Influencer Marketing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 40.51 Billion |

| Market Size (2031) | USD 152.56 Billion |

| Growth Rate (2026 - 2031) | 30.36% CAGR |

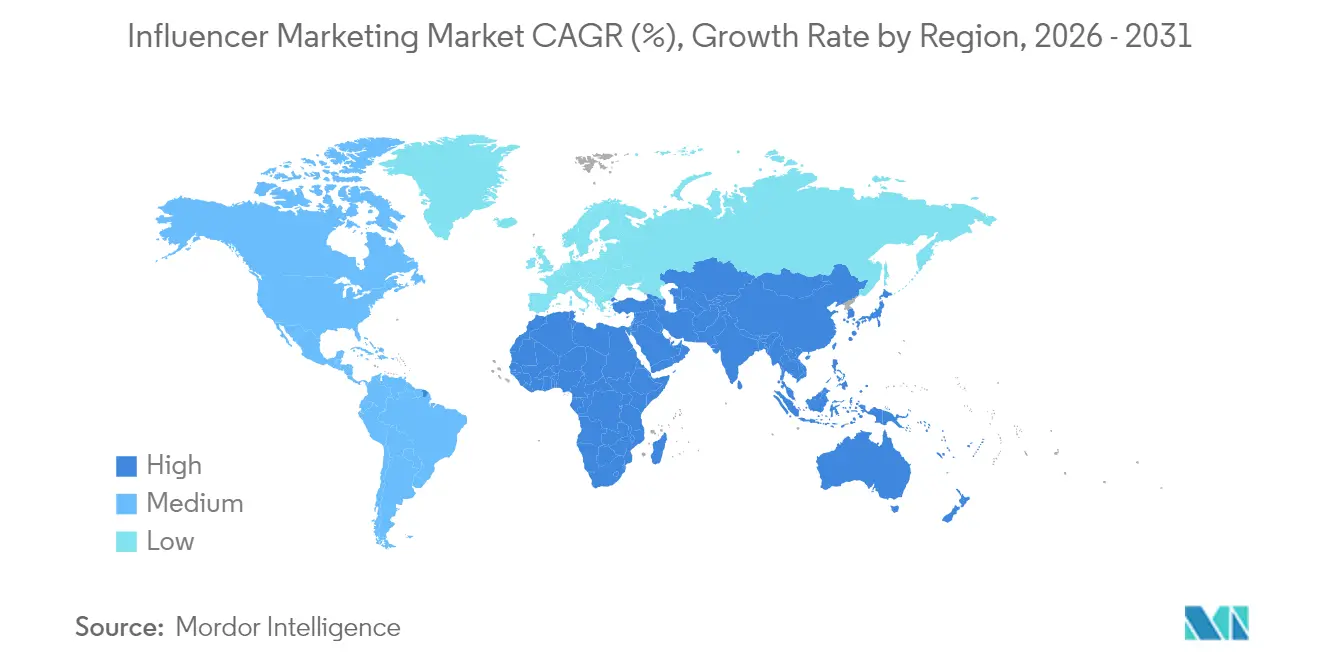

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

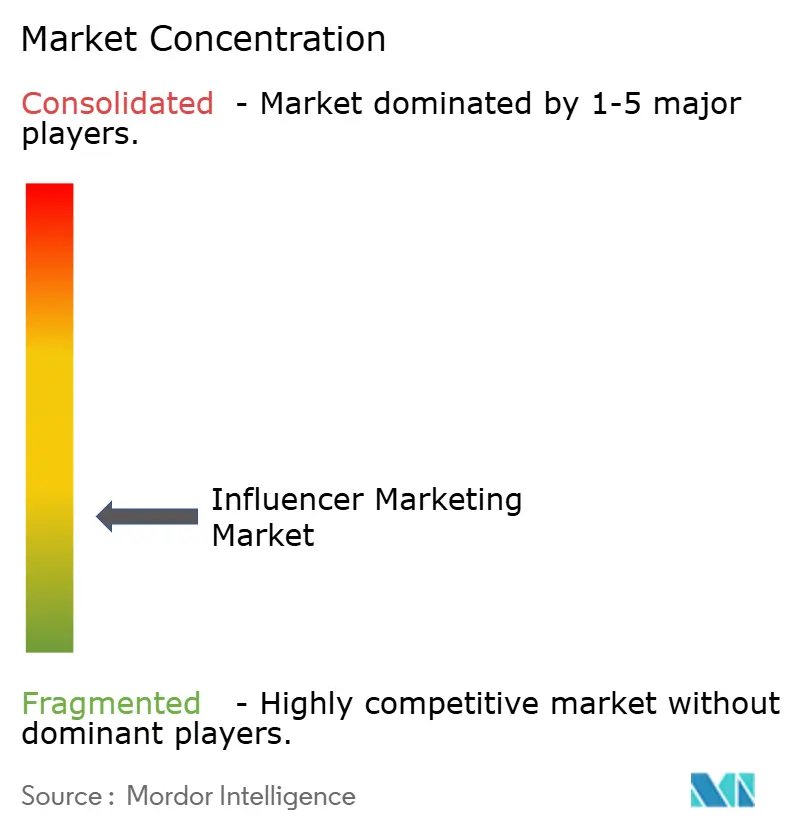

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Influencer Marketing Market Analysis by Mordor Intelligence

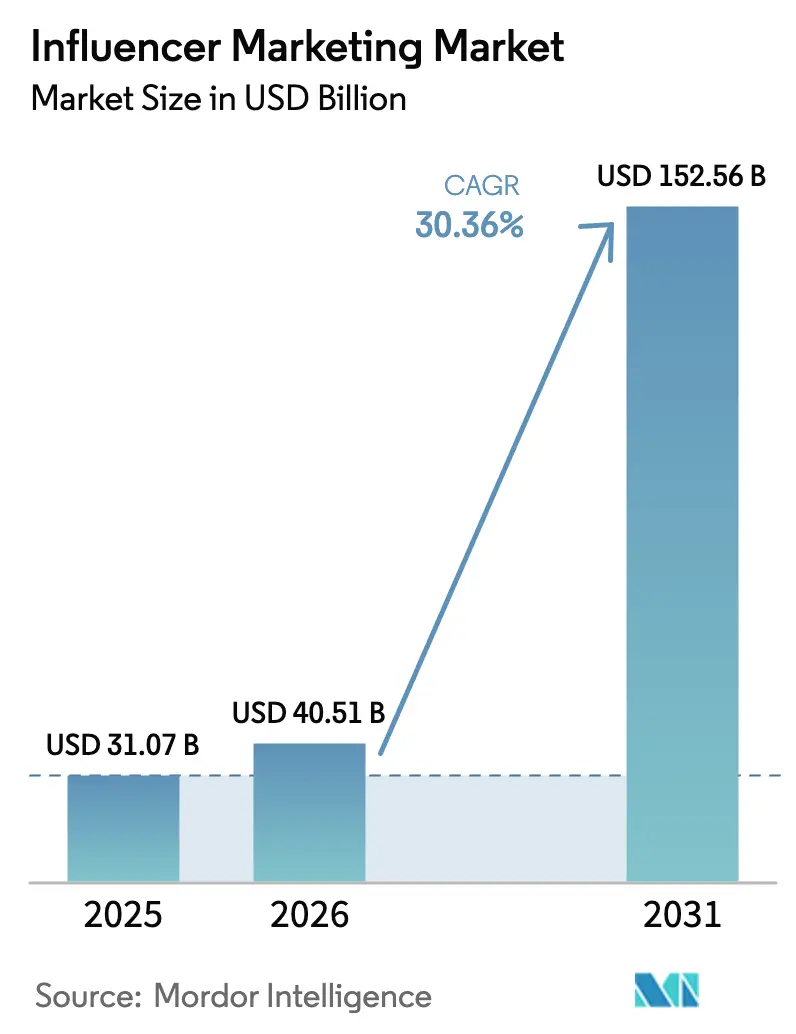

The influencer marketing market size in 2026 is estimated at USD 40.51 billion, growing from 2025 value of USD 31.07 billion with 2031 projections showing USD 152.56 billion, growing at 30.36% CAGR over 2026-2031. Brand owners now treat creator partnerships as a strategic acquisition lever rather than an experimental spend. Finance teams approve multi-year allocations because blended customer-acquisition costs fall when even a modest portion of budgets shifts from paid search to creators. In North America, which commands a 35% slice of the influencer marketing market, robust attribution stacks and clear disclosure rules let marketers prove ROI with confidence [1]Federal Trade Commission, “Disclosure 101 for Social Media Influencers,” ftc.gov. Asia-Pacific supplies the steepest incremental lift as social-commerce super-apps compress discovery, engagement, and checkout into one scroll, making the channel a measurable revenue driver.

Key Report Takeaways

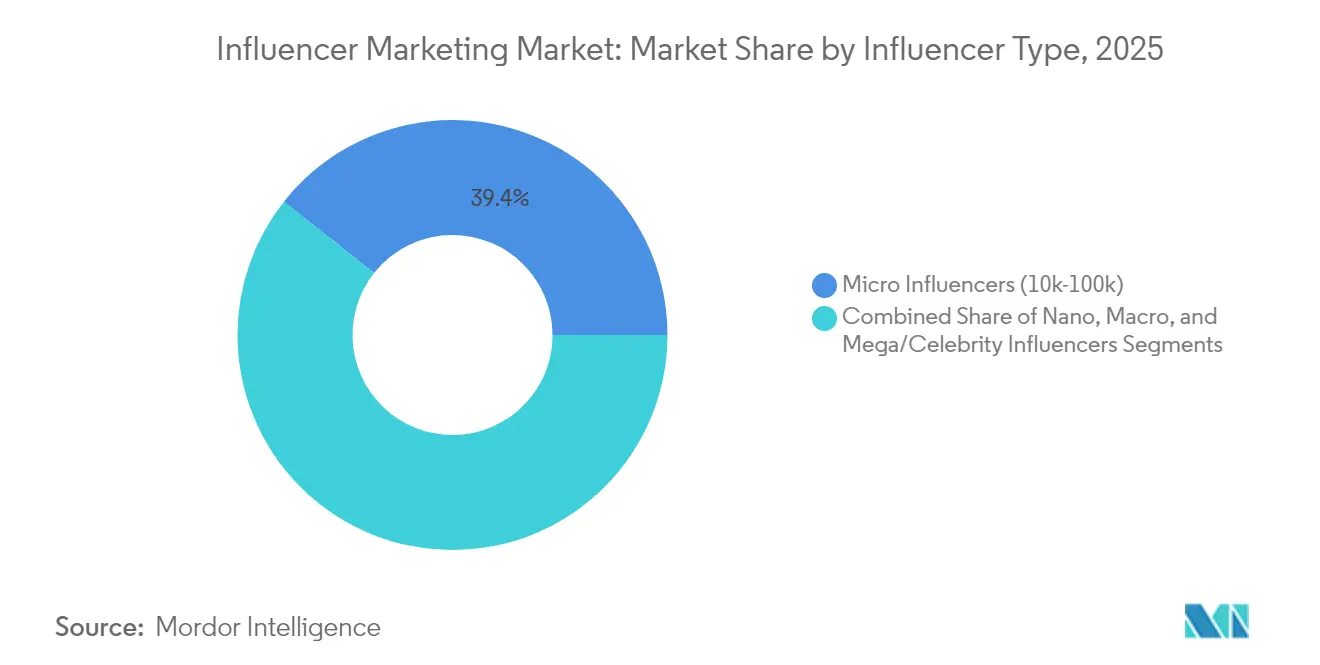

- By influencer type, micro creators held 39.35% of the influencer marketing market share in 2025, while nano creators are forecast to expand at a 34.92% CAGR through 2031.

- By social media channel, Instagram led with a 29.25% revenue share in 2025; TikTok is projected to grow at a 36.85% CAGR to 2031.

- By application, campaign-management suites accounted for a 34.20% share of the influencer marketing market size in 2025, and compliance tools are advancing at a 33.74% CAGR through 2031.

- By end user, retail and e-commerce commanded 27.45% of the influencer marketing market size in 2025, whereas gaming and entertainment are forecast to grow at a 32.66% CAGR to 2031.

- By geography, North America contributed the largest 34.55% share, while Asia-Pacific is set to record the highest 33.90% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Influencer Marketing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Dominance of Short-Form Video Platforms | +4.5% | North America and Asia | Short term (≤2 yrs) |

| Adoption of AI-Driven Creator Matching and Dynamic Pricing Engines | +3.8% | Global, led by US and EU | Medium term (3-4 yrs) |

| Integration of Social Commerce APIs | +3.2% | SEA and MENA, with global spillover | Medium term (3-4 yrs) |

| Rise of Nano/Micro Influencer Networks | +2.9% | India, Brazil, Africa | Short term (≤2 yrs) |

| Regulatory Push for Transparent #Ad and Brand Safety Tools | +2.4% | EU and US, expanding globally | Long term (≥5 yrs) |

| Shift Toward Outcome-based Pay-per-Campaign Pricing | +2.1% | Global, DTC brands leading adoption | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

Growing Dominance of Short-Form Video Platforms in Brand Budgets

Short-form vertical clips now attract the largest portion of incremental creator spend, with TikTok and Instagram Reels absorbing most 2024 budget expansions. A 5.7% average engagement rate and a 2.9% conversion rate have convinced advertisers to lean on video for both awareness and sales lifts. Beauty brands redirected nearly two-fifths of their digital budgets to short-form assets after “get-ready-with-me” content triggered launch sell-outs. Because algorithms reward content quality over follower scale, mid-tier and nano creators achieve broader reach, improving inventory liquidity and driving effective CPMs downward.

Adoption of AI-Driven Creator Matching And Dynamic Pricing Engines

Machine-learning models now score audience overlap, sentiment, and conversion history, reducing partner discovery cycles by 64% and improving return on ad spend by 28%. Dynamic pricing converts fixed fees into performance-based payouts that fluctuate with engagement. Consumer-electronics launches employing the model saw faster sell-through of limited editions, validating AI-assisted decisioning for P and L-oriented marketers.

Integration of Social-Commerce APIs Driving Attribution-Linked Spend

Creator posts that jump straight to checkout generate 3.2 times the attributable sales of campaigns that end with “learn-more” calls to action. Southeast Asian live-stream hosts pin localized affiliate links, turning broadcasts into single-screen journeys from discovery to purchase. Western retailers followed suit; by late 2024, three-quarters of large merchants had tethered inventory feeds to creator platforms, letting finance teams approve revenue-linked compensation models that expand budgets in 2025.

Rise of Nano/Micro Influencer Networks for Hyper-local Campaigns

Micro creators already command 40% of the influencer marketing market, but nano cohorts will post the highest 36% growth through 2030. A food-delivery app in India seeded 500 nano voices and lifted orders by 48% within two weeks despite modest view counts. Aggregator platforms orchestrate hundreds of small creators efficiently, enabling geo-targeted activations that preserve authenticity while operating at programmatic scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Creator Fraud and Bot Engagement | -2.7% | Emerging markets, particularly SEA and LATAM | Medium term (3-4 yrs) |

| Third-Party Cookie Deprecation | -1.9% | Global, most acute in EU | Short term (≤2 yrs) |

| Fragmented Data Standards | -1.6% | Global, cross-platform campaigns | Long term (≥5 yrs) |

| Intense Price Competition from Point-Solution Start-ups | -1.3% | Global, enterprise segment focus | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

Creator Fraud and Bot Engagement Eroding ROI in Emerging Markets

Fake-follower rates rose to 18% in parts of Southeast Asia and Latin America in 2024 [2]Federal Trade Commission, “Disclosure 101 for Social Media Influencers,” ftc.gov. Apparel campaigns uncovered inflated comment volumes with negligible conversions, leading to mid-flight audits and budget clawbacks. Verification costs climbed 42% as platforms inserted biometric and behavioral checks, yet fraud operators also evolved, making authenticity an ongoing arms race. Contracts now withhold up to 30% of payouts until third-party audits certify engagement quality.

Third-Party Cookie Deprecation Delaying Cross-Channel Attribution

Browser moves to retire cookies eroded multi-touch models by 37% in tests [3]World Wide Web Consortium, “Attribution in a Post-Cookie Era,” w3.org. Brands reverted to channel-specific metrics, muffling coordinated storytelling. Server-side tagging and clean-room data exchanges offer partial fixes, yet platform operators admit parity will not arrive before late 2025. During the gap, budgets flow toward social-commerce integrations that deliver native conversion insight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Influencer Type: Nano Creators Redefine ROI Metrics

Micro influencers accounted for 39.35% of the influencer marketing market size, equal to USD 12.23 billion in 2025. Engagement superiority over mega personalities persuades consumer brands to assign launch duties to micro pools. Nano creators produce smaller reach but sustain click-through rates above 4%, encouraging performance teams to reallocate testing budgets from paid search. Agencies adopt CRM-style tooling to manage hundreds of nano relationships without raising labor overhead.

Mega influencers remain brand-equity levers for tent-pole events, yet their relative share slipped 3.2 points last year. Macro influencers fill the consideration stage, especially for complex B2B solutions. A software company enlisted 20 macro reviewers to explain a new SaaS release and lifted lead-form completions by 32%. Tier selection thus aligns with funnel position, supporting diversified creator portfolios within the influencer marketing market.

By Social Media Channel: TikTok Disrupts Platform Hierarchy

Instagram held a 29.25% platform share, translating into USD 9.09 billion, but TikTok challenges the incumbent with a 36.85% CAGR outlook. TikTok’s discovery feed allows small voices to achieve viral reach, exemplified by a gardening tip that collected 2 million views from a 15,000-follower account. Advertisers elevated TikTok from pilot to core once SKU-level sell-outs could be traced to live-link carts.

YouTube protects its long-form niche; a home-appliance brand used 20-minute creator demos to cut returns by 18%, saving service costs. Facebook maintains relevance among over-40 audiences who trust closed-group testimonials. LinkedIn is gaining ground in financial services, where thought-leader creators drive webinar sign-ups. The platform mosaic forces marketers to build modular creative so that stories remain coherent across multiple feeds in the influencer marketing market.

By Application: Compliance Tools Gain Strategic Priority

Campaign-management suites captured a 34.20% slice, or USD 10.63 billion, in 2025. Feature roadmaps now include usage-rights ledgers, brand-safety filters, and cohort analytics that compare nano pools with macro bets in a single dashboard. Marketers reallocate budgets mid-flight using these insights to maximize return.

Compliance and fraud-detection software, the fastest-growing niche at 33.74% CAGR, surged after regulators imposed penalties for missing disclosures. A beverage brand that deployed real-time alerts cut review cycles by 55% and avoided takedowns during a launch blitz. Product-seeding systems link warehouse APIs to ship samples automatically once creators clear screening, shortening unboxing timelines. Analytics vendors move from vanity metrics to revenue attribution, reinforcing budget justification within the influencer marketing market.

By End User: Gaming Sector Accelerates Platform Innovation

Retail and e-commerce accounted for 27.45% of the influencer marketing market size, equal to USD 8.53 billion in 2025. Shoppable links convert inspiration to cart value in seconds. A footwear retailer shifted 45% of creator fees to revenue-share contracts and saw ROAS rise 22% against flat-fee deals.

Gaming and entertainment deliver the fastest 32.66% CAGR. A 2025 tournament let selected creators co-stream, lifting cosmetic-skin sales by 40% versus prior events. Fitness-equipment makers turn certified trainers into tutorial hosts, reducing customer queries by 17%. Financial institutions under strict ad codes test LinkedIn Q and As and register 27% more qualified leads, illustrating sector-specific traction in the influencer marketing market.

Geography Analysis

North America generated USD 10.74 billion of 2025 spend and integrates creator metrics directly into business-intelligence systems. Federal Trade Commission rules require conspicuous sponsorship labels, prompting platforms to automate disclosures, which reduces post-campaign legal risk. Seventy-seven percent of enterprises embed creators into omnichannel plans, moving the influencer marketing market from test budgets to core line items. Early deployment of server-side tagging counters cookie loss and keeps cross-device attribution viable.

Asia-Pacific exhibits a 33.90% CAGR outlook. Super-apps blend chat, payment, and video, fostering live-commerce sessions that compress awareness and conversion into one interaction. Chinese streams often attract six-figure audiences, propelling immediate inventory sell-outs. South Korean beauty houses now debut new items through creator collaborations before store placement, speeding revenue realization. India’s multilingual terrain favors nano networks: a telco in Tamil markets outperformed Hindi campaigns after engaging 300 local voices. Hyper-local execution, therefore, magnifies impact within the influencer marketing market.

Europe moves under a strict governance framework shaped by the Digital Services Act . Platforms introduced consent logs and age-appropriate defaults, raising engineering overhead yet supplying brands with clear compliance roadmaps. Sweden shows early adoption of AI-supported compliance plug-ins, while Southern states offer runway as broadband spreads. The United Kingdom maintains parallel standards and channels luxury-goods spend into creator collaborations that routinely over-subscribe launches. European technical rigor prompts vendors to export compliance know-how, influencing global product design in the influencer marketing market.

Competitive Landscape

The market remains moderately fragmented as specialist SaaS vendors, social platforms, and enterprise clouds vie for share. Seventeen acquisitions closed in 2024, signaling a rush toward end-to-end workflow control. Proprietary AI that predicts performance, optimizes schedules, and flags fraud serves as the new differentiator. Vendors without such intellectual property risk commoditization because basic talent databases no longer suffice.

White-space opportunities revolve around metric harmonization. Brands still reconcile disparate definitions of reach and engagement, consuming analyst hours. Start-ups that build real-time identity-resolution graphs are winning pilot projects from multinational advertisers that want to collapse reporting lag. Patent filings around creator-audience mapping underscore the strategic value of data structures in the influencer marketing market.

Native marketplaces inside social networks provide turnkey buying paths but spark channel conflict with independent platforms. Enterprise clouds counter by embedding light influencer functions, betting that procurement teams prefer single contracts. The sector is likely to bifurcate into mega suites that serve generalist needs and specialist vendors that target regulated niches. Scale, capital, and AI deployment speed will determine which cohort secures a disproportionate portion of future growth in the influencer marketing market.

Influencer Marketing Industry Leaders

Upfluence

Aspire

Mavrck

Neoreach

Traackr, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CreatorIQ acquired HypeAuditor for USD 78 million, adding fraud-detection algorithms scanning audience authenticity across 40 languages, a move that enhances global compliance credentials.

- March 2025: TikTok extended its Creator Marketplace API to all commerce platforms exceeding one million monthly buyers, enabling merchants to embed shoppable videos without custom code; early testers reported a double-digit lift in checkout conversions.

- February 2025: IZEA Worldwide raised USD 42 million in Series D financing to expand its AI-matching engine and open regional data centers in Frankfurt and Singapore for data-sovereignty compliance

- June 2024: Qoruz, an influencer marketing platform based in India, has partnered with Dabur, a brand celebrated for its natural and Ayurvedic products. This collaboration enhances Dabur's influencer marketing strategy, fostering more authentic and impactful connections with its audience. Leveraging Qoruz's sophisticated analytics and influencer management tools, Dabur aims to pinpoint influencers that resonate with the brand's fundamental values. Through Qoruz’s platform, Dabur gains data-driven insights into influencer performance and audience engagement, enabling them to craft campaigns that effectively resonate with their target demographic.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the influencer marketing market as every dollar that brands, agencies, and e-commerce sellers direct to social media creators, through software platforms or managed service networks, to distribute sponsored content and drive measurable business outcomes. According to Mordor Intelligence, this definition captures both software fees and creator compensation tied to campaigns, giving buyers a full-funnel spending view.

Scope exclusion: Pure affiliate-only tools, employee advocacy suites, and B2B word-of-mouth referral programs sit outside this market because their economics and user bases differ from creator-led advertising.

Segmentation Overview

- By Influencer Type

- Nano Influencers (1k-10k)

- Micro Influencers (10k-100k)

- Macro Influencers (100k-1M)

- Mega/Celebrity Influencers (>1M)

- By Social Media Channel

- TikTok

- YouTube

- Others (Snap, Pinterest, Twitch)

- By Application

- Campaign Management

- Search and Discovery

- Analytics and Reporting

- Product Seeding

- Compliance and Fraud Detection

- Others

- By End User

- Retail and E-commerce

- Fashion and Lifestyle

- Travel and Hospitality

- Food and Beverage

- Gaming and Entertainment

- Health and Fitness

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct structured interviews with creator economy software executives, multi-channel network managers, brand media leads, and independent nano to mega influencers across North America, Europe, Asia, and Latin America. These conversations refine average deal sizes, campaign frequency, emerging KPIs, and regional compliance costs that secondary data cannot reveal at scale.

Desk Research

We begin by mapping the spend universe with open datasets such as the U.S. Federal Trade Commission ad disclosure archives, Interactive Advertising Bureau ad spend trackers, WARC's global digital advertising dashboards, UN DESA social media penetration files, and influencer campaign counts published by Influencer Marketing Hub. Company filings, IPO prospectuses, and large platform transparency reports then anchor price and volume benchmarks.

Dow Jones Factiva and D&B Hoovers help our analysts spot revenue inflections at listed platform vendors, while periodic pulls from Statista, OECD broadband statistics, and regional trade associations validate adoption curves by geography. The sources above are illustrative only; many additional databases and public records inform the desk phase.

Market Sizing and Forecasting

Top down modeling starts with global digital ad outlays, allocates the share routed to influencer campaigns by region, and breaks this spend across creator tiers using engagement weighted penetration rates. Select bottom up checks, platform fee roll ups, sampled CPM × impression volumes, and average sponsored posts per active creator tension the totals before finalization. Key variables include social media active user counts, short form video watch hours, average campaign CPM, creator take rate trends, disclosure compliance ratios, and AI driven fee compression. A multivariate regression with ARIMA overlay projects each driver to 2030, and scenario analysis adjusts for regulatory or platform algorithm shocks. Data voids in emerging regions are bridged with trade adjusted proxy metrics validated through local expert calls.

Data Validation and Update Cycle

Outputs pass a three layer review: automated anomaly flags, peer analyst cross checks, and senior sign off. Variances versus historical ratios above 5% trigger re contact of industry sources. We refresh the entire model annually, while material events, such as platform policy shifts and landmark regulations, prompt interim updates so clients receive the latest calibrated view.

Why Mordor's Influencer Marketing Baseline Commands Reliability

Published figures differ because firms frame the opportunity in unique ways. Some count only platform subscription fees, others annualize creator earnings, and a few extrapolate ad spend shares from single country samples.

Our disciplined scope, yearly refresh, and dual lens validation temper both optimism and undue caution.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 31.07 B (2025) | Mordor Intelligence | - |

| USD 25.44 B (2024) | Global Consultancy A | Tracks software revenue only, excludes creator payouts, uses 2018 weighted CAGR |

| USD 20.24 B (2024) | Data Provider B | Applies conservative adoption ratios, omits nano influencer segment, updates biennially |

The comparison shows that wider scope selection, fresher inputs, and continuous validation allow Mordor Intelligence to deliver a balanced, transparent baseline that decision makers can trace back to clear variables and reproducible steps.

Key Questions Answered in the Report

How big is the Influencer Marketing Market?

The Influencer Marketing Market size is expected to reach USD 40.51 billion in 2026 and grow at a CAGR of 30.36% to reach USD 152.56billion by 2031.

What is the current Influencer Marketing Market size?

In 2026, the Influencer Marketing Market size is expected to reach USD 40.51 billion.

Who are the key players in Influencer Marketing Market?

Upfluence, Aspire, Mavrck, Neoreach and Traackr, Inc. are the major companies operating in the Influencer Marketing Market.

Which is the fastest growing region in Influencer Marketing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Influencer Marketing Market?

In 2025, the North America accounts for the largest market share in Influencer Marketing Market.

What years does this Influencer Marketing Market cover, and what was the market size in 2025?

In 2025, the Influencer Marketing Market size was estimated at USD 40.51 billion. The report covers the Influencer Marketing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Influencer Marketing Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: