Low Friction Coating Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.57 Billion |

| Market Size (2031) | USD 4.83 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Friction Coating Market Analysis by Mordor Intelligence

Low Friction Coating Market size market size in 2026 is estimated at USD 3.57 billion, growing from 2025 value of USD 3.36 billion with 2031 projections showing USD 4.83 billion, growing at 6.22% CAGR over 2026-2031. Strong regulatory pressure on automotive fuel economy, rapid electrification, rising aerospace composite adoption, and an expanding satellite‐launch cadence anchor near-term demand. Manufacturers also benefit from sustained medical-device miniaturization trends and the need for space-qualified tribological solutions that perform in vacuum and extreme temperature conditions. Competitive intensity remains moderate as incumbents refine energy-efficient PVD and CVD processes while newcomers focus on PFAS-free chemistries to pre-empt tightening substance restrictions. The low friction coatings market therefore enters 2025 positioned for steady, regulation-linked expansion across multiple industrial value chains.

Key Report Takeaways

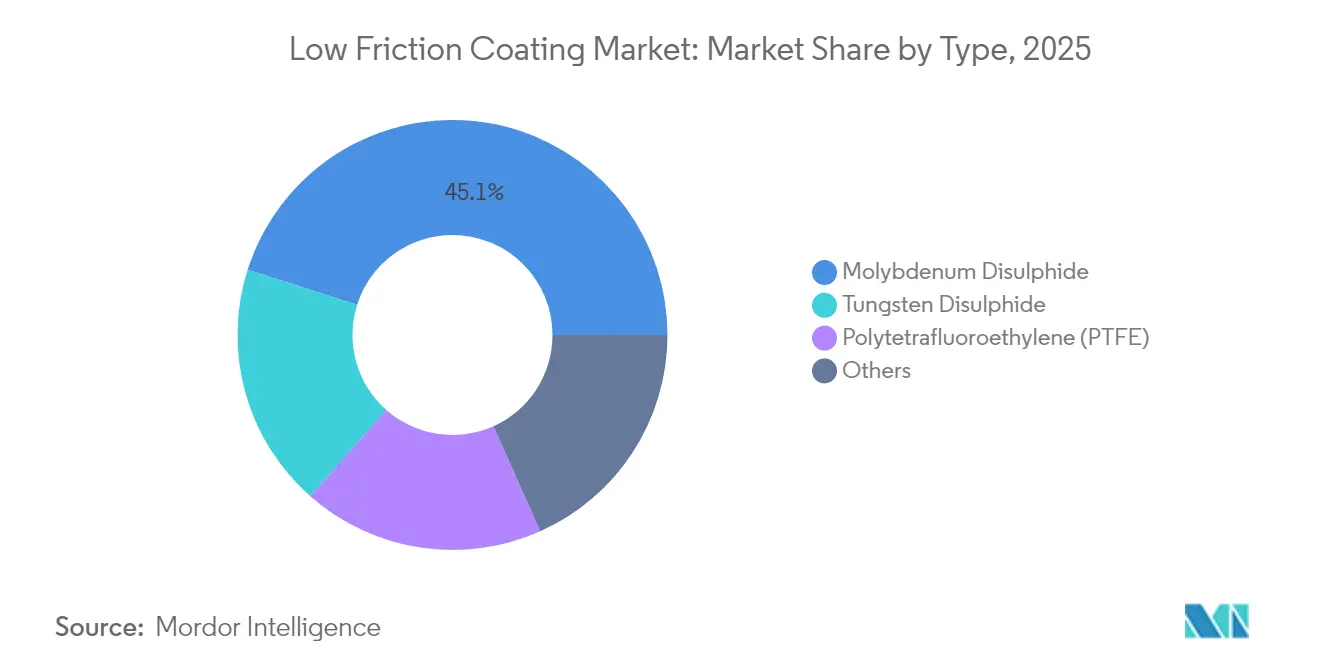

- By type, molybdenum disulfide accounted for 45.10% of the low friction coatings market share in 2025, whereas tungsten disulfide is set to pace the category with a 6.78% CAGR to 2031.

- By application, automotive parts captured 35.20% share of the low friction coatings market size in 2025 and is on course for a 7.05% CAGR through 2031.

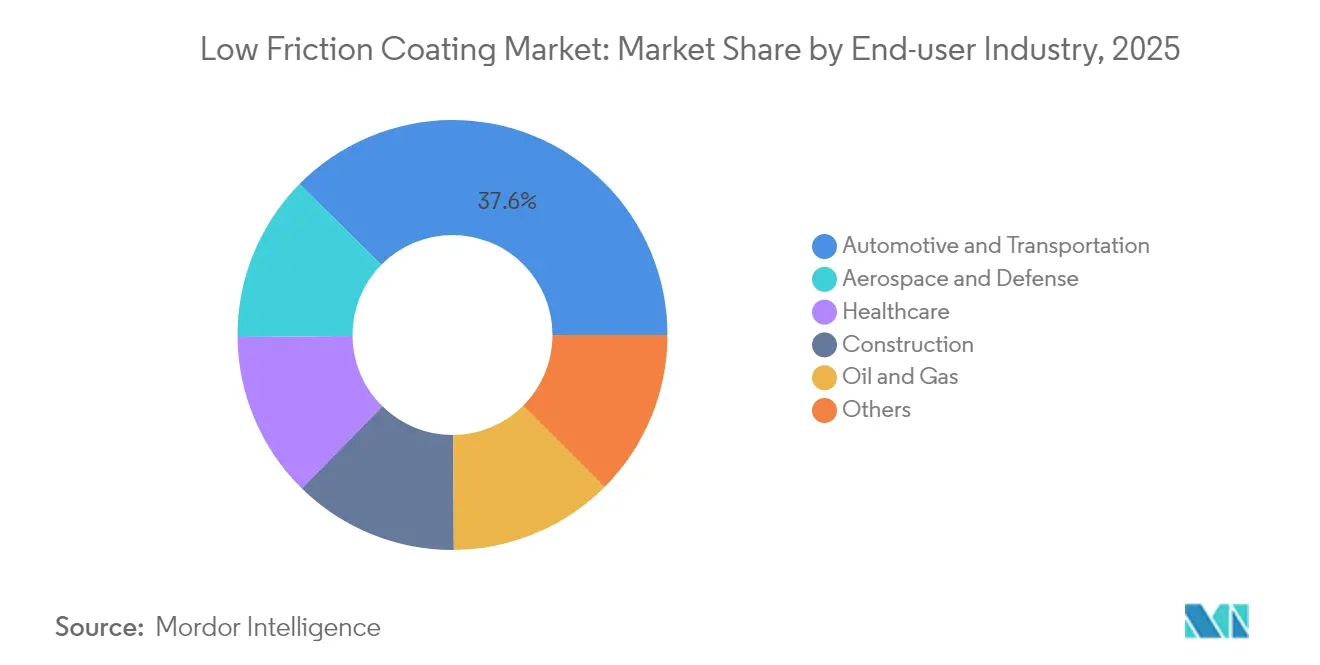

- By end-user industry, automotive and transportation held 37.60% revenue share in 2025 and is expected to grow at 7.12% CAGR through 2031.

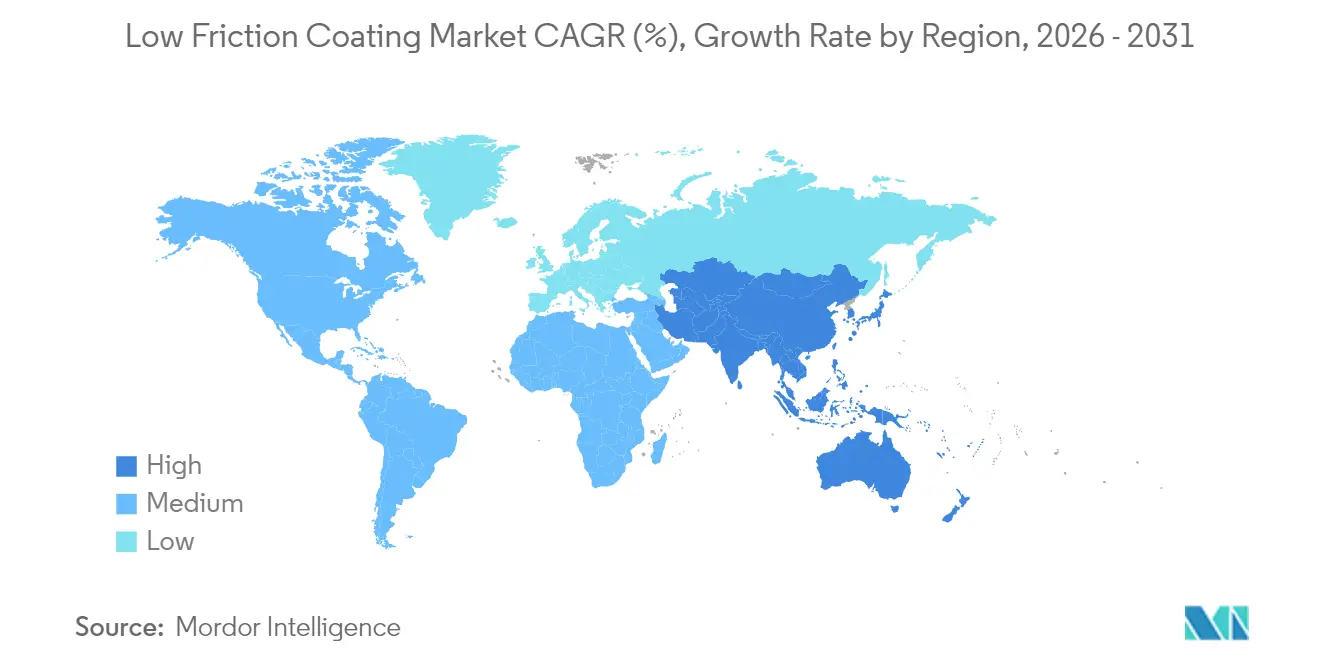

- By geography, Asia-Pacific led with 36.40% share in 2025 and is forecast to advance at a 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Low Friction Coating Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening automotive fuel-economy and EV range targets | +1.8% | Global, with strongest impact in North America and EU | Medium term (2-4 years) |

| Rapid growth of aerospace composite structures | +1.2% | North America, Europe, APAC core | Long term (≥ 4 years) |

| Push for medical-device miniaturisation | +0.9% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Expansion of high-speed e-axle bearings in EVs | +1.1% | APAC core, spill-over to North America and EU | Short term (≤ 2 years) |

| Satellite-constellation boom for space-qualified coatings | +0.7% | North America, Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Automotive Fuel-Economy and EV Range Targets

Global regulators now test axle efficiency under U.S. 40 CFR 1037.560, creating explicit performance thresholds that reward ultra-low friction surfaces[1]U.S. Environmental Protection Agency, “40 CFR 1037.560 — Axle Efficiency Test,” ecfr.gov. Automakers therefore specify coatings able to reach friction coefficients below 0.01, a figure once achievable only in laboratory settings. The switch to lower-viscosity oils intensifies surface-engineering needs because legacy lubricants no longer ensure boundary protection at reduced film thickness. EV drivetrain designers adopt similar coatings to trim parasitic losses and stretch battery range, especially in high-speed e-axles. Suppliers that can validate results across internal-combustion and electric architectures secure multi-platform platform sourcing agreements as fleet-average CO₂ caps ratchet downward in core markets.

Rapid Growth of Aerospace Composite Structures

Composite airframes shed weight but impose harsher load concentrations at bearing interfaces, elevating the value of solid-film lubricants that function in thin atmospheres. Molybdenum disulfide and tungsten disulfide deliver superlubricity in vacuum with friction coefficients nearing 0.003, enabling mechanisms such as solar-array drives to survive multiyear missions without service[2]NASA, “Gold Coating Keeps Oscars Bright,” nasa.gov. As megaconstellations multiply, each satellite may require dozens of coated components, magnifying aggregate demand. Space hardware also needs resistance to atomic oxygen and high-energy radiation, attributes that transition-metal dichalcogenide coatings supply with minimal mass penalty. Aircraft manufacturers transfer these coatings into non-pressurized fuselage sections, further expanding terrestrial uptake.

Push for Medical-Device Miniaturization

Minimally invasive surgery forces component diameters downward, which raises surface contact stress and frictional heat. Diamond-like carbon and titanium nitride films now dominate orthopedic articulations because they damp wear while limiting metal ion release in vivo. Atomic-layer-controlled PVD lets engineers tune hardness, elasticity, and surface energy at sub-micron scale so that micro-gears and valves operate smoothly inside catheters. Device makers also value the high corrosion resistance that solid films provide against disinfectant chemicals. Growing demand for ambulatory surgical solutions ensures a durable pipeline for biocompatible, low-friction surfaces across cardiovascular, neurological, and dental tool sets.

Expansion of High-Speed E-Axle Bearings in EVs

E-axle bearings spin faster and carry more electrical potential than legacy wheel hubs, exposing steel races to electrical pitting if surfaces lack insulation. Coatings incorporating transition-metal dichalcogenides paired with dielectric topcoats block stray currents while retaining low friction. Automakers endorsing all-electric portfolios by 2030 are already locking multiyear contracts for such films, aiming to guarantee drivetrain reliability out to 300,000 km duty cycles. Chemical suppliers respond with grease packages that suspend micro-coated particles, lowering start-up torque and widening temperature envelopes. Policy-driven EV adoption in Asia-Pacific accelerates early volume scale-up, in turn reducing cost for global rollout.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PFAS phase-out constraining PTFE formulations | -1.4% | Global, strongest in North America and EU | Short term (≤ 2 years) |

| Volatile Mo and W supply chain costs | -0.8% | Global, with acute impact in APAC manufacturing hubs | Medium term (2-4 years) |

| High energy intensity of PVD/CVD deposition | -0.6% | Global, particularly affecting high-volume applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PFAS Phase-Out Constraining PTFE Formulations

Multiple U.S. states ban intentionally added PFAS in consumer goods from 2025, while Canada has launched a phased prohibition that foreshadows broader restrictions. Traditional PTFE-based low friction coatings therefore face near-term disqualification in cookware, automotive, and electronics. Suppliers are reformulating around fluorine-free chemistries, yet replacements must match chemical inertness and temperature stability. Transition costs include asset re-validation, line cleaning, and customer re-qualification cycles. In parallel, European regulators prepare stricter registration rules that may further limit PFAS use, increasing compliance overhead for exporters.

High Energy Intensity of PVD/CVD Deposition

Producing dense, defect-free coatings via PVD or CVD demands vacuum systems that consume significant electricity. Rising power tariffs erode profitability for high-volume applications such as automotive fasteners. Plant managers explore magnetron sputtering enhancements and batch hybrid cycles that shorten pump-down time. Renewable energy sourcing eases the emissions profile but rarely reduces absolute cost. Process optimization and equipment upgrades therefore become gating factors for expanding capacity without sacrificing margin. Vendors offering higher throughput per kilowatt secure preference in new line tenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Molybdenum Disulfide Dominance Drives Innovation

Molybdenum disulfide held 45.10% of the low friction coatings market in 2025, underscoring its entrenched position in aerospace, automotive, and industrial machinery. Segment growth remains tied to proven performance under vacuum and boundary-lubrication regimes that defeat oil starvation. Hybrid spray and sputter systems now deposit crystalline films with sub-micron roughness, enabling carbon-fiber composite interfaces to withstand cyclical loads. Concurrently, tungsten disulfide advances at a 6.78% CAGR as designers prioritize high-temperature resilience above 400 °C. Its lamellar structure retains lubricity where molybdenum disulfide begins to oxidize, making it essential for hypersonic vehicle bearings and advanced turbine actuators.

Research teams mix both dichalcogenides with graphene platelets to create composite films that marry extreme heat tolerance with ultra-low friction. These multiphase structures better accommodate differential thermal expansion between metal substrates and polymer housings. PTFE variants lose share due to PFAS curbs, yet remain viable in sealed systems exempt from consumer-product rules. Suppliers that scale PFAS-free fluoropolymer analogs will capture replacement business as bans spread. Over the forecast window, material substitution dynamics are expected to narrow the molybdenum lead, though the tier will still command more than 40.20% by 2031.

By Application: Automotive Parts Lead Market Evolution

Automotive parts represented 35.20% of revenue in 2025 and will expand at a 7.05% CAGR to 2031, mirroring electrification’s surge. Driveline designers increasingly specify solid films on gears, splines, and e-axle shafts to cut lubricant viscosity and reduce fluid churning losses. Bearings form the second-largest application cluster, yet growth moderates as OEMs shift some demand into integrated driveline modules counted within the automotive category. Power transmission items benefit from improved torque capacity when coated surfaces suppress micro-welding under boundary conditions.

Valve components gain relevance in hydrogen-fuel platforms where gaseous media erode conventional seals. Meanwhile, actuators in robotics and semiconductor tools adopt vacuum-compatible coatings that keep particulate generation below ISO-Class 4 cleanroom limits. Collectively, these trends illustrate that application success hinges on tailoring deposition parameters to the service environment, a factor that favors coating houses with in-house tribology testing.

By End-User Industry: Automotive Sector Accelerates Adoption

Automotive and transportation accounted for 37.60% of the low-friction coatings market in 2025, reflecting broad application across pistons, fuel rails, e-axle bearings, and chassis hardware. The shift to battery electric vehicles heightens component rotational speeds and thermal gradients, raising the stakes for surfaces that minimize parasitic drag. Coatings help automakers meet fleet-average CO₂ targets and extend EV range without enlarging battery packs. Aerospace and defense preserve a smaller but high-value share anchored in space mechanisms and actuator systems requiring vacuum-stable lubricity.

Healthcare demand rises quickly as minimally invasive devices shrink; friction reduction allows smaller motors and gear trains to deliver precise motions in endoscopes. Construction, oil, and gas segments adopt hard films on hydraulic seals and drilling tools to prolong uptime in dusty or corrosive environments. Cross-industry technology transfer accelerates as coating suppliers leverage automotive economies of scale to lower unit cost for aerospace and medical customers. This interplay underscores why the low-friction coatings market maintains diversified growth pillars that reduce cyclicality.

Geography Analysis

Asia-Pacific led with a 36.40% share in 2025 and is projected to grow at a 6.98% CAGR through 2031. China’s large-scale BPA expansions provide resin feedstock cost advantages to regional formulators. The region hosts integrated automotive supply chains that rapidly adopt next-generation e-axle coatings, supported by government EV sales incentives. Japan leverages precision machining to deploy films onto hybrid power electronics, while South Korea capitalizes on domestic tungsten mining to localize high-temperature formulations. Regional collaboration among academic consortia accelerates pilot-line validation, reducing time-to-market for novel chemistries.

North America maintains a robust demand anchored in aerospace and advanced automotive programs. U.S. emission regulations and Department of Defense sourcing rules elevate scrutiny over PFAS and Chinese tungsten, prompting firms to build redundant supplier networks. Investment in space-launch infrastructure multiplies the need for vacuum-stable coatings, and Silicon Valley medical-device clusters create niche orders for miniaturized tribological solutions. Canada’s phased PFAS ban spurs early adoption of fluorine-free polymer films, positioning domestic suppliers ahead of upcoming EU rules.

Europe combines stringent sustainability mandates with enduring aerospace capability. Automakers headquartered in Germany and France lead global rollouts of PFAS-free e-axle bearing coatings that satisfy both REACH and carbon-footprint requirements. The European Space Agency’s Moon and Mars exploration roadmaps sustain long-life mechanism demand. Regional coating lines increasingly rely on renewable electricity, bolstering life-cycle assessments favored by end-users.

Value Chain Analysis

The low friction coating value chain begins with upstream feedstocks and actives, including fluoropolymers and fluorine-free polymer binders, solid lubricants such as molybdenum disulfide and tungsten disulfide, ceramic and carbon precursors for DLC-type systems, and specialty solvents and additives. These inputs move to formulators and brand owners, including anti-friction coating portfolios marketed under MOLYKOTE by DuPont, and to deposition and application specialists that operate PVD/CVD or spray and bake lines. Surface preparation is a key midstream step, since adhesion, thickness control, and particulate cleanliness often determine whether the coating can pass qualification for automotive drivetrain, aerospace, and medical components.

Downstream, coatings are supplied through direct contracts with OEMs and Tier suppliers, approved applicator networks, and in-house coating operations at component manufacturers. Qualification and audit requirements, including automotive platform approvals and aerospace quality expectations, raise switching costs and favor suppliers that package coating materials, process parameters, and test validation as an integrated offering, rather than selling coating material alone through distributors. Bottlenecks center on volatile molybdenum and tungsten costs, energy-intensive vacuum deposition capacity, and reformulation and re-qualification work as PFAS restrictions reduce PTFE-based options in some end uses.

Competitive Landscape

The low-friction coatings market displays moderate fragmentation. Leading players differentiate through proprietary target alloys, high-rate sputtering cathodes, and in-process plasma diagnostics that shorten development cycles. Equipment vendors innovate toward circular manufacturing. SKF released the first bearings designed for circular performance, highlighting coatings engineered for multiple life cycles. Raw-material volatility drives vertical integration. Producers secure molybdenum and tungsten offtake agreements and explore recycling of spent coatings via plasma stripping processes that reclaim metals. Energy efficiency remains a parallel battleground as magnetron architectures evolve toward higher power densities per chamber, trimming kilowatt-hours per square meter coated.

Low Friction Coating Industry Leaders

The Chemours Company

DuPont

Klüber Lubrication

PPG Industries, Inc.

Daikin Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity is PFAS-free substitution, where tightening substance restrictions constrain PTFE-based low friction systems and push OEMs and applicators to requalify non-fluorinated binders and solid-lubricant-rich dry films for automotive parts and industrial mechanisms. That demand pull is reinforced by drivetrain efficiency targets that favor ultra-low friction surfaces in high-speed e-axles and in axle efficiency testing environments. Suppliers that pair materials with application support can reduce customer re-qualification cycles by providing validated process windows, tribology testing, and contamination-controlled application services.

Capacity and localization opportunities are strongest where end-use growth is concentrated and lead times matter, particularly in Asia-Pacific manufacturing hubs. In Asia-Pacific manufacturing hubs, end-use growth supports regional supply. In August 2024, PPG commissioned five new production lines at its Petaling Jaya, Malaysia facility to produce waterborne and solventborne low-friction and non-stick coatings, highlighting investment in flexible production that can meet diverse specifications across industrial and consumer applications. On the technology side, 2026 research activity around 2D and carbon-based nanocomposites, including MoS2-enabled superlubricity and multifunctional corrosion-resistant low-friction networks, points to a pipeline of performance upgrades that suppliers can translate into next-generation coatings for harsh environments, vacuum-compatible mechanisms, and miniaturized medical components.

Recent Industry Developments

- June 2026: DuPont announced expansion of MOLYKOTE coatings capacity at its North American facility to meet rising demand from automotive and industrial customers. The move strengthens regional supply resilience and reduces qualification lead times for new powertrain programs. It signals sustained emphasis on dry film and anti-friction solutions within end-use markets.

- December 2025: PPG renewed its regional distribution partnership with CHIME Performance Polymers Private Limited to accelerate deployment of MOLYKOTE coated products in APAC. The arrangement enhances regional testing capabilities and speeds onboarding of new customers across automotive and industrial segments. The collaboration underscores ongoing efforts to shorten qualification cycles through integrated material and service offerings.

- May 2024: DuPont introduced MOLYKOTE D-6804 and MOLYKOTE D-6818 low-friction coatings targeting wear resistance in alternative fuel environments. The launch expands options for designers facing higher loads and changing lubrication regimes in modern powertrains, and it helps DuPont defend specification positions as OEMs update materials for efficiency and durability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the low friction coating market is the value of specialty coating materials and applied coating services designed mainly to reduce sliding friction, wear, and sticking on parts across industrial and mobility uses.

Scope exclusions: It excludes conventional liquid lubricants and greases, and it also excludes coatings sold only for corrosion protection or decoration when friction reduction is not the primary performance need.

Segmentation Overview

- By Type

- Molybdenum Disulphide

- Tungsten Disulphide

- Polytetrafluoroethylene (PTFE)

- Others

- By End-user Industry

- Automotive and Transportation

- Aerospace and Defense

- Healthcare

- Construction

- Oil and Gas

- Others

- By Application

- Bearings

- Automotive Parts

- Power Transmission Items

- Valve components and Actuators

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Thailand

- Indonesia

- Malaysia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Russia

- Spain

- Turkey

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Qatar

- United Arab Emirates

- Egypt

- Nigeria

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to map where low friction coatings are consumed and how demand moves with part production and maintenance cycles. We typically refer to public sources such as USGS for molybdenum and tungsten supply signals, the US International Trade Commission trade statistics for selected chemical and polymer categories, the US Patent and Trademark Office for coating and tribology patent activity, and the National Institutes of Health and other peer reviewed journals for device and material performance trends.

On the industry side, company annual reports, investor presentations, and product technical datasheets help validate which coating chemistries are being pushed into bearings, valve components, and power transmission parts. For pricing and shipment logic, we also use paid subscriptions for company financials and intelligence, patent databases, and shipment level import and export data where it supports cross checks. The specific list above is illustrative only, and many other public and subscription sources were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test the desk assumptions on where coatings are specified, how coating thickness and process choice affect cost, and how demand splits between OEM production and maintenance. We spoke with a mix of coating formulators, applicators, distributors, and end user engineering and sourcing contacts, and coverage was balanced across APAC, EMEA, and the Americas so regional manufacturing intensity was not over or under stated.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 41% |

| Mid tier: 58% | Functional/Unit leaders: 39% | EMEA: 34% |

| Smaller Players: 15% | Managers: 49% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where production, installed base, and maintenance intensity are used to reconstruct a realistic demand pool for coated parts, which is then converted into value using typical coating loads and average selling prices. To keep totals grounded, results are corroborated with selective bottom-up checks such as sampled supplier and applicator revenue cues, channel checks on throughput, and a simple ASP times volume approximation for common applications like bearings and valve components.

Key inputs in the model include automotive and industrial output trends, aerospace build and overhaul indicators, adoption of dry film or PTFE based solutions versus wet lubrication, typical coating thickness and recoat intervals, and raw material price direction for PTFE and disulfide based chemistries. Where a bottom-up trail is weak, for example small job-shop activity, gaps are handled using ratio based scaling from better disclosed regions and then reviewed with primary feedback.

Forecasting uses scenario analysis supported by expert consensus around electrification related part design changes, PFAS related substitution timing for certain fluoropolymer systems, and industrial capex cycles, and this is combined with smoothing on historical demand signals to avoid overreacting to one off shocks.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, so model outputs are compared against raw material movement, trade flows, and realistic application level penetration rates. When variances look high, assumptions are rechecked, and follow-up calls are triggered with respondents who are closest to pricing and coating line utilization. Before sign-off, a multi-step analyst review is run to catch anomalies in units, currency conversion timing, and region splits.

The report is refreshed annually, and interim updates are added when major events change demand or pricing direction. Right before delivery, a fresh pass is completed so clients receive the most recent view that matches the latest data pulls and interview learnings.

Mordor Intelligence's Low Friction Coating Market Size Compared With Other Published Estimates

Published market sizes for low friction coatings can look far apart because each publisher draws the line differently around what counts as a low friction solution and how much service value is included. Differences also come from the base year chosen, the way ASP is trended, and whether the number is anchored to realistic application adoption or to broader coatings revenue pools.

The biggest gap tends to come from whether adjacent surface treatments and general purpose polymer coatings are rolled in, where Mordor Intelligence counts revenue only when the coating is specified for friction reduction on applications like bearings, automotive parts, or valve components, and then validated using application level penetration checks and regional manufacturing signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.57 B (2026) | |

| Industry Publisher A | USD 3.40 B (2025) | Uses a different base year and a longer forecast window, and the scope description suggests broader inclusion of low friction solutions across more end uses, which can shift the value captured per application. |

| Industry Publisher B | USD 0.66 B (2024) | Appears to focus on a narrower tracked revenue pool tied closely to reported shipments and a limited set of product categories, which can exclude applied coating services and some higher value application areas. |

The table shows that most of the spread is explained by scope and measurement choices, rather than a single demand driver. By keeping the demand pool tied to coated part use cases, checking penetration and recoat behavior, and applying consistent currency timing, our estimate stays traceable to inputs that a reader can follow and replicate.

Key Questions Answered in the Report

What is the projected value of the low friction coatings market by 2031?

The market is expected to reach USD 4.83 billion by 2031, reflecting a 6.22% CAGR.

Which region leads demand for low friction coatings in 2025?

Asia-Pacific accounts for 36.40% of global revenue, buoyed by automotive electrification and manufacturing scale.

Which coating type holds the largest share today?

Molybdenum disulfide leads with 45.10% share due to proven aerospace and automotive performance.

Why are PFAS-free coatings gaining traction?

Regulatory bans on PFAS in North America and Europe are phasing out traditional PTFE films, pushing suppliers toward fluorine-free alternatives.

How does electrification influence coating selection?

High-speed e-axles and elevated thermal loads in EVs require ultra-low friction, electrically insulating coatings to preserve efficiency and component life.

Page last updated on: