Phase Change Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

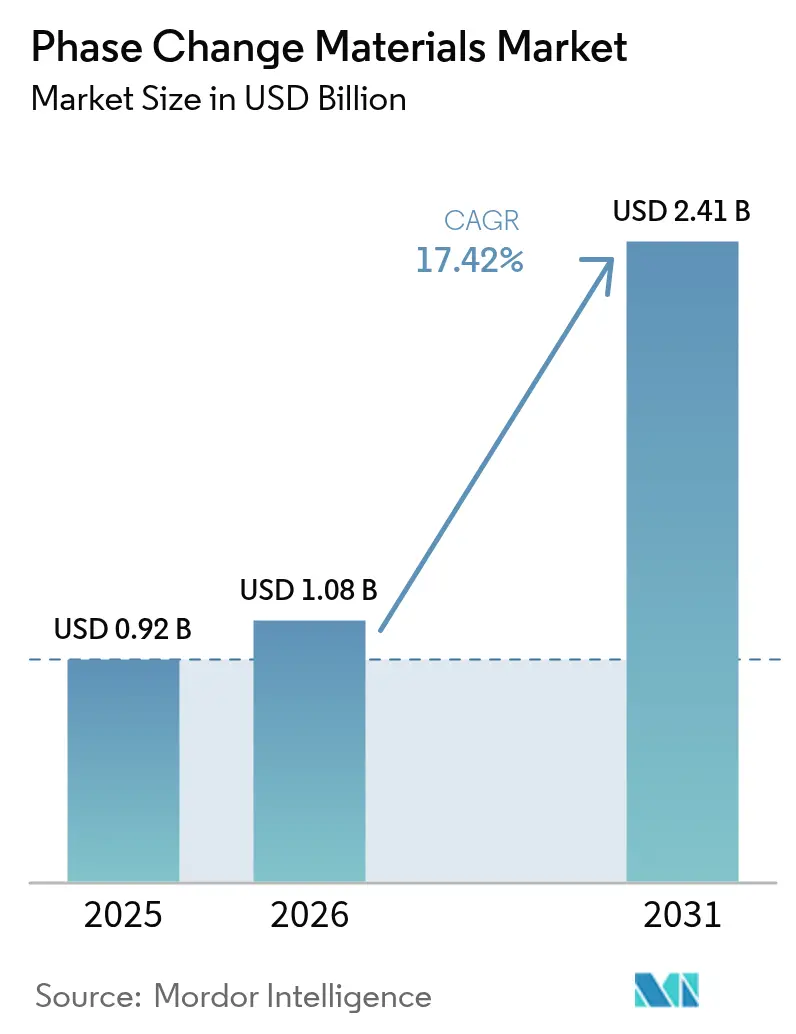

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 17.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phase Change Materials Market Analysis by Mordor Intelligence

Phase Change Materials market size in 2026 is estimated at USD 1.08 billion, growing from 2025 value of USD 0.92 billion with 2031 projections showing USD 2.41 billion, growing at 17.42% CAGR over 2026-2031. Lengthening heat waves, net-zero construction goals, and rapid electrification in transport now place latent-heat storage at the center of commercial energy strategies. Mandatory building-energy codes in Europe and North America are accelerating integration, while cold-chain logistics and electric-vehicle battery packs expand the technology’s reach into transportation, pharmaceuticals, and data-center cooling. Longly constrained by phase-separation and supercooling issues, salt hydrates are gaining traction after recent conductivity breakthroughs. At the same time, bio-based PCMs derived from agricultural residues have moved from laboratory curiosity to scalable commercial products, addressing fire safety and sustainability concerns without sacrificing thermal capacity. Regionally, Asia-Pacific is evolving into the fulcrum for capacity additions as manufacturers add local production lines to hedge supply-chain risk linked to high-purity salt hydrates.

Key Report Takeaways

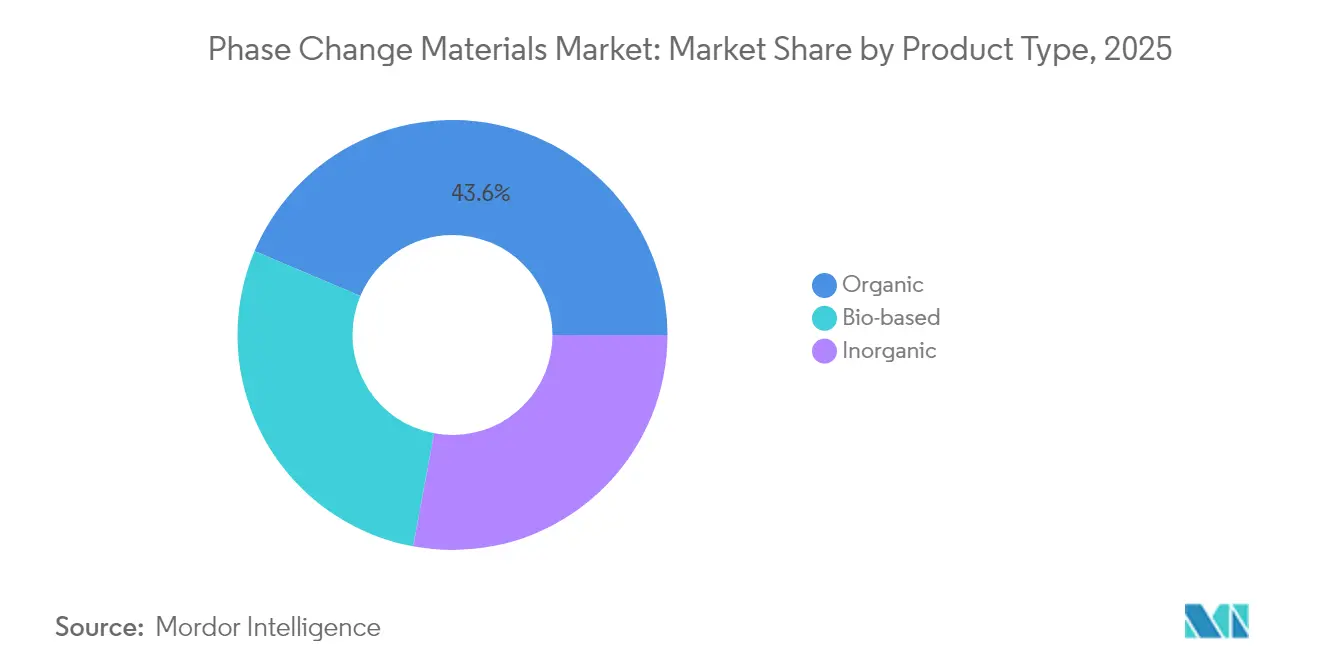

- By product type, organic PCMs led with 43.62% Phase Change Material market share in 2025; bio-based materials are forecast to expand at a 18.90% CAGR through 2031.

- By chemical composition, paraffin-based solutions held the largest revenue share at 41.02% in 2025, while salt hydrates are advancing at an 17.76% CAGR to 2031.

- By encapsulation technology, the macro-encapsulation segment captured 65.20% of the Phase Change Material market size in 2025; micro-encapsulation is expected to grow at 18.31% CAGR between 2026-2031.

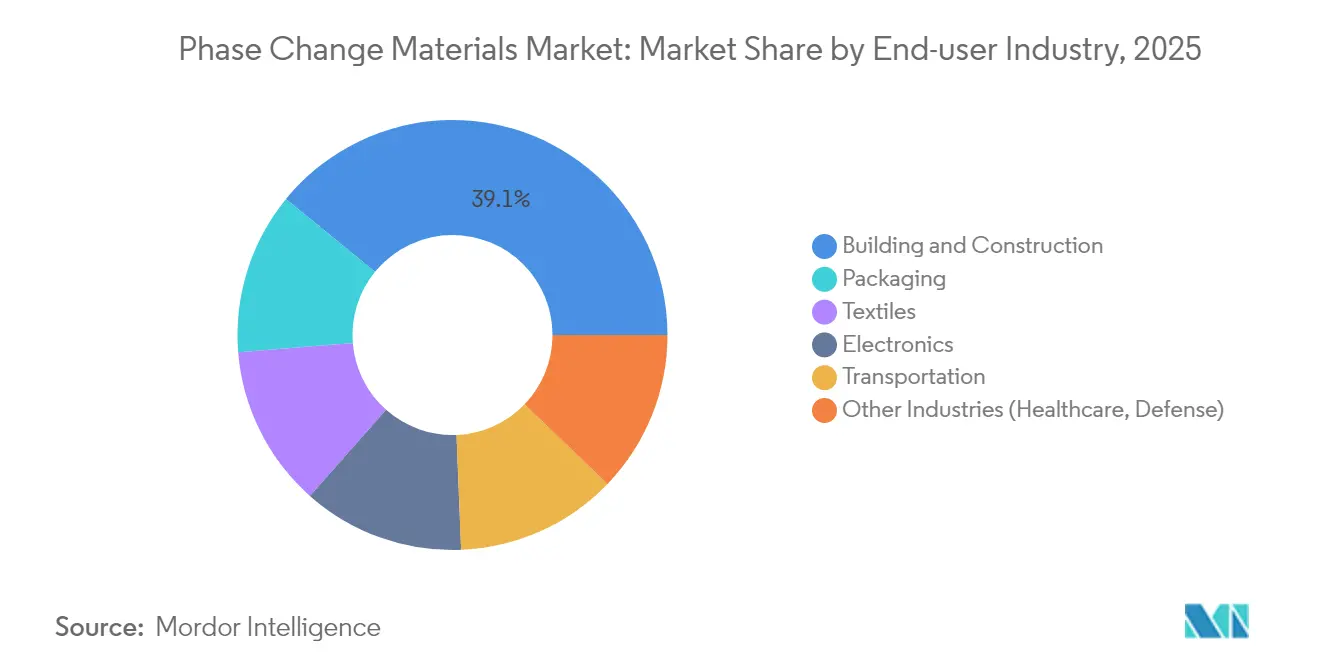

- By end-user industry, the building and construction segment commanded 39.10% share of the Phase Change Material market size in 2025 and is projected to sustain an 17.81% CAGR through 2031.

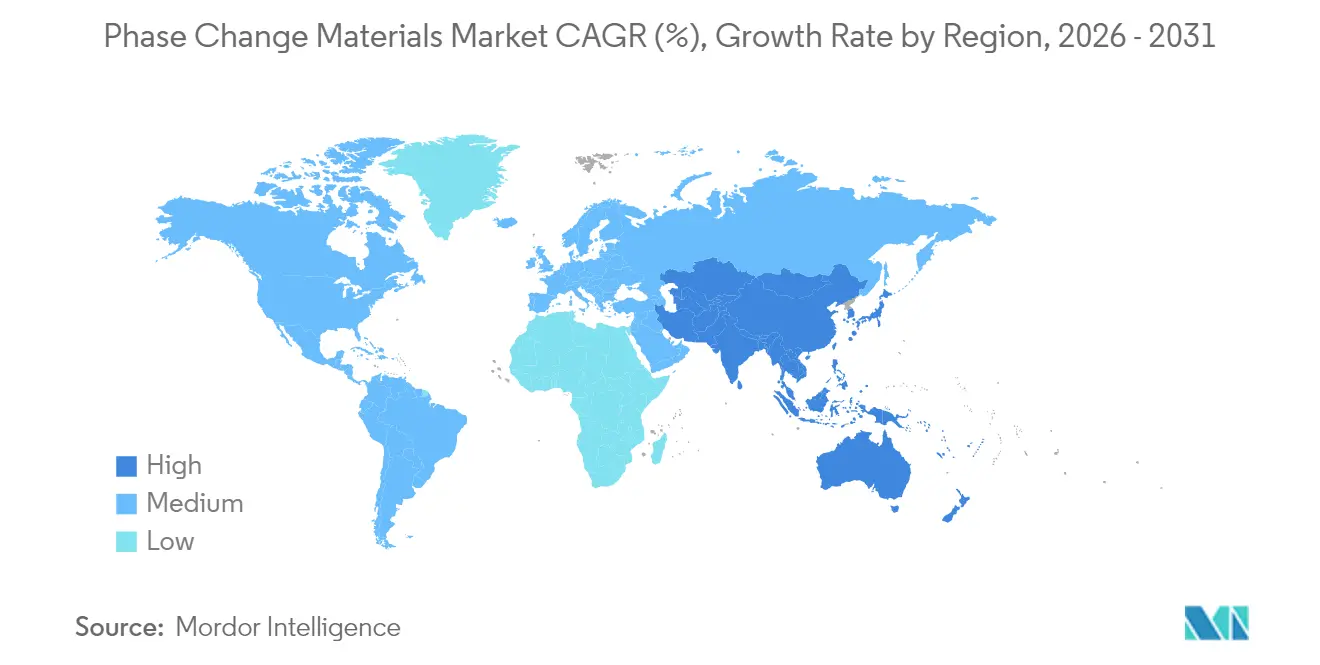

- By geography, Europe contributed 32.40% of global revenue in 2025, whereas Asia-Pacific is forecast to record the quickest regional pace at 18.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Phase Change Materials Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Mandatory Building-Energy Codes in Europe and North America Accelerating PCM Integration | +3.2% | Europe, North America | Medium term (~ 3-4 yrs) |

| Rapid Deployment of Cold-Chain Logistics Infrastructure | +2.8% | Global, with emphasis on Asia-Pacific | Short term (≤ 2 yrs) |

| Electrification of Vehicles Necessitating Advanced Thermal Battery Packs Using Salt-Hydrate PCMs | +4.5% | North America, Europe, China | Medium term (~ 3-4 yrs) |

| Government Incentives for Net-Zero Buildings Propelling Bio-based PCM Adoption | +3.9% | Europe, North America, and developed Asia-Pacific | Long term (≥ 5 yrs) |

| Expanding Global Trend Towards Energy Conservation and Sustainable Development | +3.1% | Global | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Mandatory Building-Energy Codes Accelerating PCM Integration

Performance-based compliance criteria now allow architects to substitute rigid insulation with latent-heat storage layers, unlocking a 35-45% reduction in peak cooling loads within lightweight walls. Measured field results in Minnesota reported a 5.49 °C drop in peak indoor temperature plus a 77.8% load shift toward off-peak hours, providing regulators with real-world evidence of HVAC savings[1]Minnesota Department of Commerce, “Field Study of Phase Change Material (PCM) Use for Passive Thermal Management,” mn.gov. Rising compliance thresholds for 2027 EU renovation targets are expected to place additional emphasis on PCM-infused gypsum boards and concrete blocks, thereby lifting procurement volumes across the Phase Change Material market.

Rapid Deployment of Cold-Chain Logistics Infrastructure

Vaccines, advanced biologics, and precision meats require temperature bands that often tolerate a ±0.5 °C deviation for less than three days. PCMs extend that holdover to 72 hours without external power, cutting diesel-generator reliance during airport or customs delays. Glycerol-water-NaCl blends slash carbon footprints 30-40% versus active cooling and lift pharmaceutical shelf life by 15-25%, feeding double-digit demand across the Phase Change Material market.

Electrification of Vehicles Necessitating Advanced Thermal Battery Packs

Composite salt-hydrate matrices disperse heat spikes generated under 4C discharge, maintaining cell temperatures below 39 °C and curbing thermal-runaway risk. Compared with forced-air convection, PCM plates shrink peak temperatures by up to 40% and lengthen battery longevity, a decisive factor as EV warranties stretch toward 10 years. Tier-1 suppliers are scaling graphite-reinforced pads that align with cylindrical, pouch, and prismatic cell formats, further broadening the Phase Change Material market.

Government Incentives for Net-Zero Buildings Propelling Bio-Based PCM Adoption

Bio-derived latent-heat blends sourced from plant oils, animal fats, and agricultural residues secure additional points under LEED v4 and BREEAM 2025. Bacon-fat PCMs now deliver 2.36 × the thermal-storage density of standard paraffin at a lower cost. Financial offsets, such as Germany’s BEG program covering 20% of building envelope upgrades, are triggering higher order volumes, especially as bio-PCMs exhibit reduced smoke and toxicity profiles versus petroleum alternatives.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Hazardous Nature of Phase Change Materials | -2.1% | Global, with higher impact in regions with strict chemical regulations | Short term (≤ 2 yrs) |

| Supply-Chain Volatility of High-Purity Salt Hydrates | -3.4% | Global, with particular impact on Asia-Pacific manufacturing | Medium term (~ 3-4 yrs) |

| Limited Awareness and Understanding | -1.8% | Emerging markets, particularly in South America and parts of Asia | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Hazardous Nature of Phase Change Materials

Paraffin waxes ignite at roughly 170 °C and require brominated flame retardants that add cost and can trigger health-labeling restrictions. Inorganic candidates such as LiNO₃ present toxicity risks. Recent in-situ polymerized solid-solid PCMs eliminate leakage, passing UL94 V-0 flammability without halogens. Broader adoption hinges on scaling these encapsulation advances and harmonizing global chemical safety standards.

Supply-Chain Volatility of High-Purity Salt Hydrates

Medical-grade CaCl₂·6H₂O relies on narrow mining zones and multistage purification, whose capacity additions lag demand. Spot shortages have driven 2024 contract prices, pressuring producers that depend on micro-encapsulation lines calibrated for consistent crystal purity. Graphite-reinforced composites that tolerate industrial-grade inputs while maintaining 4 W/m·K conductivity offer a mid-term safeguard. Nevertheless, any raw-material squeeze reverberates through the Phase Change Material market value chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bio-Based Solutions Accelerate Market Diversification

Organic paraffin waxes remain the revenue anchor for the Phase Change Material market, accounting for 43.62% of global sales in 2025. Their dominance reflects mature supply chains, broad temperature coverage, and compatibility with macro-encapsulation slabs used in building panels. Yet the Phase Change Material market is witnessing a sharp pivot toward bio-derived oils, tallow, and fatty-acid blends as stakeholders chase lower life-cycle emissions. The emergent sub-segment is forecast to outpace all others at 18.90% CAGR to 2031, buoyed by LEED credits and municipal green-procurement mandates that explicitly endorse biogenic materials.

By Chemical Composition: Salt Hydrates Challenge Paraffin Dominance

Paraffin-based formulations captured 41.02% of the Phase Change Material market revenue in 2025 due to their stable crystallization and ease of tailoring melting points across the 0-90 °C spectrum. Even so, salt hydrates are on course to disrupt that hierarchy, expanding at an 17.76% CAGR through 2031. High volumetric heat capacity (up to 350 kJ/L) and thermal conductivity improvements via carbon additives are allowing salt hydrates to shrink component size and weight. The resulting density advantage is especially attractive for electric-vehicle battery sleeves and compact data-center racks, where available footprint is constrained.

By Encapsulation Technology: Micro-Encapsulation Reinvents Performance Boundaries

Macro-encapsulation, drums, panels, and tubes currently safeguard 65.20% of the Phase Change Material market size, thanks to straightforward manufacturing and installation within gypsum boards, ceiling tiles, and chilled-water tanks. However, micro-encapsulation is accelerating at an 18.31% CAGR, fueled by the need for leakage-proof dispersions that can be sprayed, printed, or woven into fabrics. Capsules coated with graphene oxide now exhibit conductivity gains topping 1008% over neat paraffin, enabling faster charge–discharge cycles crucial for peak-shaving applications.

By End-User Industry: Building and Construction Remains the Anchor

The construction sector consumed 39.10% of global PCM volumes 2025 by retrofitting walls, roofs, and concrete blocks with latent heat inserts that shave 20-35% off HVAC energy demand, meeting European Energy Performance directives. Regional demonstration buildings in Spain, Sweden, and Germany show that PCM-enhanced wallboards can sustain a 5.49 °C delta for half an hour under simulated solar load. These replicable metrics justify line-item allocations in large public-sector renovation budgets, anchoring the Phase Change Material market.

The transportation category is surging due to electric-vehicle pack adoption, hybrid railcars, and refrigerated shipping containers. PCM liners now push lithium-ion cell temperatures 40% lower than natural convection equivalents, extending cycle life and improving fast-charge tolerance. Packaging follows closely, as pharmaceutical distributors prepare for ever stricter GDP (Good Distribution Practice) rules that clamp down on temperature excursions. Once limited to comfort clothing, textiles now employ PCM microcapsules in military uniforms and medical wraps for localized cooling or controlled drug release, further widening the Phase Change Material industry scope.

Geography Analysis

Europe held 32.40% of global sales in 2025, underpinned by the EU’s Energy Performance of Buildings Directive, which compels both new construction and deep-renovation projects to hit quasi-net-zero targets. Early adopters in Germany and the Nordics have shown 20-35% HVAC energy savings after embedding PCMs into external wall insulation systems. Regulatory clarity around carbon trading and green-bond eligibility continues to draw capital toward PCM-rich building materials, consolidating Europe’s leadership position in the Phase Change Material market.

Asia-Pacific is the fastest-growing region, anticipated to expand 18.55% annually through 2031. China’s aggressive heat-pump rollout complements PCM thermal storage by shaving peak electricity demand, a synergy encouraged under the “Future of Heat Pumps” roadmap.

North America combines stringent energy-code updates with an exploding electric-vehicle sector. Data-center operators in the United States, drawn by tax credits for on-site energy storage, pilot PCM-based thermal buffers to absorb server heat spikes and postpone chiller start-up.

Mordor Intelligence provides coverage of the phase change materials market across other key regional markets, including North America and Europe, each with their regulatory frameworks and demand patterns.

Value Chain Analysis

The phase change materials (PCM) value chain starts with upstream feedstocks such as petroleum-derived paraffins and specialty hydrocarbons, high-purity salt hydrates (for example, CaCl2·6H2O) that require controlled purification, and bio-based inputs sourced from plant oils, animal fats, and agricultural residues. Midstream players formulate and compound PCMs, then add stabilization and encapsulation (macro-encapsulation in panels, tubes, and pouches, and micro- or nano-encapsulation for leakage control and compatibility with coatings, textiles, and composites). Company ecosystems include specialist PCM producers and platform suppliers such as PureTemp, Phase Change Solutions, and Teappcm, with downstream converters that embed PCMs into gypsum boards, ceiling tiles, cold-chain packaging, and thermal-management components.

Downstream channels split between direct-to-OEM supply for building materials, cold-chain shippers, and thermal-management integrators, alongside project-led specification through architects, HVAC and energy service firms, and logistics providers. Qualification and certification cycles for safety and performance remain a core bottleneck, and supply-chain volatility for high-purity salt hydrates can also disrupt micro-encapsulation lines calibrated to consistent crystal quality. Recent R&D signals point to continued process innovation at the encapsulation step, including April 2026 publication of a one-step nano-encapsulation method using lauric acid reported to achieve high encapsulation efficiency, which supports finer particle sizes and improved dispersion performance for applications that require micro-encapsulated PCMs.

Competitive Landscape

The Phase Change Material market is highly fragmented, with a long tail of regional specialists competing alongside diversified multinationals. Phase Change Solutions has capitalized on vertical integration, coupling feedstock sourcing with in-house encapsulation and downstream system design, a model that compresses lead times for OEM customers. Innovation remains the chief competitive lever. High-purity salt-hydrate supply is another front; several Asia-Pacific manufacturers negotiate off-take agreements with mining firms to secure stable crystal supply, mitigating volatility that could crimp margins.

Phase Change Materials Industry Leaders

BASF

Croda International Plc

Henkel AG & Co. KGaA

Honeywell International Inc.

PureTemp LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Building-integrated thermal storage continues to create whitespace for PCM suppliers, especially where passive peak-load reduction is packaged into standard building components rather than relying on bespoke projects. In March 2026, Armstrong World Industries launched Templok ceiling tiles using an integrated salt-based PCM packaged in a metallized polymer pouch, showing how PCM content can be introduced through familiar ceiling and interior retrofit workflows. Product formats like this expand the practical address for macro-encapsulated and form-stable PCMs in renovations where building operators focus on peak shaving and comfort stabilization without major mechanical upgrades.

A second opportunity is platform consolidation and faster go-to-market for advanced PCM formulations through technology integration and scale-up of microencapsulation. In June 2026, Alexium expanded its global PCM platform through integration of Micronal technology following its acquisition of Microtek Laboratories, reflecting competitive emphasis on owning encapsulation and formulation know-how. On the manufacturing and innovation pipeline, Nippon Shokubai initiated a NEDO-supported joint research project in September 2025 with Hokkaido University and Toyo Aluminium to develop mass production technology for alloy-based latent heat storage microcapsules (h-MEPCM), which supports industrialization of higher-density latent heat materials and broadens the set of PCM chemistries beyond traditional paraffins and salt hydrates.

Recent Industry Developments

- June 2026: Alexium International Group Limited announced the expansion of its global phase change material platform through integration of the Micronal technology portfolio obtained via its acquisition of Microtek Laboratories. The move strengthens Alexium’s ability to offer packaged thermal-management solutions by combining formulation and platform assets. It also signals continued consolidation around differentiated PCM and encapsulation capabilities rather than commodity wax-only offerings.

- January 2025: Croda International Plc reported the development of CrodaTherm 5, a bio-based and biodegradable PCM positioned for cold-chain logistics applications in pharmaceutical and food supply chains. The product focus aligns with demand for lower-toxicity, sustainability-linked materials that still meet narrow temperature-band handling needs. It adds competitive pressure on incumbent paraffin systems in packaging formats where procurement increasingly screens for sustainability attributes.

- August 2024: Phase Change Solutions announced commercialization of cold-chain and cold-storage thermal management solutions in Thailand through a partnership with SCG Chemicals subsidiary Texplore. This collaboration extends PCM deployment closer to end users in a fast-expanding logistics and temperature-controlled warehousing environment. The regional push also reflects a shift toward local partnerships to shorten qualification cycles and support application engineering in-market.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this methodology, the phase change materials (PCM) market covers revenues from materials that store and release heat during a phase transition, when sold into thermal management and thermal energy storage uses across industries.

This scope excludes complete cooling or heating systems, installation services, and unrelated insulation materials that do not deliver latent-heat storage.

Segmentation Overview

- By Product Type

- Organic

- Inorganic

- Bio-based

- By Chemical Composition

- Paraffin

- Non-Paraffin Hydrocarbons

- Salt Hydrates

- Eutectics

- By Encapsulation Technology

- Macro-encapsulation

- Micro-encapsulation

- Molecular Encapsulation

- By End-user Industry

- Building and Construction

- Packaging

- Textiles

- Electronics

- Transportation

- Other Industries (Healthcare, Defense)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market frame and to anchor the model inputs that can be checked independently. We reviewed public technical and policy references, such as US Department of Energy materials and building efficiency resources, national standards bodies, and peer reviewed journal articles on PCM performance, stability, and encapsulation.

To keep the demand story grounded, we also referenced building stock and construction activity statistics (for example, US Census releases), customs trade summaries for relevant chemical classes, and association or conference material that describes adoption patterns in cold chain, construction, and electronics. Company annual reports, product datasheets, and press releases were used to confirm product positioning, end-use focus, and geographic footprint. Then, where available, a paid subscription for company financials, patent activity, and shipment-level trade screening was used selectively to validate directionally consistent totals. The sources listed here are illustrative, and many other public and subscription sources were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary discussions were run with manufacturers, distributors, formulators, and downstream users in construction materials, cold chain packaging, electronics thermal management, and transportation. Respondent input was used to stress-test adoption rates, typical PCM loadings per product, pricing bands by chemistry and encapsulation, and the pace of new project awards across key regions. Where large variances appeared in the model, we rechecked the underlying assumptions with follow-up questions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | APAC: 43% |

| Mid tier: 56% | Functional/Unit leaders: 25% | EMEA: 35% |

| Smaller Players: 18% | Managers: 60% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where construction activity, cold chain expansion, and electronics thermal management demand are translated into an addressable PCM demand pool using penetration rates and typical material intensity (kg per square foot of building element, kg per shipper, or kg per device group, depending on the use). Those demand pools are then converted to value using price bands that differ by chemistry (organic, inorganic, bio-based) and by encapsulation approach.

To keep totals realistic, the output is corroborated with selective bottom-up checks, such as roll-ups of sampled supplier revenues, channel conversations on annual volumes, and ASP x volume sense checks for common PCM grades. Inputs that typically move the model include building energy efficiency retrofits, cold chain shipment volumes, EV and data-center cooling demand signals, raw material cost direction for key feedstocks, and the share of solutions shifting toward bio-based options. For forecasting, scenario analysis is used so adoption sensitivity, price normalization, and policy-driven efficiency pushes can be tested in a simple, repeatable way. The final path is then aligned to what interviewees describe as the most likely case. Where bottom-up visibility is thin in smaller countries or niche end uses, gaps are handled through proxy intensity factors and are revisited during validation calls.

Data Validation & Update Cycle

Outputs are triangulated against independent signals, such as construction and cold chain indicators, trade direction, and observed pricing ranges, before the final numbers are signed off. Any sharp jumps in mix, price, or regional shares are flagged, reviewed by another analyst, and tracked back to the specific assumption that caused the movement.

Reports are refreshed annually, with interim updates when material events occur, such as large capacity changes, regulation shifts affecting building efficiency, or sudden feedstock price shocks. Before delivery, we do a fresh pass on key inputs and re-contact sources when a major variance appears, so the final view reflects the most current market conditions.

Mordor Intelligence's Phase Change Materials Market Sizing Compared With Other Published Estimates

Published PCM market values can appear far apart because each publisher chooses its own base year, pricing logic, and what is counted as PCM revenue versus a broader thermal solution value. Differences also come from how quickly assumptions are refreshed when feedstock costs move, or when adoption shifts across construction and cold chain.

Some external estimates roll in adjacent thermal management materials or finished solution revenues, and then extend pricing forward using generalized inflation steps. For Mordor Intelligence, only PCM material revenues by chemistry and encapsulation sold into defined end uses are counted, and the price path is rechecked through interview-backed ranges and recent project activity.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.08 B (2026) | |

| Industry Publisher A | USD 0.87 B (2025) | Uses an earlier reference year and commonly blends application-level solution value into the PCM total, which can shift the material-only revenue up or down depending on assumed attach rates. |

| Industry Publisher B | USD 0.63 B (2024) | Anchors sizing to a narrower immediate demand set and carries forward pricing with limited adjustment for encapsulation mix, so value growth stays more restrained even if volume adoption rises. |

The spread across sources mainly tracks to year selection and whether the number is kept to PCM materials or widened to include adjacent thermal offerings. By keeping the inputs tied to observable demand indicators and by revalidating the key adoption and pricing variables, the resulting number stays easier to replicate and audit over time.

Key Questions Answered in the Report

What is driving the rapid growth of the Phase Change Material market?

Demand stems from stricter building-energy codes, cold-chain logistics expansion, and electric-vehicle battery cooling, pushing the Phase Change Material market size toward USD 2.41 billion by 2031.

Which product segment is growing the fastest?

Bio-based PCMs, derived from renewable oils and fats, are expected to post a 18.90% CAGR, outpacing all other categories within the Phase Change Material market.

How do salt-hydrate PCMs compare with paraffin waxes?

Salt hydrates offer higher volumetric heat capacity and better thermal conductivity, and their share of the Phase Change Material market is advancing at 17.76% CAGR as supercooling challenges are resolved.

Why are micro-encapsulated PCMs gaining popularity?

Micro-capsules prevent leakage, improve mechanical strength, and integrate easily into paints or fabrics; this sub-segment is growing at 18.31% CAGR, the quickest among encapsulation methods.

Which region offers the highest growth potential?

Asia-Pacific is projected to expand at an 18.55% CAGR due to large-scale construction, logistics investments, and aggressive electrification programs that collectively broaden the Phase Change Material market.

Page last updated on: