Life Coaching Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

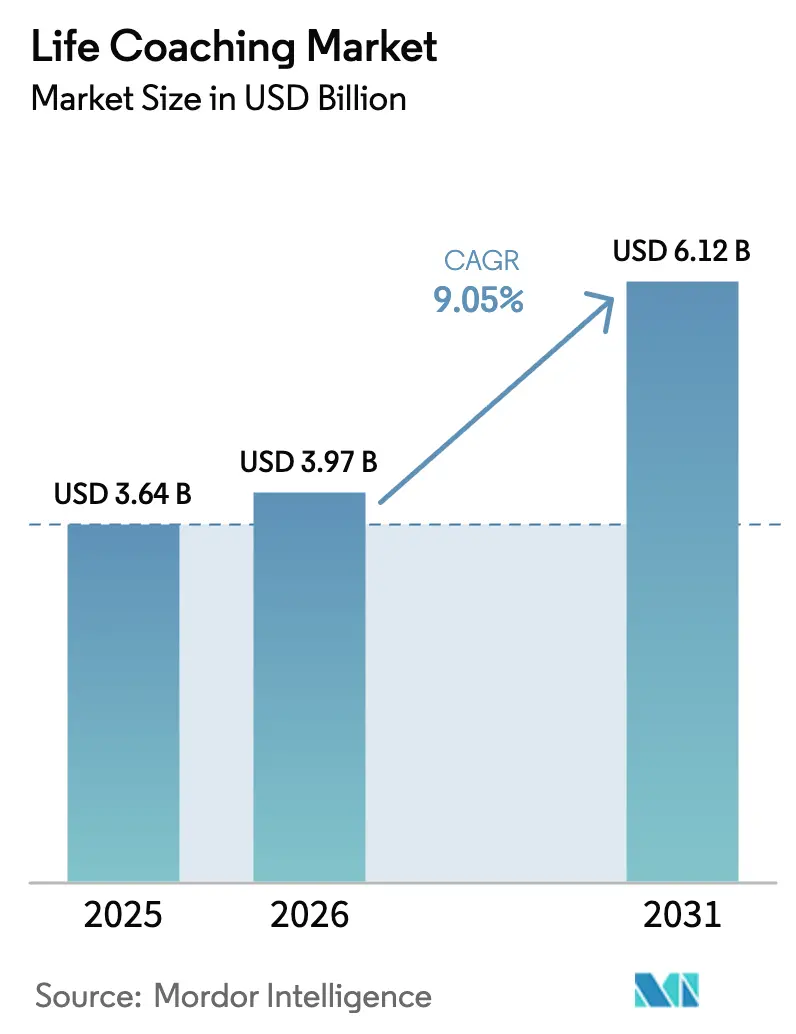

| Market Size (2026) | USD 3.97 Billion |

| Market Size (2031) | USD 6.12 Billion |

| Growth Rate (2026 - 2031) | 9.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Life Coaching Market Analysis by Mordor Intelligence

The life coaching market size was valued at USD 3.64 billion in 2025 and estimated to grow from USD 3.97 billion in 2026 to reach USD 6.12 billion by 2031, at a CAGR of 9.05% during the forecast period (2026-2031). Market momentum stems from a decisive migration to virtual platforms, heightened corporate spending on employee-development coaching, and broader consumer acceptance of subscription billing. Technology is reshaping delivery economics, with artificial-intelligence (AI) tools standardizing quality, expanding coach capacity, and delivering data-driven insights. Enterprise buyers view coaching as a measurable talent-retention lever, while individual clients link it to wellbeing, career agility, and purpose alignment. Regulatory clarity, particularly around coach credentials, remains a swing factor in unlocking institutional demand across regions.

Key Report Takeaways

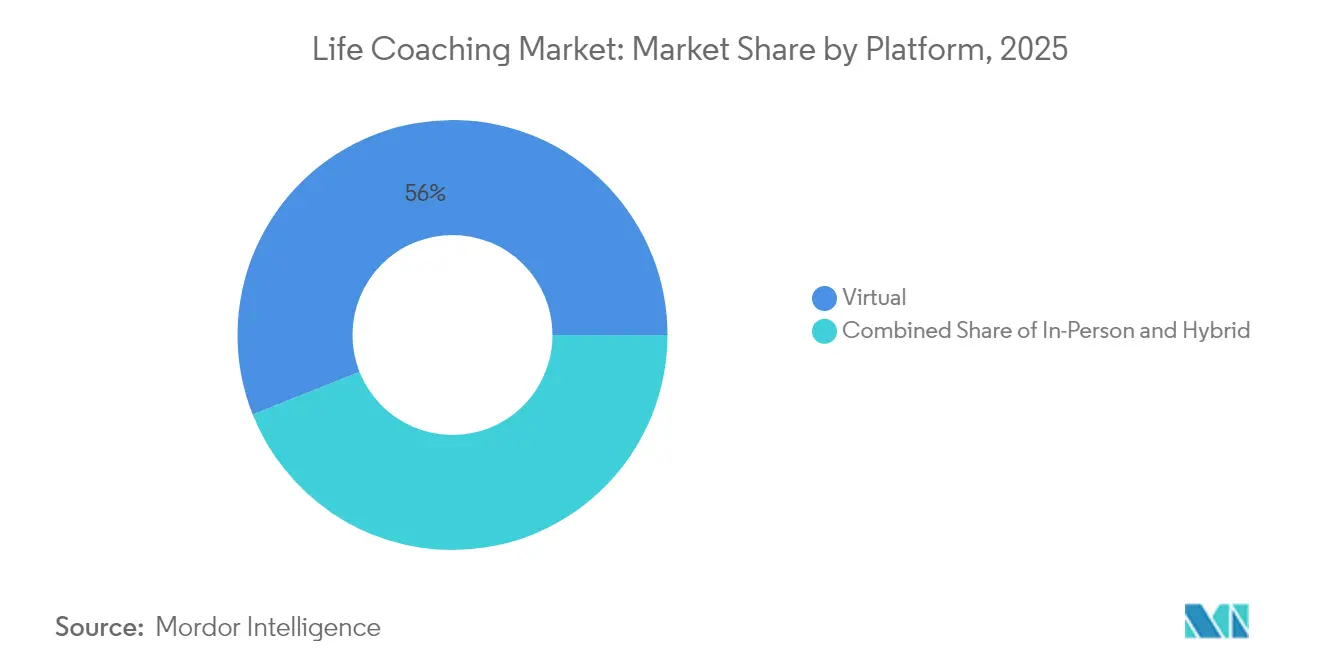

- By platform, virtual channels led with 56.02% of the life coaching market share in 2025, and the segment is tracking a 10.05% CAGR to 2031.

- By coaching type, career coaching held 27.25% revenue in 2025, while health and wellness coaching is expanding at an 11.35% CAGR through 2031.

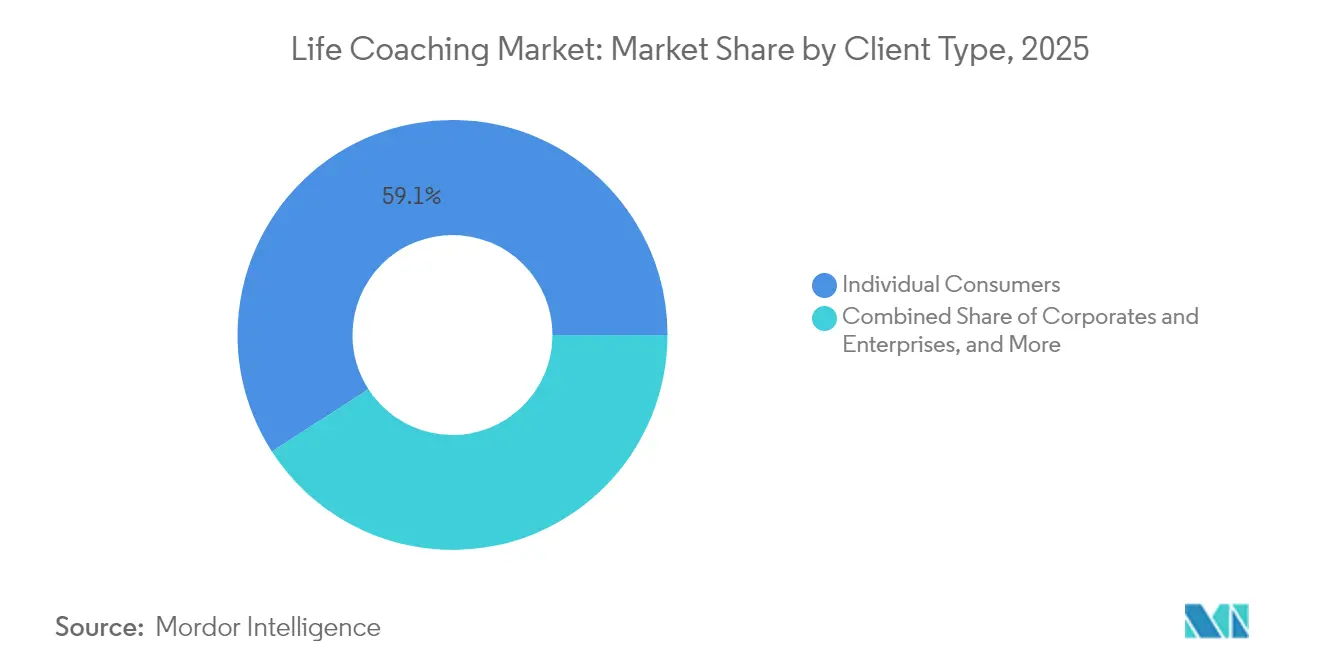

- By client type, individual consumers accounted for 59.12% share of the life coaching market size in 2025; corporate clients are advancing at a 9.55% CAGR over 2026-2031.

- By pricing model, subscriptions captured 45.05% revenue in 2025 and are scaling at a 10.9% CAGR through 2031.

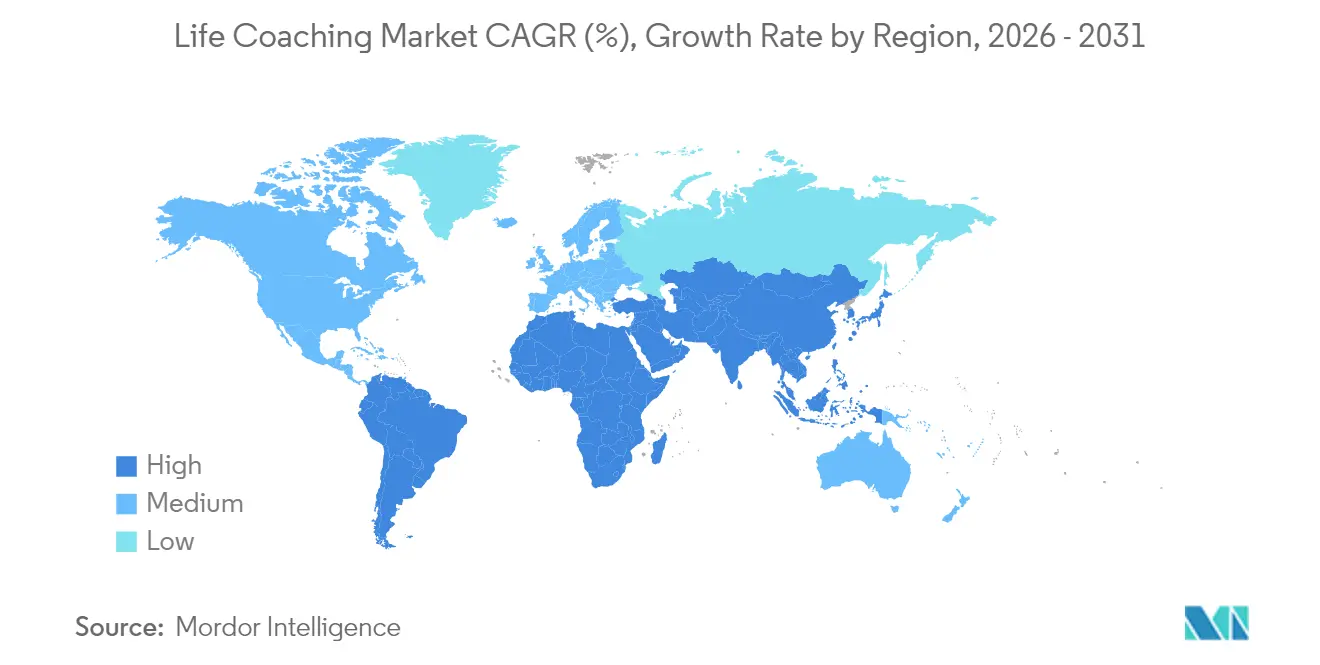

- By geography, North America contributed 38.35% of 2025 revenue; Asia-Pacific is the fastest-growing region at a 9.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Life Coaching Market Trends and Insights

Driver Impact Analyis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of virtual coaching platforms | +2.1% | Global, led by North America and Europe | Medium term (2–4 years) |

| Growing demand for career-development services | +1.8% | Global, strong in Asia-Pacific and North America | Long term (≥4 years) |

| Increased corporate investment in wellbeing | +2.3% | North America and Europe, spreading to Asia-Pacific | Medium term (2–4 years) |

| Rising disposable income and personal spending | +1.4% | Core in Asia-Pacific, emerging markets follow | Long term (≥4 years) |

| AI-powered personalized coaching affordability | +1.7% | Global, tech hubs lead | Short term (≤2 years) |

| Health-insurer reimbursement pilots | +0.8% | Primarily North America, pilots in Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Virtual Coaching Platforms

Digital platforms remove geography barriers and cut overhead, letting providers serve global clients with standardized quality and analytics dashboards. CoachHub’s February 2025 launch of AIMY, an AI-enabled assistant, shows how virtual systems scale personalization without adding headcount [1]CoachHub, “AIMY Launch Press Release,” coachhub.com. Service expansion across time zones and devices supports the 10.3% CAGR forecast for virtual delivery as firms prioritize scalable coaching for distributed staff.

Growing Demand for Career-Development Services

Career coaching retains 27.6% share because AI and automation are upending skills requirements across industries. Skillsoft’s 2025 report framed a USD 400 billion talent-development opportunity, with coaching a core pillar [2] Firstname Lastname, “Skillsoft Annual Report 2025,” skillsoft.com. Companies routinely invest USD 10,000–50,000 per executive to support reskilling and career navigation. Formal credentials carry weight: more than 80% of clients insist on certified coaches, pushing adoption of International Coaching Federation standards.

Increased Corporate Investment in Employee-Wellbeing Coaching

Employers embed coaching in wellness programs to cut absenteeism and elevate engagement, fueling a 9.9% CAGR in enterprise demand. Google and IBM publicly champion executive coaching as a leadership staple, and 92% of firms now include emotional-health components in wellness offerings. By aligning well-being with productivity metrics, corporations elevate coaching from a perk to a strategic necessity.

AI-Powered Personalized Coaching Scaling Affordability

AI engines interpret behavioral, biometric, and contextual data to deliver granular guidance at a lower cost. Maxiom’s USD 2 million seed round for a genetics-driven health-coach platform illustrates investor appetite for data-rich models. Stanford researchers showed that large language models can tailor fitness regimens around user barriers, reinforcing AI’s role in democratizing premium coaching.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of formal accreditation and standards | -1.2% | Global, varied regional approaches | Medium term (2–4 years) |

| High cost of personalized coaching sessions | -0.9% | Global, stronger among individual buyers | Short term (≤2 years) |

| Reputational risks from uncertified coaches | -0.6% | Global, high social-media penetration zones | Medium term (2–4 years) |

| Data-privacy concerns in recorded sessions | -0.4% | Europe and North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Lack of Formal Accreditation and Standards

Coaching remains largely unregulated. Utah’s 2024 Sunrise Review logged more than 200 practitioners with divergent training levels, underscoring consistency. The International Coaching Federation argues for unified self-regulation, yet the voluntary model lets uncertified providers compete on price, hindering institutional adoption.

High Cost of Personalized Coaching Sessions

Executive coaching routinely commands USD 300–500 per hour, limiting access for mid-income consumers. Subscriptions spread costs over time, but the labor-intensive nature of one-to-one engagements caps addressable volume. AI chatbots and group programs aim to close the affordability gap, though clients still prize human rapport for sensitive topics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Virtual leadership continues

Virtual channels generated 56.02% of 2025 revenue and are powering a 10.05% CAGR through 2031. AI companions such as AIMY enrich coach capacity while dashboards quantify progress. In-person engagements remain relevant for executive confidentiality and experiential retreats, yet hybrid strategies increasingly combine remote cadence with quarterly face-to-face intensives. Enterprises embrace virtual suites to train dispersed talent without travel budgets, while solo practitioners rely on video platforms to attract cross-border clients, thereby reinforcing the life coaching market’s digital tilt.

Second-order effects include richer data ecosystems. Session metadata, micro-learning completions, and pulse surveys feed analytics modules that track behavioral change. This evidence orientation reassures procurement officers that coaching budgets link to measurable KPIs, advancing contract renewals. Meanwhile, regulatory frameworks such as Europe’s GDPR push platform vendors toward bank-grade encryption and region-specific data hosting. Providers that certify compliance differentiate in government and financial-services tenders, deepening market segmentation by security posture.

By Coaching Type: Career dominance, wellness acceleration

Career coaching held 27.25% share in 2025, underpinned by rapid job disruption. Reskilling urgency elevates one-to-one guidance from perk to necessity, especially during AI-triggered role redesigns. Leadership tracks command premium fees, reinforcing revenue concentration in this segment. Credentials from the International Coaching Federation and related bodies enhance coach credibility for corporate buyers who must verify vendor quality.

Health and wellness coaching is growing fastest at 11.35% CAGR. Medicare’s 2024 decision to reimburse preventive coaching expanded addressable demand, signalling insurer confidence in non-pharmacological interventions. Start-ups integrate wearable feeds and DNA testing to personalise action plans, resonating with biohackers and chronic-disease patients. Wellness programs also counter burnout, pushing HR departments to package stress coaching within holistic benefits. Relationship, financial, and spiritual coaching occupy niche but durable lanes, attracting clients seeking specialist-led transformation.

By Client Type: Consumers lead, corporates surge

Individual buyers contributed 59.12% of 2025 revenue, reflecting rising personal-development spending among millennials and Gen Z. Mobile first design, in-app communities, and pay-as-you-grow packages meet gig-economy requirements, sustaining loyalty. Yet corporate uptake is surging at 9.55% CAGR as CFOs connect coaching with retention savings. Large accounts negotiate enterprise contracts covering hundreds of mid-managers, shifting revenue mix toward B2B. Institutional acceptance hinges on vendor credentialing and data security, nudging platforms to add compliance modules.

Educational institutions and nonprofits represent emerging sub-segments. Universities embed coaching into career-services syllabi to improve graduate outcomes, while NGOs use leadership coaching to bolster internal capacity. These categories appreciate discounted group sessions and digital resource libraries that stretch limited budgets, broadening life coaching market penetration.

By Pricing Model: Subscriptions reshape economics

Subscriptions held 45.05% of 2025 revenue and are advancing at 10.9% CAGR, marking a shift from transactional to relationship models. Predictable billing aligns with corporate procurement cycles and stabilizes coach income. Passion.io reports higher customer lifetime value when communities and content libraries accompany monthly access . Per-session billing persists for discreet interventions such as interview preparation, though price visibility pressures margins in commoditized niches.

Annual retainers and tiered packages complement subscriptions by bundling assessments, on-demand micro-learning, and progress analytics. Hybrid monetization—mixing AI chatbots for everyday queries and live sessions for deep dives—lowers average cost while preserving premium support. Scalability encourages venture capital inflows, as recurring revenue attracts valuations akin to software companies.

Geography Analysis

North America commanded 38.35% revenue in 2025. Mature corporate-wellness culture, strong disposable income, and headquarters of major platforms such as BetterUp underpin leadership. The region’s life coaching market size is on track for an 7.75% CAGR through 2031, supported by state-level mental-health mandates and tax-advantaged wellness spending.

Asia-Pacific is expanding fastest at a 9.6% CAGR. China scales coach adoption within state-owned enterprises pursuing productivity gains, while India’s growing IT workforce embraces online guidance for career mobility. Rising urban wages and cultural acceptance of coaching normalize paid self-improvement. Mobile penetration allows platforms to skip brick-and-mortar infrastructure, stretching reach into tier-two cities, thereby enlarging the life coaching market.

Europe remains a significant contributor, driven by employee wellbeing directives and GDPR-driven data safeguards. The United Kingdom capitalizes on robust financial and consulting sectors, whereas Germany links coaching to apprenticeship programs. EU AI regulation shapes vendor roadmaps, favoring companies that embed ethical-AI protocols early, which influences platform differentiation across the continent.

Competitive Landscape

The sector is fragmented, with thousands of sole proprietors coexisting alongside venture-backed platforms chasing scale. BetterUp achieved a USD 4.7 billion valuation in 2025 after raising USD 300 million in Series E funding, reflecting investor belief in B2B subscriptions. CoachHub generated USD 231.2 million revenue in 2024 and uses a full-stack platform to combine human coaches with AIMY AI for workflow automation.

Emerging entrants differentiate through deep tech. Maxiom applies genetic and wearable data to customize wellness regimens, while Stanford’s GPT-Coach research signals academic interest in language-model-driven personalization. White-space opportunities include niche verticals such as financial-literacy coaching, compliance-ready platforms for regulated industries, and multicultural coach networks matching global teams.

Consolidation is accelerating. ZRG’s purchase of Bravanti and Keystone Partners’ takeover of CCI Consulting demonstrate roll-up strategies that blend assessment, search, and coaching under one roof. Buyers seek cross-sell synergies and geographic coverage; sellers gain capital for tech upgrades and accreditation programs. Competitive intensity centers on AI roadmaps, enterprise integrations, and evidence-based outcomes.

Life Coaching Industry Leaders

BetterUp Inc.

CoachHub GmbH

Noom Inc.

Thriveworks Counseling

Coaching.com Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: CoachHub introduced AIMY, an AI-guided module that augments human coaching with real-time nudges, widening access for global users.

- February 2025: CPAClub released CPAClub Coach, an AI tool designed to guide certified public accountants on professional growth pathways.

- December 2024: CoachHub secured USD 42.3 million in debt financing, lifting total funding to USD 334 million to accelerate geographic expansion.

- October 2024: Harvard Business Review reported global corporate wellness outlays will exceed USD 94.6 billion by 2026, yet many programs underperform on wellbeing metrics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the life coaching market as the annual gross revenue earned worldwide from structured, fee-based coaching engagements that support personal, professional, and wellness goals across virtual, in-person, and hybrid delivery modes. Coaching packages, single sessions, subscription plans, and group programs sold by certified or non-certified practitioners are counted; adjacent mentoring, therapy, and self-help books are not.

Scope exclusion: Apps that only provide self-guided content without a live coach are outside this study.

Segmentation Overview

- By Platform

- Virtual

- In-Person

- Hybrid

- By Coaching Type

- Career Coaching

- Executive and Leadership Coaching

- Health and Wellness Coaching

- Relationship / Family Coaching

- Financial Coaching

- Spiritual Coaching

- Confidence and Personal-Development Coaching

- By Client Type

- Individual Consumers

- Corporates and Enterprises

- Educational Institutions

- Non-profits and NGOs

- By Pricing Model

- Subscription-based

- Per-session

- Program / Package

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview independent life coaches, HR procurement heads, platform executives, and accreditation bodies across North America, Europe, and Asia-Pacific. Qualitative calls uncover real-world utilization rates, client churn, and emerging niches, which are then checked through short online surveys with practicing coaches and buyers to validate pricing tiers and session frequencies.

Desk Research

Our analysts first gather publicly available indicators that anchor the demand pool. Major references include trade surveys from the International Coaching Federation, labor statistics from the U.S. Bureau of Labor Statistics, import-export data for coaching platform software from UN Comtrade, and demographic wellness indices published by the World Health Organization. Company filings, SEC 10-Ks, and investor decks hint at corporate spending shifts, while press releases track funding flows into digital coaching platforms. Select paid databases such as D&B Hoovers (coach company revenues) and Dow Jones Factiva (deal news) supplement the view.

These sources reveal coach population growth, average hourly fees, corporate training budgets, and regional digital adoption, supplying boundary conditions for volume and price. The list is illustrative; many other repositories were reviewed to confirm data points and clarify gray areas.

Market-Sizing & Forecasting

A top-down construct begins with coach population estimates by region and average fee income, rebuilt from accreditation counts and BLS occupational data, which are then cross-checked against corporate learning budgets and consumer wellness spend. Select bottom-up checks, such as sampled platform gross merchandising value and coach revenue roll-ups, help fine-tune totals. Key variables tracked include: 1. Certified coach headcount growth, 2. Median session price movement, 3. Corporate learning and development outlay, 4. Penetration of virtual delivery, 5. Disposable income per adult.

Multivariate regression relates these drivers to historical market size and projects forward; scenario analysis overlays optimistic and restrained adoption pathways. Gaps in bottom-up samples are bridged by median fee multipliers validated during interviews.

Data Validation & Update Cycle

Outputs pass a two-step peer review, followed by anomaly checks against third-party signals such as payment processor data and platform funding rounds. The model refreshes annually, with interim revisions whenever material events, large regulatory changes or landmark platform launches, shift any core variable. A fresh analyst pass precedes every client delivery so users receive the latest view.

Why Mordor's Life Coaching Baseline Earns Trust

Published estimates vary widely because firms choose different scopes, count only practitioner fee income or, conversely, lump in adjacent training content. Exchange-rate assumptions and refresh cadence add further spread.

Key gap drivers include: some studies focus on the U.S. alone, others track only certified coaches, and many apply flat fee averages without validating real price dispersion, whereas Mordor blends certified and non-certified data, reconciles regional fee ladders, and updates annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.64 B (2025) | Mordor Intelligence | - |

| USD 3.40 B (2024) | Global Consultancy A | Counts virtual platforms only; excludes in-person revenue and applies fixed 60 min session length for ASP |

| USD 5.34 B (2025) | Industry Association B | Measures coach fee income only; omits group programs and corporate subscription spend |

| USD 1.98 B (2024, U.S.) | Trade Journal C | Geography limited to United States, then extrapolated trend globally without adjusting for lower fee levels in emerging regions |

The comparison shows that once scope and variables differ, figures diverge swiftly. Mordor's disciplined blend of coach census data, price stratification, and cross-checks with spending proxies provides a balanced, transparent baseline that decision-makers can retrace and reproduce with confidence.

Key Questions Answered in the Report

What is the current life coaching market size and growth outlook?

The life coaching market was valued at USD 3.64 billion in 2025, is estimated at USD 3.97 billion in 2026, and is forecast to reach USD 6.12 billion by 2031, reflecting a 9.05% CAGR.

Which platform type dominates the life coaching market?

Virtual platforms delivered 56.02% of global revenue in 2025 and are on course for a 10.05% CAGR thanks to AI tools and enterprise demand.

Why is health and wellness coaching growing faster than other segments?

Medicare’s 2024 reimbursement policy and rising preventive-care awareness are driving an 11.35% CAGR for health and wellness coaching.

How are subscription models changing life coaching economics?

Subscriptions commanded 45.05% revenue in 2025 and are expanding at 10.9% CAGR, giving clients continuous access while stabilizing provider income.

Which region offers the highest growth potential for coaching providers?

Asia-Pacific is projected to expand at a 9.6% CAGR through 2031 due to rising corporate wellness adoption and increasing disposable income.

What are the main challenges hindering faster market expansion?

Key headwinds include inconsistent accreditation standards, high one-to-one coaching costs, and data-privacy concerns in recorded virtual sessions.

Page last updated on: