Thermochromic Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.77 Billion |

| Market Size (2031) | USD 3.56 Billion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

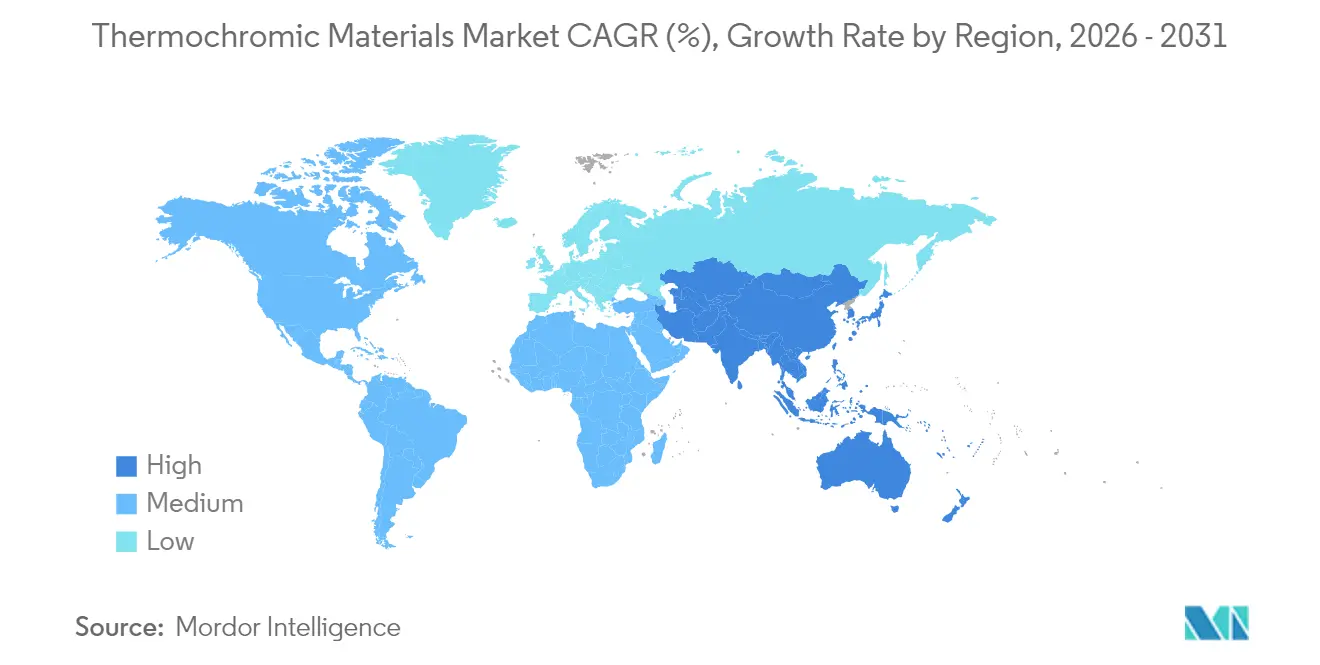

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermochromic Materials Market Analysis by Mordor Intelligence

The Thermochromic Materials Market size was valued at USD 2.64 billion in 2025 and estimated to grow from USD 2.77 billion in 2026 to reach USD 3.56 billion by 2031, at a CAGR of 5.09% during the forecast period (2026-2031). Rising compliance with cool-roof mandates, broader integration of printable smart labels, and swift gains in micro-encapsulation efficiencies collectively reinforce a steady demand curve. Reversible systems dominate both volume and value because they withstand thousands of thermal cycles, while leuco dye chemistry remains a favored option where cost sensitivity prevails. Asia-Pacific commands the largest regional position and delivers the fastest incremental growth as Chinese production capacity collocates with surging Indian consumption. Producers are simultaneously navigating cost premiums and durability constraints, prompting investments in formaldehyde-free shells and hybrid pigment systems that prolong outdoor lifetimes.

Key Report Takeaways

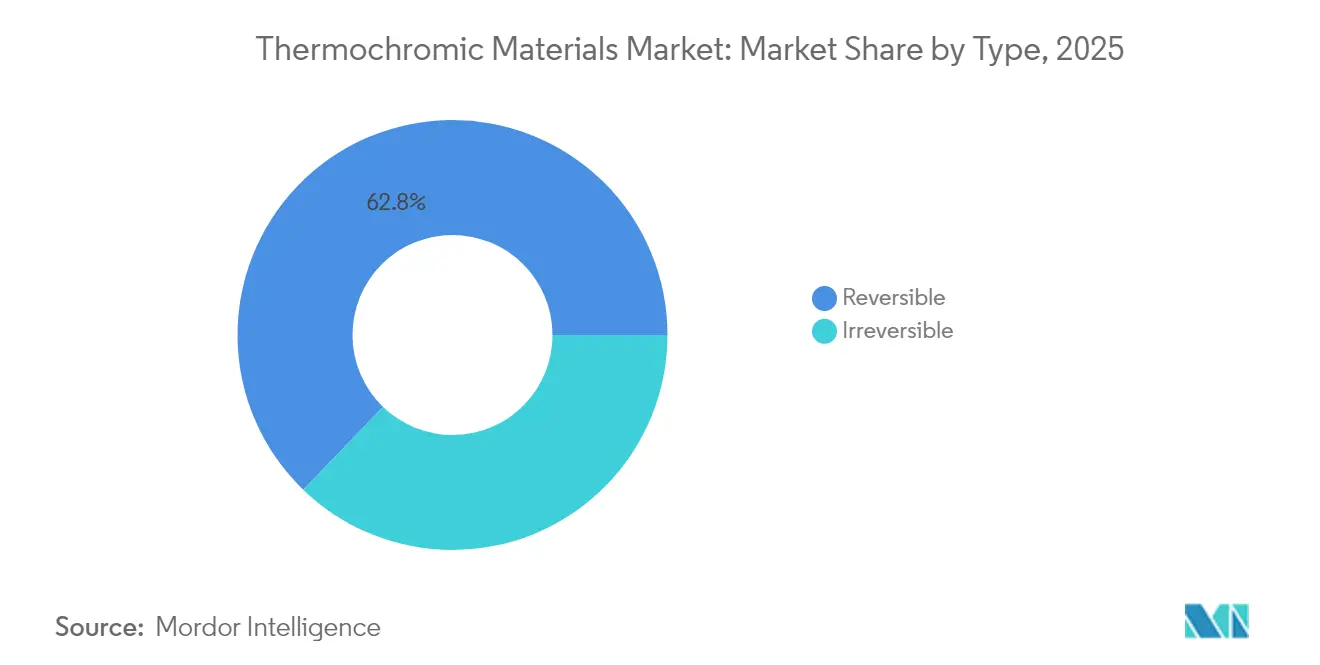

- By type, reversible systems held 62.78% of the thermochromic materials market share in 2025, while irreversible systems are forecast to post the highest 6.39% CAGR to 2031.

- By material, leuco dyes accounted for 43.72% share of the thermochromic materials market size in 2025; hybrid capsules are set to grow the quickest at 6.78% CAGR through 2031.

- By application, roof coatings led with 27.54% revenue share in 2025; the broader “other applications” basket, including battery sensing and wearables, is projected to advance at 6.92% CAGR by 2031.

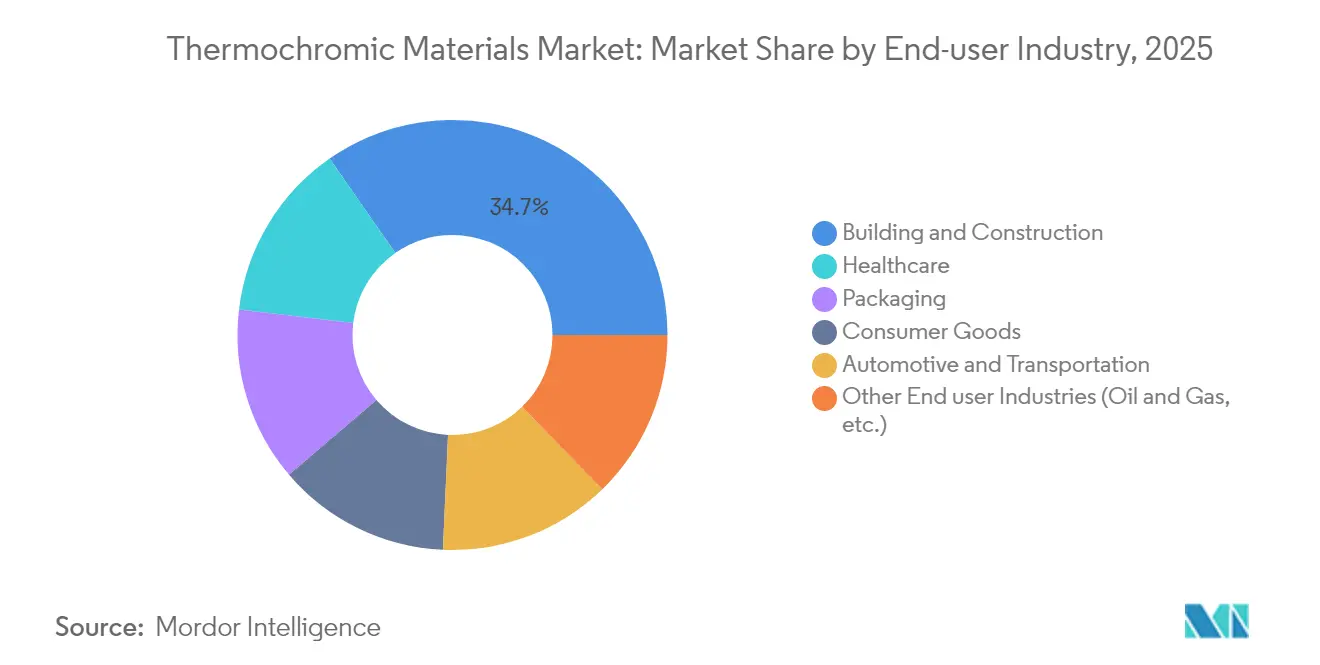

- By end-user industry, building and construction dominated with a 34.68% share in 2025, whereas healthcare is expected to record the fastest 6.62% CAGR to 2031.

- By geography, Asia-Pacific captured 41.12% of global demand in 2025 and is on track for a 5.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermochromic Materials Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cool-roof energy-saving mandates | +1.2% | North America, Europe, and expanding to APAC | Medium term (2-4 years) |

| Packaging anti-counterfeit regulations | +0.8% | Global, with emphasis on the EU and North America | Short term (≤ 2 years) |

| Printable smart-label adoption in retail | +0.6% | Global, led by developed markets | Medium term (2-4 years) |

| Rapid cost decline in micro-encapsulation | +0.9% | Global manufacturing centers in APAC | Long term (≥ 4 years) |

| Emerging demand from battery thermal sensing | +0.7% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cool-roof Energy-saving Mandates Drive Market Expansion

Compliance measures such as California’s Title 24 move thermochromic materials from niche to mainstream building supplies. Dynamic pigments allow a single coating to switch from dark gray to white at 25 °C, generating 20% to 30% yearly HVAC savings in field trials. European and Asian regulators are drafting parallel roof standards that mirror the solar-reflectance and emissivity thresholds already codified in the United States, anchoring long-term demand for color-adaptive roof finishes that curb peak electricity loads and shrink carbon footprints.

Packaging Anti-counterfeit Regulations Accelerate Adoption

Globally harmonized rules for pharmaceutical and food security labeling are steering brands toward inks that reveal tampering or temperature abuse. Thermochromic features satisfy those mandates while meeting EU Regulation 1935/2004 limits on migratory substances[1]EUR-Lex, “Regulation (EC) No 1935/2004 on Materials and Articles Intended to Come into Contact with Food,” eur-lex.europa.eu. Higher product integrity combined with simplified authentication workflows justifies premium pricing, translating directly into added value for label converters facing cost pressures.

Printable Smart-label Adoption Transforms Retail Applications

Retailers have begun embedding touch-activated patches and cold-chain indicators onto everyday goods, turning packages into informational surfaces. UV-curable formulations that remain stable during flexographic runs now enable high-volume output without sacrificing adhesion. These interactive labels deepen shopper engagement and deliver instant quality validation, spurring repeat orders across beverages, meat, and dairy aisles.

Rapid Cost Decline in Micro-encapsulation Technology

Microfluidic encapsulation lines are hitting 99% efficiency, lowering waste while extending pigment lifetime by shielding leuco dyes from oxygen and moisture. Formaldehyde-free polyurethane-urea shells further comply with food-contact rules yet retain thermal stability, narrowing the historical 3 to 5 times cost gap with conventional pigments and broadening access for budget-constrained users.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High formulation cost versus conventional pigments | -1.1% | Global, particularly impacting price-sensitive markets | Short term (≤ 2 years) |

| Photo- and thermo-fatigue limiting lifetime | -0.8% | Global, especially outdoor applications | Medium term (2-4 years) |

| Restricted food-contact approvals in EU and US | -0.6% | Europe and North America, with regulatory spillover effects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Formulation Cost Versus Conventional Pigments

A single kilogram of thermochromic powder can cost three to five times as much as a standard inorganic pigment, constraining usage in large-surface projects such as exterior façades. Process scaling and rising encapsulation yields are easing this premium, yet an upfront price hurdle endures for budget-driven buyers in emerging economies.

Photo and Thermo-fatigue Limiting Lifetime Performance

Ultraviolet exposure and repetitive heating cycles gradually break down molecular leuco dye structures, reducing switch contrast within months on south-facing façades. Research and development groups are testing hybrid shells infused with UV absorbers, but such upgrades make formulation complexity, and thus cost, even higher, tempering near-term volume growth for exterior paints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Reversible Systems Sustain Market Leadership

Reversible systems contributed 62.78% of the thermochromic materials market in 2025 and continue to command attention because they endure thousands of switch cycles with minor chromatic drift. Such resilience underpins temperature labels for reusable containers and smart textiles that must react with every wear. Premium encapsulation films now shield leuco dyes from oxygen, retaining vivid hues beyond 10,000 heating-cooling rounds, a notable leap over prior generations.

Irreversible materials, although representing a smaller slice, are slated for 6.39% CAGR as brand owners adopt “once-only” color reveals for tamper evidence in pharmaceuticals and frozen-food logistics. Increased durability expectations motivate formulators to test bio-based shells and nano-additives that suppress fatigue without elevating cost. The thermochromic materials market benefits as reversible offerings migrate into consumer-oriented products such as mood-changing ceramics and interactive notebooks. Several appliance makers are also piloting reversible panels for stovetop safety cues, broadening application breadth and deepening volume potential.

By Material: Leuco Dyes Maintain Dominance Through Cost-effectiveness

Leuco dye chemistry accounted for 43.72% of total demand in 2025, thanks to its mature supply chain and competitive unit pricing. Ongoing adoption of formaldehyde-free shell systems means leuco dyes now meet stringent contact and emission caps in Europe and North America while preserving color-transition sharpness. In turn, hybrid capsules blend leuco dyes with liquid crystals or photochromic molecules to extend the activation window, drawing a projected 6.78% CAGR to 2031.

Liquid crystals sustain a niche for high-precision thermography tools where 0.1 °C resolution is mandatory, yet their comparatively high price constrains mass-market penetration. Pigment-based inorganic solutions hold steady in ceramic glazes and plastics that need specific shade stability. Collectively, these material tiers empower formulators to select fit-for-purpose chemistries, supporting the thermochromic materials market’s breadth without compromising specialized performance.

By Application: Roof Coatings Lead Energy Efficiency Drive

Roof coatings delivered 27.54% of 2025 sales as regional building codes embraced dynamic reflectance metrics. Documented energy savings up to 11% annually continue to sway architects and facility managers toward thermochromic topcoats. The thermochromic materials market size for roof coatings is expected to expand at a healthy clip as Title 24-type provisions proliferate beyond the United States.

A wider “other applications” category covering battery thermal mapping, wearables, and smart car interiors is set for a 6.92% CAGR. Interactive labels remain essential in security printing, whereas cosmetics firms deploy color-switch balms to enrich the user experience. These collective niches illustrate how the thermochromic materials market capitalizes on both functional and aesthetic triggers to maintain momentum.

By End-User Industry: Building and Construction Dominates Through Regulatory Support

Building and construction consumed 34.68% of the 2025 demand, making the sector the principal revenue anchor. Passive daytime radiative cooling layers that rely on thermochromic pigments lower indoor temperature peaks without mechanical systems, an attractive value driver for LEED and BREEAM builders. Although healthcare holds just a smaller base, it carries the swiftest 6.62% CAGR because fever-strip makers and wearable patch developers boost volumes.

Packaging players deploy heat-sensitive inks on drug blister packs and perishable foods, ensuring temperature compliance along multi-node supply lines. Consumer goods persist as a vibrant outlet, ranging from novelty toys to color-changing mugs, reinforcing end-user diversity that cushions the thermochromic materials industry from sector-specific swings.

Geography Analysis

Asia-Pacific retained leadership with 41.12% share in 2025 as China supplied cost-effective bulk volumes and India adopted smart inks for pharmaceuticals and automotive interiors. The thermochromic materials market size in Asia-Pacific is forecast to advance at 5.97% CAGR to 2031, abetted by electric-vehicle battery sensing demand across regional gigafactories. Japan funnels research and development into liquid-crystal solutions that command premium prices for laboratory diagnostic kits, demonstrating that high-tech and mass-volume segments can coexist within one geography.

North America sustains demand momentum on the back of Title 24-like building codes, stringent food-safety labeling, and consumers who value interactive packaging. Domestic formulators continue to refine formaldehyde-free shells to meet forthcoming FDA guidance while preserving vivid color transitions. Europe follows close behind, driven by its Green Deal agenda and urban retrofits that integrate adaptive façade coatings, whereas Middle-East and Africa, and South America show incremental uptake as construction booms and retail chains scale cold-chain operations.

Collectively, regional dynamics underscore that the thermochromic materials market remains both supply-centered, owing to APAC cost advantages, and compliance-centered, owing to Western regulatory drivers. This duality enables cross-regional technology transfer yet sustains price differentials that shape buyer sourcing strategies.

Regulatory Landscape

Thermochromic material suppliers selling into Europe operate under the EU REACH framework administered by the European Chemicals Agency (ECHA), so substance selection and documentation are central for microencapsulated dyes and binder systems used in inks, coatings, plastics, and cosmetics. In February 2026, ECHA expanded the SVHC Candidate List to 253 entries, increasing the need for ongoing composition screening, updated safety data sheets, and substitution roadmaps when regulated chemistries appear in color formers, developers, solvents, or additives used in thermochromic systems.

Microencapsulation and polymeric shell chemistries also intersect with EU action on synthetic polymer microparticles. In June 2026, Commission Regulation (EU) 2026/1168 amended REACH Annex XVII by refining restrictions related to placing synthetic polymer microparticles on the market, which is relevant where thermochromic performance depends on microencapsulated particles and dispersion stability. In parallel, ISO standardization through ISO/TC 256 (pigments, dyestuffs and extenders) supports cross-border qualification by aligning terminology and test methods for pigments and dyestuffs used in thermochromic pigment and ink grades.

Value Chain Analysis

The value chain starts upstream with specialty organic intermediates and synthesis of leuco dye systems (color former, developer, solvent), alongside polymer and additive inputs used for microencapsulation shells and UV stabilization. The midstream is defined by encapsulation and pigment manufacture, where precision processing, including high-yield encapsulation, drives reversibility, cycling stability, and moisture and oxygen resistance. Producers then compound concentrates into inks, pastes, and plastic masterbatches for converting processes such as flexography, screen printing, and inkjet.

Downstream, formulators and converters integrate thermochromic concentrates into roof coatings, security and smart labels, cosmetics, textiles, and industrial indicators, then sell through coating companies, label converters, and packaging suppliers serving regulated end markets such as food and pharmaceuticals. Qualification and compliance testing, including migration, durability, and restricted-substance screening, regularly shape lead times and supplier selection, particularly for food-contact and healthcare monitoring products with stringent documentation requirements. Asia-Pacific remains anchored for bulk pigment and capsule output, while higher-margin application engineering and conversion capabilities are concentrated among specialty ink, label, and indicator companies that co-develop performance targets with brand owners.

Competitive Landscape

The thermochromic materials market is moderately fragmented, with proprietary encapsulation skill sets acting as natural barriers to entry. Chromatic Technologies concentrates on fast-switch inks tailored for high-speed label presses, while Asian newcomers pursue scale efficiencies in leuco dye powders. Patent filings around microfluidic encapsulation and bio-based shells reveal intense research and development jockeying, signaling that intellectual property rather than brute volume will decide future leadership stakes. Strategic partnerships between pigment suppliers and smart-label converters are spreading risk and accelerating time-to-market for niche applications like battery heat maps and medical patches.

Thermochromic Materials Industry Leaders

Chromatic Technologies Inc.

Hali Pigment Co. Ltd

SpotSee

OliKrom

RPM International Inc. (Rust-Oleum)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven applications in building envelopes and packaging continue to create whitespace for thermochromic systems that balance durability, low migration, and process compatibility. Cool-roof mandates and code-driven performance metrics keep roof coatings as a high-volume outlet, but adoption depends on addressing photo- and thermo-fatigue and improving outdoor lifetime. That shift is pushing producers toward hybrid capsule designs and formaldehyde-free shell systems already referenced in industry formulation roadmaps. On the packaging side, anti-counterfeit and cold-chain integrity requirements are translating into more frequent use of printable indicators and smart labels that can be authenticated and logged in workflows, sustaining demand for inks that handle high-speed converting while keeping a sharp color transition.

A second opportunity track is the move from passive indicators to connected monitoring and data workflows, particularly in life-sciences logistics where temperature, tilt, and shock events link to claims handling and quality release. This is supported by company actions such as SpotSee expanding QR-enabled monitoring products, including FreezeSafe QR, TiltWatch XTR QR, and ShockWatch Label QR, and partnering across the shipment-visibility ecosystem. In materials innovation, smart-window research increasingly emphasizes function-oriented thermochromic films and coatings, with transition kinetics and solar modulation performance engineered using specialized design tools; this supports a shift from novelty color change toward more quantified building outcomes such as energy and comfort.

Recent Industry Developments

- April 2026: SpotSee expanded its QR-enabled monitoring portfolio with FreezeSafe QR, TiltWatch XTR QR, and ShockWatch Label QR. The releases extend connected identification and data capture across multiple handling and temperature-abuse scenarios, strengthening adoption in logistics workflows that require traceability rather than standalone visual indicators.

- April 2025: SpotSee acquired Telatemp, expanding its condition-monitoring portfolio in life sciences. The deal broadened product coverage across temperature and handling indicators, supporting more bundled offerings to pharmaceutical shippers and cold-chain stakeholders.

- July 2024: Merck KGaA finalized the divestiture of its Surface Solutions unit, including thermochromic pigment solutions, to Global New Material International for USD 721 million. The ownership shift repositioned thermochromic pigment assets within a materials-focused portfolio, influencing supplier strategies and potential investment priorities for specialty pigment capabilities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers materials and formulations that intentionally change color with temperature change, and the value captured reflects sales of these thermochromic materials into commercial uses across industries.

Scope exclusions: The sizing excludes downstream finished products where the thermochromic effect is only an embedded feature and the thermochromic material value cannot be separated credibly.

Segmentation Overview

- By Type

- Reversible

- Irreversible

- By Material

- Liquid Crystal

- Leuco Dyes

- Pigments

- Other Materials (Hybrid Capsules, etc.)

- By Application

- Roof Coatings

- Printing

- Food Packaging

- Cosmetics

- Other Applications (Textiles and Fashion, etc.)

- By End-User Industry

- Building and Construction

- Packaging

- Consumer Goods

- Automotive and Transportation

- Healthcare

- Other End user Industries (Oil and Gas, etc.)

- By Geography

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public data that helps us set realistic boundaries on where thermochromic materials are actually used and sold. We reviewed sources such as USITC trade data for relevant chemical and pigment categories, the US Census Bureau and Eurostat for packaging and coatings activity indicators, and World Bank and OECD industrial output series to anchor macro demand movement.

To keep assumptions grounded, we also referred to sources such as USPTO and other patent databases to understand technology direction, plus open information from company annual reports, investor presentations, association websites, and reputable press. Where needed, paid subscriptions for company financials and news intelligence were used to cross-check business mix hints and timing of capacity or product announcements. These sources are illustrative, and many additional public references were used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Field validation was built through expert calls and structured surveys with material suppliers, compounders, ink and coating formulators, converters, and downstream buyers that specify thermochromic content in products. For a global market like this, we purposely covered APAC, EMEA, and the Americas so regional application pull (packaging, printing, coatings, and consumer goods) could be checked before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 41% |

| Mid tier: 57% | Functional/Unit leaders: 41% | EMEA: 32% |

| Smaller Players: 14% | Managers: 45% | Americas: 27% |

Market-Sizing & Forecasting

The sizing uses a top-down and bottom-up approach, where end use activity and adoption logic are first used to reconstruct demand, and then supplier side checks are applied to keep totals realistic. For top-down, we built demand pools around packaging and printing volumes, coatings activity, and consumer goods output, and then applied thermochromic penetration and typical loading rates for inks, coatings, and plastics. Because the same application can use different chemistries, the mix was adjusted using interview feedback on reversible versus irreversible usage and on leuco dye and liquid crystal prevalence.

For bottom-up corroboration, we used selective roll-ups from a sample of suppliers and formulators using public revenue cues, product mix statements, and approximate ASP ranges discussed in interviews. Where a company did not disclose thermochromic specific revenue, gaps were handled by mapping capacity signals and application exposure to a reasonable share band, which is then normalized to regional demand indicators.

Forecasts were built using scenario analysis supported by simple regression checks on the strongest drivers, including packaging output growth, construction and refurbishment activity linked to coatings, consumer goods manufacturing trends, and expected ASP progression as scale improves. Assumptions were re-tested with experts when a driver changed sharply, so the final curve stayed believable and easy to trace.

Data Validation & Update Cycle

Outputs were validated through several passes, starting with internal variance checks across regions, chemistry mix, and application splits, and then moving to external sense checks against independent signals such as packaging volumes, coatings demand indicators, and trade movement for adjacent pigment and chemical categories. If a region showed an abnormal jump, we revisited the penetration, loading rate, and pricing assumptions, and then re-contacted selected respondents to confirm what changed.

Before sign-off, the model is reviewed by another analyst to ensure the math ties out and the assumptions match the written scope. The report is refreshed annually, and interim updates are triggered when there are material events such as meaningful capacity additions, regulation shifts affecting chemical use, or large demand swings in packaging and coatings. Right before delivery, a final review is done so clients receive the latest updated view.

Mordor Intelligence's Thermochromic Material Market Size Compared With Other Published Estimates

Published market numbers for thermochromic materials can look far apart, even when the topic label seems the same. Differences usually come from what is counted as the market, which year is treated as the starting point, and how demand is validated across packaging, printing, coatings, and other uses.

Packaging output signals, coatings activity indicators, and cross-checks on chemistry level adoption are the evidence points that keep Mordor Intelligence aligned to the sell-in value of thermochromic materials rather than the broader value of finished smart products. A second driver is how pricing and mix are moved forward, since some estimates assume faster ASP expansion or include adjacent color-change technologies that do not rely on thermochromic response.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.64 B (2025) | |

| Global Consultancy A | USD 2.30 B (2024) | Uses an earlier base year and a broader application story without clearly separating thermochromic material sell-in from downstream product value, which can pull the starting point lower depending on what is excluded. |

| Industry Publisher B | USD 1.96 B (2025) | Leans on limited disclosure of scope and can undercount when liquid crystal and specialty pigment uses are treated conservatively, plus the application mapping is less explicit for printing inks and coatings. |

The spread in the table is mostly explained by year alignment and by whether the revenue is counted at the material level or closer to the finished product level. By sticking to clear application demand pools, realistic penetration and loading rates, and repeatable validation checks, we end up with a market value that is easier to track and update as conditions change.

Key Questions Answered in the Report

What is the current size of the thermochromic materials market?

Thermochromic materials market size hit USD 2.77 billion in 2026 and is projected to reach USD 3.56 billion by 2031.

Which region leads the thermochromic materials market?

Asia-Pacific holds the largest 41.12% share and is also the fastest-growing region at 5.97% CAGR through 2031.

Why are reversible thermochromic systems so prevalent?

They account for 62.78% market share because they endure thousands of color cycles, fitting reusable labels, textiles, and interactive packaging.

What is driving thermochromic adoption in construction?

Cool-roof mandates such as California’s Title 24 require dynamic heat-management coatings, making thermochromic roof layers a compliance solution that can cut annual cooling loads by up to 30%.

Which end-user industry shows the fastest growth?

Healthcare applications, including wearable fever sensors, are advancing at 6.62% CAGR through 2031 due to rising demand for real-time, non-invasive patient monitoring.

Page last updated on: