Chemicals & Materials

2nd JuneUnlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

The Mirror Coatings Market Report is Segmented by Resin Type (Epoxy, Acrylic, and More), Technology (Nano-Coatings, Solvent-Based, and More), End-User Industry (Building and Construction, Automotive and Transportation, Energy, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

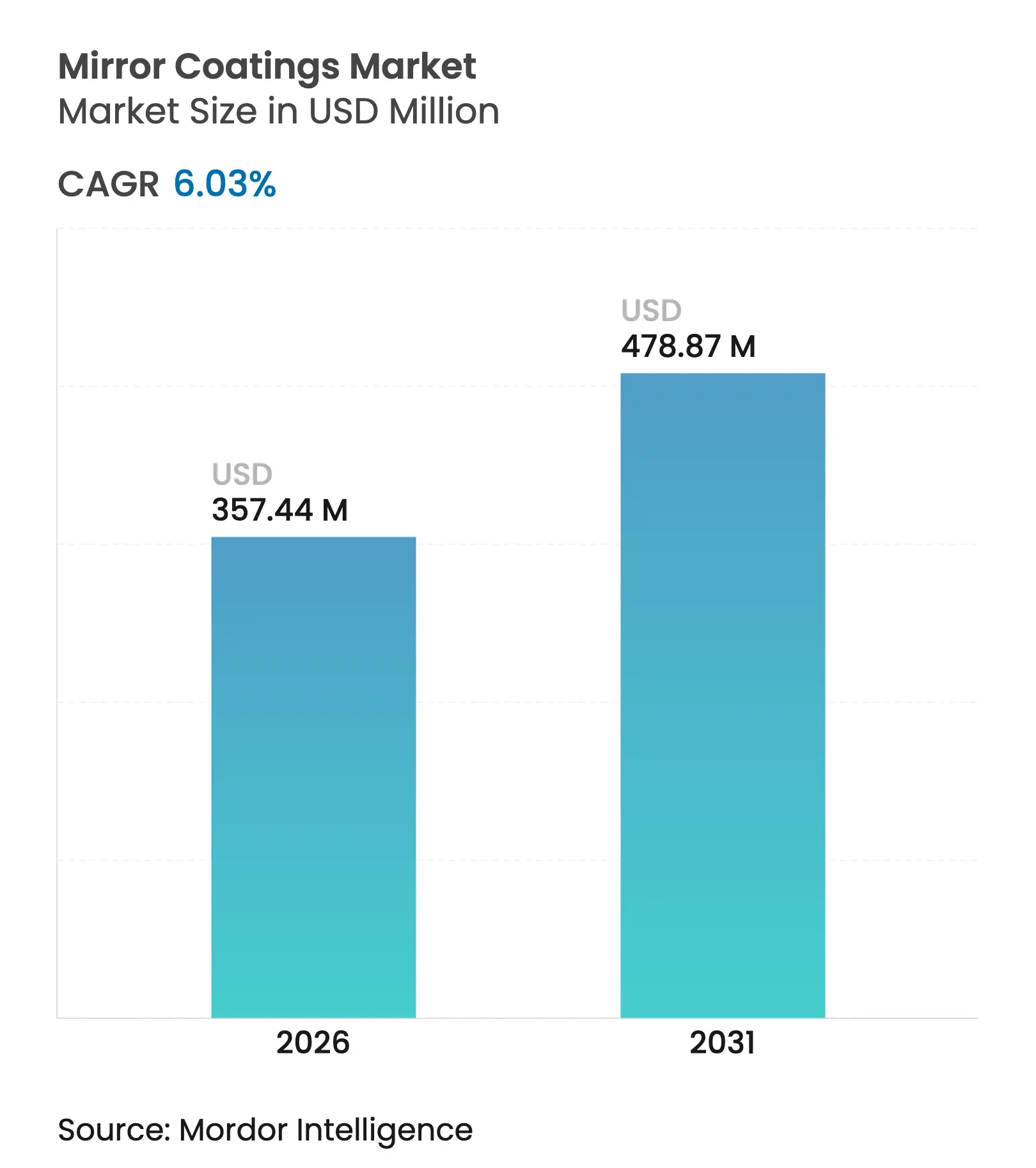

| Market Size (2026) | USD 357.44 Million |

| Market Size (2031) | USD 478.87 Million |

| Growth Rate (2026 - 2031) | 6.03 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Mirror Coatings Market size was valued at USD 337.10 million in 2025 and estimated to grow from USD 357.44 million in 2026 to reach USD 478.87 million by 2031, at a CAGR of 6.03% during the forecast period (2026-2031). Growth stems from rising demand for high-performance optical layers that improve reflectivity, durability, and environmental resistance across construction, automotive, and energy projects. Construction recovery in key economies, rapid solar build-outs, and premium electric-vehicle designs are expanding the addressable pool of applications. Manufacturers are also moving toward nano-structured and water-borne chemistries to comply with tightening VOC rules and to unlock differentiated functionality. In parallel, investments in automated sputter lines and recycling partnerships are helping leading suppliers lower costs and meet sustainability targets. Competitive intensity is rising as global glass majors and regional specialists race to secure feedstock, adopt advanced deposition technologies, and develop coatings tailored to heliostats, smart façades, and lightweight substrates.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Construction rebound in several economies

Construction rebound in several economies

| +1.5% | Global, early gains in Asia-Pacific and North America | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.5%

|

Geographic Relevance

:

Global, early gains in Asia-Pacific and North America

|

Impact Timeline

:

Medium term (2-4 years)

|

Rapid scale-up of utility CSP and heliostat retrofits

Rapid scale-up of utility CSP and heliostat retrofits

| +0.8% | MENA, North America with spill-over to Asia-Pacific | Long term (≥4 years) | |||

Weight-saving demand from premium EV makers

Weight-saving demand from premium EV makers

| +0.6% | Global, concentrated in North America, Europe, China | Medium term (2-4 years) | |||

Solar-grade low-iron glass capacity additions in MEA

Solar-grade low-iron glass capacity additions in MEA

| +0.4% | MEA core, export potential to Asia-Pacific | Long term (≥4 years) | |||

Nanostructured self-cleaning coatings commercialisation

Nanostructured self-cleaning coatings commercialisation

| +0.3% | Global, early adoption in developed markets | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Construction Rebound in Several Economies

Residential, commercial, and mixed-use construction starts are predicted to climb 9% in 2025 to USD 1.3 trillion as financing conditions improve and interest rates stabilize. The rebound is lifting demand for architectural glazing solutions that integrate high-reflectivity mirror layers for daylighting and thermal management. Developers are deploying mirrors in atriums, façades, and interior design to create modern aesthetics while managing building-energy loads. As project pipelines swell, premium formulations that endure UV exposure and maintain optical clarity command price premiums. Labor shortages and schedule pressures may restrain near-term volumes but support higher margins for specialized suppliers that can guarantee quick delivery and consistent quality.

Rapid Scale-Up of Utility CSP and Heliostat Retrofits

Utility-scale concentrated solar power plants increasingly rely on precision-coated heliostat mirrors that reflect and focus sunlight onto central receivers. Saudi Arabia and neighbouring states pushed regional solar manufacturing capacity beyond 3 GW by late 2024, with an additional 5 GW complex announced for commissioning by 2030[1]Jaideep Malaviya, “Middle East Accelerates Solar Manufacturing Push but Raw Materials a Hurdle,” Mercom India, mercomindia.com. Machine-learning-guided calibration can raise CSP energy yield by up to 44%. United States federal funding of USD 3 million for six heliostat R&D projects underscores public-sector commitment to cut system costs and extend mirror life. Rectangular mirror geometries that reduce shadowing effects are driving new specification sheets for advanced coatings tuned to oblique-angle performance.

Weight-Saving Demand from Premium EV Makers

High-end electric vehicle brands are shifting from glass to polycarbonate and acrylic substrates to curb mass and extend driving range. Vacuum-ultraviolet laser surface modification improves scratch resistance on these plastics, making reflective coatings feasible for front modules and side mirrors Crystal glass pigments enhance LiDAR reflectivity and driver visibility, while TiO₂-backside coated mirrors achieve up to 85% reflection at critical wavelengths. Coaters must balance optical transparency with electromagnetic compatibility to avoid sensor interference, spurring R&D into multi-layer stacks that combine metallic films with dielectric barriers.

Solar-Grade Low-Iron Glass Capacity Additions in MEA

Solar glass now represents 5% of global float output, and producers such as NSG Group and Vitro are commissioning dedicated lines to feed regional CSP and PV markets. AGC Glass Europe produced 42,917 MWh of low-carbon glass in 2023 and targets a 50% cullet ratio by 2030 to cut emissions. Innovations like hybrid hydrogen-electric furnaces that lower CO₂ by 75% are aligning with customer procurement policies, favouring suppliers that can market coatings as part of a sustainable materials package. High-irradiance desert conditions demand mirror layers with superior adhesion, UV stability, and abrasion resistance.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile silver pricing squeezing margin-sensitive small

businesses

Volatile silver pricing squeezing margin-sensitive small

businesses

| -0.6% | Global, particularly affecting Asia-Pacific manufacturers | Short term (≤2 years) |

(~) % Impact on CAGR Forecast

:

-0.6%

|

Geographic Relevance

:

Global, particularly affecting Asia-Pacific manufacturers

|

Impact Timeline

:

Short term (≤2 years)

|

Lack of global VOC alignment delaying water-borne shift

Lack of global VOC alignment delaying water-borne shift

| -0.4% | Global, with regulatory fragmentation across regions | Medium term (2-4 years) | |||

Skilled-labor scarcity for advanced sputter lines

Skilled-labor scarcity for advanced sputter lines

| -0.3% | North America and EU, spill-over to Asia-Pacific | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Silver Pricing Squeezing Margin-Sensitive Small Businesses

Silver demand from PV paste doubled to 6,577 tons, consuming 19% of world supply in 2024 and driving spot prices that small coaters struggle to hedge. Recycling values hover near USD 680 per kg, yet impurity variability complicates procurement. Because 72% of silver comes as a by-product of other metals, supply elasticity is weak. Niche players are testing copper substitutions, but optical performance losses limit penetration in premium mirrors. Larger groups with diversified raw-material portfolios leverage forward contracts and treasury tools to buffer volatility.

Lack of Global VOC Alignment Delaying Water-Borne Shift

California’s rulebook distinguishes between “VOC regulatory” and “VOC actual,” forcing coaters to run bespoke calculators for each formulation[2]California Air Resources Board, “VOC Limits,” arb.ca.gov. In Europe, Best Available Techniques guidelines require solvent-use minimization but enforcement varies by member state. South Coast AQMD is phasing out para-chlorobenzotrifluoride between 2025 and 2028. These fragmented timelines raise compliance costs and slow capital planning for new water-borne or UV-cure lines. Emerging markets such as Indonesia evolve at different paces, creating a patchwork of standards that multinational suppliers must navigate, often duplicating product lines to remain competitive.

By Resin Type: Acrylic Dominance Faces Polyurethane Challenge

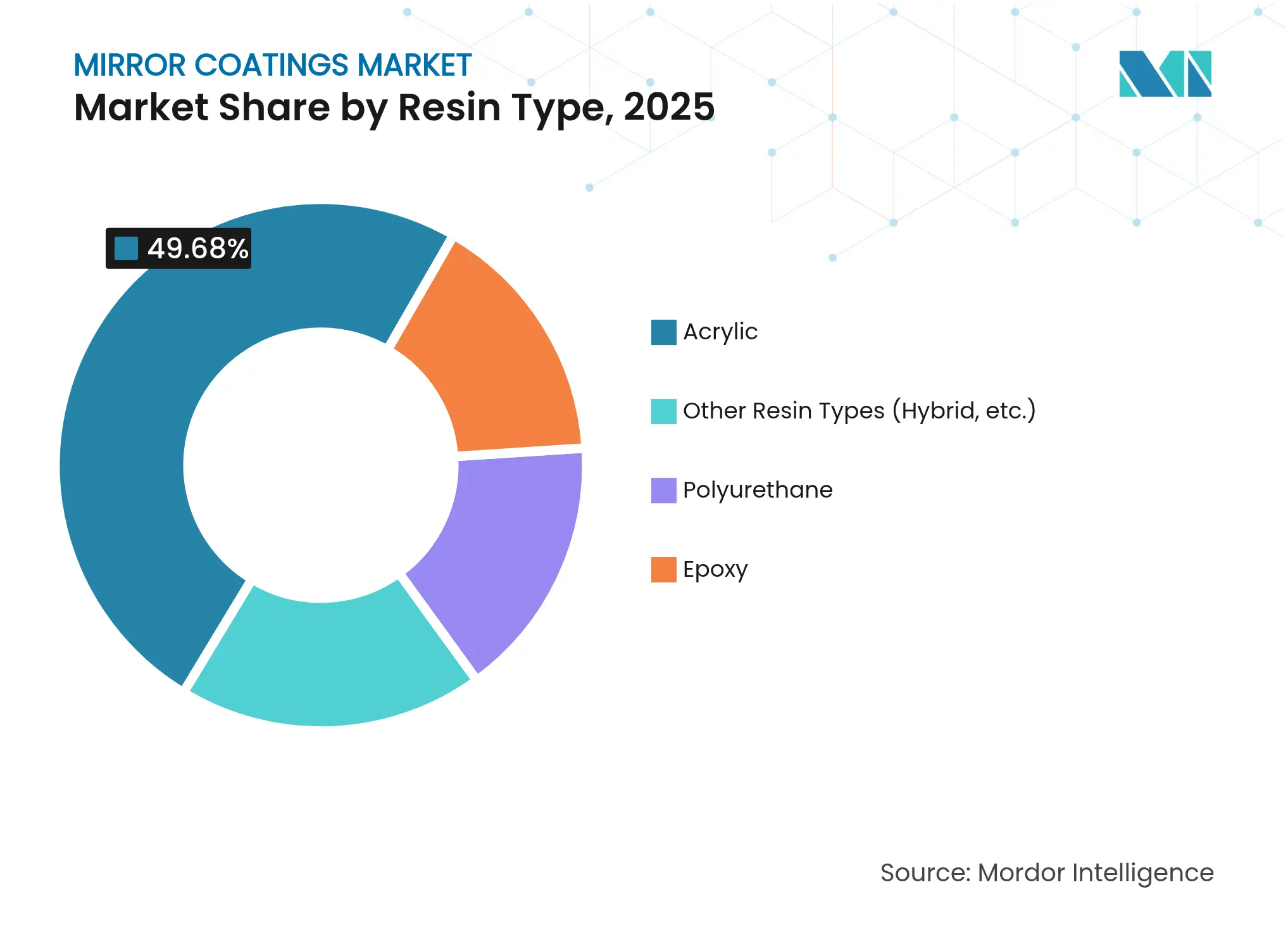

Acrylic formulations delivered 49.68% of 2025 revenues, confirming their status as the cost-effective workhorse for façades, decorative wall panels, and general-purpose mirrors. The mirror coatings market benefits from acrylic’s UV resistance and color stability that preserve reflectance in harsh climates. Industrial specifiers appreciate fast curing and easy processing, which shorten fabrication cycles. The segment’s scale also supports commoditized supply chains that keep pricing predictable.

Polyurethane resins, projecting a 7.42% CAGR, are gaining traction where mechanical stress, abrasion, and chemical exposure are high. Premium automotive exteriors, CSP heliostats operating at elevated temperatures, and rail platforms adopt polyurethane layers that bond strongly to metal backings. Advances in hydroxyl-functional prepolymers have improved flexibility while lowering isocyanate content, aligning with health and safety trends in the mirror coatings industry. Hybrid chemistries that cross-link acrylic and epoxy moieties are emerging for niche aerospace cabins and marine consoles that need both elasticity and solvent resistance.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Solvent-Based Stability Versus Nano-Coating Innovation

Traditional solvent-based methods accounted for 41.98% of turnover in 2025. They remain prevalent because they run on well-understood equipment and deliver consistent film thickness, which is vital for optical uniformity. Lower capital intensity also suits small and medium-sized coaters serving local contractors. However, environmental scrutiny is intensifying in Europe and parts of North America, where solvent emissions carry permitting risks.

Nano-coatings, predicted to register a 7.31% CAGR, promise higher performance at thinner layers. TiO₂-doped stacks confer self-cleaning properties that reduce maintenance costs on solar arrays. Ag-SiO₂ composite structures boost near-infrared reflection that improves building energy efficiency. Scaling these chemistries from pilot to mass production involves precise temperature control and advanced plasma deposition that call for skilled technicians, which is currently a supply bottleneck. Early adopters in the mirror coatings market size segments tied to renewable energy and smart infrastructure accept the price premium due to demonstrable lifecycle savings.

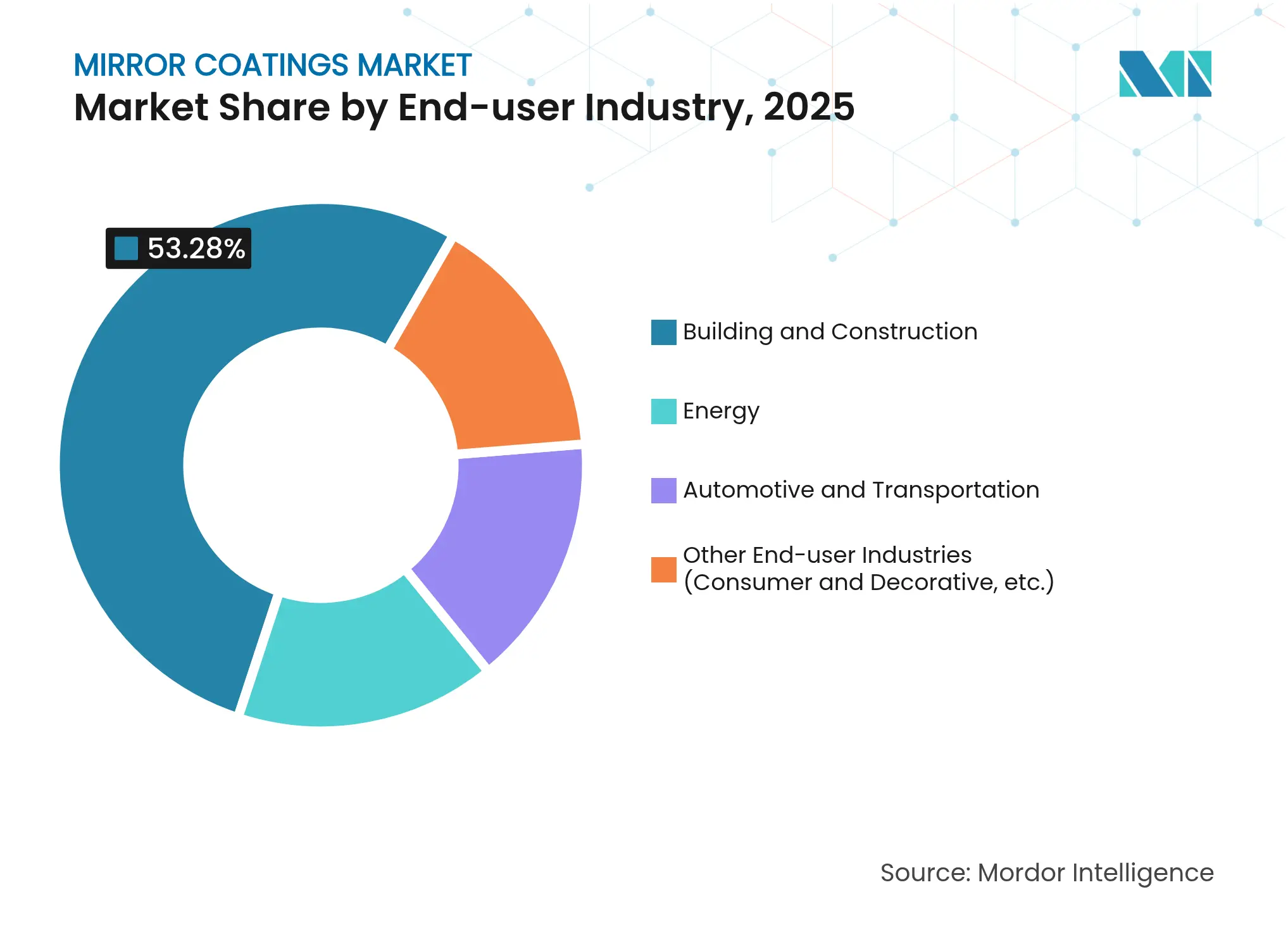

By End-user Industry: Construction Leadership Challenged by Energy Growth

The construction sector delivered 53.28% of revenue in 2025. Mixed-use skyscrapers and hospitality refurbishments specify mirrors for daylight redirection and visual expansion of interior spaces. Designers increasingly integrate mirrored louvers and canopies that reduce artificial lighting loads and elevate occupant comfort. As real estate developers target green-building certifications, demand for low-VOC and recyclable coating systems continues to climb.

Energy applications are forecast to expand at a 7.16% CAGR as solar-rich regions install parabolic troughs and heliostat fields that rely on ultra-high reflectance. Optical losses as small as 1% can translate to significant drop-offs in plant capacity factors, prompting owners to favour suppliers with rigorous quality control protocols. The mirror coatings market size attributed to CSP alone is set to outpace average sector growth because several national decarbonization strategies earmark thermal storage as a complement to variable PV generation. Automotive and transport retain steady contributions by incorporating blue-tint anti-glare rear-view mirrors and sensor-friendly exterior trims.

Note: Segment shares of all individual segments available upon report purchase

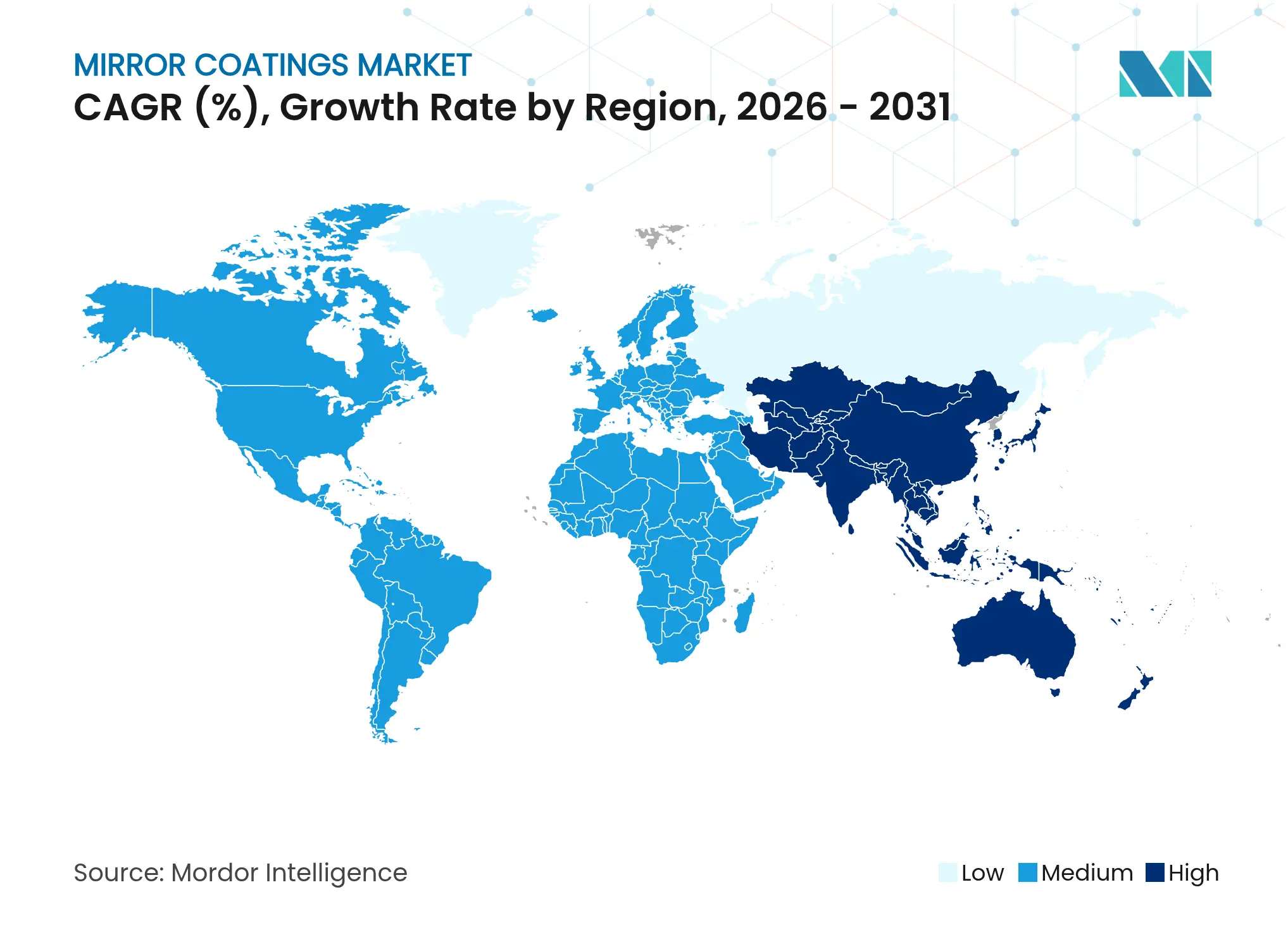

Asia-Pacific commanded 54.35% of global value in 2025 and is tracking a 7.05% CAGR through 2031. Mainland China’s 500 MW CSP base, India’s metro expansions, and Indonesia’s 6.47% annual coatings growth create layered demand streams. Local fabricators benefit from proximity to float-glass hubs and competitive labour, although volatility in silver and energy costs introduces planning complexity. Governments are simultaneously mandating higher environmental standards, leading to dual-line production where both solvent and water-borne coatings run.

North America shows mid-single-digit growth as infrastructure spending resumes and the Department of Energy funds heliostat innovation. Commercial builders in the United States favour mirrors integrated with low-e glazing to meet state energy codes. Canada’s cold-climate provinces specify mirror backings that resist cycling between freeze and thaw, creating niches for polyurethane-rich stacks.

Europe’s mature building stock supports replacement demand, while Eastern Europe’s industrial parks feed greenfield opportunities. AGC’s low-carbon float lines in Belgium and France supply architects seeking environmental product declarations. Stringent VOC thresholds are accelerating the shift to water-based dispersions, compelling global suppliers to localise production or pay duties on imported solvent mixes. South America and the Middle East and Africa contribute smaller but faster-growing slices. High-irradiance zones in Saudi Arabia and the United Arab Emirates are positioning the region as a testbed for nano-coatings that withstand sandstorms and high ambient temperatures.

Market Concentration

The mirror coatings market features a mix of diversified multinationals and nimble regional specialists. PPG Industries posted USD 18.2 billion sales in 2023, with Performance Coatings up 4.4% on aerospace and automotive gains. Guardian Glass operates more than 20 magnetron sputter coaters worldwide and holds 800 patents, underlining a technology-driven approach. Saint-Gobain commercialised MIRALITE EASYSAFE, integrating a resin backing that retains 98% of shards upon impact, signalling safety-oriented product innovation.

Strategic moves centre on capacity expansion, vertical integration, and sustainability. AGC Interpane invested in a new insulating glass line that boosts German output by 30% and adds laminated safety capability. Partnerships such as AGC’s alliance with ROSI recycle solar cover glass into float substrates, securing cullet supply and cutting energy consumption. In Asia-Pacific, several manufacturers are automating deposition lines to sharpen uniformity and lower defect rates, thereby meeting export-grade standards. Market consolidation remains moderate, with top five players together holding under 45% of revenues, leaving scope for specialised newcomers focusing on nano-engineered layers for autonomous vehicles and photovoltaic upgrades.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The mirror coatings market report includes:

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.