Prepreg Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

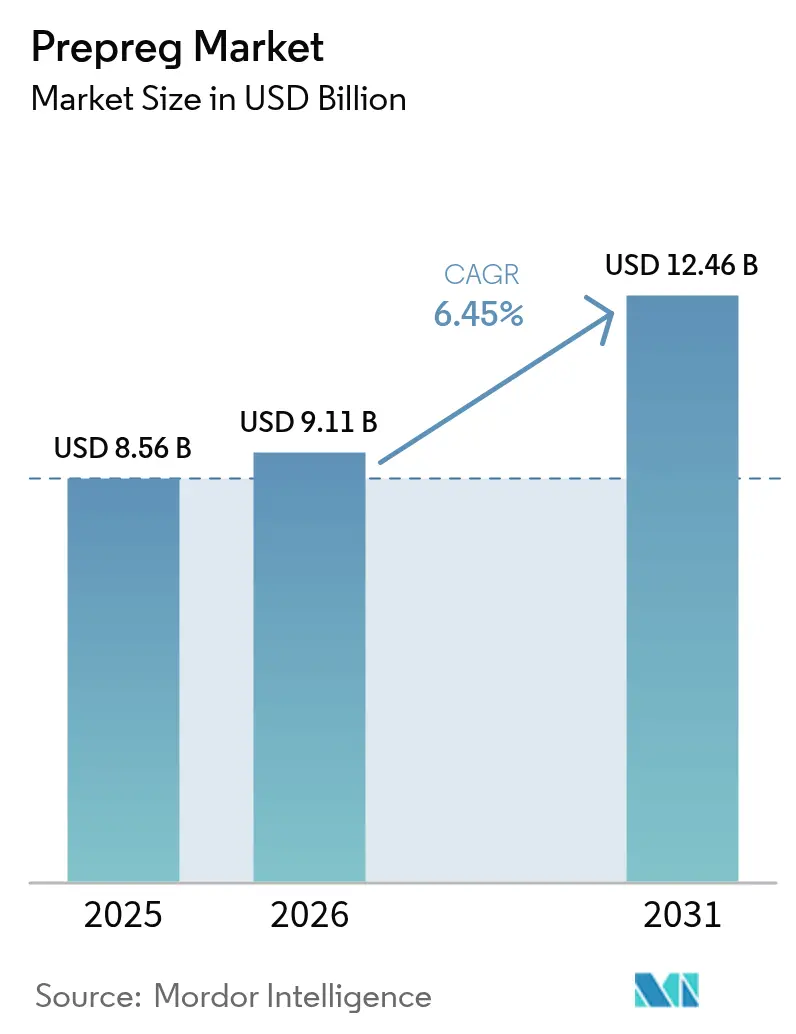

| Market Size (2026) | USD 9.11 Billion |

| Market Size (2031) | USD 12.46 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prepreg Market Analysis by Mordor Intelligence

Prepreg market size in 2026 is estimated at USD 9.11 billion, growing from 2025 value of USD 8.56 billion with 2031 projections showing USD 12.46 billion, growing at 6.45% CAGR over 2026-2031. Commercial aircraft programs that rely on composite-rich wings and fuselages, offshore wind installations that push blade lengths past 100 m, and emerging eVTOL platforms that favor thermoplastic structures collectively underpin this expansion. Strong fuel-burn economics in aerospace, policy-driven renewable-energy build-outs, and vehicle lightweighting regulations reinforce structural-composite demand even as autoclave energy costs and recycling gaps temper near-term momentum. Competitive differentiation hinges on vertical integration, automated lay-up technologies, and certified material databases that safeguard quality while controlling cost. A moderate but tightening supply landscape leaves incumbent suppliers defending price points against rapid Chinese capacity additions, particularly in standard-modulus carbon fiber grades.

Key Report Takeaways

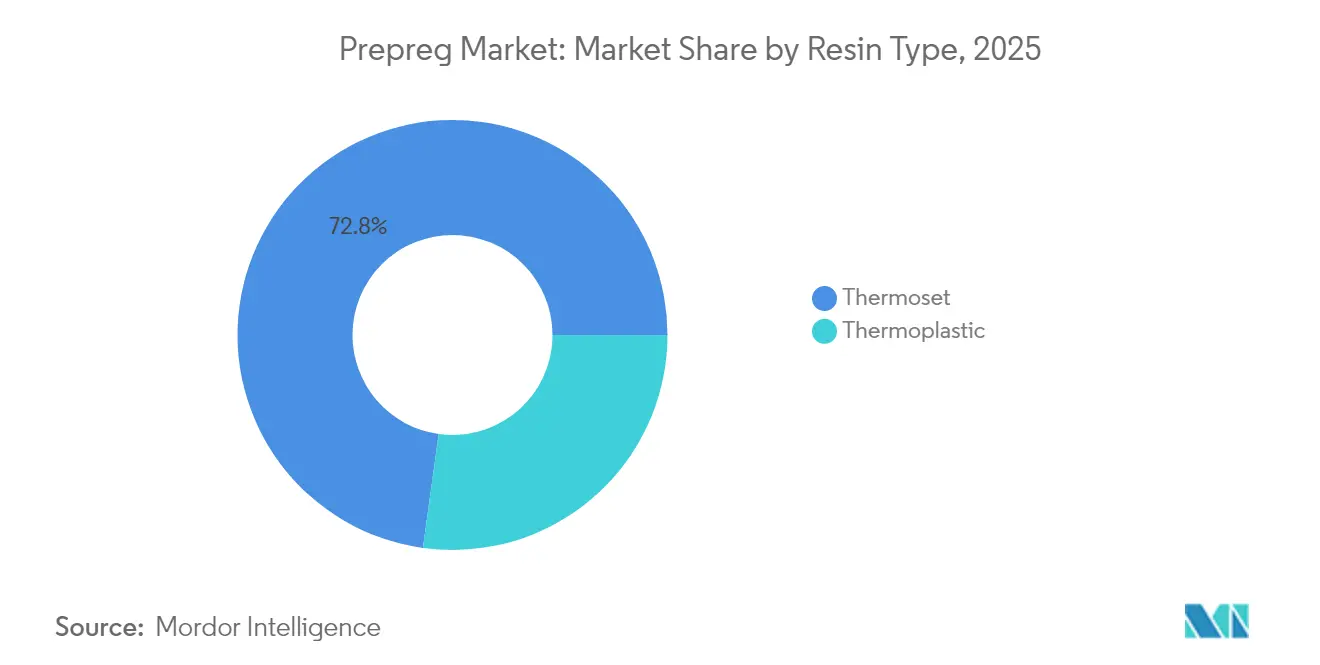

- By resin type, thermoset systems retained 72.80% revenue share in 2025; thermoplastic formulations are advancing at an 8.43% CAGR through 2031.

- By fiber type, carbon fiber commanded 80.70% of the prepreg market size in 2025, while glass fiber is the fastest-growing reinforcement at a 7.62% CAGR to 2031.

- By form, unidirectional tapes held 40.70% of the prepreg market share in 2025; tow prepreg is forecast to rise at an 7.71% CAGR through 2031.

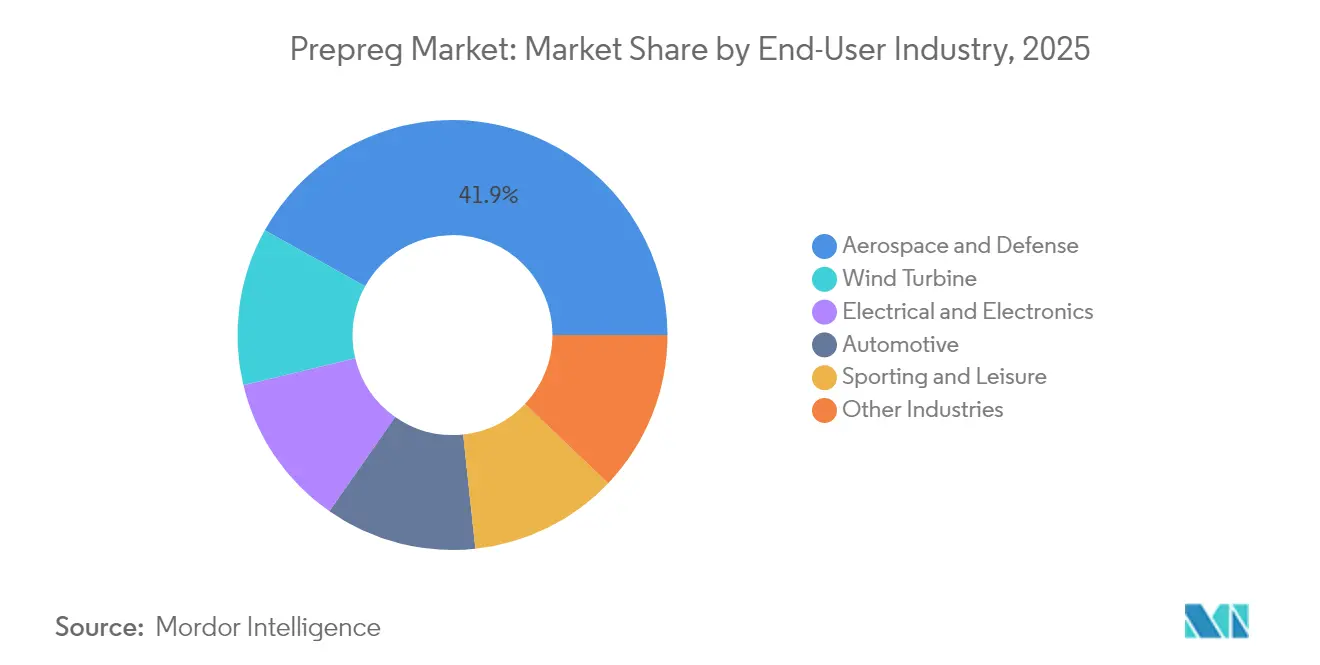

- By end-user industry, aerospace and defense led with a 41.90% prepreg market share in 2025; wind-turbine applications are projected to expand at an 7.76% CAGR through 2031.

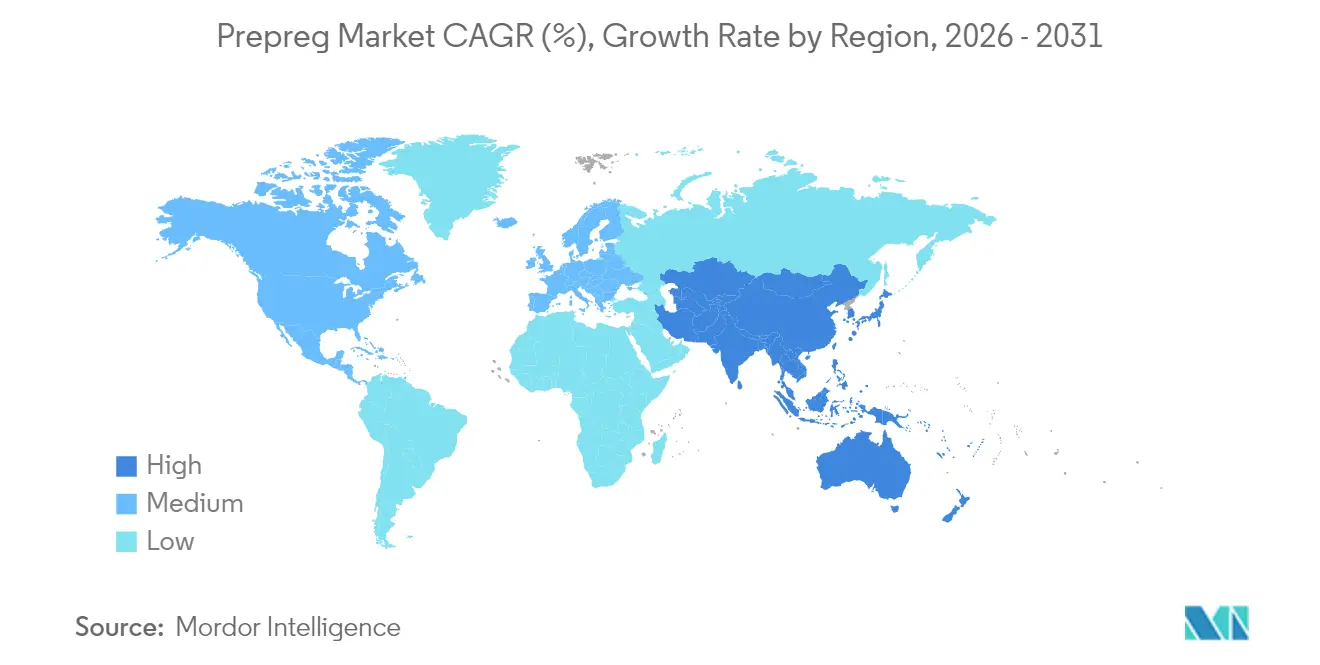

- By region, North America accounted for 37.40% of the prepreg market size in 2025, while Asia-Pacific is on track for the fastest 7.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Prepreg Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging aerospace and defense build-rates | +2.1% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Wind-turbine blade length escalation | +1.8% | Global, with early gains in Europe & Asia-Pacific | Long term (≥ 4 years) |

| Carbon-prepreg penetration in premium autos and sports | +1.2% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| eVTOL and urban-air-mobility demand for thermoplastic prepregs | +0.9% | North America & EU core markets | Long term (≥ 4 years) |

| Hydrogen pressure-vessel tow-prepreg boom | +0.7% | Global, with early adoption in Japan & Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Aerospace and Defense Build-Rates

Commercial aircraft production is rising as Boeing’s 777X and Airbus’s A350 continue composite-heavy build schedules, each incorporating more than 50% carbon-fiber-reinforced polymer by weight. High-lift structural components, fuselage barrels, and wing skins rely on certified epoxy-based prepreg that meets stringent fatigue and damage-tolerance requirements. Defense modernization across NATO members mirrors these trends, retrofitting legacy fleets with lighter mission systems that extend range and payload. Long-term contracts allow suppliers such as Toray Industries and Hexcel Corporation to amortize qualification costs while guaranteeing stable deliveries[1]“Hexcel Q1 2025 earnings call,” Hexcel Corporation, hexcel.com. As composite usage per aircraft climbs, the prepreg market benefits from both volume growth and higher average selling prices anchored by proprietary material databases.

Wind-Turbine Blade Length Escalation

Average offshore rotor diameters now exceed 200 m, forcing blade lengths above 100 m and increasing spar-cap stiffness demands. Carbon-fiber prepreg spar caps reduce blade weight by 25% while maintaining structural integrity, enabling larger turbines to be installed on existing jacket foundations[2]U.S. Department of Energy, “Wind Turbine Blade Innovations,” energy.gov. European OEMs such as Vestas have shifted from fiberglass to hybrid carbon-glass architectures, and Chinese manufacturers are following to meet capacity-addition targets. Vacuum-assisted resin transfer molding and automated fiber placement shorten cycle times and cut labor expenses, bolstering cost competitiveness. With offshore wind commitments accelerating in the North Sea and South China Sea, sustained carbon-fiber demand secures a robust long-term pipeline for the prepreg market.

Carbon-Prepreg Penetration in Premium Autos and Sports

Regulatory weight caps on premium vehicles push OEMs to integrate carbon-fiber body panels, crash structures, and monocoques that deliver 30% mass savings versus aluminum. Rapid-cure epoxy prepreg capable of sub-60-second press cycles aligns with automotive takt-time requirements, while thermoplastic systems offer recyclability that supports circular-economy objectives. Performance sporting goods—ranging from bicycle frames to tennis rackets—leverage similar high-stiffness, low-weight properties to justify premium retail prices. As electric-vehicle battery packs grow heavier, incremental weight removed from the chassis directly translates to longer driving range, reinforcing prepreg adoption.

eVTOL and Urban-Air-Mobility Demand for Thermoplastic Prepregs

Prototype eVTOL aircraft average 70% composite content, a figure that surpasses commercial airliners, and certification bodies favor damage-tolerant thermoplastic laminates for daily urban operations. Weldable joining methods allow rapid assembly and in-service repair without solvents, while inherent recyclability supports emerging sustainability mandates. Strategic alliances—such as Joby Aviation’s sourcing pact with Toray and Archer Aviation’s supply agreement with Hexcel—anchor dedicated capacity ahead of scaled production. Thermoplastic matrices including PEEK and PPS balance high heat resistance with automated fiber placement compatibility, positioning them as a growth focal point within the broader prepreg market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cap-ex and OPEX of autoclave curing lines | -1.4% | Global, particularly impacting smaller manufacturers | Short term (≤ 2 years) |

| Carbon-fiber supply-chain volatility | -1.1% | Global, with acute effects in Europe & North America | Medium term (2-4 years) |

| Weak recycling and EoL infrastructure | -0.8% | Global, with regulatory pressure in EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cap-ex and OPEX of Autoclave Curing Lines

Large-format aerospace autoclaves exceed USD 2 million in capital cost and operate 6-8-hour heat-pressure cycles that consume substantial energy. Smaller Tier-2 suppliers face steep financing barriers, limiting global expansion and introducing supply-bottleneck risk when demand surges. Out-of-autoclave processes—vacuum-bag-only curing, resin-infusion, and oven-based cycles—reduce energy by up to 50% but cannot yet replicate autoclave-derived porosity control for primary structures. Incremental adoption in secondary aerospace parts lowers cost envelopes; however, any delay in fuselage or wing certification sustains the autoclave’s dominance and continues to restrain wider prepreg market penetration.

Carbon-Fiber Supply-Chain Volatility

Spot prices for standard-modulus carbon fiber slid to USD 18/kg in 2024 following capacity overhang in China, only to rebound when aerospace demand recovered, compressing margins for prepreg converters. Export controls and geopolitical tensions threaten steady feedstock flows of polyacrylonitrile (PAN) precursor into Western markets, intensifying diversification efforts toward multiple regional production nodes. Epoxy, vinyl-ester, and unsaturated polyester resins have risen by up to EUR 200/ton since late 2024, exacerbating cost swings passed through to OEMs. Long-term contracts in aerospace that rely on fixed composite pricing become harder to negotiate, creating budgeting uncertainty for airlines and defense buyers alike.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Thermoplastic Growth Accelerates

Thermoset systems retained 72.80% revenue in 2025, underpinned by certification depth in commercial aviation and ballistic-grade defense hardware. Epoxies remain indispensable for primary wings and fuselage sections where high-temperature cures translate to consistent mechanical properties over the aircraft life cycle. In contrast, thermoplastic grades are projected to advance at an 8.43% CAGR on rising eVTOL, automotive, and hydrogen-storage requirements. That expansion contributes USD 1.29 billion to the prepreg market size between 2026 and 2031. Polyetheretherketone and polyphenylene sulfide families deliver heat resistance up to 220 °C and allow induction welding, thereby reducing assembly fastener counts and maintenance downtime.

The push for closed-loop material flows strengthens thermoplastic appeal, as scrap off-cuts can be re-melted into secondary mouldings without degrading performance. Automotive OEMs running high-tonnage compression presses report cycle-time improvements of 40% when switching from classic 180 °C epoxy cycles to sub-3-minute thermoplastic campaigns. Meanwhile, bismaleimide and phenolic systems hold their niche in high-temperature jet-engine ducts and interior panels that demand flame-smoke-toxicity compliance. Overall, contrasting growth trajectories between resin chemistries ensure competitive diversity within the prepreg market.

By Fiber Type: Carbon Dominance Faces Glass Fiber Resurgence

Carbon fiber controlled 80.70% by value in 2025 as its unmatched stiffness-to-weight ratio underpins commercial airliner, space-launch, and Formula 1 requirements. Each additional kilogram trimmed from an aircraft’s operating empty weight saves up to 75 t of fuel over its service life, a direct economic lever that keeps carbon pricing resilient even during downturns. Glass fiber, however, is projected for 7.62% CAGR growth through 2031, riding 5G electronics, LED substrates, and cost-sensitive mobility applications that tolerate lower modulus values. High-frequency printed-circuit-board laminates formulated with specialized glass-fiber prepreg meet dielectric benchmarks for 24 GHz radar and beyond.

Hybrid laminates combining carbon skins with glass core fabrics in wind-turbine spar caps optimize weight while lowering raw-material cost, widening addressable volume. Aramid fibers retain limited market presence in ballistic protection and impact-energy absorption but underscore the material-specific role each reinforcement plays. As Chinese producers scale output, lower-grade carbon fiber pricing compresses, widening the relative cost delta and spurring substitution debates where performance margins are narrower.

By Form: Unidirectional Tapes Lead, Tow Prepreg Surges

Unidirectional tapes comprised 40.70% of 2025 shipments, favored for primary aerospace skins and cryogenic pressure-vessel overwraps where aligned fiber orientation maximizes load-path efficiency. Automated fiber-placement heads deposit UD slit tapes rapidly, improving material yield and cut-rate tolerances, which sustains their lead. Tow prepreg, though smaller in total revenue, is forecast for an 7.71% CAGR driven by filament-wound hydrogen storage tanks that require continuous, void-free fibers able to withstand 700 bar service pressures. Woven fabrics address multi-directional load cases found in rotor-blade root sections and automotive sub-frames but incur lay-up labor overhead that automation only partially offsets. Thermoplastic organosheets—pre-consolidated, cross-ply laminates—target high-volume automotive press-forming, offering cycle times under one minute and scrap rates below 5%. In aggregate, the form segmentation reveals how manufacturing process economics rather than intrinsic material properties increasingly dictate prepreg selection.

By End-User Industry: Aerospace Dominance, Wind Energy Momentum

Aerospace and defense captured 41.90% revenue in 2025, reflecting stringent certification barriers that shield suppliers from commoditization pressures. Forward fuselage barrels, empennage structures, and engine nacelles rely on strictly controlled prepreg batches tracked by lot for over 20 years of airframe life. Composite share per aircraft continues to climb, and the resulting pull-through guarantees baseline growth for the prepreg market even in a conservative traffic-recovery scenario. Wind energy, while holding a smaller absolute share, is set for the fastest 7.76% CAGR as offshore installations migrate to 15-MW class turbines demanding elongated, carbon-rich blades.

Automotive uptake remains concentrated in premium and motorsports segments where cost tolerance allows carbon monocoques and Class A body panels. Yet battery-electric models that need weight mitigations to counter lithium-ion pack mass have started to adopt lower-cost glass-fiber sheet-molded composites in closure panels, signaling gradual prepreg diffusion beyond supercars. Electronics and electrical infrastructure rely on specialty glass-fiber epoxy prepregs that satisfy thermal-conductivity and dielectric metrics crucial to 5G base stations. Finally, sporting goods continue a steady high-margin trajectory, leveraging prepreg’s stiffness-to-weight superiority to differentiate professional-grade equipment.

Geography Analysis

North America retained the largest 37.40% share of the prepreg market in 2025, buoyed by Boeing’s composite-intensive 787, 777X, and proprietary space-launch structures. Pentagon modernization programs extend material demand into rotorcraft, unmanned systems, and hypersonic vehicles, ensuring stable multi-year order books. The region’s certification ecosystem favors domestic suppliers such as Hexcel and Toray Advanced Composites, both of which operate vertically integrated lines from carbonization to prepregging. Nevertheless, 2025 commercial-aerospace revenues slipped after a major narrow-body delivery adjustment, highlighting short-cycle variability amid otherwise strong defense backlogs.

Asia-Pacific emerges as the quickest-growing geography with an 7.78% CAGR forecast to 2031. Chinese state-backed carbon fiber producers are on pace to command nearly 50% of global capacity by 2030, lowering price points and catalyzing broader industrial uptake. Indigenous aerospace programs such as COMAC’s C919 and CR929, along with domestic eVTOL prototypes, provide captive demand for high-grade prepreg. Japan’s Toray and Teijin maintain technology leadership through high-modulus fibers and automotive-qualified thermoplastic laminates, while South Korea’s hydrogen-storage tank initiatives fuel tow-prepreg growth.

Europe sustains mid-single-digit growth anchored by Airbus wing-assembly, UK advanced-propulsion R&D, and aggressive offshore-wind targets in the North Sea. Policymakers intensify scrutiny of end-of-life composite waste, accelerating investment into pyrolysis and solvolysis pilot plants that can reclaim high-value fiber. Gurit’s decision to expand German aerospace-prepreg capacity while shuttering a Swiss line illustrates cost-rationalization amid tight European energy pricing. Meanwhile, automotive composite adoption faces regulatory uncertainty over potential carbon-fiber usage limits, though lighter materials remain exempt in renewable-energy and commercial-aviation contexts.

Competitive Landscape

The prepreg market retains a moderate concentration characterized by three integrated leaders—Toray Industries, Hexcel Corporation, and Teijin Limited—that control carbon-fiber precursor, fiber conversion, and prepregging under one corporate umbrella. Their collective strength in qualified aerospace programs creates high switching costs and shields margins despite raw-material volatility. Each maintains multi-decade supply contracts: Toray with Boeing’s 777X wings, Hexcel with Airbus and Kongsberg Defense, and Teijin with multiple defense UAV platforms. To preserve share, incumbents expand automation footprints, embedding real-time porosity monitoring and closed-loop lay-up vision systems that cut scrap rates below 2%.

Chinese challengers, supported by state incentives, ramp capacity concentrated in standard-modulus PAN fibers, and market them aggressively into mid-tier sporting goods, wind energy, and industrial cylinders. Their cost base, often 20% below Western peers, places downward pressure on global reference prices and accelerates commoditization outside certified aerospace grades. Western suppliers respond by advancing thermoplastic prepreg portfolios aimed at eVTOL, hydrogen storage, and automotive structural components where certification hurdles are lower but functional demands remain high.

Prepreg Industry Leaders

Hexcel Corporation

Solvay

Gurit Services AG

Mitsubishi Chemical Group Corporation

Toray Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: In 2024, Mitsubishi Chemical Group (MCG Group) earned ISCC PLUS certification for its plant-based resin prepreg products and began sample work on the BiOpreg #500 series using the mass balance approach.

- July 2024: Toray Composite Materials America Inc. partnered with Elevated Materials to recycle scrap prepreg materials from its Tacoma, Washington facility under a three-year agreement.

Global Prepreg Market Report Scope

The global prepreg market report includes:

| Thermoset |

| Thermoplastic |

| Carbon |

| Glass |

| Aramid |

| Unidirectional (UD) Tapes |

| Tow Prepreg |

| Fabric/Woven |

| Organosheets |

| Aerospace and Defense |

| Wind Turbine |

| Automotive |

| Electrical and Electronics |

| Sporting and Leisure |

| Other Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Resin Type | Thermoset | |

| Thermoplastic | ||

| By Fiber Type | Carbon | |

| Glass | ||

| Aramid | ||

| By Form | Unidirectional (UD) Tapes | |

| Tow Prepreg | ||

| Fabric/Woven | ||

| Organosheets | ||

| By End-User Industry | Aerospace and Defense | |

| Wind Turbine | ||

| Automotive | ||

| Electrical and Electronics | ||

| Sporting and Leisure | ||

| Other Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Prepreg Market size?

The prepreg market size is USD 9.11 billion in 2026 and is forecast to reach USD 12.46 billion by 2031, translating to a 6.45% CAGR over the period 2026-2031.

Which end-user industry dominates demand?

Aerospace and defense applications account for 41.90% of 2025 revenue owing to high composite content in airframes and defense programs.

Why are thermoplastic prepregs gaining share?

Thermoplastic systems offer rapid processing, weldable joints, and recyclability, driving an 8.43% CAGR led by eVTOL aircraft and hydrogen storage vessels.

How large is North America’s portion of global prepreg demand?

North America held 37.40% of the market in 2025, supported by Boeing’s production ramp and defense composite needs.

Page last updated on: