Recombinant DNA (rDNA) Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 734.44 Billion |

| Market Size (2030) | USD 974.07 Billion |

| Growth Rate (2025 - 2030) | 5.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recombinant DNA (rDNA) Technology Market Analysis by Mordor Intelligence

The Recombinant DNA Technology Market size is estimated at USD 734.44 billion in 2025, and is expected to reach USD 974.07 billion by 2030, at a CAGR of 5.81% during the forecast period (2025-2030).

Demand for recombinant protein therapeutics, accelerating CRISPR cost declines, and the mainstreaming of AI-enabled protein design continue to re-shape industry economics, lowering entry barriers for smaller innovators while rewarding established firms that modernize production footprints. Falling prices for single-use bioreactors and plasmid micro-factories now let developers pivot between therapeutic and agricultural projects without costly line changeovers, encouraging portfolio expansion into food, feed, and environmental services. North America still anchors financing and early-stage trials, but Asia-Pacific is installing capacity at a faster pace, narrowing historical skill gaps and fostering local supply chains that reduce geopolitical risk for global licensees. Competitive intensity is mounting as pharmaceutical leaders, agricultural majors, and purpose-built gene-therapy CDMOs all vie for the same vector raw materials and regulatory bandwidth.

Key Report Takeaways

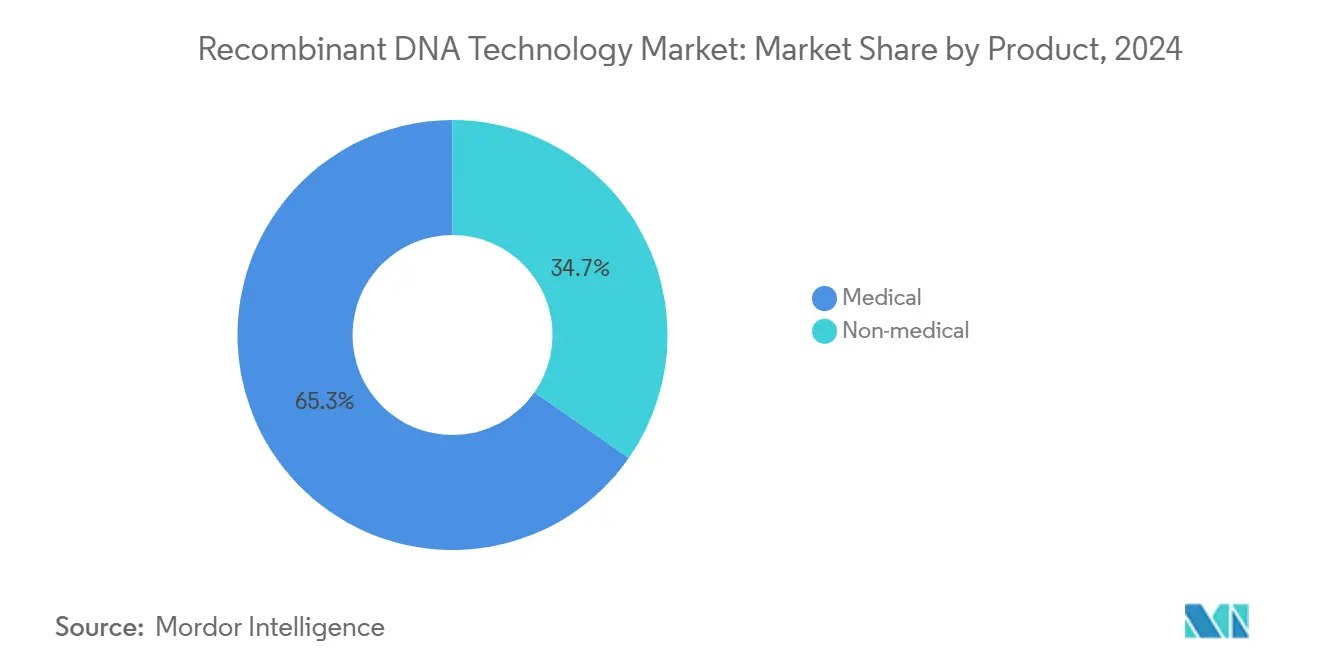

- By product, medical applications held 65.35% revenue share in 2024, while non-medical products are forecast to grow at a 12.25% CAGR to 2030.

- By component, expression systems commanded 64.53% of recom¬binant DNA technology market share in 2024; cloning vectors are expanding at 9.85% CAGR through 2030.

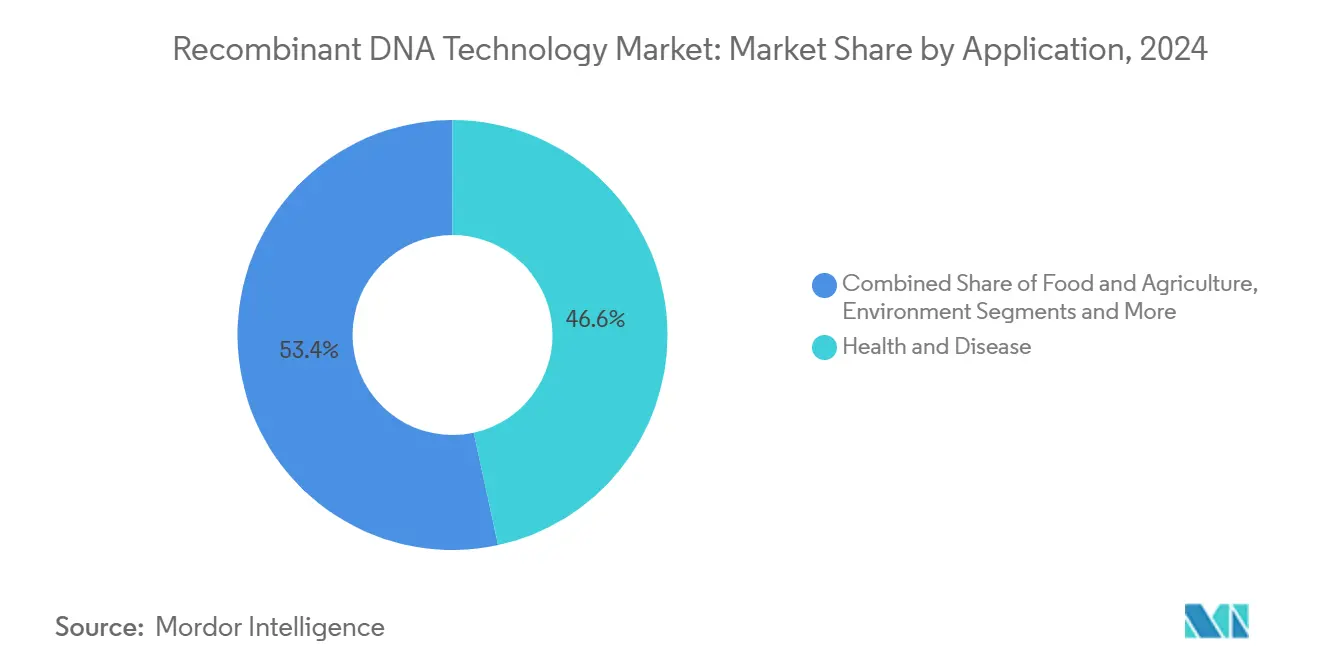

- By application, health and disease accounted for 46.62% share of the recombinant DNA technology market size in 2024; environmental uses are advancing at a 12.52% CAGR to 2030.

- By end user, biotech and pharmaceutical companies held 53.82% share in 2024, whereas academic and government institutes are projected to rise at 9.61% CAGR by 2030.

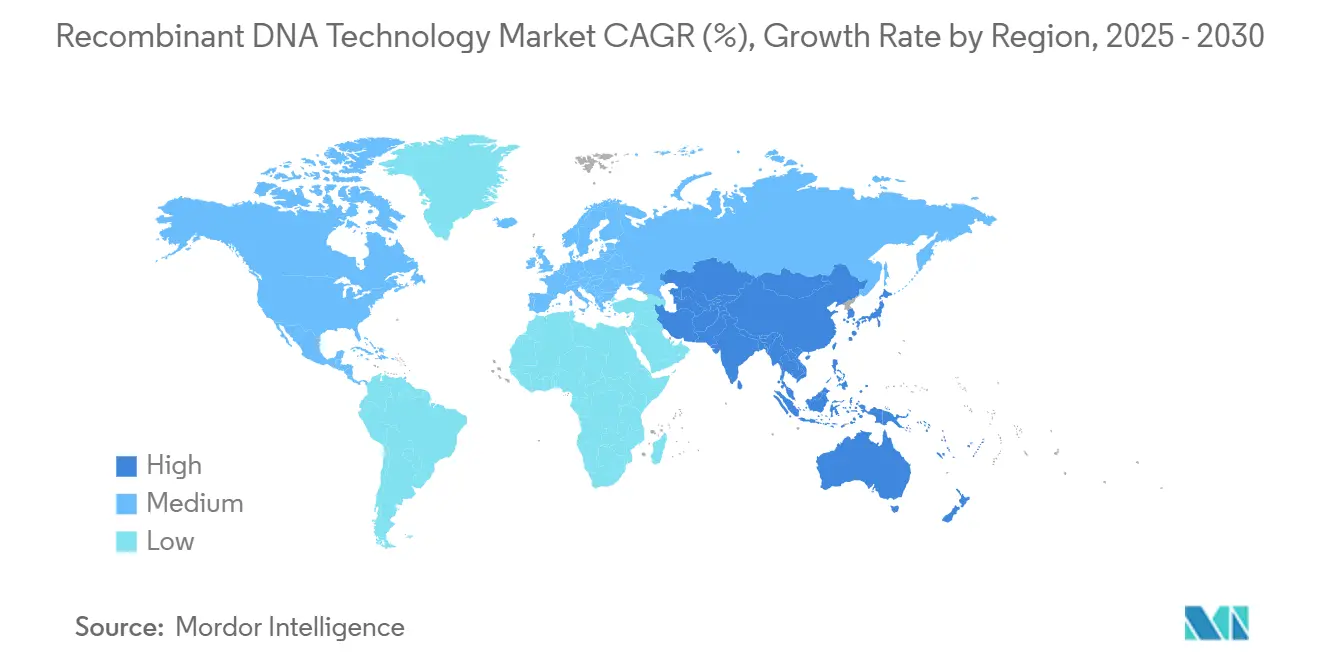

- By geography, North America led with 37.82% share in 2024, but Asia-Pacific is the fastest-growing region at an 11.81% CAGR to 2030.

Global Recombinant DNA (rDNA) Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CRISPR-Cas Cost Curve Keeps Falling | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Biopharma Demand For Recombinant Protein Drugs | +1.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| GM-Crop Acreage Expansion In Ems | +0.9% | APAC core, spill-over to Latin America & Africa | Long term (≥ 4 years) |

| AI-Driven De-Novo Protein Design Platforms | +0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Distributed, Single-Use Plasmid DNA Micro-Factories | +0.5% | Global, with faster adoption in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

CRISPR-Cas Cost Curve Keeps Falling

Widening access to nuclease-editing kits, cheaper guide-RNA synthesis, and rising vector yields have pushed the fully loaded cost of CRISPR therapies down sharply. CASGEVY’s clinical success in sickle cell disease validated the modality, even at an initial price tag near USD 3 million per patient. Aldevron then cut personalized CRISPR manufacturing time to six months, proving cycle-time gains are realistic as supply chains mature[1]Aldevron, “World’s First mRNA-Based Personalized CRISPR Therapy,” aldevron.com. A record 14 US review designations in 2024 signaled that regulators are gaining confidence, shrinking development risk premia. As costs trend lower, developers are pivoting from ultra-rare disease targets toward prevalent disorders, enlarging the recom¬binant DNA technology market addressable pool.

Biopharma Demand for Recombinant Protein Drugs

Novo Nordisk earmarked USD 4.1 billion for a new North Carolina site focused on injectable recombinant proteins, underscoring persi stent demand in diabetes and obesity care[2]CNBC, “Novo Nordisk to Build USD 4.1 Billion North Carolina Facility,” cnbc.com. Eli Lilly’s USD 3 billion Wisconsin investment and Amgen’s 35% Q1 2025 biosimilar revenue jump to USD 700 million suggest supply, not demand, is the current bottleneck. Continuous-flow bioreactors and modular single-use lines are lowering minimum efficient scale, letting smaller biotechs commercialize targeted proteins without big-pharma backing, thereby broadening competitive participation in the recombinant DNA technology market.

GM-Crop Acreage Expansion in Emerging Markets

China cleared multiple biotech crops in 2024 while Kenya commercialized Bt cotton, reversing earlier regulatory hesitancy. The UK’s Precision Breeding Act now distinguishes gene-edited traits from transgenic ones, a nuance expected to permeate EU policy debates. Ghana’s approval of nutrient-dense GM cowpea shows how food-security objectives can fast-track reviews. Bayer’s launch of Vyconic soybeans with five herbicide tolerances emphasizes that advanced trait stacking now commands a premium price justified by complex weed pressures. These shifts collectively enlarge agricultural demand for recombinant vectors, lifting long-term growth prospects for the recombinant DNA technology market.

AI-Driven De-Novo Protein Design Platforms

Cradle’s USD 73 million Series B and Illumina’s AI partnership with NVIDIA reveal how algorithm-guided design is compressing discovery timelines. AI now proposes protein folds unattainable through natural evolution, widening therapeutic scope. Novo Nordisk and Moderna’s USD 1.9 billion pact with Life Edit reflects a broader trend of pharma outsourcing computational design to specialist partners. Industrial biotech players are deploying AI-crafted enzymes to improve chemical yields, proving commercial value outside healthcare. As these platforms become turnkey, they will form the digital backbone of new entrants, accelerating rivalry across every layer of the recombinant DNA technology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving Global Gene-Editing Regulations | -0.8% | Global, with regional variations in stringency | Medium term (2-4 years) |

| Manufacturing Complexity & CAPEX | -1.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Pharmaceutical-Grade Vector Raw-Material Shortages | -0.6% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Consumer Push-Back On Gene-Edited Foods | -0.4% | EU & select APAC markets, limited US impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Evolving Global Gene-Editing Regulations

Fragmented oversight forces developers to navigate multiple dossier formats, parallel clinical protocols, and divergent post-marketing surveillance mandates. The FDA’s CoGenT Global pilot seeks alignment, yet Europe’s risk-assessment model still differs from US benefit-risk weighting[3]Greenberg Traurig LLP, “FDA Takes First Step Toward International Regulation of Gene Therapies,” gtlaw.com. China is revising its gene-therapy rules, creating uncertainty for foreign license holders even as it speeds pathways for domestic firms. Fifteen-year follow-up requirements in the US stretch the financial stamina of small developers, consolidating power among cash-rich incumbents. Collectively, regulatory divergence slows product launches and raises compliance costs, tempering near-term growth for the recombinant DNA technology market.

Manufacturing Complexity & CAPEX

Thermo Fisher’s USD 4.1 billion Solventum deal and Lonza’s USD 1.2 billion Vacaville buyout underline the premium on existing cGMP capacity. Viral-vector suites demand HEPA zoning, segregated HVAC, and high-potency disposal systems, pushing build costs beyond USD 600 million for a 30,000 liter facility. Single-use hardware trims commissioning time but inflates consumable spend, forcing operators to balance capex savings against higher unit costs. Even large biopharma players are locking in multi-year CDMO slots to hedge capacity risk, an early sign that supply constraints could cap near-term volumes in the recombinant DNA technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Medical Applications Drive Current Revenue

Medical products contributed 65.35% of overall revenue in 2024, anchored by mature therapeutic proteins that benefit from decades of process optimization and well-established reimbursement channels. The therapeutic agents subset keeps momentum through expanding GLP-1 and oncology pipelines, even as biosimilar entrants chip away at legacy monopolies. Vaccines gained new life after COVID-19 validated mRNA platforms; oncology vaccine trials now leverage the same lipid-nanoparticle chassis, cutting preclinical budgets. Outside healthcare, non-medical products are rising at a 12.25% CAGR on the back of GM crops that boost drought tolerance and specialty chemicals that replace petrochemical intermediates. Industrial enzymes now clean textiles at lower temperatures, saving energy and creating recurring royalties for enzyme licensors, an illustration of revenue resilience that cushions cyclicality in drug sales.

Specialty chemicals harness recombinant pathways to produce surfactants and fragrance precursors in fermenters, yielding lower emissions relative to petro-routes and aligning with corporate net-zero pledges. Environmental remediation organisms digest oil slicks and plastic debris, launching entirely new service niches for synthetic-biology startups. This diversification broadens the recombinant DNA technology market, reduces dependence on blockbuster drug lifecycles, and supports steady cash flows across economic cycles.

By Component: Expression Systems Maintain Dominance

Expression systems accounted for a 64.53% slice of recombinant DNA technology market share in 2024, reflecting their indispensability across human therapeutics, animal vaccines, and industrial enzymes. Mammalian cell hosts command premium pricing because they perform human-like glycosylation, a must for complex antibodies. Bacterial and yeast lines remain the workhorses for insulin and enzyme production, favored for rapid doubling times and lower media costs. Cloning vectors, growing at 9.85% CAGR, are propelled by surging gene-therapy trials that require high-grade plasmids and viral backbones.

Single-use plasmid micro-factories now fit within standard laboratory footprints, letting hospitals craft personalized vectors for compassionate-use cases. Adeno-associated and lentiviral vectors fetch prices up to USD 200,000 per batch, creating lucrative micro-segments for specialized CDMOs. The spread of distributed manufacturing is especially pronounced in low-volume rare-disease pipelines, where localized production avoids cold-chain delays and alleviates customs bottlenecks.

By Application: Health Dominance Faces Environmental Challenge

Health and disease retained 46.62% of revenue in 2024 as monoclonal antibodies, CAR-T therapies, and gene replacements secured regulatory wins across oncology and hematology. Oncology developers prize recombinant antibodies for their specificity, translating into superior progression-free survival in late-stage trials. Rare-disease treatments leverage orphan incentives to offset small cohorts, resulting in high list prices that sustain margins. North America commanded 37.82% of the recombinant DNA technology market size in 2024, showing the segment’s financial center of gravity remains in developed-market health systems.

Environmental applications are scaling fastest at a 12.52% CAGR, propelled by government subsidies for carbon capture, wastewater treatment, and plastic degradation services. Recombinant microbes that metabolize methane into protein feed showcase dual climate and food-security benefits, attracting impact-capital inflows. Agricultural biotechnology’s regulatory variance across countries still tempers universal uptake, yet emerging-market approvals in Ghana and Kenya hint at accelerating acceptance.

By End User: Academic Growth Challenges Industry Leadership

Biotech and pharmaceutical enterprises controlled 53.82% share in 2024, leveraging integrated discovery-to-commercial models to speed launches. Their head start in GMP compliance and global marketing gives them negotiating leverage over payers and raw-material suppliers, reinforcing incumbency advantages. Academic and government institutes, however, are expanding at 9.61% CAGR, buoyed by pandemic-era funding that left permanent BSL-3 lab upgrades on many campuses. The recombinant DNA technology industry now relies on university spin-outs for niche delivery technologies and advanced analytics that larger firms license under milestone structures.

Contract research organizations, tooling vendors, and analytics firms round out the user landscape, forming an interconnected ecosystem where service providers earn recurring revenues without direct exposure to clinical failure risk. This democratization of capabilities disperses innovation geographically and dilutes market power that once resided only with multinational pharma, further expanding the recombinant DNA technology market.

Geography Analysis

North America commanded 37.82% of revenue in 2024, supported by robust venture funding, favorable reimbursement, and FDA frameworks that shorten review cycles for breakthrough therapies. US biomanufacturers benefit from tax incentives and university-laboratory networks that funnel skilled graduates into industry. Canada’s investments in gene-therapy incubators add regional diversity, particularly in viral-vector R&D. The recombinant DNA technology market now sees strong state-level competition for capacity, with North Carolina, Massachusetts, and California offering matching grants for facility build-outs.

Asia-Pacific logged the fastest CAGR at 11.81% to 2030, underpinned by China’s strategic shift toward Southeast Asian partnerships that secure downstream markets and resilient supply chains. Japan’s government has revived biotech stimulus programs, targeting synthetic biology for sustainable chemicals, while South Korea’s Chaebol groups co-invest in CDMOs to capture biologics export revenue. India’s reform of its Biotechnology Regulatory Authority promises faster clearance for gene-edited crops, strengthening its position as a seed-production hub. Together, these moves are narrowing the historical production gap with Western markets and boosting local availability of recombinant inputs.

Europe balances innovation with consumer skepticism, particularly for GMO foods. The forthcoming EU Pharmaceutical Strategy aims to streamline centralized approvals for advanced therapies, yet crop approvals still face member-state opt-outs. Contract manufacturers in Ireland, Germany, and Switzerland capitalize on this split by offering scale bioreactors for global clients, letting therapy sponsors sidestep local regulatory snags in favor of export-only production. The Middle East and Africa are at a nascent stage but show policy momentum: Saudi Arabia has budgeted sovereign-fund capital for genomics centers, and Ghana’s GM cowpea clearance signals a pragmatic stance on food security. South America’s soy and corn belts provide fertile ground for GM traits, though macroeconomic volatility can dampen foreign direct investment. These diverse trajectories ensure the recombinant DNA technology market remains geographically plural, reducing concentration risk and enabling cross-border collaboration.

Competitive Landscape

Competition spans horizontal layers—research tools, vector supply, GMP capacity—and vertical slices across therapeutic, agricultural, and industrial applications. Pfizer, Amgen, and Sanofi deploy balance-sheet strength to secure early access to high-volume CDMO slots, crowding smaller firms out of prime time windows. Thermo Fisher’s USD 2 billion US expansion bundles R&D services with purification consumables, a move designed to lock customers into end-to-end supply chains. Lonza, Fujifilm Diosynth, and GenScript have scaled bioreactor fleets past 500,000 liters, positioning themselves as indispensable to late-stage gene-therapy sponsors.

Startups differentiate through platform focus: Aldevron pioneers rapid plasmid manufacture; Touchlight develops doggybone DNA vectors; Life Edit specializes in base editing. Many pair innovation with strategic partnerships—NEC Bio and AGC Biologics contracted to produce personalized cancer vaccines, combining AI antigen discovery with scalable manufacturing. The recombinant DNA technology market rewards such alliances by shortening time-to-clinic while sharing capital burden.

Competitive strategies increasingly hinge on digital enablement. Companies integrate AI for in-silico screening, digital twins for facility optimization, and blockchain for vector traceability to satisfy stricter provenance audits. Those that master data fusion achieve faster batch-release cycles and tighter yield variances, translating into lower cost-of-goods that defend margins as biosimilar erosion intensifies. Despite consolidation waves, the recombinant DNA technology market still counts hundreds of venture-backed firms tackling narrow targets, sustaining a dynamic equilibrium where incumbents buy or partner with the most promising newcomers rather than relying solely on internal R&D.

Recombinant DNA (rDNA) Technology Industry Leaders

New England Biolabs

Sanofi

GenScript

GSK plc

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Thermo Fisher Scientific unveiled a USD 2 billion US investment plan covering capital projects and life-science R&D.

- March 2025: Bayer introduced Vyconic soybeans with five herbicide tolerances, targeting US and Canadian farmers by 2027.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the recombinant DNA technology market as the worldwide revenue earned from products or processes whose core function relies on artificially recombined deoxyribonucleic acid; this spans recombinant medicines and vaccines, genetically modified crops, industrial enzymes, and the expression or cloning platforms that enable their manufacture. We consider every geographic region and end-user that purchases these outputs.

Scope Exclusions: Stand-alone gene-sequencing tools, cell-therapy platforms that never employ rDNA steps, and contract research fees without direct recombinant production have been kept outside the model.

Segmentation Overview

- By Product

- Medical

- Therapeutic Agents

- Human Proteins

- Vaccines

- Non-medical

- Biotech Crops

- Specialty Chemicals

- Other Non-medical Products

- Medical

- By Component

- Expression Systems

- Cloning Vectors

- By Application

- Food & Agriculture

- Health & Disease

- Environment

- Other Applications

- By End User

- Biotech & Pharma Companies

- Academic & Govt Institutes

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed quality-assurance leads at biologic plants, crop-science researchers, and regulatory reviewers across North America, Europe, and Asia-Pacific. Their guidance on average selling prices, batch yields, and likely approval pipelines refined desk assumptions before final triangulation.

Desk Research

We began with statutory databases such as the US FDA Biologics License files, the European Medicines Agency product registers, and UN FAOSTAT acreage data for biotech crops; then blended open journals like Nature Biotechnology, PubMed-indexed trials, and BIO or CropLife association briefs. Patent analytics mined through Questel, as well as 10-K filings, investor decks, and shipment statistics, completed baseline volume and pricing frames. Select paywalled feeds, such as Dow Jones Factiva for deal flow and D&B Hoovers for producer revenue, helped map competitive intensity. The sources named are illustrative; many additional repositories were reviewed for cross-checks.

Market-Sizing & Forecasting

A top-down reconstruction that merges global biologic drug sales, GM-seed trade, and industrial enzyme output forms our first pass, which is validated through supplier roll-ups and sampled ASP × volume checks (our single use of bottom-up, top-down). Key variables like annual FDA biologic approvals, R&D spend on gene-editing tools, hectares of biotech crops, and recombinant enzyme tonnage feed a multivariate regression that projects demand through 2030. Missing disclosures are imputed from regional penetration rates discussed with experts.

Data Validation & Update Cycle

Outputs face variance tests against historical growth bands, peer ratios, and macro signals before senior review. Reports refresh each year, and major events such as breakthrough gene-therapy approvals trigger interim updates so clients receive the latest view.

Why Mordor's Recombinant DNA Technology Baseline Commands Reliability

Published estimates often diverge, and we acknowledge this upfront for buyers who compare numbers across firms. Differences usually stem from how each analyst defines products, chooses pricing assumptions, or times currency conversion.

Key gap drivers include narrower agricultural coverage by some publishers, aggressive pipeline-success rates, or refresh cycles that miss fast-moving biologic approvals. Mordor's disciplined scope and annual updates limit such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 734.44 B (2025) | Mordor Intelligence | - |

| USD 780.0 B (2024) | Global Consultancy A | excludes industrial enzymes, older FX rates |

| USD 856.81 B (2024) | Industry Publisher B | combines diagnostics revenue, assumes 100 % pipeline success |

Taken together, the comparison shows that Mordor grounds its baseline in clearly delineated revenue streams, verified multi-source inputs, and an annual refresh cadence, giving decision-makers a balanced and reproducible starting point.

Key Questions Answered in the Report

What is the current size of the recombinant DNA technology market?

The market was valued at USD 734.44 billion in 2025 and is set to rise to USD 974.07 billion by 2030, posting a 5.81% CAGR.

Which product segment leads revenue generation?

Medical applications accounted for 65.35% of 2024 revenue, mainly through therapeutic proteins and fast-growing gene therapies.

Which region is growing fastest?

Asia-Pacific is projected to grow at an 11.81% CAGR through 2030, driven by expanding manufacturing footprints in China and Southeast Asia.

What factor exerts the strongest positive impact on growth?

Rising biopharma demand for recombinant protein drugs adds roughly +1.8 percentage points to the forecast CAGR.

Why are cloning vectors outpacing expression systems in growth?

Gene-therapy pipelines require high-grade viral and plasmid vectors, pushing the segment toward a 9.85% CAGR through 2030.

How do regulatory differences affect market entry?

Divergent gene-editing rules across the US, EU, and China compel multi-jurisdictional compliance strategies, adding time and cost before launch.

Page last updated on: