Healthcare Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 60.76 Billion |

| Market Size (2031) | USD 102.77 Billion |

| Growth Rate (2026 - 2031) | 11.09% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Cloud Computing Market Analysis by Mordor Intelligence

The Healthcare Cloud Computing Market size is projected to expand from USD 54.69 billion in 2025 and USD 60.76 billion in 2026 to USD 102.77 billion by 2031, registering a CAGR of 11.09% between 2026 to 2031.

The expansion is propelled by health systems shifting away from legacy servers toward scalable, AI-ready cloud platforms that can handle real-time analytics, genomic workloads, and telehealth traffic. Regulatory pushes for data sharing, notably the EU’s Health Data Space rules, add urgency to modernize infrastructure, while the end of data-egress charges at the largest hyperscale providers improves total cost of ownership. Hospitals gain from cloud elasticity during seasonal surges, and payers lower claims adjudication costs by running revenue-cycle automation in multicloud environments. Clinicians increasingly rely on cloud-based AI for radiology triage and ambient documentation, which drives incremental demand for high-performance computing capacity.

Key Report Takeaways

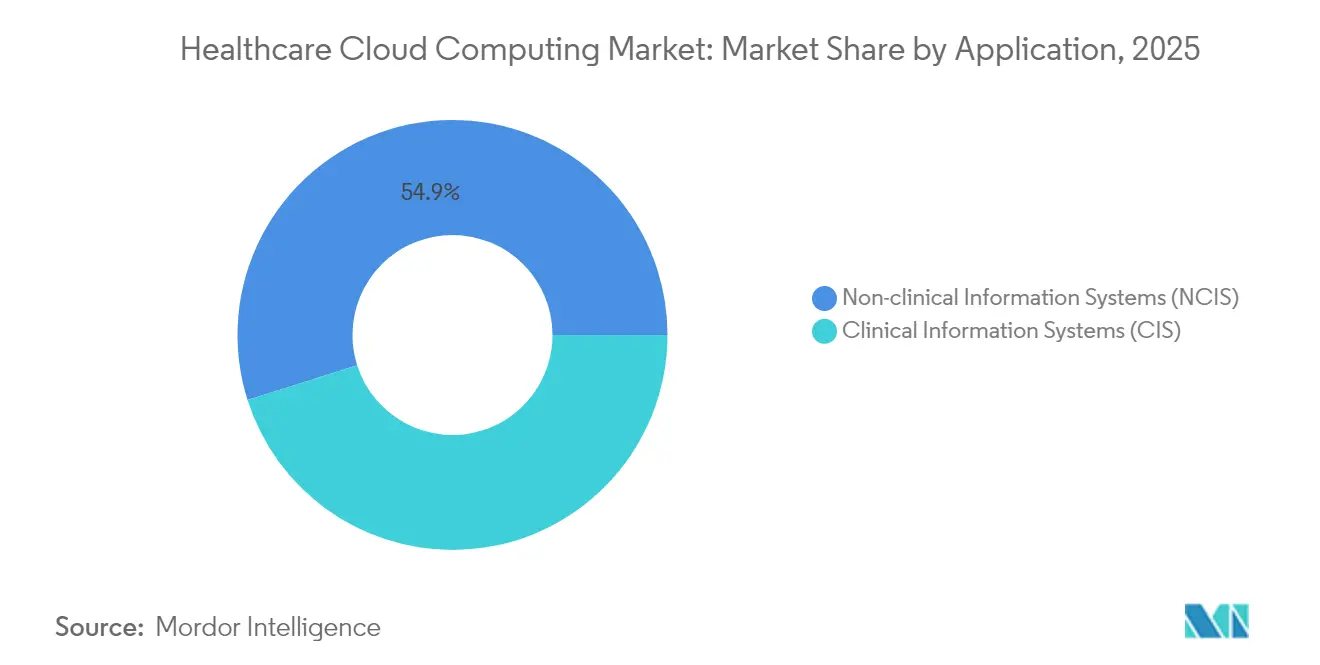

- By application, Clinical Information Systems held 45.12% of Healthcare Cloud Computing market share in 2025; Non-clinical Information Systems are expanding at a 12.28% CAGR through 2031.

- By deployment, Private Cloud commanded 55.10% of the Healthcare Cloud Computing market size in 2025, while Public Cloud is advancing at an 18.30% CAGR to 2031.

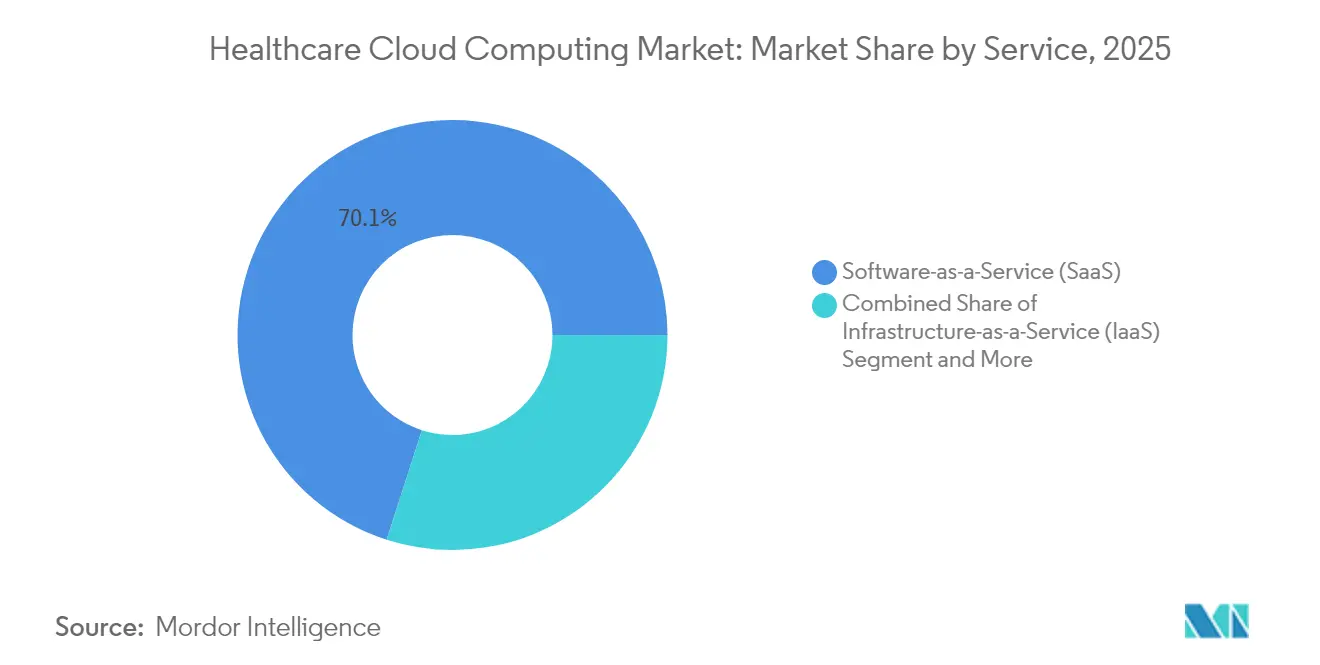

- By service, Software-as-a-Service captured 70.05% share of the Healthcare Cloud Computing market size in 2025; Platform-as-a-Service is forecast to record a 18.74% CAGR through 2031.

- By end user, Providers led with 71.60% Healthcare Cloud Computing market share in 2025, whereas Payers show the fastest growth at 18.02% CAGR through 2031.

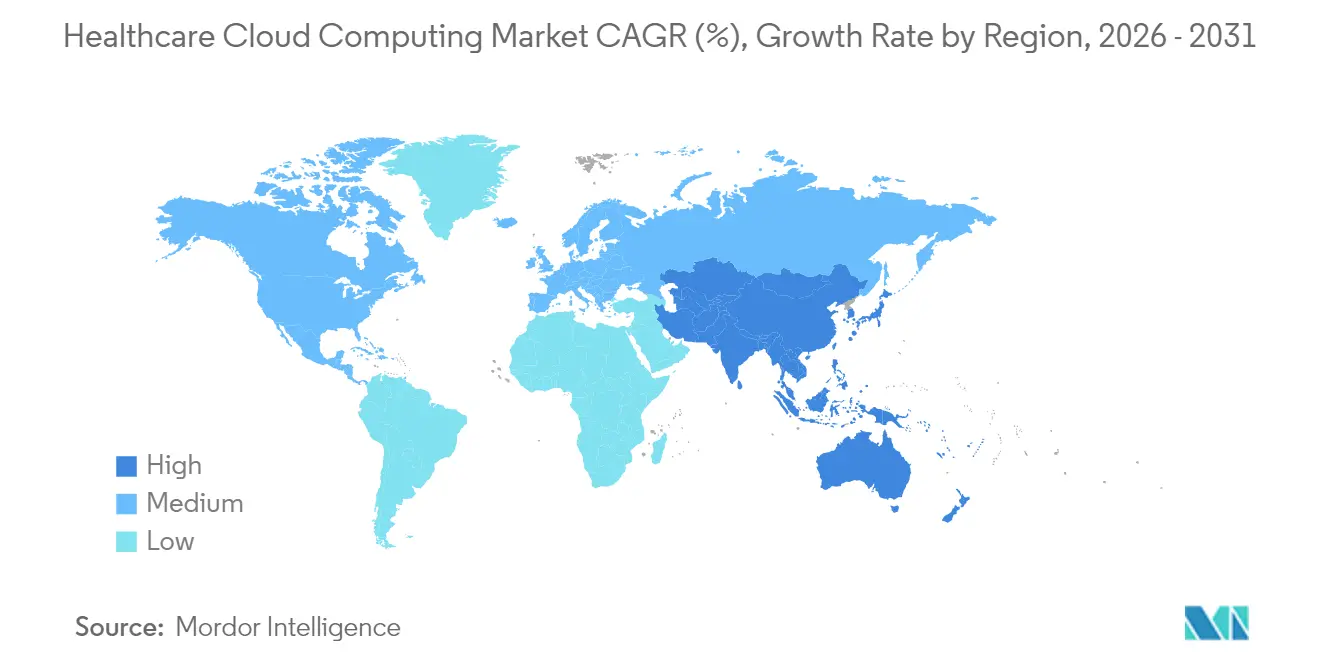

- By geography, North America accounted for 48.30% of the Healthcare Cloud Computing market size in 2025, and Asia-Pacific is the fastest expanding geography with a 18.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Healthcare Cloud Computing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IT adoption across healthcare settings | +2.8% | Global, strongest in APAC | Medium term (2-4 years) |

| Cost-saving and scalability advantages | +3.2% | North America and EU | Short term (≤ 2 years) |

| Easier access to advanced analytics and ML | +2.1% | High-income markets | Medium term (2-4 years) |

| FHIR-based API push | +1.9% | North America and EU | Long term (≥ 4 years) |

| Real-time clinical-genomics workloads | +1.4% | Developed economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Adoption of IT Across Healthcare Settings

Hospitals, clinics, and diagnostic networks now treat digital transformation as a core strategic lever rather than a crisis response. Modern cloud platforms replace aging on-premise data centers, bringing built-in redundancy, instant provisioning, and automated patching that small provider IT teams could rarely support. Pandemic-era investments in telehealth evolved into full-scale virtual-care ecosystems that depend on scalable video, storage, and AI triage running in the cloud. Health systems restructure clinical workflows around real-time dashboards, IoMT device feeds, and predictive models that surface sepsis or deterioration alerts at the bedside. Smaller rural hospitals use multitenant SaaS EHRs to access decision-support tools that once required academic-center budgets. Integrated delivery networks pursue common data fabrics so that clinicians see unified longitudinal records during cross-facility consults, strengthening the cloud computing in healthcare industry.

Cost-Saving and Scalability Advantages of Cloud

Removing capital-intensive hardware refresh cycles and shifting to pay-as-you-go compute reduces budget pressure in a period of margin contraction for US hospitals. The major hyperscale providers canceled egress fees in 2024, lowering multicloud exit barriers and giving CIOs stronger negotiating leverage. Elastic infrastructure absorbs traffic spikes during mass vaccination drives or claims-submission peaks without overprovisioning. Outsourced patching, backup, and high-availability architecture free internal staff for higher-value data-science work. Payers cut adjudication turnaround when cloud-native rules engines process tens of thousands of claims per minute, leading to faster member reimbursements. Cloud cost savings also manifest in energy reduction and data-center real-estate divestments, which align with provider sustainability objectives and accelerate the healthcare cloud computing market.

Easier Access to Advanced Analytics and ML Tools

Hyperscale marketplaces now offer turnkey imaging-segmentation models, ambient-note transcription engines, and population-risk stratification pipelines that healthcare buyers can activate with minimal DevOps overhead. Radiology groups route large study volumes to cloud GPUs to accelerate AI triage, reducing time-to-diagnosis for stroke or pulmonary embolism cases. Cloud NLP services mine unstructured clinical notes, turning them into coded data for quality reporting and prior-authorization automation. Smaller health systems adopt pre-trained large language models within secure environments, delivering personalized outreach or medication-adherence nudges without deep ML expertise. Providers combine de-identified EHR and claims data in cloud data warehouses to build predictive models that flag rising-risk patients and support value-based care contract performance, reinforcing the cloud computing in healthcare market.

FHIR-Based API Push Enabling Cloud-Native Interoperability

FHIR’s REST architecture fits naturally with serverless functions and container orchestration, enabling low-latency exchange among EHRs, telemedicine apps, and wearables. US and EU policy makers set hard deadlines for payer-provider data exchange, making cloud FHIR gateways a compliance imperative. Vendors expose granular patient-level APIs that consumers can authorize from smartphones, supporting app ecosystems for medication reminders or clinical-trial matching. Health information exchanges deploy cloud-native consent management services so patients can control how their records flow across borders. The resulting data liquidity fuels real-time analytics, quality-measure automation, and unified patient engagement portals.

Restraints Impact Analysis of Healthcare Cloud Computing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security and integrity concerns | -1.8% | Global, stricter in US and EU | Short term (≤ 2 years) |

| Lack of interoperability and standards | -1.2% | Fragmented markets | Medium term (2-4 years) |

| High egress fees and vendor lock-in risks | -0.9% | High-income regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Security and Integrity Concerns

Cyberattacks against hospitals surged, with ransomware crews targeting misconfigured object storage and unpatched APIs. Breaches trigger HIPAA fines, class-action lawsuits, and board-level scrutiny, prompting security audits before cloud migration approvals. CIOs wrestle with the shared-responsibility model and sometimes underestimate their role in hardening identity management, logging, and encryption. Insurance premiums spike after large breaches, adding hidden costs to transformation budgets. Regulators respond with tighter audit trails and incident-reporting timelines, increasing compliance overhead for smaller community providers that lack dedicated cybersecurity talent.

Lack of Interoperability and Standards

Legacy HL7 v2 interfaces, proprietary imaging formats, and inconsistent terminologies slow unified data-fabric efforts. Many EHR vendors still charge premium fees for API access, complicating third-party innovation. Semantic mismatches in lab codes or problem lists undermine cross-provider analytics even when records sync. Country-specific privacy laws force architecture workarounds, such as in-region data zones or data-sovereignty partitions, which increase design complexity. Absence of global consent frameworks delays cross-border tele-oncology services despite cloud backbone availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Healthcare Cloud Computing Market Segment Analysis

By Application:

Clinical Systems Drive Digital TransformationClinical Information Systems represented nearly half of total 2025 spending, reflecting the centrality of EHR, PACS, and radiology workflows to patient safety. The Healthcare Cloud Computing market size for clinical workloads benefited from federal stimulus that required certified EHR technology and set quality-reporting thresholds. Cloud-hosted EHRs provide instant upgrades and integrated clinical-decision plugins, improving physician satisfaction scores. Imaging departments route CT and MR studies to cloud AI services that flag critical findings, cutting turnaround times.

Non-clinical applications expand as finance departments seek cloud-based revenue-cycle analytics that cut denial rates. Health systems deploy SaaS billing platforms that scale during open enrollment, ensuring claims adjudication keeps pace with member growth. HR teams use cloud scheduling and payroll engines to manage traveling nurses and remote coders with geofenced compliance. Predictive supply-chain dashboards in the Healthcare Cloud Computing market forecast drug shortages and optimize just-in-time inventory, freeing cash for clinical programs.

By Deployment:

Private Cloud Maintains Security EdgePrivate Cloud maintains majority share because many providers place PHI-heavy workloads in single-tenant environments with hardware-level isolation. Institutions running genomic research clusters or intensive care telemetry choose dedicated infrastructure to meet sovereign-data rules. Customizable firewalls and on-premise adjunct nodes let CISOs enforce granular policies.

Public Cloud accelerates fastest after providers grow confident in HITRUST, GDPR, and HDS certifications offered by hyperscalers. The removal of egress fees and arrival of confidential-computing chipsets ease vendor-lock concerns. Many IDNs adopt a hybrid pattern: surgical video and telemetry stream into local private clouds for low latency, while anonymized research datasets replicate to public clouds for AI model training. This balanced approach keeps critical workloads close while exploiting hyperscale economics for secondary analytics, strengthening the cloud computing in healthcare industry.

By Service:

SaaS Dominance Reflects Operational PrioritiesTurnkey SaaS remains the default choice for hospitals aiming to limit capital outlay and internal maintenance. SaaS EHR vendors push quarterly feature drops that bundle regulatory updates and cybersecurity patches, preventing compliance drift. Patient-engagement portals running on SaaS achieve cross-browser functionality without local dev cycles, driving portal adoption metrics.

Platform-as-a-Service surges as analytics centers of excellence build custom FHIR aggregators and API gateways. DevOps teams appreciate managed Kubernetes clusters that abstract complexity yet allow fine-grained scaling of microservices. PaaS notebooks host data-science workflows where clinicians and data scientists co-develop risk models for readmissions. Infrastructure-as-a-Service maintains niche relevance when legacy imaging archives need specialized GPU drivers or when disaster-recovery sites mirror on-premise stacks in the cloud.

By End User:

Provider-Payer Convergence AcceleratesProviders drive most consumption because inpatient volumes still generate the largest data footprint. Academic medical centers pioneer AI scribes that reduce documentation burden by listening to clinician-patient conversations and populating structured notes. Ambulatory clinics adopt cloud email and secure messaging that meet HIPAA encryption standards while supporting mobile workflows.

Payers catch up quickly as value-based contracts hinge on unified clinical-administrative datasets. Cloud risk-adjustment engines parse encounter data to flag coding gaps, boosting RAF scores and reimbursement. Member-experience teams deploy generative-AI chatbots in the Healthcare Cloud Computing market to answer benefit questions and schedule appointments, leading to higher Net Promoter Scores. Merged payvider entities establish joint data-lakes to coordinate care pathways and reduce duplication.

Geography Analysis

North America Healthcare Cloud Computing Market

North America’s 48.30% share reflects long-standing EHR mandates and the presence of all top hyperscalers with healthcare-focused compliance toolkits. US health systems increasingly shift disaster-recovery to the cloud, freeing on-premise floor space for revenue-generating clinical units. Canadian provinces deploy centralized imaging archives on sovereign hyperscale regions to support teleradiology across vast distances.

Europe Healthcare Cloud Computing Market

Europe benefits from the European Health Data Space Regulation, which prescribes interoperable standards and patient access rights. Cloud providers respond by opening additional EU-based availability zones certified to C5 and GDPR codes, allowing hospitals to consolidate silos without breaching residency laws. German public-private consortiums pilot FHIR-based cancer registries hosted in private clouds that federate across Länder, improving research data depth. Scandinavian systems leverage high renewable-energy grids to power carbon-neutral cloud data centers that align with national climate targets.

APAC Healthcare Cloud Computing Market

Asia-Pacific registers the fastest 18.88% CAGR due to rising healthcare spend and smartphone penetration. India’s national ABDM digital-health stack rides on domestic cloud exchanges that enable small clinics to issue interoperable electronic health records. In Southeast Asia, private hospital chains launch virtual-first insurance plans that rely on public cloud tele-consult engines. Australia’s My Health Record integrates lab and imaging results via cloud FHIR services, raising data completeness and patient engagement. Regional unevenness persists though, as bandwidth constraints in rural Indonesia and data-localization rules in China shape bespoke deployment topologies.

Competitive Landscape

Competition centers on domain-specific accelerators rather than raw compute pricing. AWS, Microsoft Azure, and Google Cloud embed compliance blueprints and sector-tuned AI services such as automated prior-authorization workflows. AWS collaborates with GE HealthCare on generative-imaging AI models that customers can run directly within their cloud VPCs[3]GE HealthCare, “GE HealthCare and AWS Announce Strategic Collaboration to Accelerate Healthcare Transformation With Generative AI,” investor.gehealthcare.com. Microsoft bundles Teams telehealth connectors with Azure API for FHIR to deliver an end-to-end virtual-care stack. Google Cloud’s Medical Imaging Suite integrates de-identification APIs and analytics dashboards, aiming to shorten AI deployment cycles.

Specialist vendors maintain footholds by offering managed services and shared-responsibility frameworks. ClearDATA provides 24×7 DevSecOps monitoring tailored to HIPAA, while athenahealth’s multi-tenant EHR serves community hospitals lacking robust IT staff. Datavant focuses on tokenization and record linkage, allowing research collaborators to combine datasets without exposing identifiers. These niche players often partner with hyperscalers for infrastructure layers while adding domain-specific orchestration.

M&A remains brisk as cloud providers buy analytics boutiques or compliance start-ups to deepen vertical stacks. Oracle’s multiyear, multibillion-dollar hosting deal linked to its Cerner acquisition signals intent to combine clinical data with enterprise resource planning. Siemens Healthineers teams with regional governments to deploy oncology cloud platforms that bundle imaging hardware, AI, and managed services in subscription models. Investors reward vendors demonstrating quantified outcome gains, so market leaders publish case studies highlighting reduced sepsis mortality or improved first-pass claim resolution.

Healthcare Cloud Computing Industry Leaders

IBM Corporation

Oracle

Dell Technologies

Koninklijke Philips N.V.

Amazon Web Services (AWS)

- *Disclaimer: Major Players sorted in no particular order

Healthcare Cloud Computing Market Companies Covered in this Report

- Amazon Web Services (AWS)

- Microsoft

- IBM

- Google Cloud

- Oracle

- Dell Technologies

- Siemens Healthineers

- Koninklijke Philips

- ClearDATA

- athenahealth

- CareCloud

- ZYMR

- OSP Labs

- Euris

- Google Cloud (Alphabet)

- Salesforce

- SAP

- Cisco Systems

- Medidata Solutions

Recent Industry Developments in Healthcare Cloud Computing Market

- March 2025: GE HealthCare launched Genesis, a suite of cloud enterprise-imaging SaaS modules that provide edge ingestion, vendor-neutral archive, and migration tools.

- February 2025: Royal Philips extended its cloud radiology-informatics portfolio across Europe and started testing generative-AI features for structured reporting.

Global Healthcare Cloud Computing Market Report Scope

As per the scope of this report, cloud computing has been defined as the practice of using remote servers in place of local servers or networks to store, manage, and process data. Therefore, using the cloud moves the data center infrastructure outside the organization. This report analyzes and discusses the market for cloud computing in the healthcare sector. The revenue from cloud services has been tracked in the report. The healthcare cloud computing market is segmented by application (Clinical Information Systems (CIS) (Electronic Health Record (EHR), Picture Archiving and Communication System (PACS), Radiology Information Systems (RIS), Computerized Physician Order Entry (CPOE), and other applications) and Non-clinical Information Systems (NCIS) (Revenue Cycle Management (RCM), Automatic Patient Billing (APB), Payroll Management System, and other Non-clinical Information Systems)), Deployment (Private Cloud and Public Cloud), Service (Software-as-a-Service (SaaS), Infrastructure-as-a-Service (IaaS), and Platform-as-a-Service (PaaS)), end user (Healthcare Providers and Healthcare Payers), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for all the above segments.

Segmentation Overview

| Clinical Information Systems (CIS) | Electronic Health Record (EHR) |

| Picture Archiving & Communication System (PACS) | |

| Radiology Information System (RIS) | |

| Computerized Physician Order Entry (CPOE) | |

| Other CIS Applications | |

| Non-clinical Information Systems (NCIS) | Revenue Cycle Management (RCM) |

| Automatic Patient Billing (APB) | |

| Payroll Management System | |

| Other NCIS |

| Private Cloud |

| Public Cloud |

| Hybrid Cloud |

| Software-as-a-Service (SaaS) |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Healthcare Providers |

| Healthcare Payers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Clinical Information Systems (CIS) | Electronic Health Record (EHR) |

| Picture Archiving & Communication System (PACS) | ||

| Radiology Information System (RIS) | ||

| Computerized Physician Order Entry (CPOE) | ||

| Other CIS Applications | ||

| Non-clinical Information Systems (NCIS) | Revenue Cycle Management (RCM) | |

| Automatic Patient Billing (APB) | ||

| Payroll Management System | ||

| Other NCIS | ||

| By Deployment | Private Cloud | |

| Public Cloud | ||

| Hybrid Cloud | ||

| By Service | Software-as-a-Service (SaaS) | |

| Infrastructure-as-a-Service (IaaS) | ||

| Platform-as-a-Service (PaaS) | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of Healthcare Cloud Computing by 2031?

The market is expected to reach USD 102.77 billion by 2031, rising from USD 60.76 billion in 2026.

Which application segment currently contributes most to spending?

Clinical Information Systems, including EHR and imaging platforms, accounted for 45.12% of 2025 revenue.

Why are providers favoring private cloud deployments?

Dedicated environments deliver stricter access controls and easier compliance audits for protected health information.

How fast is Asia-Pacific adoption growing?

Spending across Asia-Pacific is forecast to expand at a 18.88% CAGR between 2026 and 2031.

Which service model is gaining momentum for custom AI projects?

Platform-as-a-Service is growing at a 18.74% CAGR as hospitals build bespoke analytics and interoperability applications.

What cybersecurity challenge most affects cloud migration decisions?

Rising ransomware attacks and the complexity of shared-responsibility security models heighten caution during cloud adoption planning.

Page last updated on: