Automotive Fuel Rail Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

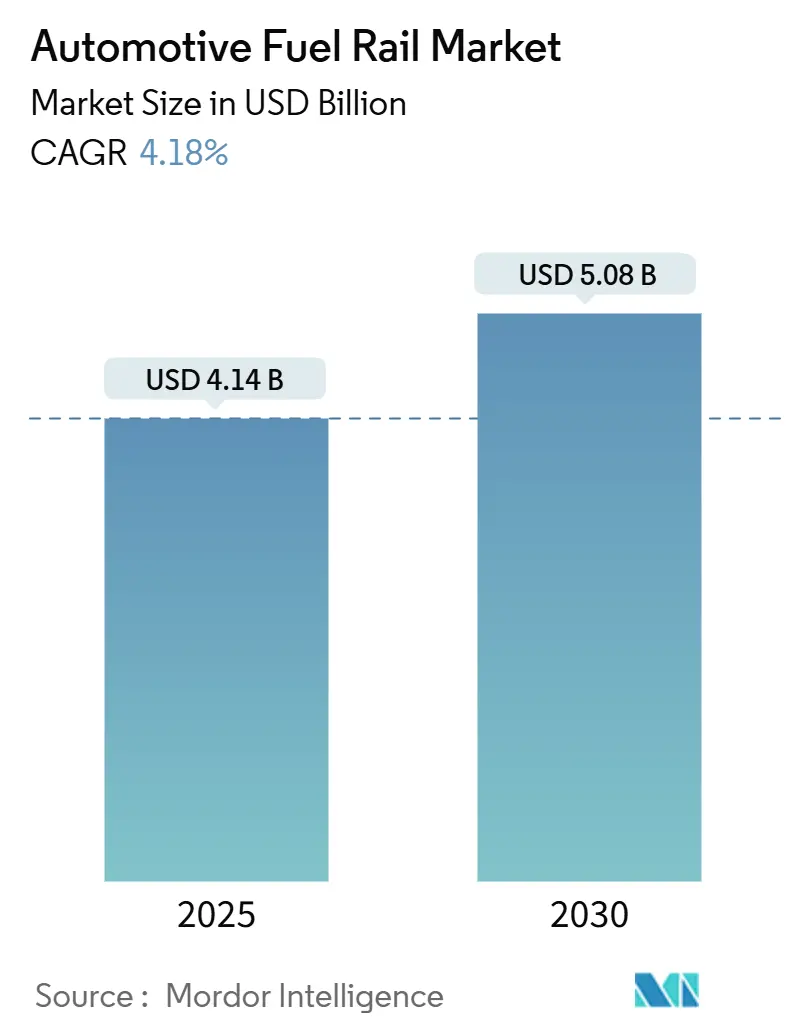

| Market Size (2025) | USD 4.14 Billion |

| Market Size (2030) | USD 5.08 Billion |

| Growth Rate (2025 - 2030) | 4.18% CAGR |

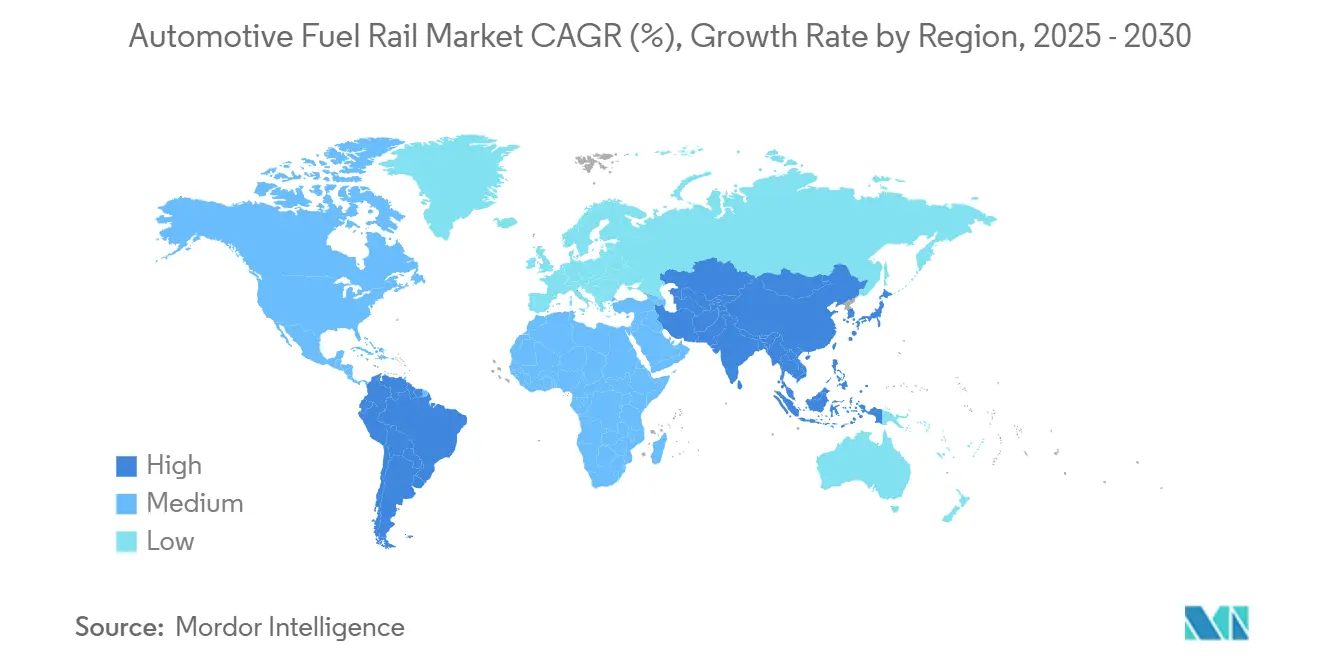

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

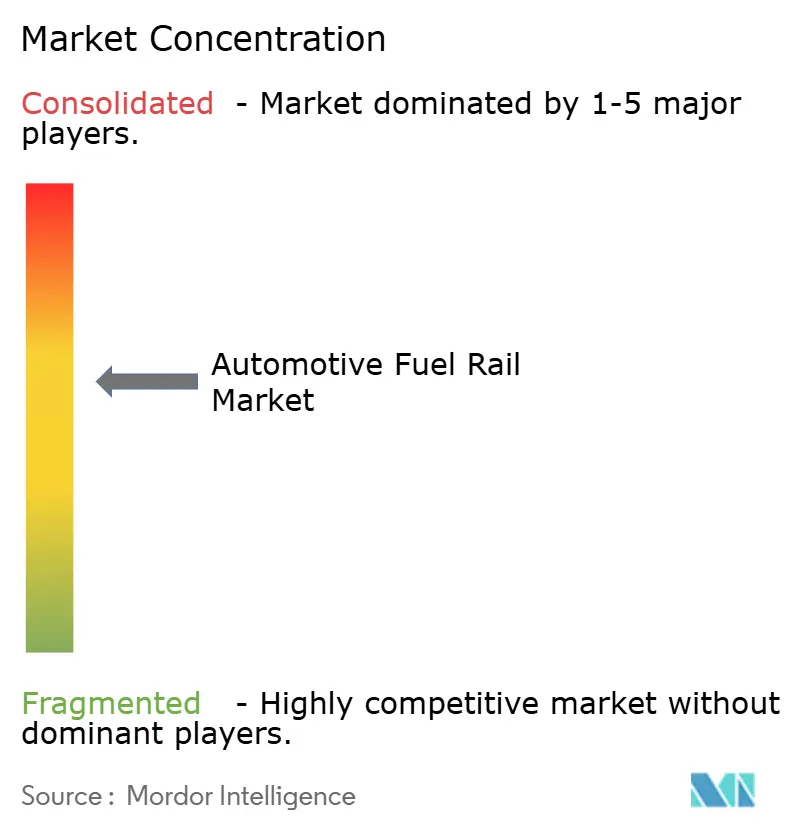

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Fuel Rail Market Analysis by Mordor Intelligence

The automotive fuel rail market size stood at USD 4.14 billion in 2025 and is forecast to climb to USD 5.08 billion by 2030, advancing at a 4.18% CAGR over the period. The trajectory reflects resilient internal-combustion demand even as automakers juggle tougher emissions rules and gradual electrification. Stricter Euro 6d, China VI-b, and U.S. LEV III norms are anchoring high-pressure gasoline direct-injection adoption, while aluminum rails gain favor as a lightweight countermove to heavier after-treatment packs. Asia-Pacific maintains momentum thanks to rebounding light-vehicle production in China, India, and the ASEAN bloc. At the same time, tier-1 suppliers sharpen portfolios around 350-bar architectures, ethanol-compatible lines, and early hydrogen ICE pilots to hedge battery-electric uncertainty.

Key Report Takeaways

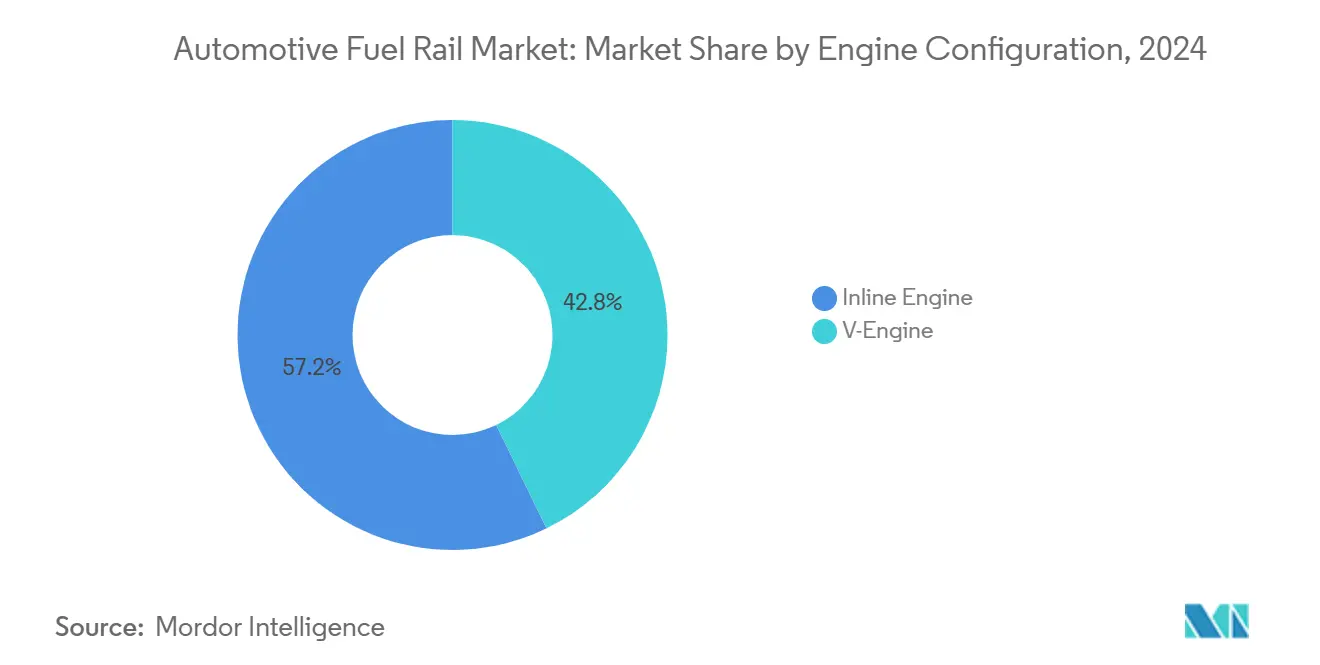

- By engine configuration, inline layouts captured 57.15% of the automotive fuel rail market share in 2024 and are on course for a 4.65% CAGR, outpacing V-engine applications.

- By material type, stainless steel retained 49.33% of the automotive fuel rail market share in 2024, but aluminum alloy rails are advancing at a 6.05% CAGR to 2030.

- By pressure system, high-pressure rails held 64.26% of the automotive fuel rail market share in 2024, with the segment projected to rise at a 4.97% CAGR through 2030.

- By vehicle type, passenger cars accounted for 63.15% of the automotive fuel rail market size in 2024, and are slated to expand at a quicker 5.44% CAGR through 2030.

- By fuel type, gasoline retained 55.36% of the automotive fuel rail market share in 2024, but hydrogen is advancing at a 7.13% CAGR to 2030.

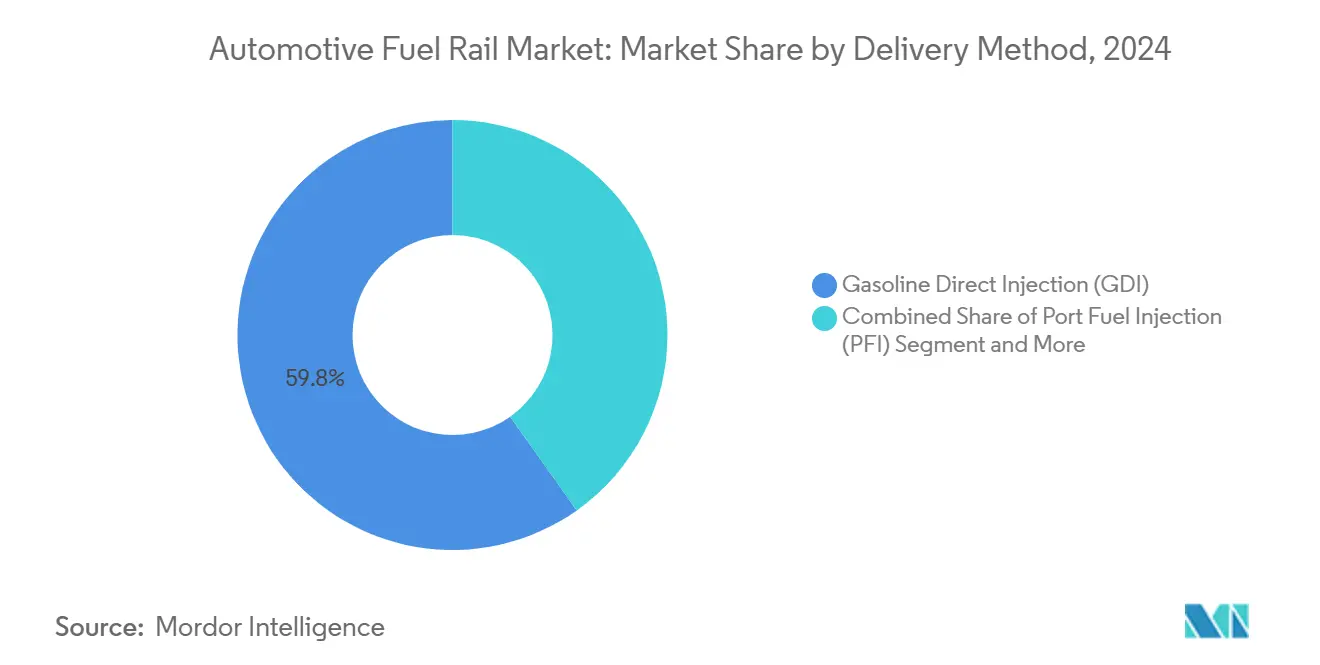

- By delivery method, gasoline direct injection led with 59.77% of the automotive fuel rail market share in 2024, and is projected to record the fastest 5.87% CAGR to 2030.

- By distribution channel, OEM (factory-fitted) rails retained 70.11% of the automotive fuel rail market share in 2024, while aftermarket (replacement) segment is projected to expand at a 6.71% CAGR to 2030.

- By geography, Asia-Pacific held a 36.25% of the automotive fuel rail market share in 2024, with the segment projected to rise at a 5.14% CAGR through 2030.

Global Automotive Fuel Rail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter Global Emissions Norms | +1.2% | Europe, China, North America | Medium term (2-4 years) |

| OEMs Shift to 350-Bar GDI | +0.8% | Global | Short term (≤ 2 years) |

| APAC Light-Vehicle Production Rebounds | +0.7% | Asia-Pacific | Short term (≤ 2 years) |

| Stainless-To-Aluminum Rail Lightweighting | +0.5% | Global | Medium term (2-4 years) |

| Expansion of Flex-Fuel Programs | +0.4% | Brazil, India, U.S. Midwest | Long term (≥ 4 years) |

| Hydrogen ICE Pilot Programs | +0.2% | Japan, Germany, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Euro 6d, China VI-b and US LEV III Emissions Norms Spur High-Pressure Rails

Mandatory particulate-number ceilings and real-driving emissions tests mean automakers must deploy 350-bar fuel systems that maintain leak-tight integrity under wide thermal swings. Euro 6d became compulsory for all new EU registrations in 2024, while China VI-b mirrors the particulate limits and adds dynamic testing. U.S. LEV III phases in a fleet-average 0.030 g/mile NOx cap by 2025, effectively mandating direct injection coupled with gasoline particulate filters [1]U.S. Environmental Protection Agency, “LEV III Final Rule,” EPA.gov .

OEM Drive Toward 350-Bar GDI for 15% Lower Fuel Burn in Downsized Engines

Higher rail pressure translates to finer atomization, faster burn, and fewer wall wetting losses, enabling 3- and 4-cylinder units to match the torque of outgoing sixes without hybrid costs. Continental and Bosch have broadened 350-bar pump lines, while dealer groups are ramping technician training to safely handle elevated pressures [2]“High-Pressure Gasoline Systems Portfolio,” Continental AG, continental.com.

Rapid APAC Light-Vehicle Production Recovery Post-2023 Chip Crunch

China’s annual passenger-car output exceeded 27 million units throughout 2024, and India logged double-digit growth with Maruti Suzuki retaining its leading share. Indonesia’s assembly volumes rebounded as semiconductor supply normalized, restoring fuel-rail call-offs and shortening delivery lead times for component suppliers.

Stainless-to-Aluminum Rail Light-Weighting to Offset Heavier After-Treatment

Aluminum rails trim roughly 40% mass relative to AISI 304 units while sustaining 350-bar duty cycles. Extruded 6000-series alloys coupled with friction-stir welding curb porosity, and anodized bores resist ethanol-rich blends. Lightweight gains help recapture the 15-25 kg penalty added by particulate filters and SCR systems [3]“Automotive Extrusions Factsheet,” Aluminum Association, Aluminum.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European EV Share Rises | -0.9% | Europe | Medium term (2-4 years) |

| Nickel Price Volatility Concerns | -0.6% | Global | Short term (≤ 2 years) |

| Technician Skill Gap Challenges | -0.3% | North America, Europe | Medium term (2-4 years) |

| Counterfeit Rails in Southeast Asia | -0.2% | ASEAN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Share Above 30% of New Sales in Europe by 2030 Curbs ICE Rail Demand

EU battery-electric uptake accelerated after the 2025 CO₂ fleet target stepped down to 93 g/km. As the ICE share shrinks, suppliers face volume attrition and must pivot toward flex-fuel or hydrogen programs to offset declining call-offs.

Raw-Material Price Volatility for Nickel-Bearing Stainless Grades

LME nickel swings feed straight into AISI 304 and 316 feedstock, squeezing margins when fixed-price OEM contracts prevail. Smaller fabricators struggle to hedge, risking shortcuts that may trigger leak-related recalls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Configuration: Inline Dominance Drives Standardization

Inline engines accounted for a 57.15% slice of the automotive fuel rail market in 2024 and are on track for a 4.65% CAGR to 2030. Inline layouts simplify rail packaging, enabling single-piece extrusions, trimming tooling outlay, and assembly time. Automakers favor inline three- and four-cylinders for C-segment crossovers, reinforcing demand concentration. Their straight-shot architecture also eases common-component strategies across global platforms.

Standardization lets tier-1 suppliers amortize capital over higher volumes, defending margins as OEM cost-down targets tighten. Yet dependence on inline volumes creates exposure if market preferences swing toward electrified skateboard platforms where ICE engines recede. Suppliers pair inline rail lines with emerging hydrogen and ethanol variants to broaden revenue streams.

By Material Type: Aluminum Alloy Gains Momentum

Stainless steel kept a 49.33% of the automotive fuel rail market share in 2024, but aluminum alloy rails are registering the swiftest 6.05% CAGR through 2030. Weight savings approach 50%, a key lever for balancing heavier particulate filters. Extruded 6061-T6 profiles with friction-stir weld caps withstand cyclic 350-bar pulses while meeting burst targets above 1,000 bar.

Lifecycle assessments now favor aluminum on recyclability, persuading OEMs despite premium ingot costs. Design hurdles include galvanic pairing with steel injectors and higher thermal expansion, but silicon-rich alloys and sleeve bushings mitigate risks. Suppliers mastering aluminum machining and automatic optical leak-test cells are carving defensible niches.

By Pressure System: High-Pressure Rails Accelerate

High-pressure assemblies occupied 64.26% of the automotive fuel rail market share in 2024 and are forecast to climb 4.97% annually. Euro 6d particulate caps leave GDI as the de facto gasoline architecture, cementing >300-bar rails as standard. Value per unit rises with pressure rating, cushioning suppliers from ICE volume erosion.

Low-pressure lines linger in value-oriented markets, yet face a gradual sunset as real-driving protocols proliferate. Vendors are bundling rails with 350-bar pumps and particulate filters to deepen content per vehicle and lock in long-term contracts.

By Vehicle Type: Passenger Cars Lead Market Evolution

Passenger cars generated 63.15% of the automotive fuel rail market share in 2024 demand and will advance 5.44% yearly as the SUV mix and per-vehicle injector count climb. Light-duty segments adopt new particulate filters first, accelerating high-pressure rail refresh cycles. Commercial vehicle rails skew toward diesel common-rail formats where upgrade cadence is slower.

SUV heft boosts lightweight-rail pull-through, pushing aluminum adoption curves. Meanwhile, last-mile delivery van electrification poses a long-term headwind, urging rail makers to diversify toward ethanol and hydrogen lines servicing heavier trucks.

By Fuel Type: Gasoline Dominance Faces Hydrogen Challenge

Gasoline systems represented 55.36% of the automotive fuel rail market share in 2024 turnover, yet hydrogen shows a 7.13% CAGR on a small base. Hydrogen ICE pilots require 70-MPa rail bursts and permeation-resistant seals, furnishing new specialty revenue pools. Flex-fuel rails grow in Brazil and India as E20 and E85 mandates creep upward.

CNG/LPG niches persist where fiscal incentives survive but lack the global momentum to offset gasoline moderation. Suppliers promoting fuel-agnostic rail platforms can shift output with minimal retooling as regional policies evolve.

By Delivery Method: GDI Systems Drive Technology Adoption

Gasoline Direct Injection (GDI) captured 59.77% of the automotive fuel rail market share in 2024, and headed toward a 5.87% growth rate. Direct injection’s stratified burn slashes particulate counts, embedding 350-bar rails as core hardware. Port injection remains cost-effective for non-regulated markets, while diesel common-rail volume declines with passenger-car diesel share.

Suppliers concentrate R&D on injector-rail harmonization to cut pressure pulsation and noise. Integrated pressure sensors and in-rail flow damper chambers emerge as differentiators, raising barriers for new entrants.

By Distribution Channel: Aftermarket Growth Accelerates

Factory-fit rails comprised 70.11% of the automotive fuel rail market share in 2024, yet aftermarket sales will rise 6.71% annually through 2030. The average vehicle age in the U.S. exceeds 12 years, increasing replacement cycles for high-pressure lines prone to ethanol-induced corrosion. Counterfeits remain a threat, so branded players leverage QR-coded traceability to reassure workshops.

OEM service arms bundle rail kits with injectors and seals, generating higher ticket sizes. Independent distributors seek competitively priced aluminum variants that install without line-relearning, expanding share in emerging markets.

Geography Analysis

Asia-Pacific topped the automotive fuel rail market with 36.25% in 2024, propelled by China’s steady monthly passenger-car output, India’s double-digit production rebound, and Indonesia’s strong two-wheeler base. The region is forecast for a 5.14% CAGR to 2030, underpinned by rising middle-class car ownership and localized component sourcing mandates. Government incentives for E20 and E85 blends in India and Thailand further widen the product scope for ethanol-compatible rails.

Europe follows as a regulation-driven territory where OEMs rush to deploy 350-bar GDI and lightweight aluminum solutions. However, the high penetration of the battery-electric market threatens long-term ICE volumes, prompting rail vendors to hedge with hydrogen-ready portfolios. North America combines stable pickup and SUV ICE demand with expanding flex-fuel programs across corn-belt states, securing a middle-ground growth path.

South America benefits from Brazil’s mature flex-fuel fleet, fostering steady demand for ethanol-tolerant rails, while Argentina’s volatile currency constrains near-term imports. The Middle East & Africa remain nascent but draw investment from global suppliers to offset European volume decline. Localization rules in Saudi Arabia’s emerging auto hub may spark joint ventures to produce rails for regional assembly plants.

Competitive Landscape

The automotive fuel rail market is moderately consolidated: Bosch, Denso, and Continental account for a sizeable combined share by bundling rails, pumps, and injectors into turnkey modules. Their global footprints, ISO 9001 rigor, and deep co-development ties allow early involvement in powertrain programs, anchoring high entry barriers. Hitachi Astemo and Stanadyne fortify mid-tier positions by specializing in high-pressure gasoline pumps paired with matching rails.

Suppliers diversify toward aluminum extrusion, ethanol-compatible coatings, and hydrogen-rated seal chemistries. Bosch recently expanded its Brazilian site to fabricate anodized aluminum flex-fuel rails, while Denso partnered with a Japanese alloy maker to trial friction-stir processes. Continental launched an aftermarket 350-bar rail kit integrated with a pressure sensor to pre-empt leak-related callbacks. These moves defend margins as OEM price-downs intensify.

Strategic collaborations rise: Cummins allied with Westport to validate hydrogen ICE rails, and Mahle is piloting composite over-molded rail bodies for sub-1500 cc engines. Private-equity interest grows in niche aluminum machinists that boast CT-scanned quality gates. Competitive intensity remains highest in Asia-Pacific, where domestic fabricators leverage cost advantages yet struggle to attain 100% burst-test yields demanded by European OEMs.

Automotive Fuel Rail Industry Leaders

Robert Bosch GmbH

Denso Corporation

Continental AG

Aptiv PLC

Magneti Marelli

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Mahindra is engineering flex-fuel engines calibrated for E30, adding ethanol sensors and fuel-rail heaters to guarantee cold starts and corrosion resistance.

- April 2025: Ford recalled 33,000 Escape and Bronco Sport SUVs to update powertrain control software that detects rail-pressure drops and disables the pump, mitigating injector crack-related fire risk.

Global Automotive Fuel Rail Market Report Scope

| Inline Engine |

| V-Engine |

| Stainless Steel |

| Aluminum Alloy |

| Plastic |

| Steel Forged |

| High-Pressure Fuel Rail |

| Low-Pressure Fuel Rail |

| Passenger Cars | Hatchback |

| Sedan | |

| SUV | |

| Coupe | |

| Commercial Vehicles | LCV |

| MCV | |

| HCV |

| Gasoline |

| Diesel |

| Flex Fuel (E10-E85) |

| CNG/LPG |

| Biofuel/Synthetic |

| Hydrogen |

| Gasoline Direct Injection (GDI) |

| Port Fuel Injection (PFI) |

| Common-Rail Diesel Injection |

| OEM (Factory-Fitted) |

| Aftermarket (Replacement) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Engine Configuration | Inline Engine | |

| V-Engine | ||

| By Material Type | Stainless Steel | |

| Aluminum Alloy | ||

| Plastic | ||

| Steel Forged | ||

| By Pressure System | High-Pressure Fuel Rail | |

| Low-Pressure Fuel Rail | ||

| By Vehicle Type | Passenger Cars | Hatchback |

| Sedan | ||

| SUV | ||

| Coupe | ||

| Commercial Vehicles | LCV | |

| MCV | ||

| HCV | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Flex Fuel (E10-E85) | ||

| CNG/LPG | ||

| Biofuel/Synthetic | ||

| Hydrogen | ||

| By Delivery Method | Gasoline Direct Injection (GDI) | |

| Port Fuel Injection (PFI) | ||

| Common-Rail Diesel Injection | ||

| By Distribution Channel | OEM (Factory-Fitted) | |

| Aftermarket (Replacement) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the automotive fuel rail market in 2025?

The automotive fuel rail market size reached USD 4.14 billion.

How fast is the sector expected to grow through 2030?

The market is projected to advance at a 4.18% CAGR between 2025 and 2030.

Which region leads global demand for fuel rails?

Asia-Pacific commanded 36.25% of 2024 revenue, driven by vehicle production rebounds in China and India.

What new opportunities are emerging beyond gasoline applications?

Hydrogen ICE pilots and expanded ethanol blending mandates are opening niches for specialized high-pressure and corrosion-resistant rail designs.

Page last updated on: