Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

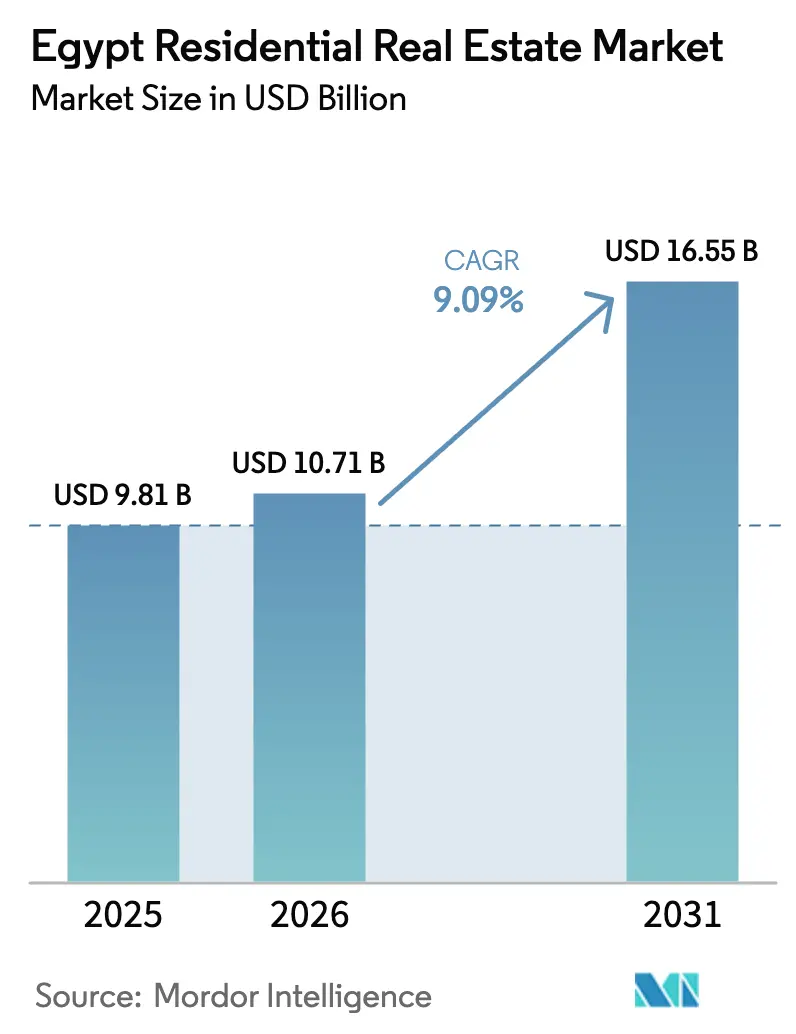

| Base Year Market Size (2025) | USD 9.81 Billion |

| Market Size (2026) | USD 10.71 Billion |

| Market Size (2031) | USD 16.55 Billion |

| Growth Rate (2026 - 2031) | 9.09% CAGR |

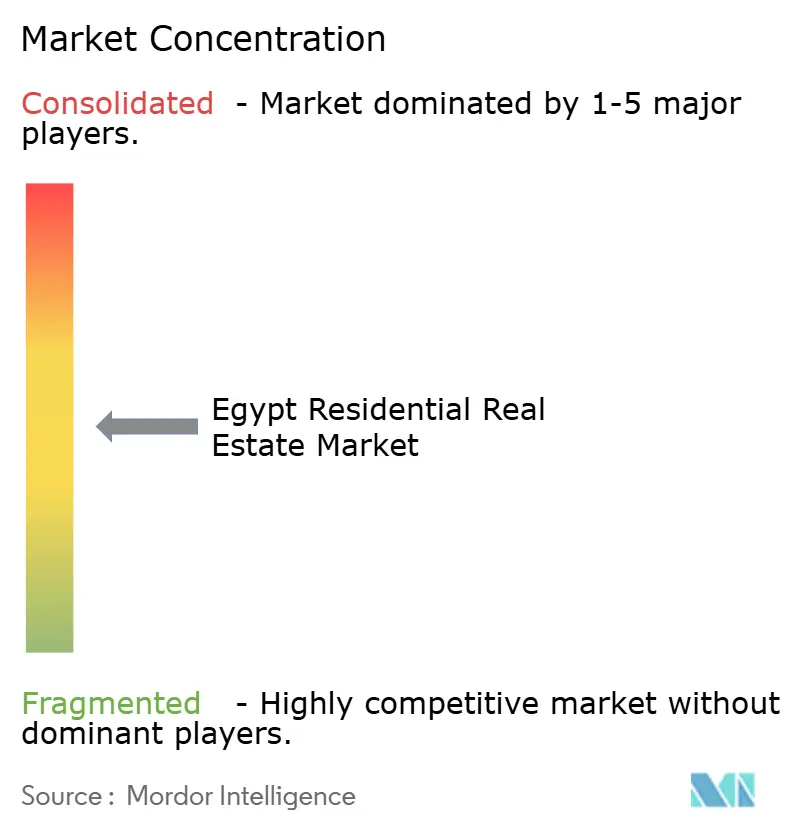

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Residential Real Estate Market Analysis by Mordor Intelligence

The Egypt Residential Real Estate Market size is expected to increase from USD 9.81 billion in 2025 to USD 10.71 billion in 2026 and reach USD 16.55 billion by 2031, growing at a CAGR of 9.09% over 2026-2031.

Demand pivots around Greater Cairo’s population pressure, the government’s new-city program, and remittance-fueled capital seeking a hedge against currency weakness. A cumulative 625-basis-point policy-rate cut in 2025 offered limited relief because consumer mortgage rates still exceeded 24%, keeping ownership expensive and nudging many households toward rentals. Developers continued to front-load demand through installment plans that ask for only 5% to 10% cash up-front, thereby sustaining primary sales even as inflation held near 12%. Infrastructure rollouts in the New Administrative Capital (NAC) and West & East Cairo corridors underpin future absorption, while fiscal ties between land sales and foreign-currency inflows keep state incentives aligned with construction activity.

Key Report Takeaways

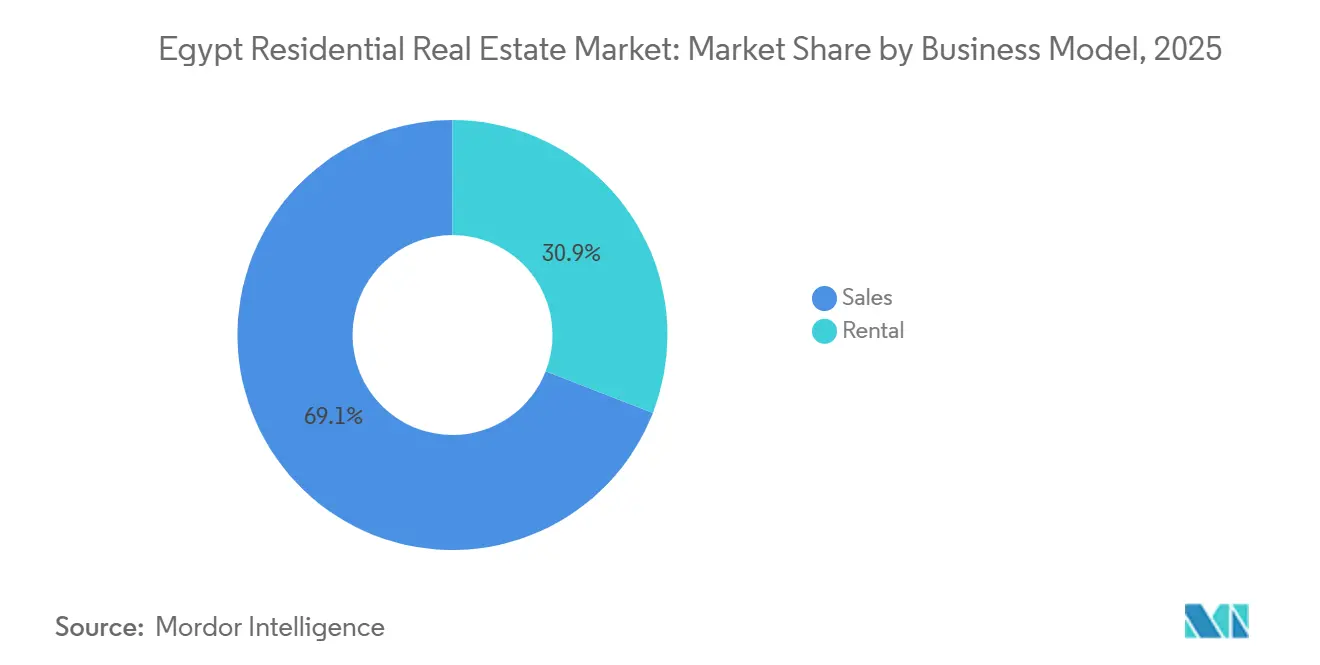

- By business model, sales transactions captured 69.1% of the 2025 value; rentals are forecast to advance at a 9.71% CAGR through 2031.

- By property type, apartments and condominiums accounted for 62.5% of 2025 revenue; villas are the fastest-rising category at a 10.78% CAGR to 2031.

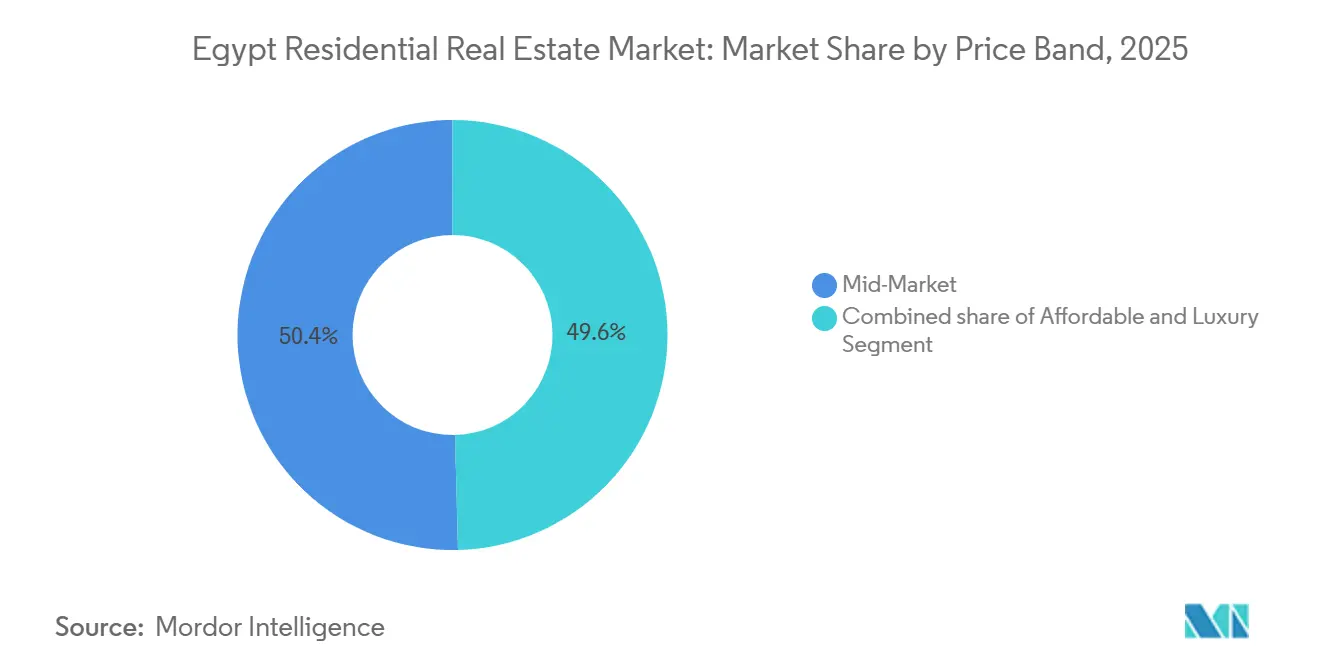

- By price band, mid-market units priced between USD 41,700 and USD 104,200 represented 50.4% of 2025 spending; luxury homes above USD 312,500 are poised for a 10.71% CAGR through 2031.

- By mode of sale, primary new-builds commanded a 62.2% share in 2025 and are expected to climb at a 10.31% CAGR on the back of flexible developer financing.

- By geography, Cairo held 43.9% of the 2025 value and is set to grow at a 10.78% CAGR through 2031, bolstered by NAC’s 100,000 delivered units and USD 3.8 billion CBD outlay.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong demographics and rapid urbanization sustaining end-user demand | +2.5% | Greater Cairo, New Alamein, New Mansoura | Long term (≥ 4 years) |

| Government-led new towns and infrastructure unlocking large-scale supply | +2.0% | NAC, 6th of October, New Alamein, New Mansoura | Medium term (2–4 years) |

| Social/affordable-housing programs and PPPs supporting mid-income segments | +1.5% | Nationwide, especially city peripheries | Medium term (2–4 years) |

| Diaspora and non-resident buyers injecting hard currency | +1.8% | Cairo, North Coast, NAC luxury zones | Short term (≤ 2 years) |

| Shift toward master-planned, amenitized communities | +1.5% | New Cairo, 6th of October, NAC, North Coast | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Strong Demographics And Rapid Urbanization Sustaining End-User Demand

Egypt’s population surpassed 107 million in 2024, and roughly 30% of residents are aged 18-35 years, a cohort forming new households at a pace. Greater Cairo’s density encourages moves to satellite cities where land is 30%-50% cheaper than in the core, lowering entry prices for developers. The New Urban Communities Authority securitized USD 625 million of land receivables in 2024 to accelerate utilities in 6th of October and New Alamein. Yet the Central Bank subsidized mortgages priced at 3% cover homes under USD 29,200, leaving many informal-sector workers excluded[1]Central Bank of Egypt, “Monthly Statistical Bulletin — October 2025,” cbe.org.eg . As a result, pent-up need at the lower-income end coexists with tight supply, reinforcing medium-term demand momentum.

Government-Led New Towns And Infrastructure Unlocking Large-Scale Supply

The April 2024 relocation of 48,000 civil servants to the NAC validated Egypt’s flagship new-city model, but only 1,200 families had occupied units by mid-2024, exposing a synchronisation gap between jobs and housing. China State Construction Engineering’s USD 3.8 billion CBD contract will hand over 20 towers by 2027, anchoring commercial demand[2]China State Construction Engineering Corporation, “Contract Details for NAC CBD,” cscec.com . New Alamein targets 3 million residents with USD 58 billion planned investment, yet off-season occupancy remains below 20%, signaling absorption risk. Utility tie-ins trail housing completions by up to 18 months, forcing some developers to fund interim networks. Nevertheless, state land sales, such as the USD 35 billion Ras El Hekma deal, channel badly needed hard currency, ensuring that public policy stays supportive of continued rollout.

Social/Affordable-Housing Programs And PPPs Supporting Mid-Income Segments

The Sakan Misr program had delivered more than 600,000 units by 2024 toward a 1.1 million-unit 2030 target, with ticket sizes initially below USD 2,900 but now trending closer to USD 12,500 due to inflation. Central Bank 3% mortgages financed about 80,000 loans in 2024, yet 15%-20% down-payments still bar many households. Private developers, therefore, partner with state entities: Emaar Misr and MIDAR launched a USD 292 million initial project in 2025 aimed at middle-income buyers with flexible plans. This partnership template blends subsidized land, streamlined permits, and developer marketing reach, gradually filling the affordability gap left by purely public schemes.

Expansion of Mortgage Finance Improving Affordability for Middle-Income Buyers

Worker remittances jumped 47.2% year-on-year to USD 26.6 billion in the first eight months of 2025 as the pound weakened from 31 to nearly 50 per U.S. dollar. Developers increasingly quote prices in dollars in North Coast resorts and NAC luxury zones, insulating buyers and sellers from further depreciation. A villa priced at USD 500,000 in 2023 cost USD 765,000 equivalent in local currency by mid-2025, underlining the hedge appeal for expatriates. Gulf capital amplified the trend, exemplified by Qatar’s USD 7.5 billion commitment in April 2025. The influx lifts top-tier absorption while widening the affordability divide for domestic, pound-earning households.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High inflation, currency devaluation, and steep interest rates weakening affordability | −2.2% | Nationwide, most acute in Greater Cairo | Short term (≤ 2 years) |

| Construction-cost spikes and contractor stress squeezing margins | −1.5% | New-city zones with high import content | Short term (≤ 2 years) |

| Regulatory and utility delays heightening execution risk | −0.5% | NAC, New Alamein, New Mansoura, 6th of October edge | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Inflation, Currency Devaluation, And Steep Interest Rates

Despite a 625-bp policy-rate cut in 2025, consumer mortgage offers averaged 24.5%, leaving monthly debt service above 40% of gross income for many applicants. Housing and utilities inflation ran at 16.2% in August 2025, eroding real wages. Devaluation lifted imported finishings and appliances, pushing all-in ownership costs higher than basic shell prices indicate. A July 2025 rent-law tweak allowed more frequent adjustments, pushing rents up 10.4% in September 2025 and reducing disposable income for down-payments. The effect is a bifurcated market: cash-rich luxury buyers proceed unimpeded, while middle-income households either rent longer or use developer installments that transfer credit risk away from banks.

Construction-Cost Spikes And Contractor Stress

Cement touched USD 104 per ton in early 2025 before export caps and restarted lines cooled prices to around USD 83, but steel and finishings were still up 18%-25% year-on-year. Developers with thin capital structures renegotiated contractor terms or slowed launches, creating spotty site activity. Madinet Masr disclosed USD 854 million in 2024 contracted sales but flagged margin compression due to escalation clauses[3]Madinet Masr, “Annual Report 2024,” madinetmasr.com . Smaller contractors, borrowing at more than 25%, strained liquidity when milestone payments slipped, causing delivery slippage that dents buyer confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Rentals Outperform As Ownership Defers

Sales dominated with 69.1% of the Egyptian residential real estate market share in 2025, yet rentals are forecast to post a 9.71% CAGR through 2031, making them the fastest-growing track. The July 2025 rent-law amendment unleashed supply from landlords awaiting regulatory clarity, while elevated mortgage coupons deterred leveraged purchases. Developers sustain primary sales by accepting 5% to 10% down payments over ten years, but young professionals earning USD 420-USD 630 monthly still lean toward leasing. Institutional funds began assembling build-to-rent portfolios in 2024, anticipating cap-rate compression as policy rates normalize after 2026. The widening yield gap-apartment rents imply 6%-8% gross returns versus 24.5% mortgage costs-keeps leveraged investors sidelined and underscores why cash buyers dominate the ownership market.

The Egypt residential real estate market size for rentals remains smaller than sales today, yet upside rests on demographic churn and nascent institutional platforms. As job clusters expand in new cities, tenants seek flexible tenure rather than commit to mortgage debt on still-developing peripheries. Over time, seasoned REITs could bundle stabilized rental blocks, injecting professionalism and liquidity into what is now an owner-managed segment. The sales model, in turn, will rely on installment plans and diaspora cash to preserve momentum until borrowing rates fall below the double-digit threshold.

By Property Type: Apartments Anchor Volume, Villas Capture Premium

Apartments captured 62.5% Egypt residential real estate market share in 2025 and are set to grow at a 9.98% CAGR as their price points align with subsidized financing ceilings. High-rise supply in NAC and New Cairo maximizes land and meets the density targets of planned towns. Villas, although smaller in volume, are on a 10.78% CAGR trajectory because they cater to dollar-earning expatriates and Gulf nationals seeking private outdoor space. Tatweer Misr’s villa-only Scenes phase sold out within six months, demonstrating deep premium appetite. Financing remains a divider: buyers of units priced above USD 312,500 usually pay cash or negotiate dollar-linked schedules that bypass local-rate mortgages.

Apartments dominate older districts such as Nasr City and Maadi, but also headline new-city skylines where land values justify vertical builds. For villas, peripheral land at one-third the central-Cairo cost underpins generous plot ratios and landscaped master plans. Developers extend the same low-down-payment schedules to villas, such as Hyde Park Views priced from USD 340,000 with 5% down, but absolute ticket sizes still limit the pool to affluent cohorts. Over time, hybrid formats like low-rise garden apartments may emerge to bridge the gap between affordability and space, particularly once infrastructure links tighten commute times to employment hubs.

By Price Band: Luxury Leads Growth While Mid-Market Holds Scale

Homes priced USD 41,700-USD 104,200 formed 50.4% of 2025 spending, cementing the mid-tier as the Egypt residential real estate market’s volume anchor. The luxury bracket above USD 312,500 will grow the fastest at 10.71% CAGR, powered by remittances and Gulf capital. Currency-pegged payment plans, the promise of freehold titles in tourist zones, and marquee amenities such as private marinas lure this cohort. Mid-tier demand thrives on developer installments that mimic mortgages without bank underwriting, an arrangement that shifts credit risk to builders but keeps monthly outflows manageable for salaried buyers.

Affordability programs supply the sub-USD 29,200 band but face chronic utility-infrastructure bottlenecks, slowing handovers. At the other extreme, developers like Emaar Misr price North Coast towers directly in dollars, reflecting a structural segmentation of the Egypt residential real estate market. Policy makers may need to expand subsidized ceilings or lengthen mortgage tenors to prevent the middle band from thinning as inflation persists.

By Mode of Sale: Primary Market Innovation Drives Growth

Primary new-builds delivered 62.2% of the 2025 value and are forecast to expand at a 10.31% CAGR through 2031, buoyed by attractive developer terms and the government’s new-city bias. Secondary resales lag because buyers must marshal 20%-30% equity and endure high-street lending rates. Pre-sales at projects such as Bloomfields and Kayan City recycle early cash into construction, compressing project cycles. Yet developers shoulder receivable risk until delivery, a concern if macro conditions trigger buyer default spikes.

Secondary trade will gain depth after 2027 as the first waves of NAC and New Cairo residents upsize or relocate. Transparency will be critical: Egypt still lacks a mature title registry and automated valuation platforms, keeping bank appetite for resale mortgages low. In the interim, the Egyptian residential real estate market size remains skewed toward off-plan stock, where payment flexibility compensates for construction-period uncertainty.

Geography Analysis

Cairo commanded 43.9% of the 2025 market value and is predicted to notch the nation’s fastest 10.78% CAGR to 2031, underpinned by the NAC’s 100,000 delivered homes and the USD 3.8 billion CBD now rising. Relocation of ministries started in 2024, securing daytime footfall while master-planning suburbs in New Cairo and 6th of October to harvest spillover demand. Installment-heavy offerings such as Hyde Park Views have shortened sales cycles, illustrating how flexible financing marries with amenity-rich layouts to pull families out of congested cores. West Cairo also enjoys proximity to central workplaces; projects like SODIC West leverage expressway access to keep commute times reasonable even as they deliver low-density living.

Alexandria and the wider North Coast carry a smaller weight yet differentiate in leisure and diaspora pull. Emaar Misr’s planned USD 20 billion Red Sea community underscores optimism, but off-season occupancy still barely crosses 20%, highlighting absorption risk tied to tourism patterns. Giza’s West Cairo pocket benefits from mature schools and hospitals in NEW GIZA and surrounding compounds, solidifying value retention despite macro swings. Rental yields here run 100-150 basis points lower than emerging NAC districts, showing how service completeness tempers investor required returns.

Beyond Greater Cairo, new-city corridors such as New Alamein and New Mansoura are embryonic. Infrastructure lags have capped handovers, but long-haul prospects rest on industrial and logistics nodes spurring year-round employment. The government has earmarked hundreds of square kilometers for social housing, yet only 40% of parcels had live utilities by mid-2025, delaying affordable-unit delivery. Developers like Orascom Development, with resorts in El Gouna and Makadi Heights, diversify revenue between tourism and residential to hedge regional volatility. Over the medium term, improved port and expressway links should gradually raise the rest-of-country share as household migration follows jobs.

Competitive Landscape

Competition remains moderate, with five leading developers holding just over half of contracted sales, a level that enables price leadership yet allows nimble mid-caps to flourish. Talaat Moustafa Group, Emaar Misr, SODIC (85% owned by Aldar-ADQ), Palm Hills, and Madinet Masr together control extensive land banks exceeding 60 million m². Their scale secures priority access to state sites and financing; for example, Madinet Masr placed USD 135 million of capex in 2024 to expand Taj City and Sarai while booking USD 854 million in sales.

Strategic moves increasingly center on public-private partnerships that swap discounted land for shared infrastructure outlays. Emaar Misr’s USD 292 million tie-up with MIDAR streamlines permits and locks in pipeline visibility worth up to USD 2.1 billion. Aldar-ADQ’s backing of SODIC injects Gulf balance sheet strength that supports North Coast experiments priced in dollars. Mid-tier entrants like Tatweer Misr and City Edge differentiate via thematic townships—education-centric Bloomfields or waterfront Etapa—rather than brute scale, using digital marketing to reach diaspora buyers abroad.

Cost inflation has nudged many players to renegotiate contractor agreements toward fixed-price or shared-risk models. Some, such as Palm Hills with 19 launches in 2024, hedge by staggering phases and matching cash collections to milestone payments. Technology adoption remains patchy: CRM systems and virtual tours are mainstream, yet Internet-of-Things building management features are still confined to showcase towers in NAC. Looking ahead, developers that can securitize receivables or tap green-bond markets stand to buffer margin swings while meeting rising ESG disclosure demands from foreign investors.

Egypt Residential Real Estate Industry Leaders

Orascom Development

Palm Hills Developments

Emaar Misr

Talaat Moustafa Group (TMG)

SODIC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Hyde Park Developments unveiled Hyde Park Views in New Cairo with 5% down and 10-year installments, targeting handover in 2027.

- September 2025: Emaar Misr announced a USD 20 billion Red Sea project featuring Golden Coast and Sky Tower, aimed at Gulf nationals and expatriates.

- August 2025: Qatar pledged USD 7.5 billion for Egyptian real estate and infrastructure, underscoring Gulf confidence.

- March 2025: Mountain View partnered with STM Investment on the 500-feddan Kayan City villa scheme slated for a 2026 sales launch.

Egypt Residential Real Estate Market Report Scope

Residential real estate refers to properties designed primarily for housing purposes. This includes various dwellings such as single-family homes, apartments, condominiums, townhouses, and villas. Residential real estate is characterized by its use for living accommodations rather than commercial or industrial purposes. A complete background analysis of the Egypt residential real estate market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends is covered in the report.

The Egypt residential real estate market is segmented by type (apartments and condominiums, villas, and landed houses) and commercial real estate (offices, retail, hospitality, and others). The report offers market size and forecasts for all the above segments in value (USD).

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

How large is the Egyptian residential real estate market in 2026?

The market is valued at USD 10.71 billion in 2026 and is projected to reach USD 16.55 billion by 2031 on a 9.09% CAGR.

Which city captures the biggest share of housing demand?

Cairo commands 43.9% of the 2025 value and is forecast to remain the fastest-growing location through 2031.

Why are rentals growing faster than sales?

High mortgage rates and 20%–30% equity requirements encourage younger households to lease, helping rentals log a 9.71% forecast CAGR.

What drives luxury housing momentum?

Dollar inflows from expatriates and Gulf investors, plus developers quoting prices in U.S. dollars, underpin a 10.71% CAGR for homes above USD 312,500.

Which restraint poses the greatest near-term threat?

Elevated borrowing costs and double-digit inflation reduce affordability, shaving an estimated 2.2 percentage points off forecast CAGR.

Are installment plans replacing mortgages?

For many buyers, yes—developers offering 5%–10% down and 10-year schedules have become a primary financing channel in new-build communities.

Page last updated on: