Personal Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

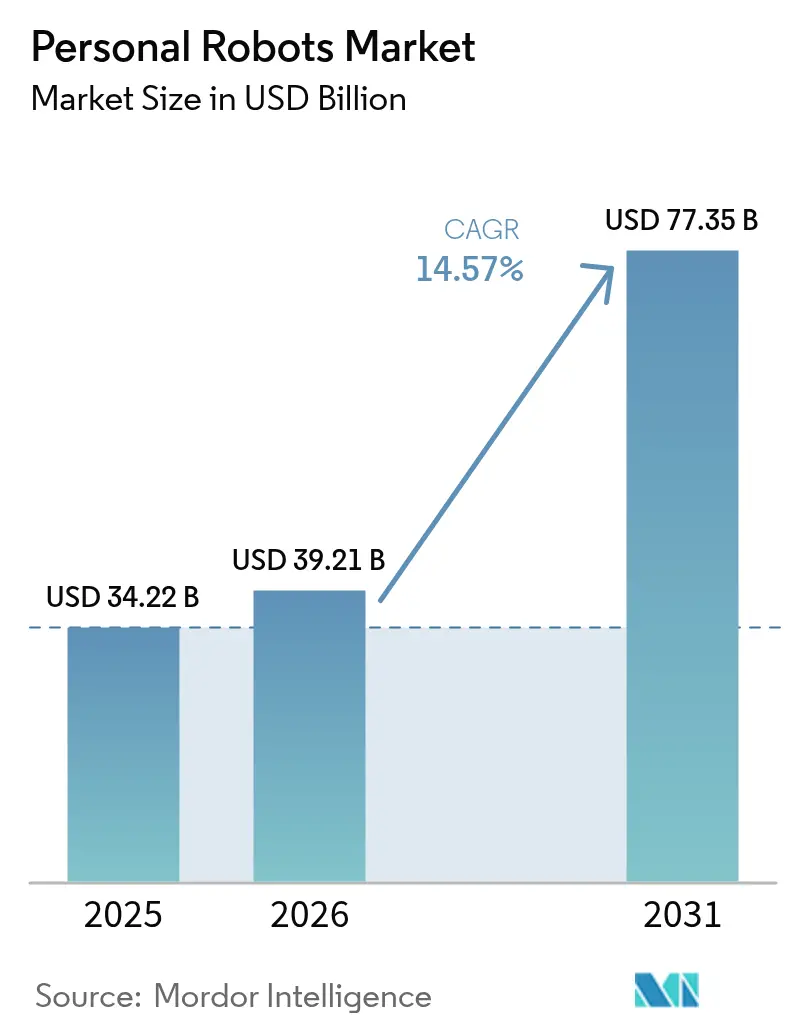

| Market Size (2026) | USD 39.21 Billion |

| Market Size (2031) | USD 77.35 Billion |

| Growth Rate (2026 - 2031) | 14.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Robots Market Analysis by Mordor Intelligence

The personal robots market size was valued at USD 34.22 billion in 2025 and estimated to grow from USD 39.21 billion in 2026 to reach USD 77.35 billion by 2031, at a CAGR of 14.57% during the forecast period (2026-2031). Growth rides on three converging forces: affordable on-device AI, aging societies that need care assistance, and navigation software that lets robots move safely around cluttered homes. Vacuum cleaners remain the primary revenue engine, proving that consumers trust autonomous devices and are willing to let them roam freely. Asian manufacturers dominate component supply, giving the region cost advantages that accelerate global adoption. Meanwhile, cloud-based software and subscription add-ons have begun to reshape revenue models, turning one-time hardware sales into recurring income streams.

Key Report Takeaways

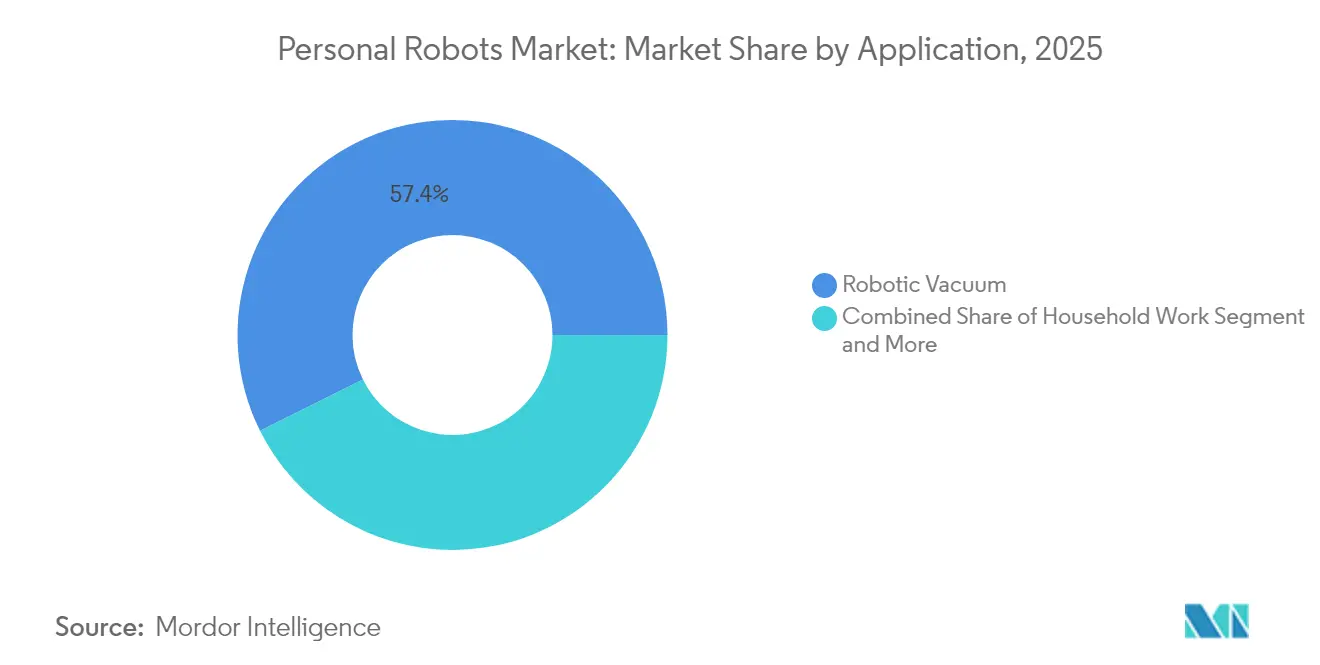

- By application, household work still commanded 57.35% of the personal robots market share in 2025, but elderly & handicap assistance is forecast to post the fastest 23.2% CAGR to 2031.

- By mobility, mobile wheeled designs held 66.20% revenue share in 2025; humanoid bipedal systems are poised for the quickest 28.4% CAGR through 2031.

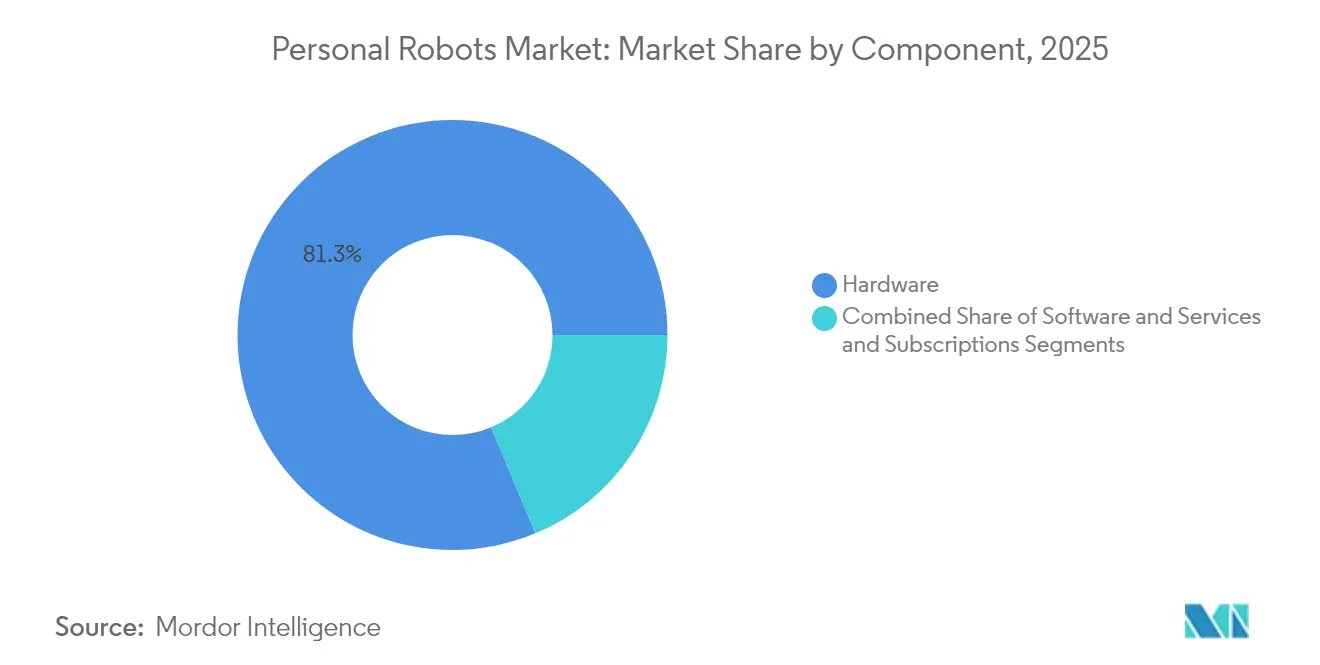

- By component, hardware accounted for 81.30% of the personal robots market size in 2025, while services and subscriptions are expanding at 21.6% CAGR.

- By control interface, app-controlled units led with 43.40% share in 2025, yet fully autonomous robots are accelerating at 26.9% CAGR.

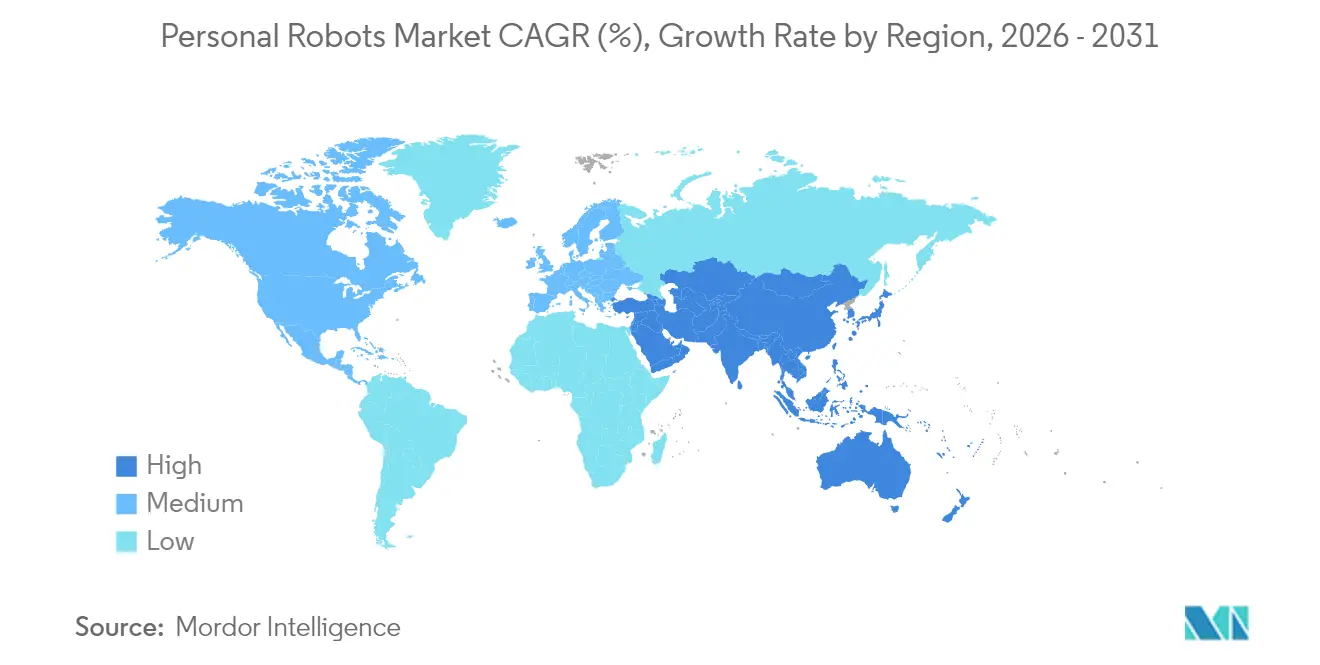

- By geography, Asia-Pacific secured 34.60% revenue share in 2025; the Middle East is the fastest-growing region with a 19.1% CAGR out to 2031.

- Ecovacs, Roborock and iRobot together captured nearly one-third of 2024 shipments, yet iRobot’s Q4 2024 revenue fell 45%, signaling intensifying price pressure.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Robots Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Boom in household robotic vacuum adoption | 3.2% | Global, with strongest penetration in North America and Europe | Short term (≤ 2 years) |

| Increased availability of low-cost AI processors | 2.8% | APAC core manufacturing, spill-over to global markets | Medium term (2-4 years) |

| Integration with smart-home ecosystems | 2.1% | North America and EU leading, expanding to APAC urban centers | Medium term (2-4 years) |

| Ageing-in-place initiatives in OECD countries | 3.5% | OECD countries, with early gains in Japan, Germany, South Korea | Long term (≥ 4 years) |

| Hospital pilot programs for in-room delivery | 1.4% | North America and EU healthcare systems | Medium term (2-4 years) |

| Open-source ROS-based platforms lowering entry barriers | 1.8% | Global, with concentration in tech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Boom in Household Robotic Vacuum Adoption

Robotic vacuums normalized the very idea of letting an autonomous device roam inside private spaces, lowering psychological and technical barriers for more complex helpers. Chinese vendors scaled production and undercut prices, pushing iRobot into a 45% revenue slide in Q4 2024 while Ecovacs logged RMB 16.54 billion in sales[1]Dyson, “Dyson 360 Vis Nav robot vacuum cleaner,” dyson.com and Roborock RMB 11.95 billion in the same year. Premium players kept margins by touting performance; Dyson’s 360 Vis Nav model ships with six-times competitor suction at a USD 799.99 price, proving that high-spec niches can coexist with mass adoption.

Increased Availability of Low-Cost AI Processors

Specialized chips from Qualcomm and NVIDIA are halving core component costs, trimming a humanoid bill-of-materials from USD 35,000 in 2025 to as low as USD 13,000 by 2030-35.[2]Bank of America Institute, “Transformation: Humanoid Robots 101,” institute.bankofamerica.com The new economics let startups like Figure AI move domestic pilots up by two years, while China’s UBTech readies mass production for Walker S2 units in late 2025.

Integration with Smart-Home Ecosystems

Robots now serve as mobile nodes in a multi-device household. Amazon’s million-robot milestone and Samsung’s USD 180 million stake in Rainbow Robotics show that big-tech is racing to fold robots into existing IoT frameworks. SwitchBot’s K20 Plus Pro can convert from vacuum to air purifier or delivery cart using modular add-ons,[3]SwitchBot, “K20 Plus Pro Modular Robot,” switch-bot.com underscoring a shift from hardware specs to seamless ecosystem performance.

Ageing-in-Place Initiatives in OECD Countries

Governments face shrinking caregiver pools and soaring medical bills. Japan’s METI and AMED fund pilot deployments, while research indicates hospital falls alone cost USD 50 billion each year—an expense that preventive robotics can meaningfully cut. Field studies in Australian nursing homes confirm that staff accept robots once training and workflow changes are in place.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data-privacy concerns around home mapping | -2.3% | EU and North America regulatory environments | Short term (≤ 2 years) |

| High replacement cost of batteries and sensors | -1.8% | Global, with higher impact in price-sensitive markets | Medium term (2-4 years) |

| Fragmented global safety standards | -1.5% | Global, with regional compliance variations | Long term (≥ 4 years) |

| Limited SLAM accuracy in cluttered Asian apartments | -0.9% | APAC urban centers, particularly dense housing markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Concerns Around Home Mapping

Strict regimes such as GDPR require explicit consent for the maps and behavioral data robots collect. A January 2025 YouGov poll found privacy ranked as the top barrier for 48% of Americans considering a household robot, just ahead of reliability worries at 49%. Firms now spend heavily on on-device processing, data localization and user-controlled sharing to satisfy regulators.

High Replacement Cost of Batteries and Sensors

Consumables can equal 20-40% of a unit’s lifetime cost. Lithium-ion packs run USD 200-800 and LiDAR sensors USD 1,000-3,000, forcing owners into expensive mid-life overhauls. Annual upkeep typically adds 5-12% of purchase price, driving suppliers toward modular designs and predictive maintenance to soften sticker shock—yet those measures raise initial R&D spend.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Cleaning Dominance Yields to Care Innovation

Household work robots generated the largest slice of 57.35% in the personal robots market in 2025. Vacuum cleaners deliver clear time savings and predictable outcomes, sustaining user trust and high repeat-buy intent. Entertainment robots such as Mixi’s CES-winning Romi have broadened category visibility. Meanwhile, elderly & handicap assistance is scaling fastest at a 23.2% CAGR as hospitals pilot in-room delivery and families seek reliable toileting, medication and fall-alert support.

The revenue shift illustrates a maturing category moving from convenience to necessity. As unit tasks diversify, subscription software for mapping, AI upgrades and diagnostics further expands the personal robots market size for service providers.

By Mobility: Wheeled Systems Bridge to a Bipedal Future

In 2025, mobile wheeled designs captured 66.20% of total value thanks to efficient power draw and affordable parts. Stationary models remain niche, focused on security or local telepresence.

Humanoid bipedal forms are the growth story, climbing at 28.4% CAGR through 2031. Figure AI’s USD 2.6 billion valuation and Genesis AI’s USD 105 million seed round highlight investor belief that bipedal machines will navigate human-built spaces with minimal modification, ultimately lifting the personal robots market share for bipedal systems as balance control and AI reasoning mature.

By Component: Hardware Foundation Enables Software Innovation

Hardware still owned 81.30% of 2025 outlays, reflecting the capital intensity of motors, sensors and frames. Falling sensor prices and AI chips have expanded addressable use-cases, yet safety, styling and tactile requirements keep BOMs high.

Services and subscriptions—mapping, firmware, cloud AI, remote diagnostics—are rising at 21.6% CAGR. Recurring packages lengthen product life, create stickier brands and incrementally grow the personal robots market size without large new hardware investments.

By Control Interface: Autonomy Advances Despite App Dominance

App-centric control led with 43.40% in 2025, leveraging familiar smartphone UX patterns. Voice interfaces surged once Alexa and Google Assistant enabled plug-and-play skill integration.

Full autonomy now records the fastest 26.9% CAGR. Multi-modal perception and large language models let robots interpret casual requests, a prerequisite for elderly care where users may lack technical fluency. Toyota’s alliance with Hyundai’s Boston Dynamics to apply generative AI shows manufacturers converging on hands-free operation.

Geography Analysis

Asia-Pacific held 34.60% of 2025 revenue, buoyed by China’s component scale and Japan’s elderly-care pilots. China’s humanoid robot market hit USD 2.9 billion in 2024 and is projected to soar past USD 46 billion by 2031 at a 48.6% CAGR, dwarfing global growth rates. Government subsidies, mature supply chains and cultural comfort with robotics sustain leadership. South Korea’s 5G infrastructure supports vision-heavy applications, while India’s urban middle class presents long-run volume upside once price points fall.

North America remains influential in AI research, venture funding and premium tiers. The United States recorded USD 0.56 billion in humanoid robot sales in 2024, and the region holds 47.5% of global humanoid revenue today. Interest levels are healthy—38% of Americans like the idea of a household robot—but 32% still cap their budget below USD 500, evidence of elasticity challenges that vendors must address through feature bundling or financing plans.

The Middle East is the fastest-growing region at 19.1% CAGR through 2031. Oil-funded diversification programs, retail expansion to USD 386.9 billion by 2028 and young tech-forward populations underpin demand. UAE and Saudi Arabia have carved out robotics test zones, while Israel’s startup ecosystem supplies AI talent. Turkey’s USD 20 billion home robotics spend in 2024 confirms appetite across non-Gulf economies, reinforcing the region’s role as an early target for premium and service-rich offerings.

Competitive Landscape

Market structure is moderately fragmented: the top five vendors control just under 50% of shipments. iRobot’s steep 45% Q4 2024 revenue slide revealed how quickly share can swing when lower-cost rivals match feature sets. Ecovacs and Roborock leveraged RMB-scale supply chains to grow 2024 sales to RMB 16.54 billion and RMB 11.95 billion respectively. Samsung secured a USD 180 million position in Rainbow Robotics, an indicator that consumer-electronics giants prefer acquisition over ground-up R&D.

Strategy falls into three lanes. First, premium performance illustrated by Dyson’s 360 Vis Nav that uses six-times competitor suction. Second, ecosystem integration typified by Amazon’s Astro tying into Ring security and Alexa voice. Third, cost leadership, dominated by Chinese firms iterating at lightning pace.

Emerging white-space is visible in logistics and healthcare. GXO Logistics inked a multi-year contract with Agility Robotics for warehouse bipedals, the first sizeable commercial rollout. Software is the new frontier: Figure AI’s valuation hinges on its Helix AI model, not on actuators, while Apptronik teams with Google DeepMind to fuse Gemini reasoning into its Apollo bots.

Personal Robots Industry Leaders

Sony Corporation

Honda Motor Company, Ltd.

Ecovacs Robotics Inc.

iRobot Corporation

Samsung Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Figure AI fast-tracked home trials, launching alpha testing two years early to exploit breakthroughs in Helix AI.

- February 2025: Bank of America Institute projected humanoid shipments will hit 18,000 units in 2025 and 1 million annually by 2030-35 as component costs fall.

- January 2025: Sony Honda Mobility debuted the AFEELA 1 EV with 40 sensors and AI-centric UX; deliveries start mid-2026.

- January 2025: UBTech confirmed mass production of Walker S2 humanoids for late 2025, targeting 500-1,000 industrial units.

Global Personal Robots Market Report Scope

Personal robots are designed for personal activities like household work, education, entertainment, and education. Its design and human interface make it useful for individuals. The market studied has been segmented based on the types of personal robots and geography. The study includes a comprehensive analysis of the personal robots market based on several aspects, such as demand and supply, technological trends, susceptibility to innovation, and future growth prospects. The study also includes a detailed analysis of COVID-19 impact on the personal robots market.

| Household Work |

| Entertainment and Social Companion |

| Elderly and Handicap Assistance |

| Home Security and Surveillance |

| Education and Research |

| Stationary |

| Mobile Wheeled |

| Humanoid Bipedal |

| Hardware |

| Software |

| Services and Subscriptions |

| App-Controlled |

| Voice-Controlled |

| Gesture / Vision-Controlled |

| Fully Autonomous |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Household Work | |

| Entertainment and Social Companion | ||

| Elderly and Handicap Assistance | ||

| Home Security and Surveillance | ||

| Education and Research | ||

| By Mobility | Stationary | |

| Mobile Wheeled | ||

| Humanoid Bipedal | ||

| By Component | Hardware | |

| Software | ||

| Services and Subscriptions | ||

| By Control Interface | App-Controlled | |

| Voice-Controlled | ||

| Gesture / Vision-Controlled | ||

| Fully Autonomous | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the personal robots market?

It is valued at USD 39.21 billion in 2026 and projected to reach USD 77.35 billion by 2031.

Which application dominates spending today?

Household work robots, mainly vacuum cleaners, accounted for 57.35% of 2025 revenue.

Which mobility type is growing fastest?

Humanoid bipedal robots lead growth with a 28.4% CAGR through 2031 as balance control and AI reasoning mature.

Why is Asia-Pacific ahead in adoption?

The region combines manufacturing scale, government support and cultural acceptance, giving it a 34.60% revenue lead in 2025.

What restrains faster uptake in North America and Europe?

Consumer privacy concerns surrounding home mapping and data handling impose regulatory and design costs that slow rollout.

How are vendors shifting their revenue models?

Firms now package cloud mapping, AI upgrades and predictive maintenance as subscriptions, boosting recurring income streams alongside hardware sales.

Page last updated on: