Application Delivery Controllers (ADC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

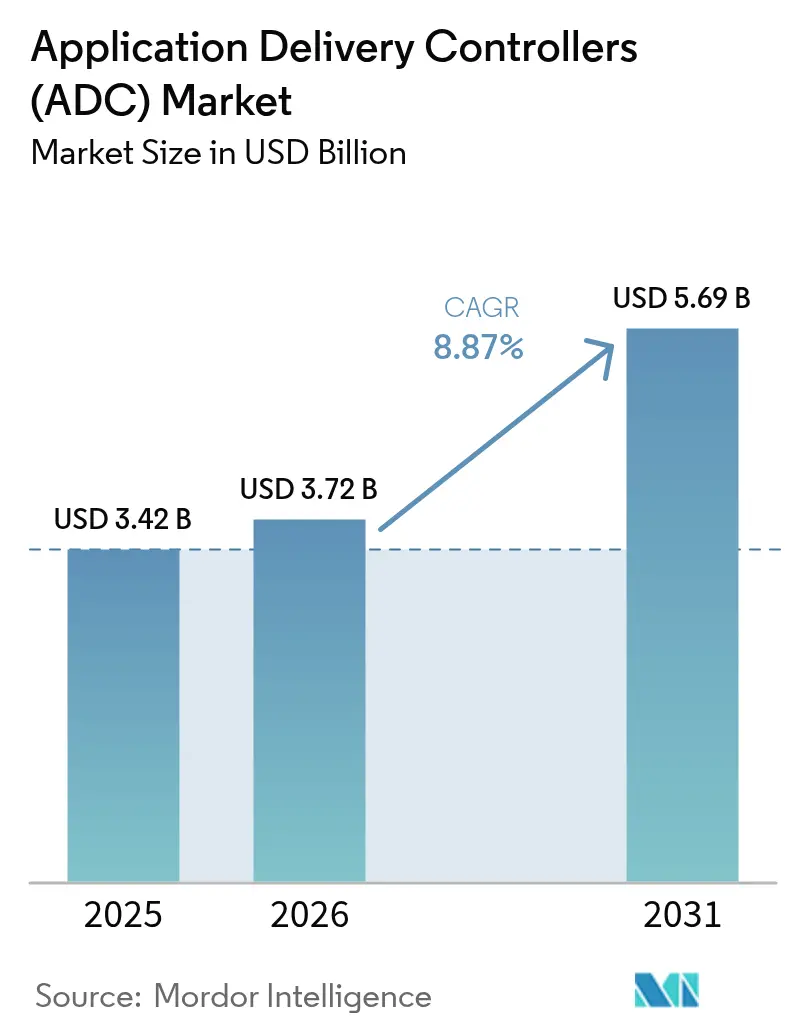

| Market Size (2026) | USD 3.72 Billion |

| Market Size (2031) | USD 5.69 Billion |

| Growth Rate (2026 - 2031) | 8.87% CAGR |

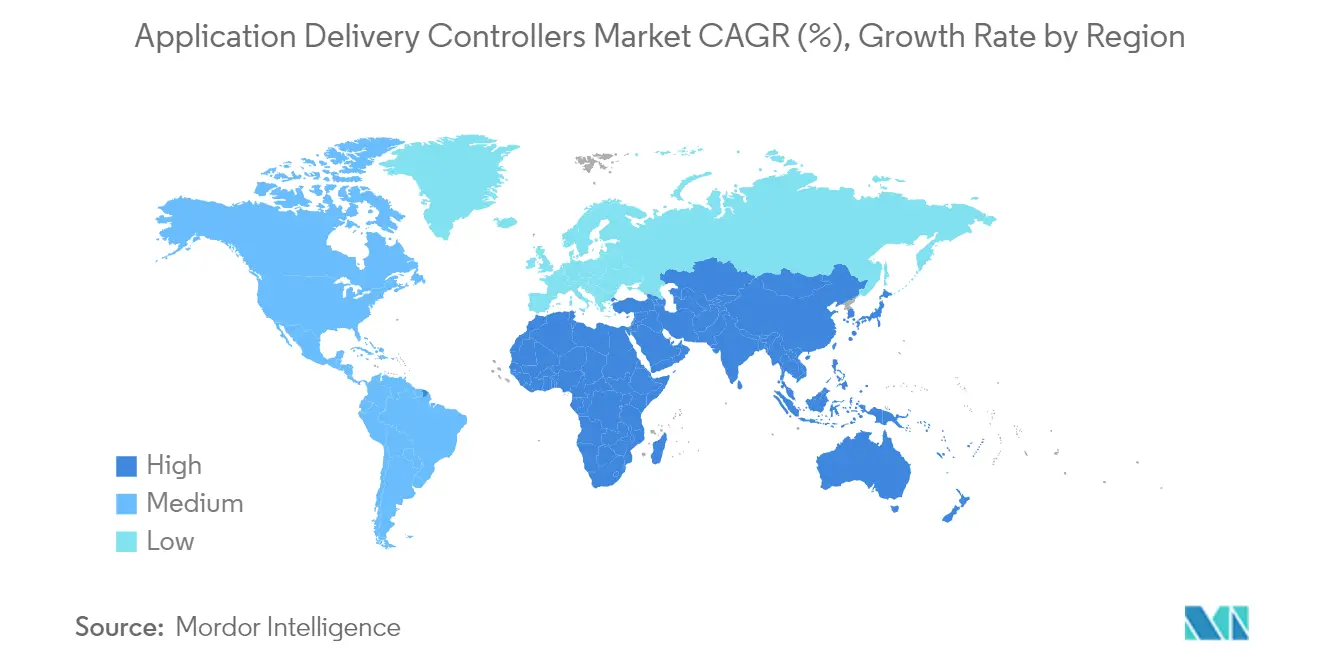

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players_Market_Major_Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Application Delivery Controllers (ADC) Market Analysis by Mordor Intelligence

application delivery controllers market size in 2026 is estimated at USD 3.72 billion, growing from 2025 value of USD 3.42 billion with 2031 projections showing USD 5.69 billion, growing at 8.87% CAGR over 2026-2031. Rapid migration to cloud-native architectures, rising east-west data-center traffic, and persistent multi-cloud strategies keep demand high for intelligent, security-aware traffic‐management platforms. Vendors now bundle advanced Layer-7 security, API protection, and AI-assisted analytics into single offerings, allowing enterprises to improve user experience while containing risk. Hardware appliances still dominate performance-critical workloads, yet virtual and cloud-managed form factors are scaling faster as organizations prioritize agility and consumption-based economics. Regionally, North America leverages mature IT estates and regulatory tailwinds to hold leadership, while Asia-Pacific’s 5G build-outs and digital initiatives create the steepest growth curve.

Key Report Takeaways

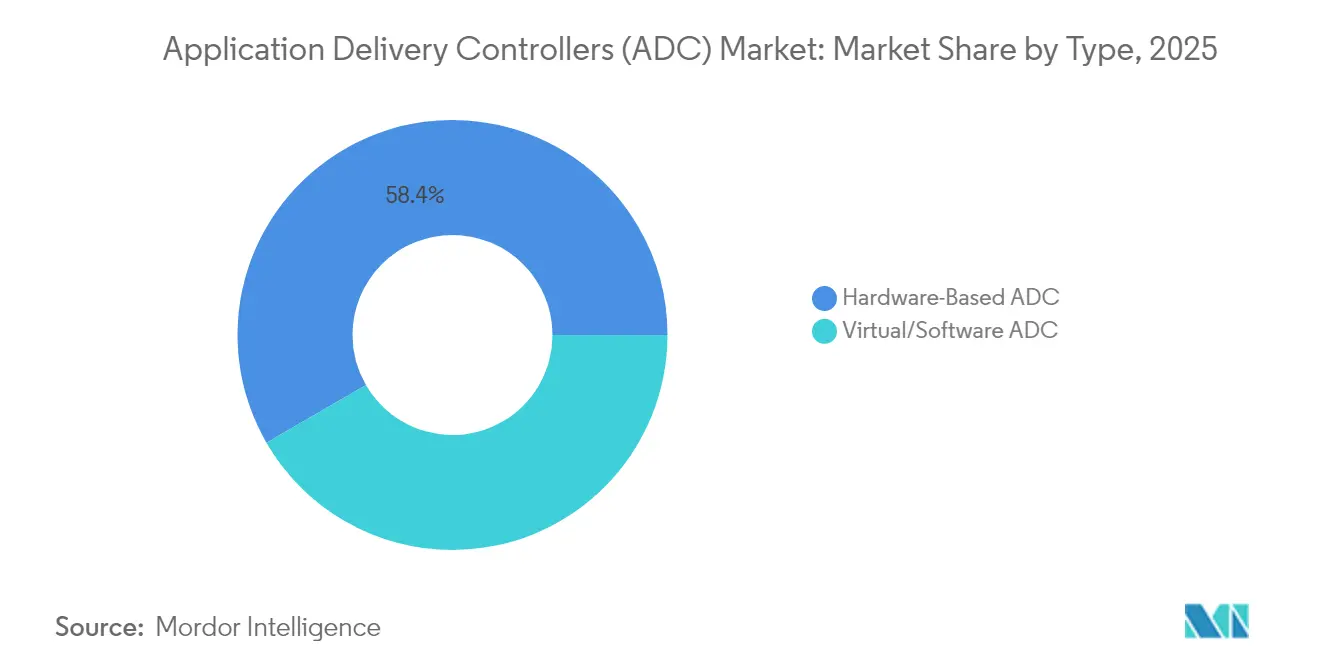

- By type, hardware appliances led with 58.35% of the application delivery controllers market share in 2025; software ADCs are advancing at a 14.12% CAGR to 2031.

- By deployment, on-premise solutions accounted for 63.25% of the application delivery controllers market size in 2025, while cloud-managed/hosted models post the highest 14.68% CAGR through 2031.

- By component, solutions captured 69.40% revenue in 2025; services are forecast to expand at 11.54% CAGR.

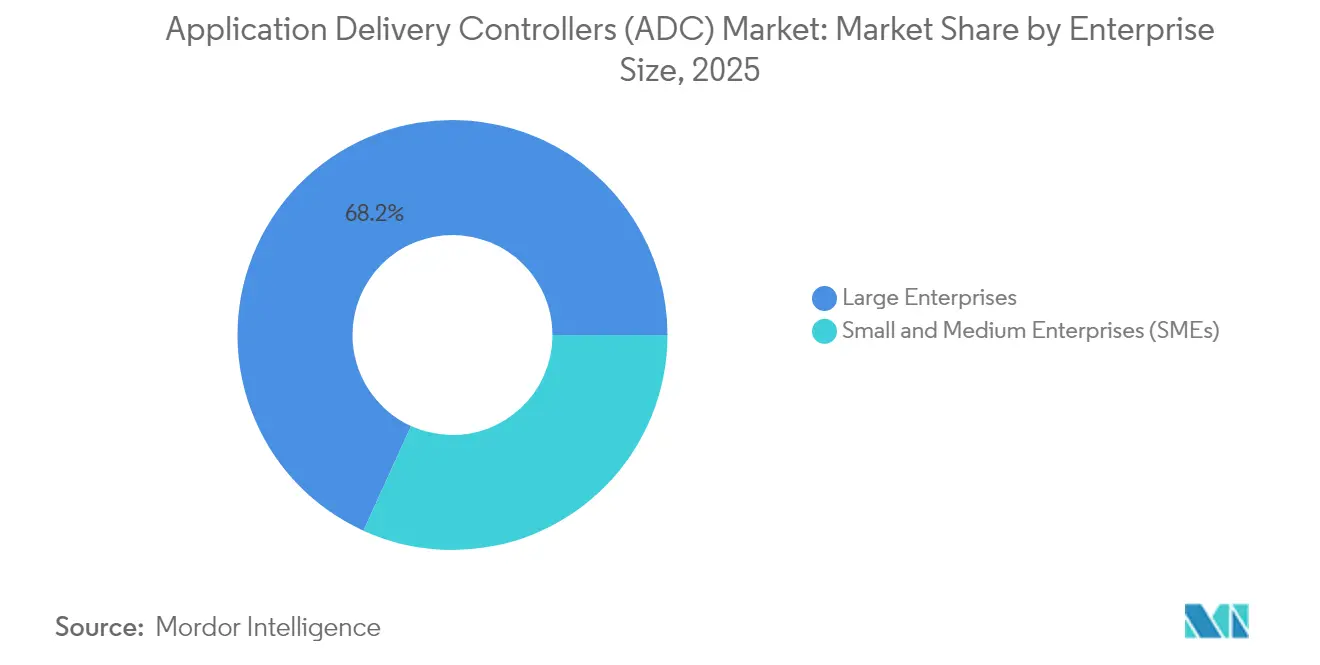

- By enterprise size, large enterprises dominated with a 68.20% share in 2025, whereas SMEs grew fastest at 10.08% CAGR.

- By vertical, IT & Telecom held 29.60% of the application delivery controllers market size in 2025; Healthcare & Life Sciences accelerated at 11.86% CAGR.

- By region, North America retained a 33.70% share in 2025; Asia-Pacific is set to climb at a 12.35% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Application Delivery Controllers (ADC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Cloud-Native and Microservices Architecture | +2.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Exponential East-West Data-Center Traffic Growth | +1.9% | North America, Europe, Advanced APAC | Medium term (2-4 years) |

| Regulatory Mandates for Secure Digital Banking in North America and EU | +1.2% | North America, Europe, with spillover to advanced APAC | Short term (≤ 2 years) |

| Growing 5G Roll-outs Driving Edge ADC Adoption in Asia | +1.7% | APAC, with secondary impact in North America and Europe | Medium term (2-4 years) |

| Rising Multi-Cloud and Hybrid IT Strategies among Global 2000 | +2.1% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Cloud-Native And Microservices Architecture

More than half of enterprise workloads already run as containerized or serverless components, forcing the application delivery controllers market to pivot toward lightweight, API-centric form factors that sit inside Kubernetes clusters and service meshes. These micro-gateways inject granular traffic steering, mutual-TLS termination, and automated scaling hooks that match the ephemeral nature of modern applications [1] F5 Inc., “2025 State of Application Strategy Report,” f5.com. Vendors are embedding schema-aware API firewalls and distributed rate-limiters to close security gaps opened by east-west service calls. As CIOs push for platform engineering, declarative “ADC-as-code” integrates seamlessly with GitOps pipelines, reducing hand-offs between Dev and NetOps.

Exponential East-West Data-Center Traffic Growth

Virtual server density has multiplied internal flows, outpacing traditional north-south patterns and elevating latency-sensitive micro-transactions. Distributed ADC instances now sit closer to workload pods, providing pervasive telemetry and inline decryption without introducing bottlenecks [2]Fortinet, “Data Center Trends and Network Security Impact,” fortinet.com. Financial exchanges, telcos, and gaming providers deploy thousands of lightweight proxies that collectively enforce Layer-7 policies yet adapt to bursty resource pools.

Regulatory Mandates for Secure Digital Banking

Rules such as the EU’s Digital Operational Resilience Act compel banks to prove application-layer defense in depth by January 2025. Institutions are hardening API gateways, bot management, and encrypted-traffic inspection within ADC stacks to satisfy auditors without compromising single-millisecond response-time targets. Similar statutes in the United States and Asia-Pacific replicate the compliance-driven spend trajectory.

Growing 5G Roll-outs Driving Edge ADC Adoption

Ultra-low-latency 5G services push compute toward radio access sites, elevating demand for ruggedized, power-efficient ADC micro-instances that can autonomously orchestrate QoS, content caching, and security at the edge [3]Global TD-LTE Initiative, “5G-AxAI White Paper,” gtigroup.org. MEC deployments for autonomous vehicles, AR/VR, and industrial IoT rely on per-packet telemetry and AI-based anomaly detection embedded inside these edge ADC footprints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Layer-7 Policy Configuration Burdens IT Ops | -1.4% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Cost Inflation of Advanced ADC Licensing Models | -1.1% | Global, with higher impact in price-sensitive regions | Short term (≤ 2 years) |

| Commoditization of Basic Load-Balancing Features | -0.8% | Global | Medium term (2-4 years) |

| Shortage of Skilled NetOps and DevSecOps Talent | -1.2% | Global, more severe in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex Layer-7 Policy Configuration Burdens IT Ops

Enterprise teams confront hundreds of heterogeneous applications, each demanding bespoke routing, rewrite, or WAF logic. Maintaining accuracy across multi-cloud estates strains scarce DevSecOps talent and can stall broader ADC roll-outs. Vendors answer with intent-based templates, AI-assisted rule creation, and visual dependency maps, yet skill gaps persist.

Cost Inflation of Advanced ADC Licensing Models

Subscription-tiering and add-on security modules have raised overall spend, especially for organizations migrating from perpetual hardware to SaaS-delivered ADCs. Budget-bound SMEs often delay upgrades or seek open-source substitutes, slowing penetration in price-sensitive regions until flexible, usage-metered models normalize expenditure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software ADCs Disrupt Hardware Dominance

Hardware appliances represented 58.35% of the application delivery controllers market in 2025, supported by specialized SSL offload chips and deterministic throughput. Yet the virtual segment is scaling at 14.12% CAGR as DevOps teams embed ADC images directly into CI/CD pipelines, reducing rack footprint and accelerating rollout windows. The application delivery controllers market size for virtual solutions is forecast to surge alongside container adoption, challenging hardware’s grip on mission-critical tiers.

Mature vendors hedge by releasing container-native proxies that inherit their policy engines while shedding appliance overhead. Cost transparency plus cloud marketplace billing appeal to agile teams, driving incremental share gains for software even inside traditional enterprises. As TLS 1.3 and QUIC adoption climb, code-level agility will further tilt decisions toward software form factors, though hardware will persist for ultra-high TPS gateways in finance and telecom cores.

By Deployment: Cloud-Managed Solutions Accelerate

On-premise instances still command 63.25% of the application delivery controllers market size in 2025, favored by sectors bound to data-sovereignty mandates. Integrated threat analytics modules and pay-as-you-grow capacity licensing now refresh legacy estates without forklift replacements .

Conversely, the cloud-managed model rises at 14.68% CAGR as platform teams offload patching, scaling, and telemetry to vendor-operated control planes. Multi-region rollouts complete in hours, and unified API policy enforcement eliminates site-level drift, making it the preferred path for digital-native firms. The application delivery controllers market continues to blend these modes through hybrid dashboards that configure hardware, virtual, and SaaS endpoints from a single console.

By Component: Services Growth Outpaces Solutions

Core solutions—load balancing, acceleration, and integrated security—captured 69.40% revenue in 2025, but services post a sharper 11.54% CAGR as architects seek guidance on weaving ADC logic into zero-trust and platform-engineering initiatives. Consulting partners now deliver blueprint libraries, automation scripts, and continuous posture assessments that shorten value-realization cycles. Managed services contracts bundle 24/7 policy tuning, threat-signature updates, and SLO monitoring, addressing the talent crunch hindering in-house operations. This recurrent-revenue motion incentivizes vendors to enhance AIOps modules that cut mean-time-to-detect, expanding service attach rates across the application delivery controllers industry.

By Enterprise Size: SMEs Close the Adoption Gap

Large enterprises held 68.20% revenue in 2025, running multi-tier, multi-cluster ADC grids spanning private and public clouds. Central orchestration and cross-site failover protect revenue-critical platforms, making ADC refresh cycles a board-level priority.

SMEs, traditionally constrained by CapEx, now exploit SaaS ADCs with daily metering and low entry points. Growth at 10.08% CAGR reflects the democratization of sophisticated traffic management once exclusive to Fortune 500. Low-code dashboards and curated policy bundles dissolve technical hurdles, positioning the application delivery controllers market as a foundational layer for mid-market digital commerce.

By End-User Vertical: Healthcare Accelerates Digital Infrastructure

IT & Telecom accounted for 29.60% of the application delivery controllers market in 2025. Global carriers hinge on edge-deployed ADC clusters to meet stringent latency targets for voice over 5G, cloud gaming, and OTT video. Telcos also front-load AI-driven analytics to anticipate congestion and preempt outages.

Healthcare & Life Sciences grow fastest at 11.86% CAGR, catalyzed by telemedicine, imaging exchange, and electronic health record portals that demand secure, always-on access. HIPAA and GDPR mandates drive the uptake of integrated WAF and API anomaly detection. Purpose-built clinical filters accelerate DICOM streams, underscoring vertical-specific tuning within the broader application delivery controllers market.

Geography Analysis

North America retained 33.70% of the application delivery controllers market in 2025, buoyed by hyperscaler ecosystems and stringent data-privacy regulations that elevate integrated security requirements. Consolidation plays, such as F5’s reported displacement of hundreds of Citrix NetScaler estates, demonstrate churn within mature accounts.

Asia-Pacific delivers the steepest 12.35% CAGR as 5G rollouts and Industry 4.0 agendas spur demand for low-latency, multi-tenant ADC fabrics across factories and smart cities. Government cloud programs in China and India embed ADC functionality inside sovereign clouds, driving local vendor partnerships.

Europe balances on-prem and cloud adoption, reinforced by DORA compliance deadlines influencing bank and fintech upgrades. Regulators’ focus on data residency fuels demand for policy-driven location fencing.

Middle East and Africa tap ADCs to underpin USD 3.7 trillion in megaproject construction, IoT-enabled utilities, and nationwide digital-government portals. Hybrid models satisfy both performance needs and limited regional data-center footprints.

South America’s financial-services modernization and retail e-commerce spur incremental uptake, with cloud-based ADCs preferred to circumvent capital constraints amid economic volatility.

Competitive Landscape

Competition remains vigorous as legacy hardware leaders rebuild portfolios around software and AI. F5 shifted 58% of product revenue to software by 2025 and introduced an AI Gateway that optimizes model inference pipelines while enforcing API security. Citrix, rebranded NetScaler, emphasizes secure access for healthcare and public-sector clients, yet partner realignments have opened migration windows.

Cloud providers such as AWS and Azure continue to bundle native load balancers that satisfy basic routing, pressuring standalone vendors to differentiate through deep observability, TLS 1.3 acceleration, and threat-intel integration. Open-source HAProxy sustains momentum; 91% of users recommend it despite steeper self-support effort, signaling healthy community innovation.

Strategic moves in 2025 include Radware’s elastic licensing deal with a top Italian bank to counter 265% YoY growth in Web DDoS attacks, and Kubermatic’s release of KubeLB, a multi-tenant load balancer purpose-built for Kubernetes. M&A talk circles around edge-native specialists and API security start-ups, foreshadowing further convergence.

Application Delivery Controllers (ADC) Industry Leaders

F5 Networks Inc.

NetScaler (Citrix Systems)

Fortinet Inc.

A10 Networks Inc.

Array Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: F5 Networks introduced the AI Gateway for hybrid multicloud AI workloads.

- March 2025: Radware expanded cloud protection at a top-5 Italian bank, including Alteon ADC with Global Elastic License.

- February 2025: F5 launched its converged “ADC 3.0” platform for AI-era applications.

- February 2025: Citrix detailed NetScaler-centric secure access road-map for heavily regulated sectors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the application delivery controllers (ADCs) market as all hardware-based and virtual appliances that sit between application servers and client devices, offering Layer-4-7 load balancing, traffic acceleration, SSL off-loading, and integrated security features such as basic WAF or DDoS mitigation. According to Mordor Intelligence, worldwide ADC revenue reached USD 3.42 billion in 2025 and is projected to climb to USD 5.26 billion by 2030.

Scope exclusion: tools whose sole function is DNS, API gateway, or pure web-application-firewall without integrated traffic steering are not counted.

Segmentation Overview

- By Type

- Hardware-Based ADC

- Virtual/Software ADC

- By Deployment

- On-premise

- Cloud-Managed/Hosted

- By Component

- Solutions (Control, Acceleration, Security)

- Services (Integration, Managed, Training)

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-user Vertical

- IT and Telecom

- BFSI

- Retail and E-commerce

- Healthcare and Life Sciences

- Government and Public Sector

- Manufacturing and Industrial 4.0

- Media and Entertainment

- Energy and Utilities

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Peru

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed North American and Asian network architects, European cloud-platform engineers, and procurement heads in BFSI and telecom to validate typical device refresh cycles, virtual-to-physical mix shifts, and region-specific average selling prices. Insights from these conversations filled data gaps and helped align traffic-growth assumptions with on-ground realities.

Desk Research

Our team first mapped the demand pool using open datasets from agencies such as the U.S. FCC on broadband capacity, Eurostat cloud-computing uptake, India's TRAI internet-traffic reports, and China MIIT data on data-center footprints. Industry bodies like the Cloud Native Computing Foundation and the Open Compute Project offered adoption benchmarks for virtual ADC components, while patent analytics from Questel clarified innovation hotspots around TLS 1.3 off-load. Company 10-Ks and investor decks supplied price-band signals, and news archives on Dow Jones Factiva tracked large-scale rollouts. These examples illustrate but do not exhaust the secondary sources referenced during desk work.

Market-Sizing & Forecasting

A top-down build began with global internet traffic and data-center server counts, which are then split by application-tier penetration and ADC attachment ratios. Select bottom-up roll-ups of supplier shipments and sampled ASP × volume checks fine-tuned totals. Key model drivers include encrypted-traffic share, microservices adoption, cloud workload migration rate, 5G edge node growth, and enterprise DevSecOps staffing levels. Forecasts apply multivariate regression on these variables, choosing the best-fit model through adjusted-R² tests. Scenario analysis, guided by expert consensus, handles macro volatility.

Data Validation & Update Cycle

Outputs pass variance checks against customs data, analyst peer reviews, and anomaly flags from our paid dashboards. Reports refresh annually, with interim updates when material events, such as a major security mandate, shift demand. A last-mile analyst review ensures clients receive the most recent view.

Why Mordor's Application Delivery Controllers Baseline Commands Reliability

Estimates from different publishers rarely match because each selects its own scope boundaries, pricing ladders, and update cadence.

Key gap drivers include whether virtual ADC software running inside service meshes is counted, the treatment of bundled WAF features, currency conversion dates, and how aggressively future TLS traffic growth is priced into ASPs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.42 B (2025) | Mordor Intelligence | - |

| USD 4.35 B (2024) | Global Consultancy A | Includes stand-alone WAF and ADC-aaS revenues; earlier base year inflates total |

| USD 4.50 B (2024) | Trade Journal B | Uses shipment value at list price without regional discounts |

| USD 3.60 B (2024) | Industry Research C | Excludes hardware refresh under five-year contracts; narrower enterprise scope |

The comparison shows that once like-for-like adjustments are applied, Mordor's balanced mix of scope discipline, variable transparency, and yearly refresh cadence offers decision-makers the most dependable baseline.

Key Questions Answered in the Report

What is driving the strongest growth in the application delivery controllers market?

Rapid adoption of cloud-native microservices, 5G-enabled edge computing, and regulatory mandates for secure digital banking are propelling demand, pushing the global CAGR to 8.87%.

How large is the application delivery controllers market size today?

The application delivery controllers market size stands at USD 3.72 billion in 2026 and is forecast to reach USD 5.69 billion by 2031.

Which region is growing fastest for ADC deployments?

Asia-Pacific is the fastest-growing region with a projected 12.35% CAGR as 5G rollouts and Industry 4.0 projects multiply low-latency application needs.

Why are software ADCs gaining momentum over hardware?

Software and container-native ADCs integrate seamlessly into CI/CD pipelines, scale elastically, and reduce capital outlay, leading to a 14.12% CAGR versus hardware’s slower growth.

How are vendors addressing the skills gap in ADC management?

Providers embed AI-driven policy automation, visual configuration wizards, and managed service offerings to simplify Layer-7 rule creation and ongoing tuning for organizations lacking NetOps expertise.

What impact will regulatory frameworks like DORA have on the market?

Regulations requiring demonstrable application-layer resilience drive immediate upgrades in the financial sector, adding an estimated 1.2% boost to overall market CAGR through 2027.

Page last updated on: