Nucleic Acid Amplification Testing (NAAT) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

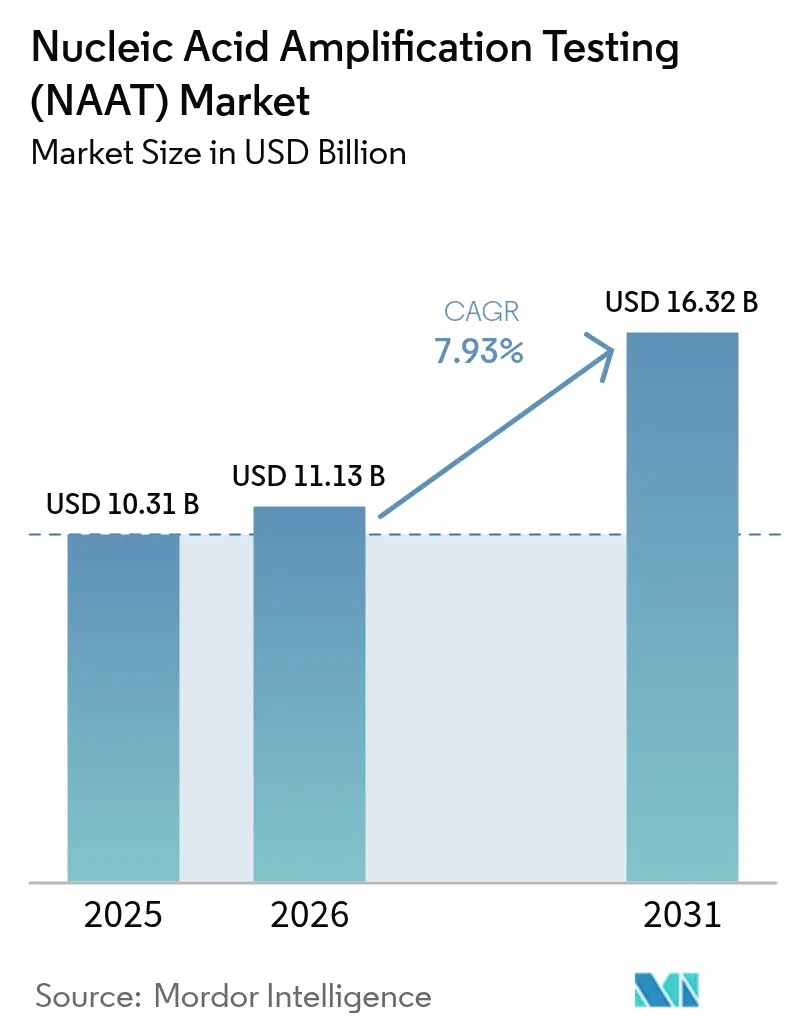

| Market Size (2026) | USD 11.13 Billion |

| Market Size (2031) | USD 16.32 Billion |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nucleic Acid Amplification Testing (NAAT) Market Analysis by Mordor Intelligence

The nucleic acid amplification testing (NAAT) market size was valued at USD 10.31 billion in 2025 and estimated to grow from USD 11.13 billion in 2026 to reach USD 16.32 billion by 2031, at a CAGR of 7.93% during the forecast period (2026-2031). A shift toward precision medicine, routine syndromic surveillance, and value-based care is amplifying demand as molecular assays become embedded in everyday clinical work-flows. Hospitals and reference laboratories alike are scaling capacity through automation, while artificial-intelligence modules optimize everything from sample triage to result interpretation. These digital layers reduce human error, accelerate clinical decisions, and mitigate staffing shortfalls. At the same time, the nucleic acid amplification testing market is expanding into primary-care clinics, retail health, and public-health programs once reliant on conventional immunoassays. Isothermal chemistries advance decentralization, and regulatory momentum around liquid biopsy is positioning molecular oncology as the next high-volume frontier.

Key Report Takeaways

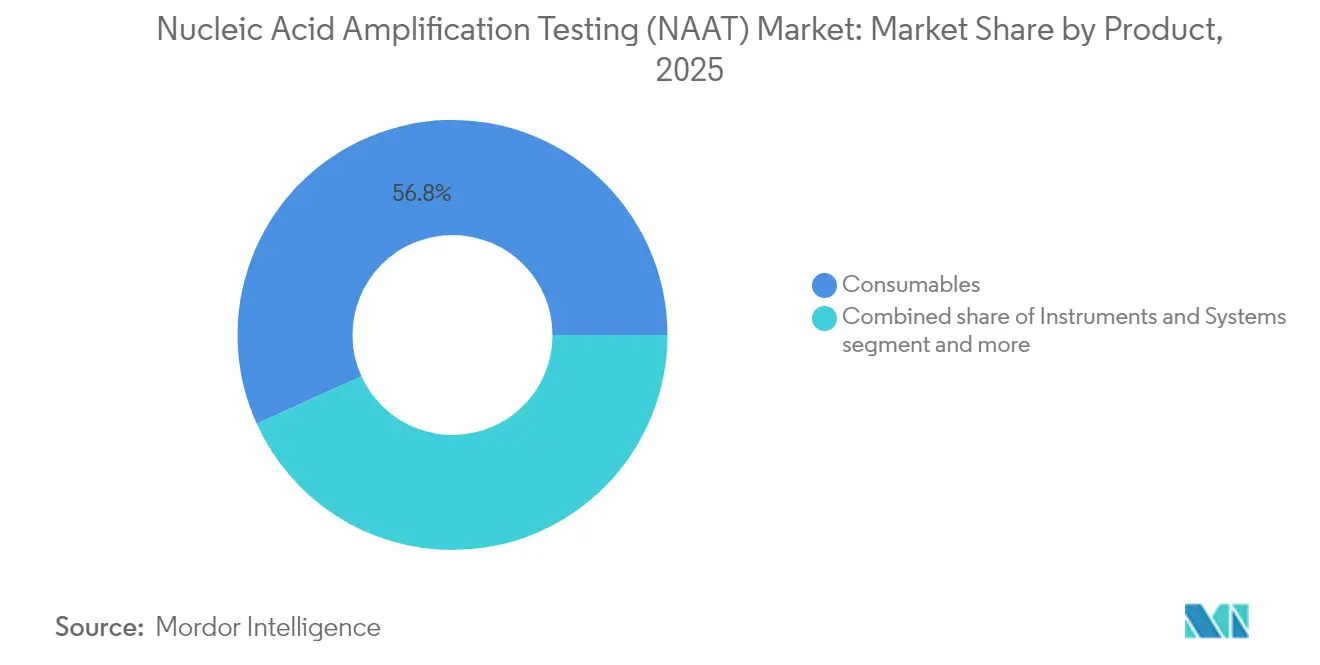

- By product, consumables captured 56.78% of revenue in 2025 and is projected to grow at a 9.28% CAGR through 2031.

- By technology, PCR held 67.12% of the nucleic acid amplification testing market share in 2025; INAAT systems are on track for a 9.94% CAGR through 2031.

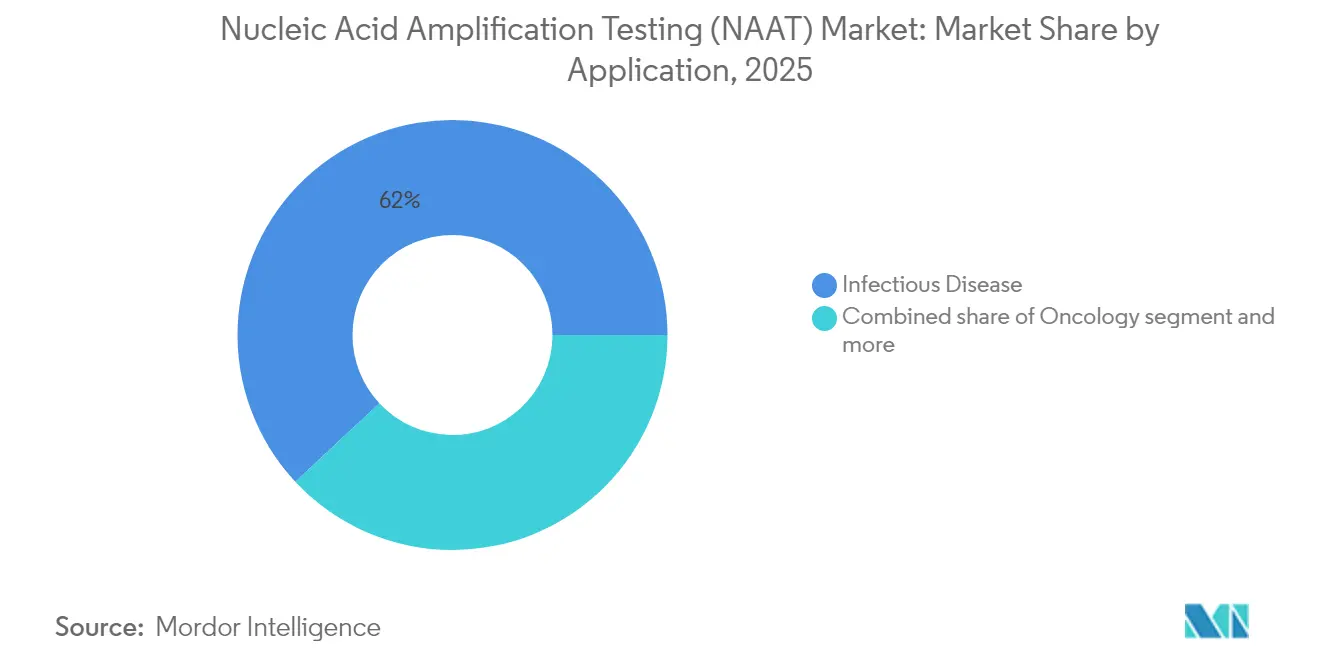

- By application, infectious disease dominated with 61.95% of the nucleic acid amplification testing market size in 2025, while oncology assays are forecast to grow at a 9.06% CAGR to 2031.

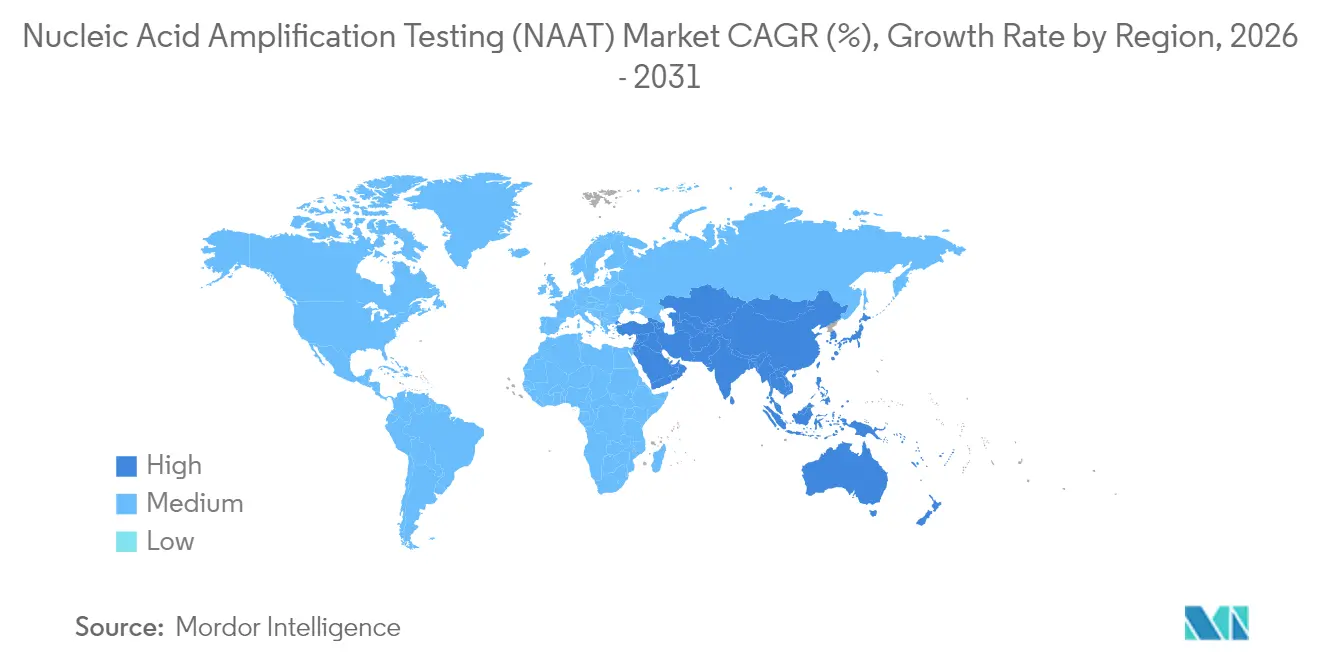

- By geography, North America led with 43.10% of nucleic acid amplification testing market share in 2025; Asia-Pacific is projected to deliver a 9.88% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nucleic Acid Amplification Testing (NAAT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Demand for Multiplexed Respiratory Pathogen Panels | +2.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rapid Adoption of Isothermal Loop-Mediated Platforms for Decentralized Testing | +1.8% | Global, with emphasis on emerging markets | Long term (≥ 4 years) |

| Integration of NAAT with Automated Sample-to-Answer Cartridges | +1.5% | North America, Europe, developed Asia-Pacific | Medium term (2-4 years) |

| Inclusion of NAAT in Blood-Screening Mandates | +1.2% | Global, with stronger impact in regulated markets | Long term (≥ 4 years) |

| Growth of ctDNA NAAT Companion Diagnostics in Oncology | +0.9% | North America, Europe, China, Japan | Long term (≥ 4 years) |

| Private Investment Surge in Portable CRISPR-Based NAAT Solutions | +0.7% | North America, Europe, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Demand for Multiplex Respiratory Pathogen Panels

Syndromic respiratory panels allow clinicians to detect several viruses and bacteria in one run[1]ScienceDirect, “Exploring the Utility of Multiplex Infectious Disease Panel Testing for ...,” sciencedirect.com, cutting diagnostic uncertainty and guiding targeted therapy within hours. Hospitals report shorter lengths of stay and reduced empiric antibiotic use, advantages that align with value-based payment models. Laboratory managers also appreciate streamlined workflows that ease staffing pressure during seasonal surges. Because many of these panels are cartridge-based, they integrate smoothly with existing analyzers and help laboratories justify capital upgrades. Overall, their adoption is pushing the nucleic acid amplification testing market deeper into urgent-care and outpatient settings.

Rapid Adoption of Isothermal Loop-Mediated Platforms for Decentralized Testing

Loop-mediated amplification eliminates thermal cycling[2]ScienceDirect, “The Evolution of Isothermal Amplification Technology,” sciencedirect.com, enabling devices the size of a smartphone to perform sensitive detection in clinics, pharmacies, and field sites. Publication volume on LAMP and RPA rose steadily from 2013-2024, signalling maturing science. Coupled with microfluidic chips, these chemistries support sample-to-answer formats that require no lab bench. As emerging markets invest in infectious-disease surveillance, isothermal tools can reach rural zones where PCR systems are impractical, broadening the nucleic acid amplification testing market footprint.

Integration of NAAT with Automated Sample-to-Answer Cartridges

Closed cartridges combine extraction, amplification, and detection in a sealed path that reduces contamination risk and shrinks hands-on time to minutes mdpi.com. Built-in analytics translate raw curves into clear calls, freeing technologists for higher-value tasks. Vendors targeting outpatient clinics cite ease of use as the top buying criterion, and reimbursement policies increasingly recognize these rapid molecular results. Automation therefore propels the nucleic acid amplification testing market into lower-complexity laboratories without compromising accuracy.

Inclusion of NAAT in Blood-Screening Mandates

Window-period infections once slipped past serology; molecular assays now close that gap. National regulators in the United States, Japan, and parts of Europe require NAAT for HIV, HBV, and HCV screening, guaranteeing baseline demand for high-throughput instruments able to process thousands of donors daily. As more countries harmonize standards, the nucleic acid amplification testing market gains a stable, compliance-driven revenue stream in transfusion medicine.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Qualified Molecular Technologists | -1.2% | Global, most severe in emerging markets | Long term (≥ 4 years) |

| High Per-Test Cost of Proprietary Cartridge Systems | -0.9% | Global, particularly impactful in LMICs | Medium term (2-4 years) |

| Primer Redesign Needs Owing to Pathogen Mutations | -0.7% | Global | Short term (≤ 2 years) |

| Reagent Supply-Chain Vulnerabilities During Demand Surges | -0.5% | Global, with a greater impact in import-dependent regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Qualified Molecular Technologists

Vacancy rates in public-health and clinical labs climbed in 2024, increasing overtime costs and limiting batch runs. Training pipelines lag behind demand, and rural facilities struggle to offer competitive salaries. Consequently, vendors emphasize plug-and-play designs that require minimal expertise, ensuring the nucleic acid amplification testing market can still grow despite labor shortages.

High Per-Test Cost of Proprietary Cartridge Systems

Closed cartridges simplify workflows but add financial strain, especially in low-resource settings. A Unitaid report[3]Unitaid, “Gonorrhea Point-of-Care Diagnostics Technology and Market Landscape Report,” unitaid.org showed many STI programs shelved NAAT despite WHO recommendations because test prices exceed treatment costs. Manufacturers responding with microfluidic reagent-sparing designs may unlock untapped segments of the nucleic acid amplification testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Drive Recurring Revenue Streams

Consumables represented 56.78% of 2025 revenue, anchoring the nucleic acid amplification testing market with dependable, repeat sales tied directly to test volumes. Reagent kits, probe mixtures, and disposable cartridges form the backbone of laboratory budgets. Multi-year procurement contracts shield buyers from price swings and assure manufacturers of predictable run-rates, reinforcing the segment’s projected 9.28% CAGR. Meanwhile, smart packaging that embeds RFID tags supports automated inventory tracking, addressing stock-out risk and helping laboratories meet accreditation requirements. As point-of-care platforms proliferate, single-use cartridges become the dominant consumable form factor, further scaling the nucleic acid amplification testing market size for consumables.

Instruments and systems, although purchased less frequently, catalyze assay expansion. Modular analyzers that accept both PCR and isothermal chemistries protect capital investment and future-proof laboratories. Software and services revenue rises as facilities subscribe to cloud analytics and preventive-maintenance packages. Machine-learning upgrades that classify amplification curves in real time can be sold as annual licenses, giving vendors recurring top-line growth that rivals consumables within the nucleic acid amplification testing market.

By Technology: PCR Dominance Challenged by Isothermal Innovations

PCR held 67.12% nucleic acid amplification testing market share in 2025, leveraging decades of validation, robust supply chains, and a vast installed base. Vendors refine multiplex kits to detect up to 30 targets, making PCR panels competitive with newer syndromic arrays. High-speed thermal cyclers now complete 45-cycle runs in under 20 minutes, keeping PCR relevant even when rapid results are mandatory.

Isothermal nucleic-acid amplification technology is projected to post a 9.94% CAGR, the fastest in the nucleic acid amplification testing market. LAMP’s six-primer architecture confers exceptional specificity, and colorimetric readouts remove the need for fluorescence optics, cutting hardware costs. Recombinase polymerase amplification operates at body temperature, simplifying heater design for portable devices. These attributes position isothermal tools for field diagnostics, border-screening, and emergency triage. Ligase chain reaction, albeit niche, remains indispensable for single-nucleotide variant confirmation in targeted oncology assays, securing a small but stable slice of the nucleic acid amplification testing market.

By Application: Infectious Disease Testing Expands Beyond COVID-19

Infectious diseases contributed 61.95% of revenue in 2025. COVID-19 volumes have normalized, yet syndromic panels for respiratory and gastrointestinal pathogens continue climbing. Expanded WHO guidelines on tuberculosis endorse molecular assays like Xpert Ultra, ensuring sustained uptake in high-burden nations. Sexually transmitted infection testing also expands as programs move from syndromic treatment to etiological diagnosis. The nucleic acid amplification testing market size for infectious disease therefore remains robust despite pandemic tapering.

Oncology is forecast for the highest growth at 9.06% CAGR. Liquid biopsy permits serial monitoring, driving recurrent revenue per patient. Laboratories integrate ctDNA panels into comprehensive genomic profiling workflows, attracting precision-therapy referrals. Genetic and mitochondrial disorder testing is another growth pocket, as newborn-screening programs adopt next-generation sequencing combined with amplification confirmations to ensure accuracy. These diversified applications collectively broaden the nucleic acid amplification testing market.

By End-User: Hospitals Lead While Reference Laboratories Grow Fastest

Hospitals captured 47.63% of 2025 revenue. Many institutions now install rapid molecular platforms in emergency departments to guide admission decisions within 30 minutes. Pharmacogenomic assays tailored to cardiology and psychiatry are gaining traction, widening test menus and reinforcing hospital dominance in the nucleic acid amplification testing market.

Reference laboratories are slated for an 8.66% CAGR, boosted by national programs outsourcing high-plex oncology panels and rare pathogen screens. Centralized labs leverage economies of scale to offer broad test menus cost-effectively, drawing samples from physician-office networks. Public-health labs adopt molecular workflows for surveillance, and retail health chains pilot influenza-COVID combo tests using cartridge-based analyzers. Each setting adds incremental volumes, expanding the overall nucleic acid amplification testing market size across end-user categories.

Geography Analysis

North America retained 43.10% of global revenue in 2025, supported by mature reimbursement, continuous innovation, and early adoption of digital-health integrations. Precision-oncology programs bolster molecular volumes, and capitated payment models reward faster, more accurate diagnoses. Cloud-based result portals allow rural clinicians to access expert molecular data, extending specialty care beyond tertiary hospitals. The nucleic acid amplification testing market is expected to advance at a steady pace as these dynamics deepen.

Asia-Pacific is projected for the fastest 9.88% CAGR, propelled by rising health budgets and domestic manufacturing. China’s provincial procurement schemes favor made-in-China instruments, accelerating local adoption. India’s public-private laboratory networks are expanding molecular menus in tuberculosis and HIV programs, offering vendors scale. Portable isothermal systems remove infrastructure barriers in Southeast Asia, further enlarging the nucleic acid amplification testing market.

Europe commands a significant share with an 8.01% CAGR outlook. Stringent quality regulations mandate standardized result reporting, boosting demand for instruments with built-in audit trails. Funding initiatives such as the EU4Health program finance molecular upgrades across member states, sustaining growth. The Middle East & Africa will grow at 9.52% CAGR; Gulf countries invest in world-class hospital complexes featuring full molecular suites, while donor-funded programs retrofit GeneXpert systems for broader disease panels. South America is set for 8.97% CAGR as Brazil and Colombia expand universal-health coverage and adopt rapid molecular diagnostics for Zika, dengue, and COVID-flu combos. Together, these regions deepen global penetration, lifting the nucleic acid amplification testing market.

Competitive Landscape

The nucleic acid amplification testing market shows moderate concentration: the top five firms hold a large chunk of revenue share, leaving space for regional specialists and technology disruptors. Abbott, Roche, and Thermo Fisher Scientific expand via acquisitions that bundle sample prep, amplification, and post-analytic software into a single ecosystem. This one-vendor approach appeals to hospital administrators seeking integrated solutions that minimize validation labor.

Mid-tier innovators capture niches through isothermal chemistries, CRISPR-based detection, and AI-powered decision support. For example, Synoligo Biotechnologies’ TR-FRET probes sharpen sensitivity in portable assays, challenging incumbent PCR systems. Start-ups leverage cloud platforms to deliver real-time epidemiological dashboards, a service that larger firms may acquire to round out offerings.

Equipment openness is emerging as a differentiator; platforms that accept third-party reagents reduce consumable lock-in, a major concern for cost-constrained buyers. Several public tenders in Asia now require reagent interchangeability clauses, pressuring closed-cartridge incumbents to alter business models. Competitive intensity therefore remains high, and sustained R&D investment is essential to retain share in the nucleic acid amplification testing market.

Nucleic Acid Amplification Testing (NAAT) Industry Leaders

Abbott Laboratories

bioMérieux SA

F. Hoffmann-La Roche AG

Grifols SA

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Synoligo Biotechnologies partnered with Lumiphore to integrate TR-FRET probes into CRISPR-based assays, delivering higher sensitivity for portable infectious-disease tests.

- February 2025: The FDA cleared Abbott’s Alinity m You-Create for laboratory-developed molecular assays, giving clinical labs flexibility to design custom panels on a standardized platform.

- December 2024: WHO updated tuberculosis guidelines to endorse Xpert MTB/RIF and Xpert Ultra molecular assays for routine diagnosis and drug-resistance detection.

- July 2024: Roche completed its acquisition of LumiraDx, adding microfluidic point-of-care technology to its molecular portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the nucleic acid amplification testing (NAAT) market as all commercial in-vitro diagnostic assays, instruments, reagents, and software that detect specific DNA or RNA sequences in human clinical specimens by Polymerase Chain Reaction, Isothermal Technologies, or Ligase Chain Reaction. The focus stays on patient-care use across hospitals, independent and reference laboratories, and near-patient settings.

Scope Exclusion: Single-donor blood screening test kits sold only to blood banks and veterinary NAAT products remain outside countable revenue.

Segmentation Overview

- By Product

- Consumables

- Reagents

- Assay Kits

- Other Consumables

- Instruments & Systems

- Software & Services

- Consumables

- By Technology

- Polymerase Chain Reaction (PCR)

- Isothermal Nucleic Acid Amplification Technology (INAAT)

- Ligase Chain Reaction (LCR)

- By Application

- Infectious Disease

- COVID-19

- Sexually Transmitted Infections

- Mosquito Borne

- Gastrointestinal Infections

- Tuberculosis

- Hepatitis

- Other Infectious Diseases

- Oncology

- Genetic & Mitochondrial Disorder Testing

- Others

- Infectious Disease

- By End-User

- Hospitals

- Independent & Reference Laboratories

- Other End-Users

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with molecular laboratory directors, infectious-disease clinicians, procurement leads, and regional distributors across North America, Europe, Asia-Pacific, Latin America, and the Middle East validate incidence-based demand pools, price dispersion, and capacity utilization. These conversations allow us to fill data gaps surfaced during secondary review and to stress-test model assumptions before sign-off.

Desk Research

We first map the demand environment using open data from the World Health Organization, Centers for Disease Control and Prevention, European Centre for Disease Prevention and Control, and national ministries that publish infectious-disease incidence and cancer registry figures. Regulatory filings on the FDA 510(k) and European CE marking databases help our team track newly cleared NAAT platforms and their labeled claims, while peer-reviewed journals such as Clinical Infectious Diseases provide sensitivity benchmarks that inform likely adoption.

To size supply, Mordor analysts extract laboratory volumes from association portals such as the College of American Pathologists, merge shipment metadata available on Volza, and verify average selling prices through D&B Hoovers company filings and Dow Jones Factiva news archives. Patent trends from Questel signal upcoming innovations that may tilt future mix and pricing. The sources listed are illustrative only, and many additional references underpin our desk work.

Market-Sizing & Forecasting

A blended top-down and bottom-up model converts reportable disease incidence into likely NAAT test volumes, adjusts for test penetration, and multiplies by weighted average selling price to reach the 2025 baseline. Supplier roll-ups and channel checks offer a bottom-up approximation that is cross-verified against the incidence build. Key variables include reported PCR kit shipments, average throughput per installed analyzer, reimbursement tariff movements, prevalence of multi-plex panels, and oncology liquid-biopsy utilization rates. Five-year forecasts rely on multivariate regression that links volume growth to incidence trajectories, guideline changes, and expected price compression, all benchmarked with expert consensus. Gaps in bottom-up inputs are bridged through regional indexation to verified proxy metrics.

Data Validation & Update Cycle

Outputs pass anomaly checks, peer review, and senior analyst scrutiny before release. Models refresh annually, with interim updates triggered by material events such as large-scale outbreaks or pivotal technology approvals. A final validation pass occurs right before a client receives the deliverable.

Why Our Nucleic Acid Amplification Testing Baseline Commands Reliability

Published NAAT estimates often diverge because firms pick different product baskets, base years, and revision cadences. According to Mordor Intelligence, clarity on scope, live data feeds, and yearly refreshes hold the key to a dependable baseline.

Key gap drivers include varying inclusion of donor-screening assays, disparate ASP trajectories, and the choice of constant versus incidence-linked growth rates, which are then compounded by currency conversion practices and update frequency.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.31 B (2025) | Mordor Intelligence | - |

| USD 7.30 B (2022) | Global Consultancy A | Narrower scope; excludes INAAT and uses older base year |

| USD 10.11 B (2024) | Research Portal B | Adds blood-bank screening and OTC kits; uniform CAGR assumption |

| USD 9.60 B (2025) | Analytics Firm C | Counts contract manufacturing revenue; holds ASP flat |

These comparisons show that our disciplined variable selection and timely refresh give decision-makers a balanced, transparent starting point they can confidently build on.

Key Questions Answered in the Report

Which nucleic-acid amplification technique dominates routine laboratory testing?

Polymerase chain reaction (PCR) remains the workhorse because it delivers high analytical sensitivity, accepts many sample types, and integrates easily with automated workflows.

What makes isothermal amplification attractive for point-of-care use?

Isothermal chemistries operate at a constant temperature, eliminating bulky thermal cyclers and enabling battery-powered devices that clinicians can deploy in clinics, pharmacies, or field settings.

How do multiplex respiratory panels benefit patient management?

By identifying multiple pathogens in a single run, syndromic panels cut diagnostic uncertainty, support targeted antimicrobial therapy, and shorten the time from sample collection to clinical action.

Why are consumables such a crucial revenue stream for NAAT suppliers?

Every test consumes fresh reagents and cartridges, so recurring consumable purchases provide stable cash flow and align vendor incentives with laboratory throughput.

How is the shortage of molecular technologists influencing instrument design?

Vendors are prioritizing fully automated, sample-to-answer systems with built-in analytics so laboratories can maintain testing capacity even when skilled staff are limited.

What impact does circulating-tumor-DNA testing have on oncology practice?

Liquid-biopsy assays allow oncologists to monitor treatment response and detect minimal residual disease without invasive tissue sampling, enabling more timely therapy adjustments.

Page last updated on: