Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

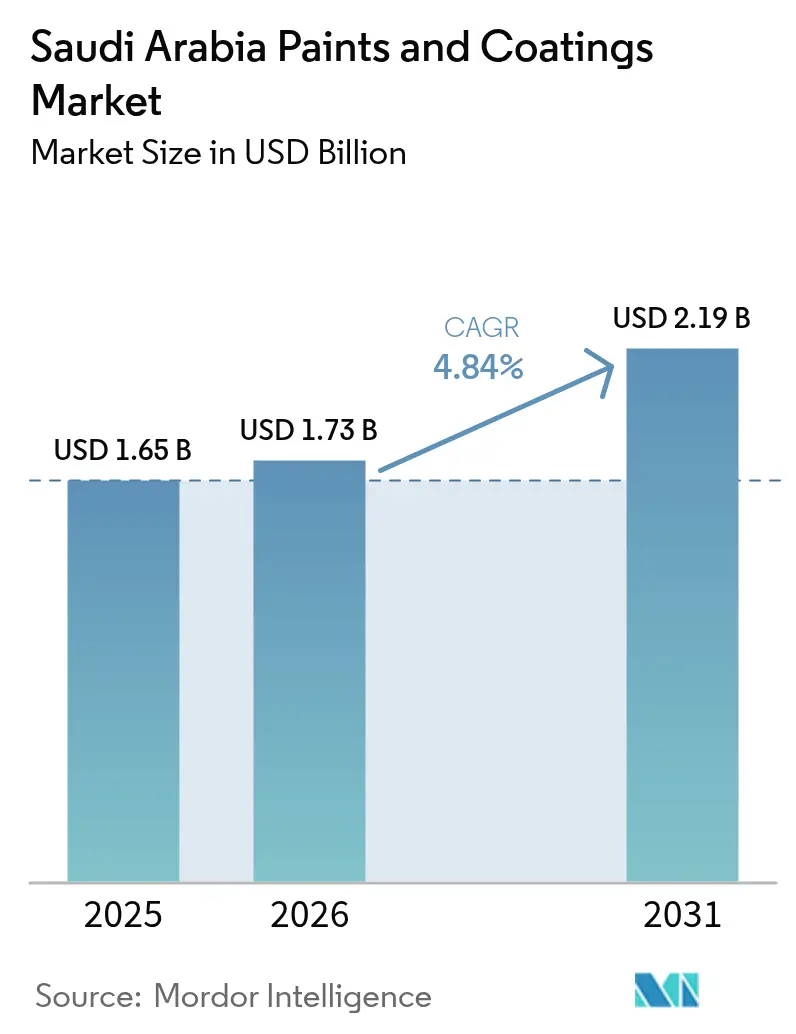

| Base Year Market Size (2025) | USD 1.65 Billion |

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.19 Billion |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Paints And Coatings Market Analysis by Mordor Intelligence

The Saudi Arabia Paints and Coatings Market size was valued at USD 1.65 billion in 2025 and estimated to grow from USD 1.73 billion in 2026 to reach USD 2.19 billion by 2031, at a CAGR of 4.84% during the forecast period (2026-2031). Robust public-sector spending under Vision 2030, tighter environmental rules, and rising localization levels are the main forces behind this increase. Landmark projects such as NEOM, King Salman International Airport, and Diriyah are generating sustained demand for high-performance architectural finishes, while the fast switch to low-VOC systems strengthens the position of water-borne and powder technologies. Strategic joint ventures led by Saudi Aramco and the Public Investment Fund are anchoring international know-how inside the Kingdom, creating fresh capacity for specialty resins and advanced protective chemistries. At the same time, volatile petrochemical feedstock costs and the rise of modular building methods are reshaping cost structures and application practices, compelling suppliers to tighten production efficiency and diversify raw-material sources.

Key Report Takeaways

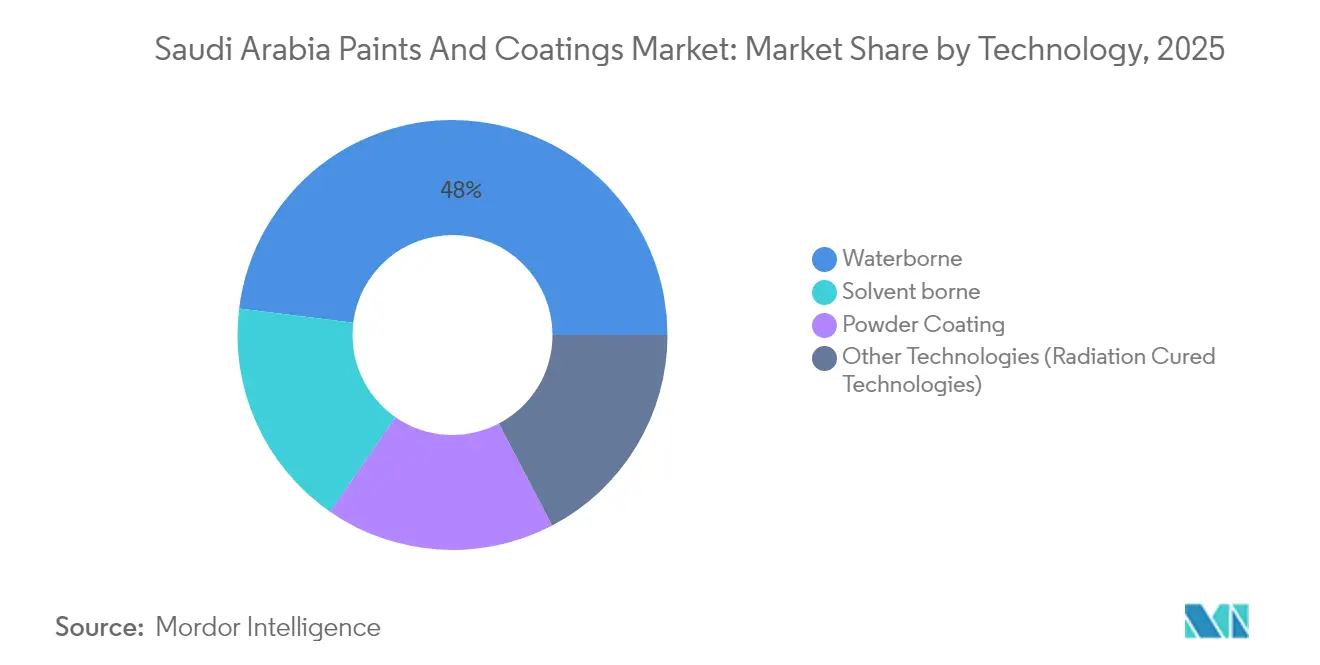

- By technology, water-borne products held 48.02% of the Saudi Arabia paints and coatings market share in 2025 and are forecast to deliver the highest 5.21% CAGR through 2031.

- By resin type, acrylic systems captured 48.43% of the Saudi Arabia paints and coatings market size in 2025 and are projected to grow at a 5.18% CAGR to 2031.

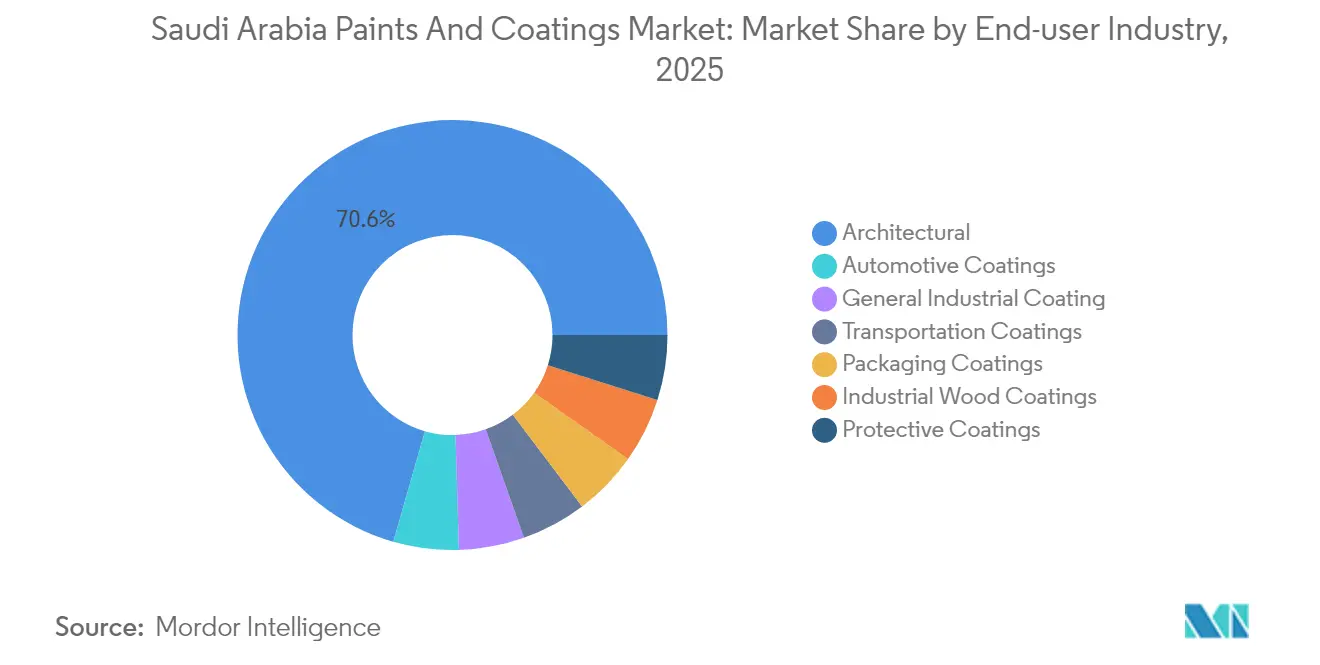

- By end-user industry, architectural applications led with 70.56% revenue share in 2025 and represent the fastest-growing category and are slated for a 5.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision-2030 infrastructure boom | +1.2% | National, with concentration in NEOM, Riyadh, and Eastern Province | Long term (≥ 4 years) |

| Mandatory local-content rules for coatings in oil and gas assets | +0.8% | Eastern Province and industrial cities (Jubail, Yanbu) | Medium term (2-4 years) |

| Rapid switch to water-borne and powder technologies to meet VOC caps | +1.0% | National, with stricter enforcement in industrial zones | Short term (≤ 2 years) |

| Giga-projects (NEOM, Red Sea) specifying solar-reflective façades | +0.6% | Northwestern regions (NEOM, Red Sea coastline) | Long term (≥ 4 years) |

| Localisation of pipeline and hydrogen-ready anti-corrosion coatings | +0.5% | Eastern Province and hydrogen corridor developments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision-2030 Infrastructure Boom

The Kingdom’s pipeline of 18,000 projects under Vision 2030 is the single largest demand catalyst, pushing the architectural share of the Saudi Arabia paints and coatings market to 71.12% in 2024[1]Saudi Press Agency, “Coating Namira Mosque Surroundings Lowers Temperatures,” spa.gov.sa. Projects such as the USD 147 billion King Salman International Airport require multi-layer coating systems able to endure dust abrasion, intense UV radiation, and thermal shock for 30-year design lives. Mixed-use developments alone add over 555,000 residential units and 275,000 hotel keys, translating into unprecedented volumes of primers, sealers, and high-solids decorative finishes. Underground civil assets like the Riyadh Metro drive uptake of abrasion-resistant epoxy linings that can withstand cyclic humidity and heavy passenger traffic[2]Abdullah AlQahtani et al., “Air Quality Levels in Jubail,” Frontiers in Environmental Engineering, frontiersin.org . This surge is reverberating across the Saudi Arabia paints and coatings market through stronger pull for alkali-resistant acrylics, zinc-rich anti-corrosion primers, and antimicrobial interior emulsions.

Mandatory Local-Content Rules for Coatings in Oil and Gas Assets

Saudi Aramco’s In-Kingdom Total Value Add program reached 43% localization in 2024 and targets 70% by 2030, rewarding suppliers that move resin synthesis, pigment dispersion, and canning inside Saudi Arabia. The shift is especially evident in fusion-bonded epoxy pipe coatings for the world’s largest seawater injection network, where domestic plants now fabricate internal linings that previously had to be imported. New hydrogen transmission lines mandate specialty polyamide-cured epoxies and thermally sprayed aluminum barriers, opening white-space for local SME formulators and multinationals willing to build Saudi production hubs. Technology-transfer clauses embedded in long-term framework agreements are turning the Eastern Province into a regional center of excellence for high-build anti-corrosion chemistries.

Rapid Switch to Water-Borne and Powder Technologies to Meet VOC Caps

The Environmental Law (Royal Decree M/165), effective January 2025, bans products exceeding strict VOC limits, prompting water-borne paints to seize 48.41% share of the Saudi Arabia paints and coatings market in 2024. Industrial estates in Jubail and Yanbu apply even tighter caps, accelerating the move to powder coatings whose 100% solids formulation eliminates solvent emissions. Factory applicators favor these powders for window frames, cladding, and data-center racks because faster curing reduces line energy use and boosts throughput. Nanocomposite powder technologies now incorporate silica-modified acrylics that improve scratch resistance and UV retention, making them suitable for premium façades exposed to sandstorms and 50 °C summer peaks.

Giga-Projects Specifying Solar-Reflective Façades

Climate-adaptive designs in NEOM and the Red Sea Project stipulate solar-reflective coatings that cut roof temperatures by 20 °C and slash annual cooling loads by up to 48.6%. These coatings combine high-albedo pigments with infrared-transparent binders, and some variants embed self-cleaning titania nanoparticles to counter dust deposition. Marine-grade polyurethane topcoats meeting ISO 12944 C5-M standards protect coastal resort assets against salt spray, while hydrogen-ready epoxy phenolic systems safeguard underground storage caverns. Successful qualification on giga-projects is quickly cascading to mainstream commercial builds, lifting overall specification standards across the Saudi Arabia paints and coatings market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petrochemical feedstock pricing | -0.7% | National, with concentration in petrochemical hubs (Jubail, Yanbu) | Short term (≤ 2 years) |

| Tightening VOC and hazardous-solvent regulation | -0.4% | National, with stricter enforcement in industrial and urban zones | Short term (≤ 2 years) |

| Emerging prefab-construction methods cutting paint consumption | -0.3% | Urban centers (Riyadh, Jeddah, Dammam) with modular construction adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Petrochemical Feedstock Pricing

Crude-to-chemicals integration is lowering Saudi naphtha exports, curbing solvent availability, and inflating input costs for alkyd and polyurethane producers. The Satorp and Yasref expansions will divert larger crude volumes into aromatics and olefins, magnifying cost swings for resin monomers such as styrene and butyl acrylate. Suppliers are therefore diversifying toward water-borne polyurethane dispersions and bio-based polyols that mitigate reliance on petrochemical streams. Risk hedging, through multi-month feedstock contracts with Aramco Trading, and lean inventory management have become critical to protect margins in the Saudi Arabia paints and coatings market.

Emerging Prefab-Construction Methods Cutting Paint Consumption

Modular builders like Prefabex assemble full wall panels in controlled factories, complete with primer and topcoat, reducing field painting work scopes by 20–30% on high-rise projects. These plants apply robot-sprayed, oven-cured powder systems that deliver uniform film builds and reduced rework. While total square-meter output of coatings declines on a per-unit basis, higher-value factory-grade formulations partially offset volume losses. Traditional distributors that rely on job-site deliveries are adapting by supplying specialized touch-up kits and color-matched repair aerosols compatible with off-site finishes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Dominance Accelerates Environmental Compliance

Water-borne products controlled 48.02% of the Saudi Arabia paints and coatings market share in 2025, advancing at a 5.21% CAGR through 2031 as specifiers pivot toward zero-to-low-odor work sites. Solvent-borne alkyds still prevail in high-temperature pipelines where fast drying and moisture tolerance are essential, but replacements are emerging via water-reducible alkyd emulsions. Powder coatings are expanding into façades, electrical enclosures, and stadium seating, aided by new super-durable polyester-acrylic hybrids that deliver 3,000-hour QUV resistance. Radiation-cured systems play a small yet growing role in furniture lines and plastic automobile parts needing tack-free handling in seconds.

Longer term, the Saudi Arabia paints and coatings market size linked to water-borne technology will rise as government ministries roll out public procurement policies mandating VOC-free interiors for schools and hospitals. Multilingual labeling and easy-clean attributes appeal to contractors responsible for maintaining the 120 million passenger-per-year King Salman Airport. Powder suppliers are preparing capacity expansions near Riyadh’s new dry port to capture architectural cladding demand, reinforcing the Kingdom’s ambition to act as an export node to the wider GCC.

By Resin Type: Acrylic Leadership Drives Versatility and Performance

Acrylic chemistries amassed 48.43% of the Saudi Arabia paints and coatings market size in 2025 on the back of exceptional UV durability and color fastness, and are advancing at a CAGR of 5.18%. Fast-drying styrene-acrylic emulsions today coat school halls and hospital corridors that must return to service overnight. Polyurethane systems dominate high-build roof membranes exposed to temperature cycling and occasional acid rain events generated by industrial clusters. Epoxy novolacs protect tank linings and offshore platforms, while polyester resins underpin the surge in TGIC-free powder exports to Africa.

Next-generation silicone-modified acrylics promise dirt-shedding exteriors for skyscrapers exceeding 400 m in Riyadh’s new CBD. Frontier research and development is focusing on graphene-enhanced acrylic binders that double tensile strength without sacrificing gloss, aligning with Vision 2030 initiatives to industrialize advanced carbon materials.

By End-User Industry: Architectural Segment Captures Infrastructure Boom Benefits

The architectural segment held a commanding 70.56% share of 2025 revenues, mirroring unprecedented new-build volumes across residential, hospitality, and mixed-use assets, and is advancing at a CAGR of 5.10%. Interior emulsions with formaldehyde-scavenging additives meet SASO indoor-air guidelines, while elastomeric exterior paints bridge façade hairline cracks caused by thermal cycling. Specialty solar-reflective roof membranes that lower heat-island effects are standard on LEED-certified hotels lining the Red Sea coast. Automotive coatings rank second in growth priority, supported by Hyundai’s 50,000-unit plant that will consume e-coat, basecoat, and clearcoat systems engineered for desert sand abrasion.

Protective coatings flourish around Aramco’s gas compression projects, where novolac epoxies and thermal-spray aluminum protect assets designed for a 50-year life. Industrial wood and packaging coatings ride the e-commerce wave, as Saudi furniture exporters and food processors raise product-appearance standards. Transportation coatings benefit from Riyadh Metro’s railcar refurbishments, requiring anti-graffiti clearcoats and low-smoke interior finishes compliant with EN45545.

Geography Analysis

The Eastern Province is seeing a growth in consumption owing to Jubail and Yanbu industrial cities, where heavy-duty primers, tank linings, and marine topcoats account for almost one-third of the Saudi Arabia paints and coatings market. Riyadh, boosted by mega-airport and metro works, represents the most dynamic pocket, fueling demand for low-odor, quick-turnaround interior systems suited to tight build schedules. Western Province tourism assets, notably the Red Sea luxury resorts, mandate ISO-12944 C5-M coatings capable of resisting chloride and sulfate attack, sustaining robust volumes of polyaspartic polyurethanes.

In the Northwest, NEOM’s USD 500 billion vision is rewriting specification books with net-zero embodied-carbon targets, positioning solar-reflective acrylics and hydrogen-compatible epoxies as default choices. The Southern mining belt, anchored by Maaden, spurs protective paint demand for phosphoric-acid tank farms and conveyor galleries. Central Province agriculture and solar PV push adoption of ultra-weatherable powder coatings on mounting structures. Each region’s distinct industrial mix underpins localized product portfolios, yet the overall Saudi Arabia paints and coatings market remains unified through national SASO standards and centralized raw-material supply chains.

Competitive Landscape

The market is moderately fragmented. Major players' research and development centers in Dammam and Jeddah fine-tune color spaces for desert illumination and sandstorm exposure. Jazeera Paints, National Paints, and Al-Jazeera Factory exhibit strong brand recognition in retail emulsion channels and benefit from Arabic label familiarity. Innovation races now orbit around hydrogen-ready coatings, super-durable powders, and AI-assisted color-matching applications. PPG’s SPEEDHIDE MAX zero-VOC range expanded to seven sheens, offering contractors higher tint strength with reduced odor. Localization depth, proven sand-storm durability, and digital color-spec support will separate winners from laggards over the next five years.

Saudi Arabia Paints And Coatings Industry Leaders

Jotun

Akzo Nobel N.V.

Hempel A/S

Jazeera Paints

Sigma Paints (PPG Industries Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Jazeera Paints announced its interior range now meets Ultra-Low VOC criteria to improve school and hospital indoor air quality.

- February 2025: Jazeera Paints signed an agreement with NHC to supply high-performance, sustainability-certified products across upcoming residential and commercial builds.

Saudi Arabia Paints And Coatings Market Report Scope

Paints and coatings are homogeneous mixtures of pigments, binders, additives, and various other components. Upon application on a substrate, these paints and coating make a thin layer of the solid film through polymerization or evaporation. Paints and coatings are widely used to improve aesthetics and protect the substrate from deterrents like corrosion and other types of deterioration. Saudi Arabia paints and coatings market is segmented by resin type (acrylic resin, alkyd resin, polyurethane resin, epoxy resin, polyester resin, and other resin types), technology (water-borne coatings, solvent-borne coatings, powder coatings, and other technologies), and end-user industry (architectural, automotive coatings, protective coatings, general industrial coatings, transportation coatings, and packaging coatings). The report offers market size and forecasts revenue (USD million) for the above segments.

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coating |

| Other Technologies (Radiation Cured Technologies) |

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types ?(Vinyl, Nitrocellulose, Latex) |

By End-user Industry

| Architectural |

| Automotive Coatings |

| Industrial Wood Coatings |

| Protective Coatings |

| General Industrial Coating |

| Transportation Coatings |

| Packaging Coatings |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder Coating | |

| Other Technologies (Radiation Cured Technologies) | |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types ?(Vinyl, Nitrocellulose, Latex) | |

| By End-user Industry | Architectural |

| Automotive Coatings | |

| Industrial Wood Coatings | |

| Protective Coatings | |

| General Industrial Coating | |

| Transportation Coatings | |

| Packaging Coatings |

Key Questions Answered in the Report

How large is the Saudi Arabia paints and coatings market in 2026?

The Saudi Arabia paints and coatings market size is USD 1.73 billion in 2026, with projections indicating USD 2.19 billion by 2031 at a 4.84% CAGR.

Which coating technology is growing fastest in Saudi Arabia?

Water-borne products are expected to post the fastest 5.21% CAGR through 2031, driven by zero-VOC mandates and energy-efficient curing advantages.

What segment dominates paint demand in Saudi Arabia?

Architectural applications account for 70.56% of total 2025 revenues owing to the Vision 2030 construction boom.

How are local-content rules impacting suppliers?

Saudi Aramco’s IKTVA program rewards companies manufacturing inside the Kingdom, already enabling 43% localization and targeting 70% by 2030.

What environmental laws shape product formulation?

Royal Decree M/165 imposes strict VOC caps effective 2025, accelerating the shift to water-borne and powder systems throughout the supply chain.

Page last updated on: