Smart Contact Lenses Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

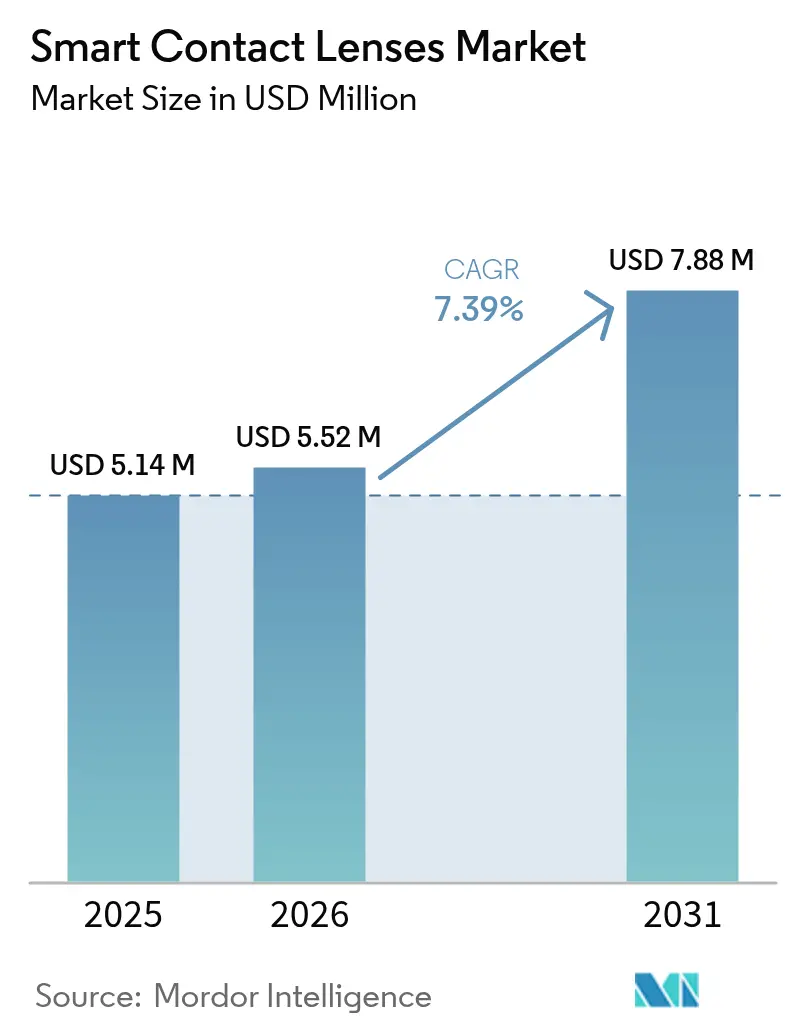

| Market Size (2026) | USD 5.52 Million |

| Market Size (2031) | USD 7.88 Million |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

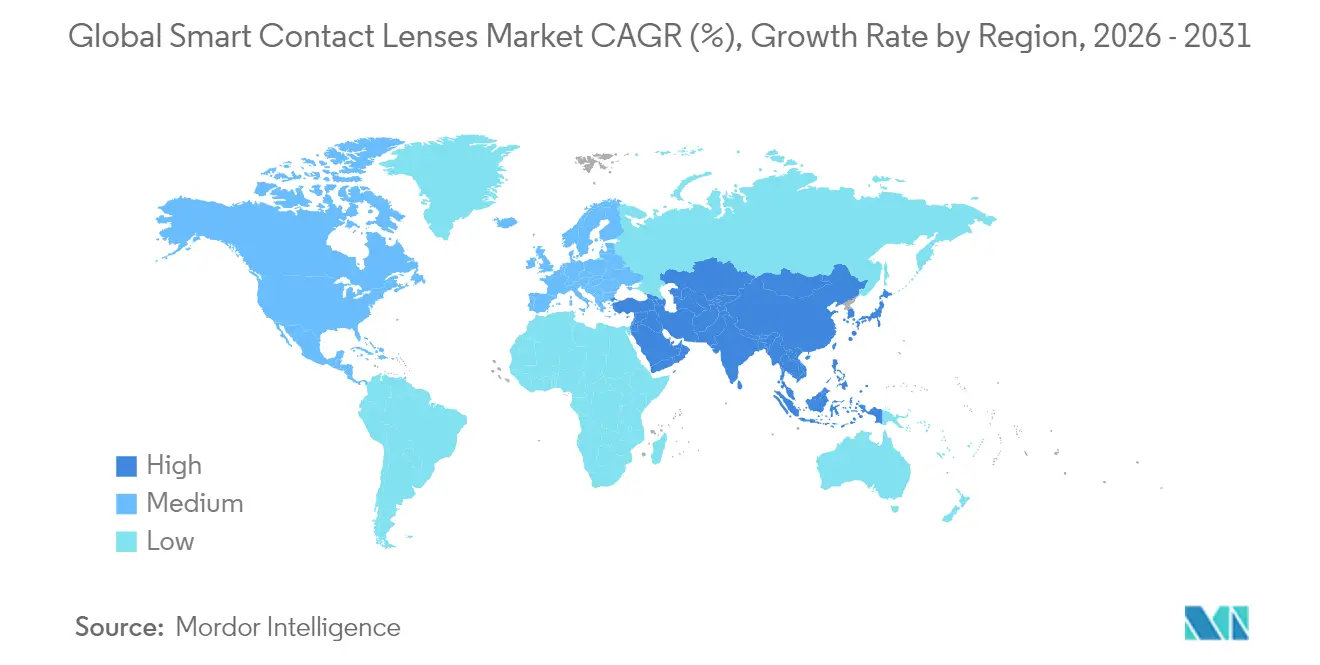

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

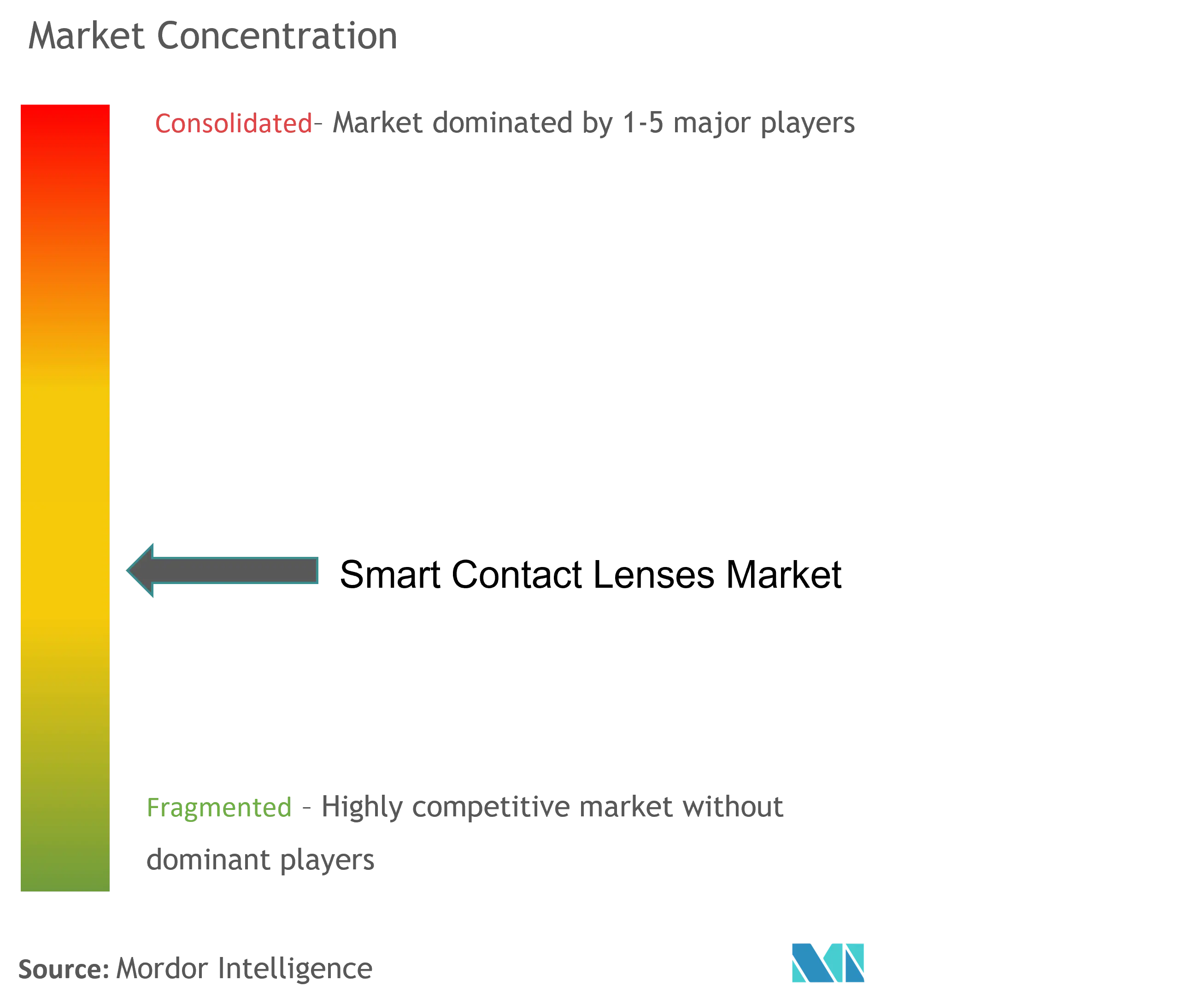

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Smart Contact Lenses Market Analysis by Mordor Intelligence

The smart contact lenses market size is expected to grow from USD 5.14 million in 2025 to USD 5.52 million in 2026 and is forecast to reach USD 7.88 million by 2031 at 7.39% CAGR over 2026-2031. This upswing is linked to maturing sub-µW biosensors that support continuous tear-based glucose and intraocular pressure (IOP) monitoring, an emerging set of reimbursement codes in major healthcare systems, and growing preference for non-invasive, real-time diagnostics over episodic clinic visits. Silicon-hydrogel nanocomposites have lowered manufacturing rejects, supporting economies of scale, and 5G/LTE-M connectivity enables secure data transmission to electronic health record systems. Early FDA clearances for drug-eluting lenses signal regulatory momentum, while Asia-Pacific’s technology ecosystems accelerate product iteration and cost reduction. These forces collectively underpin double-digit expansion of the smart contact lenses market despite current price premiums.

Key Report Takeaways

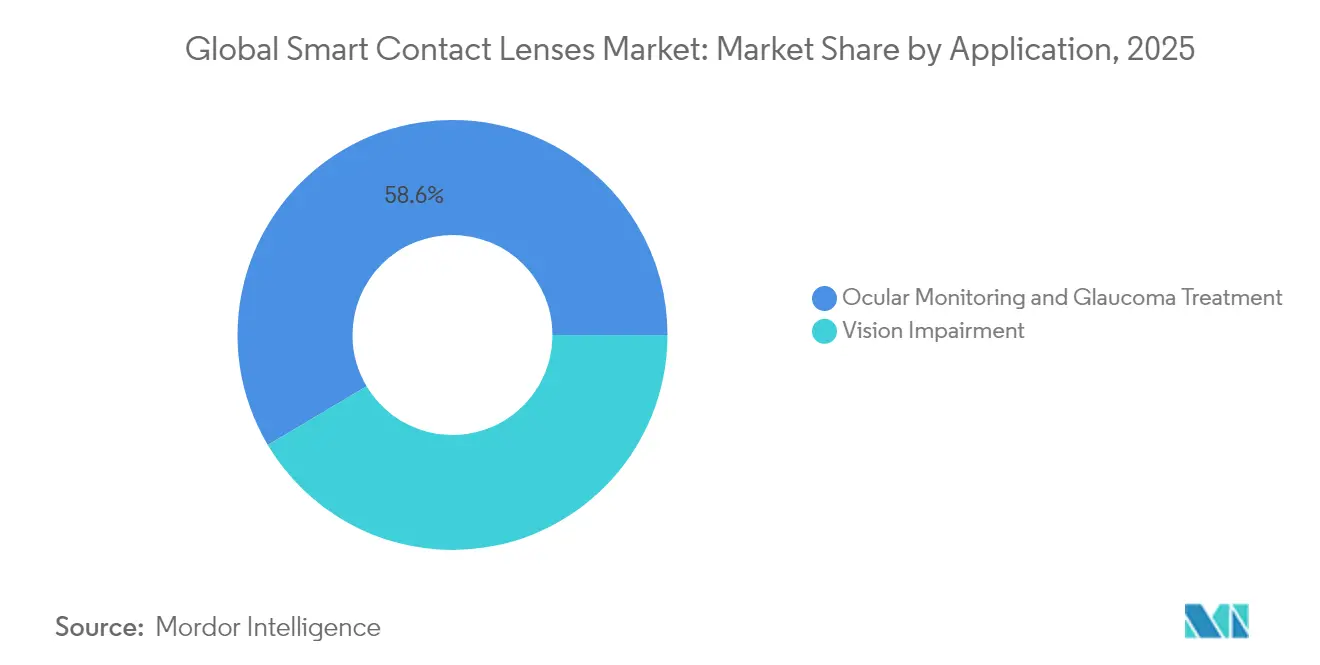

- By application, Ocular monitoring and glucose treatment lenses accounted for 58.55% revenue share in 2025, whereas drug-delivery lenses are projected to grow at 7.72% CAGR through 2031.

- By end user, hospitals and ophthalmology clinics captured 45.96% of the smart contact lenses market size in 2025, while the home-care segment is pacing a 7.93% CAGR to 2031.

- By geography, North America led with 58.54% market share in 2025; Asia-Pacific is the fastest-growing region at 8.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Contact Lenses Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturised on-lens biosensors reach sub-µW power levels | +2.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Reimbursement codes emerging for IOP & glucose tear monitoring | +2.1% | North America & EU primarily, expanding to APAC | Short term (≤ 2 years) |

| 5G / LTE-M eSIM modules enable continuous lens connectivity | +1.9% | Global, led by APAC infrastructure rollouts | Medium term (2-4 years) |

| Silicon-hydrogel nanocomposites slash manufacturing rejects | +1.4% | Global manufacturing hubs | Short term (≤ 2 years) |

| Pharma-device bundle deals for ocular drug-delivery lenses | +1.2% | North America & EU regulatory environments | Long term (≥ 4 years) |

| Big-Tech licensing of AR micro-display IP to lens makers | +1.6% | Global, concentrated in tech innovation centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Miniaturised On-Lens Biosensors Reach Sub-µW Power Levels

Sub-µW biosensors now harvest ~150 µW at 3.3 V from combined flexible solar and metal-air sources, allowing autonomous operation without bulky battery packs. Ti₃C₂Tx MXene sensors demonstrate 12.52 mV/mmHg sensitivity for IOP, validating high-accuracy ocular measurements with minimal irritation. This leap enables a shift from research prototypes to commercial devices capable of continuous glucose monitoring, a use-case that commands the largest share of the smart contact lenses market. Lower power budgets also simplify thermal management, preserving corneal comfort during extended wear. Collectively, these advances convert a core technical bottleneck into a launchpad for multi-sensor product roadmaps.

Reimbursement Codes Emerging for IOP & Glucose Tear Monitoring

In 2025, Medicare issued a category III CPT code for continuous tear glucose monitoring, greatly improving provider economics in the United States. Earlier, FDA cleared Acuvue Theravision with Ketotifen, illustrating a feasible path for ophthalmic combination devices. Payer recognition lowers out-of-pocket costs for chronic-disease patients, aligning incentives for wider prescription. EU payers are piloting similar codes under digital therapeutics frameworks, and Japan’s universal coverage system is reviewing inclusion criteria. Reimbursement momentum accelerates volume adoption, particularly in diabetes care where continuous monitoring curbs long-term complications and associated costs.

5G/LTE-M eSIM Modules Enable Continuous Lens Connectivity

Embedding eSIMs compliant with LTE-M Release 14 allows secure over-the-air provisioning, eliminating manual SIM swaps that are impractical in ophthalmic devices. Field tests show 4.5 Mbps throughput over resonant magneto-quasistatic channels with negligible path-loss variance at typical eye-to-hand distances. As carriers densify low-power IoT networks, lenses can transmit real-time data to cloud dashboards and trigger clinician alerts. The same link also supports AR overlays, broadening the addressable use-cases beyond medical monitoring to wellness and infotainment, which together underpin expansion of the smart contact lenses market.

Silicon-Hydrogel Nanocomposites Slash Manufacturing Rejects

Dual-cure 3D printing coupled with in-mold reactive bonding trims reject rates by 38%, according to a 2024 multi-site manufacturing study. Mel4 peptide coatings reduce P. aeruginosa colonization by 99% after seven-day soak tests, addressing infection risk when electronics are embedded.. These material innovations decrease unit costs and enhance safety, supporting volume ramps. Improved yields also foster design experimentation, accelerating time-to-market for advanced functions such as drug-reservoir layers or micro-LED arrays.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-term biocompatibility of stretchable antennas uncertain | -1.8% | Global regulatory scrutiny | Long term (≥ 4 years) |

| High BOM keeps ASP > USD 300 per lens in 2025 | -2.3% | Global cost pressures | Medium term (2-4 years) |

| Fragmented global approval pathways (FDA, MDR, MFDS, NMPA) | -1.5% | Global, varying by jurisdiction | Medium term (2-4 years) |

| Supply of medical-grade micro-LEDs <5 µm remains constrained | -1.9% | Global manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Long-Term Biocompatibility of Stretchable Antennas Uncertain

Current ISO 10993 ocular protocols do not fully address nano-scale metal dissolution from serpentine silver-graphene traces used as antennas. Early 26-week rabbit trials revealed trace silver ion accumulation in retro-bulbar tissues, prompting the FDA to request multi-year follow-ups before approving continuous-wear indications. Manufacturers now explore biodegradable poly-L-lactic acid substrates and parylene-encapsulated interposers to curb leaching risks. Until long-term safety data matures, market penetration in chronic-use segments such as glaucoma and diabetes remains gated, restraining CAGR.

High BOM Keeps Low ASP per Lens in 2025

A single micro-LED display stack contains ~2 million chips at < 5 µm pitch, demanding ±1 µm placement accuracy under 10 minutes to maintain cost targets. Yield shortfalls in mass-transfer bump bonding still exceed 4%, adding USD 55 to unit cost. Medical-grade micro-batteries, hermetic encapsulation, and eSIM modules further inflate bills of materials. These economics confine early adoption to affluent health systems and premium consumer segments, delaying the scale advantages that would compress the smart contact lenses market size in developing regions. Supplier roadmaps promise 40% cost erosion by 2028, but interim price points remain a headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Glucose Monitoring Leads, Drug Delivery Accelerates

Glucose-monitoring devices accounted for 58.55% of 2025 revenues, capitalizing on a diabetic population exceeding 540 million worldwide and the demonstrated clinical correlation between tear and blood glucose (R² > 0.87 in recent human trials). Continuous glucose trackers reduce hypoglycemic events by 28% compared with finger-stick monitoring in a 180-day multi-center study, justifying payer coverage. Intraocular pressure monitoring serves 80 million glaucoma patients, enabling detection of nocturnal IOP spikes missed in clinic. Augmented reality overlays remain pre-commercial but fuel long-term upside as micro-LED efficiency improves.

Drug-delivery lenses, the fastest-growing application at 7.72% CAGR, employ vitamin E barriers or micro-reservoirs to sustain therapeutic dosing over days, addressing chronic adherence gaps in conditions like allergic conjunctivitis. FDA clearance of ketotifen-eluting lenses validates the regulatory pathway and spurs pipelines for prostaglandin analogs. The multi-functional lens archetype—diagnostic plus therapeutic—promises platform differentiation, reinforcing expansion of the smart contact lenses market.

By End User: Home-Care Segment Transforms Market Dynamics

Hospitals and ophthalmology clinics retained 45.96% of smart contact lenses market size in 2025, anchoring early adoption via clinician-supervised fitting and data interpretation. These settings generate real-world evidence vital for reimbursement. Yet, app-enabled remote monitoring propels the home-care segment to a 7.93% CAGR through 2031. Bluetooth Low Energy relays tear glucose or IOP readings to smartphone dashboards, empowering self-management. Payers endorse at-home models that cut clinic visits and associated costs.

Enterprise wellness programs in North America and corporate health insurers in Japan subsidize smart lenses for high-risk diabetic employees, accelerating workplace uptake. Pharmacies leveraging tele-optometry kiosks expand access in suburban and rural areas. As form factors converge with daily-wear soft lenses, the locus of care shifts decisively toward the consumer, catalyzing deeper penetration of the smart contact lenses market.

Geography Analysis

North America maintained 58.54% smart contact lenses market share in 2025, underpinned by FDA clearances and robust reimbursement that cushion USD 300+ price points. The United States hosts production hubs for micro-LEDs and biosensors, anchoring supply chains and sparking university-industry consortia for ocular bioelectronics. Canada’s single-payer system began pilot tear-glucose programs in 2025, broadening public coverage. Mexico leverages maquiladora incentives to attract lens assembly lines, compressing regional logistics cycles. Together, these dynamics preserve North America’s leadership despite high labor costs.

Asia-Pacific delivers the fastest CAGR at 8.19%, buoyed by South Korea’s expedited MFDS fast-track designations, Japan’s AMED grants for bio-sensorization, and China’s volume-driven component ecosystem. In China, a diabetic base of 141 million boosts demand for glucose lenses, while domestic display makers channel Mini-LED expertise into lens projects. India’s Ayushman Bharat scheme begins covering remote IOP monitoring, activating rural demand. This confluence positions Asia-Pacific as the growth engine of the smart contact lenses market.

Europe records steady uptake as MDR clarity improves. Germany’s DIGA framework now reimburses digital ophthalmic therapeutics, and France’s Haute Autorité de Santé released 2025 guidelines for continuous ocular monitoring. United Kingdom spin-outs from University of Manchester advance graphene antennas compliant with NHS Cybersecurity Toolkit standards. Southern Europe and the Nordics pursue EU Structural Funds to equip regional hospitals with smart lens diagnostics. While CE-marking timelines extend launch cycles, Europe’s emphasis on safety and data privacy cultivates user trust, reinforcing gradual but resilient adoption.

Competitive Landscape

The competitive field blends heritage contact-lens manufacturers with semiconductor and digital health entrants, yielding moderate fragmentation. Companies leverage ISO-certified plants and established optometrist channels to introduce sensor-ready silicone-hydrogel lines. Sony Corporation contribute micro-LED and ASIC IP, licensing display engines to optical majors. Samsung Electronics’ LEDoS roadmap targets 3,500 ppi resolution at < 2 mW, enticing OEM partners seeking AR integrations[2]Source: Samsung Electronics, “Advanced Micro-Displays for AR,” samsung.com .

Patent activity exceeds 1,400 filings since 2023, with Smartlens holding 40 grants focused on anterior-segment diagnostics. Supply-side barriers persist around micro-LED mass transfer and medical-grade encapsulation, favoring incumbents with capex muscle. Nonetheless, nimble start-ups exploit open-innovation grants in Asia-Pacific to pilot novel drug-reservoir designs, occasionally outpacing corporate decision cycles.

Smart Contact Lenses Industry Leaders

-

Innovega Inc.

-

SEED Co., Ltd. (Sensimed SA)

-

Smartlens, Inc.

-

Azalea Vision

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Samsung Electronics announced LEDoS micro-display production plans for 2027, targeting smart lenses and AR glasses

- May 2025: Warby Parker partnered with Google on AI-powered eyewear, with USD 150 million committed to R&D.

- March 2025: XPANCEO unveiled prototype smart lenses offering night vision and gaze-controlled zoom at Mobile World Congress 2025.

Global Smart Contact Lenses Market Report Scope

As per the scope of the report, a smart contact lens consists of non-see-through components onto a lens that is in direct contact with the eye. Smart contact lenses diagnose diabetes and glaucoma by measuring the glucose level in tears and monitoring intraocular pressure within the eyes. Smart contact lenses can be used as medical devices, health trackers, and audio and video recorders. The Smart Contact Lenses market is Segmented by Type (Rigid Gas-Permeable, Daily-wear Soft Lenses, Extended-Wear Lenses, and Others), Application (Continuous Glucose Monitoring and Intraocular Pressure Monitoring), End User (Hospitals, Ophthalmology Clinics, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments. The report offers the value (USD million) for the above segments.

| Ocular Monitoring & Glaucoma Treatment |

| Vision Impairment |

| Hospitals & Ophthalmology Clinics |

| Home-care / Self-monitoring Consumers |

| Others (Academic Institutes, Rehabilitation Centers, among others) |

| North America |

| Europe |

| Asia-Pacific |

| Rest of the World |

| By Application | Ocular Monitoring & Glaucoma Treatment |

| Vision Impairment | |

| By End User | Hospitals & Ophthalmology Clinics |

| Home-care / Self-monitoring Consumers | |

| Others (Academic Institutes, Rehabilitation Centers, among others) | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of the World |

Key Questions Answered in the Report

What is the current Global Smart Contact Lenses Market size?

The Global Smart Contact Lenses Market is projected to register a CAGR of 7.39% during the forecast period (2026-2031)

What is the current smart contact lenses market size?

The smart contact lenses market size stands at USD 5.52 million for 2026 and is projected to reach USD 7.88 million by 2031 at a 7.39% CAGR.

Which material leads the market?

Silicon-hydrogel lenses dominate with 67.58% market share in 2025, offering superior oxygen permeability and electronics compatibility.

Which application segment is expanding fastest?

Drug-delivery lenses are growing at 7.72% CAGR through 2031, driven by FDA-cleared ketotifen-eluting designs.

Why is Asia-Pacific the fastest-growing region?

Rapid 5G roll-outs, government funding for digital health, and large diabetic populations fuel a 8.19% CAGR in Asia-Pacific.

Page last updated on: