Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

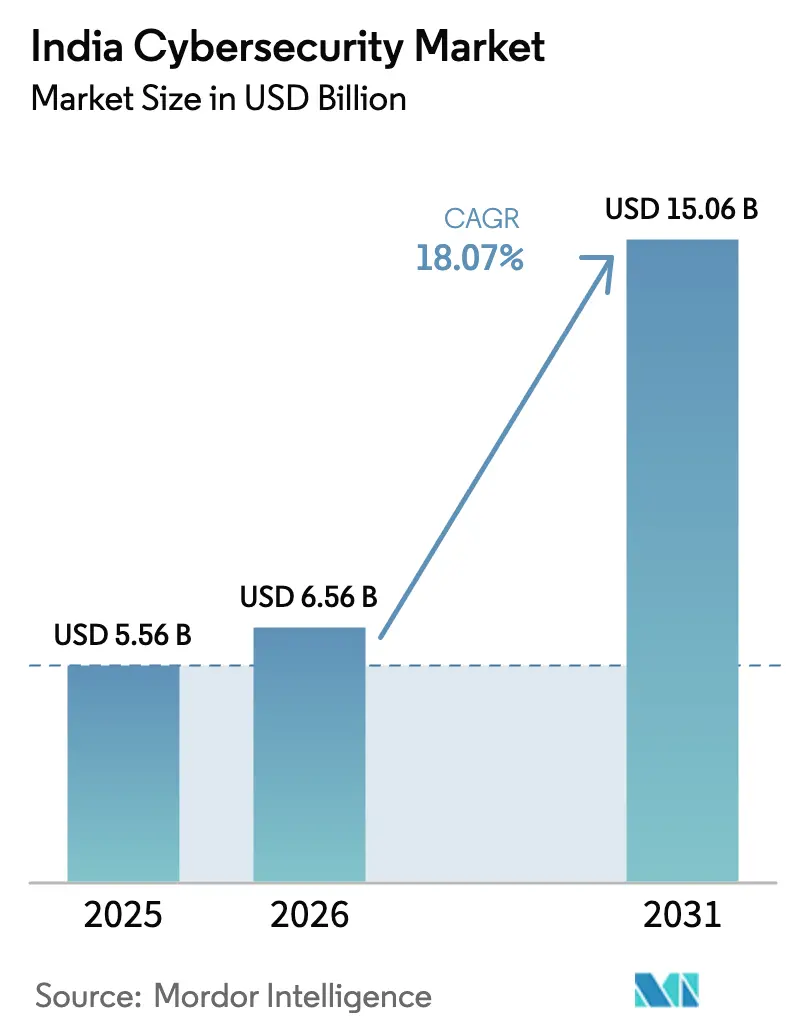

| Base Year Market Size (2025) | USD 5.56 Billion |

| Market Size (2026) | USD 6.56 Billion |

| Market Size (2031) | USD 15.06 Billion |

| Growth Rate (2026 - 2031) | 18.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Cybersecurity Market Analysis by Mordor Intelligence

The India cybersecurity market size was valued at USD 5.56 billion in 2025 and estimated to grow from USD 6.56 billion in 2026 to reach USD 15.06 billion by 2031, at a CAGR of 18.07% during the forecast period (2026-2031). Cloud-first public programs, rising breach volumes, and tougher data-protection rules combine to keep spend growth well above the global average. The Digital Personal Data Protection Act (DPDPA) imposes steep penalties, so boards are accelerating encryption, monitoring, and incident-response outlays. Real-time payments, especially UPI, create identity-fraud pressure that steers budgets toward zero-trust controls. Managed detection and response contracts multiply as enterprises confront a talent shortfall, while venture funding props up home-grown innovators that address India-specific threat patterns. Overall, the market is pivoting from point tools to platform approaches that promise faster compliance, lower mean-time-to-detect, and deeper network-security convergence.

Key Report Takeaways

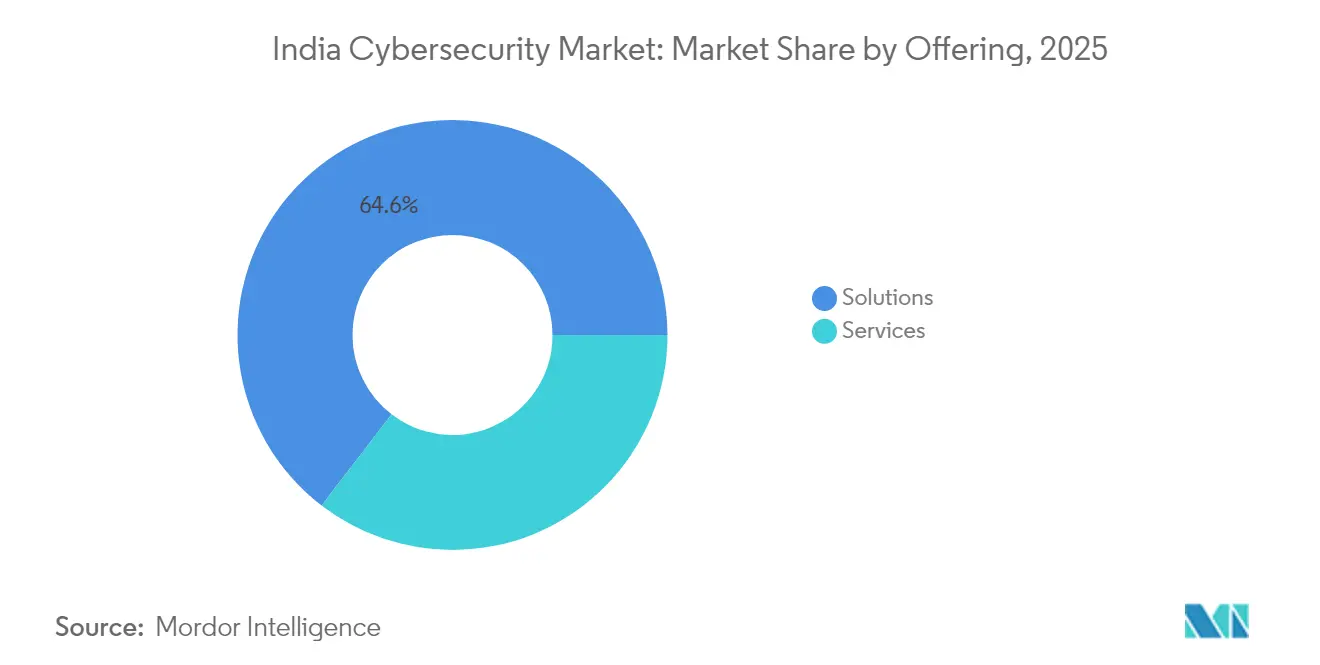

- By offering, solutions commanded 64.58% revenue share in 2025; services are on track for an 18.62% CAGR through 2031.

- By deployment mode, on-premise held 54.35% of the India cybersecurity market share in 2025; cloud is forecast to expand at a 21.92% CAGR.

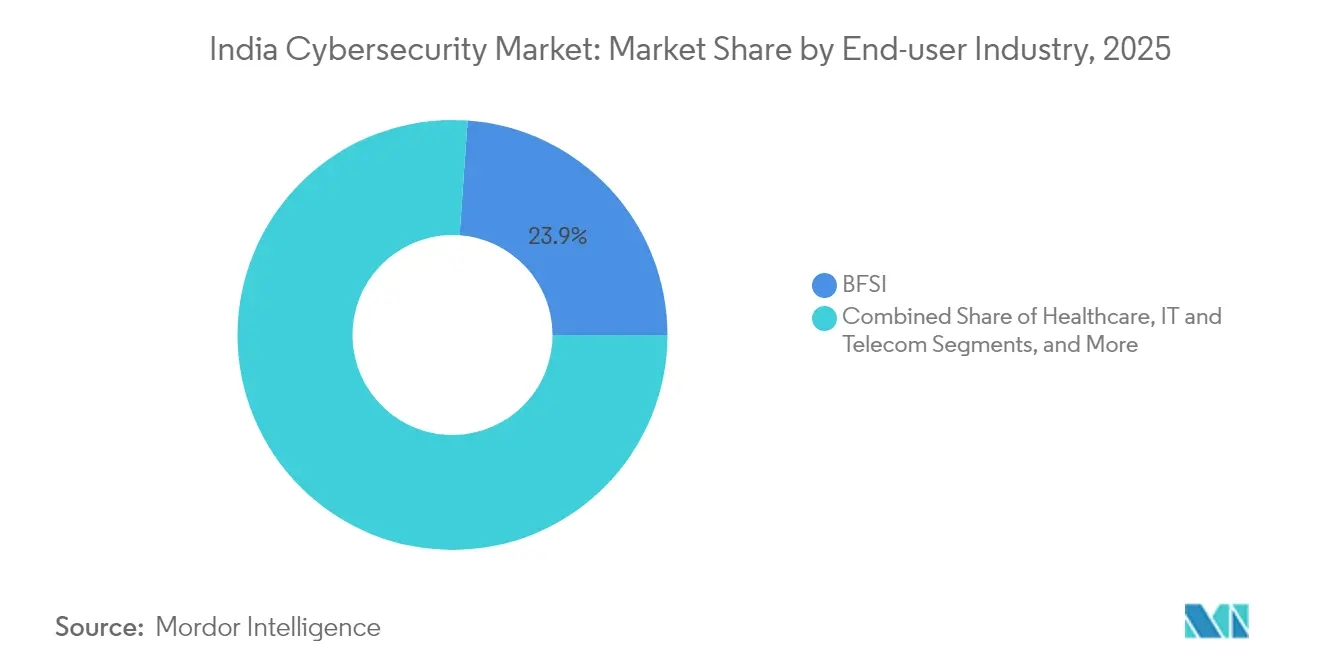

- By end-user industry, BFSI led with 23.88% revenue share in 2025; healthcare is advancing at 18.86% CAGR.

- By end-user enterprise size, large enterprises captured 69.72% of 2025 spending, while SMEs are expected to grow at a 19.74% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital India and Enterprise Modernization Mandating Robust Cybersecurity Controls | +4.20% | Tier 1 metros; rising in Tier 2 | Medium term (2-4 years) |

| Surge in UPI and Real-Time Payments Driving Identity/Fraud Protection Demand | +3.80% | Nationwide; urban first | Short term (≤ 2 years) |

| Government DPDP Act and CERT-In Compliance Deadlines Accelerating Security Spend | +5.10% | Uniform across India | Short term (≤ 2 years) |

| 5G and IoT Roll-outs Exposing New Attack Surface in Telecom and Smart Manufacturing | +2.70% | Urban then semi-urban | Medium term (2-4 years) |

| Rise of Ransomware-as-a-Service Targeting Public Sector and Critical Infrastructure | +2.30% | Major metros | Short term (≤ 2 years) |

| Venture Capital and Government Grants Fueling Indian Cybersecurity Start-up Ecosystem | +1.90% | Bengaluru, Mumbai, Delhi NCR, Hyderabad | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital India and Enterprise Modernization Mandating Robust Cybersecurity Controls

The Digital India program has digitized citizen services at record speed, expanding the national attack surface and making cybersecurity an integral budget line for ministries and state agencies. UPI processes more than 15 billion transactions each month, a scale that forces banks to integrate adaptive authentication and real-time fraud-detection engines [1]National Payments Corporation of India, “UPI Product Statistics,” npci.org.in. CFO surveys reveal that 60% of Indian corporates will raise security allocations in 2025, notably higher than the 47% global average. Enterprises now embed zero-trust checkpoints in every modernization sprint, resulting in shorter procurement cycles for identity, cloud-workload, and data-loss-prevention controls.

Surge in UPI and Real-Time Payments Driving Identity/Fraud Protection Demand

The Unified Payments Interface has re-defined retail finance, but its convenience also attracts credential-stuffing and man-in-the-browser attacks. Financial institutions logged more than 2,500 security incidents in the second half of 2024 alone. Banks respond by enforcing multi-factor authentication and behavioral biometrics, which in turn stimulates growth for identity-and-access-management (IAM) suites. The sector’s move toward zero-trust architectures is supported by regulators that prioritize continuous monitoring over periodic audits, broadening the addressable market for AI-driven fraud-analytics vendors.

Government DPDP Act and CERT-In Compliance Deadlines Accelerating Security Spend

India’s DPDPA sets fines up to INR 500 crore (USD 5.82 crore) for personal-data breaches, compelling organizations to encrypt records, retain logs for 180 days, and file incident reports within six hours. CIOs therefore bundle breach-notification automation, key-management services, and data-protection impact assessments into annual capex plans. The draft enforcement rules issued in January 2025 further codify consent, cross-border transfer, and impact-assessment norms, locking compliance budgets for at least the medium term. These obligations strengthen demand for managed security services that guarantee audit-ready dashboards.

5G and IoT Roll-outs Exposing New Attack Surface in Telecom and Smart Manufacturing

Nationwide 5G coverage is connecting millions of industrial sensors, smart meters, and autonomous devices. Weekly cyber-attack volumes in India already exceed 3,300, well above the global average, with defense and aerospace facing the steepest risk. Telcos respond by embedding security gateways into network cores, while manufacturers deploy agentless discovery tools to map operational-technology traffic. The convergence of IT and OT stacks is therefore propelling sales of unified visibility platforms that can ingest industrial protocols and cloud telemetry alike.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified SOC Analysts | −2.5% | Nationwide; sharper in Tier 2/3 | Medium term (2-4 years) |

| Price Sensitivity among MSMEs Limiting Adoption of Enterprise-Grade Solutions | −1.8% | Industrial clusters | Short term (≤ 2 years) |

| Fragmented Regulation on Cross-border Data Flows Creating Procurement Delays | −1.4% | Multinationals in IT/ITeS hubs | Medium term (2-4 years) |

| Legacy infrastructure complexity | −1.0% | Regulated industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified SOC Analysts

Enterprises struggle to fill tier-1 and tier-2 analyst seats, driving uptake of automation and outsourced monitoring. CERT-In and Fortinet have partnered with universities to embed security curricula that will seed the talent pipeline over the next three years[2]Express Computer, “Fortinet and CERT-In launch joint initiatives for academia,” expresscomputer.in. In the interim, managed detection and response contracts are growing at double-digit rates because service providers can pool scarce expertise across multiple clients.

Price Sensitivity among MSMEs Limiting Adoption of Enterprise-Grade Solutions

Small manufacturers and services firms often rank cybersecurity below immediate revenue drivers. The average ransom demand against SMEs rose sharply in 2024, yet many owners still view advanced tooling as unaffordable. Vendors now package endpoint protection, email security, and basic log-retention into pay-as-you-go bundles, allowing MSMEs to phase investments without heavy upfront capital. Government-led awareness clinics further highlight the financial impact of downtime, slowly shifting perceptions from “nice-to-have” to “must-have.”

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Dominate, Services Accelerate

Solutions remain the revenue anchor, holding 64.58 % of the India cybersecurity market share in 2025. Network security, cloud-workload protection, and identity-and-access management packages are refreshed first whenever boards approve catch-up spending. Vendors add AI analytics and consolidated dashboards to shrink alert fatigue, keeping renewal rates high.

The services arm of the India cybersecurity market is forecast to post an 18.62 % CAGR to 2031 as talent constraints force organizations to outsource detection and response. Managed security service providers that guarantee six-hour incident reporting—mirroring CERT-In rules—win multi-year contracts. Advisory practices that blend compliance and threat-hunting expertise see rising attach rates, confirming that process depth, not head-count scale, now drives buying decisions.

By Deployment Mode: Cloud Upshifts Security Architecture

On-premise controls still claim 54.35 % of 2025 spending, largely inside banking, telecom, and critical-infrastructure estates where data-sovereignty audits remain strict. These buyers refresh appliances only if the gear exposes open APIs that feed cloud SIEMs, proving that hybrid design is the new norm.

Conversely, cloud deployments in the India cybersecurity market race ahead at a 21.92 % CAGR, propelled by the fact that 99 % of domestic firms run hybrid clouds. CISOs prize identity brokering, container runtime defense, and posture-management modules that auto-map to DPDPA controls. Cloud-native vendors thus lead short-lists whenever DevOps speed trumps legacy lock-in.

By End-user Industry: BFSI Leads, Healthcare Accelerates

The BFSI vertical commands 23.88 % of current revenue, validating its long-standing reputation as the bellwether for the India cybersecurity market. Fraud-loss pressure pushes banks to pilot behavioral biometrics, while regulators insist on immutable audit trails. The healthcare sector is advancing at a 18.86 % CAGR in the India cybersecurity market.

Healthcare budgets spike after the 2024 breach at the Regional Cancer Center, prompting hospital CIOs to inventory every connected diagnostic device. OT-security specialists now pitch asset-discovery and micro-segmentation bundles, expanding the total India cybersecurity market size across life-sciences campuses.

By End-user Enterprise Size: SMEs Narrow the Protection Gap

Large enterprises account for 69.72 % of the India cybersecurity market size in 2025, leveraging bulk licenses and integrated SOC workflows to pull telemetry from thousands of endpoints. Decision makers increasingly benchmark vendors on automation coverage and breach-containment metrics rather than feature tallies.

SMEs, though smaller in absolute spend, show a faster 19.74 % CAGR as tiered SaaS bundles reduce sticker shock. Flexible billing has shifted perception from cost center to business enabler, nudging more mid-market firms onto zero-trust roadmaps. The trend suggests the India cybersecurity industry will become less top-heavy over the forecast window.

Geography Analysis

Mumbai, Bengaluru, and Delhi NCR continue to anchor over half of the India cybersecurity market because data-center density, stock-exchange activity, and head-office clusters all demand round-the-clock protection. State tenders increasingly stipulate log-retention aligned with DPDPA, giving vendors with automated compliance dashboards a head start. Foreign cloud regions launched in these metros further accelerate SaaS security adoption.

Tier-2 cities such as Hyderabad, Pune, and Jaipur register double-digit growth as shared-services hubs and semiconductor fabs go online. Local chambers of commerce co-host cyber-readiness boot camps, normalizing endpoint encryption even for export-oriented SMEs. Managed service providers respond by opening satellite SOCs, ensuring low-latency telemetry routing and satisfying data-residency clauses that shape the India cybersecurity market.

Rural and semi-urban districts remain early in the curve, yet mobile-banking penetration exposes them to phishing and botnet traffic. Public-sector banks running financial-inclusion drives bundle endpoint security with micro-credit apps, surfacing new revenue pockets for low-footprint agents. Telecom tower operators deploy edge-firewalls to harden backhaul links, proving that geography no longer dictates basic protection standards inside the broader India cybersecurity industry.

Competitive Landscape

The India cybersecurity market shows moderate concentration. Domestic integrators—Tata Communications, Wipro, HCLTech, and Infosys—blend legacy network contracts with next-gen SOC operations, creating sticky full-stack deals. Their compliance playbooks, honed across public-sector audits, beat global rivals when bid scoring favors local delivery credentials.

Global pure-plays such as Cisco, Check Point, and Fortinet ride deep R&D budgets to seed AI-enhanced firewalls and XDR platforms. Check Point’s 2025 report citing a 44 % rise in attacks has upped its boardroom visibility [3]Check Point Software, “2025 Security Report finds 44% increase in cyber-attacks,” checkpoint.com. Fortinet leverages network-security convergence, with its new G-series boosting IPsec throughput by 11 × at lower power draw [4]Fortinet Inc., “Fortinet Delivers Unmatched Security and Efficient Network Performance with New Next-Gen Firewalls,” investor.fortinet.com.

A vibrant startup cohort—PingSafe, Safe Security, Indusface, and Quick Heal—expands the India cybersecurity market by addressing localized pain points such as multilingual phishing and Aadhar-linked fraud. Venture funding and government seed grants speed feature velocity, while channel alliances with system integrators fast-track enterprise adoption. The interplay of incumbents and disruptors ensures solution diversity without fragmenting support ecosystems.

India Cybersecurity Industry Leaders

Quick Heal Technologies Limited

Tata Communications

Cisco Systems, Inc.

Palo Alto Networks, Inc.

Wipro Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Through CERT-In and BITS Pilani, India has rolled out a national cybersecurity upskilling initiative targeting both government and industry professionals.

- June 2025: Check Point Software Technologies has introduced a data residency instance in India for its Harmony Secure Access Service Edge (SASE) platform.

- May 2025: Radware has bolstered its global DDoS mitigation efforts by inaugurating cloud security centers in Nairobi, Mumbai, and Chennai, responding to the escalating threats faced by web applications.

- May 2025: NxtGen Cloud Technologies has teamed up with global cybersecurity giant Thales to bolster India's sovereign cloud with defense-grade protection.

India Cybersecurity Market Report Scope

Cybersecurity solutions are required to safeguard a company's digital operations and platforms from potential cyber-attacks and threats. A company faces several threats, such as ransomware, spyware, data breaches, etc., that might adversely impact its operations. Hence, cybersecurity services and products offered by solution providers help protect the company.

The India cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries),. The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the forecast CAGR for the India cybersecurity market through 2031?

An 18.07 % CAGR is projected over 2026-2031.

Which deployment model is growing fastest?

Cloud-based security is forecast to grow at 21.92 % CAGR, the quickest inside the India cybersecurity industry.

Why are services outpacing product sales?

Talent shortages push enterprises to outsource detection and response, lifting managed-service revenue at an 18.62 % CAGR.

Which vertical currently dominates spending?

BFSI leads with 23.88 % of 2025 revenue because financial data remains the highest-value target.

Page last updated on: