Market Overview

| Study Period | 2020 - 2031 |

|---|---|

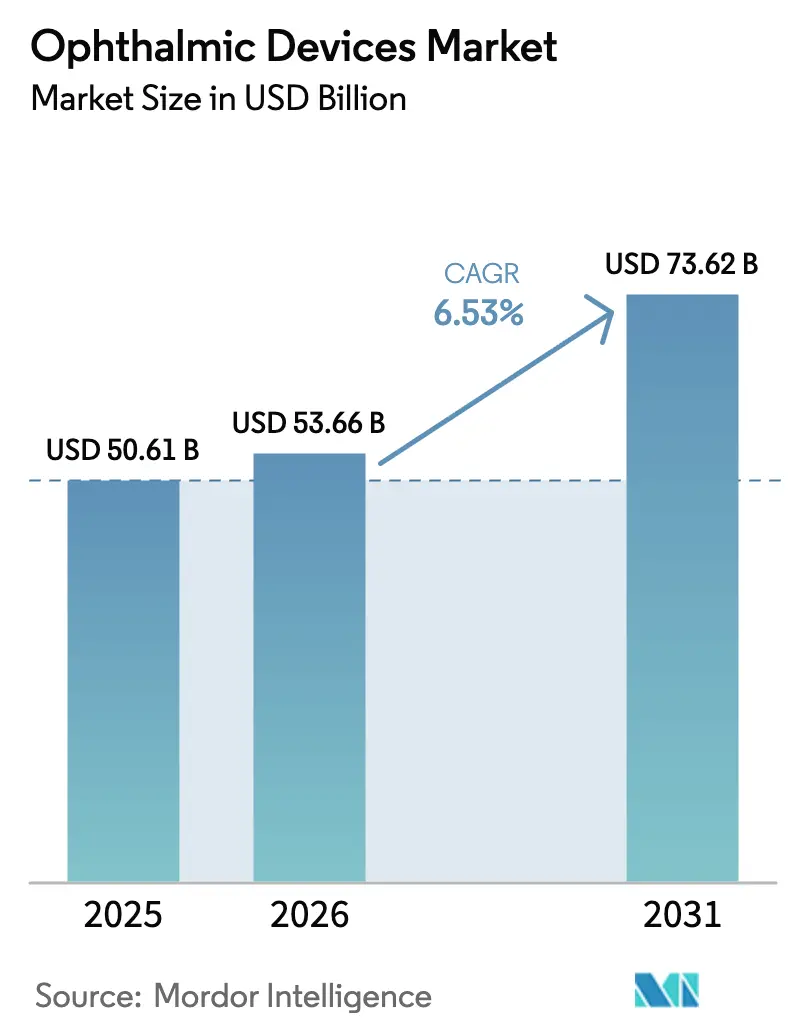

| Market Size (2026) | USD 53.66 Billion |

| Market Size (2031) | USD 73.62 Billion |

| Growth Rate (2026 - 2031) | 6.53% CAGR |

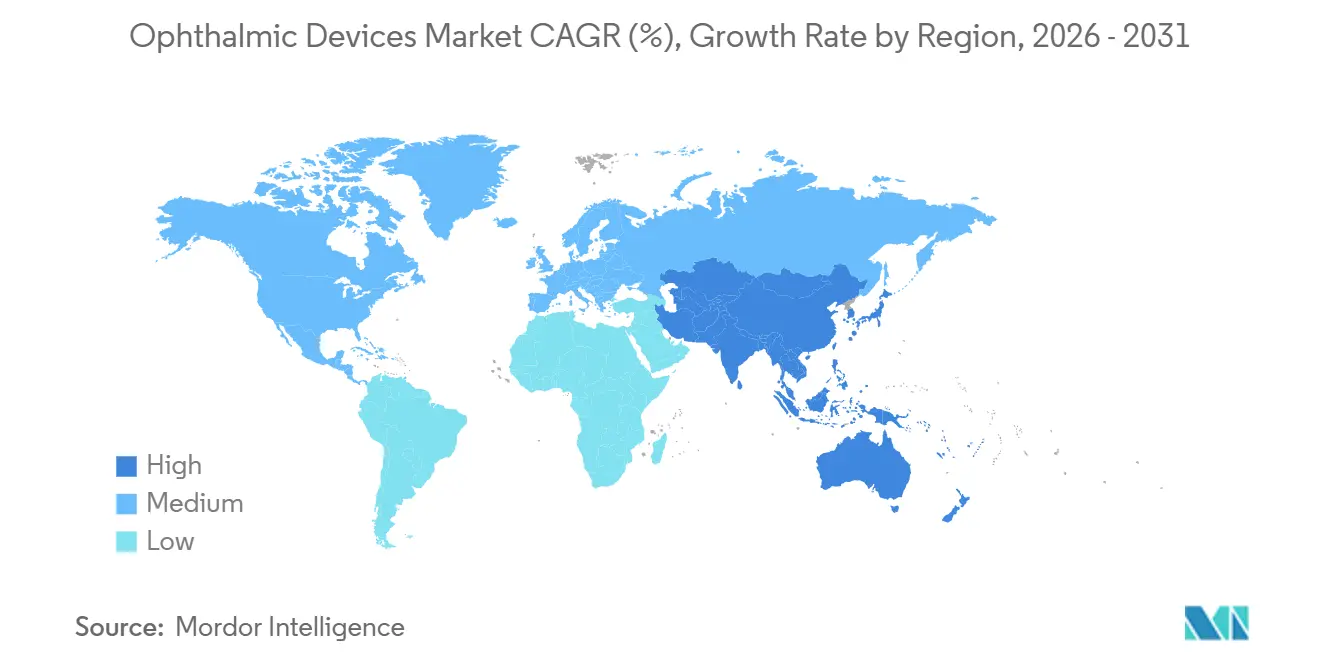

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ophthalmic Devices Market Analysis by Mordor Intelligence

The Ophthalmic Devices Market size is expected to grow from USD 50.61 billion in 2025 to USD 53.66 billion in 2026 and is forecast to reach USD 73.62 billion by 2031 at 6.53% CAGR over 2026-2031.

Demographic aging, surging diabetes incidence, and rapid commercialization of AI-enabled diagnostic imaging compress traditional screening cycles from weeks to minutes, catalyzing equipment replacement as health systems pivot toward preventive eye care. Vision care devices retained volume leadership, yet commoditization pressures on contact lenses and frames are redirecting capital toward diagnostics that generate recurring scan revenues under value-based reimbursement schemes. Hospitals remain the single largest spending venue, but payers are accelerating the shift to ambulatory surgery centers to shave facility fees by up to 40%, thereby bolstering demand for compact femtosecond lasers, MIGS micro-stents, and single-use instrument kits that support same-day discharge models. Competitive intensity is rising as vertically integrated majors bundle diagnostic hardware, surgical consumables, and data analytics into lock-in contracts. At the same time, cybersecurity mandates add development timelines that favor well-capitalized firms able to absorb compliance overhead.

Key Report Takeaways

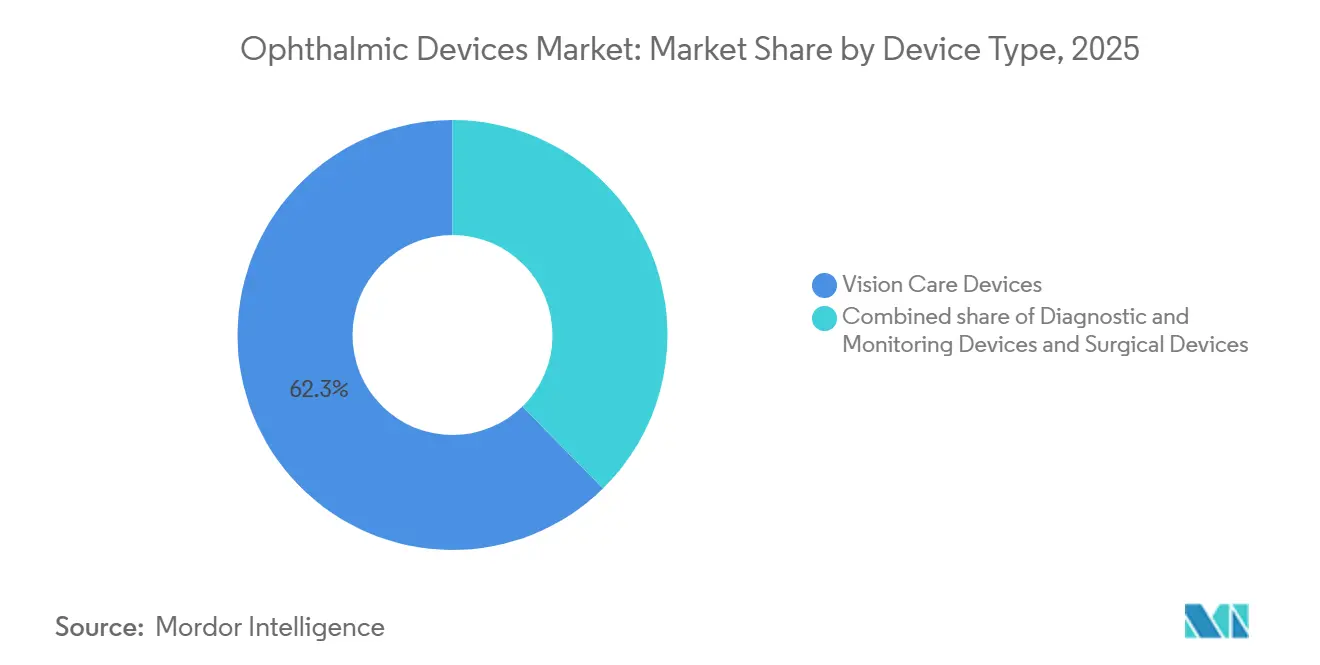

- By device type, Vision Care Devices led with 62.34% revenue share in 2025; Diagnostic & Monitoring Devices are projected to grow at an 8.65% CAGR through 2031.

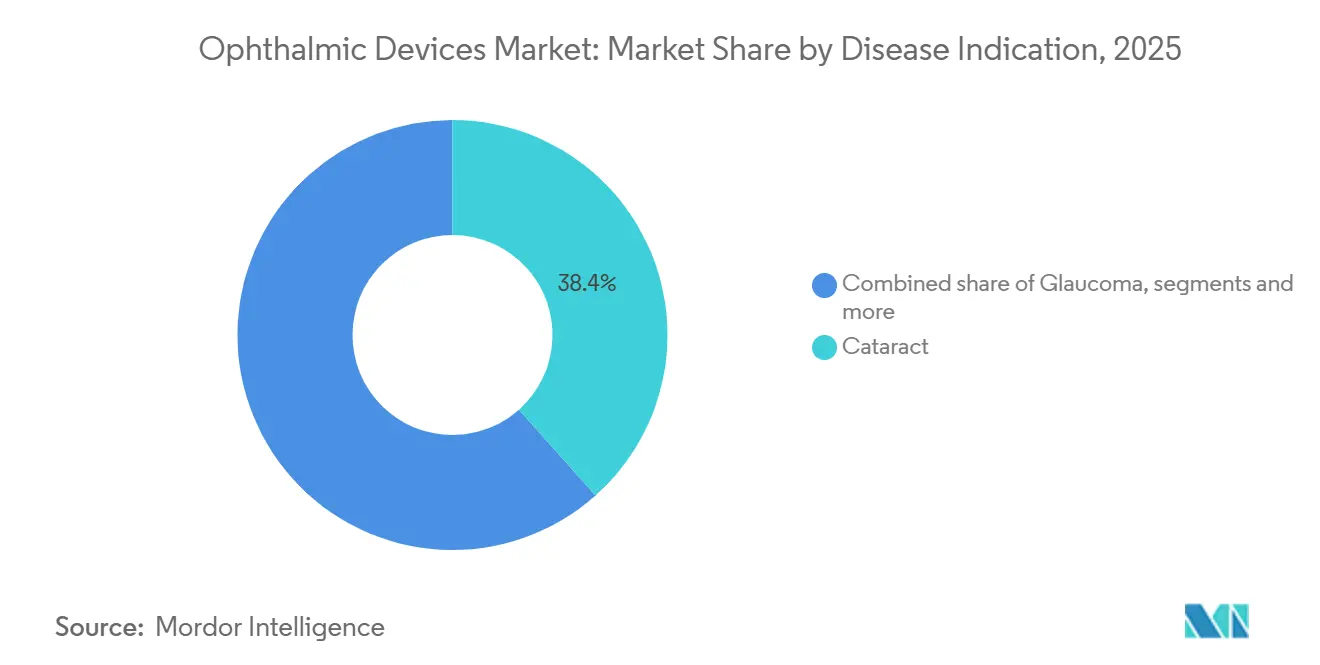

- By disease indication, cataract procedures accounted for 38.41% of spending in 2025, while diabetic retinopathy treatment is advancing at a 7.82% CAGR through 2031.

- By end-user, hospitals held 42.74% of the ophthalmic devices market share in 2025, whereas ambulatory surgery centers recorded the fastest trajectory at 7.67% CAGR to 2031.

- By geography, North America captured 39.94% of the 2025 revenue; the Asia Pacific is forecast to expand at a 7.12% annual rate through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Ophthalmic Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Integrated Ophthalmology-Primary Care Clinics in Emerging Markets | +0.9% | APAC core (India, China, Indonesia), spill-over to Sub-Saharan Africa | Medium term (2-4 years) |

| Growing Adoption of AI-Enabled Diagnostic Imaging Systems | +1.2% | Global, with early penetration in North America & EU, rapid uptake in APAC urban centers | Short term (≤ 2 years) |

| Rising Prevalence of Vision Disorders in Aging Populations | +1.5% | Global, concentrated in North America, Europe, Japan, and China | Long term (≥ 4 years) |

| Surge in Employer-Funded Digital Eye-Health Wellness Programs | +0.6% | North America & EU corporate hubs, pilot programs in Singapore and UAE | Short term (≤ 2 years) |

| Technological Advancements in Minimally Invasive Ophthalmic Surgeries | +1.1% | Global, led by North America and Europe, accelerating adoption in Latin America and Middle East | Medium term (2-4 years) |

| Adoption of Sustainable, Single-Use Ophthalmic Instruments to Reduce Infection Risk | +0.7% | Global, with regulatory push in EU (MDR compliance) and North America (FDA guidance) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Integrated Ophthalmology-Primary Care Clinics in Emerging Markets

Integrated eye-care hubs across India, China, and Southeast Asia embed tonometry, fundus photography, and visual-acuity tests into routine wellness visits, shortening referral cycles from six weeks to two days. India’s National Programme for Control of Blindness established 1,200 vision centers in 2024, each linked via tele-ophthalmology to tertiary hospitals, enabling the early detection of glaucoma and retinopathy while boosting equipment utilization for portable slit lamps and autorefractors[1]Ministry of Health and Family Welfare, India, “National Programme for Control of Blindness,” mohfw.gov.in. China’s Healthy China 2030 blueprint mandates annual eye exams for citizens over 60, stimulating the purchase of compact OCTs and handheld tonometers in township clinics that previously lacked ophthalmic capital assets. Private chains, such as Aravind Eye Care, offer turnkey clinic franchises that bundle diagnostics, EMR platforms, and workforce training, thereby accelerating ophthalmic device market penetration across Tier-2 and Tier-3 cities. Earlier detection pulls surgical volume forward, lifting cataract and MIGS procedures while lowering lifetime treatment costs, giving policymakers fiscal incentives to expand the model.

Growing Adoption of AI-Enabled Diagnostic Imaging Systems

Autonomous AI algorithms for diabetic retinopathy and AMD have received FDA and CE clearances, empowering primary-care teams to execute point-of-care retinal scans with over 90% sensitivity in under 60 seconds, comparable to the performance of retina specialists. EyeArt deployments reached over 900 U.S. sites by mid-2025, resulting in a 40% increase in retinopathy detection compared to legacy referral pathways, as patients receive same-visit results and immediate care plans. Payers reimburse USD 50–75 per AI scan, compared to USD 150 for specialist consultations, catalyzing rapid uptake in cost-conscious systems and reinforcing preventive care contracts. The technology also addresses workforce deficits, with the American Academy of Ophthalmology forecasting a shortage of 4,000 retina specialists by 2030, allowing specialists to focus on managing complex therapeutics while AI screens routine cases[2]American Academy of Ophthalmology, “2025 Workforce Projections,” aao.org. Vendors now integrate AI modules directly into OCT and fundus platforms, converting hardware into software-upgradable assets and anchoring long-term service revenues.

Rising Prevalence of Vision Disorders in Aging Populations

Global citizens aged 60+ will climb to 1.4 billion by 2030, driving cataract prevalence past 32 million and glaucoma cases toward 112 million by 2031. Japan and South Korea already log more than 1.5 million cataract surgeries per year, sustaining premium IOL demand despite reimbursement headwinds. China’s seniors are projected to reach 400 million by 2035, triggering an exponential increase in purchases of phacoemulsification units and MIGS micro-stents, as domestic manufacturers capture a 20% share by offering price points 40% lower than those of their international counterparts. High-income nations face an escalation of AMD, which doubled between 2010 and 2025, fueling anti-VEGF injection kit volumes and the adoption of sustained-release implants. Aging demographics, therefore, guarantee procedure growth even when device ASPs moderate under competitive pressure, underpinning the long-run outlook for the ophthalmic devices market.

Surge in Employer-Funded Digital Eye-Health Wellness Programs

Corporations in North America and Europe embed smartphone-based vision tests into annual wellness checks, citing productivity gains once refractive errors are corrected. VSP Vision Care and EyeMed rolled out remote refraction apps in 2024, enabling employees to obtain prescriptions without in-person clinic visits and order lenses directly, thereby increasing the utilization of daily-disposable contacts. Johnson & Johnson Vision installed on-site screening kiosks at Fortune 500 campuses, identifying undiagnosed intraocular pressure spikes in 18% of the screened staff, catalyzing early glaucoma referrals. Employers report a 3:1 return on investment within 18 months owing to fewer visual-error-related mistakes and reduced absenteeism. Pilot programs have been implemented in Singapore and the UAE, signaling potential global expansion that will increase the ophthalmic devices market.

Restraints Impact Analysis of Ophthalmic Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Ophthalmic Equipment | -0.8% | Global, acute in emerging markets (India, Indonesia, Sub-Saharan Africa) and rural North America | Medium term (2-4 years) |

| Rising Cybersecurity Risks in Connected Diagnostic Devices | -0.5% | Global, heightened in North America & EU due to regulatory scrutiny | Short term (≤ 2 years) |

| Stringent and Divergent Global Regulatory Compliance Requirements | -0.6% | Global, with friction points between FDA, EU MDR, and China NMPA | Long term (≥ 4 years) |

| Supply Chain Vulnerabilities for Specialty Optical Components | -0.7% | Global, concentrated impact in North America and Europe due to reliance on Asian component suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Ophthalmic Equipment

Femtosecond lasers listed above USD 500,000 and swept-source OCT systems run USD 120,000–150,000, pricing out independent practices that perform fewer than 200 cataract surgeries per year, despite leasing programs that still demand USD 8,000–12,000 monthly[3]American Society of Cataract and Refractive Surgery, “Capital Cost Survey 2025,” ascrs.org. Public hospitals in India and Indonesia allocate under USD 50,000 annually for ophthalmic capital expenditure, delaying upgrades by half a decade and concentrating technology in urban centers. Zeiss launched a USD 75,000 OCT variant in 2025, trading scan density for affordability, but image-quality compromises slow uptake among clinicians sensitive to diagnostic accuracy. Capital hurdles thus curb the penetration of next-generation devices and temper the growth of the ophthalmic devices market in price-constrained geographies.

Rising Cybersecurity Risks in Connected Diagnostic Devices

Fourteen ransomware incidents at U.S. eye-care networks in 2024 exposed vulnerabilities in networked OCT and fundus cameras, prompting the FDA to draft guidance mandating secure boot protocols and software bills of materials. Compliance extends clearance timelines by up to 18 months and adds USD 2–3 million per product line, favoring large OEMs with in-house security teams. Hospitals now require third-party penetration tests before procurement, which stretches sales cycles and increases working-capital demands on smaller vendors. Legacy devices, about 40% of installed fleets, cannot accept firmware patches, forcing practices to weigh replacement costs against operational continuity, a dilemma that restrains ophthalmic devices market refresh rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Diagnostics Outpace Vision Care in Growth

Diagnostic & monitoring devices generated robust demand, advancing at an 8.65% CAGR from 2026 to 2031, significantly faster than overall ophthalmic devices market expansion. Swept-source OCT and widefield fundus cameras deliver tenfold faster scans than time-domain units, unlocking earlier choroidal neovascularization detection and guiding anti-VEGF therapy escalation. Hand-held tonometers priced below USD 5,000 extend glaucoma screening into pharmacies and primary-care clinics across the Asia Pacific, broadening the installed base underpinning the ophthalmic devices market size for diagnostics. In contrast, Vision Care Devices retained 62.34% of 2025 revenue but faces ASP erosion as direct-to-consumer disruptors cut spectacle and contact lens margins by 30–40%.

Vision care remains volume-dominant, buoyed by urban myopia prevalence exceeding 50% in China and South Korea; however, slower growth will gradually reduce its contribution to the ophthalmic devices market share over time. CooperVision’s MiSight lenses, which curb axial elongation by 50% over three years, generated USD 120 million in sales in 2025, illustrating a willingness to pay for clinically differentiated products despite price sensitivity. Smart contact lenses with embedded glucose and pressure sensors are slated for 2027 launches, promising new revenue streams but facing regulatory complexity that could temper the near-term growth of the ophthalmic devices market. Surgical devices are growing moderately as ASCs opt for refurbished machines bundled with consumables. This model locks practices into long-term contracts, thereby impeding the displacement of new entrants by incumbents.

By Disease Indication: Diabetic Retinopathy Gains Momentum

Cataract surgeries captured 38.41% of the 2025 disease-indication revenue, driven by aging demographics and widespread access to phacoemulsification. In contrast, diabetic retinopathy is expected to command the fastest expansion at a 7.82% CAGR through 2031. Autonomous AI screening slashes per-patient costs from USD 150 to USD 50, enabling payers to mandate annual retinal scans in diabetes care plans, which boosts the ophthalmic devices market size associated with fundus imaging and OCT. The rising prevalence of diabetes, projected to affect 643 million adults by 2030, escalates demand for OCT, injection kits, and sustained-release implants, such as Genentech’s Susvimo, which halves the injection frequency and improves compliance.

Glaucoma interventions via MIGS and laser trabeculoplasty are also advancing steadily, with Glaukos and Alcon securing a 60% U.S. share in 2025, owing to favorable Medicare codes that reimburse USD 1,200–1,500 per procedure. Anti-VEGF therapies for AMD generated USD 6 billion in device-linked revenue from injection systems in 2025, demonstrating sizable but mature spend patterns relative to faster-growing diabetic retinopathy. Large emerging markets, such as India and China, are expected to exceed 15 million cataract procedures annually by 2030, supporting the uptake of premium IOLs and femtosecond lasers, albeit at ASPs 40% below Western pricing due to domestic competition. This will expand the ophthalmic devices market size, albeit at the expense of diluting the gains for multinationals.

By End-User: ASCs Capture Share from Hospitals

Hospitals accounted for 42.74% of 2025 revenue, reflecting complex cases that require overnight monitoring, but ambulatory surgery centers are rising at a 7.67% CAGR to 2031 as Medicare’s site-neutral payments erase historical hospital premiums and accelerate ophthalmic devices market migration. ASCs conduct 15-minute cataract procedures versus 45-minute hospital sessions, thereby elevating daily case counts and boosting the return on capital for femtosecond lasers, which are priced at USD 500,000.

Specialty ophthalmic clinics capture a 30% share in 2025 by focusing on refractive and cosmetic surgeries, which are often financed out-of-pocket, thereby insulating revenue from payer cuts and fostering the rapid adoption of high-margin femtosecond lasers and premium IOLs. Optical retail chains integrate autorefractors and tele-optometry links to deliver prescriptions within 20 minutes, siphoning routine eye-exam traffic away from clinics and widening the ophthalmic devices market as chains expand internationally. Hospitals retain dominance in complex pediatric and vitreoretinal surgery; however, routine diagnostics and cataract workflows continue to shift toward ASCs and clinics, redistributing the ophthalmic devices market share across care settings.

Geography Analysis

North America Ophthalmic Devices Market

North America accounted for 39.94% of 2025 revenue, driven by Medicare funding for advanced imaging and MIGS devices. However, saturation limits growth to mid-single digits, as cataract penetration surpasses 90% of eligible patients. Autonomous AI screening approvals and 18 ophthalmic device clearances in 2024 sustain innovation, but the adoption of refurbished equipment and bundled contracts exerts pricing pressure on OEMs. Canada’s single-payer model constrains capital budgets for premium OCT and femtosecond lasers, shifting upgrade demand to private clinics serving self-pay patients willing to fund rapid access to advanced procedures.

APAC Ophthalmic Devices Market

The Asia Pacific is the fastest-growing region, with a 7.12% CAGR through 2031, driven by China’s Healthy China 2030 annual examination mandate and India’s rollout of 1,200 vision screening centers, which together add millions of diagnostic encounters each year. Japan and South Korea perform more than 1.5 million cataract surgeries annually, maintaining a high consumable pull-through for premium IOLs despite moderating device ASPs. Domestic manufacturers such as MOPTIM and Suowei captured 20% of China’s phacoemulsification systems market in 2025 by offering units at USD 30,000, a 50% discount to Western brands, and exporting to Southeast Asia, thereby expanding the regional ophthalmic devices market size. Rising medical tourism in Thailand and Singapore further scales the volume of refractive surgery, bundling LASIK with hospitality packages that attract regional patients and bolster sales of femtosecond lasers.

EMEA and South America Ophthalmic Devices Market

Europe generated 25% of global revenue in 2025; however, EU MDR compliance delayed 30% of planned product launches, temporarily constricting replenishment cycles and increasing refurbishment demand. NHS cataract wait times exceeding 18 months prompted private-sector chains, such as Optegra, to charge GBP 2,500 (USD 3,200) per eye for expedited surgery, stimulating demand for premium lenses and reinforcing the ophthalmic devices market in the UK . The Middle East & Africa and South America remain underpenetrated, with a 5% CAGR, as public systems focus on basic cataract interventions. However, mobile eye clinics and tele-diagnostics are expanding their reach into rural areas, setting the stage for the future growth of portable devices priced under USD 10,000.

Regulatory Landscape

Ophthalmic devices face increasingly divergent regulatory pathways across major markets, especially for drug-device combinations used in retinal therapy and glaucoma. In the United States, FDA oversight for certain ophthalmic products packaged with dispensers is anchored in combination product requirements under 21 CFR Part 4, which raises quality-system and documentation expectations for manufacturers accustomed to device-only workflows. In the European Union, EU Regulation 2017/745 (MDR) interacts with the medicinal-products framework for integral drug-device combinations, with EMA noting that device components must meet relevant MDR General Safety and Performance Requirements and be CE marked when used with medicinal products.

Standards updates also continue to shape technical compliance and labeling for key ophthalmic categories. ISO 15004-1:2020 (general requirements for ophthalmic instruments) was confirmed in September 2025, reinforcing baseline safety and performance expectations for diagnostic and surgical instruments. For intraocular lenses, ISO 11979-4:2026 (labeling and information) was published in February 2026, tightening requirements around IOL information provided to clinicians and patients and increasing conformity work for premium IOL portfolios being expanded by large OEMs.

Value Chain Analysis

The ophthalmic devices value chain extends from specialty optical components and precision manufacturing through regulated assembly, sterilization, and multi-channel distribution into hospitals, ambulatory surgery centers, clinics, and optical retail. Upstream inputs include lenses, coatings, sensors, micro-mechanical components, and electronics used in connected OCT and fundus platforms, while midstream work centers on OEM design controls, verification and validation, and manufacturing of capital equipment (diagnostic and surgical platforms) alongside high-volume consumables (IOLs, contact lenses, and single-use surgical packs). Downstream, distributors and integrated OEM service organizations support installation, calibration, training, and recurring software and service contracts, reflecting the market shift toward bundled offerings that combine hardware, consumables, and analytics.

For drug-device combinations and delivery-related ophthalmology products, value creation depends on coordinated execution across pharma or biotech sponsors, specialized device manufacturers, and contract manufacturers with combination-product experience. Under the FDA policy posture for certain ophthalmic products under 21 CFR Part 4, the importance of cGMP-aligned packaging and primary container systems (including dispensers) increases, and integration burden grows across formulation, container-closure integrity, and device mechanics. Sterility assurance and in-transit integrity for prefilled systems and implantables act as practical bottlenecks, while regulatory documentation and testing requirements add time and cost that favor well-capitalized OEMs and partners able to handle dual-regime expectations across FDA and EU MDR/EMA workflows.

Competitive Landscape

The ophthalmic devices market concentration is moderate, with Alcon, Bausch + Lomb, Johnson & Johnson Vision, and Zeiss capturing approximately 45% of the 2025 revenue by bundling diagnostic platforms, surgical consumables, and analytics services into multi-year contracts that raise switching costs for hospitals and ASCs. These majors leverage extensive installed bases of phaco and OCT systems to lock customers into proprietary consumable ecosystems, stabilizing recurring revenue even as hardware ASPs deflate. Glaukos, STAAR Surgical, and Heidelberg Engineering exploit subspecialty niches—MIGS implants, implantable collamer lenses, ultra-widefield imaging—where targeted clinical superiority commands premium pricing and circumvents broad incumbent dominance.

Direct-to-consumer disruptors such as Warby Parker and Lenskart capture eyewear sales by integrating in-store autorefractors with remote prescription verification, seizing 12% of U.S. eyewear revenue by 2025 and pressuring traditional optical chains to digitize their dispensing workflows. Chinese OEMs EYEGOOD and Suowei underprice Western phaco systems by 50% while meeting NMPA standards, mirroring their playbook in orthopedics and cardiovascular devices and threatening global incumbents in price-sensitive markets. Cybersecurity and EU MDR compliance pose barriers that smaller firms struggle to overcome without partnerships or acquisitions, foreshadowing further consolidation as capital-intensive regulatory demands reshape the competitive dynamics in the ophthalmic devices market.

Ophthalmic Devices Industry Leaders

Alcon Inc.

Johnson & Johnson Vision Care

Lumibird Medical

Bausch + Lomb

ZEISS Group

- *Disclaimer: Major Players sorted in no particular order

Ophthalmic Devices Market Companies Covered in this Report

- Alcon

- Bausch + Lomb

- Canon

- The Cooper Companies

- Glaukos

- HAAG-Streit

- Heidelberg Engineering, Inc.

- HOYA

- Johnson & Johnson Vision Care

- Danaher

- Lumibird Medical

- Lumenis

- Nidek

- Oculus

- STAAR Surgical

- Topcon

- Visionix

- Volk Optical

- Carl Zeiss

- Ziemer Group

Market Opportunities and Future Outlook

Premium cataract and refractive workflows are creating whitespace for differentiated IOL designs, parameter expansion, and surgical-platform upgrades as care continues moving toward higher-throughput sites. In 2026, major OEM activity reinforced this direction, with Alcon launching the Clareon TruPlus monofocal and toric IOL line and introducing the UNITY Cataract System in Canada, and Johnson & Johnson expanding US commercial availability of the TECNIS PureSee IOL. Together, these moves support opportunities for suppliers that help enable faster ASC-compatible workflows, digital planning and postoperative management, and consumable pull-through tied to installed platforms.

Sustained-delivery retinal and glaucoma approaches are also driving investment and reimbursement experimentation in drug-device integrated platforms, where value sits across implants, delivery systems, and enabling diagnostics used for chronic-disease management. In May 2026, the AMA CPT Editorial Panel approved a new add-on Category III CPT code for SpyGlass Pharma's bimatoprost drug pad-IOL system, pointing to an active pathway for coding and evidence generation around implantable, long-acting therapies. Capital allocation continues to move toward long-acting ocular delivery, as Bayer signed a definitive agreement in May 2026 to acquire Perfuse Therapeutics for up to USD 2.45 billion, centered on an intravitreal implant program. In Japan, Chugai filed in March 2026 for the medical device component of its port delivery platform with ranibizumab, underscoring ongoing pipeline and regulatory momentum for combination products designed to reduce injection burden.

Recent Industry Developments in Ophthalmic Devices Market

- July 2026: Alcon entered into a non-exclusive collaboration agreement with RxSight to co-develop adjustable presbyopia-correcting intraocular lenses. The partnership combines Alcon's IOL capabilities with adjustable-lens technology, targeting premium cataract segments where postoperative customization supports differentiation and pricing.

- October 2025: MacuMira Medical Devices launched its first Health Canada-approved device for treating dry age-related macular degeneration. The company expanded availability across Canada, broadening access to a non-invasive modality and adding competitive pressure in vision preservation pathways beyond drug therapy.

- October 2024: ZEISS expanded its ophthalmic portfolio with an emphasis on digital AI tools and new surgical solutions designed to improve efficiency and outcomes. The update strengthened ZEISS positioning in integrated diagnostics and surgery workflows, supporting bundled selling into hospitals and high-volume eye-care networks.

Ophthalmic Devices Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers medical devices used to diagnose, monitor, treat, and correct eye and vision conditions across hospital, clinic, and ambulatory surgery settings. It includes ophthalmic diagnostic and monitoring equipment, surgical devices, and vision care products that are primarily sold for ophthalmic use.

Scope exclusions: standalone pharmaceuticals and software-only eye care tools that are not sold as part of a device offering are excluded.

Segments Covered in This Report

- By Device Type

- Diagnostic & Monitoring Devices

- OCT Scanners

- Fundus & Retinal Cameras

- Autorefractors & Keratometers

- Corneal Topography Systems

- Ultrasound Imaging Systems

- Perimeters & Tonometers

- Other Diagnostic & Monitoring Devices

- Surgical Devices

- Cataract Surgical Devices

- Vitreoretinal Surgical Devices

- Refractive Surgical Devices

- Glaucoma Surgical Devices

- Other Surgical Devices

- Vision Care Devices

- Spectacle Frames & Lenses

- Contact Lenses

- Diagnostic & Monitoring Devices

- By Disease Indication

- Cataract

- Glaucoma

- Diabetic Retinopathy

- Other Disease Indications

- By End-User

- Hospitals

- Specialty Ophthalmic Clinics

- Ambulatory Surgery Centers (ASCs)

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean view of demand and supply signals that are visible in public data, then mapping them to the device scope used in this report. We leaned on sources such as the World Health Organization for eye health burden signals, the US CDC for vision and diabetes related indicators, and public US FDA pages for device clearances and safety actions that can affect shipment timing.

Next, we used trade and macro series to sanity check direction and scale, including UN Comtrade for relevant trade movement patterns, plus World Bank and OECD health spending indicators, and peer-reviewed ophthalmology journals to understand procedure adoption and device utilization changes over time. Company filings, investor presentations, and reputable press were used to cross-check product mix shifts and regional exposure. A paid subscription for company financials and another for patent databases were used selectively to fill gaps around revenue splits and innovation cadence. These examples are not exhaustive, and other public sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what actually drives revenues in ophthalmic devices, since published procedure volumes and device mix do not always move together. We spoke with a mix of device-side and care-side experts, including product managers, distribution leaders, procurement stakeholders, and ophthalmologists, with coverage across APAC, EMEA, and the Americas to check regional pricing, utilization, and channel structure differences.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 53% |

| Mid tier: 52% | Functional/Unit leaders: 41% | EMEA: 29% |

| Smaller Players: 14% | Managers: 45% | Americas: 18% |

Market-Sizing & Forecasting

Market sizing was built using a mix of top-down and bottom-up checks, so totals stay tied to real care activity without assuming every revenue line is fully visible. In the top-down build, procedure and patient pools were reconstructed by region using eye disease prevalence signals and treatment penetration, then translated into device demand using utilization rates for diagnostic tests and surgical procedures.

To keep the model grounded, several practical inputs were tracked, including cataract and glaucoma procedure trends, OCT and tonometry test utilization, ambulatory surgery center share shifts, replacement cycles for capital equipment, and average selling price movement by device class and region. Those assumptions were then corroborated with selective bottom-up approximations, including sampled ASP times estimated unit volumes and supplier and channel checks on product mix, which helps reveal where public data may overstate or understate consumption.

For forecasting, we primarily used scenario analysis with a light multivariate structure. Volume drivers like procedure growth, aging population signals, and access expansion were adjusted alongside price drivers such as mix shift toward premium IOLs and adoption of minimally invasive techniques, using interview inputs to guide the magnitude. When bottom-up visibility was weak in smaller regions or niche device lines, we handled gaps through proxy indicators like installed base and replacement timing, followed by a consistency check against regional healthcare spending direction.

Data Validation & Update Cycle

Validation is done through stepwise triangulation, where model outputs are checked against independent signals such as procedure trends, device regulatory activity, and trade movement direction, and then reviewed for outliers. If a region or device class shows an unusual jump, we revisit the driver assumptions, re-check inputs, and re-contact select experts to confirm whether the change is real or a data timing issue.

Before sign-off, the dataset and logic are reviewed by another analyst to catch variance issues and ensure the steps are repeatable. The report is refreshed annually, and interim updates are made when material events affect pricing, utilization, or supply availability. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Opthalmic Devices Market Size Versus Other Published Estimates

Published market sizes for ophthalmic devices can look far apart even when they describe a similar space, because the category boundaries and the value build are not always consistent. Differences usually come from what is counted as vision care, how capital equipment and consumables are treated, and whether price and volume are normalized to the same year and currency timing.

By tracking device-type level splits and refreshing price and utilization assumptions using primary checks, Mordor Intelligence keeps the total tied to diagnostic, surgical, and vision care demand rather than mixing in adjacent eye health categories or one-time timing effects. Gaps also show up when some estimates focus on a narrower definition like equipment-only, or when a base year is set earlier and inflation or mix shift is applied using a single blanket factor across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 53.66 B (2026) | |

| Industry Analytics Group A | USD 31.90 B (2024) | Uses an earlier base year and a different scope mix, where lens and equipment boundaries are grouped differently, which can compress the total when vision care is treated more narrowly. |

| Global Business Publisher B | USD 31.45 B (2025) | Leans on broader product buckets such as implants, consumables, and equipment, and the value build can shift based on how capital equipment is annualized and how regional price levels are normalized. |

The spread in the table is mainly explained by scope choices and how price and utilization are aligned to the stated year. When the device boundary is kept consistent across diagnostic, surgical, and vision care, and assumptions are checked against real procedure and test activity, the resulting market size becomes easier to trace and repeat year to year.

Key Questions Answered in the Report

What is the projected value of the ophthalmic devices market by 2031?

The market is forecast to reach USD 73.62 billion by 2031, expanding at a 6.53% CAGR.

Which device category is growing fastest in ophthalmology?

Diagnostic & Monitoring devices are advancing at 8.65% CAGR as AI imaging and point-of-care OCT gain traction.

Why are ambulatory surgery centers gaining share in eye-care procedures?

Payers favor ASCs because same-day cataract and MIGS cases cut facility fees by up to 40% compared to hospital settings.

How is AI influencing diabetic retinopathy screening?

FDA-cleared autonomous AI systems halve per-scan costs and raise detection rates 40%, integrating screening into routine primary-care visits.

What are the key restraints on advanced ophthalmic equipment uptake?

High capital costs, divergent global regulations, and cybersecurity requirements slow adoption, especially in emerging and rural markets.

Page last updated on: