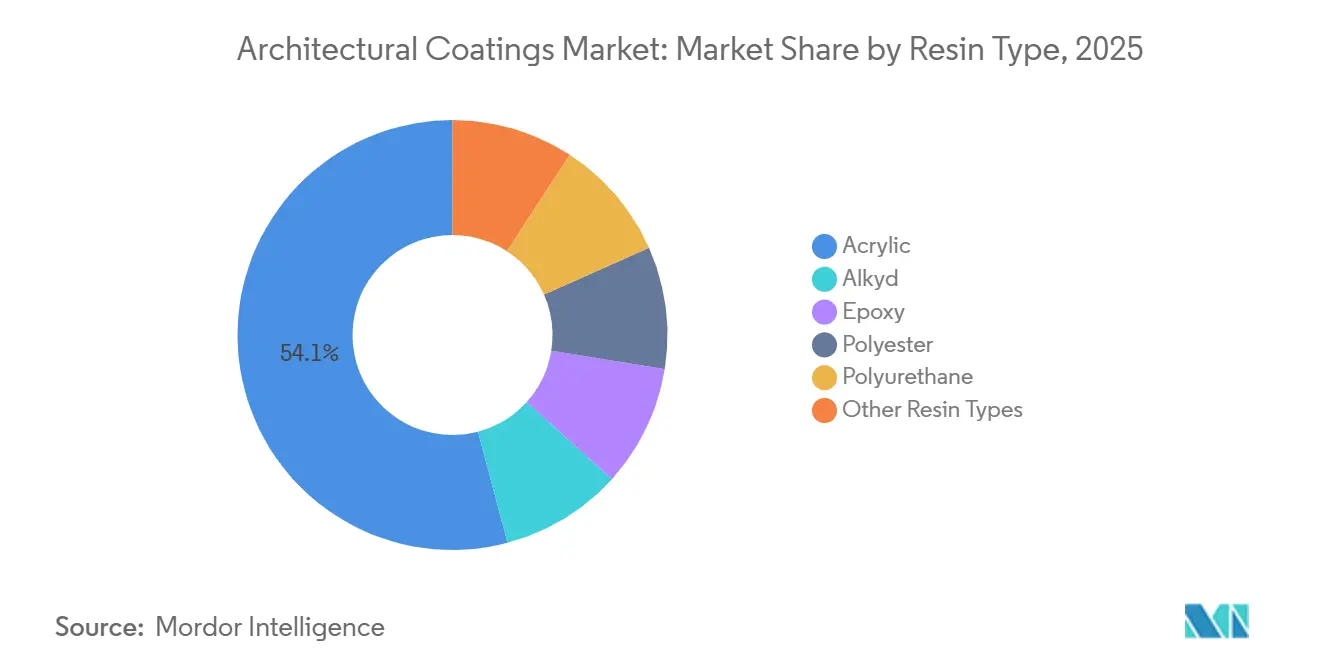

- By resin type, acrylic led with 54.13% architectural coatings market share in 2025 and is projected to advance at a 4.68% CAGR through 2031.

- By technology, water-borne captured 52.12% of the architectural coatings market size in 2025 and is expanding at a 4.78% CAGR to 2031.

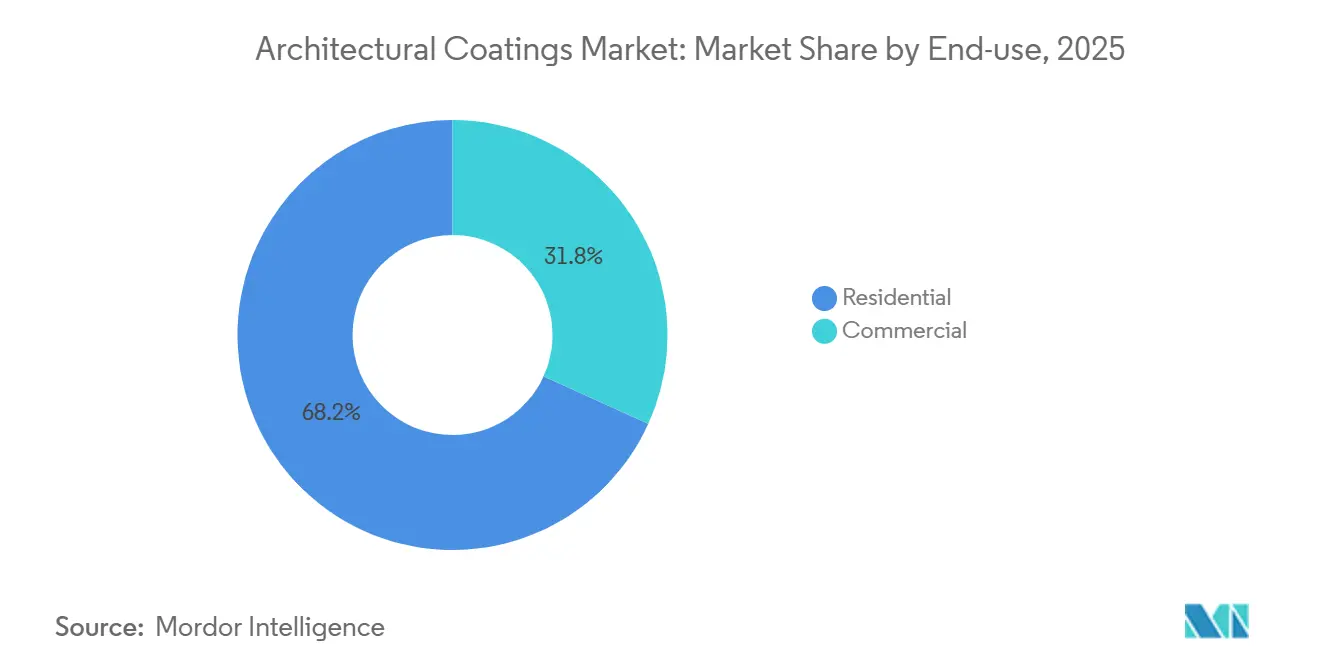

- By end use, residential accounted for 68.22% of the architectural coatings market size in 2025 and is expanding at a 4.53% CAGR to 2031.

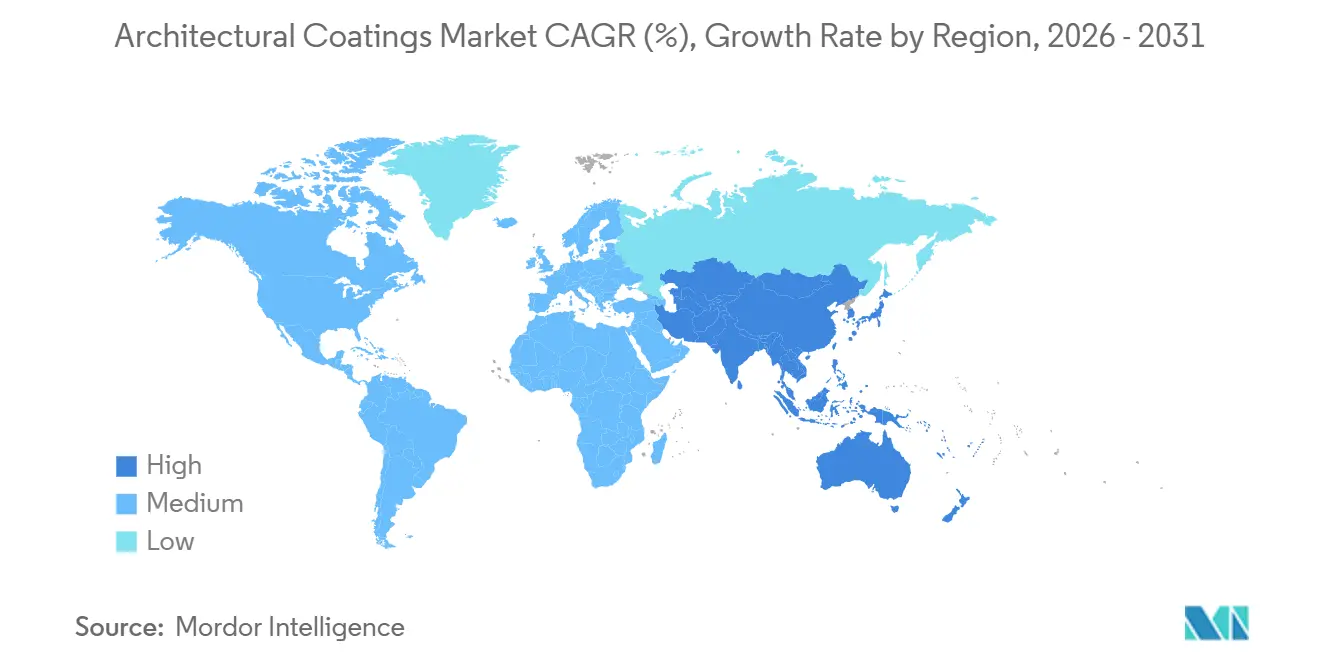

- By geography, Asia-Pacific held 46.11% of the architectural coatings market size in 2025 and is expected to grow at a 5.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Architectural Coatings Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-VOC regulations accelerating global switch to water-borne systems | +1.2% | Global, with strongest enforcement in EU, California, China | Medium term (2-4 years) |

| Surging renovation of post-1970 housing stock in North America and Europe | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Explosive growth of organised DIFM trade-painter networks in ASEAN metros | +0.8% | ASEAN core (Indonesia, Vietnam, Thailand, Philippines) | Short term (≤ 2 years) |

| Rapid e-commerce penetration enabling direct-to-consumer paint fulfilment | +0.6% | North America, Europe, urban APAC | Medium term (2-4 years) |

| On-site robotic/3-D-printed façade modules demanding nano-filled coatings | +0.4% | Global, early adoption in Middle-East, Singapore, select EU cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low-VOC Regulations Accelerating Global Switch to Water-Borne Systems

California lowered the VOC ceiling for interior flats to 50 g/L in 2024, forcing reformulation of 40% of products sold in the state and nudging manufacturers everywhere to harmonize recipes for scale[1]South Coast Air Quality Management District, “Rule 1113 Architectural Coatings,” aqmd.gov . The EU followed in 2025 with a 30 g/L cap, a level that effectively eliminates traditional solvent-rich alkyd primers unless costly bio-based substitutes are introduced. China’s extension of its low-VOC mandate to Tier-3 cities widened compliance coverage to another 180 million residents and accelerated the retirement of solvent lines. Global majors amortize reformulation costs across wider volumes, but small regional firms either license technology at 3%–5% of sales or cede premium segments entirely.

Surging Renovation of Post-1970 Housing Stock in North America and Europe

The United States houses built between 1970 and 1990 now require exterior refreshes, driving USD 510 billion in improvement spending projected for 2026. Canada’s Greener Homes Grant covers up to USD 3,700 for energy upgrades, propelling a 19% increase in applications during 2025. Europe’s Renovation Wave aims to double retrofit rates by 2030, and Germany alone disbursed USD 13 billion in low-interest loans for façade updates in 2025. These programs tilt demand toward acrylic and elastomeric coatings with 15-20 year lifespans that satisfy homeowners looking to minimize repeat labor. Skilled labor shortages, however, have stretched project lead times to eight-to-twelve weeks, tempering near-term volume growth.

Explosive Growth of Organized DIFM Trade-Painter Networks in ASEAN Metros

Indonesia’s painter cooperatives grew from 12,000 in 2023 to 27,000 by mid-2025, earning 15%-20% bulk discounts in exchange for brand exclusivity. Vietnam introduced mandatory licensing in 2024, lifting certified applicator share from 18% to 34% in 18 months and spurring adoption of warranty-backed premium water-borne systems. Thailand’s largest home-improvement chain launched a DIFM marketplace late 2024 that captured 9% of Bangkok’s repaint jobs within one year. Professionalization shifts preference toward brands that supply consistent batch quality, digital ordering, and next-day delivery, compressing project cycles by as much as 25%.

Rapid E-Commerce Penetration Enabling Direct-to-Consumer Paint Fulfillment

Sherwin-Williams generated USD 340 million online in 2025, with average order values 22% higher than stores after algorithm-driven upsells. Benjamin Moore’s color-visualization tool pushed return rates below 2% by letting users preview shades on their own photos. Dulux’s augmented-reality calculator has been downloaded 1.2 million times since 2024, cutting over-ordering by 30%. As online share reached 18% in cities such as Seoul and Singapore during 2025, independent dealers in North America saw their channel share slip five points to 33%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ and epoxy feedstock prices post-2024 supply shocks | -0.7% | Global, acute in import-dependent markets (India, Brazil, MEA) | Short term (≤ 2 years) |

| Scarcity of skilled painters in mature markets inflating installation costs | -0.5% | North America, Europe, Australia | Medium term (2-4 years) |

| EU biocide restrictions cutting allowable in-can preservative loadings | -0.3% | Europe, with spillover to export-oriented manufacturers in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ and Epoxy Feedstock Prices Post-2024 Supply Shocks

TiO₂ climbed from USD 2,800/t in Q1 2024 to USD 3,300/t in Q1 2025 after Chinese environmental shutdowns, easing later when Saudi capacity came online, yet margins for Indian and Brazilian producers still fell by up to 180 basis points because of currency swings. Epoxy costs spiked 22% after force-majeure events at bisphenol-A plants, forcing formulators to shift to polyester in non-critical roles. Majors hedge via partial ownership of TiO₂ assets; PPG’s 30% stake in a Chinese supplier secures 40,000 t per year at fixed prices, insulating earnings. Smaller firms negotiate quarterly pass-throughs, limiting strategic flexibility.

Scarcity of Skilled Painters in Mature Markets Inflating Installation Costs

The United States recorded 87,000 unfilled painter roles in 2025, driving hourly wages up 14% since 2023 and lifting the cost of a typical exterior repaint to USD 7,200[2]U.S. Bureau of Labor Statistics, “Occupational Outlook for Painters,” bls.gov . Germany faces a 9,000-person gap, while Australian contractors report project backlogs of 10-14 weeks. Homeowners either delay work or downgrade product choices, softening premium demand despite manufacturer-sponsored training academies that only partly address the shortfall.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Rooted in Regulatory Alignment

Acrylic commanded 54.13% of 2025 demand, the largest slice of the architectural coatings market size, and is projected to outpace the overall architectural coatings market at a 4.68% CAGR to 2031. Low-VOC compliance and robust exterior durability in humid climates underpin this leadership. Alkyd demand is contracting as solvent caps render many lines non-compliant without expensive capture systems.

Epoxies are known for their high abrasion resistance but remain constrained by UV instability and elevated cost, while polyurethanes are driven by coastal gloss-retention needs. Polyester powder coatings are favoured for factory-finished metal framing, and bio-based hybrids draw fresh R&D as firms seek differentiators for circular-economy labels.

By Technology: Water-Borne Systems Gain Despite Infrastructure Gaps

Water-borne comprised 52.12% of 2025 volume and are growing 4.78% annually, as regulations and indoor-air expectations rise. Solvent-borne, useful for low-temperature or high-humidity job sites, and stabilizing in India, where masonry substrates need deeper penetration.

The other technologies cover powder, high-solids, and UV-cured lines whose adoption scales with prefabrication trends. Powder finishes deliver almost 100% transfer efficiency but remain limited to factory conditions. High-solids sprays cut VOCs per liter yet demand costly gear that small painters rarely purchase, while UV-cure systems thrive in cabinetry shops but face line-of-sight limitations on complex shapes.

By End-use: Residential Segment Anchored by Renovation Cycles

Residential generated 68.22% of 2025 revenue and expanding at 4.53% thanks to steady repaint cycles and emerging-market housing starts. U.S. single-family improvements alone spent USD 34 billion on coatings in 2025, while India’s housing initiatives are lift demand regionally.

Commercial is also growing as hybrid work suppresses office repainting even as hospitality assets specify antimicrobial finishes and institutional owners pursue LEED credits that tilt choices toward premium water-borne acrylic. Retail refurbishments bifurcate: luxury stores commission bespoke finishes, whereas value chains choose cost-optimized systems.

Geography Analysis

Asia-Pacific contributed 46.11% of the 2025 volume and will lead the architectural coatings market growth at 5.57%. India is advancing under Smart Cities funding that raised middle-class homeownership to 58%. Southeast Asian markets grew as FDI-backed logistics hubs and social-housing programs expanded coating consumption .

In North America, the United States accounted for most of the spending on architectural finishes as owners chose upgrades over moving in a high-rate mortgage environment. Canada added growth on the back of energy-retrofit incentives, while Mexico grew with near-shoring industrial builds.

In Europe, Germany, France, and the United Kingdom together represented the majority of regional value, each leveraging public loan or grant schemes to spur façade upgrades and low-emission interior paints. Central and Eastern Europe caught up with growth funded by EU structural allocations, while NORDIC markets maintained niche growth under strict environmental codes.

In South America, Brazil’s social-housing expansion and agribusiness-led commercial builds drove growth, whereas currency pressures in Argentina redirected buyers to local brands. Chile, Peru, and Colombia benefited from mining-related infrastructure projects needing worker housing.

The Middle-East and Africa comprised lower demand but will post a substantial demand as Saudi Vision 2030 mega-projects require premium exterior coatings tolerant of extreme heat, and sub-Saharan urbanization lifts baseline consumption despite fragmented logistics.

Competitive Landscape

The five largest suppliers controlled 49% of 2025 revenue, signaling moderate consolidation in the architectural coatings market. Sherwin-Williams, PPG, and AkzoNobel are leveraging vertical integration into TiO₂ and resin production, which lifted PPG's gross margin 120 basis points in fiscal 2025. Asian Paints and Nippon Paint jointly hold through dense distribution and tinting reach.

Digital engagement differentiates leaders: PPG’s “Voice of Color” app drove an 18% rise in online conversions, while AkzoNobel’s AR-based “Dulux Visualizer” cut product returns 25%. Market niches include antimicrobial interior finishes that grew in 2025 and graphene-enhanced eco-paints pitched to sustainability-minded consumers, though disruptors still own less than 1% share. Patent filings concentrate on nano-dispersion and bio-based acrylics, with BASF registering 14 new families in 2025.

Regional specialists such as Berger Paints, DAW SE, and CIN defend home-market share with localized color palettes and swift delivery yet struggle to spread R&D costs across broader geographies. Acquisition remains the preferred growth vector; Nippon Paint’s 51% stake in a Turkish producer opened direct access to Middle-Eastern and North African channels in 2025.

Architectural Coatings Industry Leaders

The Sherwin-Williams Company

AkzoNobel N.V.

Nippon Paint Holdings Co., Ltd

Asian Paints Ltd.

Pittsburgh Paints Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: BASF started a new production line for dispersions used in architectural coatings at its facility in Dilovası, Türkiye. This enabled BASF to better serve the architectural coatings market by supplying low-VOC (volatile organic compound) dispersions that improved indoor air quality.

- December 2024: PPG Industries Inc. sold its U.S. and Canadian architectural coatings business to American Industrial Partners (AIP) for approximately USD 550 million. The divestiture included manufacturing facilities, distribution centers, and over 15,000 points of sale, with the unit renamed Pittsburgh Paints Co..

Global Architectural Coatings Market Report Scope

Architectural coatings are protective and decorative finishes applied to stationary structures, such as interior and exterior walls, roofs, and floors of residential, commercial, and industrial buildings. These coatings, including paints, sealants, and varnishes, provide protection against UV rays, moisture, and corrosion while enhancing aesthetic appeal.

The architectural coatings market is segmented by resin type, technology, end-use, and geography. By resin type, the market is segmented into acrylic, alkyd, epoxy, polyester, polyurethane, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, and other technologies. By end-use, the market is segmented into residential and commercial. The report also covers the market size and forecasts for the architectural coatings in 24 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

| Other Technologies |

By End-use

| Residential |

| Commercial |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Thailand | |

| Philippines | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Poland | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Acrylic | |

| Alkyd | ||

| Epoxy | ||

| Polyester | ||

| Polyurethane | ||

| Other Resin Types | ||

| By Technology | Water-borne | |

| Solvent-borne | ||

| Other Technologies | ||

| By End-use | Residential | |

| Commercial | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Vietnam | ||

| Thailand | ||

| Philippines | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Poland | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the architectural coatings market in 2031?

The architectural coatings market is forecast to reach USD 123.96 billion by 2031, growing at a 4.33% CAGR from 2026-2031.

Which resin type commands the largest share in global demand?

Acrylic resins led with 54.13% share in 2025 thanks to their low-VOC compliance and exterior durability.

How fast is the Asia-Pacific region growing?

Asia-Pacific demand is advancing at 5.57%, the fastest regional CAGR, driven by urbanization and rising per-capita paint usage.

What share do water-borne technologies hold?

Water-borne coatings already represent 52.12% of global volume and are expanding faster than the overall market.

Page last updated on: