Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.34 Billion |

| Market Size (2031) | USD 10.09 Billion |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

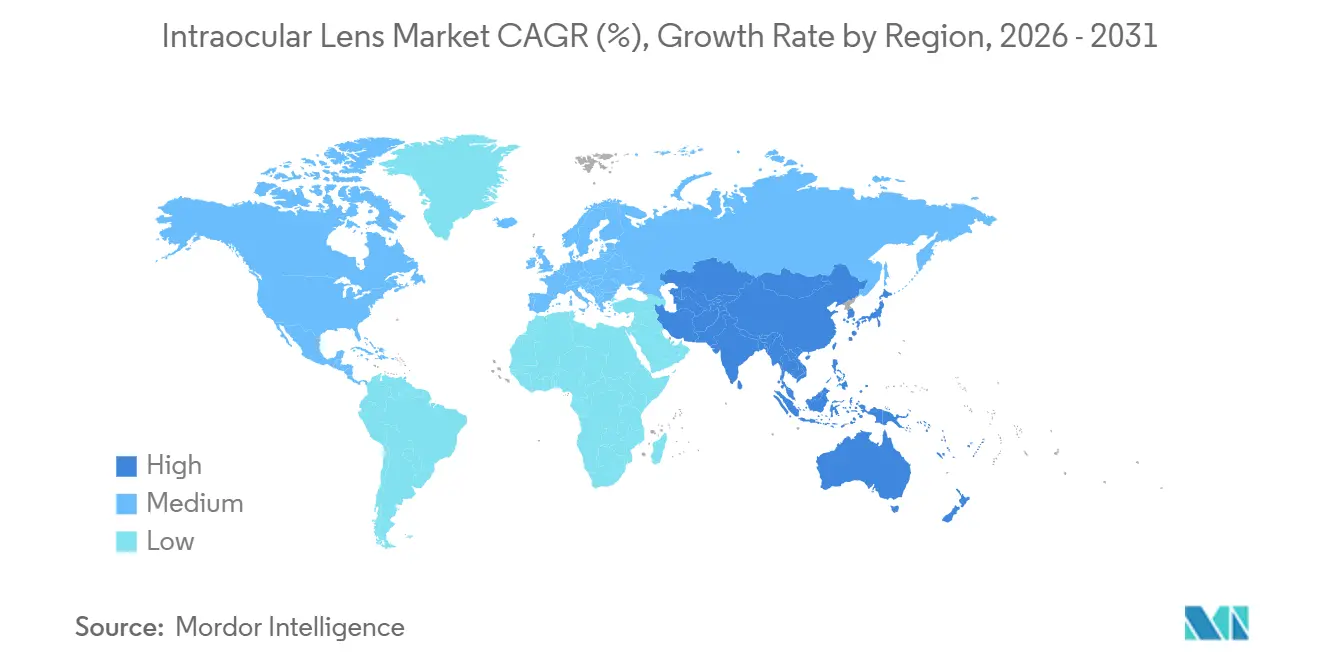

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

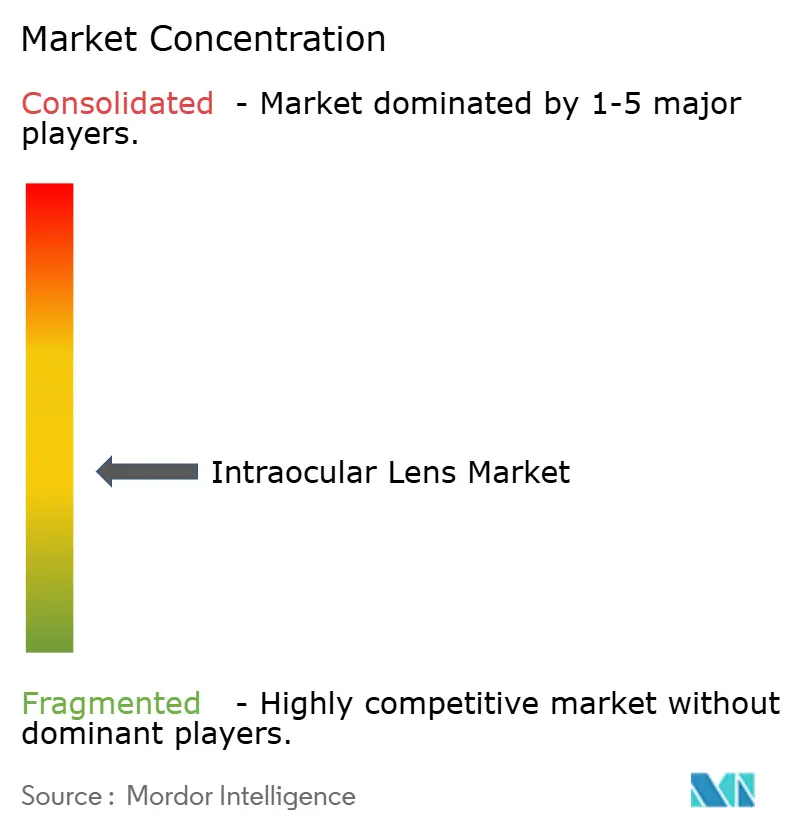

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Intraocular Lens Market Analysis by Mordor Intelligence

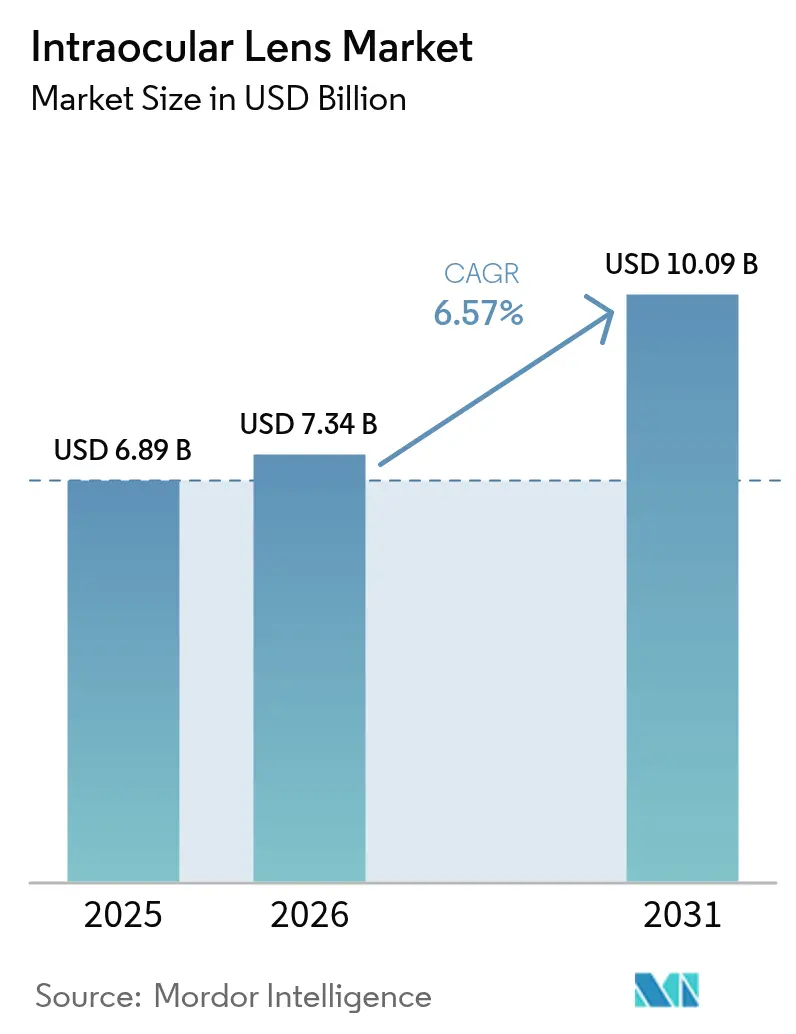

The Intraocular Lens Market size was valued at USD 6.89 billion in 2025 and is estimated to grow from USD 7.34 billion in 2026 to reach USD 10.09 billion by 2031, at a CAGR of 6.57% during the forecast period (2026-2031).

The baseline expansion is fueled by an aging population that increases cataract incidence, while premium presbyopia-correcting designs and light-adjustable technologies drive step-ups in average selling price. Surgeon confidence in toric calculators and extended-depth-of-focus optics continues to rise, encouraging broader adoption beyond traditional early adopters. Market access, however, is uneven: high out-of-pocket costs curb premium penetration in publicly funded systems, whereas bundled cataract-refractive packages in private ambulatory centers accelerate elective uptake. Technology cycles are compressing as AI-driven lens geometry optimization shortens the interval between design iterations. Parallel progress in single-use, pre-loaded delivery systems meets operating-room throughput goals but raises sustainability concerns in regions with stringent plastic regulations.

Key Report Takeaways

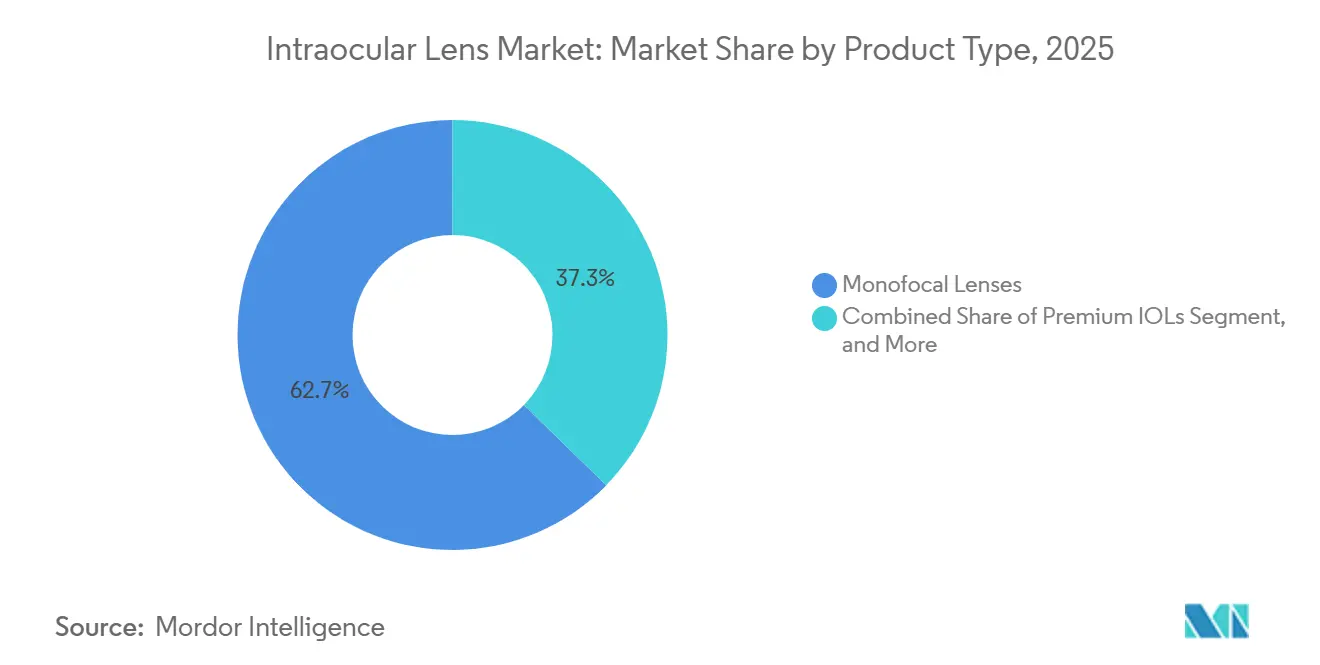

- By product type, monofocal lenses accounted for 62.68% of the intraocular lens market share in 2025; premium IOLs are projected to grow at a 7.16% CAGR through 2031.

- By material, hydrophobic acrylic accounted for 45.02% of the intraocular lens market in 2025, while silicone lenses led growth at a 7.05% CAGR through 2031.

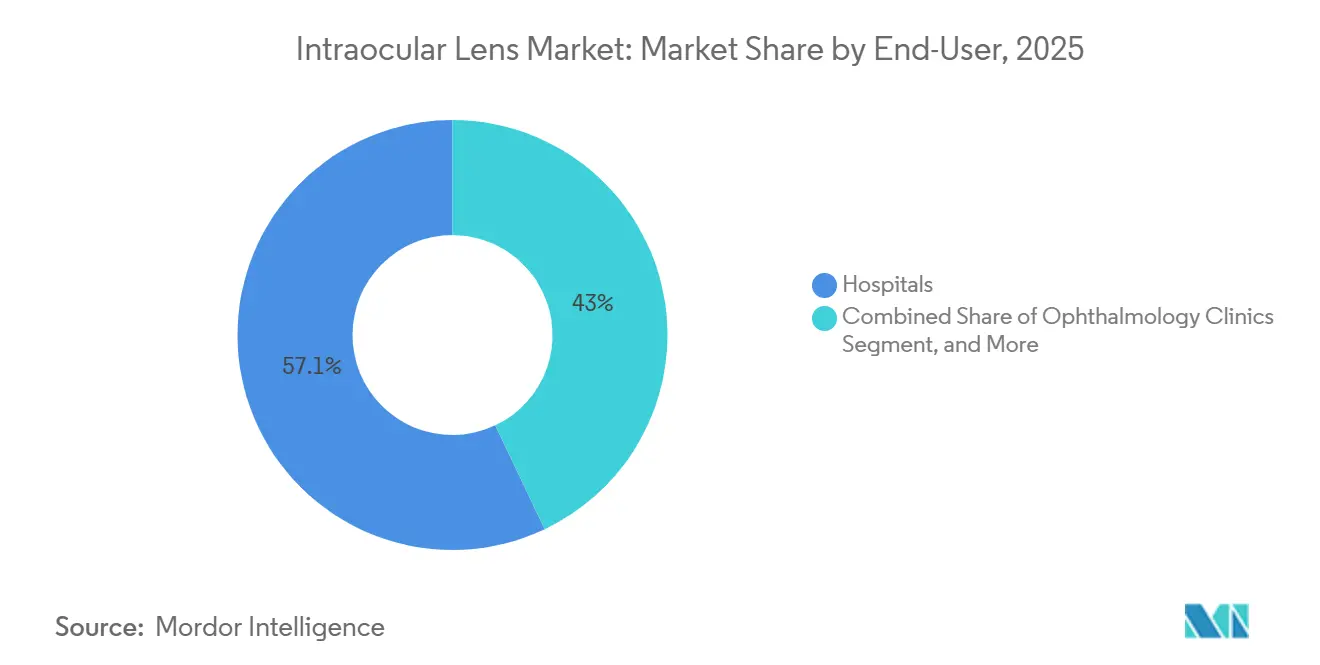

- By end user, hospitals captured 57.05% revenue in 2025, whereas ophthalmology clinics posted the fastest 7.02% CAGR through 2031.

- By application, cataract surgery accounted for 76.61% of the intraocular lens market size in 2025, and corneal-disorder use cases are advancing at a 6.95% CAGR.

- By geography, North America led with a 41.76% share in 2025, yet Asia-Pacific expanded at a 7.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intraocular Lens Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging-linked rise in global cataract procedures | +1.8% | Global, concentrated in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Surge in adoption of premium presbyopia-correcting IOLs | +1.5% | North America, Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Rapid product cycles: light-adjustable and AI-designed lenses | +1.0% | North America, Western Europe | Medium term (2–4 years) |

| Growth of refractive lens exchange in the 40–60 age cohort | +0.9% | North America, Europe, high-income Asia-Pacific | Short term (≤ 2 years) |

| Medical-tourism hubs lowering procedure cost | +0.7% | India, Thailand, Singapore | Medium term (2–4 years) |

| Pre-loaded single-use systems easing operating-room bottlenecks | +0.6% | Global, early uptake in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging-Linked Rise in Global Cataract Procedures

Cataract incidence parallels population longevity. Individuals over 80 have a 70% likelihood of developing lenticular opacity, and many expect high-quality vision for continued digital engagement and later-life employment. Ambulatory surgery centers already log cataract as their largest case type, representing 19% of ASC volume in 2024.[1]Medicare Payment Advisory Commission, “Ambulatory surgical center services,” medpac.gov Capacity pressure in Asia-Pacific magnifies because demographic aging outpaces clinic build-out, so providers increasingly adopt high-throughput models that pair phaco units with preloaded lens systems. China performs over 4 million cataract surgeries annually, yet surgical coverage in rural areas remains below 50%. In Japan, with its aging population, the health ministry reports a steady increase in cataract admissions, driving higher per-capita usage of IOLs. The Aravind network in India exemplifies a high-volume, cost-effective surgical model. However, India's national surgical rate is only 6,000 per million, significantly below the 10,000 benchmark. This underscores a major opportunity to address access gaps through mobile eye camps and tele-ophthalmology.

Surge in Adoption of Premium Presbyopia-Correcting IOLs

Premium penetration rose from 15.5% in 2019 to 18.5% in 2021 despite reimbursement gaps. Light-adjustable optics let surgeons refine power post-op, shrinking the risk of residual refractive error. Alcon holds more than 60% of this segment on the strength of PanOptix and Vivity families. Enhanced monofocal designs such as Tecnis Eyhance extend depth without the photic issues of diffractive rings, broadening eligibility for patients wary of halo or glare. Patients are increasingly perceiving cataract surgery as a refractive procedure. A 2024 meta-analysis revealed that enhanced monofocal lenses outperformed standard designs, boosting intermediate acuity by 0.2 logMAR. In 2025, toric models captured nearly 30% of the premium market share, driven by calculators achieving sub-0.25 D accuracy.[2]National Center for Biotechnology Information, “Dysphotopsia After Intraocular Lens Implantation,” ncbi.nlm.nih.gov However, affordability remains a dividing factor: while urban patients readily invest in upgrades, their rural counterparts often settle for basic implants. Demonstrating long-term cost benefits could encourage payers to expand their coverage.

Rapid Product Cycles: Light-Adjustable and AI-Designed Lenses

RxSight’s lens, cleared by FDA, offers power adjustments up to 3.50 D using UV modulation, while Rayner’s AI-optimized spiral-pattern optic maintains contrast and curbs glare. The FDA-qualified AIOLIS patient-reported-outcome metric accelerates clinical evaluation, shortening R&D time lines for premium concepts.[3]American Academy of Ophthalmology, “AIOLIS Patient-Reported Outcome Tool Qualified by FDA,” aao.org

Alcon and Carl Zeiss are developing machine-learning models that tailor aspheric profiles to match corneal topography, eyeing a commercial launch in the next two years. As commercial life spans shrink, manufacturers are increasingly pressured to invest in continuous R&D and maintain nimble regulatory submissions.

Growth of Refractive Lens Exchange in the 40-60 Age Cohort

EUROQUO reporting shows lens exchange accounts for 80% of refractive surgery, fueled by presbyopes who view surgery as a lifelong vision upgrade.[4]Elsie Chan, "Refractive lens exchange – the evidence behind the practise," Eye, nature.com Office-based suites handled 2.2% of United States cataract volume in Q1 2023, pointing to cost savings and patient comfort as catalysts for broader adoption.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High out-of-pocket cost and patchy reimbursement | −0.8% | Global; acute in North America and Europe | Medium term (2–4 years) |

| Post-operative dysphotopsia concerns | −0.5% | Global, especially in developed markets | Short term (≤ 2 years) |

| Supply-chain dependence on specialty hydrophobic acrylics | −0.3% | Global; resin production centered in U.S., Europe, Japan | Medium term (2–4 years) |

| Sustainability pressures on single-use plastics | −0.2% | Europe, spillover to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High out-of-pocket cost and uneven reimbursement for premium IOLs

Patients often pay USD 1,500-3,000 per eye because CMS lists no New Technology IOL codes, creating a two-tier access model. The financial load includes diagnostic aberrometry and follow-up adjustments, deterring price-sensitive candidates. International travel can lower the bill, yet quality assurance varies across facilities. CMS restricts payments to standard monofocal lenses, placing the financial burden of premium surcharges squarely on patients. This policy is mirrored in both Germany and the United Kingdom. In response, manufacturers present cost-utility data highlighting diminished reliance on spectacles. Yet, payers maintain a conservative approach, limiting access predominantly to wealthier segments.

Post-Operative Dysphotopsia Concerns Limiting Surgeon Uptake

Meta-analyses link trifocal optics to halos that curb patient satisfaction. The AIOLIS tool shows dysphotopsia drives most complaints, and lens exchanges increase cost and risk. New refractive-segmented optics, such as the enVista Envy, claim 86% low-disturbance rates, easing surgeon apprehension. A 2024 review found that 15%-20% of multifocal recipients reported glare or halos, with up to 3% undergoing explantation.[5]National Center for Biotechnology Information, “Global Cataract Surgery and Visual Outcomes,” ncbi.nlm.nih.gov Non-diffractive EDOF models, such as Tecnis Symfony and Vivity, lower incidence but do not eradicate it. Cautious practitioners therefore default to monofocals for risk-averse patients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Monofocals Anchor Volume, Premiums Drive Margin

Monofocal lenses retained volume leadership with 62.68% intraocular lens market share in 2025. Premium categories, spanning trifocal, toric, EDOF, and accommodating designs, post a 7.16% CAGR that surpasses baseline cataract growth. Demand stems from patients who prioritize uncorrected near vision and from surgeons promoting refractive outcomes as part of cataract management. Multifocal options like PanOptix yield high spectacle independence and fewer halos than early bifocal models. Toric monofocals correct up to 4 D of corneal cylinder and have become routine in eyes with ≥1 D astigmatism. EDOF optics, such as Tecnis Symfony, trade some near acuity for reduced photic side effects, fitting patients skeptical about diffractive rings. Accommodating prototypes including Juvene target ≥3.5 D amplitude, aiming to replicate physiologic focus change, a milestone market observers expect to unlock accelerated premium conversion.

Surgical centers bundle presbyopia-correcting lenses with femtosecond-assisted capsulotomy to enhance centration, while topographers refine pre-op planning for toric axis alignment. Clinicians report that post-refractive-surgery patients often prefer premium solutions because light-adjustable technology can fine-tune residual error. The premium tier extends revenue per procedure, helping clinics offset reimbursement headwinds and encouraging investment in advanced diagnostics.

By Material: Hydrophobic Acrylics Lead, Silicone Gains on Foldability

Hydrophobic acrylic posted a 45.02% 2025 share and underpins most premium optics due to low PCO. Silicone is resurging at 7.05% CAGR because its high elasticity suits 2.0 mm micro-incisions, reducing surgically induced astigmatism. Newer silicone optics incorporate UV-blocking chromophores and can accept post-implant femtosecond power refinement. Hydrophilic acrylic now represents 28.90% of units, rehabilitated by cross-linked polymers and anti-calc coatings that preserve clarity in diabetic vitreous environments. PMMA use declines except in trauma cases that benefit from rigid stability.

Material research focuses on reducing posterior capsule opacification through edge-design micro-texturing and exploring bioresorbable haptics that vanish after capsular fibrosis secures the optic. Suppliers stress the need for dual sourcing of raw monomers because pandemic disruptions revealed dependency risks in hydrophobic acrylic chains.

By End-User: Hospitals Dominate, Clinics Accelerate

Hospitals comprised 57.05% of revenue in 2025, retaining complex comorbidity cases. Ophthalmology clinics and ambulatory surgery centers are expanding at a 7.02% CAGR as payors tilt toward bundled outpatient payments. Clinics combine diagnostics, surgery, and follow-up in a single visit cycle, thereby shortening the time to treatment. Office-based suites, now 2.15% of United States volume, appeal to surgeons seeking scheduling control and to patients who prefer familiar environments. Self-pay RLE patients show high net promoter scores when surgery occurs in physician-owned suites, supporting word-of-mouth expansion. Insurers examine bundled-payment pilots that could accelerate the shift by aligning facility and professional fees.

The migration amplifies demand for compact phaco platforms and sterile-packaged IOL cartridges that fit smaller procedure rooms. Equipment vendors now supply modular cabinets with laminar airflow and digital microscopes suited to clinic retrofits.

By Application: Cataract Dominates, Corneal Disorders Emerge

Cataract accounts for 76.61% of application revenue and will stay the bedrock segment through 2031. Refractive lens exchange for presbyopia grows fastest in premium ASP terms. Phakic IOLs addressing high myopia and ectasia log 6.95% CAGR, led by STAAR Surgical’s EVO platform. Combined collagen cross-linking and toric IOL implantation restores functional acuity in 94% of treated eyes. Presbyopia correction is broadened by the IC-8 Apthera pinhole optic, which masks higher-order aberrations. Surgeons treating Fuchs dystrophy coordinate DMEK with lens implantation, illustrating a trend toward combined anterior segment procedures.

AI-driven calculators merge tomographic and axial length data to model the effective lens position more accurately in irregular corneas, thereby reducing postoperative surprises. These tools reinforce the surgeon's willingness to expand the indications for premium lenses in complex eyes that were once considered marginal candidates.

Geography Analysis

North America led the intraocular lens market in 2025, accounting for 41.76% of revenue, as Medicare covers baseline cataract surgery and patients can self-fund upgrades. Premium penetration in the United States exceeds 21.80%, and ophthalmology practices deploy heavy advertising to attract RLE candidates.

Asia-Pacific records the fastest CAGR of 7.22% due to demographic aging, expanding middle-class spending power, and thriving medical tourism clusters. Thailand and Singapore package premium IOL surgery with three-day recovery stays, drawing inbound volumes that lift average selling prices. China continues to scale cataract capacity, yet premium uptake remains below 9.75%, signaling sizable headroom for growth once income and reimbursement levels rise. India’s high-volume hubs replicate the Aravind model, combining efficiency with modular pricing, bringing premium adoption within reach for urban consumers.

Europe features mature reimbursement but strong sustainability norms. Regulators encourage the use of reduced-plastic delivery systems, prompting lens makers to trial bio-derived cartridge polymers. Germany and Spain report premium penetration near 19.70%, while the United Kingdom remains conservative amid National Health Service budget constraints. CE-marked launches such as Clareon Vivity in 2025 broaden surgeons' presbyopia-correction options.

The Middle East and Africa expand from a lower base as public-private partnerships build specialty eye hospitals in Gulf states and North Africa. Wealthy patients often fly to Europe or Asia for premium surgery, but new centers in Dubai and Riyadh aim to reverse the outbound flow. South America benefits from price arbitrage by North American consumers; Brazil’s private insurers now reimburse specific EDOF lenses, boosting regional demand.

Competitive Landscape

Market concentration is moderate, with technology leadership rather than price defining share. Alcon sustains more than 60% premium-segment revenue through PanOptix, Vivity, and the new 94%-light-utilization PanOptix Pro. Its AutonoMe preloaded driver embeds into efficiency narratives for high-volume clinics. Johnson & Johnson Vision’s TECNIS Odyssey touts low-light contrast gains, positioning the firm as the main challenger. Carl Zeiss Meditec integrates IOLs with diagnostic biometers and femtosecond platforms, locking in ecosystem advantages.

Strategic M&A shapes portfolios. Alcon’s Lensar acquisition strengthens femtosecond guidance, while Carl Zeiss Meditec bought DORC to add retina and cornea tools, enabling full anterior-posterior offerings. Bausch + Lomb secured FDA clearance for the enVista Envy in 2024, betting on glistening-free optics that mitigate dysphotopsia. Start-ups pursue shape-changing, accommodating prototypes or post-implant adjustments. RxSight expanded the number of US centers certified for its light-adjustment station, and Perfect Lens advances femtosecond index shaping that tunes in situ power. Suppliers hedge raw-material risk by near-shoring polymer production in the Americas and Europe.

Value-chain alliances emerge as diagnostics companies partner with lens makers to embed cloud-based nomograms that update with real-world outcomes. Hospitals and payers evaluate outcome-based contracts that tie lens reimbursement to spectacle-free rates at three months, a model that could rewrite competitive yardsticks.

Intraocular Lens Industry Leaders

-

Hoya Corporation

-

Eyekon Medical

-

Carl Zeiss Ag

-

Alcon Inc.

-

Bausch Health Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Surgeons completed the first United States implantations of BVI’s FineVision HP trifocal IOL, offering high-contrast distance, intermediate, and near performance.

- January 2026: Johnson & Johnson Vision sought USD 12 million in municipal incentives to build a packaging and distribution center in Jacksonville and upgrade manufacturing equipment with a USD 500 million outlay.

- June 2025: Rayner’s RayOne Galaxy and RayOne Galaxy Toric became available in Brazil after a successful multicenter study using an AI-generated non-diffractive spiral optic.

- March 2025: Alcon secured CE Mark and launched Clareon Vivity across Europe, pairing extended-range optics with low-halo risk.

- February 2025: Alcon introduced Clareon PanOptix Pro in the United States, integrating ENLIGHTEN NXT optics on its AutonoMe pre-loaded platform.

Global Intraocular Lens Market Report Scope

As per the scope of the report, an intraocular lens is implanted in the eye as part of a treatment for cataracts or myopia. These synthetic lenses are designed for vision correction and replace the eye's natural lens.

The intraocular lens market is segmented by product, end user, and geography. By product, the market is segmented into monofocal intraocular lens, accommodative intraocular lens, multifocal intraocular lens, and toric intraocular lens. By application, the market is segmented into cataract, presbyopia, corneal disorder, and other applications. By end user, the market is segmented into hospitals, ambulatory centers, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. This market analysis report also covers the estimated intraocular lens market sizes and trends for 17 countries across major regions globally. For each segment, the market size is provided in terms of value (USD).

By Product Type

| Monofocal IOL | |

| Premium IOL | Multifocal |

| Toric | |

| Accommodating | |

| Phakic Intraocular Lens (PIOL) | |

| Others |

By Material

| Hydrophobic Acrylic |

| Hydrophilic Acrylic |

| Silicone |

| Polymethyl-methacrylate (PMMA) |

| Others |

By End User

| Hospitals |

| Ambulatory Surgery Centers |

| Ophthalmology Clinics |

| Others |

By Application

| Cataract |

| Presbyopia |

| Corneal Disorders |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Monofocal IOL | |

| Premium IOL | Multifocal | |

| Toric | ||

| Accommodating | ||

| Phakic Intraocular Lens (PIOL) | ||

| Others | ||

| By Material | Hydrophobic Acrylic | |

| Hydrophilic Acrylic | ||

| Silicone | ||

| Polymethyl-methacrylate (PMMA) | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Ophthalmology Clinics | ||

| Others | ||

| By Application | Cataract | |

| Presbyopia | ||

| Corneal Disorders | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the intraocular lens market?

The intraocular lens market stands at USD 7.34 billion in 2026 and is projected to reach USD 10.09 billion by 2031.

Which region is growing fastest for intraocular lenses?

Asia-Pacific posts the highest 7.22% CAGR, driven by aging populations and robust medical-tourism networks.

How quickly are premium IOLs expanding?

Premium lenses grow at 7.16% CAGR, outpacing monofocal options as patients seek spectacle independence.

Which material leads lens production today?

Hydrophobic acrylic holds 45.02% share, though silicone alternatives show the fastest 7.05% growth.

Why do some surgeons hesitate to adopt premium IOLs?

High out-of-pocket costs and concerns about dysphotopsia limit uptake despite clear visual benefits.

Who dominates the premium intraocular lens segment?

Alcon controls more than 60.00% of global premium-segment revenue on the strength of PanOptix and Vivity offerings.

Page last updated on: