Rapid Prototyping Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

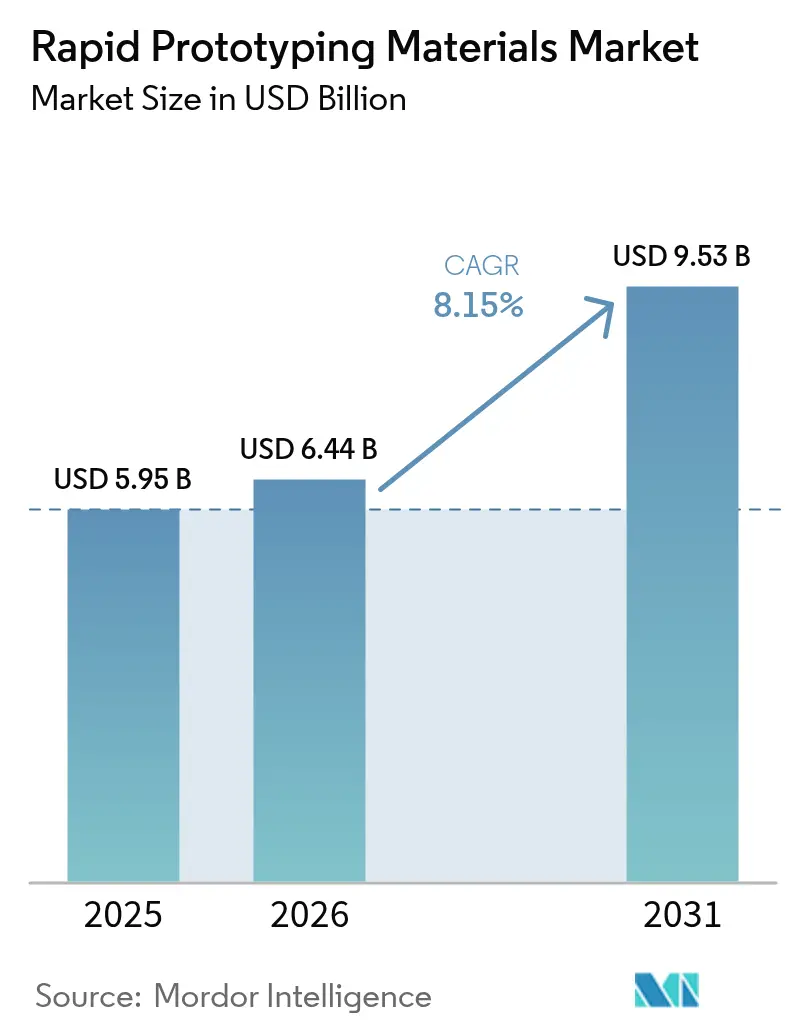

| Market Size (2026) | USD 6.44 Billion |

| Market Size (2031) | USD 9.53 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

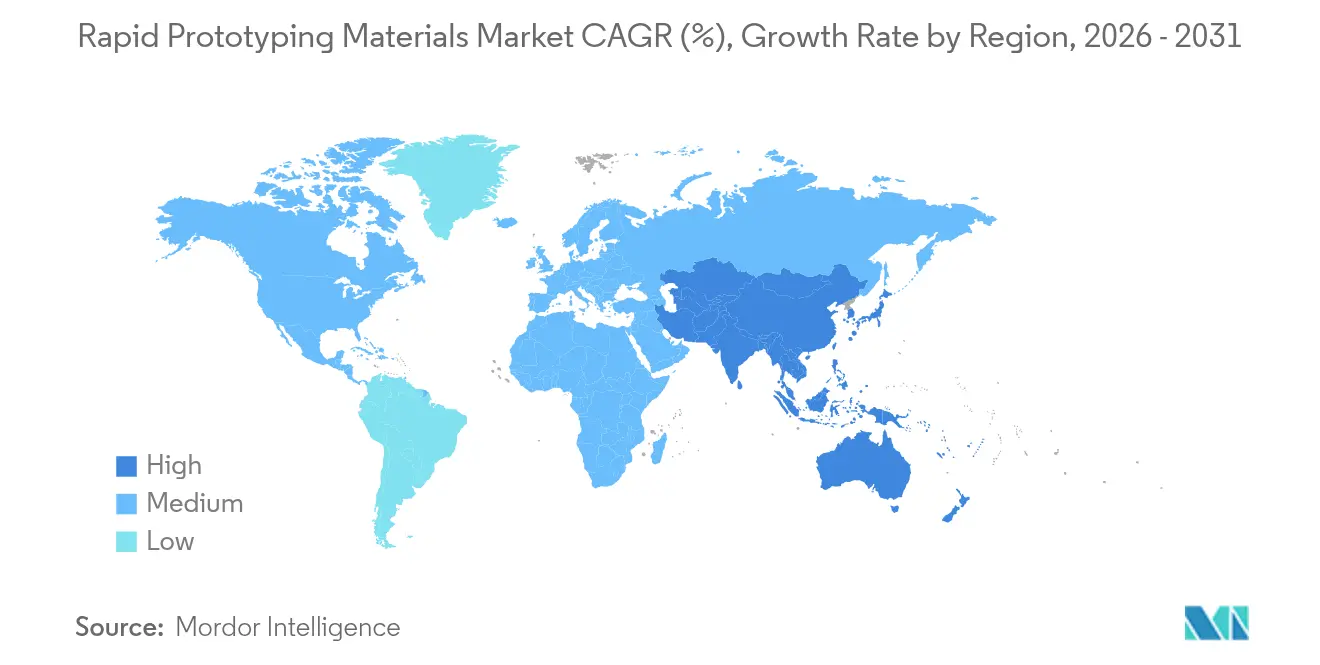

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rapid Prototyping Materials Market Analysis by Mordor Intelligence

The Rapid Prototyping Materials market size is expected to grow from USD 5.95 billion in 2025 to USD 6.44 billion in 2026 and is forecast to reach USD 9.53 billion by 2031 at 8.15% CAGR over 2026-2031. This momentum is propelled by the steady shift from subtractive to additive workflows, allowing manufacturers to shorten design-to-launch cycles, minimize material waste, and customize parts at scale. Sustainability regulations are simultaneously driving demand for bio-based polymers; more than 60 BASF products now carry ISCC+ certification. Metals and alloys are gaining traction in aerospace, where ceramic-matrix‐composite-reinforced parts withstand temperatures up to 1,300 °C and slash component weight. Regionally, North America leverages strong aerospace and defense budgets to command headline share, while Asia Pacific accelerates through China’s rapidly scaling additive manufacturing ecosystem.

Key Report Takeaways

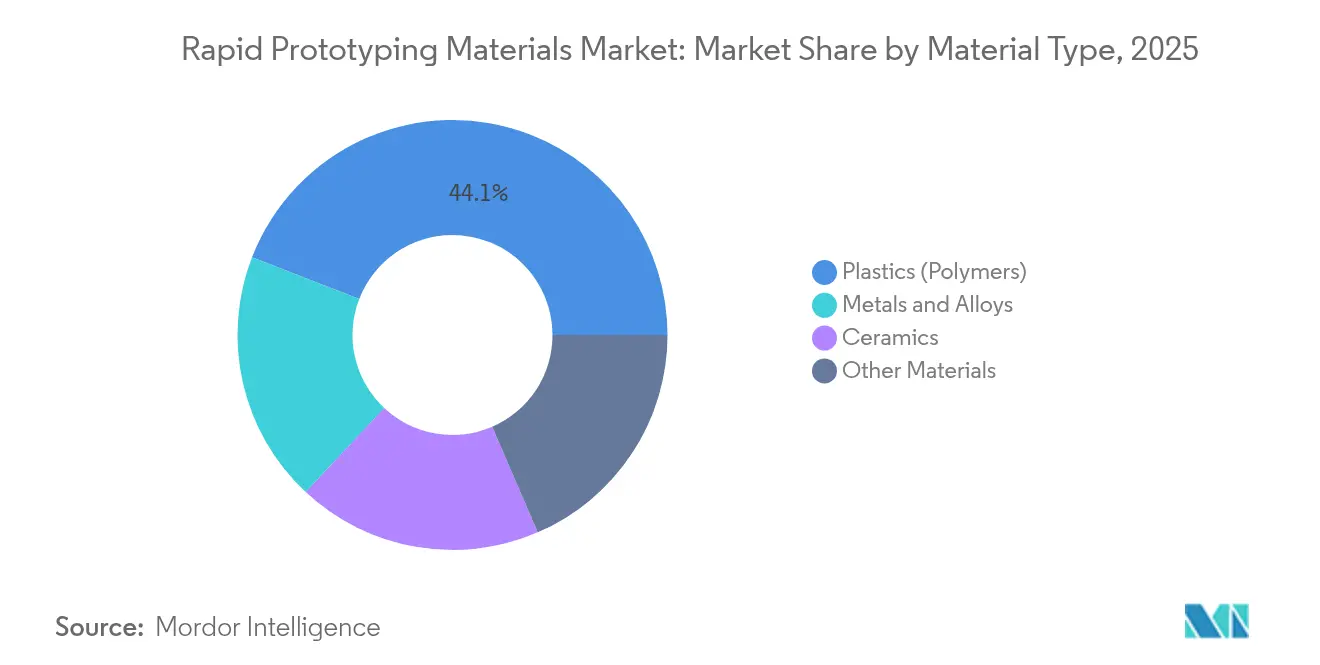

- By material type, plastics held 44.12% of the rapid prototyping materials market share in 2025, whereas metals and alloys are projected to post the fastest 10.03% CAGR through 2031.

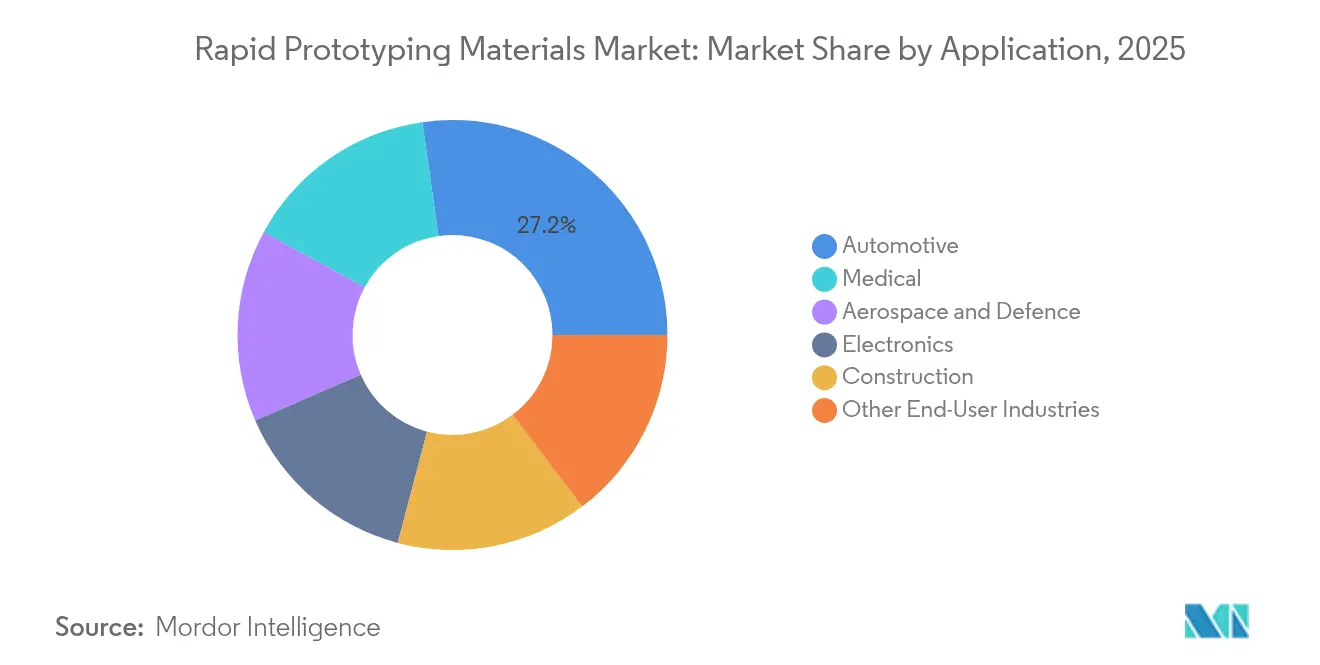

- By end-user industry, the automotive sector accounted for 27.24% revenue share in 2025, while medical applications are advancing at the highest 10.55% CAGR to 2031.

- By geography, North America led with 31.21% of the rapid prototyping materials market in 2025; Asia Pacific is forecast to grow at a 10.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rapid Prototyping Materials Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding adoption of additive manufacturing in aerospace and defense prototyping | +2.1% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Surge in medical implants and anatomical models needing biocompatible materials | +1.8% | Global; early gains in North America, Europe, Japan | Short term (≤ 2 years) |

| Continued decline in polymer and metal powder prices | +1.4% | Global | Short term (≤ 2 years) |

| OEM push for lightweight automotive parts | +1.2% | APAC core; spill-over to North America and Europe | Medium term (2-4 years) |

| Government-funded circular-economy mandates favoring bio-based polymers | +0.9% | Europe and North America; expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Adoption of Additive Manufacturing in Aerospace and Defense Prototyping

The aerospace and defense community is accelerating additive uptake to compress design iterations and unlock complex internal geometries. The U.S. Defense Advanced Research Projects Agency (DARPA) initiated its AMME program to localize production of intricate micro-electronic systems and safeguard supply sovereignty. GE’s single-piece 3D-printed LEAP fuel nozzle demonstrated 25% weight reduction and a fivefold durability improvement compared with legacy builds. Ceramic-matrix-composite components able to tolerate 1,300 °C are now integrated in turbine pathways, contributing to higher thermal efficiency and lower emissions. Boeing and Airbus have each expanded in-house printing farms to accommodate flight-certified polymer and metal parts, recognizing that every kilogram shed translates directly into airline operating-cost savings.

Surge in Medical Implants and Anatomical Models Needing Biocompatible Materials

Healthcare facilities are moving toward point-of-care printing of patient-specific devices. In 2025, 3D Systems produced the first MDR-compliant PEEK facial implant directly inside a hospital setting. The solution removes lengthy external machining queues and lets surgeons adjust designs minutes before surgery. Alternative alloys such as tantalum and niobium are being trialed to solve titanium rejection in certain patient sub-groups. Updated FDA guidelines clarify validation routes for additive devices, enabling shorter approval cycles. Evonik has commercialized carbon-fiber-reinforced PEEK filaments promising enhanced load-bearing performance in spinal cages. These developments, alongside progress in scaffold-based tissue engineering, underpin the rapid ascent of personalized medical solutions within the rapid prototyping materials market.

Continued Decline in Polymer and Metal Powder Prices

Falling raw-material prices are democratizing access to additive workflows for small and mid-sized enterprises. Wider recycling of aluminum and steel powders improves throughput and visibility, counterbalancing headline metal price inflation signaled by the World Bank through 2025[1]“World Bank Commodity Outlook 2025,” worldbank.org. Alternative feedstock formats, notably metal wire and injection-molding pellets, deliver 15% to 40% part-cost savings while maintaining printability. Circular-economy pioneers such as Continuum supply recycled superalloys compatible with Desktop Metal binder-jet systems, lowering material costs while meeting aerospace pedigree requirements

OEM Push for Lightweight Automotive Parts

Regulators are extending emissions rules to non-exhaust sources such as brake discs, forcing automakers to re-evaluate every gram in the vehicle chassis. ArcelorMittal’s additive-dedicated steel powders permit lattice‐reinforced brake calipers that outperform cast iron on thermal conductivity while trimming mass. Researchers at the University of Glasgow combined polypropylene and polyethylene matrices with carbon nanotubes to create metamaterials displaying high impact absorption yet low density.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of titanium and high-performance polymer feedstock prices | -1.6% | Global; acute in North America and Europe | Short term (≤ 2 years) |

| Skills gap for large-scale additive manufacturing design and material processing | -1.2% | Global; pronounced in emerging markets | Medium term (2-4 years) |

| Supply bottlenecks of rare-earth alloying elements for advanced metal powders | -0.8% | Global; critical to aerospace and defense | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility of Titanium and High-Performance Polymer Feedstock Prices

Titanium mill prices climbed 4.48% year-over-year to a U.S. PPI of 219.99 in December 2024, straining aerospace procurement budgets[2]“PPI Titanium Mill Shapes December 2024,” bls.gov. Geopolitical risk, amplified by Russia-Ukraine tensions, constrains sponge supply, while new entrants in the Middle East and North America require multi-year scale-up periods. Manufacturers either stockpile or accept lower margins because qualification cycles for flight- or implant-grade resins preclude rapid material substitution. Volatility thus acts as a drag on capital allocation to greenfield additive lines.

Skills Gap for Large-Scale Additive Manufacturing Design and Material Processing

The additive boom outpaces workforce upskilling. SME documented an 80% rise in metal-printer shipments over 24 months but flagged stagnant operator certification volumes. MIT and Penn State now run full-semester curricula on topology optimization and powder handling, yet graduate output still trails hiring demand. ASTM and EOS co-launched machine-operator certification, but the rapid evolution toward multi-material hybrids forces a continuous learning loop that many firms struggle to maintain. The capability gap hits emerging markets hardest, compelling firms to import expertise and raising project costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polymers Dominate Despite Metal Innovation

Plastics retained 44.12% of the rapid prototyping materials market share in 2025, confirming their versatility and cost advantage over metals. High-temperature grades such as Victrex’s PAEK, engineered for lower refresh rates in powder-bed systems, extend polymer use into under-hood automotive and aerospace ducting applications. Metals and alloys are expanding faster, clocking a 10.03% CAGR as aerospace primes demand fatigue-resistant titanium aluminide and cobalt-chrome implants populate orthopedics.

A parallel trend centers on process innovation. Foundation Alloy’s solid-state metallurgy bypasses melt-pool instabilities and can deliver alloys twice as strong as wrought counterparts while cutting development cycles to months. Such breakthroughs will help metals narrow the cost gap with polymers by reducing post-processing. Polymers, however, are likely to retain the lion’s share because of continual upgrades in UV-curable resins and elastomers. Overall, material diversification enlarges the total rapid prototyping materials market and hedges against feedstock price shocks.

By End-User Industry: Automotive Leads While Medical Accelerates

Automotive OEMs accounted for 27.24% share of the rapid prototyping materials market in 2025, using lattice-filled brackets and air-flow-optimized ducts to shave vehicle mass while meeting Euro 7 particulate caps. ArcelorMittal’s steel-powder family allows thin-wall structures that dissipate braking heat without extra machining steps, scaling additive parts into mid-volume production.

Medical applications, growing at 10.55% annually, are set to eclipse aerospace incremental demand after 2027. More than 80 cranial reconstructions have been conducted using 3D Systems’ EXT 220 MED printer, illustrating clinical confidence. Construction represents an emergent outlet: graphene-infused concrete mixes provide 31% lower embodied carbon while boosting compressive strength, mirroring wider decarbonization imperatives.

Geography Analysis

North America held 31.21% of the rapid prototyping materials market in 2025 on the back of robust aerospace and medical infrastructure. DARPA’s cumulative USD 35 billion investment in advanced manufacturing, plus FDA fast-track pathways for additive devices, incentivize commercial scale-up.

Asia Pacific is the fastest grower, clocking a 10.31% CAGR through 2031. India’s iterative prototyping culture within large teaching hospitals drives localized demand for biocompatible polymers. Japan applies additive solutions to miniaturized consumer electronics, while South Korea’s automakers seek lattice-reinforced seat frames.

Europe maintains a competitive position anchored in sustainability-first policy. The EU Raw Materials Foresight Study prioritizes additive manufacturing for strategic autonomy through 2050. Germany’s EOS and SGL Carbon pioneer high-temperature resin and ceramic portfolios; the UK channels aerospace research and development into powder-bed fusion of scalmalloy flight parts.

Competitive Landscape

The rapid prototyping materials market is consolidated in nature. Chemical powerhouses BASF, Evonik, and Arkema exploit global logistics and deep polymer chemistries to serve cross-industry demand. Meanwhile, 3D Systems, Stratasys and EOS emphasize printer-material co-optimization. Future rivalry will pivot on multi-material deposition and integrated post-processing. Players integrating in-situ inspection and AI-guided parameter tuning stand to capture higher margins as customers favor turnkey solutions over standalone powders or printers. Intellectual-property depth around alloy chemistry and material databases will further dictate competitive staying power within the rapid prototyping materials market.

Rapid Prototyping Materials Industry Leaders

Arkema

BASF

3D Systems Inc.

EOS GmbH

Stratasys Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Evonik Industries AG launched INFINAM FR 4100L, a flame-retardant, mechanically durable photopolymer for DLP printers.

- May 2023: Model Solution and PROTOTECH signed an MoU to expand rapid prototyping services and develop high-value 3D-printed parts

Global Rapid Prototyping Materials Market Report Scope

Rapid prototyping enables manufacturers to quickly develop and test products, making adjustments and resolving issues as needed. A prototype model serves as a detailed construction guide, allowing for more accurate planning and scheduling of the actual structure. The rapid prototyping market is segmented by materialtype, end-user industry, and geography. By mateiral type, the market is segmented into ceramics, metals and alloys, plastics, and other material types. By end-user industry, the market is segmented into automotive, aerospace and defense, construction, medical, electronics, and other end-user industries. The report also covers the market size and forecasts for the Rapid Prototyping Market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD Million).

| Plastics (Polymers) |

| Metals and Alloys |

| Ceramics |

| Other Materials |

| Automotive |

| Aerospace and Defence |

| Medical |

| Electronics |

| Construction |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Plastics (Polymers) | |

| Metals and Alloys | ||

| Ceramics | ||

| Other Materials | ||

| By End-User Industry | Automotive | |

| Aerospace and Defence | ||

| Medical | ||

| Electronics | ||

| Construction | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the rapid prototyping materials market?

The market is valued at USD 6.44 billion in 2026 and is projected to grow to USD 9.53 billion by 2031.

Which material segment is expanding the fastest?

Metals and alloys are expected to post the highest 10.03% CAGR through 2031, driven by aerospace and biomedical demand.

Why is Asia Pacific the fastest-growing region?

China’s aggressive capacity build-out and India’s burgeoning medical-device sector underpin a 10.31% regional CAGR, outpacing other geographies.

How are sustainability mandates influencing material choices?

ISCC-certified bio-based polymers and recycled metal powders are gaining traction as regulators impose carbon-reduction targets and circular-economy goals.

What is the major bottleneck limiting large-scale additive adoption?

A global skills gap in advanced design optimization and material processing constrains production scaling despite rising hardware installations.

Page last updated on: