Intelligent PDU Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.52 Billion |

| Market Size (2030) | USD 5.53 Billion |

| Growth Rate (2025 - 2030) | 3.52% CAGR |

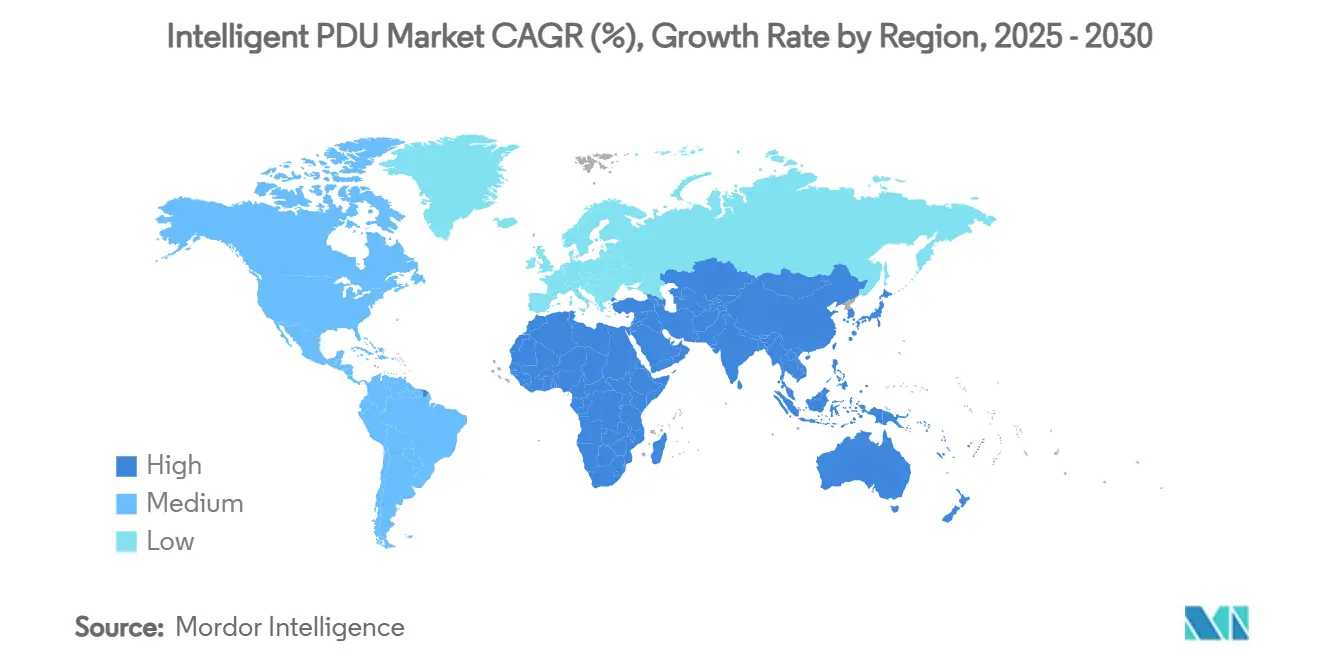

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intelligent PDU Market Analysis by Mordor Intelligence

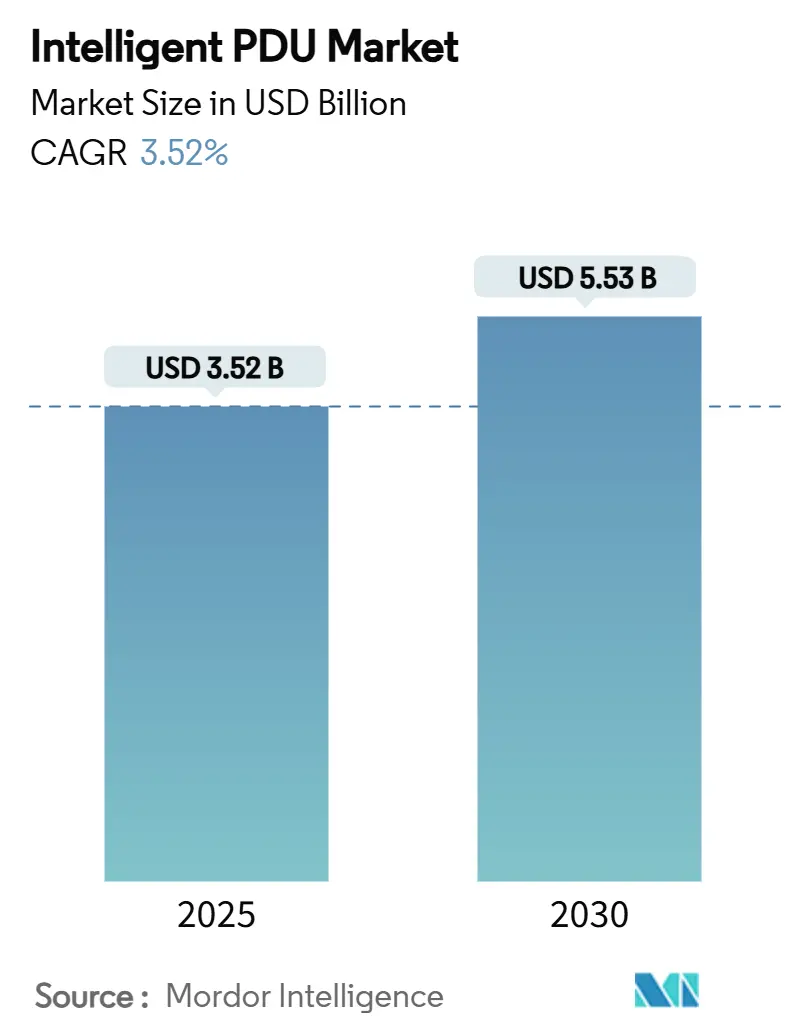

The intelligent PDU market size is USD 3.52 billion in 2025 and is forecast to reach USD 5.53 billion by 2030, reflecting a 9.44% CAGR. Rapid uptake of AI-ready data centers, the migration from single- to three-phase rack power, and enterprise-wide energy-efficiency mandates are amplifying demand for intelligent, networked power distribution that combines metering, switching, and predictive analytics. Growth is reinforced by rising rack power densities that now exceed 30 kW in many hyperscale deployments, outpacing the capabilities of legacy basic PDUs. Cyber-hardened features, hot-swap designs, and advanced carbon-reporting functions have become decisive purchasing criteria as operators align with ESG reporting rules in the European Union and North America. [1]European Commission, “Commission adopts EU-wide scheme for rating sustainability of data centres,” energy.ec.europa.eu The intelligent PDU market is also benefitting from strategic vendor moves, such as Schneider Electric’s USD 700 million U.S. investment plan and Eaton’s USD 1.4 billion Fibrebond acquisition, aimed at broadening turnkey power-distribution offerings.

Key Report Takeaways

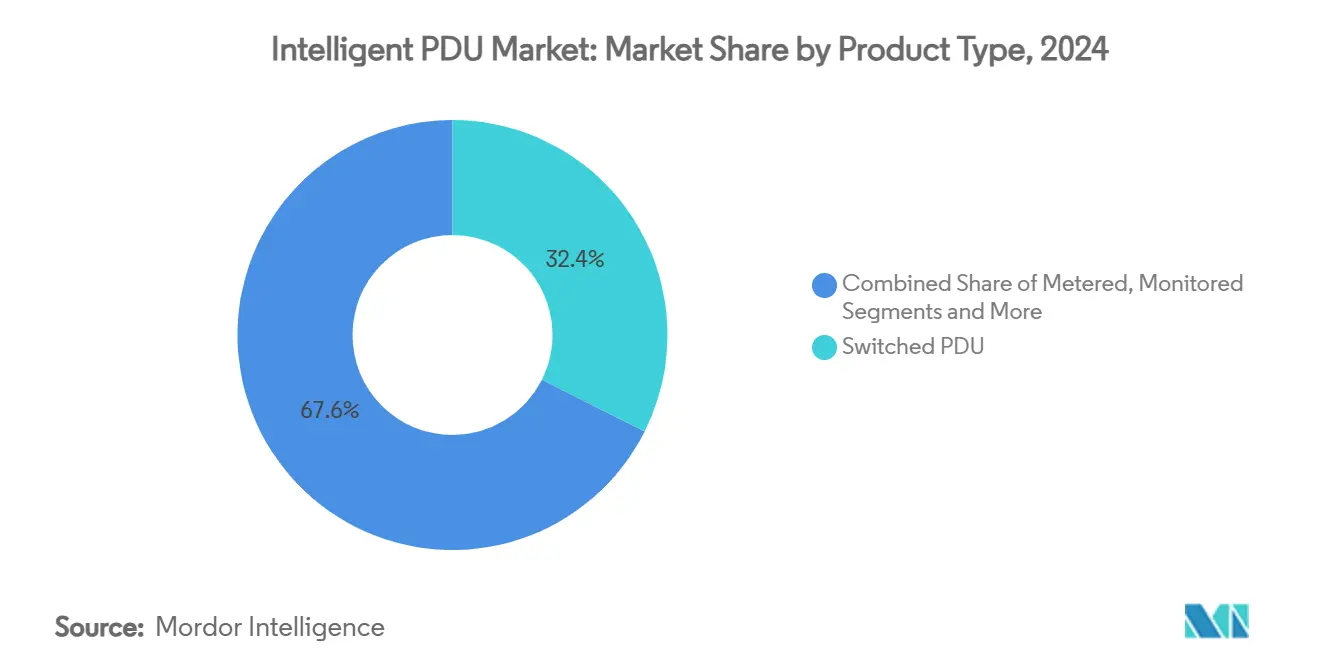

- By product type, switched PDUs accounted for 32.4% revenue share of the intelligent PDU market size in 2024, while hot-swap PDUs are projected to expand at a 9.8% CAGR to 2030.

- By power phase, three-phase architecture held 60.5% of the intelligent PDU market share in 2024 and is forecast to grow at 9.6% CAGR through 2030.

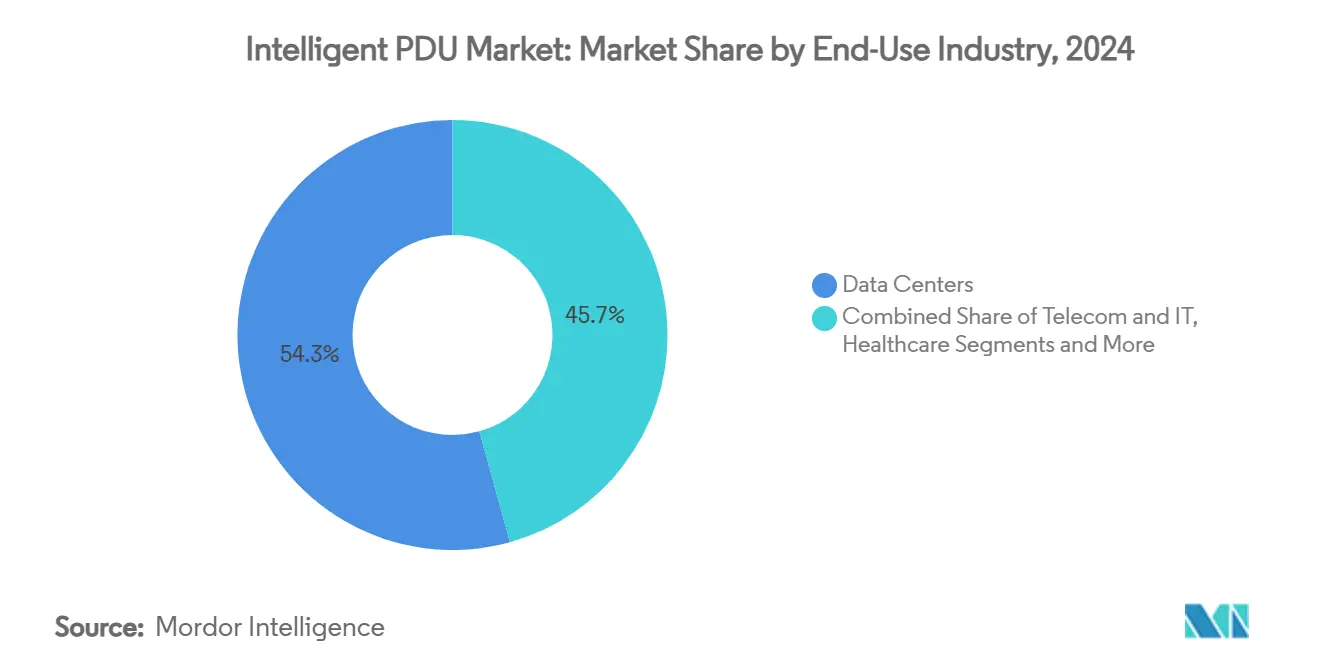

- By end-use, data centers commanded 54.3% share of the intelligent PDU market size in 2024; AI-driven hyperscale facilities are advancing at a 9.6% CAGR to 2030.

- By form factor, rack-mounted units represented 78.4% of the intelligent PDU market share in 2024 and are growing at 10.4% CAGR through 2030.

- By geography, North America led with 37.2% share in 2024, while Asia Pacific is expected to deliver a 9.9% CAGR to 2030.

Global Intelligent PDU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of hyperscale data centers | +2.1% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Rising rack power densities (>30 kW) needing outlet-level monitoring | +1.8% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Enterprise energy-efficiency & PUE-reduction initiatives | +1.3% | Global, strongest in EU due to EED mandates | Long term (≥ 4 years) |

| Shift from single- to three-phase rack power architectures | +1.1% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| AI workload demand for sub-cycle power-quality analytics | +1.7% | North America, expanding globally | Short term (≤ 2 years) |

| ESG-driven rack-level carbon reporting mandates | +1.4% | Europe & North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Hyperscale Data Centers

Hyperscale operators are rolling out AI-optimized sites that require power densities equivalent to 1,000 homes in one rack, compelling a shift toward intelligent PDUs with granular monitoring, automated load balancing, and advanced thermal analytics. Three-phase configurations dominate these deployments, allowing efficient distribution while simultaneously supporting mixed-voltage IT loads. Vendors now bundle sub-cycle analytics and hot-swap metering boards to satisfy uptime obligations and reduce manual intervention. These functionalities lower stranded capacity and improve ROI for hyperscale owners that pursue aggressive energy-efficiency targets.

Rising Rack Power Densities Needing Outlet-Level Monitoring

AI training clusters pushing 40–140 kW per rack have eclipsed standard data-center designs, making outlet-level current and power-factor monitoring indispensable. Intelligent PDUs spot overload trends in real time, enabling capacity planners to rebalance phases before breakers trip. Coupled with liquid cooling, PDUs feed telemetry to DCIM tools that orchestrate fan speed, coolant flow, and workload placement. The resulting insights avert unplanned outages and extend equipment life.

Enterprise Energy-Efficiency & PUE-Reduction Initiatives

EU sustainability rules require large data centers to disclose PUE, CER, CUE, and WUE metrics each year beginning 2024, forcing operators to embed high-resolution metering at the rack. Intelligent PDUs collect outlet-level data that feeds live dashboards, allowing facilities to shave energy waste and benchmark sites globally. As utility costs escalate, CFOs increasingly factor PDU-enabled savings into capital-budget cycles, stimulating uptake across colocation, telecom, and enterprise segments.

Shift from Single- to Three-Phase Rack Power Architectures

Data centers are upgrading to three-phase power that supplies 1.7 times more capacity per circuit while maintaining dual-voltage compatibility. Intelligent PDUs police phase balance continuously, preventing breaker trips and UPS inefficiencies. Alternating-phase outlets simplify cord routing, boost airflow, and reduce cable bulk. As rack densities rise, the TCO gap versus single-phase widens, driving rapid migration in North America and Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost versus basic PDUs | -1.2% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Absence of unified cybersecurity standards for networked PDUs | -0.8% | Global, critical in regulated industries | Medium term (2-4 years) |

| Semiconductor metering-IC supply constraints | -0.6% | Global, concentrated in APAC manufacturing hubs | Short term (≤ 2 years) |

| Thermal limits of legacy racks for high-density iPDU retrofits | -0.4% | North America & Europe, mature data center markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Basic PDUs

Intelligent models fetch 3–5 times the price of basic units, straining budgets for small enterprises. While lower downtime and energy savings improve lifecycle economics, payback horizons can exceed three years in price-sensitive regions. Vendors now tout subscription models and metered-energy rebates to soften capex headwinds, but adoption in emerging markets remains tempered.

Absence of Unified Cybersecurity Standards for Networked PDUs

Hard-coded credentials and firmware flaws have surfaced across major brands, leaving more than 100,000 units exposed on public networks. Without an industry-wide benchmark akin to IEC 62443, buyers must perform vendor-by-vendor audits, elongating procurement cycles. UL 2900 certification is gaining traction yet covers only a subset of models, underscoring the need for harmonized guidance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Switched PDUs Lead Market Evolution

Switched designs captured 32.4% of the intelligent PDU market share in 2024 through remote on-off control that minimizes on-site maintenance. The ability to script outlet sequencing supports graceful server restarts, slashing mean-time-to-repair. Hot-swap PDUs are climbing at 9.8% CAGR as zero-downtime maintenance becomes table stakes for colocation SLAs. Combined monitoring-switching hybrids blur traditional categories, with Server Technology’s CWG series now accounting for 40% of the company’s revenue following its patent victory. ATS PDUs re-enter the spotlight as cloud operators add redundant feeds to meet Tier IV design goals.

Next-generation firmware integrates RESTful APIs that align with cloud-native observability stacks, enabling real-time power orchestration. Edge deployments favor compact switched units that fit wall-mount enclosures yet retain full SNMP and Syslog support. As software control wins mindshare, basic metered models see flat demand confined to cost-sensitive small offices.

By Power Phase: Three-Phase Architecture Dominance

Three-phase units accounted for 60.5% of the intelligent PDU market size in 2024 and are expanding at 9.6% CAGR through 2030 as AI-centered racks exceed 30 kW load. Their superior amperage distribution reduces conductor count by one-third, cutting copper costs and airflow obstruction. Advanced models leverage alternating-phase outlet layouts that equalize voltage drop across chassis, improving efficiency. Single-phase PDUs persist in edge closets and branch offices where loads stay under 10 kW, yet their share declines each refresh cycle.

Liquid-cooling manifolds and rear-door heat exchangers demand slimline power strips, a niche addressed by three-phase zero-U PDUs with HDOT outlets. Manufacturers tout RFID-tagged breakers that pair with digital twins, enabling phase-realignment suggestions surfaced in DCIM dashboards. This closed-loop visibility lowers neutral-conductor overheating and extends UPS runtime during transfer events.

By End-Use Industry: Data Centers Drive AI Transformation

Data centers retained 54.3% of the intelligent PDU market size in 2024, and hyperscale AI facilities are accelerating at 9.6% CAGR as trillion-parameter models enter production. Telecom operators deploy intelligent PDUs at 5G edge sites, pairing them with compact UPS modules for millisecond failover. Hospitals migrate to networked PDUs meeting NFPA 99, guaranteeing restoration within 10 seconds during outages. [2]Terakraft, “Data Center Design Requirements for AI Workloads,” terakraft.no

Industrial users adopt ruggedized PDUs compliant with MIL STD 810 for plant-floor IIoT nodes. Governments stipulate IEC 60309 twist-lock connectors in defense data centers, spurring demand for specialized enclosures. Energy utilities integrate PDUs with SCADA systems, leveraging outlet telemetry to optimize substation IT loads tied to renewable-energy forecasting.

By Form Factor: Rack-Mounted Solutions Accelerate

Rack-mount designs delivered 78.4% of the intelligent PDU market share in 2024 and are growing at 10.4% CAGR as zero-U strips reclaim vertical rail space. High-density outlet technology raises receptacle count by 20% within the same footprint, essential as mixed GPU-CPU trays multiply. Floor-standing PDUs remain relevant for 50–500 kVA distribution in mega-facilities but cede volume to rack-integrated offerings.

Wall-mount models serve retail edge hubs lacking racks, equipped with conformal-coated boards for dust resistance. Emerging Class 4 fault-managed power systems from Panduit promise 600 W over 2 km, presenting a long-reach alternative to PoE and spurring new enclosure formats.

Geography Analysis

North America maintained 37.2% of the intelligent PDU market share in 2024 thanks to early AI adoption, abundant hyperscale capital, and state incentives for clean-energy data centers. Enterprise focus on carbon disclosures drives extensive PDU retrofit programs that feed ESG dashboards. [3]Schneider Electric, “Schneider Electric Plans to Invest Over $700 million in the U.S.,” se.comCanada’s cold climate attracts new hyperscale campuses, magnifying demand for three-phase rack strips compatible with medium-voltage feeds.

Asia Pacific is the fastest-growing region at 9.9% CAGR as governments underwrite smart-city and cloud-first agendas that aim to double regional data-center capacity within five years. China’s Tier 2 cities roll out industrial-internet zones with in-rack PDUs tied to microgrid controllers. India’s new data-localization rules spur colocation builds that default to intelligent metered-switching combos. Singapore’s moratorium easing anchors sustainable designs with liquid-cooling and high-density racks.

Europe follows with robust growth driven by the Energy Efficiency Directive and carbon-border-adjustment measures that prioritize granular metering. Operators retrofit PDUs capable of CO₂-equivalent reporting to satisfy annual disclosures. Nordic nations leverage abundant renewables to market “green colocation” bundles, coupling intelligent PDUs with free cooling. The Middle East accelerates capacity linked to national AI visions, and operators deploy desert-rated PDUs inside containerized modules resilient to 55 °C ambient temperatures.

Competitive Landscape

The market remains moderately fragmented. Schneider Electric integrates power, cooling, and DCIM in turnkey offers, underpinned by its USD 700 million U.S. expansion program. Vertiv posted 57 % organic orders growth in Q2 2024 and capitalizes on AI workloads via its 360AI architecture. Eaton’s USD 1.4 billion Fibrebond deal unlocks pre-integrated modular power rooms that embed intelligent PDUs at the factory.

Patent litigation underscores IP importance; Server Technology secured USD 10.8 million from Schneider’s APC over vertical-strip metering patents. Panduit pioneers UL 1400-1 Class 4 fault-managed power, carving a niche in long-distance low-voltage distribution. Mil-spec specialist Milpower Source launches hybrid PDU-switch units for defense platforms, demonstrating cross-sector innovation.

Competitive intensity rises as cloud and telco customers demand integrated hardware-software ecosystems over discrete PDUs. Vendors differentiate through AI-driven analytics, cybersecurity certifications, and lifecycle service bundles that guarantee SLA compliance. Consolidation is expected as Tier-2 players seek scale to fund R&D for sub-cycle analytics and zero-trust firmware updates.

Intelligent PDU Industry Leaders

Schneider Electric (APC)

Vertiv Group Corp.

Eaton Corporation plc

Legrand SA (Raritan, Server Technology)

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Schneider Electric announced plans to invest over USD 700 million in the U.S. by 2027, including a new PDU lab focused on AI data-center testbeds.

- March 2025: Eaton agreed to acquire Fibrebond Corporation for USD 1.4 billion, expanding modular power-room offerings.

- December 2024: Schneider Electric unveiled AI-ready power solutions including Galaxy VXL UPS and GB200 NVL72 reference designs with NVIDIA.

- November 2024: Vertiv projected 12–14 % organic sales CAGR to 2029 at its investor day, citing high-density power as a core growth pillar.

Global Intelligent PDU Market Report Scope

| Metered |

| Monitored |

| Switched |

| Automatic Transfer Switch (ATS) |

| Hot-Swap |

| Single-Phase |

| Three-Phase |

| Rack-Mounted |

| Floor / Stand-Alone |

| Wall-Mounted |

| Data Centers |

| Telecom and IT |

| Industrial and Manufacturing |

| Healthcare |

| Energy and Utilities |

| Government and Defense |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Metered | ||

| Monitored | |||

| Switched | |||

| Automatic Transfer Switch (ATS) | |||

| Hot-Swap | |||

| By Power Phase | Single-Phase | ||

| Three-Phase | |||

| By Form Factor / Mounting | Rack-Mounted | ||

| Floor / Stand-Alone | |||

| Wall-Mounted | |||

| By End-Use Industry | Data Centers | ||

| Telecom and IT | |||

| Industrial and Manufacturing | |||

| Healthcare | |||

| Energy and Utilities | |||

| Government and Defense | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the intelligent PDU market?

The intelligent PDU market is valued at USD 3.52 billion in 2025.

How fast is demand for three-phase intelligent PDUs growing?

Three-phase units are forecast to grow at 9.6% CAGR through 2030, outpacing single-phase models.

Which region shows the strongest growth potential for intelligent PDUs?

Asia Pacific leads with a projected 9.9% CAGR to 2030 due to aggressive data-center expansion programs.

Why are switched PDUs preferred over basic metered units?

Switched designs provide remote outlet control, reducing manual site visits and supporting fast service restoration.

How does intelligent PDU adoption support ESG targets?

Intelligent PDUs deliver rack-level energy and carbon metrics, enabling operators to meet regulatory reporting mandates and optimize PUE.

Page last updated on: