Railway Wiring Harness Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

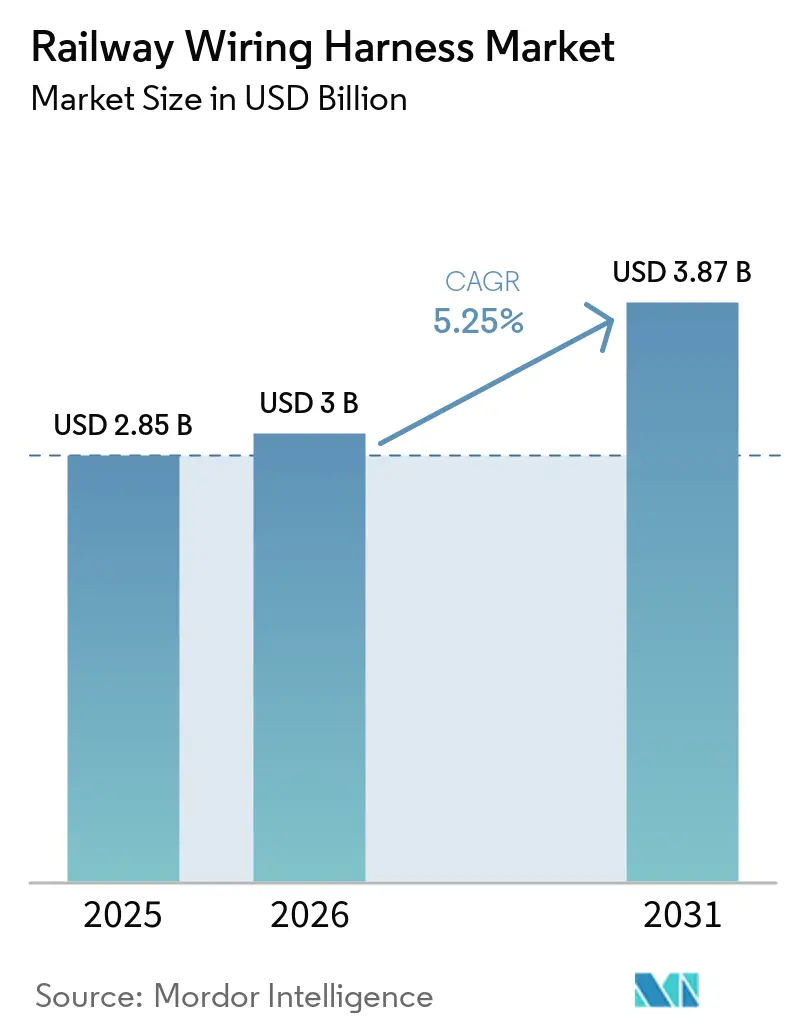

| Market Size (2026) | USD 3 Billion |

| Market Size (2031) | USD 3.87 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

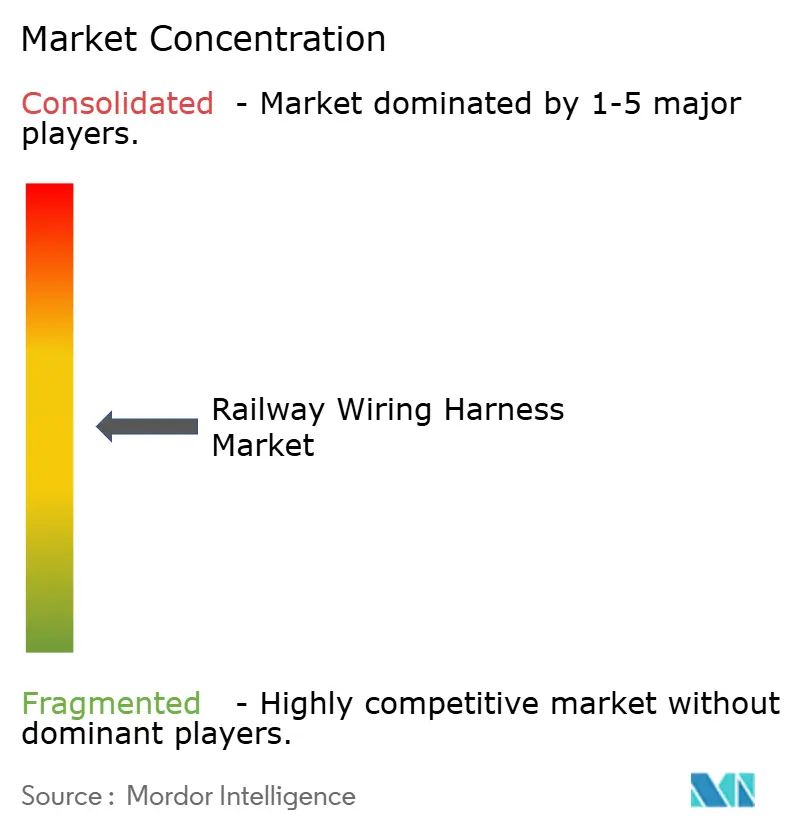

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Railway Wiring Harness Market Analysis by Mordor Intelligence

The Railway Wiring Harness market size is expected to grow from USD 2.85 billion in 2025 to USD 3 billion in 2026 and is forecast to reach USD 3.87 billion by 2031 at 5.25% CAGR over 2026-2031. Momentum comes from national rail-electrification targets, the spread of high-speed lines, and stricter safety rules that steer operators toward low-smoke, halogen-free cabling. Asia-Pacific keeps demand buoyant as China and India fast-track network upgrades, while Europe’s ETCS mandate and Taxonomy regulation sustain premium cable adoption. Persistent copper price volatility incentivizes copper-clad aluminium (CCA) substitution, and urban migration spurs investment in driverless metro projects that rely on complex, high-bandwidth harnesses.

Key Report Takeaways

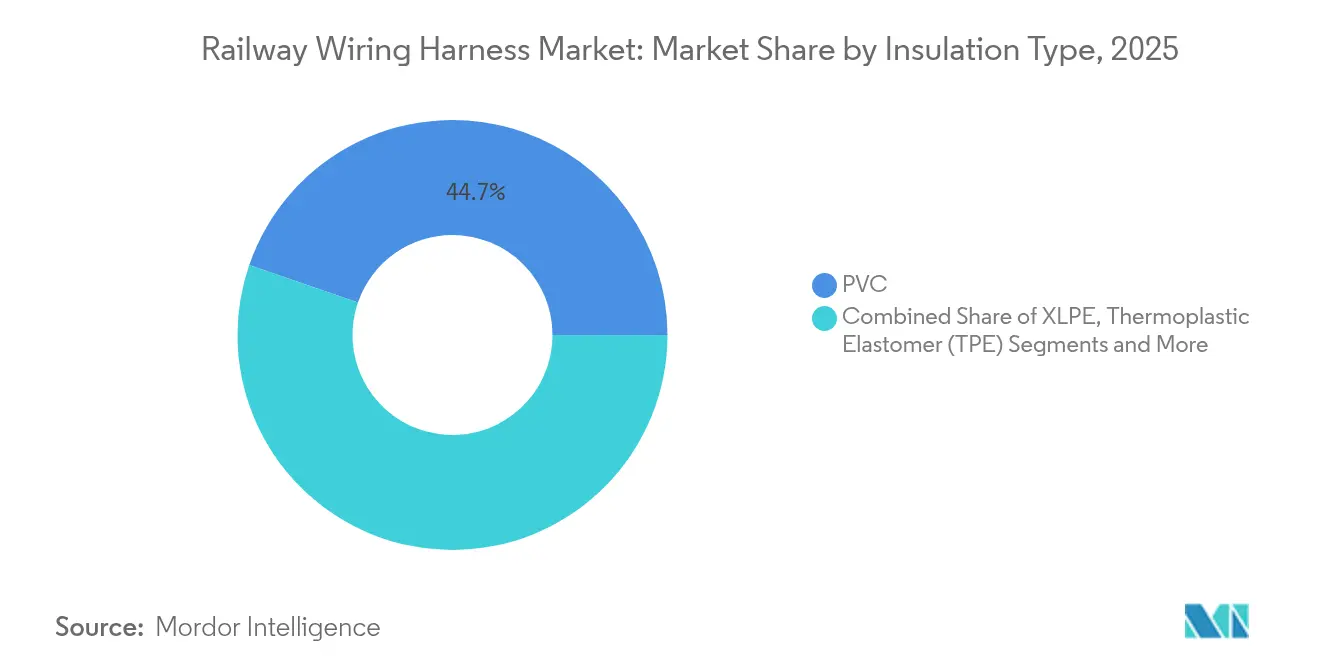

- By insulation type, PVC controlled 44.72% of the railway wiring harness market size in 2025; halogen-free flame-retardant (HFFR) materials are advancing at a 7.58% CAGR over the same period.

- By wire material, copper held 58.15% of the railway wiring harness market share in 2025, while optical fiber is expected to post a 7.22% CAGR to 2031.

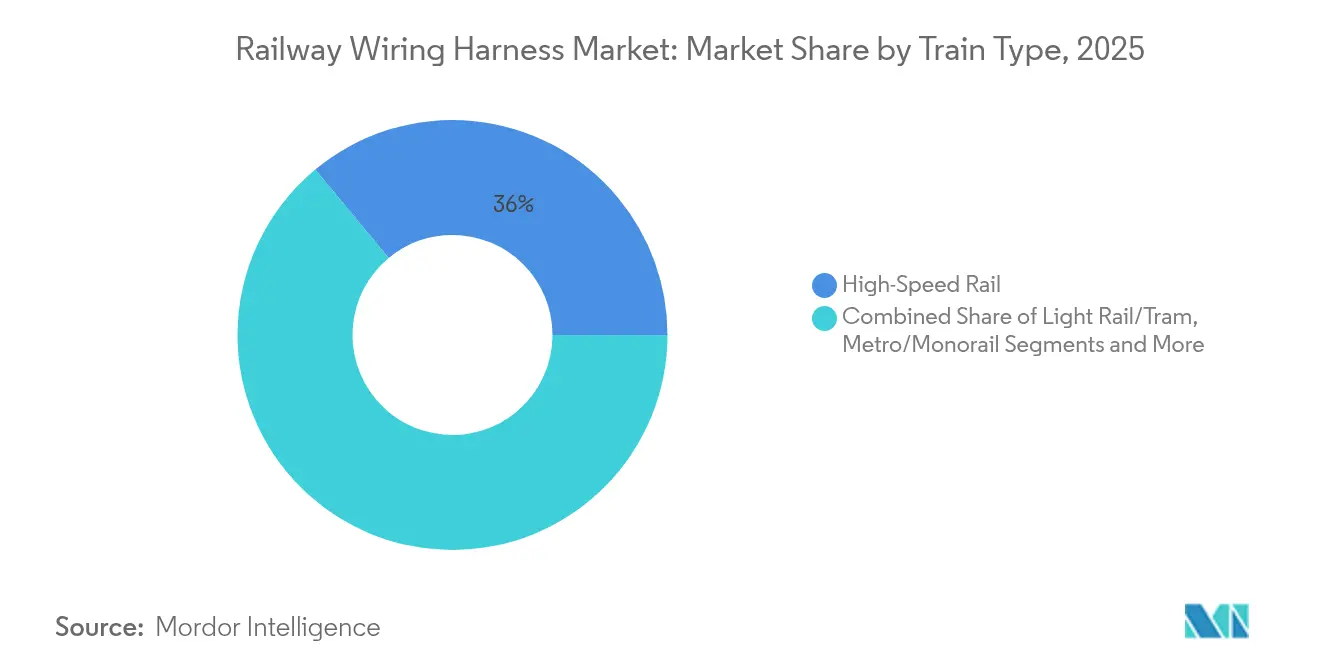

- By train type, high-speed rail accounted for 36.02% of the railway wiring harness market size in 2025; the metro segment is projected to grow at a 6.18% CAGR from 2026 to 2031.

- By application, engine and traction systems secured a 33.12% share in 2025, whereas infotainment connectivity is anticipated to rise at a 7.89% CAGR to 2031 in the Railway Wiring Harness Market.

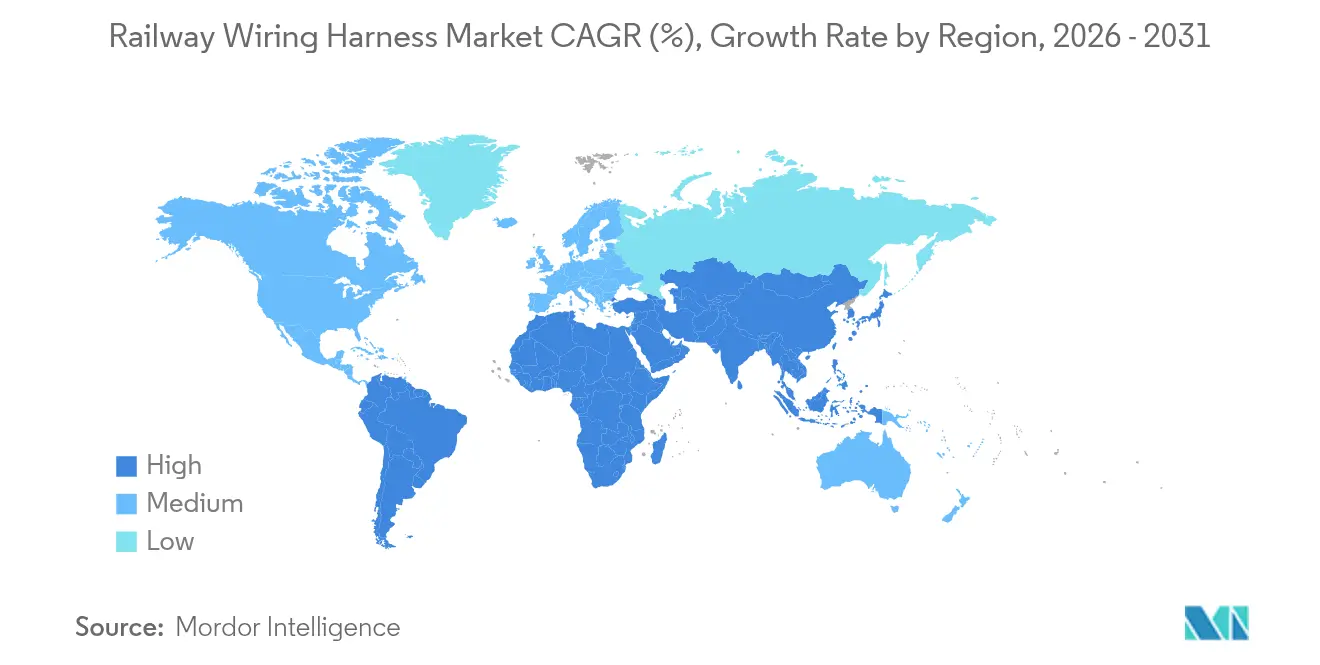

- By geography, Asia-Pacific led with a 44.05% revenue share in 2025, and the region is forecast to expand at a 7.45% CAGR through 2031 in the Railway Wiring Harness Market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Railway Wiring Harness Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Rail-Electrification Pipelines | +1.8% | Global, with concentration in India, Europe, and Asia-Pacific | Medium term (2-4 years) |

| High-Speed Rail Network Expansion | +1.2% | Asia-Pacific core, spill-over to Europe and North America | Long term (≥ 4 years) |

| Demand for Driverless & CBTC-Equipped Metros | +0.9% | Urban centers globally, led by Europe and Asia-Pacific | Medium term (2-4 years) |

| Shift to Copper-Clad Aluminium (CCA) | +0.7% | Global, early adoption in Europe and North America | Short term (≤ 2 years) |

| Smart-Cabling for Predictive Maintenance | +0.5% | Developed markets, expanding to emerging economies | Long term (≥ 4 years) |

| EU Taxonomy Rules | +0.4% | Europe, with regulatory spillover to other regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government rail-electrification pipelines

India completed 98.83% electrification of its 69,512 km broad-gauge system by March 2025, cutting annual diesel use by 136 crore liters.[1]“98.83% Electrification of Broad Gauge Network Achieved,” Ministry of Railways, indianrailways.gov.in Lithuania approved EUR 398 million to bring its network to 39% electrified by 2030 with EU Cohesion Fund support. Denmark’s Banedanmark is converting 1,150 km of regional lines, citing 40% lower operating costs once energised. The US Federal Railroad Administration now endorses intermittent electrification paired with dual-mode locomotives, a cost-efficient template for North American corridors. Across projects, demand rises for harnesses certified for 25 kV AC duty and robust electromagnetic compatibility, underpinning steady market volume additions in the Railway Wiring Harness Market.

High-speed rail expansion in Asia-Pacific & Europe

Vietnam’s parliament cleared USD 67 billion for a 1,541 km Hanoi–Ho Chi Minh City line that targets six-hour journeys and an 8% GDP lift. Germany ring-fenced EUR 500 billion for rail-first infrastructure, pledging 744 km of new or upgraded track by 2030.[2]“Germany Launches Rail-First Investment Strategy,” Federal Ministry of Transport, bundesregierung.de US policy momentum includes USD 8.2 billion under the Bipartisan Infrastructure Law, enabling the Las Vegas–Los Angeles corridor. India’s Mumbai–Ahmedabad Shinkansen project deploys a dual 25 kV supply for 320 km/h operations. In the Railway Wiring Harness Market,These large-scale schemes elevate demand for precision-engineered harnesses covering traction, signaling, and broadband services inside aerodynamically optimised rolling stock.

Shift to copper-clad aluminium (CCA)

Spot copper traded near USD 5 per pound in early 2025, inflating cable bills by up to 35% for manufacturers. Leoni’s liquid-cooled CCA cables cut up to 75% of weight while preserving conductivity. BHP projects copper demand to climb 70% to 50 million t by 2050, intensifying sourcing risks. Automated harness assembly, proven in automotive lines by CelLink, offers rail vendors a path to cost control when paired with lighter conductors. Theft deterrence pushes rail operators toward CCA because the resale value is lower than pure copper. Immediate use cases focus on signal wiring, where high-frequency performance is stringently tested before fleet-wide roll-outs in the Railway Wiring Harness Market.

Demand for driverless & CBTC-equipped metros

Siemens Mobility will automate Copenhagen’s 170 km S-bane to Grade of Automation 4 by 2033, enhancing peak capacity.[3]“Copenhagen S-bane GoA4 Contract Press Release,” Siemens Mobility, siemens.com Hitachi Rail used 5G CBTC to modernise New York’s Crosstown Line, shrinking lifecycle cost while boosting data throughput.[4]“5G CBTC Deployment on New York Crosstown Line,” Hitachi Rail, hitachirail.com Beijing Metro Line 12 integrates Frauscher Advanced Counter as a SIL 4-certified fallback, an industry first in China. SNS Telecom forecasts USD 1.2 billion cumulative spend on FRMCS-ready 5G rail networks from 2024 to 2027. India’s Kavach system plans 36,000 km coverage by 2030, with 10,000 km under tender, unlocking sizeable harness demand suited for high-bandwidth and redundant safety circuits in the Railway Wiring Harness Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper Price Volatility | -1.1% | Global, most acute in cost-sensitive markets | Short term (≤ 2 years) |

| Lengthy Homologation Cycles | -0.8% | Europe and North America, with regulatory spillover | Medium term (2-4 years) |

| Skilled-Labour Shortages | -0.6% | Developed markets, emerging in APAC manufacturing hubs | Long term (≥ 4 years) |

| EMC/EMI Compliance Hurdles | -0.4% | Global, with strictest requirements in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Copper price volatility is squeezing OEM margins

Copper’s 2025 rally strained budgets, pushing builders to defer cable orders and renegotiate contracts every quarter. The construction sector alone absorbs 20% of US copper, creating spill-over inflation for rail procurement. BHP warns that mine depletion could outpace new supply despite strong price signals. Smaller harness shops lack hedging tools, so the margin compression can reach double digits. High prices encourage theft, forcing operators to deploy additional surveillance and substitute lower-value conductors. These pressures throttle short-run project starts, dampening near-term shipment volumes.

Lengthy homologation cycles for new materials

European NoBos must validate every novel compound under Decision 2010/713/EU, and EN 45545-2 fire tests extend over twelve months for full scope approvals. Suppliers investing in HFFR or thermoplastic elastomers shoulder extra carrying costs as they await certification. In the US, AAR technical approval adds a separate queue to stretch timelines further for freight applications. Start-ups find the multi-year delay discouraging, tilting the field toward incumbents with deeper balance sheets. Consequently, market penetration for innovative materials lags technology readiness, moderating the upside for rapid substitution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insulation Type: HFFR Leads Innovation Drive

PVC retained market leadership with a 44.72% share in 2025 due to incumbency and cost advantage. The shift to halogen-free flame-retardant compounds accelerates because EU Taxonomy financing now rewards low-smoke materials and EN 45545-2 mandates strict toxicity thresholds. HFFR therefore posts a 7.58% CAGR, the fastest among insulation categories, as European orders convert en masse. XLPE is growing due to superior dielectric strength suited for high-voltage traction, while thermoplastic elastomer is expanding owing to its flexibility in passenger-door harnesses. The other bracket, mainly silicone and fluoropolymer blends, covers niche uses in extreme temperature zones.

Regulatory catalysts continue to favour HFFR despite a 2-4-year homologation lag. EU REACH Annex XVII formaldehyde limits from August 2026 further constrain PVC volumes, nudging operators to accelerate specification updates. Regulation (EU) 2024/1781 on ecodesign adds recyclability metrics, bolstering halogen-free adoption. Suppliers able to certify new formulas promptly will capture premium margins. Therefore, the railway wiring harness market sees a measured but persistent redirection of insulation demand toward sustainable compounds that satisfy both safety and circular-economy objectives.

By Wire Material: Optical Fiber Gains Traction

Copper continues to dominate with 58.15% share, yet pricing headwinds revive interest in CCA. Optical fiber is estimated to deliver a 7.22% CAGR through 2031 as predictive maintenance, passenger Wi-Fi, and real-time video monitoring intensify data traffic needs. Hybrid conductor solutions in the other segment serve specialty functions such as power-over-fiber links in tunnel environments.

Digitalisation strategies drive fiber demand most in Europe, where national operators deploy 5G trackside networks. Sumitomo Electric’s EUR 90 million purchase of Südkabel expands high-voltage fiber-optic offerings that couple with traction cables. Meanwhile, sustained copper volatility incentivises exploration of aluminium-based alternatives, and automotive precedence validates CCA for signal lines. Over the forecast period, the material mix gradually pivots toward combinations that balance conductivity, bandwidth, weight, and cost.

By Train Type: Driverless Metro Transformation

High-speed rail commands a 36.02% share, underpinned by ongoing megaprojects in Asia-Pacific. Metro and monorail systems with the driverless subsegment expanding fastest at 6.18%, due to Grade of Automation 4 deployments in Copenhagen, Paris, and several Chinese cities. Light rail and tram lines is increasing, whereas locomotives and freight cars contribute amid renewed North American electrification interest.

Harness complexity scales with automation. Driverless stock needs redundant safety circuits, higher data rates, and integrated cybersecurity layers. This translates into greater conductor counts and increased use of shielded, foil-wrapped twisted pairs. Vendors delivering pre-assembled modular harness kits gain installation efficiency. Meanwhile, freight locomotives adopt dual-mode architectures that still require robust 25 kV cabling but in lower volumes than passenger fleets.

By Application: Infotainment Connectivity Surge

Engine and traction systems remain core at 33.12% because every electrified train mandates high-power distribution. HVAC follows as operators pursue energy-efficient climate control, demand for lighting with LED retrofits extending service intervals. The railway wiring harness market growth for infotainment is poised to climb with 7.89% CAGR, as operators bundle real-time journey data, streaming content, and e-commerce portals.

The rising infotainment requirement pushes data, power, and antenna lines into single modular looms, improving installation and maintainability. Concurrently, India’s Kavach roll-out and Europe’s ETCS upgrades stimulate demand in safety circuits, particularly for shielded Ethernet and fiber backbones. Suppliers can integrate multifunction harnesses that consolidate consumption points in crowded car body spaces and unlock cost and weight benefits for car builders.

Geography Analysis

Asia-Pacific controls 44.05% of revenue and exhibits a robust 7.45% CAGR through 2031. China aims for 50,000 km of high-speed track, and India funds USD 30 billion of network upgrades, including the Shinkansen-based Mumbai–Ahmedabad corridor. Vietnam approved the USD 67 billion North-South line, while Thailand cooperates with China on the Trans-Asian Railway, each elevating demand for high-specification harnesses. The Asian Development Bank estimates rail investment needs to be 0.4% of regional GDP by 2035, underpinning a sizeable, long-term opportunity.

In Europe, Germany’s EUR 500 billion rail plan, Lithuania’s electrification, and continent-wide ETCS adoption combine to stimulate replacement and expansion spending. EU Taxonomy and EN 45545-2 regulations propel the uptake of HFFR products, and simultaneous decarbonisation objectives open space for CCA and fiber upgrades. The market nonetheless contends with homologation bottlenecks that can slow the arrival of novel materials.

In North America, the Bipartisan Infrastructure Law channels USD 8.2 billion into high-speed corridors, and SEPTA’s USD 724.3 million car order demonstrates traction for domestically produced equipment. Adopting intermittent electrification and dual-mode locomotives can bridge the gap between diesel fleets and full catenary coverage, gradually enlarging the harness demand. South America and Middle East and Africa are smaller today, yet projects in Brazil and Saudi Arabia suggest incremental volume as economic diversification and urbanisation advance.

Competitive Landscape

Market fragmentation persists, though consolidation accelerates as leaders seek scale and technology breadth. Hitachi Rail’s EUR 1.66 billion purchase of Thales Ground Transportation Systems forms a EUR 7.3 billion entity that targets JPY 1 trillion revenue and deepens signaling capability. Siemens Mobility, Alstom, and Wabtec concentrate on turnkey automation, driving demand for system-level harness integration.

Material innovators like Leoni launch liquid-cooled, recyclable CCA cables under the 100% circular LIMEVERSE range, claiming 75% weight reduction. Nexans reports a 14.1% organic uplift in electrification businesses, which is underpinned by rail and mining contract wins. Samvardhana Motherson operates 107 harness plants and aligns vertically to stabilise quality and cost. Emerging challengers like CelLink prove to be fully automated, with modular harness production that compresses lead time and supports high-mix programs.

Competition now pivots to lifecycle value rather than pure component sales. Vendors bundle digital twin software, analytics, and cybersecurity into wiring propositions. The shift parallels the automotive industry’s pivot to software-defined vehicles, prompting TE Connectivity and Yazaki to reorganise around cross-domain platforms. Success rests on mastering weight reduction, automation, and regulatory compliance simultaneously.

Railway Wiring Harness Industry Leaders

TE Connectivity

Prysmian Group

Samvardhana Motherson

Leoni AG

Furukawa Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Siemens Mobility and Leonhard Weiss won a EUR 2.8 billion Deutsche Bahn contract for modern control and safety technology within a wider EUR 6.3 billion framework commitment.

- December 2024: Hitachi Rail, FirstGroup, and Angel Trains agreed to lease 14 new five-car Class 80X units valued at GBP 500 million over 10 years, extending open-access service to the London–Carmarthen route.

- May 2024: Hitachi Rail completed its EUR 1.66 billion acquisition of Thales Ground Transportation Systems, expanding operations to 51 countries.

- April 2024: Siemens Mobility secured a EUR 270 million contract to upgrade Copenhagen’s 170 km S-bane to GoA 4, enabling unattended operation by 2033.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the railway wiring harness market as the value of newly produced, insulated cable assemblies that distribute power, control signals, and data within rolling-stock subsystems, including propulsion, HVAC, braking, lighting, safety, and passenger information, across metros, light rail, high-speed, freight, and locomotive platforms.

We explicitly exclude harnesses sold solely for wayside signaling or track electrification infrastructure from the analysis.

Segmentation Overview

- By Insulation Type

- PVC

- XLPE

- Thermoplastic Elastomer (TPE)

- Halogen-Free Low-Smoke (HFFR)

- Others

- By Wire Material

- Copper

- Copper-Clad Aluminium

- Optical Fibre

- Others

- By Train Type

- High-Speed Rail

- Light Rail / Tram

- Metro / Monorail

- Locomotive & Freight Cars

- By Application

- HVAC

- Engine & Traction

- Lighting

- Braking System

- Infotainment & Connectivity

- Safety & Signalling

- Others

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Turkey

- South Africa

- Egypt

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed harness fabricators, rolling-stock OEM engineers, depot managers, and transit-authority buyers across Asia Pacific, Europe, and North America. Insights on meters of cable per car, the shift toward halogen-free insulation, and regional procurement cycles closed key data gaps and guided assumption ranges, giving Mordor analysts confidence in every variable used.

Desk Research

We began by mapping global rolling-stock deliveries through open procurement portals, UN Comtrade shipment codes, and fleet statistics issued by the International Union of Railways and Eurostat. Next, we gathered electrical standards, insulation specifications, and average harness weights from trade associations such as the Railway Industry Association and standards bodies that release EN 50155 or AAR guidelines. Company filings, investor presentations, and quarterly shipment commentaries supplied pricing and material-mix trends, while paid feeds from D&B Hoovers and Dow Jones Factiva helped us benchmark leading suppliers' revenue splits. These streams allowed us to size the historical demand pool and detect price inflections linked to copper volatility. The list above is illustrative, and many other public and paid sources were reviewed for context, validation, and clarification.

Market-Sizing & Forecasting

We apply a top-down rolling-stock delivery volume model multiplied by average harness weight and blended ASP to derive yearly spending. Results are then cross-checked with sampled supplier revenue roll-ups, channel checks, and refurbishment demand to refine totals. Key variables include new car deliveries, refurbishment rates, copper and CCA price curves, insulation-mix migration, and metro electrification kilometers. Multivariate regression, layered with scenario analysis vetted by primary respondents, underpins the 2025-2030 forecast. Where supplier splits were missing, import values and historical price-volume elasticities bridged the gaps.

Data Validation & Update Cycle

Our outputs pass a two-step peer review, variance checks against independent fleet and commodity indices, and anomaly flags trigger re-contact with sources. Mordor refreshes the dataset annually and issues interim revisions when material policy or price shocks occur, ensuring clients always receive the latest view.

Why Mordor's Railway Wiring Harness Baseline Commands Reliability

We acknowledge that published estimates often diverge because firms apply different rolling-stock scopes, material baskets, ASP assumptions, and currency conversions.

Key Gap Drivers include varying inclusion of aftermarket retrofits, list-price versus realized ASP use, and shorter refresh cadences that overlook the recent softening in copper.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.85 B (2025) | Mordor Intelligence | Aligned scope |

| USD 3.92 B (2024) | Global Consultancy A | Includes trackside cabling and optimistic ASP escalation |

| USD 1.72 B (2024) | Industry Research B | Excludes metro refurbishments and conservative delivery outlook |

The comparison shows that our disciplined scope selection, variable tracking, and annual refresh give decision-makers a balanced, transparent baseline that is traceable to clear assumptions and readily repeatable.

Key Questions Answered in the Report

What is the current size of the railway wiring harness market?

The market reached USD 3 billion in 2026 and is forecast to grow to USD 3.87 billion by 2031.

Which region leads the railway wiring harness market?

Asia-Pacific holds the lead with 44.05% revenue share in 2025 and is expanding fastest at 7.45% CAGR.

Why are halogen-free cables gaining traction in rail applications?

EU Taxonomy financing and EN 45545-2 fire-safety rules incentivise operators to replace PVC with low-smoke, halogen-free materials.

How will copper-clad aluminium affect railway wiring harness supply chains?

CCA mitigates copper price volatility and reduces harness weight by up to 75%, lowering material costs and theft risk.

What drives demand for optical fiber in rail wiring?

Predictive maintenance, 5 G-enabled CBTC, and passenger connectivity require high-bandwidth links that optical fiber best delivers.

How is automation influencing harness design?

Driverless metro systems need redundant safety circuits and high data capacity, prompting the need for modular, shielded harness solutions optimized for fast installation.

Page last updated on: