Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

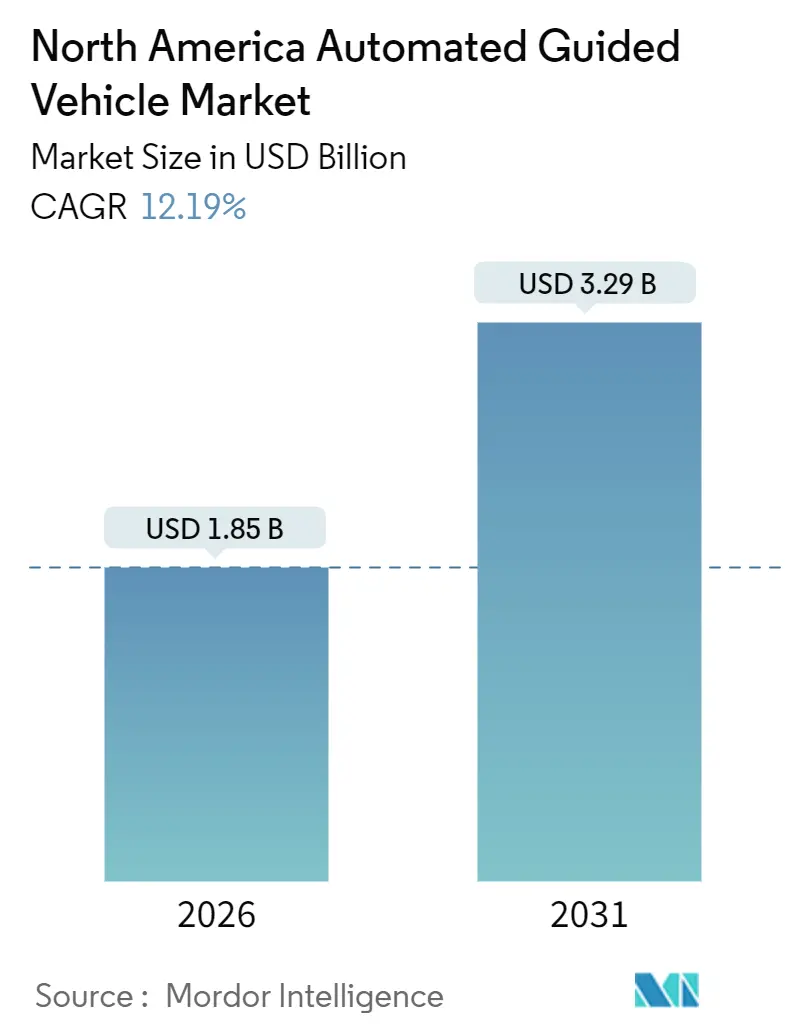

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 3.29 Billion |

| Growth Rate (2026 - 2031) | 12.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automated Guided Vehicle Market Analysis by Mordor Intelligence

The North America automated guided vehicle market size is valued at USD 1.85 billion in 2026 and is projected to reach USD 3.29 billion by 2031, advancing at a 12.19% CAGR. E-commerce fulfillment density, electric-vehicle assembly complexity, and rising labor costs are expanding capital budgets for warehouse and factory automation, while AI-enabled fleet orchestration shortens payback periods by coordinating mixed fleets inside existing facilities. Brownfield retrofits now outnumber greenfield projects because software layers allow legacy fixed-path vehicles and new vision-guided units to share tasks, minimizing building modifications. Laser guidance remains dominant for heavy-duty routes, yet camera-based navigation is scaling quickly as sensor prices fall and open-source SLAM toolkits simplify integration. Power-train choices are shifting in parallel: lithium-ion packs are displacing lead-acid on lifetime-cost grounds, especially in continuous-shift warehouses. Collectively, these trends are stabilizing deployment risk and deepening penetration across logistics, manufacturing, and cold-chain environments, reinforcing a positive outlook for the automated guided vehicle (AGV) market.

Key Report Takeaways

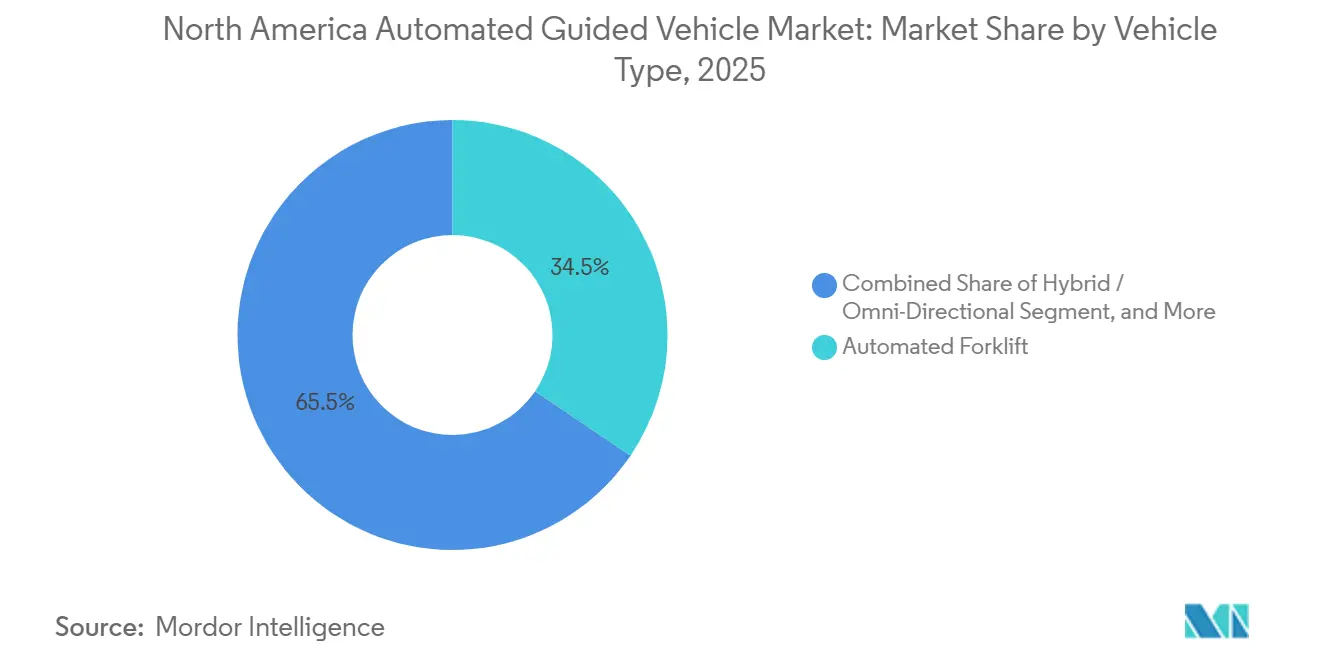

- By vehicle type, automated forklifts held a 34.49% automated guided vehicle market share in 2025. Hybrid and omni-directional vehicles are forecast to expand at a 12.94% CAGR through 2031.

- By navigation technology, laser guidance led with 58.11% revenue share in 2025. Vision and SLAM guidance are projected to grow at a 12.55% CAGR to 2031.

- By component, hardware captured 62.24% of spending in 2025. Software is advancing at a 13.11% CAGR through 2031.

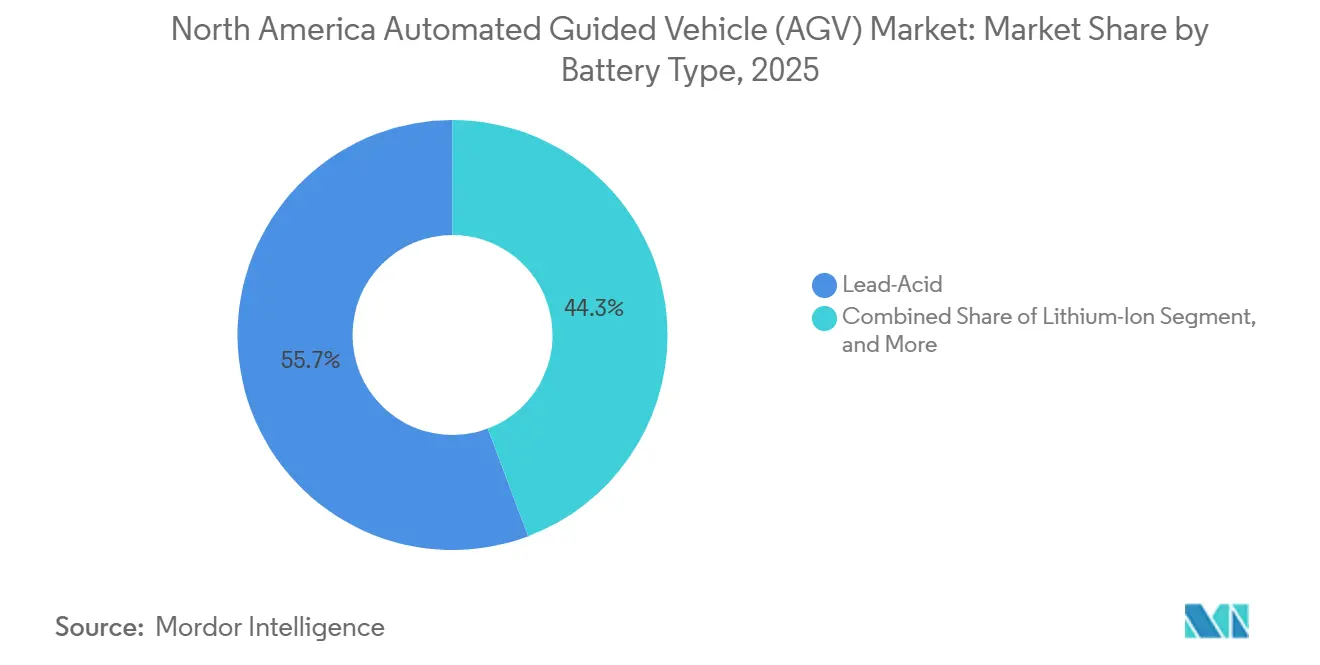

- By battery type, lead-acid retained a 55.74% share in 2025. Lithium-ion batteries are poised to rise at a 13.31% CAGR by 2031.

- By end-user industry, automotive commanded 30.10% demand in 2025. Logistics and warehousing are expected to post a 12.74% CAGR through 2031.

- By geography, the United States accounted for 82.39% of 2025 revenue. Mexico is set to record a 13.53% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Automated Guided Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Fulfillment Boom Accelerating Warehouse Automation Adoption | +2.80% | United States (primary), Canada (secondary), Mexico (emerging) | Short term (≤ 2 years) |

| Rising Labor Costs and Shortages in U.S. and Canadian Logistics Hubs | +2.30% | United States and Canada, concentrated in Midwest and Ontario | Medium term (2-4 years) |

| Automotive OEM Re-tooling for EV Platforms Demanding Flexible Material Flow | +1.90% | United States (Michigan, Tennessee, Kentucky), Canada (Ontario), Mexico (Nuevo León, Guanajuato) | Medium term (2-4 years) |

| Stricter Workplace-Safety Regulations Mandating Ergonomic Material Handling | +1.40% | United States (OSHA jurisdiction), Canada (provincial labor codes) | Long term (≥ 4 years) |

| Expansion of U.S. On-shoring Incentives Fueling Greenfield Smart-Factory Builds | +1.60% | United States (Rust Belt, Southeast), Mexico (border states) | Long term (≥ 4 years) |

| AI-Enabled Fleet Orchestration Unlocking Multi-Robot ROI in Brownfield Sites | +2.00% | United States (brownfield retrofits), Canada (limited), Mexico (greenfield integration) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfilment Boom Accelerating Warehouse Automation Adoption

Rising same-day delivery expectations are pushing 3PLs and retailers to upgrade legacy facilities with goods-to-person workflows powered by AGVs. Amazon deployed more than 750,000 mobile robots by late 2024 and continues to scale fleets to meet order-cycle targets. Walmart invested USD 200 million in automated forklifts across 42 regional DCs in 2024, targeting a 30% drop in injury rates. As U.S. online retail penetration reached 16.3% of total sales in 2025, AGV installations clustered in Texas, California, Pennsylvania, and Ohio, where fulfillment density justifies capital intensity. The automated guided vehicle market benefits from this shift away from conveyor-bound sortation toward mobile systems that flex with SKU proliferation. With Canada and Mexico following similar trajectories, albeit at lower e-commerce baselines, the driver remains the single largest uplift to near-term demand.

Rising Labor Costs and Shortages in Logistics Hubs

Median hourly wages for U.S. material movers climbed to USD 17.85 in 2025, a 22% increase since 2020, while vacancy rates in inland logistics corridors topped 8% despite signing bonuses. Automation economics now favor replacing two full-time positions with one lithium-ion forklift at a capital cost of USD 80,000, yielding payback inside 24 months. Turnover costs compound savings, as each employee exit can cost 50% to 60% of annual salary in recruitment and downtime. Consequently, the automated guided vehicle market is widening the competitive divide between large operators with cheap capital and mid-sized firms struggling to self-finance. Canada shows identical wage inflation patterns in Ontario’s Golden Horseshoe region, while Mexico’s labor cost advantage tempers but does not negate automation pull, especially for export-oriented factories.

Automotive OEM Re-Tooling for EV Platforms Demanding Flexible Material Flow

Ford allotted USD 5 billion to modernize Michigan and Tennessee plants in 2024, embedding vision-guided AGVs that reroute battery trays in real time. General Motors orchestrated 120 mixed-fleet vehicles at Spring Hill in 2025, cutting staging time by 35%. Stellantis introduced omni-directional carriers in Ontario to maneuver oversized packs through constrained aisles. Battery modules worth USD 10,000 to USD 15,000 require gentle handling, and AGVs deliver sub-centimeter accuracy while mitigating human-error risk. Mexico’s new EV factories in Nuevo León and Guanajuato are designing AGV lanes from day one, illustrating how nearshoring and electrification jointly lift the automated guided vehicle market.

AI-Enabled Fleet Orchestration Unlocking Multi-Robot ROI in Brownfield Sites

Machine-learning platforms now allocate tasks, schedule charging, and predict maintenance across heterogeneous fleets, lifting throughput by nearly 30% without adding hardware. Locus Robotics secured USD 150 million in 2025 to globalize its SaaS orchestration layer. OTTO Motors demonstrated a 40% productivity gain coordinating 80 cross-brand vehicles at a Michigan auto supplier. By abstracting navigation differences, software lets operators prolong legacy assets, smoothing capex and densifying adoption curves. For the automated guided vehicle market, this driver sustains double-digit growth even in facilities with existing automation footprints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front System and Integration Costs for Mid-Sized Warehouses | -1.70% | United States (regional distribution centers), Canada (secondary markets) | Short term (≤ 2 years) |

| Intermittent Wireless Dead-Zones in Large Metal-Dense Facilities | -0.90% | United States (automotive, heavy manufacturing), Mexico (aerospace, automotive) | Medium term (2-4 years) |

| Limited Skilled Technicians for AGV Maintenance in Secondary Cities | -1.10% | United States (Tier 2 and Tier 3 cities), Canada (outside Greater Toronto Area), Mexico (interior states) | Long term (≥ 4 years) |

| Emerging AMR Alternatives Cannibalizing Fixed-Path AGV Spending | -1.50% | United States (e-commerce, third-party logistics), Canada (limited), Mexico (minimal) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front System and Integration Costs for Mid-Sized Warehouses

A turnkey AGV deployment in a 200,000 square-foot facility can require USD 1.5 million to USD 2.5 million before workflow engineering and staff training. Integrators often add 30% to 40% for customization and safety validation, stretching payback beyond five years for operators with revenue below USD 50 million. Short lease terms in U.S. distribution real estate, averaging six years, further hinder amortization. As a result, automation density remains concentrated among large enterprises, slowing penetration of the automated guided vehicle market in the mid-tier segment. Vendors responding with modular, infrastructure-light offerings could soften this drag over the forecast window.

Emerging AMR Alternatives Cannibalizing Fixed-Path AGV Spending

Vision-guided autonomous mobile robots entered North America with 35% year-on-year shipment growth in 2024, dwarfing AGV unit gains. Chinese entrants such as Geek+ price systems 30% below European rivals, tempting e-commerce operators that refit floor layouts seasonally. While AGVs still dominate loads above 1,500 kilograms, AMRs threaten pallet-handling niches that favour route flexibility. The cannibalization risk is most acute for general warehouses in the United States, where lease constraints discourage fixed infrastructure, placing downward pressure on certain pockets of the automated guided vehicle market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Forklift Dominance Meets Omni-Directional Agility

Automated forklifts retained 34.49% of 2025 revenue as factories replaced diesel units with lithium-ion models to satisfy OSHA air-quality rules and slash maintenance downtime. This mature cohort underpins the North America automated guided vehicle market, yet hybrid and omni-directional carriers are emerging with a 12.94% growth trajectory fueled by cold-storage and pharma demand for lateral motion. Tow and tugger trains remain staples in automotive kitting, whereas unit-load carriers automate inbound pallet transfers in cross-docks. Assembly-line vehicles, fitted with lift tables and vision sensors, secure battery packs with millimeter precision. Special-purpose machines serve hazardous and cleanroom niches, justifying premium margins and buffering vendors against price-led competition.

During 2025-2026, manufacturers began pairing collaborative arms with mobile bases, converting transport platforms into manipulation systems that pick or inspect components on the fly. Toyota’s cobot-equipped forklift debuted in 2025, signaling a convergence of mobility and dexterity that could compress fleet sizes. Lithium-ion retrofit kits broaden upgrade options, while predictive-maintenance software pushes uptime toward 98%, reinforcing the North America automated guided vehicle market’s shift from capital purchase to performance subscription.

By Navigation Technology: Laser Incumbency Faces Vision Disruption

Laser guidance owned 58.11% of 2025 revenue thanks to proven reflector grids in high-throughput automotive and food plants. Still, camera-based vision and SLAM platforms are expanding at a 12.55% CAGR as image-sensor costs fall and open-source libraries mature. Operators in leased distribution centers favour infrastructure-free navigation to avoid landlord approvals, propelling vision adoption. Magnetic and inductive lines linger in outdoor mills and metal-dense environments where reflections or dust confound optics. Natural navigation blends GPS, IMU, and lidar for port yards and container terminals, providing bridge technology between indoor and outdoor zones.

Competitive intensity is reshaping price curves. Chinese vendors use low-cost cameras to undercut European laser players, compelling incumbents to emphasize software differentiation. OTTO Motors achieved sub-10-millimeter precision by fusing cameras with lidar, proving parity with lasers in structured aisles. As multi-sensor fusion matures, the North America automated guided vehicle market may see a gradual phase-out of reflector maintenance budgets, freeing opex for fleet expansion.

By Component: Hardware Revenue Dominance Yields to Software Subscription Growth

Hardware captured 62.24% of 2025 spend, reflecting heavy chassis, drive trains, and sensing suites. Fleet refresh cycles, especially swapping lead-acid packs for lithium-ion, kept hardware billing strong. Yet software revenue is set to climb 13.11% annually through 2031 as subscription models tie vendor income to uptime and throughput. Locus, Seegrid, and OTTO offer per-vehicle or per-task fees, embedding AI analytics, traffic management, and cybersecurity updates in recurring contracts. Services, while the smallest slice, benefit from operators outsourcing 24/7 monitoring and predictive maintenance.

For buyers, the pivot toward SaaS reallocates capital outlay into operating budgets, reducing hurdle rates and broadening eligibility for mid-market adopters. Vendors gain stickier relationships and data-driven upsell pathways. As multi-site operators demand enterprise dashboards, interoperability APIs become decision criteria, anchoring software’s centrality to the automated guided vehicle market.

By Battery Type: Lead-Acid Incumbency Erodes as Lithium-Ion Economics Improve

Lead-acid held 55.74% share in 2025, anchored by lower sticker prices and a legacy fleet tuned to its voltage curves. However, opportunity charging, longer cycle life, and floor-space liberation tilt economics toward lithium-ion, now growing 13.31% annually. Pack prices fell 20% in 2024 on lithium-iron-phosphate overcapacity, slicing payback to two years in 24-hour operations. Retrofit kits from Toyota and Jungheinrich cut changeover cost, accelerating swap-out cycles. Nickel-cadmium cells serve sub-zero warehouses, whereas hydrogen fuel cells stay experimental, hampered by USD 50,000-plus unit prices and scant fuelling networks.

Regulatory catalysts could accelerate zero-emission mandates, but today economics alone is driving migration. As lead-acid fades, vendors embedding battery-analytics software capture additional subscription revenue, further reinforcing the service-heavy direction of the North America automated guided vehicle market.

By End-User Industry: Automotive Leadership Faces Logistics Surge

Automotive accounted for 30.10% of demand in 2025, buoyed by EV platform refits requiring flexible, heavy-payload movement. Decades-old conveyor lines give way to vision-guided carriers that accommodate varied battery geometries. Yet logistics and warehousing is on track for a 12.74% CAGR, lifted by peak-season scalability needs at Amazon, Walmart, DHL, and UPS. Food and beverage operators automate sub-zero pallet moves to curb exposure times, while electronics assemblers deploy cleanroom AGVs that avoid electrostatic discharge. Healthcare institutions use unit-load vehicles for pharmacy delivery, freeing clinical staff for patient care.

The automated guided vehicle market thus evolves into a portfolio play: heavy-duty precision in automotive, high-velocity flexibility in e-commerce, and specialized compliance in cold chain and healthcare. Vendors aligning roadmaps to vertical pain points are positioned to outpace generic hardware suppliers.

Geography Analysis

The United States dominated the North America automated guided vehicle market with an 82.39% revenue share in 2025. Amazon’s 750,000-plus mobile robots exemplify scale, while Walmart’s USD 200 million forklift rollout underscores mainstream retail adoption. Onshoring incentives under the CHIPS and Science Act motivate semiconductor and battery plants in the Midwest and Southeast to embed AGV lanes during construction. Up-front integration costs remain a barrier for mid-sized warehouses on six-year leases, leaving growth concentrated among corporates with balance-sheet strength.

Mexico is the region’s growth pacesetter at 13.53% CAGR, propelled by nearshoring, labor arbitrage, and EV investment corridors. Tesla’s USD 5 billion Nuevo León plant will integrate AGVs from day one, and BMW and GM follow similar blueprints. Aerospace clusters in Baja California and electronics hubs in Jalisco extend adoption beyond automotive. Nevertheless, capital and skills gaps among domestic small-to-medium enterprises limit nationwide diffusion, keeping volume centered in multinational greenfield.

Canada’s market growth trails its neighbors, bound by fewer large facilities and the absence of U.S.-level automation tax credits. Ontario’s EV supply chain leverages AGVs for battery module staging, and 3PL pilots in Quebec aim to mitigate warehouse labor shortages. Cross-border parent companies dictate platform choices, driving harmonization but capping independent momentum. Overall, geographic expansion of the automated guided vehicle market mirrors investment incentives and industrial footprints across North America.

Competitive Landscape

The North America automated guided vehicle market is moderately fragmented: the top five suppliers, Daifuku, Dematic, Toyota Material Handling, Jungheinrich, and Swisslog, collectively hold roughly 45% to 50% revenue. Dematic’s 2024 purchase of Reddwerks added orchestration software, evidencing a pivot toward end-to-end solutions.

Venture-backed challengers such as Locus Robotics, Seegrid, and OTTO Motors raised more than USD 300 million since 2024, pairing subscription pricing with rapid deployment for e-commerce hubs. Chinese entrants like Geek+ and Quicktron discount hardware by up to 40%, compressing margins and pushing incumbents toward services and vertical integration.

Technology competition now centers on AI fleet intelligence, cobot integration, and battery analytics. OTTO’s cobot-armed carrier performed pick-and-place at a Michigan auto supplier in 2025, consolidating tasks and improving capital efficiency. Service portfolios, from 24/7 remote monitoring to predictive spare-parts logistics, are emerging as key differentiators as hardware commoditizes. With no single player above a 20% share, the market remains open for consolidation and specialization.

North America Automated Guided Vehicle Industry Leaders

John Bean Technologies Corporation

Seegrid Corporation

Toyota Material Handling

Swisslog Holding AG (KUKA AG)

Daifuku Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Locus Robotics raised USD 150 million Series F to extend AI orchestration across North America and Europe.

- November 2024: Ford committed USD 5 billion to EV plant overhauls in Michigan and Tennessee, fully integrating vision-guided AGVs.

- October 2024: Walmart invested USD 200 million in automated forklifts across 42 DCs for faster order cycles.

- September 2024: Dematic acquired Reddwerks to merge AGV hardware and warehouse-management software under one platform.

North America Automated Guided Vehicle Market Report Scope

Automated guided vehicles (AGVs) are fully automated transport systems with unmanned vehicles. Automated guided vehicles offer many advantages, such as reduced operational costs, enhanced workforce safety, and decreased production time.

The North America Automated Guided Vehicle (AGV) Market Report is Segmented by Vehicle Type (Automated Forklift, Tow/Tugger, Unit Load Carrier, Assembly Line, Hybrid, Special Purpose), Navigation (Laser, Magnetic, Vision/SLAM, Inductive, Natural), Component (Hardware, Software, Services), Battery (Lead-Acid, Lithium-Ion, Nickel, Fuel Cell), End-User (Automotive, Food and Beverage, Retail, Electronics, Manufacturing, Healthcare, Logistics), and Geography (United States, Canada, Mexico). Market Forecasts are in Value (USD).

By Vehicle Type

| Automated Forklift |

| Tow/Tugger |

| Unit Load Carrier |

| Assembly Line Vehicle |

| Hybrid / Omni-Directional |

| Special Purpose Vehicle |

By Navigation Technology

| Laser Guidance |

| Magnetic Guidance |

| Vision / SLAM Guidance |

| Inductive / Wire Guidance |

| Natural Navigation |

By Component

| Hardware |

| Software |

| Services |

By Battery Type

| Lead-Acid |

| Lithium-Ion |

| Nickel-Based |

| Fuel Cell |

By End-User Industry

| Automotive |

| Food and Beverage |

| Retail and E-commerce |

| Electronics and Electricals |

| General Manufacturing |

| Healthcare and Pharmaceuticals |

| Logistics and Warehousing |

By Country

| United States |

| Canada |

| Mexico |

| By Vehicle Type | Automated Forklift |

| Tow/Tugger | |

| Unit Load Carrier | |

| Assembly Line Vehicle | |

| Hybrid / Omni-Directional | |

| Special Purpose Vehicle | |

| By Navigation Technology | Laser Guidance |

| Magnetic Guidance | |

| Vision / SLAM Guidance | |

| Inductive / Wire Guidance | |

| Natural Navigation | |

| By Component | Hardware |

| Software | |

| Services | |

| By Battery Type | Lead-Acid |

| Lithium-Ion | |

| Nickel-Based | |

| Fuel Cell | |

| By End-User Industry | Automotive |

| Food and Beverage | |

| Retail and E-commerce | |

| Electronics and Electricals | |

| General Manufacturing | |

| Healthcare and Pharmaceuticals | |

| Logistics and Warehousing | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current value of the North America automated guided vehicle market?

The automated guided vehicle market size in North America stands at USD 1.85 billion in 2026.

How fast is the market expected to grow over the next five years?

The market is projected to expand at a 12.19% CAGR, reaching USD 3.29 billion by 2031.

Which vehicle type holds the largest share today?

Automated forklifts lead with a 34.49% share because factories are replacing diesel units with lithium-ion electric models.

Why are lithium-ion batteries gaining popularity in AGVs?

Lithium-ion packs enable opportunity charging, support 3,000-plus cycles, and free floor space, shortening payback periods to around two years.

Which country will experience the fastest growth in AGV adoption?

Mexico is forecast to grow at a 13.53% CAGR through 2031 as nearshoring fuels greenfield smart-factory construction.

How are software subscriptions changing AGV economics?

Vendors now bundle AI fleet management and predictive maintenance into monthly fees, minimizing upfront capex and aligning costs with performance gains.

Page last updated on: