Pupillometer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

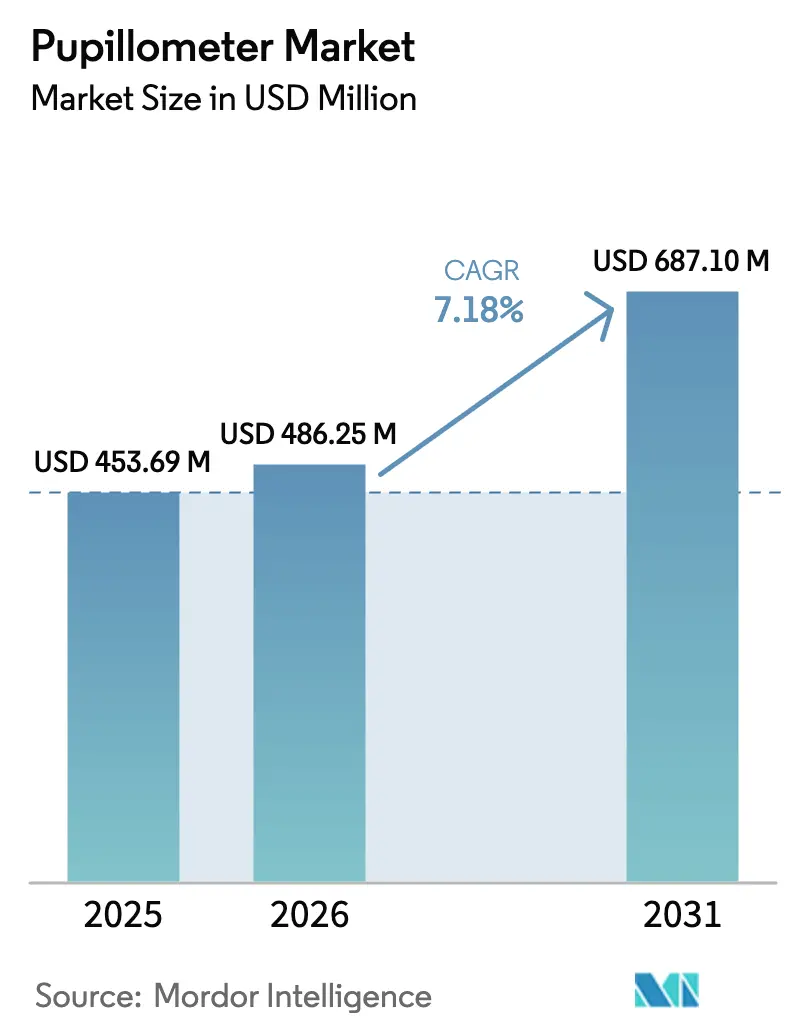

| Market Size (2026) | USD 486.25 Million |

| Market Size (2031) | USD 687.1 Million |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pupillometer Market Analysis by Mordor Intelligence

The pupillometer market size was valued at USD 453.69 million in 2025 and estimated to grow from USD 486.25 million in 2026 to reach USD 687.1 million by 2031, at a CAGR of 7.18% during the forecast period (2026-2031). Rapid adoption of quantitative pupillometry in trauma centers and intensive care units is widening clinical acceptance, while the fusion of infrared optics with AI algorithms is shrinking assessment time from minutes to seconds, boosting critical-care responsiveness. Original equipment manufacturers (OEMs) are embedding secure cloud connectivity that streams de-identified pupillary metrics to electronic health records, aiding trend analysis and early neurological intervention. Sports medicine, defense healthcare, and tele-neurology are opening new addressable volumes as portable and smartphone-based devices allow field deployment. Meanwhile, reimbursement ambiguity and clinician training gaps continue to temper near-term uptake despite clear evidence of outcome improvement.

Key Report Takeaways

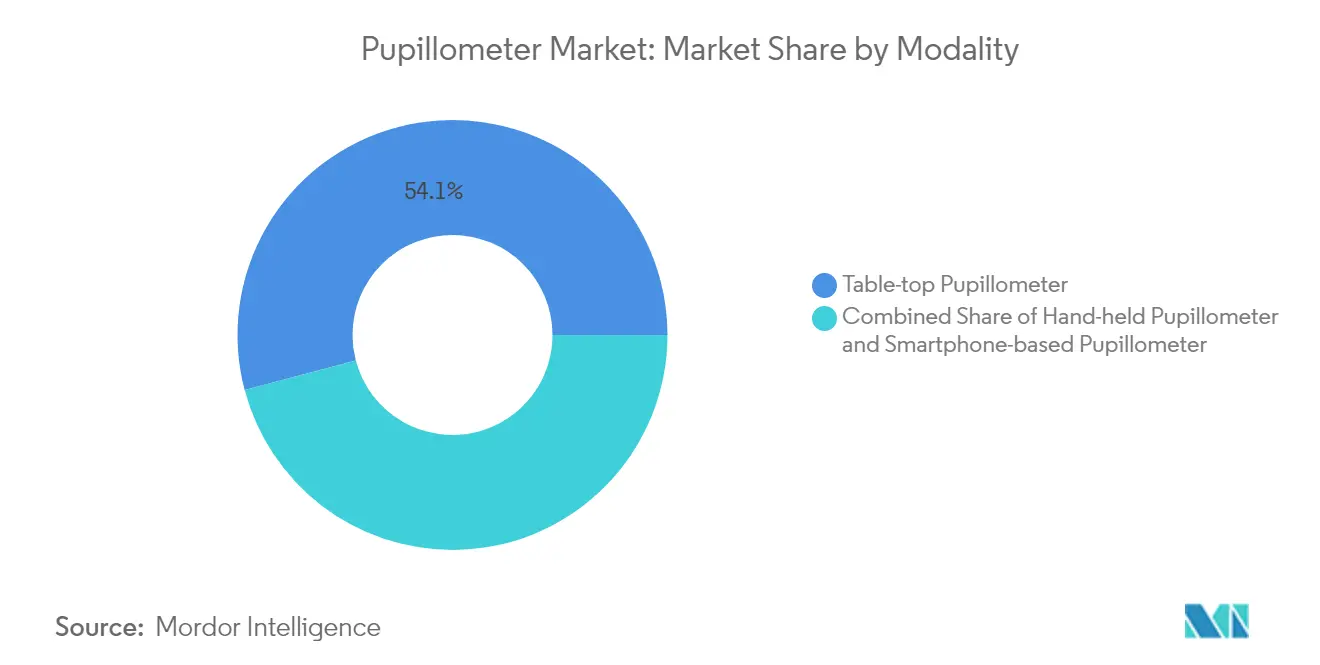

- By modality, table-top systems led with 54.12% revenue share in 2025; hand-held devices are forecast to expand at a 7.72% CAGR through 2031.

- By type, video technology captured 51.62% of the pupillometer market share in 2025, while digital infrared systems are growing at 7.89% CAGR.

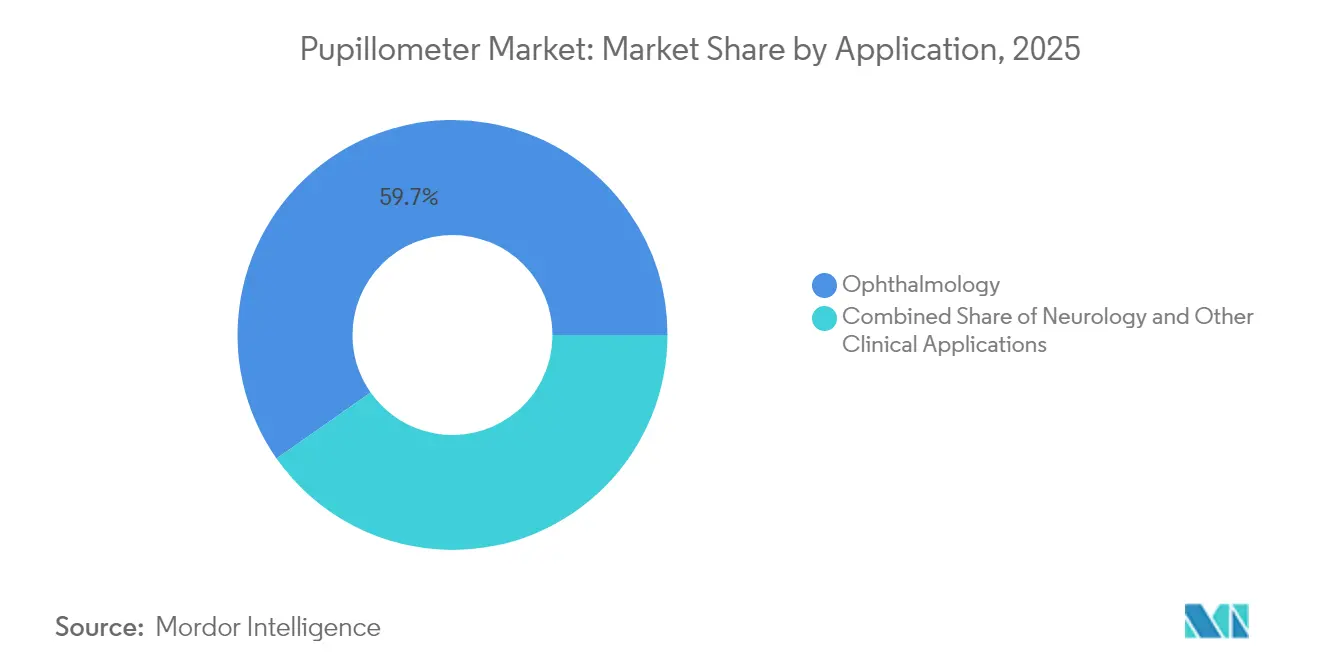

- By application, ophthalmology accounted for 59.74% share of the pupillometer market size in 2025; neurology applications are advancing at an 8.19% CAGR to 2031.

- By end user, hospitals retained 58.56% share in 2025; eye clinics and vision centers are set to grow at an 8.33% CAGR through 2031.

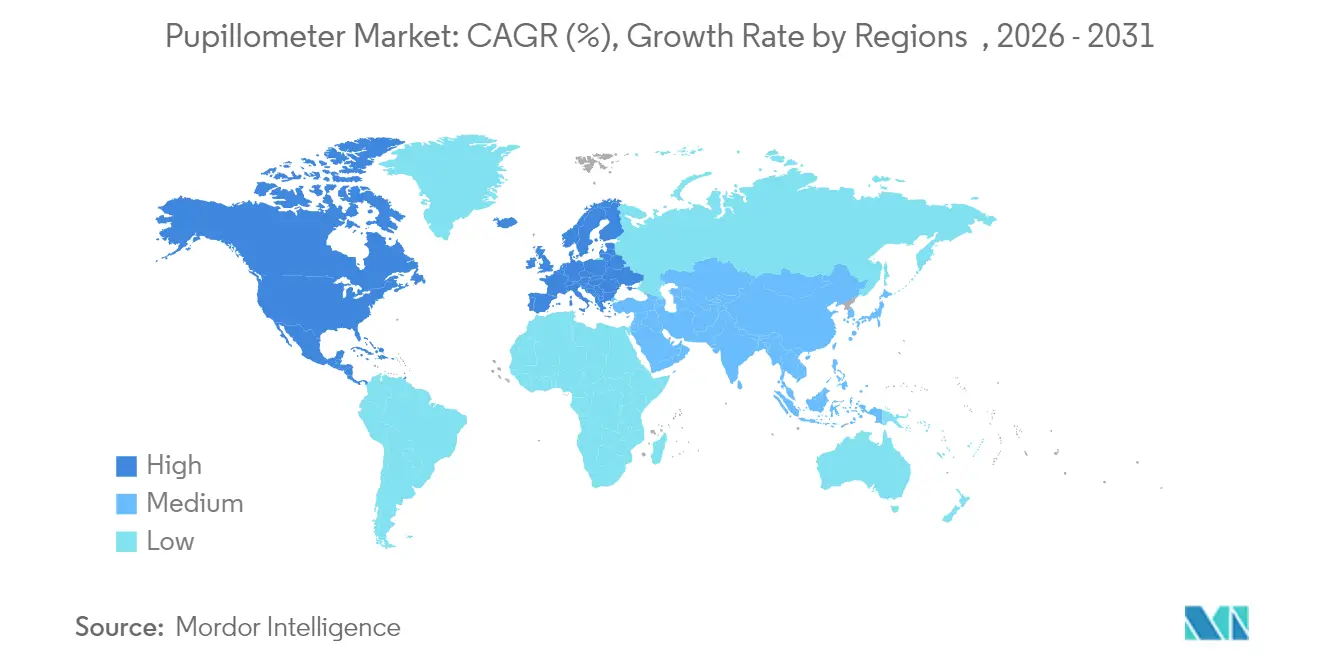

- Regionally, North America dominated with 42.75% share in 2025; Asia-Pacific is the fastest-growing region at an 8.53% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pupillometer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in awareness & technological advances in quantitative pupillometry | +1.8% | Global, with North America & Europe leading adoption | Medium term (2-4 years) |

| Growing prevalence of neuro-critical care & TBI cases | +1.5% | Global, concentrated in regions with aging populations | Long term (≥ 4 years) |

| Increasing adoption for glaucoma & refractive-surgery screening | +1.2% | APAC core, spill-over to North America & Europe | Medium term (2-4 years) |

| Integration into AI-enabled ophthalmic diagnostics | +1.0% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Expansion of point-of-care & tele-neurology platforms | +0.8% | Global, with rural and underserved areas prioritized | Short term (≤ 2 years) |

| Use in sports concussion & battlefield triage protocols | +0.6% | North America & EU, military applications global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Awareness & Technological Advances in Quantitative Pupillometry

Clinicians are shifting from subjective flashlight checks to algorithm-driven Neurological Pupillary Index (NPi) readings that correlate tightly with intracranial pressure changes. Real-time analytics now quantify constriction velocity and dilation lag across diverse iris pigmentations. Portable devices equipped with infrared LEDs fit emergency carts and ambulances, widening the pupillometer market in pre-hospital triage. Cloud dashboards plot longitudinal pupil trends, flagging subclinical neurological shifts up to 4 hours earlier than Glasgow Coma Scale variations. Such objective metrics are convincing payers to pilot outcome-based reimbursement models in high-acuity settings.

Growing Prevalence of Neuro-Critical Care & TBI Cases

Global TBI rates remain elevated in aging populations and contact-sport participants, spurring hospitals to add handheld units across trauma bays. Military medics employ ruggedized devices during battlefield triage, where a 30-second pupil scan informs evacuation priority. Cardiac arrest teams use pupillometry for prognostication within the first 24 hours post-ROSC, trimming ICU length of stay when poor neurological outcomes are predicted early. The expanding evidence base positions the pupillometer market for deeper penetration into comprehensive stroke centers and concussion clinics.

Increasing Adoption for Glaucoma & Refractive-Surgery Screening

Ophthalmologists integrate quantitative pupil analysis to detect retinal ganglion cell dysfunction before visual field loss manifests. Refractive-surgery centers map scotopic and photopic pupil diameters to refine LASIK optical zone design, reducing night-vision complaints. Smartphone-based pupillometers paired with AI grading let outreach programs screen rural populations in minutes, a development accelerating Asia-Pacific volume growth. Pupil metrics also aid diabetic retinopathy risk stratification, merging eye care with chronic disease management.

Integration into AI-Enabled Ophthalmic Diagnostics

Machine-learning models now detect subtle relative afferent pupillary defects with clinician-level accuracy. EHR-linked dashboards chart month-on-month NPi shifts, helping neurologists adjust therapy in real time. Virtual-reality headsets embed eye-tracking sensors that perform covert pupillometry during cognitive tests, blending neurology and mental-health evaluation. Multi-modal platforms combine optical coherence tomography, visual-field data, and pupil metrics, generating 360-degree ocular-neuro profiles that support precision medicine.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition cost & limited reimbursements | -1.2% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Shortage of clinicians trained in neuro-ophthalmic interpretation | -0.8% | Global, with rural areas most affected | Long term (≥ 4 years) |

| Regulatory uncertainty for software-as-medical-device algorithms | -0.6% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Data-privacy concerns over cloud-based pupil recordings | -0.4% | Global, with EU GDPR compliance most stringent | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition Cost & Limited Reimbursements

Capital-intensive units price above USD 20,000, deterring smaller clinics where billing codes remain ambiguous [1]F. Gupta, “Clinical Codes Lacking for Pupillometry,” Aetna Clinical Policy Bulletin, aetna.com. Absence of a dedicated CPT code forces bundling under general eye exams, cutting cost recovery by up to 40%. Service contracts, software licenses, and staff training push total cost of ownership higher. Emerging smartphone alternatives come in below USD 1,000 and threaten to erode premium hardware margins while broadening the pupillometer market footprint among cost-conscious providers.

Shortage of Clinicians Trained in Neuro-Ophthalmic Interpretation

Global neuro-ophthalmology fellowships number fewer than 50 annually, constraining expertise pipelines. Complex pupil physiology demands multidisciplinary knowledge that generalists often lack. Rural hospitals therefore under-utilize installed devices, lowering return on investment. Cloud-based AI analytics that supply auto-generated interpretations will be pivotal to scaling usage beyond tertiary centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: Portability Catalyzes Hand-Held Uptake

Hand-held devices are moving the pupillometer market forward with a 7.72% CAGR as emergency departments and athletic programs favor lightweight designs that run an entire shift on a single charge. Table-top systems still secure 54.12% of 2025 revenue by integrating seamlessly into ICU monitoring arrays, offering multi-parameter analytics alongside vital signs.

Advances in lithium-ion batteries and miniaturized optics are shrinking unit weight below 300 grams, allowing first responders to capture pupillary metrics mid-transport. Table-top platforms increasingly bundle AI dashboards that push alerts to neurologists’ smartphones, retaining relevance despite their stationary footprint. Market entrants leveraging smartphone chassis bypass proprietary hardware costs, signaling a future where mobility defines competitive edge.

By Type: Video Leads, Infrared Accelerates

Video units accounted for 51.62% pupillometer market share in 2025, reflecting widespread hospital protocols that require high-frame-rate recordings for medico-legal documentation. Digital infrared devices are gaining at an 7.89% CAGR as sensor fidelity now compensates for iris pigmentation variance.

High-resolution video streams allow frame-by-frame review of constriction dynamics, benefitting teaching hospitals that archive de-identified clips for AI model training. Infrared units excel under ambient-light fluctuations, supporting rural outreach vans where dark room conditions are hard to maintain. Hybrid products combining video and infrared tracking are slated for launch in 2026, aiming to unify best-in-class features while expanding the pupillometer market size across both acute and ambulatory settings.

By Application: Neurology Outpaces Ophthalmology

Ophthalmology sustained 59.74% of 2025 revenue, yet neurology is climbing fastest at 8.19% CAGR as TBI screening protocols standardize objective pupil checks. The pupillometer market size for neurology-specific usage is projected to reach USD 193.6 million by 2031, underpinned by sports-concussion mandates.

Cardiac ICUs are embedding NPi alerts into code-blue dashboards, letting intensivists track recovery trajectories post-resuscitation. Ophthalmology continues leveraging pupil metrics for glaucoma detection, but integrated AI decision support now shortens chair time by 15%, freeing capacity for higher-margin surgical consults. Cross-disciplinary adoption underscores the expanding clinical canvas for quantitative pupillometry.

By End User: Vision Centers Close the Gap

Hospitals led spending with 58.56% in 2025; however, eye clinics and vision centers are adding units at an 8.33% CAGR. Their share of the pupillometer market size is forecast to climb to USD 228.4 million by 2031 as LASIK volumes rebound.

Retail optical chains pilot kiosk-based pupil exams that funnel glaucoma suspects into affiliated ophthalmology practices, demonstrating new retail–clinical synergies. Teaching hospitals deploy multi-unit fleets covering neuro-trauma, anesthesia, and stroke units, ensuring round-the-clock availability. Meanwhile, military clinics integrate ruggedized models into battlefield telehealth kits, highlighting the technology’s versatility across end-user segments.

Geography Analysis

North America retained 42.75% of global revenue in 2025 as FDA Class I classification minimizes regulatory overhead, accelerating hospital procurement cycles . Multi-center trials funded by the National Institutes of Health continue to validate new AI algorithms, reinforcing payer confidence. Collegiate athletics increasingly require baseline pupil scans, creating incremental device placements outside traditional hospital settings.

Asia-Pacific is set to register the swiftest trajectory at an 8.53% CAGR through 2031. High myopia prevalence and growing neurologic disease burden are compelling governments to subsidize early-detection technologies. Private ophthalmology chains in India and China are bundling pupil analytics with cataract and refractive packages to differentiate service offerings. Domestic startups are also entering the pupillometer market with low-cost smartphone adaptors, intensifying price competition.

Europe continues to capitalize on cohesive regulatory pathways under the Medical Device Regulation, facilitating faster rollouts of digital infrared innovations. Aging demographics drive elevated glaucoma incidence, sustaining device demand across public hospitals and private clinics. Cross-border telemedicine initiatives linking rural Baltic clinics with neuro-ophthalmology hubs in Germany exemplify collaborative deployment models that extend diagnostic reach.

Regulatory Landscape

In the United States, pupillometers are regulated as medical devices and listed under 21 CFR 886.1700 as Class I devices, which generally reduces the premarket notification (510(k)) burden while still requiring establishment registration and device listing. From February 2, 2026, the FDA Quality Management System Regulation (QMSR) aligns more directly with ISO 13485:2016 expectations, increasing the emphasis on documented design controls, manufacturing controls, and traceability across the pupillometer supply base.

For OEMs and new entrants adding software analytics, cloud connectivity, or AI modules, compliance programs increasingly span both device-quality requirements and broader privacy and cybersecurity obligations tied to de-identified pupil recordings and EHR connectivity. This matters most in connected workflow deployments, where hospitals evaluate device procurement alongside QMS maturity and interoperability readiness rather than optics performance alone.

Value Chain Analysis

The pupillometer value chain begins with component sourcing, particularly infrared emitters, optical sensors, camera modules for video systems, microcontrollers, batteries, and housings designed for clinical cleaning and durability. Device OEMs then integrate optics, embedded software, and calibration routines, followed by validation for use cases spanning ophthalmology clinics and neuro-critical care. With the FDA QMSR update taking effect on February 2, 2026, quality-system alignment with ISO 13485:2016 raises expectations for supplier qualification, incoming inspection, and documentation.

Go-to-market pathways typically mix direct sales to hospitals and IDNs for ICU and ED deployment with channel distribution into ophthalmology and optometry clinics, where pupillometry is often bundled into broader diagnostic suites. After installation, value capture increasingly depends on software licensing, connectivity modules that feed pupil metrics into EHR and analytics dashboards, service and calibration contracts, and clinician training, which together shape total cost of ownership and renewal economics.

Competitive Landscape

The pupillometer market is moderately fragmented. NeurOptics, Essilor Instruments, and NIDEK anchor the premium tier through validated algorithms and broad distribution. NeurOptics extended its NPi-300 rollout to 15 countries in 2024, reinforcing clinical brand equity [3]NeurOptics Inc., “NPi-300 Global Launch Press Release,” neuroptics.com . Essilor Instruments leverages its spectacle-lens network to cross-sell digital infrared units into retail optometry. NIDEK bundles pupillometry with auto-ref keratometers, targeting high-volume Asian clinics.

Smartphone-centric entrants are disrupting incumbents by slashing capital outlay to sub-USD 1,000 and offering pay-per-use analytics subscriptions. A leading app developer recently partnered with an EHR vendor to auto-populate NPi scores into patient charts, shortening documentation time by 30%. OEMs respond by unveiling hybrid software-hardware solutions and pursuing CE-marked AI modules that deliver clinician-grade analysis on consumer devices.

Partnerships dominate strategic activity. In 2025, a US hospital network inked a deal with a cloud-AI specialist to link bedside pupillometers to a centralized neuro-dashboard, pooling data from 50 ICUs. Simultaneously, a European defense agency ordered ruggedized units capable of withstanding −20 °C field conditions, underscoring niche-application potential. Patent filings center on gaze-independent pupil tracking and machine-vision algorithms, signaling a pivot toward software-defined differentiation.

Pupillometer Industry Leaders

NeurOptics Inc.

Essilor Group (Essilor Instruments)

NIDEK SA

Reichert Inc.

Konan Medical USA Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space exists in scaling quantitative pupillometry beyond tertiary centers into workflows that already prioritize speed, repeatability, and documentation, including emergency medicine, trauma bays, transport, and tele-neurology. Connectivity and workflow integration are a practical lever: NeurOptics has highlighted objective pupillometry for critical care and neurology and has promoted connected approaches intended to support clinical adoption, while hospital decision-makers increasingly assess pupillometers as part of a broader data pipeline rather than as standalone measurement tools.

In ambulatory eye care, opportunities concentrate on embedding objective pupil checks into multi-test diagnostic lanes and refractive screening, supported by established ophthalmic equipment vendors. Konan Medical USA markets EyeKinetix for objective pupil checking alongside clinical practice guidance, and Reichert Technologies continues to emphasize diagnostic integration, aligning with clinics seeking single-vendor workflows and streamlined exams. Across both acute and ambulatory settings, pricing pressure from lower-cost and smartphone-centric alternatives creates room for tiered offerings, where premium devices compete on validated algorithms, interoperability, and service, while entry systems compete on access and deployment volume.

Recent Industry Developments

- May 2026: NeurOptics held clinical education sessions featuring NPi pupillometry technology at AACN NTI 2026. The event points to educational and clinical adoption momentum in critical care as practitioners encounter pupillometry data during rounds. This broadens professional awareness and potential EMR interoperability within ICU workflows.

- May 2026: NIDEK launched ICE-2 Intelligent Blocker to support accurate lens edging processes. The launch extends product-level activity within the ophthalmic device manufacturing ecosystem. It could strengthen adoption of NIDEK pupillometry linked workflows across clinics.

- March 2026: NeurOptics installed NPi-Connect SmartGuard Connectivity Hub across University of Nebraska Medical Center critical care departments. The deployment shows how centralized pupillometry analytics can be integrated into ICU data flows. It supports broader uptake by connecting pupillometry with EMR systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers revenues from pupillometer devices used to measure pupil size and reactivity in clinical and screening settings, including handheld and table-top systems sold for ophthalmic and neurologic assessment.

Scope exclusions: We exclude general eye exam devices that do not measure pupil dynamics, along with software-only tools and non-medical consumer apps that do not qualify as pupillometers.

Segmentation Overview

- By Modality

- Hand-held Pupillometer

- Table-top Pupillometer

- Smartphone-based Pupillometer

- By Type

- Digital (Infrared) Pupillometer

- Video Pupillometer

- Photorefractor-based Pupillometer

- By Application

- Ophthalmology

- Neurology

- Other Clinical Applications

- By End User

- Hospitals

- Eye Clinics & Vision Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public healthcare and medical device reference points to keep the sizing grounded in real demand signals. Sources used include, for example, the US FDA device databases, US National Library of Medicine resources, the World Health Organization, the World Bank macro indicators, and OECD health statistics, which help with care setting mix and spending context.

We also reviewed company filings, investor presentations, distributor catalogs, hospital procurement notes in reputed press, and clinical society pages where available. These sources were used to understand typical use cases and purchasing cycles. In a few cases, we used paid subscriptions for company financials and news, and a paid patent database, mainly to confirm product activity and timing of launches. These desk sources are not exhaustive, and additional public and paid references were used to collect, cross-check, and clarify inputs.

Primary Interviews and Surveys

Primary work relied on interviews and short surveys with a mix of device-side experts and care delivery stakeholders, including clinical users in ophthalmology and critical care, biomedical procurement teams, and distribution-channel participants. Since adoption patterns differ by care setting, these conversations were used to validate unit placement logic, replacement timing, and how pricing varies between handheld and table-top purchases.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 21% | APAC: 44% |

| Mid tier: 44% | Functional/Unit leaders: 37% | EMEA: 35% |

| Smaller Players: 22% | Managers: 42% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down pathway where the demand pool is reconstructed from care setting adoption, procedure and monitoring intensity, and the share of sites that use quantitative pupillary measurement as part of routine workflow. We then cross-checked those totals with selective bottom-up approximations, such as sampled average selling price ranges multiplied by estimated unit volumes by modality, followed by distributor and channel checks to keep the totals realistic.

Key model inputs included the installed base trend in hospitals and eye clinics, replacement cycles for handheld devices, average device utilization by care setting, and pricing bands by modality and feature level (digital versus video capabilities). We also accounted for regional uptake differences linked to clinical protocols and training. Where bottom-up evidence was thin for smaller geographies, we filled gaps using validated proxy ratios from similar care settings and then adjusted with expert feedback so the assumptions remained explainable.

Forecasting used scenario analysis supported by a light multivariate view of drivers such as hospital critical care capacity additions, ophthalmology diagnostic volumes, and pricing drift from feature upgrades. The final trajectory was accepted only after the driver paths matched what interviewees described for purchasing lead times and budget constraints.

Data Validation & Update Cycle

Validation was performed through stepwise cross-checks to reduce single-source bias. We compared outputs against independent signals like the direction of regional healthcare spending, reported device adoption cues in clinical settings, and visible product activity, then reviewed results for outliers before sign-off.

Where the model produced sharp jumps, we revisited the assumptions and, if needed, re-engaged primary contacts to confirm whether a change was real or a data artifact. Reports refresh annually, with interim updates triggered by material events such as regulatory changes, major launches, or supply shifts. Before delivery, an analyst performs a final check to ensure the latest available information is reflected in the market numbers and narrative.

Mordor Intelligence's Pupillometer Market Size Versus Other Published Estimates

Published pupillometer market values can look inconsistent because each publisher makes different calls on what is counted, which year is treated as the base, and how pricing is carried forward. The table helps show how those choices can move the number up or down even when the growth story appears similar.

A common gap driver is scope. Some estimates bundle broader eye examination equipment or related neuro-monitoring tools, which inflates the addressable pool beyond true pupillometers. Differences also come from pricing methods, since a straight-line ASP assumption can overshoot reality when mix shifts toward handheld devices, and from refresh cadence, since older models may not reflect recent purchasing pauses or protocol-driven adoption changes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 453.69 M (2025) | |

| Trade Journal A | USD 379.20 M (2023) | Uses an earlier base year and appears to emphasize device shipments without fully adjusting for price mix by modality, which can understate revenue when higher-feature systems are purchased. |

| Industry Publisher B | USD 310.00 M (2024) | Covers a narrower device definition and assumes conservative adoption in critical care, which reduces the implied installed base and keeps the total lower than a care setting driven demand build. |

The table shows a spread that mainly comes from base-year choice and what gets counted as a qualifying device, and in Mordor Intelligence's model the total is built around pupillometer-only revenues across clinical use cases, with modality-level pricing and adoption checks used to keep the figure traceable to real purchasing behavior.

Key Questions Answered in the Report

How big is the Pupillometer Market?

The Pupillometer Market size is expected to reach USD 486.25 million in 2026 and grow at a CAGR of 7.18% to reach USD 687.1 million by 2031.

Which modality is growing fastest?

Hand-held devices post the highest growth at a 7.72% CAGR as emergency medicine, sports clinics, and military units favor portable diagnostics.

Who are the key players in Pupillometer Market?

NeurOptics Inc., Essilor Group (Essilor Instruments), NIDEK SA, Reichert Inc. and Konan Medical USA Inc. are the major companies operating in the Pupillometer Market.

Why is Asia-Pacific the fastest-growing region?

Expanding healthcare infrastructure, high myopia prevalence, and rising neurological disease incidence are propelling an 8.53% CAGR in Asia-Pacific.

Which region has the biggest share in Pupillometer Market?

In 2025, the North America accounts for the largest market share in Pupillometer Market.

What barriers limit wider adoption?

High capital cost, inconsistent reimbursement, and a shortage of clinicians trained in neuro-ophthalmic interpretation remain key obstacles.

Page last updated on: